Futures Dip, Yields Jump Ahead Of Critical Inflation Report

Futures Dip, Yields Jump Ahead Of Critical Inflation Report

Another day, another extremely tight range of overnight futures trading – with spoos stuck in a 1% range for the past two weeks, it feels as if nothing can push the index away from..

Futures Dip, Yields Jump Ahead Of Critical Inflation Report

Another day, another extremely tight range of overnight futures trading - with spoos stuck in a 1% range for the past two weeks, it feels as if nothing can push the index away from its massive gamma gravity around 4,400, although today's CPI - if it shocks either higher or lower relative to expectations - may be just the trigger that breaks this boring rangebound market. 10Y Yield rose as high as 1.375% as the dollar tracked the move higher.

Amid muted trading volumes, S&P futures dipped slightly lower from a fresh record ahead of data out today showing U.S. consumer prices probably jumped again in July; Nasdaq futures fell on Wednesday, while Dow indicators rose slightly as investors swapped heavyweight technology stocks with economically sensitive sectors following the approval of a U.S. infrastructure bill. At 745am ET, Dow e-minis were up 2 points, or 0.1%, S&P 500 e-minis were down -5 points, or 0.11%, and Nasdaq 100 e-minis were down 31points, or 0.2%.

Coinbase Global rose in pre-market trading after reporting second quarter results, while biotech firm Cohbar Inc. surged on results from a treatment study. Energy firms Exxon, Schlumberger, Marathon Oil, Occidental Petroleum and Halliburton fell between 0.6% and 1.5%, tracking crude prices. Heavyweight FAAMG stocks edged lower, weighed down by a rise in Treasury yields. Heavy industrials Caterpillar and Deere, construction materials suppliers Vulcan Materials, and Nucor Corp rose between 0.4% and 1.9% in premarket trading, adding to sharp gains in the previous session on hopes of reaping gains from infrastructure projects. Here are some of the other most notable premarket movers today:

Airline stocks are lower, with investors spooked by a Southwest Airlines (LUV) warning that a recent surge in Covid-19 cases is weighing on U.S. bookings. Southwest shares slip 2%.

Barnwell Industries (BRN) surges 9% after the company reported a 28% increase in third quarter revenue.

FuboTV (FUBO) shares rise 12%, with Roth saying the streaming company’s 2Q results delivered a solid beat and raise.

Good Times Restaurants (GTIM) surges 27% after saying revenue rose to $33.9m in the fiscal third quarter, up 39% from a year ago.

Mogo Inc. (MOGO) rallies 20% after raising its forecast for fourth-quarter subscription and services revenue growth.

ON24 (ONTF) shares drop 20% after the company gave an outlook that analysts said was weak, prompting firms to slash their price targets.

PubMatic (PUBM) gains 7% as analysts are positive on the digital advertising software company after it reported second-quarter results and raised its full-year revenue view.

Splunk (SPLK) gains 2% after being upgraded to buy at UBS, which writes that the application software company is showing signs of improved stability.

Upstart (UPST) soars 22% after the artificial intelligence lending platform forecast full-year revenue that topped expectations.

Vine Energy Inc. (VEI) gains 7% after Chesapeake Energy Corp. agreed to acquire the company in a deal valued at about $2.2 billion.

WW International (WW) plunges 24% after it offered year forecasts that were well below analysts’ projections and second- quarter results that also fell short.

Wix.com (WIX) shares are down 9% after the company cut its full-year revenue outlook.

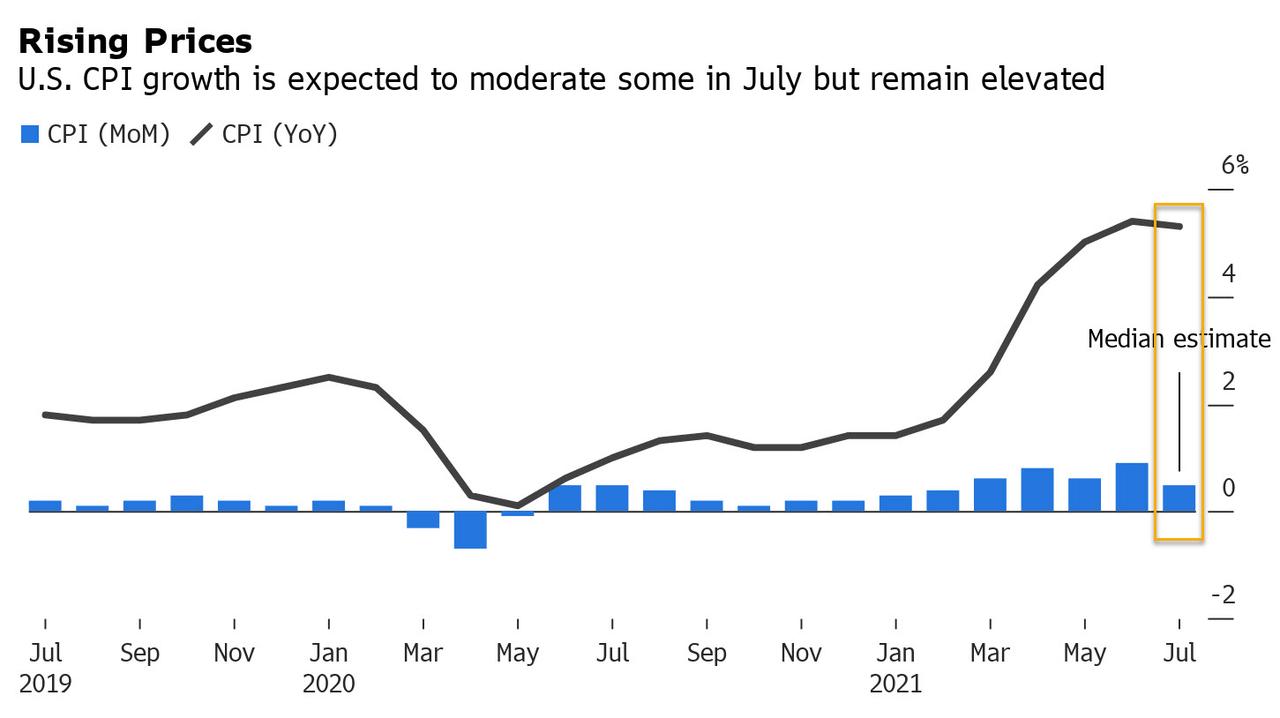

Data due at 0830 a.m. ET will likely show U.S. consumer prices rose 5.3% year-on-year in July, according to a Reuters poll, and at a time when two U.S. central bank officials said inflation was already at levels that satisfy one leg of a key test for tightening policy. Inflation has dictated market sentiment in the past few months, with market participants fearing higher price pressures could force the Fed to pare back its ultra-loose accommodative stance sooner than expected.

As DB's Jim Reid notes, "today should be a big day, however the evidence from recent big CPI prints is that the market doesn’t believe it’s sustainable so it might take a lot to shake things up today. For the record our US economists are expecting a +0.5% m/m increase in headline CPI and a tick down to 5.3% y/y, after last month came in at +0.9% m/m, which took the y/y reading to +5.4%. They expect a +0.4% m/m and +4.3% y/y core print after June was +0.9% m/m and +4.5% y/y. This follows three straight months of higher-than-expected headline price increases, +0.9% (+0.5% expected) in June, +0.6% (+0.5% expected) in May, and +0.8% (+0.2% expected) in April. The market saw Treasury yields move more than 5bps on the day of the last three CPI prints. US 10yr Treasury yields rose +5.2bps on last month’s release, and back in May, when the April data surprised to the upside for the first time, yields rose +7.0bps. On the other hand, yields fell -5.9bps the month in between when the data was more in-line with expectations. Yields have also fallen in the days following recent prints as markets haven’t been convinced. Let’s see if anything changes today. The breakdown will be very important so let’s see if more of the transitory inflation filters into non-covid related sectors."

“This is important in terms of short-term sentiment,” said Giles Coghlan, chief currency analyst at HYCM. Investors, however, will then turn to whether the Fed will signal timings on tapering stimulus at a meeting of central bankers in Jackson Hole, Wyoming, on Aug. 26-28, Coghlan said. U.S. non-farm payrolls figures due in September could also influence tapering if they are particularly strong.

"The big question at the moment is are we at peak CPI or is there more in the tank?” said Michael Hewson, chief markets analyst at CMC Markets.

He added that a strong figure could trigger a spike in bond yields and send jitters through stocks. Investor focus on U.S. price data comes as Federal Reserve officials talk up the prospects of unwinding some of the stimulus that has helped the recovery from the pandemic. Chicago Fed President Charles Evans said he expects substantial further progress later this year on the central bank’s tapering intentions.

In Europe, the Stoxx 600 index hit a new record high for an eighth consecutive session amid strong earnings from the likesof ABN Amro Bank NV and Stop & Shop owner Royal Ahold Delhaize NV. Here are some of the biggest European movers today:

ABN Amro shares gain as much as 5% after the Dutch lender posted 2Q results that will likely spark consensus upgrades, Jefferies writes.

Avast shares rise as much as 4.7% in London after NortonLifeLock agreed to buy the company in a cash and stock deal valued at as much as $8.6b.

Spirax-Sarco shares advance as much as 6.7%, hitting a record high, following 1H results that Jefferies said look “good.”

Thyssenkrupp shares slide as much as 7.5% after 3Q results; while adj. Ebit was just above consensus average, FY free cash flow guidance was a little worse than before, according to Baader.

Quilter shares decline as much as 4.9% as the U.K. wealth manager gives a cautious outlook alongside first-half results.

Deliveroo shares reverse earlier gains to trade as much as 4.7% lower after results, with Citi flagging comments over signs of moderating growth in Europe, and “conservative” guidance from the food delivery company.

Earlier in the session, Asian stocks were steady as cyclical shares benefited on Wednesday from an increase in bond yields, with traders turning their focus to key inflation data from the U.S. The MSCI Asia Pacific Index was little changed after tech stocks dragged the gauge back from a gain of as much as 0.4%. Energy and financial stocks were higher, and the passing of a $550 billion infrastructure plan by the U.S. Senate boosted construction-related shares. In a relatively quiet trading day in Asia, many investors were waiting for the report on U.S. consumer-price inflation on Wednesday. The release will help investors gauge the Federal Reserve’s tapering intentions as officials meet at the Jackson Hole conference later this month. U.S. 10-year Treasury yields breached the 1.37% level in their sixth straight days of gains ahead of the inflation report. The Asian stock benchmark appears to be on better footing in August, with a 1.8% advance so far, following two straight monthly declines. While the spread of the delta variant of Covid-19 is taking a toll on economies in the region, the wild swings in Chinese shares triggered by new regulations have calmed even as investors continue to try to figure out Beijing’s next policy change. READ: Real-Time Data Suggest Asia’s Economy Already Feeling Delta Hit “We expect policy risks to be near-term overhang, so it doesn’t really change our long-term positive view about structural growth,” Lilian Leung, portfolio manager for Greater China equities at JPMorgan Asset Management, told Bloomberg Television. The cyclicals-heavy Japanese stock indexes were among the best performers in Asia Pacific, while Singapore equities declined even after the country raised its annual economic-growth forecast to between 6% and 7%. Indonesia’s stock market was closed for a holiday.

Japanese equities rose for a fourth straight day, as cyclicals outperformed following a rise in U.S. bond yields. Banks and automakers were the biggest boosts to the Topix, which advanced 0.9%. Fast Retailing and Daikin were the largest contributors to a 0.7% gain in the Nikkei 225. U.S. tech stocks slumped in contrast to a broader gains in the overall market Tuesday, exposing lingering concerns about the ability of the economy to weather less stimulus and rising Covid outbreaks. Treasury yields rose. The Senate passed a $550 billion infrastructure plan that would represent the biggest burst of spending on U.S. public works in decades. “U.S. long-terms yields, which have been extremely low, have finally recovered to around 1.35%, and cyclical Japanese equities are likely to get a lift,” said Mitsushige Akino, a senior executive officer at Ichiyoshi Asset Management. “But given the weakness in semiconductor-related stocks in the U.S., upside for the local chips sector, which is representative of value stocks, will likely be limited.”

Most Indian shares ended lower as small and mid-sized securities fell for a third day on concern that new measures by local bourse BSE Ltd. would hurt the outlook for penny stocks. The S&P BSE Sensex dropped less than 0.1% at the close, with 17 stocks down and 13 up. The NSE Nifty 50 Index ended flat. Ten of the 19 sector sub-indexes compiled by BSE Ltd. slipped, led by a gauge of healthcare companies. The BSE S&P SmallCap Index ended 0.8% lower, following an intraday slump of as much as 3.3%. A midcap measure declined 0.2%. Both gauges trimmed earlier losses after BSE clarified it will introduce price bands on the movement of certain stocks based on their performance over a period of six months, one year, two years and three years. The bourse’s proposals have sparked concerns it may introduce similar rules across mid and smallcap space. The selling was sentiment-driven, said Kishor Ostwal, managing director of Mumbai-base CNI Research Ltd. “Such rules disturb the price discovery mechanism in the market, which investors don’t like,” he said by phone

In Australia, the S&P/ASX 200 index rose 0.3% to close at 7,584.30, a fresh record. Banks contributed the most to the benchmark’s advance after CBA reported a surge in earnings. Australia’s largest lender also unveiled a record A$6 billion share buyback plan and boosted its dividend. Iress was among the top performers after saying it plans to back EQT’s sweetened takeover proposal. Megaport was the worst performer after broker downgrades. In New Zealand, the S&P/NZX 50 index fell 0.1% to 12,748.07.

In rates, Treasuries were mildly cheaper across belly of the curve as market awaits 10-year auction that follows solid German 10-year sale. Yields were higher by up to 1.5bp across 7-year sector, cheapening the 2s7s30s fly 2.4bp on the day and to widest levels since July 7; 10-year yields around 1.37%. In Asia, both Aussie and Japan sales were soft overnight. Traders will focus on July CPI print, with inflation expected to remain hot and little sign that households are balking at paying more for goods and services. U.S. auctions continue with $41b 10-year note sale at 1pm ET, and Thursday’s $27b 30-year concludes this weeks sales.

In FX, the dollar headed towards this year’s high against the euro and achieved a five-week peak against the yen ahead of the CPI data. The U.S. currency rose to 110.72 yen, and the euro eased to $1.1714. The greenback was supported by rises in longer and shorter dated treasury yields, which reached their highest levels since mid-July with yields on benchmark 10-year Treasury notes at 1.3675%.

In commodities, Crude oil prices tumbled below $70 a barrel, pressured by a CNBC report that the White House will call on OPEC and its allies to boost production in an effort to combat escalating gasoline prices. WTI was down 1.3% at $67.43 a barrel, while Brent crude fell 1.16% to $69.81.

Elsewhere, Bitcoin was back above $46,000 even as the Senate passed an infrastructure bill containing broad oversight of virtual currencies.

Looking at the day ahead now, outside of the aforementioned US CPI July data, we will get similar prints from Italy and Germany later today. US data will also include July’s monthly budget statement and weekly MBA mortgage applications. There will be more fed speakers today as Governor Bostic speaks for the second time this week and we will also hear from Governors Logan and George. The vast majority of earnings are currently behind us but there are some large cap names reporting today, including NIO, Prudential, EBAY, SMC Corp, Vestas, and Commonwealth Bank of Australia.

Market Snapshot

S&P 500 futures down 0.1% to 4,424.25

STOXX Europe 600 little changed at 472.73

MXAP little changed at 200.78

MXAPJ down 0.3% to 663.66

Nikkei up 0.7% to 28,070.51

Topix up 0.9% to 1,954.08

Hang Seng Index up 0.2% to 26,660.16

Shanghai Composite little changed at 3,532.62

Sensex down 0.2% to 54,421.81

Australia S&P/ASX 200 up 0.3% to 7,584.30

Kospi down 0.7% to 3,220.62

Brent Futures up 0.4% to $70.90/bbl

Gold spot up 0.2% to $1,732.61

U.S. Dollar Index little changed at 93.15

German 10Y yield up 2.1 bps to -0.436%

Euro little changed at $1.1714

Brent Futures up 0.4% to $70.90/bbl

Top Overnight News from Bloomberg

Senate Democrats took a major step toward the biggest expansion in decades of federal efforts to reduce poverty, care for the elderly and protect the environment, passing a $3.5 trillion budget framework that opens the way for President Joe Biden’s economic agenda

New York Governor Andrew Cuomo’s resignation on Tuesday creates a power vacuum in the politics of a state he had dominated for a decade, adding new uncertainty for Democrats gearing up for crucial congressional and state elections next year

Poland’s ruling coalition has crumbled, endangering the nationalists’ grip on power halfway through their second term

A more detailed look at global markets courtesy of Newsquawk

APAC stocks saw a mixed session following the similar handover from Wall Street, which saw the SPX and DJIA pushed to new records, whilst the NDX was pressured by higher sector-wide gains. The Nikkei 225 (+0.7%) took an early lead on the back of strength in its industrial and financial names, but later pulled back towards the 28k mark whilst Softbank shares remained weak following underwhelming earnings. The KOSPI (-0.7%) stayed subdued after North Korea warned of “massive security crises every minute”, as the US and South Korea gear up for the annual military drills. The Hang Seng (+0.2%) was choppy and fluctuated between gains and losses whilst the Shanghai Comp (+0.1%) was somewhat stable following the volatile price action earlier this week.

Top Asian News

China Evergrande Soars After Confirming Talks to Sell Assets

China’s Credit Expands at Slowest Pace Since February 2020

JBS’s Salmon Deal at Risk as Billionaire Forrest Ups Stake

China Vaccine Makers Fall After Global Sector Weakness

European equities (Eurostoxx 50 +0.2%) trade with marginal gains with the Stoxx 600 once again printing a fresh record high. Fresh macro developments for the region remain sparse with some of the discrepancies between individual indices dictated by earnings. The APAC lead was a relatively mixed one, whilst US futures currently trade with marginal losses after the SPX and DJIA rose to record highs during yesterday’s session. Developments stateside have seen the US Senate vote 50-49 to approve the USD 3.5trl Democratic Budget plan and thus pave the way for developing the budget bill and implementing priorities of the Biden administration. Elsewhere, the taper timeline debate remains at the forefront of market commentary with the latest Fed-speak from 2021 voter Evans suggesting that he would like to see a few more jobs reports before making a decision on tapering. Sectors trade predominantly firmer in Europe with minor outperformance in Media, Oil & Gas and Retail. To the downside, Travel & Leisure names lag as a by-product of Flutter Entertainment giving back some of yesterday’s earnings-inspired gains, whilst the rate-sensitive Tech sector is seen lower amid advances in global bond yields. Individual movers include ABN AMRO (+4.1%) at the top of the Stoxx 600 after reporting a firmer than expected recovery in net profit and announcing the resumption of dividend payments. Avast (+2.1%) sits at the top of the FTSE 100 after announcing that NortonLifeLock is to acquire the Co. in a USD 8.6bln deal. To the downside, ThyssenKrupp (-6.9%) sits at the foot of the Stoxx 600 after noting alongside earnings that contract structures at the Co. mean that there will be a delay in increased raw material and steel prices feeding through to revenues and earnings. Deliveroo (-4.4%) are also seen lower on the session post-encouraging earnings results with the Co. noting that it has not had any discussions with Delivery Hero since it invested and views it as just a financial investment.

Top European News

Prudential 1H Adj Op. Profit From Cont Ops $1.57B vs $1.29B Y/Y

Deliveroo Emerges From Lockdown With Sales Jump, Order Surge

Wind Giant Vestas Plunges as Commodities Rally Bites

European Gas Keeps Breaking Records on Tight Supply

In FX, the overriding theme is still Dollar outperformance, and with few exceptions to the rule as the DXY ventures further above 93.000 and nearer the final highs that stand in the way of the current 2021 pinnacle at 93.439 set right at the end of Q1. For the record, these stand at 93.194 from July 21 and 93.338 on April 1 vs 93.192 thus far in wake of last Friday’s strong US jobs data that has been widely recognised as constituting another step in the right direction for QE tapering by Fed officials including the ‘influencer’ and VC Clarida. However, the Euro is putting up a stern fight in defence of its y-t-d low and perhaps on the grounds that it resides in close proximity to a psychological level and Fib retracement just a few pips below 1.1700. Moreover, Eur/Usd may be deriving some traction indirectly via decent option expiry interest in the Eur/Gbp cross at the 0.8450 strike (1.1 bn) and the fact that this aligns with yesterday’s new 2021 base. Whatever the rationale, Eur/Usd is hovering within a 1.1726-06 range and Cable between 1.3844-07 parameters having retreated through technical support in the form of the 21 DMA (1.3830) and a Fib (1.3826 representing the 38.2% reversal 1.3982 to 1.3573) awaiting US CPI data, more Fed speak and the 2nd tranche of Quarterly Refunding.

NZD/AUD/CAD - Cross-currents are also impacting trade down under as Aud/Nzd chops and changes from circa 1.0511 to 1.0471, and is probing the downside at present to the benefit of the Kiwi relative to the Aussie that is also contending with unfolding virus developments. On that very note, lockdown in Melbourne has been extended for another week to keep Aud/Usd depressed beneath 0.7350 along with consumer confidence, while Nzd/Usd continues to pivot 0.7000. Elsewhere, the Loonie continues to draw some comfort from comparative stability in WTI crude and is holding above 1.2550.

CHF/JPY - The low yielders remain weak against the backdrop of more pronounced US Treasury bear-steepening, with the Franc now struggling to keep its head afloat of 0.9250 and the Yen trying to arrest a decline into 111.00 with little left in the way of support aside from mid/late June and early July troughs at 110.81 and 110.97.

In commodities, WTI and Brent are currently in proximity to the unchanged mark on the session, having given up the European morning’s initial modest gains, which took the benchmarks to highs of USD 68.78/bbl and USD 71.17/bbl respectively. Newsflow throughout the APAC session and this morning has been very minimal and not changed the dial for the complex at any point; for reference, the Private Inventories last night came in at a marginally smaller build than expected for the headline with the internals mixed and the report overlooked. Elsewhere, Iranian President Raisi has submitted his list of candidates for Parliamentary Cabinet positions which pertinently has Amir-Abdollahian as the Foreign Minister and Javad Oji as the Oil Minister. The foreign minister has historically been in charge of nuclear talks but Officials cited by the Times of Israel write that at this stage it is unclear if this will continue to be the case or if responsibility will transition to the National Security Council, for instance. Moving to metals, where it is once again a relatively uneventful session for spot gold and silver which haven’t been too afflicted by either the firmer USD or elevated yields thus far; currently, posting gains of 0.3% on the session. For the session ahead the US CPI print is the next point to watch for the metal and a preview of the release is available within the US Premarket Themes post. Elsewhere, copper prices are a touch softer in respite from the modest gains seen at this time yesterday as attention around the metal centres on negotiations around BHPs Escondida, Chile mine; which, thus far, have not resulted in a deal and as such government-mediated talks are ongoing. As a reminder, in the event a deal is not attained then the Union would be able to instigate strike action.

US Event Calendar

8:30am: July CPI MoM, est. 0.5%, prior 0.9%; YoY, est. 5.3%, prior 5.4%;

8:30am: July CPI Ex Food and Energy MoM, est. 0.4%, prior 0.9%; YoY, est. 4.3%, prior 4.5%

8:30am: July Real Avg Weekly Earnings YoY, prior -1.4%, revised -1.0%

2pm: July Monthly Budget Statement, est. -$300b, prior -$63b

DB's Jim Reid concludes the overnight wrap

Three days to go before my holidays. We are staying at home as quarantine rules (that have now been lifted) made us change our plans. Instead we are going to various theme parks in the south of England amongst other things. I can’t think of a worse way of relaxing and unwinding though, so expect me frazzled on my return. In preparation, today my wife is in training for the two weeks ahead and is taking the kids to “Diggerworld”. Their faces when I showed them a video of what goes on there last night suggests that watching today’s big US CPI print will be a far quieter affair.

So today should be a big day, however the evidence from recent big CPI prints is that the market doesn’t believe it’s sustainable so it might take a lot to shake things up today. For the record our US economists are expecting a +0.5% m/m increase in headline CPI and a tick down to 5.3% y/y, after last month came in at +0.9% m/m, which took the y/y reading to +5.4%. They expect a +0.4% m/m and +4.3% y/y core print after June was +0.9% m/m and +4.5% y/y. This follows three straight months of higher-than-expected headline price increases, +0.9% (+0.5% expected) in June, +0.6% (+0.5% expected) in May, and +0.8% (+0.2% expected) in April. The market saw Treasury yields move more than 5bps on the day of the last three CPI prints. US 10yr Treasury yields rose +5.2bps on last month’s release, and back in May, when the April data surprised to the upside for the first time, yields rose +7.0bps. On the other hand, yields fell -5.9bps the month in between when the data was more in-line with expectations. Yields have also fallen in the days following recent prints as markets haven’t been convinced. Let’s see if anything changes today. The breakdown will be very important so let’s see if more of the transitory inflation filters into non-covid related sectors.

As we approached the big day, equity markets were once again fairly steady yesterday, with the S&P 500 up +0.10% and the STOXX 600 rising +0.35% as cyclical stocks took the lead again. Energy stocks gained both in Europe (+0.44%) and the US (1.72%) as oil prices rebounded following their roughly 10% decline in the first handful of business days this month. Outside of energy, materials (+1.48%) and banks (+1.44%) were among the best performing industries in the S&P 500, while semiconductors (-1.36%), software (-0.76%) and tech hardware (-0.22%) were the largest laggards. In Europe, the reopening trade rebounded with travel & leisure (+1.99%) and basic resources (+1.43%) leading the overall index to a new record.

Ahead of today’s inflation data from the US, Fed Governor Mester yesterday addressed the new inflation targeting frameworks implemented by the Federal Reserve and European Central Bank. She said the new policy frameworks “were driven in part to just changes in inflation dynamics over the past two decades.” Looking forward, she noted that “understanding whether there is now a change in dynamics again in the aftermath of the pandemic is of vital interest” to central banks. Unlike Governor Bostic the day prior, she did not give any insight into tapering.

On the fiscal policy side, the US Senate passed their bipartisan infrastructure package that includes a $550 billion of new spending over the next eight years. The bill passed with a 69-30 vote margin in one of the more bipartisan bills passed in recent years, outside of the first two pandemic relief bills. The Senate will now recess as the House is set to take up the bill, though the lower chamber is on recess until September 20 currently. Senate Majority Leader Schumer quickly pivoted to the larger $3.5 trillion economic package that overhauls policies on healthcare, climate change, paid family leave, middle-class tax cuts, and higher education while increasing taxes on corporations and the wealthy to help pay for it. Schumer and Democratic leaders are expected to put that bill into a budget resolution framework that would only require 50 Senators and the Vice President’s tie-breaking vote to pass.

Whether it was the anticipation of another CPI upside surprise or in response to the infrastructure bill finally moving on, US 10yr Treasury yields rose +2.5bps to 1.349%. That was their 5th consecutive daily increase and leave rates just above of where they were the day after last month’s CPI release. The increase was driven by inflation expectations (+2.6bps) which rose to their highest levels of the month. In Europe sovereign bonds were largely unchanged with yields on 10yr German bunds (+0.3bps) and UK gilts (+0.5bps) slightly higher, while those on OATs (-0.1bps) and BTPs (-0.3bps) were the other side of unchanged.

Asian markets are mostly trading higher this morning outside of the Kospi (-0.56%) as South Korea reported a record number of daily coronavirus infections (more below). The Nikkei (+0.51%), Hang Seng (+0.21%), Shanghai Comp (+0.27%) and Asx (+0.42%) are all up. Futures on the S&P 500 are trading a touch weaker at -0.08% while yields on 10y USTs are a shade higher at 1.356%.

On the pandemic, the EU announced that it would not reinstate travel restrictions on non-essential travel from the US, which buoyed the airline industry as referenced above. However the Biden administration has kept its foreign travel restrictions largely in place, citing the high level of delta variant cases even as the US recorded over a 100k cases per day last week on average. Overnight, President Biden has urged Americans in states at risk of facing hurricanes to get vaccinated, saying the surging delta variant in those places would exacerbate any fallout from a severe storm. In terms of vaccinations, the UK has now inoculated 75% of adults with two doses. Lastly Asian economies are continuing to grapple with the increasing spread of the delta variant in the region. The outbreak in China is continuing to grow slowly, with another 111 cases reported yesterday. South Korea also reported a record 2,219 daily infections yesterday while Australia’s second largest city, Melbourne, has extended its lockdown by another week.

Back to data and in the US, the NFIB Small Business Optimism index was slightly lower than expected at 99.7 (102.0 expected) and down from last month’s 102.5 reading, with a record number of respondents saying they had trouble filling positions and planned to raise compensation in the next three months, tying into what we saw with the JOLTS data the day before. Preliminary Q2 Nonfarm productivity also missed to the downside, coming in at 2.3% (3.2% expected) after Q1 was revised down to 4.3% from 5.4%.

To the day ahead now, outside of the aforementioned US CPI July data, we will get similar prints from Italy and Germany later today. US data will also include July’s monthly budget statement and weekly MBA mortgage applications. There will be more fed speakers today as Governor Bostic speaks for the second time this week and we will also hear from Governors Logan and George. The vast majority of earnings are currently behind us but there are some large cap names reporting today, including NIO, Prudential, EBAY, SMC Corp, Vestas, and Commonwealth Bank of Australia.

"I Can't Even Save": Americans Are Getting Absolutely Crushed Under Enormous Debt Load

While Joe Biden insists that Americans are doing great - suggesting in his State of the Union Address last week that "our economy is the envy of the world," Americans are being absolutely crushed by inflation (which the Biden admin blames on 'shrinkflation' and 'corporate greed'), andof course - crippling debt.

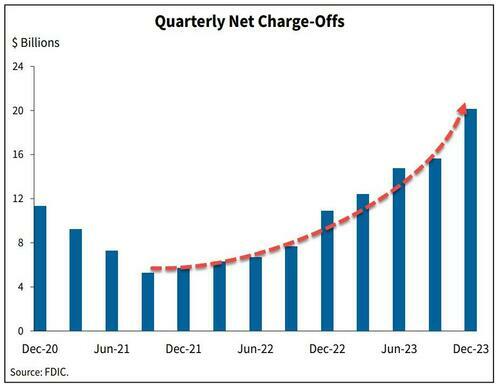

The signs are obvious. Last week we noted that banks' charge-offs are accelerating, and are now above pre-pandemic levels.

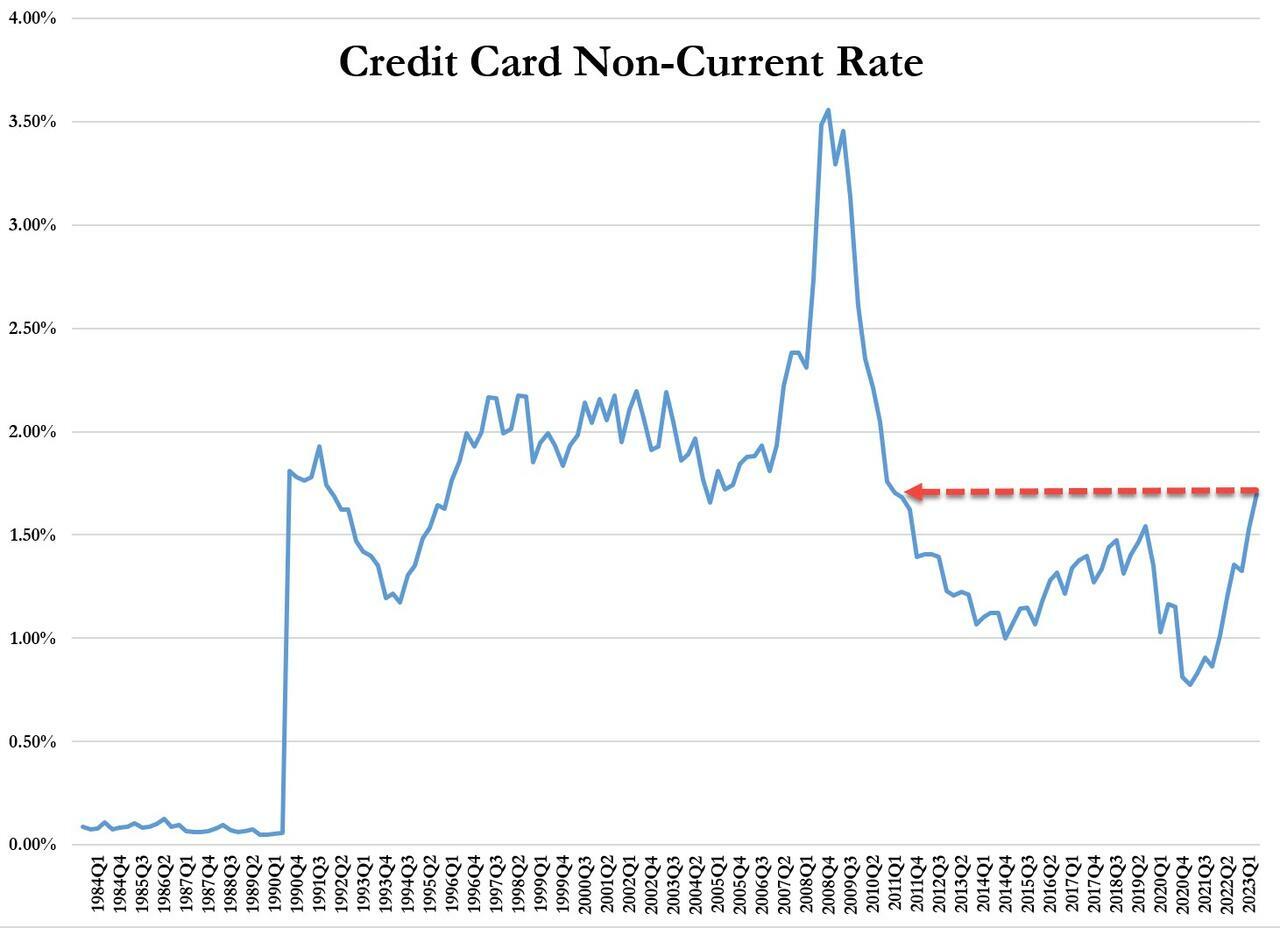

...and leading this increase are credit card loans - with delinquencies that haven't been this high since Q3 2011.

On top of that, while credit cards and nonfarm, nonresidential commercial real estate loans drove the quarterly increase in the noncurrent rate, residential mortgages drove the quarterly increase in the share of loans 30-89 days past due.

And while Biden and crew can spin all they want, an average of polls from RealClear Politics shows that just 40% of people approve of Biden's handling of the economy.

Crushed

On Friday, Bloomberg dug deeper into the effects of Biden's "envious" economy on Americans - specifically, how massive debt loads (credit cards and auto loans especially) are absolutely crushing people.

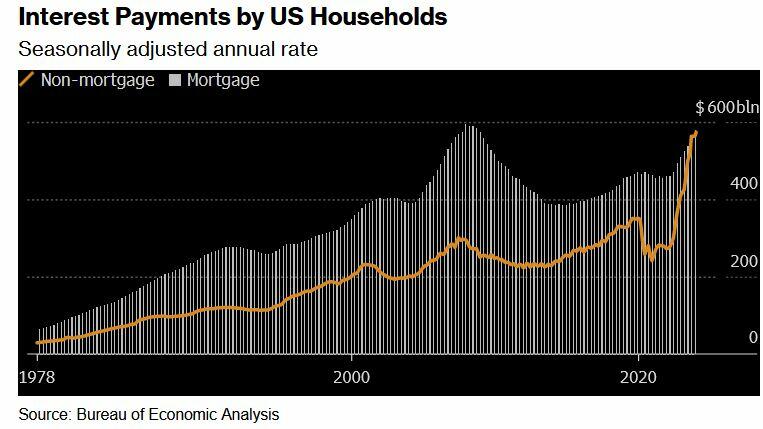

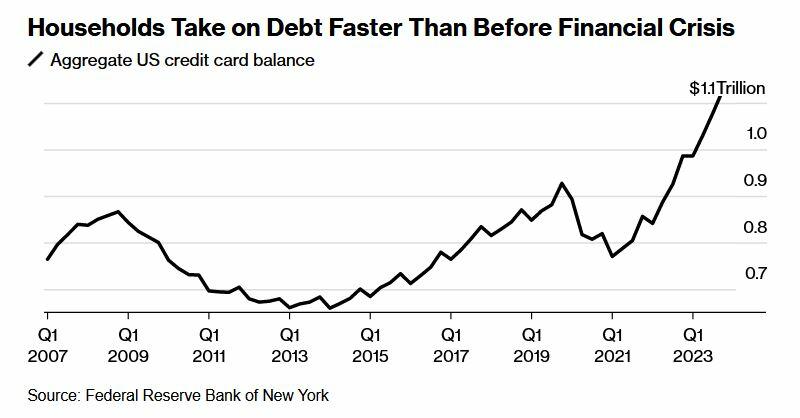

Two years after the Federal Reserve began hiking interest rates to tame prices, delinquency rates on credit cards and auto loans are the highest in more than a decade. For the first time on record, interest payments on those and other non-mortgage debts are as big a financial burden for US households as mortgage interest payments.

According to the report, this presents a difficult reality for millions of consumers who drive the US economy - "The era of high borrowing costs — however necessary to slow price increases — has a sting of its own that many families may feel for years to come, especially the ones that haven’t locked in cheap home loans."

The Fed, meanwhile, doesn't appear poised to cut rates until later this year.

According to a February paper from IMF and Harvard, the recent high cost of borrowing - something which isn't reflected in inflation figures, is at the heart of lackluster consumer sentiment despite inflation having moderated and a job market which has recovered (thanks to job gains almost entirely enjoyed by immigrants).

In short, the debt burden has made life under President Biden a constant struggle throughout America.

"I’m making the most money I've ever made, and I’m still living paycheck to paycheck," 40-year-old Denver resident Nikki Cimino told Bloomberg. Cimino is carrying a monthly mortgage of $1,650, and has $4,000 in credit card debt following a 2020 divorce.

"There's this wild disconnect between what people are experiencing and what economists are experiencing."

CBS: Do you attribute the inflation crisis to the pandemic or Biden?

WISCONSIN VOTER: "It's been YEARS now since the pandemic — I'm not buying that anymore. At first I did; I'm not buying that anymore because yogurt is STILL going up in price!" pic.twitter.com/apahb65scB

What's more, according to Wells Fargo, families have taken on debt at a comparatively fast rate - no doubt to sustain the same lifestyle as low rates and pandemic-era stimmies provided. In fact, it only took four years for households to set a record new debt level after paying down borrowings in 2021 when interest rates were near zero.

Meanwhile, that increased debt load is exacerbated by credit card interest rates that have climbed to a record 22%, according to the Fed.

[P]art of the reason some Americans were able to take on a substantial load of non-mortgage debt is because they’d locked in home loans at ultra-low rates, leaving room on their balance sheets for other types of borrowing. The effective rate of interest on US mortgage debt was just 3.8% at the end of last year.

Yet the loans and interest payments can be a significant strain that shapes families’ spending choices. -Bloomberg

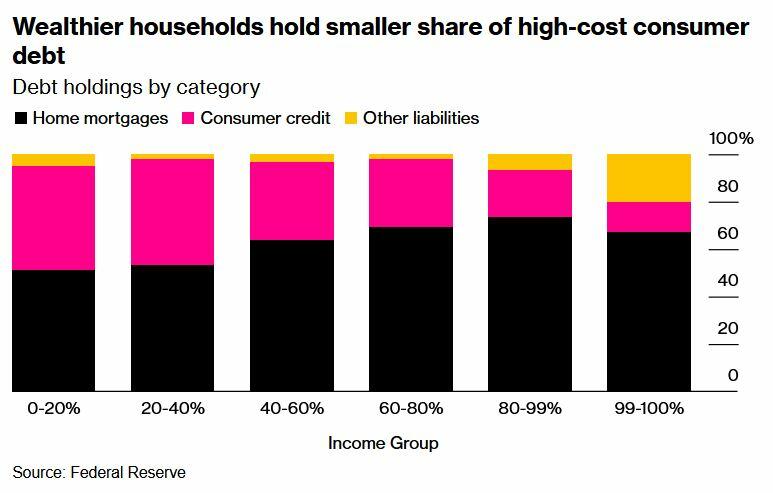

And of course, the highest-interest debt (credit cards) is hurting lower-income households the most, as tends to be the case.

The lowest earners also understandably had the biggest increase in credit card delinquencies.

"Many consumers are levered to the hilt — maxed out on debt and barely keeping their heads above water," Allan Schweitzer, a portfolio manager at credit-focused investment firm Beach Point Capital Management told Bloomberg. "They can dog paddle, if you will, but any uptick in unemployment or worsening of the economy could drive a pretty significant spike in defaults."

"We had more money when Trump was president," said Denise Nierzwicki, 69. She and her 72-year-old husband Paul have around $20,000 in debt spread across multiple cards - all of which have interest rates above 20%.

During the pandemic, Denise lost her job and a business deal for a bar they owned in their hometown of Lexington, Kentucky. While they applied for Social Security to ease the pain, Denise is now working 50 hours a week at a restaurant. Despite this, they're barely scraping enough money together to service their debt.

The couple blames Biden for what they see as a gloomy economy and plans to vote for the Republican candidate in November. Denise routinely voted for Democrats up until about 2010, when she grew dissatisfied with Barack Obama’s economic stances, she said. Now, she supports Donald Trump because he lowered taxes and because of his policies on immigration. -Bloomberg

Meanwhile there's student loans - which are not able to be discharged in bankruptcy.

"I can't even save, I don't have a savings account," said 29-year-old in Columbus, Ohio resident Brittany Walling - who has around $80,000 in federal student loans, $20,000 in private debt from her undergraduate and graduate degrees, and $6,000 in credit card debt she accumulated over a six-month stretch in 2022 while she was unemployed.

"I just know that a lot of people are struggling, and things need to change," she told the outlet.

The only silver lining of note, according to Bloomberg, is that broad wage gains resulting in large paychecks has made it easier for people to throw money at credit card bills.

Yet, according to Wells Fargo economist Shannon Grein, "As rates rose in 2023, we avoided a slowdown due to spending that was very much tied to easy access to credit ... Now, credit has become harder to come by and more expensive."

According to Grein, the change has posed "a significant headwind to consumption."

Then there's the election

"Maybe the Fed is done hiking, but as long as rates stay on hold, you still have a passive tightening effect flowing down to the consumer and being exerted on the economy," she continued. "Those household dynamics are going to be a factor in the election this year."

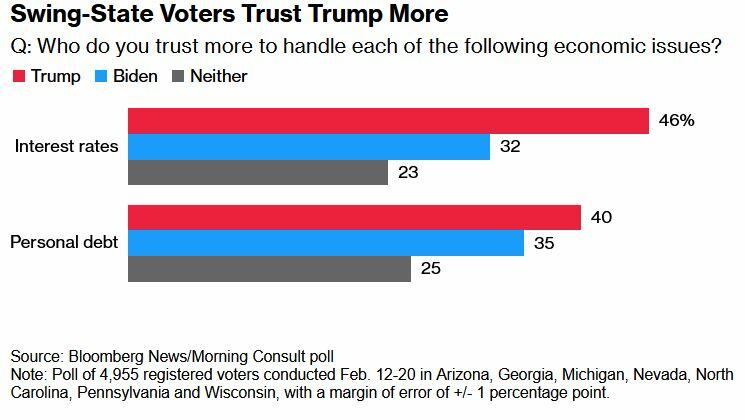

Meanwhile, swing-state voters in a February Bloomberg/Morning Consult poll said they trust Trump more than Biden on interest rates and personal debt.

Reverberations

These 'headwinds' have M3 Partners' Moshin Meghji concerned.

"Any tightening there immediately hits the top line of companies," he said, noting that for heavily indebted companies that took on debt during years of easy borrowing, "there's no easy fix."

Sylvester researchers, collaborators call for greater investment in bereavement care

MIAMI, FLORIDA (March 15, 2024) – The public health toll from bereavement is well-documented in the medical literature, with bereaved persons at greater…

MIAMI, FLORIDA (March 15, 2024) – The public health toll from bereavement is well-documented in the medical literature, with bereaved persons at greater risk for many adverse outcomes, including mental health challenges, decreased quality of life, health care neglect, cancer, heart disease, suicide, and death. Now, in a paper published in The Lancet Public Health, researchers sound a clarion call for greater investment, at both the community and institutional level, in establishing support for grief-related suffering.

Credit: Photo courtesy of Memorial Sloan Kettering Comprehensive Cancer Center

MIAMI, FLORIDA (March 15, 2024) – The public health toll from bereavement is well-documented in the medical literature, with bereaved persons at greater risk for many adverse outcomes, including mental health challenges, decreased quality of life, health care neglect, cancer, heart disease, suicide, and death. Now, in a paper published in The Lancet Public Health, researchers sound a clarion call for greater investment, at both the community and institutional level, in establishing support for grief-related suffering.

The authors emphasized that increased mortality worldwide caused by the COVID-19 pandemic, suicide, drug overdose, homicide, armed conflict, and terrorism have accelerated the urgency for national- and global-level frameworks to strengthen the provision of sustainable and accessible bereavement care. Unfortunately, current national and global investment in bereavement support services is woefully inadequate to address this growing public health crisis, said researchers with Sylvester Comprehensive Cancer Center at the University of Miami Miller School of Medicine and collaborating organizations.

They proposed a model for transitional care that involves firmly establishing bereavement support services within healthcare organizations to ensure continuity of family-centered care while bolstering community-based support through development of “compassionate communities” and a grief-informed workforce. The model highlights the responsibility of the health system to build bridges to the community that can help grievers feel held as they transition.

The Center for the Advancement of Bereavement Care at Sylvester is advocating for precisely this model of transitional care. Wendy G. Lichtenthal, PhD, FT, FAPOS, who is Founding Director of the new Center and associate professor of public health sciences at the Miller School, noted, “We need a paradigm shift in how healthcare professionals, institutions, and systems view bereavement care. Sylvester is leading the way by investing in the establishment of this Center, which is the first to focus on bringing the transitional bereavement care model to life.”

What further distinguishes the Center is its roots in bereavement science, advancing care approaches that are both grounded in research and community-engaged.

The authors focused on palliative care, which strives to provide a holistic approach to minimize suffering for seriously ill patients and their families, as one area where improvements are critically needed. They referenced groundbreaking reports of the Lancet Commissions on the value of global access to palliative care and pain relief that highlighted the “undeniable need for improved bereavement care delivery infrastructure.” One of those reports acknowledged that bereavement has been overlooked and called for reprioritizing social determinants of death, dying, and grief.

“Palliative care should culminate with bereavement care, both in theory and in practice,” explained Lichtenthal, who is the article’s corresponding author. “Yet, bereavement care often is under-resourced and beset with access inequities.”

Transitional bereavement care model

So, how do health systems and communities prioritize bereavement services to ensure that no bereaved individual goes without needed support? The transitional bereavement care model offers a roadmap.

“We must reposition bereavement care from an afterthought to a public health priority. Transitional bereavement care is necessary to bridge the gap in offerings between healthcare organizations and community-based bereavement services,” Lichtenthal said. “Our model calls for health systems to shore up the quality and availability of their offerings, but also recognizes that resources for bereavement care within a given healthcare institution are finite, emphasizing the need to help build communities’ capacity to support grievers.”

Key to the model, she added, is the bolstering of community-based support through development of “compassionate communities” and “upskilling” of professional services to assist those with more substantial bereavement-support needs.

The model contains these pillars:

Preventive bereavement care –healthcare teams engage in bereavement-conscious practices, and compassionate communities are mindful of the emotional and practical needs of dying patients’ families.

Ownership of bereavement care – institutions provide bereavement education for staff, risk screenings for families, outreach and counseling or grief support. Communities establish bereavement centers and “champions” to provide bereavement care at workplaces, schools, places of worship or care facilities.

Resource allocation for bereavement care – dedicated personnel offer universal outreach, and bereaved stakeholders provide input to identify community barriers and needed resources.

Upskilling of support providers – Bereavement education is integrated into training programs for health professionals, and institutions offer dedicated grief specialists. Communities have trained, accessible bereavement specialists who provide support and are educated in how to best support bereaved individuals, increasing their grief literacy.

Evidence-based care – bereavement care is evidence-based and features effective grief assessments, interventions, and training programs. Compassionate communities remain mindful of bereavement care needs.

Lichtenthal said the new Center will strive to materialize these pillars and aims to serve as a global model for other health organizations. She hopes the paper’s recommendations “will cultivate a bereavement-conscious and grief-informed workforce as well as grief-literate, compassionate communities and health systems that prioritize bereavement as a vital part of ethical healthcare.”

“This paper is calling for healthcare institutions to respond to their duty to care for the family beyond patients’ deaths. By investing in the creation of the Center for the Advancement of Bereavement Care, Sylvester is answering this call,” Lichtenthal said.

Follow @SylvesterCancer on X for the latest news on Sylvester’s research and care.

# # #

Article Title: Investing in bereavement care as a public health priority

DOI: 10.1016/S2468-2667(24)00030-6

Authors: The complete list of authors is included in the paper.

Funding: The authors received funding from the National Cancer Institute (P30 CA240139 Nimer) and P30 CA008748 Vickers).

Disclosures: The authors declared no competing interests.

# # #

Journal

The Lancet Public Health

DOI

10.1016/S2468-2667(24)00030-6

Article Title

Investing in bereavement care as a public health priority

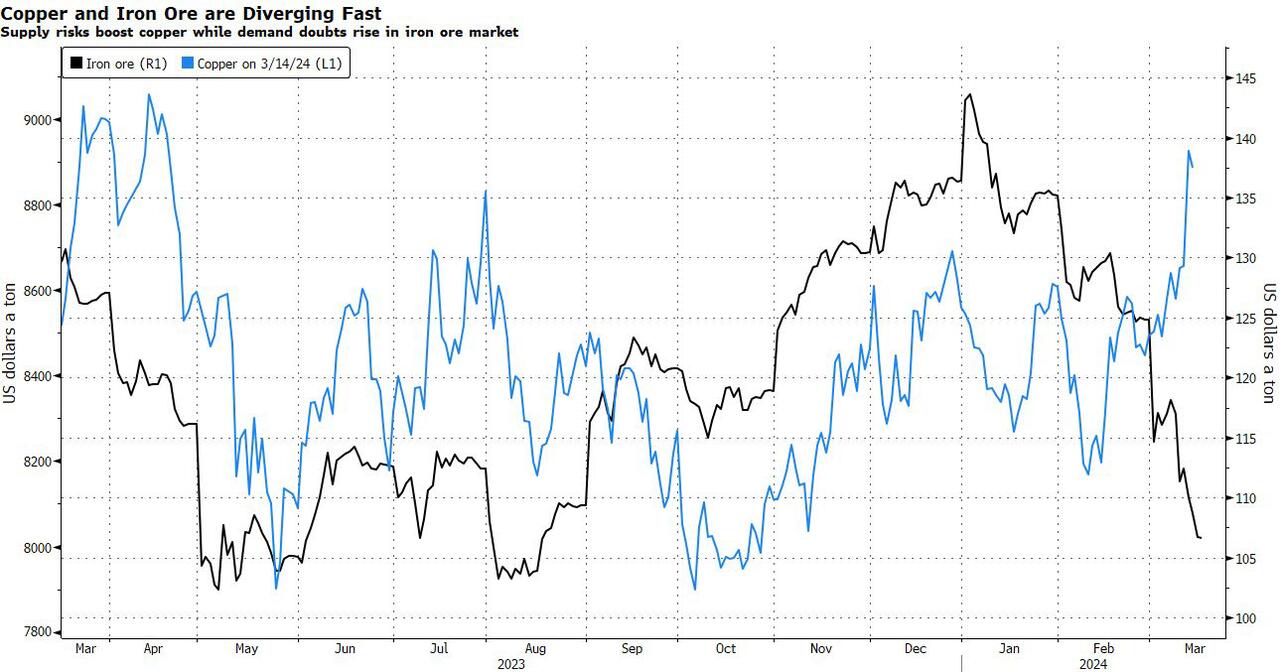

Copper Soars, Iron Ore Tumbles As Goldman Says "Copper's Time Is Now"

After languishing for the past two years in a tight range despite recurring speculation about declining global supply, copper has finally broken out, surging to the highest price in the past year, just shy of $9,000 a ton as supply cuts hit the market; At the same time the price of the world's "other" most important mined commodity has diverged, as iron ore has tumbled amid growing demand headwinds out of China's comatose housing sector where not even ghost cities are being built any more.

Copper surged almost 5% this week, ending a months-long spell of inertia, as investors focused on risks to supply at various global mines and smelters. As Bloomberg adds, traders also warmed to the idea that the worst of a global downturn is in the past, particularly for metals like copper that are increasingly used in electric vehicles and renewables.

Yet the commodity crash of recent years is hardly over, as signs of the headwinds in traditional industrial sectors are still all too obvious in the iron ore market, where futures fell below $100 a ton for the first time in seven months on Friday as investors bet that China’s years-long property crisis will run through 2024, keeping a lid on demand.

Indeed, while the mood surrounding copper has turned almost euphoric, sentiment on iron ore has soured since the conclusion of the latest National People’s Congress in Beijing, where the CCP set a 5% goal for economic growth, but offered few new measures that would boost infrastructure or other construction-intensive sectors.

As a result, the main steelmaking ingredient has shed more than 30% since early January as hopes of a meaningful revival in construction activity faded. Loss-making steel mills are buying less ore, and stockpiles are piling up at Chinese ports. The latest drop will embolden those who believe that the effects of President Xi Jinping’s property crackdown still have significant room to run, and that last year’s rally in iron ore may have been a false dawn.

Meanwhile, as Bloomberg notes, on Friday there were fresh signs that weakness in China’s industrial economy is hitting the copper market too, with stockpiles tracked by the Shanghai Futures Exchange surging to the highest level since the early days of the pandemic. The hope is that headwinds in traditional industrial areas will be offset by an ongoing surge in usage in electric vehicles and renewables.

And while industrial conditions in Europe and the US also look soft, there’s growing optimism about copper usage in India, where rising investment has helped fuel blowout growth rates of more than 8% — making it the fastest-growing major economy.

In any case, with the demand side of the equation still questionable, the main catalyst behind copper’s powerful rally is an unexpected tightening in global mine supplies, driven mainly by last year’s closure of a giant mine in Panama (discussed here), but there are also growing worries about output in Zambia, which is facing an El Niño-induced power crisis.

On Wednesday, copper prices jumped on huge volumes after smelters in China held a crisis meeting on how to cope with a sharp drop in processing fees following disruptions to supplies of mined ore. The group stopped short of coordinated production cuts, but pledged to re-arrange maintenance work, reduce runs and delay the startup of new projects. In the coming weeks investors will be watching Shanghai exchange inventories closely to gauge both the strength of demand and the extent of any capacity curtailments.

“The increase in SHFE stockpiles has been bigger than we’d anticipated, but we expect to see them coming down over the next few weeks,” Colin Hamilton, managing director for commodities research at BMO Capital Markets, said by phone. “If the pace of the inventory builds doesn’t start to slow, investors will start to question whether smelters are actually cutting and whether the impact of weak construction activity is starting to weigh more heavily on the market.”

* * *

Few have been as happy with the recent surge in copper prices as Goldman's commodity team, where copper has long been a preferred trade (even if it may have cost the former team head Jeff Currie his job due to his unbridled enthusiasm for copper in the past two years which saw many hedge fund clients suffer major losses).

As Goldman's Nicholas Snowdon writes in a note titled "Copper's time is now" (available to pro subscribers in the usual place)...

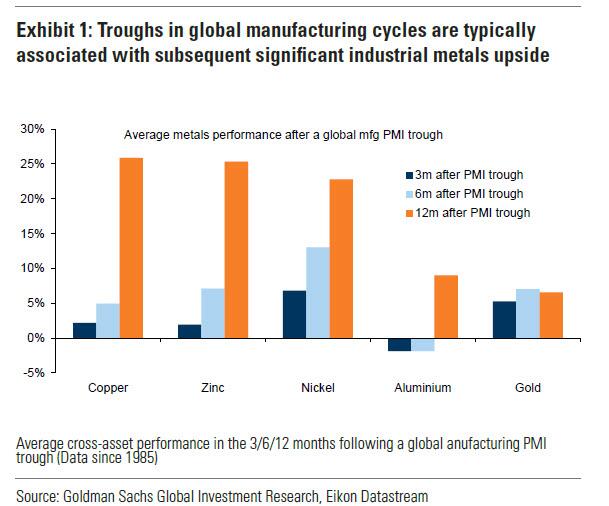

... there has been a "turn in the industrial cycle." Specifically according to the Goldman analyst, after a prolonged downturn, "incremental evidence now points to a bottoming out in the industrial cycle, with the global manufacturing PMI in expansion for the first time since September 2022." As a result, Goldman now expects copper to rise to $10,000/t by year-end and then $12,000/t by end of Q1-25.’

Here are the details:

Previous inflexions in global manufacturing cycles have been associated with subsequent sustained industrial metals upside, with copper and aluminium rising on average 25% and 9% over the next 12 months. Whilst seasonal surpluses have so far limited a tightening alignment at a micro level, we expect deficit inflexions to play out from quarter end, particularly for metals with severe supply binds. Supplemented by the influence of anticipated Fed easing ahead in a non-recessionary growth setting, another historically positive performance factor for metals, this should support further upside ahead with copper the headline act in this regard.

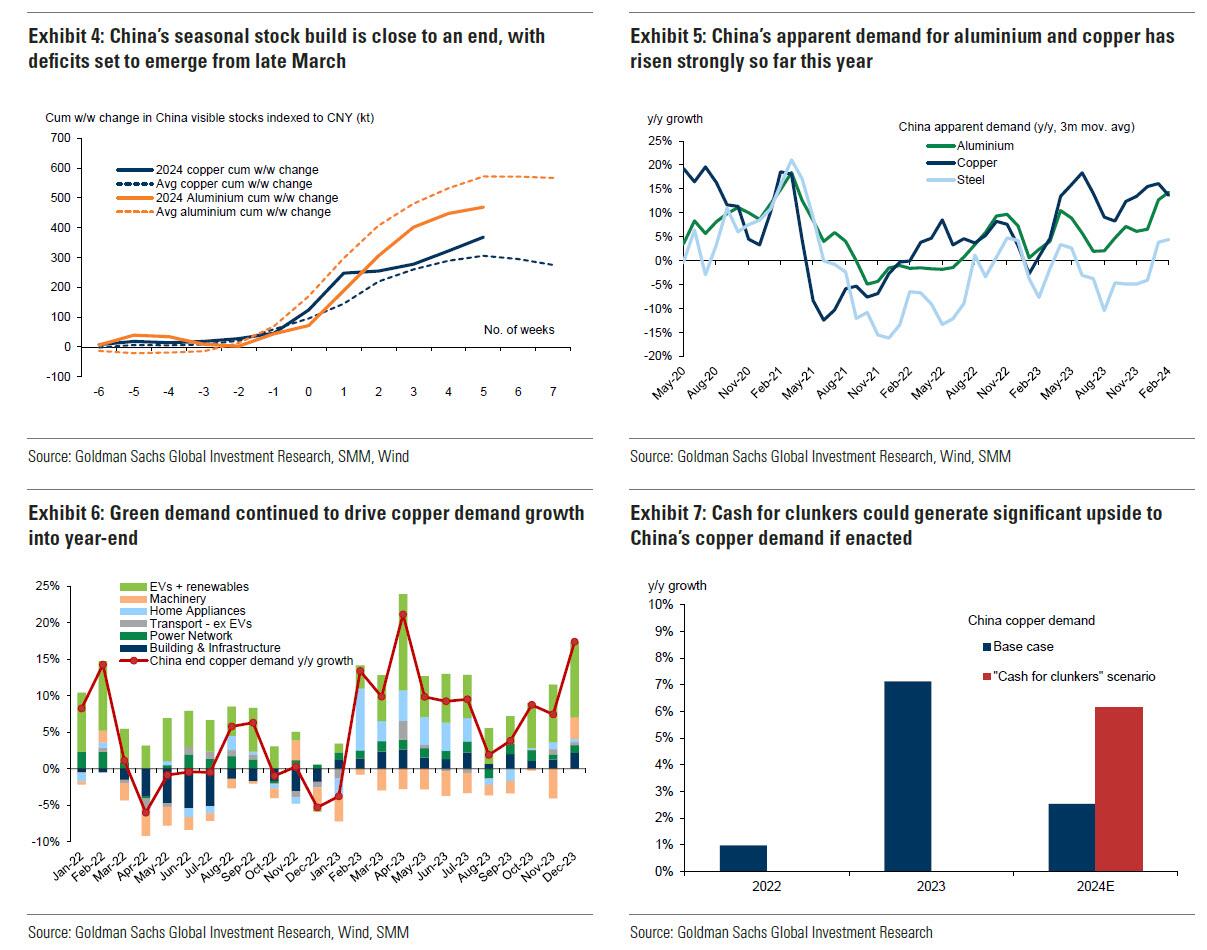

Goldman then turns to what it calls China's "green policy put":

Much of the recent focus on the “Two Sessions” event centred on the lack of significant broad stimulus, and in particular the limited property support. In our view it would be wrong – just as in 2022 and 2023 – to assume that this will result in weak onshore metals demand. Beijing’s emphasis on rapid growth in the metals intensive green economy, as an offset to property declines, continues to act as a policy put for green metals demand. After last year’s strong trends, evidence year-to-date is again supportive with aluminium and copper apparent demand rising 17% and 12% y/y respectively. Moreover, the potential for a ‘cash for clunkers’ initiative could provide meaningful right tail risk to that healthy demand base case. Yet there are also clear metal losers in this divergent policy setting, with ongoing pressure on property related steel demand generating recent sharp iron ore downside.

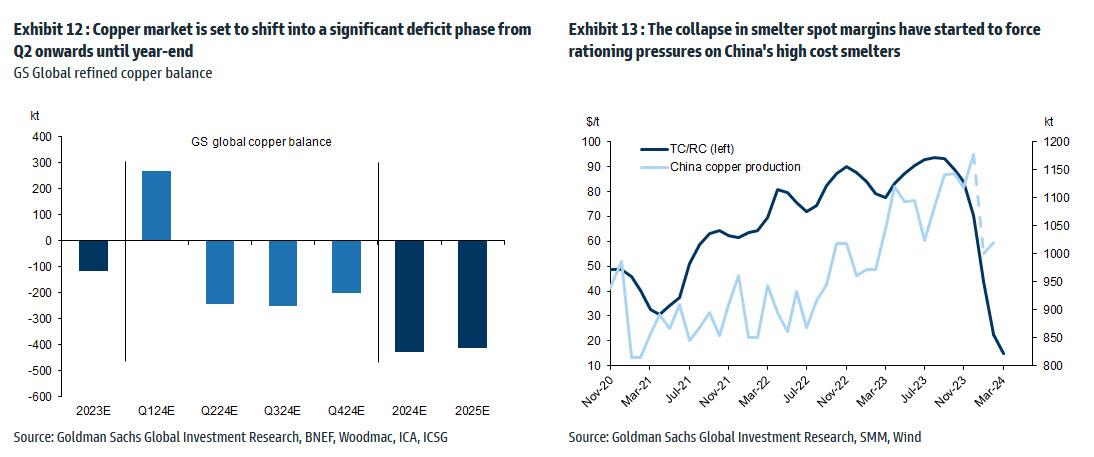

Meanwhile, Snowdon believes that the driver behind Goldman's long-running bullish view on copper - a global supply shock - continues:

Copper’s supply shock progresses. The metal with most significant upside potential is copper, in our view. The supply shock which began with aggressive concentrate destocking and then sharp mine supply downgrades last year, has now advanced to an increasing bind on metal production, as reflected in this week's China smelter supply rationing signal. With continued positive momentum in China's copper demand, a healthy refined import trend should generate a substantial ex-China refined deficit this year. With LME stocks having halved from Q4 peak, China’s imminent seasonal demand inflection should accelerate a path into extreme tightness by H2. Structural supply underinvestment, best reflected in peak mine supply we expect next year, implies that demand destruction will need to be the persistent solver on scarcity, an effect requiring substantially higher pricing than current, in our view. In this context, we maintain our view that the copper price will surge into next year (GSe 2025 $15,000/t average), expecting copper to rise to $10,000/t by year-end and then $12,000/t by end of Q1-25’

Another reason why Goldman is doubling down on its bullish copper outlook: gold.

The sharp rally in gold price since the beginning of March has ended the period of consolidation that had been present since late December. Whilst the initial catalyst for the break higher came from a (gold) supportive turn in US data and real rates, the move has been significantly amplified by short term systematic buying, which suggests less sticky upside. In this context, we expect gold to consolidate for now, with our economists near term view on rates and the dollar suggesting limited near-term catalysts for further upside momentum. Yet, a substantive retracement lower will also likely be limited by resilience in physical buying channels. Nonetheless, in the midterm we continue to hold a constructive view on gold underpinned by persistent strength in EM demand as well as eventual Fed easing, which should crucially reactivate the largely for now dormant ETF buying channel. In this context, we increase our average gold price forecast for 2024 from $2,090/toz to $2,180/toz, targeting a move to $2,300/toz by year-end.

We use cookies on our website to give you the most relevant experience by remembering your preferences and repeat visits. By clicking “Accept”, you consent to the use of ALL the cookies.

This website uses cookies to improve your experience while you navigate through the website. Out of these, the cookies that are categorized as necessary are stored on your browser as they are essential for the working of basic functionalities of the website. We also use third-party cookies that help us analyze and understand how you use this website. These cookies will be stored in your browser only with your consent. You also have the option to opt-out of these cookies. But opting out of some of these cookies may affect your browsing experience.

Necessary cookies are absolutely essential for the website to function properly. These cookies ensure basic functionalities and security features of the website, anonymously.

Cookie

Duration

Description

cookielawinfo-checbox-analytics

11 months

This cookie is set by GDPR Cookie Consent plugin. The cookie is used to store the user consent for the cookies in the category "Analytics".

cookielawinfo-checbox-functional

11 months

The cookie is set by GDPR cookie consent to record the user consent for the cookies in the category "Functional".

cookielawinfo-checbox-others

11 months

This cookie is set by GDPR Cookie Consent plugin. The cookie is used to store the user consent for the cookies in the category "Other.

cookielawinfo-checkbox-necessary

11 months

This cookie is set by GDPR Cookie Consent plugin. The cookies is used to store the user consent for the cookies in the category "Necessary".

cookielawinfo-checkbox-performance

11 months

This cookie is set by GDPR Cookie Consent plugin. The cookie is used to store the user consent for the cookies in the category "Performance".

viewed_cookie_policy

11 months

The cookie is set by the GDPR Cookie Consent plugin and is used to store whether or not user has consented to the use of cookies. It does not store any personal data.

Functional cookies help to perform certain functionalities like sharing the content of the website on social media platforms, collect feedbacks, and other third-party features.

Performance cookies are used to understand and analyze the key performance indexes of the website which helps in delivering a better user experience for the visitors.

Analytical cookies are used to understand how visitors interact with the website. These cookies help provide information on metrics the number of visitors, bounce rate, traffic source, etc.

Advertisement cookies are used to provide visitors with relevant ads and marketing campaigns. These cookies track visitors across websites and collect information to provide customized ads.

{kind=link}

{kind=link}

{kind=link}