Uncategorized

Futures Fall As Tech-Led Rally Fizzles, Yields And Oil Rebound

Futures Fall As Tech-Led Rally Fizzles, Yields And Oil Rebound

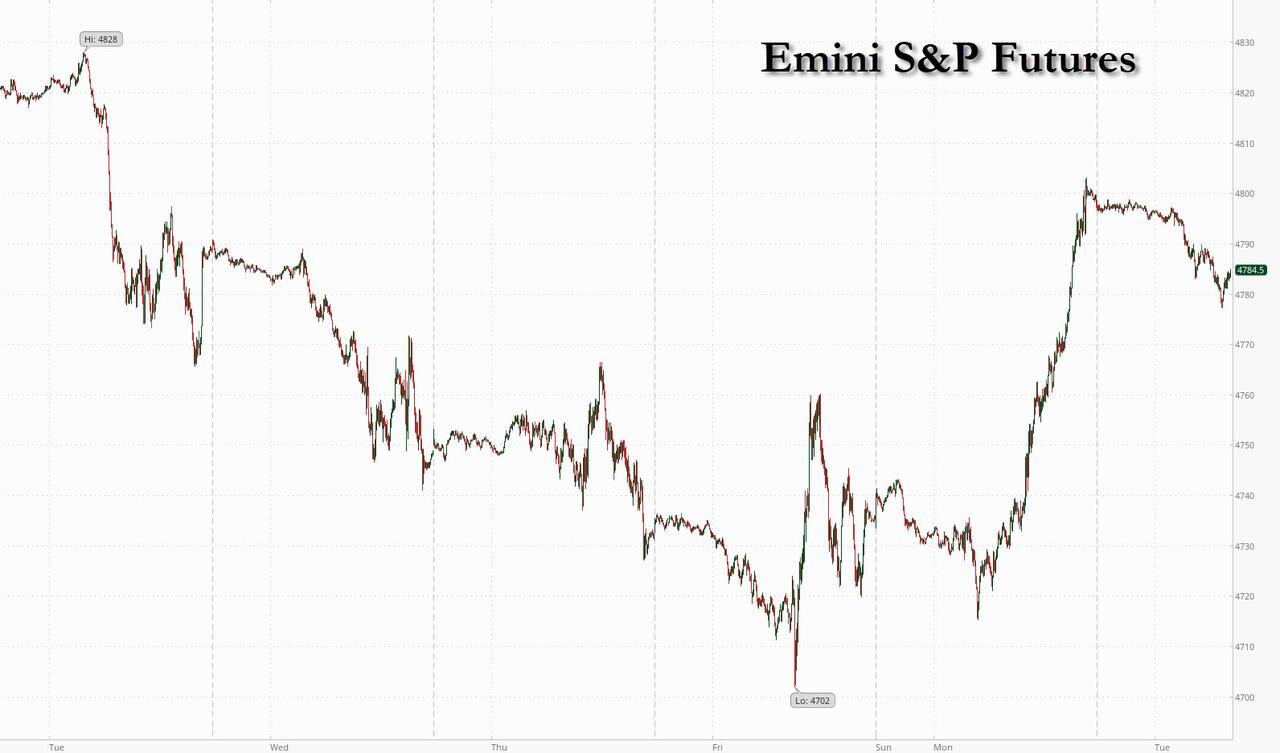

US stock futures dropped amid a risk-off tone as Monday’s tech-fueled bounce…

Share this:

US stock futures dropped amid a risk-off tone as Monday's tech-fueled bounce fizzled and investors turned their attention to this week's inflation print as well as the start of corporate earnings season. As of 7:40am ET, S&P futures were down 0.3%, and Nasdaq futures dropped 0.5% following European bourses lower. The tech rally in US stocks on Monday came as Nvidia surged after announcing new AI products for personal computers. The Nasdaq 100 jumped the most since November on Monday and the S&P 500 traded near a record high while Japan’s Nikkei 225 index closed up 1.2% — a level unseen since March 1990. Bonds are lower pushing the 10Y yield as high as 4.05% as oil bounced back from the largest drop in about a month on signs of a weaker physical market, including a deep pricing cut by OPEC+ leader Saudi Arabia; Brent traded near session highs around $78. The USD was flat while the yen reversed earlier gains. Bitcoin dipped after surging past $47,000 on bets that the US is set to approve the first spot ETF.

In premarket trading, Juniper Networks jumped 23% after the Wall Street Journal reported the company was in advanced talks to be sold to Hewlett Packard Enterprise. Tinder-parent Match Group gained 14% after the Wall Street Journal reported that Elliott Investment Management had built a stake of about $1 billion in the dating-app company. Here are some other notable premarket movers:

- CrowdStrike rises 2% after being upgraded at Morgan Stanley, which sees a better demand outlook for the software firm’s services.

- Eversource Energy slips 3% after saying it’s in advanced talks to unload its share in three offshore wind projects that it planned to build with Orsted A/S.

- GoDaddy advances 1.5% after Piper upgrades the web-platform firm, saying a re-acceleration in growth with 30%+ normalized Ebitda margin in 2024 could reverse a five-year trend of multiple compression.

- MaxCyte climbs 5% after posting preliminary 4Q revenue that’s higher than the year-ago period.

- Microchip Technology slips 3% after the chipmaker said its preliminary 3Q revenue is down sequentially about 22%, compared to its previous guidance of 15% to 20%.

- Netflix drops 2% as Citi cuts its rating on the streaming-video company to neutral, citing “lofty” expectations.

- PayPal dips 2% after the payments firm was cut to equal-weight by Morgan Stanley, which highlighted “slower-than-expected progress.”

The 10-year Treasury yield held above 4%, a level Bill Gross called “overvalued” even after it surged 17 basis points last week as robust labor-market data spurred traders to pare bets on rapid Fed easing. Long-dated Gilts were among the biggest decliners in Europe after the government sold 2.25 billion pounds ($2.9 billion) of 20-year debt. And speaking of bonds, BlackRock issued a warning about the dangers of debt-fueled government spending in an election year as government bonds slumped under supply from countries including the UK, Italy and Belgium. This echoed what we published last night in "Citadel Trader: "Fed Wants To Avoid Pain AT ALL COSTS Ahead Of Elections; This Will Lead To Epic Fiscal Irresponsibility."

"The new year is already putting the 2023 Santa rally to the test," said Evelyne Gomez-Liechti, a strategist at Mizuho International, citing pressures including unexpected US labor strength, an overextended rally and heavy supply of new government and corporate debt.

In other news, Investigators probing the fuselage blowout on a Boeing 737 Max 9 plane on Jan. 5 determined that the door plug moved upward before ejecting. In other news, a Chinese agency claims it has devised a way to identify users who send messages via Apple’s AirDrop feature as part of China’s broader efforts to root out undesirable content.

With CPI due Thursday, earning kicking off later this week and JPM's influential Healthcare conference, this is the calm ahead of the proverbial storm. The major macro data points are CPI and PPI on Thurs and Fri, and prints may be market-moving as the bond market tries to determine the timing of the first rate cut among March, May, and June. Goldman claims the first cut will be in March while JPM maintains a call for cuts kicking off in June.

European stocks and US futures are on the back foot as oil prices bounce back from Monday’s steep fall. The Stoxx 600 is down 0.2% with miners and tech stocks among the worst-performing stocks, while energy and health care advance. Shares and bonds of Spanish blood plasma firm Grifols SA tumbled after short seller Gotham City Research LLC published a report criticizing the company’s financial reporting.

- Nexans rises as much as 6.1% after Berenberg starts coverage of the French cable manufacturer with a buy rating, saying the stock sits at an interesting entry point and the long-term outlook remains positive.

- DWS rises as much as 2.8% after Goldman Sachs upgraded the German asset management firm to buy, citing continued momentum and undervaluation.

- Pirelli gains as much as 3.5%, rising to the highest level in almost two years, after Italian investors in the Italian tiremaker agreed to boost their holding to more than 20%.

- Grifols plummets as much as 43%, a record drop since listing in 2006, after short seller Gotham City Research published a negative report on the blood plasma firm.

- Infineon and STMicro lead a drop in European chipmakers on Tuesday after US peer Microchip said its preliminary revenue for the quarter ending December fell by 22% q/q, worse than its guidance.

- Hays sinks as much as 19%, pulling peers PageGroup and Randstad down with it, after the company’s net fees fell sharply. The firm warns of challenging market conditions going forward.

- U-blox falls as much as 8% after Baader downgraded the Swiss wireless communications technologies provider to add from buy, saying it has lower short-term expectations.

- United Internet falls as much as 2.4% as UBS downgrades the stock, noting that shares are close to fair value after a rapid re-rating.

- Tecan slumps as much as 5.6% after the Swiss lab equipment maker released FY23 sales figures below expectations due to lower Covid-related sales and lower pass-through of material costs.

- Meyer Burger drops as much as 12% after Baader downgraded the Swiss solar-equipment manufacturer to reduce from buy, citing lack of visibility on the resilience bonus in Germany.

- Games Workshop shares drop as much as 3.5% after analysts had mixed reactions to the company’s first-half results, despite reported growth in both revenue and profits.

- SCA falls as much as 2.4% after Handelsbanken cut its short-term recommendation for the Swedish forestry and paper firm to hold from buy ahead of its 4Q report, due on Jan. 26.

Earlier in the session, stock gains across Asia faded after tech shares surrendered opening strength. The Hang Seng Tech index turned negative after wiping out 1.6% rally, and the Kospi erases advance following a Samsung earnings miss. Japanese markets remain in the green following Monday’s holiday. Chinese shares eked out modest gains amid steadily growing expectations for a near-term policy easing.

In FX, the Bloomberg Dollar Spot Index firmed while the Treasury 10-year yield rose as much as two basis points to 4.05%. Bloomberg Economics expects core US CPI Thursday to show disinflation continues to be very slow in supercore categories, while PPI data on Friday to reflect renewed supply-chain bottlenecks. The yen tops G-10 leaderboard with a 0.4% gain while Aussie reverses early uptick. Onshore yuan is marginally softer.

Treasuries slightly lower across the curve with losses led by long-end, steepening 2s10s, 5s30s spreads by 1.5bp and 1bp on the day. US yields cheaper by up to 2bp across long-end of the curve with 10-year sector trading around 4.05%. Bunds and gilts trade cheaper by 4.5bp and 4bp in the sector, as European supply skewed toward longer-end sales weighs. Swap spreads remain near top of Monday’s range, following surge wider on the back of weekend comments from Fed Dallas President Lorie Logan. JGB futures turned positive after BOJ kept long-end bond buying amount unchanged. Core European rates underperform, weighing on Treasuries as market participants brace for the first of this week’s auctions. Meanwhile, Treasury auctions resume at 1pm with $52b 3-year notes, followed by $37b 10- and $21b 30-year sales Wednesday and Thursday. The When Issued 3-year is at ~4.125% is 36.5bp richer than December’s stop-out, which tailed the WI by 1.7bp, and below auction stops since May

In commodities WTI crude oil futures higher by more than 2% on the day, paring a portion of Monday’s 4.1% drop and adding to cheapening pressure on Treasury yields; gold rises ~$5 to $2,033.

Bitcoin dipped after surging past $47,000 on bets that the US is poised to approve the launch of the nation’s first exchange-traded funds investing directly in the world’s largest digital asset.

To the day ahead now, and data releases include German industrial production for November and the Euro Area unemployment rate for November, whilst in the US there’s the NFIB’s small business optimism index for December, and the trade balance for November. From central banks, we’ll hear from Fed Vice Chair for Supervision Barr, and the ECB’s Villeroy.

Market Snapshot

- S&P 500 futures down 0.3% to 4,787.25

- MXAP up 0.2% to 165.53

- MXAPJ little changed at 511.29

- Nikkei up 1.2% to 33,763.18

- Topix up 0.8% to 2,413.09

- Hang Seng Index down 0.2% to 16,190.02

- Shanghai Composite up 0.2% to 2,893.25

- Sensex up 0.1% to 71,459.92

- Australia S&P/ASX 200 up 0.9% to 7,520.52

- Kospi down 0.3% to 2,561.24

- STOXX Europe 600 down 0.1% to 477.48

- German 10Y yield little changed at 2.18%

- Euro little changed at $1.0943

- Brent Futures up 1.6% to $77.36/bbl

- Gold spot up 0.4% to $2,036.05

- U.S. Dollar Index up 0.10% to 102.31

Top Overnight News

- Japan’s Tokyo CPI for December cooled more than anticipated on a headline basis (+2.4% vs. +2.7% in Nov and vs. the Street’s +2.5% forecast) while core was inline (+3.5% ex-food/energy vs. +3.6% in Nov and vs. the Street’s +3.5% forecast). BBG

- Saudi Arabia raised $12 billion in its biggest borrowing abroad since 2017. It’s been a record start to the year for emerging markets as issuers seek to lock in lower funding costs. BBG

- Microsoft’s $13 billion investment into OpenAI faces the potential of a full-blown EU merger probe, after a mutiny at the ChatGPT creator laid bare deep ties between the two companies. BBG

- Grifols tumbled after short seller Gotham City said the Spanish blood plasma firm artificially reduced leverage by consolidating earnings of units it doesn’t control and overstated profit. Grifols denied the allegations. BBG

- Israel is shifting away from major ground/air operations toward a more targeted phase of the war against Hamas and hopes to have the transition complete by the end of January. NYT

- Investors are warning governments around the world over “unmoored” levels of public debt, saying excessive pre-election borrowing promises risk sparking a bond market backlash. Government debt issuance in the US and the UK is expected to soar to the highest level on record in the coming year, with the exception of the early stages of the Covid pandemic. FT

- Congress on Monday began an uphill push to pass a new bipartisan spending agreement into law in time to avoid a partial government shutdown next week, with Speaker Mike Johnson encountering stiff resistance from his far-right flank to the deal he struck with Democrats. NYT

- Boeing slipped again premarket after United found loose bolts in some of its 737 Max 9 jetliners. Alaska Air said loose hardware was visible on some planes during inspections. The NTSB said it might widen its Max 9 probe beyond the model on which the accident occurred. BBG

- HPE is in advanced talks to buy JNPR for about $13 billion, in a bid to better position the nearly 100-year-old technology company in the era of artificial intelligence. WSJ

- The combination of low current valuations and a healthy economic outlook indicates that the Russell 2000 small-cap index should return roughly 9% in the next 6 months and 15% in the next 12 months. This compares with Goldman's forecast that the large-cap S&P 500 will rise by 7% to 5100 at the end of 2024 (total return of 9% including dividends). In recent decades, nearly two thirds of the variation in Russell 2000 12-month returns has been explained by valuations at the start of each period and real US economic growth during the period. If Goldman's 2024 US GDP growth forecast of 2% is realized, these historical relationships suggest small-caps should generate solid returns in coming months. GIR

A more detailed look at global markets courtesy of Newsquawk

APAC stocks traded higher as the region took impetus from the gains on Wall Street where tech outperformed as risk appetite was fuelled by a lower yield environment and a drop in oil prices. ASX 200 climbed above 7,500 with the index led by tech and consumer-related sectors owing to softer yields. Nikkei 225 printed its highest since March 1990 and rallied to just shy of 34,000 where it hit resistance. KOSPI was clouded after disappointing preliminary quarterly earnings from Samsung Electronics. Hang Seng and Shanghai Comp initially benefitted amid the broad constructive mood and recent PBoC hints at tools to boost credit including RRR although the upside was reversed after the PBoC drained liquidity and with Chinese oil majors pressured by the recent fall in oil prices.

Top Asian News

- Taiwan's ruling party presidential candidate Lai said Taiwan will build up defence deterrence and economic security, while he will maintain the status quo and current President Tsai's policies.

- Japanese police are investigating a suspicious object which was discovered in front of the main gate of the national diet building, via NTV

- ByteDance is further scaling back its ambitions in the gaming industry and is in talks to sell game titles to several prospective buyers, according to WSJ

- China's CPCA (auto industry) says China sold 2.37mln passenger vehicles in December, +8.3% Y/Y. 2023 retail passenger vehicle sales +5.6% Y/Y

- China's CPCA says China's auto exports set to overtake Japan as the largest in both volume and value terms in 2023

- "China’s economic growth in 2024 is forecast to continue to gain pace, with the estimated annual GDP growth rate to reach 5.3%, said a report by the Center for Forecasting Science under Chinese Academy of Sciences on Tuesday", according to Global Times

- Chinese Commerce Ministry says China is looking to further suspend tariff cuts on products including agriculture, fishery, machinery, auto parts and textiles from Taiwan

European bourses, Stoxx600 (-0.3%), initially began the session on a firmer footing echoing APAC optimism before succumbing to selling pressure as sentiment dwindled. IBEX 35 (-1.7%) underperforms, dragged down by Grifols (-42%) following a Gotham City Research report which said "we believe shares are uninvestable, likely zero"; Grifols to hold a board meeting on Tuesday. European sectors hold a negative tilt; Energy holds at the top of the pile as it attempts to nurse the prior day's hefty losses whilst Tech lags after outperforming yesterday. Recruitment names have been hit by a profit warning from London-listed Hays (-12%).

Top European News

- Hapag Lloyd (HLAG GY) says it deems the situation in the Red Sea as "still dangerous" and will continue to sail around the Cape of Good Hope; will take next decision as of January 15th

- ECB's Centeno says the ECB will not have to wait until May to make policy decisions, via econostream.

- Barclays said UK December consumer spending rose 2.3% Y/Y (prev. 2.9%).

- French PM Borne resigned and will act as caretaker until a new government is named. It was later reported that a new French PM is to be named on Tuesday morning, according to AFP.

FX

- DXY is directionless and contained within a 102.10-41 range, with the 21DMA residing just below the trough at 102.07.

- EUR continues to oscillate around the 1.0950 mark in light of a lack of fresh catalysts; session low at 1.0934.

- Yen is the best G10 performer, looking to make up ground lost last week, but still some way from its 28th December base at 140.24.

- Australian Building Approvals and Retail Sales initially supported the AUD, though strength faded alongside weakness in Iron prices.

- PBoC set USD/CNY mid-point at 7.1010 vs exp. 7.1502 (prev. 7.1006).

Fixed Income

- USTs are within yesterday's bounds but pressured with concession ahead of a 3yr auction which is likely factoring; yield curve incrementally flatter thus far.

- Bunds are pressured but remain above the prior sessions respective 135.15 and 135.06 troughs. Overall, action appears to be influenced by concession as corporate supply remains in focus.

- Gilts were initially the relative laggard, given looming supply, though after the strong Gilt auction (record investor demand) the benchmark jumped back above 100.00, but shy of the initial 100.26 session high.

- Netherlands sells EUR 2.08bln vs. Exp. EUR 2.0-2.5bln 2.5% 2030 DSL; average yield 2.334% vs. prev. 2.950%

- UK sells GBP 2.25bln 4.75% 2043: b/c 3.62x, average yield 4.391%, 0.2bps tail.

- Italy to raise EUR 10bln from new 7yr BTP (demand was over EUR 73bln), and EUR 5bln from a tap of a 30yr, according to leads (demand was over UR 91bln).

- Saudi Arabia completes first issuance of USD international bonds worth USD 12bln, according to a statement.

Commodities

- Crude futures are largely retracing some of yesterday’s hefty losses coupled with added tailwinds from geopolitics – with recent reports suggesting three Hezbollah members were killed in an Israeli strike.

- Spot gold is trading within recent ranges and trimming some of the prior day’s losses despite a relatively rangebound Dollar and quiet newsflow; Base metals show a mixed picture with the breadth of the market narrow.

- Motiva's Port Arthur, Texas refinery (636k BPD) large crude unit and coker were shut on Monday.

- Hezbollah is reportedly attempting to target to target Israel's offshore gas infrastructure “Karish” with drones, Saudi Al-Hadath reports citing sources via journalist Oseran; Aurora Intel clarifies a FPSO was targeted and not a gas rig.

Geopolitics

- Israeli officials said they will tell US Secretary of State Blinken that Palestinians will not return to northern Gaza unless Hamas releases more hostages, according to Al Jazeera.

- US Secretary of State Blinken said he found leaders in the Middle East determined to prevent a wider conflict but added they all recognised hurdles and nobody thinks anything will happen overnight.

- Three Hezbollah members were reportedly killed in a targeted strike on a vehicle in Ghandouriyeh in southern Lebanon, according to Reuters sources.

- Hezbollah says it attacked the Northern Command base with drones in retaliation for the killing of Arouri and the commander of the Radwan force, according to Walla News' Elster.

US Event Calendar

- 06:00: Dec. SMALL BUSINESS OPTIMISM 91.9, est. 91.0, prior 90.6

- 08:30: Nov. Trade Balance, est. -$64.9b, prior -$64.3b

Central Bank speakers

- 12:00: Fed’s Barr Speaks on Bank Regulation

DB's Jim Reid concludes the overnight wrap

Morning from what promises to be a nice day here in Helsinki which has warmed up significantly to around -2C as I type. Markets also warmed up considerable yesterday to start a new week with the S&P 500 (+1.41%) posting its biggest advance since mid-November and taking it back to 'only' -0.13% YTD. Yields on 10yr Treasuries (-1.6bps) gave up most of their initial rally but still saw their biggest decline of 2024 so far. The equity move was buoyed by renewed tech optimism but otherwise it was a fairly quiet day, with sentiment supported by falling commodity prices along with some decent data releases, which collectively added to hopes that a soft landing could still be achieved.

The good data news came primarily from the New York Fed’s latest Survey of Consumer Expectations. This showed another decline in inflation expectations across several horizons, and 1yr expectations were down to 3.0%, which is the lowest since January 2021. In addition, 3yr expectations were down to 2.6%, which was the lowest since June 2020, and 5yr expectations came down to 2.5%, which is the lowest since March 2023. So plenty of good news from the Fed’s perspective ahead of US CPI on Thursday.

At the same time, yesterday brought some significant declines for oil and gas prices, with Brent crude down -3.35% to $76.12/bbl, whilst WTI fell by -4.12% to $70.77/bbl. So another positive tailwind on the inflation side, which followed Saudi Arabia’s decision to cut their oil prices for buyers in all regions. That decline was echoed among several other commodities too, with European natural gas (-7.89%) falling back, whilst soybean (-0.82%) prices fell to their lowest in over two years.

This backdrop proved supportive for equities, especially in the US, as the S&P 500 (+1.41%) had its best day since mid-November, while Europe’s STOXX 600 (+0.38%) posted a more modest gain. T ech stocks led the advance, and the NASDAQ (+2.20%) and the FANG+ Index (+2.75%) saw even larger gains. The tech rally was led by chipmaker Nvidia, which gained +6.43% after announcing new products aimed at making better use of AI on personal computers. The main exception from the equity rally were those companies affected by last week’s incident on an Alaska Airlines flight, when part of the fuselage came off the plane. The result was that Boeing (-8.03%) was the worst performer in the entire S&P 500, and there was also a big slump for Spirit AeroSystems (-11.13%), a supplier for Boeing. Boeing’s decline led to a notable underperformance for the industrial Dow Jones index of just 30 companies (+0.58%).

With inflation expectations falling back, it was a favourable day for bond investors, though we did see a substantial reversal of the bond rally in the latter half of the US session. This reversal was helped by comments from Atlanta Fed President Bostic (an FOMC voter this year) shortly after the European close who, while noting that inflation had come down by more than he expected, reiterated that he expected rate cuts to come only in Q3. Near the end of the session we also heard from Fed Governor Bowman, one of the most hawkish FOMC voices, who said that policy appeared sufficiently restrictive to hit the 2% inflation target but that “we are not yet” at the point of rate cuts becoming appropriate, and noted “the risk that the recent easing in financial conditions” could stall the progress on inflation.

On the back of this, fed funds futures slightly downgraded the prospects of imminent cuts. The chances of a Fed cut by March were down to 63% at the close, their lowest since the December FOMC, from 73% the day before (and an intra-day high of 76% shortly after the NY Fed’s consumer survey). Treasuries still rallied modestly on the day – with the 2yr yield down -0.5bps to 4.38%, whilst the 10yr yield fell -1.6bps to 4.03% – but these closing levels were 7-8bps above their intra-day lows. Overnight in Asia, yields on the 10yr USTs (-2.1bps) are slightly lower again, trading at 4.01% as we go to print.

Looking back at Europe, there was some data optimism as the European Commission’s survey offered a fresh signal that activity was bottoming out in December, with economic sentiment up for a 3rd consecutive month to 96.4. That takes it up to its highest level since May, whilst the final consumer confidence reading was revised up a tenth from the flash print to -15.0, which is the highest since February 2022. We did get some more mixed data out of Germany, with factory orders seeing a smaller than anticipated rebound in November (+0.3% vs +1.1% expected), but this subdued signal was offset by more encouraging export data for the same month (+3.7% vs +0.5% expected).

Otherwise in Europe, there was also a rally for sovereign bonds. That came even as the ECB’s Vujcic said that they were “not talking about cutting interest rates now, and probably won’t before summer”. So some fresh pushback on the idea of imminent rate cuts coming from one of the more hawkish ECB voices. Nevertheless, sovereign bond yields still fell on the day, with those on 10yr bunds (-2.1bps), OATs (-3.0bps) and BTPs (-3.0bps) all moving lower.

Asian equity markets are mostly advancing this morning after the tech led rally on Wall Street overnight. In terms of specific moves, the Nikkei (+1.1%) has reopened firmly after a public holiday while the Hang Seng (+0.16%), and the Shanghai Composite (+0.05%) are losing some momentum after a decent open on fresh hopes of PBOC easing (more below). Elsewhere, the KOSPI (-0.25%) is also reversing after index heavyweight Samsung Electronics slashed its earnings forecast for 4Q23. In overnight trading, US futures are seeing small losses with those on the S&P 500 (-0.10%) and NASDAQ 100 (-0.12%) slightly lower

On the topic of China policy, yesterday we heard from Zou Lan, the head of the PBOC’s monetary policy department, that the PBOC may use its monetary policy tools to provide support for the growth in credit. So a potential hint at more easing coming before too long.

Elsewhere, early morning data showed that Tokyo’s inflation rate slowed more than expected to +2.4% y/y in December (v/s +2.5% expected) from an upwardly revised gain of +2.7% in the previous month. Meanwhile, core inflation came in at +2.1% y/y in December, slowing for the second-straight month in line with expectations and down from November’s +2.3% increase, thus taking some pressure off the BoJ to rush into exiting its ultra-loose monetary policy. Other data showed that household spending fell -2.9% y/y in November (-2.5% in October), declining for a ninth consecutive months and worse than the market forecast for a -2.3% decline. The Japanese yen (+0.45%) is gaining for the second straight day and trading at 143.58 versus the dollar.

To the day ahead now, and data releases include German industrial production for November and the Euro Area unemployment rate for November, whilst in the US there’s the NFIB’s small business optimism index for December, and the trade balance for November. From central banks, we’ll hear from Fed Vice Chair for Supervision Barr, and the ECB’s Villeroy.

Uncategorized

Women’s basketball is gaining ground, but is March Madness ready to rival the men’s game?

The hype around Caitlin Clark, NCAA Women’s Basketball is unprecedented — but can its March Madness finally rival the Men’s?

Share this:

In March 2021, the world was struggling to find its legs amid the ongoing Covid-19 pandemic. Sports leagues were trying their best to keep going.

It started with the NBA creating a bubble in Orlando in late 2020, playing a full postseason in the confines of Disney World in arenas that were converted into gyms devoid of fans. Other leagues eventually allowed for limited capacity seating in stadiums, including the NCAA for its Men’s and Women’s Basketball tournaments.

The two tournaments were confined to two cities that year — instead of games normally played in different regions around the country: Indianapolis for the men and San Antonio for the women.

But a glaring difference between the men’s and women’s facilities was exposed by Oregon’s Sedona Prince on social media. The workout and practice area for the men was significantly larger than the women, whose weight room was just a single stack of dumbbells.

Let me put it on Twitter too cause this needs the attention pic.twitter.com/t0DWKL2YHR

— SEDONA (@sedonaprince_) March 19, 2021

The video drew significant attention to the equity gaps between the Men’s and Women’s divisions, leading to a 114-page report by a civil rights law firm that detailed the inequities between the two and suggested ways to improve the NCAA’s efforts for the Women’s side. One of these suggestions was simply to give the Women’s Tournament the same March Madness moniker as the men, which it finally got in 2022.

But underneath the surface of these institutional changes, women’s basketball’s single-biggest success driver was already emerging out of the shadows.

During the same COVID-marred season, a rookie from Iowa led the league in scoring with 26.6 points per game.

Her name: Caitlin Clark.

As it stands today, Clark is the leading scorer in the history of college basketball — Men’s or Women’s. Her jaw-dropping shooting ability has fueled record viewership and ticket sales for Women’s collegiate games, carrying momentum to the March Madness tournament that has NBA legends like Kevin Garnett and Paul Pierce more excited for the Women’s March Madness than the Men’s this year.

Related: Ticket prices for Caitlin Clark's final college home game are insanely high

But as the NCAA tries to bridge the opportunities given to the two sides, can the hype around Clark be enough for the Women’s March Madness to bring in the same fandom as the Men for the 2024 tournaments?

TheStreet spoke with Jon Lewis of Sports Media Watch, who has been following sports viewership trends for the last two decades; Melissa Isaacson, a veteran sports journalist and longtime advocate of women’s basketball; and Pete Giorgio, Deloitte’s leader for Global and US Sports to dissect the rise Caitlin Clark and women’s collegiate hoops ahead of March Madness.

“Nobody is moving the needle like Caitlin Clark,” Lewis told TheStreet. “Nobody else in sports, period, right now, is fueling record numbers on all these different networks, driving viewership beyond what the norm has been for 20 years."

The Caitlin Clark Effect is real — but there are other reasons for the success of women's basketball

The game in which Clark broke the all-time college scoring record against Ohio State on Sunday, Mar. 3 was seen by an average of 3.4 million viewers on Fox, marking the first time a women’s game broke the two million viewership barrier since 2010. Viewership for that game came in just behind the men’s game between Michigan State vs Arizona game on Thanksgiving, which Lewis said was driven by NFL viewership on the same day.

A week later, Iowa’s Big Ten Championship win over Nebraska breached the three million viewers mark as well, and the team has also seen viewership numbers crack over 1.5 million viewers multiple times throughout the regular season.

The success on television has also translated to higher ticket prices, as tickets to watch Clark at home and on the road have breached hundreds of dollars and drawn long lines outside stadiums. Isaacson, who is a professor at Northwestern, said she went to the game between the Hawkeyes and Northwestern Wildcats — which was the first sellout in school history for the team — and witnessed the effect of Clark in person.

“Standing in line interviewing people at the Northwestern game, seeing men who've never been to a women's game with their little girls watching and so excited, and seeing Caitlin and her engaging with little girls, it’s just been really fun,” Isaacson said.

But while Clark is certainly the biggest success driver, her game isn’t the only thing pulling up the women’s side. The three-point revolution, which started in the NBA with the introduction of deeper analytics as well as the rise of stars like Steph Curry, has been a positive for the Women’s game.

“They backed up to the three-point line and it’s opening up the game,” Isaacson said.

One of the major criticisms from a lot of women’s hoops detractors has been how the game does not compare in terms of quality to the men. However, shooting has become a great equalizer, displayed recently during the 2024 NBA All-Star Weekend last month when the WNBA’s Sabrina Ionescu nearly defeated Curry — who is widely considered the greatest shooter ever — in a three-point contest.

Clark has become the embodiment of the three-point revolution for the women. Her shooting displays have demanded the respect of anyone who has doubted women’s basketball in the past because being a man simply doesn’t grant someone the ability to shoot long-distance bombs the way she can.

Basketball pundit Bill Simmons admitted on a Feb. 28 episode of “The Bill Simmons Podcast” that he used to not want to watch women’s basketball because he didn’t enjoy watching the product, but finds himself following the women’s game this year more than the men’s side in large part due to Clark.

“I think she has the chance to be the most fun basketball player, male or female, when she gets to the pros,” Simmons said. “If she’s going to make the same 30-footers, routinely. It’s basically all the same Curry stuff just with a female … I would like watching her play in any format.”

But while Clark is driving up the numbers at the top, she’s not the only one carrying the greatness of the product. Lewis, Isaacson, Giorgio — and even Simmons, on his podcast — agreed that there are several other names and collegiate programs pulling in fans.

“It’s not just Iowa, it’s not just Caitlin Clark, it’s all of these teams,” Giorgio said. “Part of it is Angel Reese … coaches like Dawn Staley in South Carolina … You’ve got great stories left and right.”

The viewership showed that as well because the SEC Championship game between the LSU Tigers and University of South Carolina Gamecocks on Sunday, Mar. 10 averaged two million viewers.

Bridging the gap between the Men’s and Women’s March Madness viewership

The first reason women are catching up to the men is really star power. While the Women’s division has names like Clark and Reese, there just aren’t any names on the Men’s side this year that carry the same weight.

Garnett said on his show that he can’t name any men’s college basketball players, while on the women’s side, he could easily throw out the likes of Clark, Reese, UConn’s Paige Bueckers, and USC’s JuJu Watkins. Lewis felt the same.

Kevin Garnett energy towards WBB is unmatched. Sorry for the language but that’s how he talks. Just watch. pic.twitter.com/0yGBRGaF3O

— The9450 Podcast Network (@The9450) March 8, 2024

“The stars in the men's game, with one and done, I genuinely couldn't give you a single name of a single men’s player,” Lewis said.

A major reason for this is that the Women’s side has the continuity that the Men’s side does not. The rules of the NBA allow for players to play just one year in college — or even play a year professionally elsewhere — before entering the draft, while the WNBA requires players to be 22-years-old during the year of the draft to be eligible.

“You know the stars in the women's game because they stay longer,” Lewis said. “[In the men’s game], the programs are the stars … In the women's game, it's a lot more like the NBA where the players are the stars.”

Parity is also a massive factor on both sides. The women’s game used to be dominated by a few schools like UConn and Notre Dame. Nowadays, between LSU, Iowa, University of South Carolina, Stanford, and UConn, there are a handful of schools that have a shot to win the entire tournament. While this is more exciting for fans, the talent in the women's game isn’t deep enough, so too many upsets are unlikely. Many of the biggest draws are still expected to make deep runs.

But on the men’s side, there is a bigger shot that the smaller programs make it to the end — which is what was seen last year. UConn eventually won the whole thing, but schools without as big of a national fanbase in San Diego State, Florida Atlantic University, and the University Miami rounded out the Final Four.

“People want to see one Cinderella,” Lewis said. “They don't want to see two and three, they want one team that isn't supposed to be there.”

Is Women's March Madness ready to overtake the Men?

Social media might feel like it’s giving more traction to the Women’s game, but experts don’t necessarily expect that to show up in the viewership numbers just yet.

“There’s certainly a lot more buzz than there used to be,” Giorgio said. “It’s been growing every year for not just the past few years but for 10 years, but it’s hard to compare it versus Men’s.”

But the gap continues to get smaller and smaller between the two sides, and this year's tournament could bridge that gap even further.

One indicator is ticket prices. For the NCAA Tournament Final Four in April, “get-in” ticket prices are currently more expensive for the Women’s game than the Men’s game, according to TickPick. The ticketing site also projects that the Women’s Final Four and Championship game ticket prices will smash any previous records for the Women’s side should Clark and the Hawkeyes make a run to the end.

Getty Images/TheStreet

The caveat is that the Women’s Final Four is played in a stadium that has less than a third of the seating capacity of the Men’s Final Four. That’s why the average ticket prices are still more expensive for the men, although the gap is a lot smaller this year than in previous years.

But that caveat pretty much sums up where the women’s game currently stands versus the men’s: There is still a significant gap between the distribution and availability of the former.

While Iowa’s regular season games have garnered millions of viewers, the majority of the most-viewed games are still Men’s contests.

To illustrate the gap between the men’s and women’s game — last year’s Women’s Championship game that saw the LSU Tigers defeat the Hawkeyes was a record-breaking one for the women, drawing an average of 9.9 million viewers, more than double the viewership from the previous year.

One of the main reasons for that increase, as Lewis pointed out, is that last year’s Championship game was on ABC, which was the first time since 1995 that the Women’s Championship game was on broadcast television. The 1995 contest between UConn and Tennessee drew 7.4 million viewers.

The Men’s Championship actually had a record low in viewership last year garnering only 14.7 million viewers, driven in-part due to a lack of hype surrounding the schools that made it to the Final Four and Championship game. Viewership for the Men’s title game has been trending down in recent years — partly due to the effect the pandemic had on collective sports viewership — but the Men’s side had been easily breaching 20 million viewers for the game as recently as 2017.

Iowa's Big Ten Championship win on Sunday actually only averaged 6,000 fewer viewers than the iconic rivalry game between Duke and University of North Carolina Men’s Basketball the day prior. However, there is also the case that the Iowa game was played on broadcast TV (CBS) versus the Duke-UNC game airing on cable channel (ESPN).

So historical precedence makes it unlikely that we’ll see the women’s game match the men’s in terms of viewership as early as this year barring another massive viewership jump for the women and a lack of recovery for the Men’s side.

But ultimately, this shouldn’t be looked at as a down point for Women’s Basketball, according to Lewis. The Men’s side has built its viewership base for years, and the Women’s side is still growing. Even keeping pace with the Men’s viewership is already a great sign.

“The fact that these games have Caitlin Clark are even in the conversation with men's games, in terms of viewership is a huge deal,” Lewis said.

Related: Angel Reese makes bold statement for avoiding late game scuffle in championship game

recovery pandemic covid-19Uncategorized

One city held a mass passport-getting event

A New Orleans congressman organized a way for people to apply for their passports en masse.

Share this:

While the number of Americans who do not have a passport has dropped steadily from more than 80% in 1990 to just over 50% now, a lack of knowledge around passport requirements still keeps a significant portion of the population away from international travel.

Over the four years that passed since the start of covid-19, passport offices have also been dealing with significant backlog due to the high numbers of people who were looking to get a passport post-pandemic.

Related: Here is why it is (still) taking forever to get a passport

To deal with these concurrent issues, the U.S. State Department recently held a mass passport-getting event in the city of New Orleans. Called the "Passport Acceptance Event," the gathering was held at a local auditorium and invited residents of Louisiana’s 2nd Congressional District to complete a passport application on-site with the help of staff and government workers.

'Come apply for your passport, no appointment is required'

"Hey #LA02," Rep. Troy A. Carter Sr. (D-LA), whose office co-hosted the event alongside the city of New Orleans, wrote to his followers on Instagram (META) . "My office is providing passport services at our #PassportAcceptance event. Come apply for your passport, no appointment is required."

More Travel:

- A new travel term is taking over the internet (and reaching airlines and hotels)

- The 10 best airline stocks to buy now

- Airlines see a new kind of traveler at the front of the plane

The event was held on March 14 from 10 a.m. to 1 p.m. While it was designed for those who are already eligible for U.S. citizenship rather than as a way to help non-citizens with immigration questions, it helped those completing the application for the first time fill out forms and make sure they have the photographs and identity documents they need. The passport offices in New Orleans where one would normally have to bring already-completed forms have also been dealing with lines and would require one to book spots weeks in advance.

These are the countries with the highest-ranking passports in 2024

According to Carter Sr.'s communications team, those who submitted their passport application at the event also received expedited processing of two to three weeks (according to the State Department's website, times for regular processing are currently six to eight weeks).

While Carter Sr.'s office has not released the numbers of people who applied for a passport on March 14, photos from the event show that many took advantage of the opportunity to apply for a passport in a group setting and get expedited processing.

Every couple of months, a new ranking agency puts together a list of the most and least powerful passports in the world based on factors such as visa-free travel and opportunities for cross-border business.

In January, global citizenship and financial advisory firm Arton Capital identified United Arab Emirates as having the most powerful passport in 2024. While the United States topped the list of one such ranking in 2014, worsening relations with a number of countries as well as stricter immigration rules even as other countries have taken strides to create opportunities for investors and digital nomads caused the American passport to slip in recent years.

A UAE passport grants holders visa-free or visa-on-arrival access to 180 of the world’s 198 countries (this calculation includes disputed territories such as Kosovo and Western Sahara) while Americans currently have the same access to 151 countries.

stocks pandemic covid-19 grantsUncategorized

Fast-food chain closes restaurants after Chapter 11 bankruptcy

Several major fast-food chains recently have struggled to keep restaurants open.

Share this:

{kind=link}

Competition in the fast-food space has been brutal as operators deal with inflation, consumers who are worried about the economy and their jobs and, in recent months, the falling cost of eating at home.

Add in that many fast-food chains took on more debt during the covid pandemic and that labor costs are rising, and you have a perfect storm of problems.

It's a situation where Restaurant Brands International (QSR) has suffered as much as any company.

Related: Wendy's menu drops a fan favorite item, adds something new

Three major Burger King franchise operators filed for bankruptcy in 2023, and the chain saw hundreds of stores close. It also saw multiple Popeyes franchisees move into bankruptcy, with dozens of locations closing.

RBI also stepped in and purchased one of its key franchisees.

"Carrols is the largest Burger King franchisee in the United States today, operating 1,022 Burger King restaurants in 23 states that generated approximately $1.8 billion of system sales during the 12 months ended Sept. 30, 2023," RBI said in a news release. Carrols also owns and operates 60 Popeyes restaurants in six states."

The multichain company made the move after two of its large franchisees, Premier Kings and Meridian, saw multiple locations not purchased when they reached auction after Chapter 11 bankruptcy filings. In that case, RBI bought select locations but allowed others to close.

Image source: Chen Jianli/Xinhua via Getty

Another fast-food chain faces bankruptcy problems

Bojangles may not be as big a name as Burger King or Popeye's, but it's a popular chain with more than 800 restaurants in eight states.

"Bojangles is a Carolina-born restaurant chain specializing in craveable Southern chicken, biscuits and tea made fresh daily from real recipes, and with a friendly smile," the chain says on its website. "Founded in 1977 as a single location in Charlotte, our beloved brand continues to grow nationwide."

Like RBI, Bojangles uses a franchise model, which makes it dependent on the financial health of its operators. The company ultimately saw all its Maryland locations close due to the financial situation of one of its franchisees.

Unlike. RBI, Bojangles is not public — it was taken private by Durational Capital Management LP and Jordan Co. in 2018 — which means the company does not disclose its financial information to the public.

That makes it hard to know whether overall softness for the brand contributed to the chain seeing its five Maryland locations after a Chapter 11 bankruptcy filing.

Bojangles has a messy bankruptcy situation

Even though the locations still appear on the Bojangles website, they have been shuttered since late 2023. The locations were operated by Salim Kakakhail and Yavir Akbar Durranni. The partners operated under a variety of LLCs, including ABS Network, according to local news channel WUSA9.

The station reported that the owners face a state investigation over complaints of wage theft and fraudulent W2s. In November Durranni and ABS Network filed for bankruptcy in New Jersey, WUSA9 reported.

"Not only do former employees say these men owe them money, WUSA9 learned the former owners owe the state, too, and have over $69,000 in back property taxes."

Former employees also say that the restaurant would regularly purchase fried chicken from Popeyes and Safeway when it ran out in their stores, the station reported.

Bojangles sent the station a comment on the situation.

"The franchisee is no longer in the Bojangles system," the company said. "However, it is important to note in your coverage that franchisees are independent business owners who are licensed to operate a brand but have autonomy over many aspects of their business, including hiring employees and payroll responsibilities."

Kakakhail and Durranni did not respond to multiple requests for comment from WUSA9.

bankruptcy pandemic

Key shipping company files for Chapter 11 bankruptcy

Women’s basketball is gaining ground, but is March Madness ready to rival the men’s game?

These Cities Have The Highest (And Lowest) Share Of Unaffordable Neighborhoods In 2024

Tight inventory and frustrated buyers challenge agents in Virginia

Industrial Production Increased 0.1% in February

Key shipping company files Chapter 11 bankruptcy

One city held a mass passport-getting event

Southwest and United Airlines have bad news for passengers

The hostility Black women face in higher education carries dire consequences

Simple blood test could predict risk of long-term COVID-19 lung problems

-

Uncategorized3 weeks ago

Uncategorized3 weeks agoAll Of The Elements Are In Place For An Economic Crisis Of Staggering Proportions

-

International1 week ago

International1 week agoEyePoint poaches medical chief from Apellis; Sandoz CFO, longtime BioNTech exec to retire

-

Uncategorized4 weeks ago

Uncategorized4 weeks agoCalifornia Counties Could Be Forced To Pay $300 Million To Cover COVID-Era Program

-

Uncategorized3 weeks ago

Uncategorized3 weeks agoApparel Retailer Express Moving Toward Bankruptcy

-

Uncategorized1 month ago

Uncategorized1 month agoIndustrial Production Decreased 0.1% in January

-

International1 week ago

International1 week agoWalmart launches clever answer to Target’s new membership program

-

Spread & Containment3 days ago

Spread & Containment3 days agoIFM’s Hat Trick and Reflections On Option-To-Buy M&A

-

Uncategorized4 weeks ago

Uncategorized4 weeks agoRFK Jr: The Wuhan Cover-Up & The Rise Of The Biowarfare-Industrial Complex