Evermore Global Advisor: Opportunity In Europe

Evermore Global Advisor commentary for the month of October 2020, discussing the EU recovery plan. Q4 2020 hedge fund letters, conferences and more Opportunity Highlights We believe the European business climate over the next five years will be unlike…

Share this:

Evermore Global Advisor commentary for the month of October 2020, discussing the EU recovery plan.

Q4 2020 hedge fund letters, conferences and more

Opportunity Highlights

- We believe the European business climate over the next five years will be unlike any period investors have witnessed in our lifetimes.

- The COVID-19 pandemic is evolving into a game changing catalyst for Europe-focused investors.

- The European Union (“EU”) and European Commission (“EC”) stimulus packages, coupled with the explosion of American-style entrepreneurs, family-controlled businesses and aggressive corporate leadership teams will be, in our view, a driving force behind significant value creation for investors in the years ahead.

- Special situations, that we believe should do well regardless of macro inputs, are expected to benefit from the underpinning of these transformative and unprecedented plans and are positioned to deliver potentially exceptional results. The micro (bottom up) is now coinciding with what we believe are improving macro (big picture, top down) tailwinds.

- We highlight opportunities in several businesses and sectors in the pages to follow.

Setting The Table

For years, we have maintained that while the EU and EC building process was likely to be worse than a messy sausage making process, when all was said and done, together, Europe should have a feast at the end.

Many investors believe that the opportunity for compelling investment returns in Europe has been a tomorrow story for many years now. This negative sentiment is pervasive among many market participants with whom we speak these days. Throughout our investing careers, there have been several long stretches where Europe has delivered exceptional returns. There have also been other periods that were more like false starts. While the U.S markets have substantially outperformed Europe since the 2008/2009 financial crisis, we believe that the COVID-19 pandemic is evolving into the catalyst that knocks over the first phase of many dominoes to fall there over the coming years.

This memo will review some highlights from the EC and EU stimulus packages that are game changers for the continent. We will discuss how the stimulus plans, when coupled with the explosion of creative entrepreneurs, aggressive corporate restructurings and leadership from family-controlled businesses, should allow some businesses to strategically change and perhaps leapfrog their competition.

We believe that the real opportunity in Europe is not to buy Europe, but rather, to take advantage of special situations in Europe including:

- A growing wave of entrepreneurialism, especially in Sweden, Norway, Denmark, Germany and France

- De-conglomerating of multi-industry holding companies into singularly focused businesses via break-ups, spin-offs and restructurings

- Re-conglomerating, or integration by acquisition, to create powerhouse groups in various industries, including, media, industrial and renewables

Investors do not seem to fully understand what is happening, especially with government and corporate stimulus plans really beginning to be implemented as we enter 2021. In Europe, the shift from merely “talking” to actually “doing” is underway. It is real, changes are accelerating, and we believe they will yield a multi-year opportunity for investors.

To set the table, we believe that special situations will benefit from the underpinning of these transformative and unprecedented plans and are positioned to deliver potentially exceptional results.

The Influences That Inform An Investor Are Vital

During times of crisis, we believe it is important to step back and think about what information is useful and trustworthy as we seek to guide and inform our path ahead. For us, listening to leadership (governmental or corporate) is invaluable. Much more so than headlines or the rhetoric from media.

We have read extensively on the New Generation EU Recovery Plan and stimulus, and we have formed some strong opinions as it relates to future investment opportunities in Europe. It is our conclusion that the EU’s COVID-19 response is the biggest-ever effort of cross-border solidarity and sends a strong signal of internal cohesion.

In recent years, the European Union has had its share of loud controversies that ended in somewhat complex but workable compromises. This is part of the game, but as we look at the path ahead for investors, we believe the European business climate over the next five years will be unlike any investors have witnessed in their lifetimes.

We begin with a review of the EU’s Official Recovery Plan and underscore our perspectives.

Importance Of Having A Plan

The COVID-19 pandemic has seen a clear need for massive investment at scale and speed, and at both public and private levels.

- If left to individual countries alone, the recovery would likely be incomplete, uneven and unfair.

- Jointly tackling this crisis will help to drive Europe’s recovery.

- Ultimate outcome will reaffirm the interdependence of European economies and the importance of a fully functioning Single Market.

- Human tragedy element is real.

- Europe must try to ensure that what started as a health pandemic, and became an economic emergency, does not become an all-out social crisis.

Economic Priorities

The economic impact of the crisis will differ greatly between different parts of the union. Businesses providing client-facing services, or relying on crowded workplaces and customer areas, are most affected. The various funding programs and tools are outlined below:

- Solvency Support Instrument: initial €30 billion / up to €300 billion (target)

- Provides support to previously healthy companies now at risk from economic shutdown in sectors, regions and countries most affected.

- Support to mitigate Unemployment Risks in an Emergency (“SURE”): €100 billion

- Temporary €100 billion pool to support people to stay employed.

- Primary use is to help workers keep their income and ensure businesses can stay afloat and retain staff.

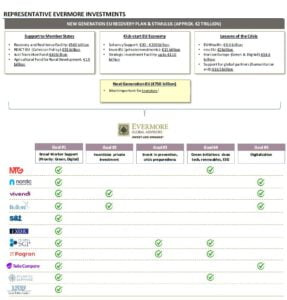

- Next Generation EU: €750 billion

- Most important for investors is the €750 billion euro recovery instrument.

- Accelerates two primary European agendas - Green/ESG and Digital Transitions. These priorities will help to strengthen Europe’s competitiveness, resilience and position as a global player.

- EU will try to spend the recovery fund money fast, by its own standards. 70% of the grants committed in 2021 and 2022; remainder in 2023.

- Positive development for businesses in research, engineering, manufacturing, assembly and servicing. These are businesses in many different parts of Europe.

- Facilitate businesses to become more competitive and focus on what they do best.

How Will They Invest The Money?

First, and foremost, there is a commitment to full transparency and democratic accountability.

- Goal #1: Priority given to workers’ support broadly and the larger green and digitalization agendas. Expected recipients of grants include: small- and mid-cap businesses of all types, but sectors like health systems, industrials, pharmaceuticals, chemicals, down to tourism and culture.

- Goal #2: Incentivize private investment. Renovation Wave will focus on creating jobs in construction, renovation and other labor-intensive industries.

- Goal #3: EU4Health - invest in prevention, crisis preparedness, the procurement of vital medicines and equipment, as well as improving long-term health outcomes

- Goal #4: European Green Deal is Europe’s growth strategy.

Public investments will respect the green oath to “do no harm". Efforts will focus on unlocking investment in clean technologies, renewable energy and value chains.

ESG is a secular tailwind for Europe.

- Goal #5: Digitalization – seeking a deeper and more digital single market; will invest in more and better connectivity.

- The rapid deployment of 5G is expected to have positive spillover effects across the whole digital society and increase Europe’s strategic autonomy.

- Stronger industrial and technological presence in strategic parts of the digital supply chain.

Invest in strategic digital capacities and capabilities, including: - o artificial intelligence, cybersecurity, secured communication, data and cloud infrastructure, 5G and 6G networks, supercomputers, quantum and blockchain.

- This will be a priority as digitalization, 1) reduces administrative burden, making it easier for companies, especially small sized companies, to use digital tools, such as e-signature, and, 2) facilitates easier access to data and reduces red tape.

EU Recovery Plan Conclusion

Taken from the EC’s Recovery Plan itself:

“This is Europe’s moment. Our willingness to act must live up to the challenges we are facing. National efforts alone will not be enough - Europe is in a unique position to be able to invest in a collective recovery and a better future for next generations.

This will need political will and courage and buy-in from all of society. This is a common good for our shared future.”

Our Take: The Case For Europe

- Before COVID-19, Europe already had the tailwinds of:

- Wider discounts than the U.S. in small and mid-caps.

- Widespread operational and financial restructurings.

- Strategic sales of non-core or struggling assets.

- Unprecedented higher rate of shareholder activism and M&A activity.

- These tailwinds are now amplified, and the timing has been accelerated.

- The EU Recovery Plan provides more reason for optimism:

- Accommodative monetary policy and a supportive growth agenda are intended to provide more catalysts for Europe.

- Should have a positive impact on the European macro outlook in the coming years.

- Help reinforce a strong cyclical EPS recovery from the trough.

- The investment case for European equities should also benefit from higher and more stable trend EPS growth as the region's stock markets transition to a superior sector mix.

- The EU Recovery Fund is a game changer for Europe.

- Should usher in a new period of stronger economic growth.

- More effective and coordinated policymaking.

- A structural reduction in the region's risk premium – real and perceived.

- The reduced tail risks in Europe should boost the case for European equities in general.

- But special situations have the potential to win more.

- The reduced tail risks in Europe should boost the case for European equities in general.

- Europe's relative EPS profile should start to improve cyclically.

- Looking out over the next 1-2 years, we see two potential catalysts to improve Europe's relative EPS profile:

- Europe's EPS has fallen much more sharply than other regions over the last nine months and the stock market recovery that has taken U.S. markets to new highs has only increased the relative valuation gaps with Europe, which has participated minimally in this massive liquidity and stimulus driven recovery.

- Hence, they should offer greater rebound potential.

- Any potential increase in corporate tax rates after the U.S. election could lead to something of a reversal of the trends in U.S. EPS.

- Europe's EPS has fallen much more sharply than other regions over the last nine months and the stock market recovery that has taken U.S. markets to new highs has only increased the relative valuation gaps with Europe, which has participated minimally in this massive liquidity and stimulus driven recovery.

- The changing face of European equities means Europe's stock market composition is becoming more growth-oriented structurally.

- Changing sector mix.

- In 2010, Banks and Energy were the two largest sectors in Europe, accounting for 25% of market cap.1

- Today, these same two sectors represent just 10% of the MSCI Europe Index 1

- Comparable to Capital Goods alone and meaningfully trailing Pharma at 14% of the index. 1

- Europe's sector mix contributed significantly to its price underperformance in 9 of the last 10 years

- Very low technology exposure compared to the US markets.

- But looking forward, this effect should be considerably reduced.

- Changing sector mix.

- Should be a better macro backdrop for Value where there is either underlying growth or significant catalysts that could expose and release the intrinsic value of select equities

- Improving economic data at the start of a new cycle.

- Reduced European political risk.

- Extreme valuation dispersion.

- Low investor positioning:

- Europe is the only region globally to have seen significant equity outflows over the last couple of years.

- All of this creates the compelling backdrop for the types of investments we seek to own: businesses that don’t require the market to rally, but rather have that as an added bonus to their potential investment outcomes

- Opportunity to be found among misunderstood and under-researched companies offering:

- Lack of natural shareholder base as result of spinoffs/breakups.

- Disparate businesses with underutilized/undermanaged assets.

- Management changes.

- Forced sellers / block transactions.

- Company or sector catalysts that investors generally do not value appropriately until realization.

- Overcapitalized balance sheets.

- Missed earnings estimates or suspended dividends.

- Conglomerates breaking up or spinning off undervalued (or hidden) assets.

- Opportunity to be found among misunderstood and under-researched companies offering:

- Hidden gem opportunity that has not been widely discussed: EU Green Deal and Taxonomy

- A key component of the future of Europe is the €1 trillion EU Green Deal

- Called the EU Taxonomy, this program aims to redirect €175 – 290 billion per year in private capital to decarbonization and many forms of Green transformation investments

- Companies that are likely to benefit the most from the package are transitioning companies, which will have access to cheap funding (Green bonds).

- These will include construction and installation companies, renewable energy companies, technical consultants and suppliers to these businesses.

- The EU Taxonomy will initially focus on sectors with the highest emissions, which implies that not all sectors and companies are covered.

- We expect the EU Taxonomy to have a substantial impact on valuations and should expand the supply of ideas to work on and likely present new Green candidates that may evolve from mispriced securities into stock market Green darlings.

- A key component of the future of Europe is the €1 trillion EU Green Deal

- Core of the EU Green Deal:

- Decarbonize the energy sector which currently accounts for ~75% of the EU’s greenhouse gas emissions.2

- Renovate and insulate buildings.

- 40% of the EU’s energy consumption is buildings.3

- Drive industrial transformation and innovation.

- European industry currently only uses 12% recycled materials.4

- Provide cleaner, cheaper private and public transportation which alone accounts for 27% of emissions in the EU currently.5

Modern Times Group (MTGB SS)

Market cap: $950 million

Sweden-based holding company that primarily consists of digital entertainment assets in Esports, online and mobile gaming, and investments in various venture capital funds that provide additional exposure to leading businesses in the Esports ecosystem. In April 2019, MTG successfully spun off its legacy Nordic broadcasting and media assets into Nordic Entertainment (NENT Group). Company has about $170 million in net cash (18% of market cap).

Catalysts on the Horizon:

- MTG is at a critical crossroad: may sell gaming assets to focus solely on Esports (or vice versa), grow both verticals, or liquidate and distribute proceeds to shareholders

- The board has been recently reconstituted with three new, highly credentialed professionals (note: David Marcus is on the nomination committee and was integral in changing the board)

- Active Ownership Capital, a Germany‐based activist investor has amassed close to an 8% stake and is now pushing for board representation to accelerate the transformation of this undervalued group of assets

- Esports and gaming sectors are going through major M&A and consolidation. MTG stands to be a key player in industry consolidation

Nordic Entertainment Group (NENTB SS)

Market cap: $2.8 billion

Nordic broadcasting and media company comprised of free TV, Pay TV, distribution platforms (satellite, IPTV, cable networks, streaming) and a leading content portfolio. Spun out of former parent, Modern Times Group, in April 2019. We believe that investors have not yet appreciated the subscriber growth in NENT’s premium streaming segment – the company successfully navigated early on the changing, competitive media landscape with the proliferation of streaming and cord cutting. Strong management led by, in our view, an underrated CEO (Anders Jensen).

Catalysts on the Horizon:

- Closing of transformative joint venture with Telenor for its satellite Pay TV business (now called Allente) should unlock substantial synergies (cash flow)

- Launched Viaplay (premium streaming) in Iceland, expanded Viaplay to the Baltics

- Continues to accelerate operational streamlining with cost cutting initiatives, including moving broadcast center from U.K. to Sweden

- Consolidation opportunities

Vivendi (VIV FP)

Market cap: $33.3 billion

Global media and telecom conglomerate based in France that controls the largest music company in the world, Universal Music Group or UMG (the largest music company in the world), Canal+ (Pay TV company) and Havas (one of the largest advertising media companies globally). Also holds stakes in Mediaset (29%), Telecom Italia (24%), Spotify (5%) and various other assets. Under the leadership of the Bollore Family, the company has been transformed from a poorly managed disparate group of telecom and media assets with substantial debt into a more focused group of media assets at its core. Vivendi sold 10% of Universal Music Group for €3 billion to Tencent, the Chinese conglomerate, which values UMG at approx. $35 billion (USD/EUR 1.172), or more than the market cap of Vivendi ($33 billion). At Vivendi’s current market cap, we are essentially getting all of the other assets at Vivendi for free at this implied valuation level. Warner Music Group (WMG), the third largest music publisher (by revenue) in the world, went public recently in early June.

6 Applying WMG’s EV/EBITDA multiple to UMG imputes a value of about $38 billion (€32.4 billion) for UMG, further underpinning the implied value from the recent Tencent transaction.

Catalysts on the Horizon:

- IPO of Universal Music Group (UMG) 18-24 months

- Additional potential strategic partnerships in UMG ahead of the IPO

- Litigation settlement with Mediaset in Italy should allow those investments to improve cash flow substantially

- Continues to be a buyer of underperforming media-related assets where Vivendi can transform the target and create value. Vivendi has amassed a 26.7% stake in Lagardère, a perennial "tomorrow" story in France with compelling assets in media, publishing and travel-related retail. We believe Vivendi is eyeing Lagardère's Hachette publishing group, one of the largest globally

Bolloré (BOL FP)

Market cap: $11.1 billion

200-year-old conglomerate controlled by Vincent Bolloré, an aggressive value creator with a proven track record. Bolloré also controls media assets including 29% of Vivendi, discussed previously. It also holds leading positions in all its activities: ports, transportation and logistics businesses in Africa, communications and electricity storage solutions.

Catalysts on the Horizon:

- Significant strategic change is underway at Vivendi with breakup, asset sales and a complete refocusing of its businesses (see above)

- Simplification of complicated crossholding structure – Bolloré is essentially controlled by intermediate holding companies, which in turn, own direct and indirect stakes in Bolloré. Elimination of the treasury shares implicit in the crossholdings should be extremely accretive

- Sneaking through the back door to get indirect exposure to opportunities in Africa

S&T (SANT FP)

Market cap: $1.4 billion

S&T AG provides traditional IT services to small and medium enterprises in Eastern Europe. It also provides software embedded hardware solutions for high-cost-of-failure applications within industrial and infrastructure end markets. We believe the company’s valuation is modest given the growth trajectory of S&T’s end markets, as well as its demonstrable ability to acquire—and quickly turn around—distressed assets while putting very little capital at risk. Management owns significant equity and has been aggressively buying shares personally on the open market.

Catalysts on the Horizon:

- Potential tender by Foxconn which indirectly owns 27% of S&T.

Exor (EXO IM)

Market cap: $13.7 billion

Exor is the investment vehicle of the Agnelli Family of Italy. John Elkann, great-great grandson of Giovanni Agnelli, the founder of Fiat, has done an admirable job of building great business franchises through M&A, portfolio pruning, and targeted investments within portfolio companies. Exor trades at an approximate 30% discount to the sum of its listed holdings. However, we believe that a number of these holdings, namely Fiat Chrysler Automobiles (undergoing a transformational merger with Peugeot), and CNH Industrial (splitting into two publicly-traded entities) are cheap in their own right. Lastly, we believe the company’s large investment in PartnerRe is likely to be monetized in the medium term, which should provide the company with significant firepower for shareholder returns or savvy M&A.

Catalysts on the Horizon:

- Completion of the merger between FCA and Peugeot, slated for Q1 2021, is expected to yield massive cost synergies of more than €5 billion.

- The spinoff of the On-Highway business from CNH Industrial, which we expect sometime in 2021, will create two separate publicly-traded industrial leaders.

- Potential monetization of PartnerRe.

PharmaSGP (PSG GY)

Market cap: $440 million

Recently listed pure-play pharmaceutical and consumer health company in Germany. PharmaSGP has a broad portfolio of chemical free, over-the-counter healthcare products; as a result of its first-mover advantage, it has one of the largest portfolios of products and pharmaceutical marketing authorizations for new products in Europe. In Germany, and in the core markets in Western Europe in which the company operates, OTC healthcare products can be only sold in pharmacies. The regulatory environment serves as a natural barrier to entry as the sale of these products is strictly controlled. More specifically, under the German Pharmacy Act, large pharmacy chains or consumer multinational companies are prohibited from entering Germany. The company is the market share leader in its core markets in Europe (Germany, France, Italy, Spain Belgium, Austria). PharmaSGP has a solid business model (asset light, highly scalable) and is characterized by a high free cash flow conversion (over 90%) with minimal capital expenditure requirements and working capital needs.

Catalysts on the Horizon:

- In spite of COVID-19, PharmaSGP had strong sales growth in its core and international markets (especially Italy). Continued strong execution and cash generation

- Strengthened presence and market share capture in Austria through successful brand extension launches

- Entry into the French market is ongoing and on track. Secured approval from regulatory authorities to initiate ad marketing for its products

- Recently hired a dedicated chief business development officer, Maria-Johanna Schaecher, to further drive growth through acquisitions. We believe there are many potential acquisitions of poorly capitalized, smaller competitors or individual product authorizations

Fagron (FAGR BB)

Market cap: $1.84 billion

Belgium-based leader in pharmaceutical compounding based on formulations of existing active pharmaceutical ingredients (“APIs”) that are no longer under patent. Market leading positions in Europe, #1 market share in Brazil and U.S. is currently growing (Evermore assumed no value to the U.S. during the restructuring). Fagron has transformed from an underperforming business with a weak balance sheet to a rapidly growing group of relatively recession-resilient businesses in Europe, the U.S. and Latin America with a strong balance sheet.

Catalysts on the Horizon:

- The largest U.S. competitor, Pharmedium (wholly owned by AmerisourceBergen), announced that it would permanently close all operations due to insurmountable FDA-related issues. Huge opportunity to capture market share in the U.S. compounding business.

- Fagron also supplies critical ingredients for several potential treatments that are currently undergoing testing worldwide as potential treatments for COVID-19 in some of the most severe cases. Upside potential in the event of a worse-than-expected second wave of COVID-19.

- Natural beneficiary of the €750 billion Next Generation EU Stimulus, specifically Goal #4 (EU4Health) pertaining to a pandemic crisis preparedness.

Telia (TELIA SS)

Market cap: $16.6 billion

Based in Sweden, Telia is the largest telecom operator in the Nordics and Baltics that has been a massive underperformer in the last five years. This was once the government-controlled phone company in Sweden that eventually got “fat” and unwieldy over time. Classic Evermore investment case: restructuring, breakup and potential spin-off. New Chairman (Lars-Johan Jarnheimer) and CEO (Allison Kirkby) at the helm – both highly regarded with aggressive restructuring and turnaround pedigrees. Over the years, we have learned that the best activist cases may be the ones where the management itself is the activist.

Catalysts on the Horizon:

- Allison Kirkby has already moved quickly since assuming her role as CEO this past May. Within the first two months under the CEO, Telia announced the sale of a non-core asset in Turkcell Holding

- Replaced four members of the legacy management team with two new well-regarded hires – a new head of strategy and new head of communication, governance and sustainability. We expect more changes to occur in the near term

- In July, the CFO was replaced with Per Christian Morland, the former CFO of Telia Norway (since October 2015) who also has 16 years of deep telecom experience in the Nordics, Central Europe and Asia. The COO was also replaced by a highly credentialed industry expert that is external to the company

- We expect additional restructuring and cost cutting initiatives to be announced over the coming months

- Potential for additional non-core asset sales and/or spin-off to shareholders

Atlantic Sapphire (ASA NO)

Market cap: $918 million

Headquartered in Norway, Atlantic Sapphire is revolutionizing Atlantic salmon farming by growing fish entirely in large tanks on land. By eliminating biological risk factors found at sea (predators, disease, microplastics) and substantially reducing transportation times, Sapphire’s “Blue House” salmon should command both favorable market pricing and low production costs. In what is a structurally tightly-supplied market, we expect the company to enjoy industry-leading margins. Today, the company has a proof of concept facility in Denmark (producing ~2,500 tons annually). At the helm is an entrepreneurial and experienced team with significant skin in the game.

Catalysts on the Horizon:

- First ever U.S. salmon harvest at Atlantic Sapphire’s U.S. facility (newly-constructed 10,000 ton facility in Homestead, Florida) completed at the end of September

- In the coming weeks, the U.S. commercial harvest will be sold under the “Bluehouse Salmon” label to stores such as Giant Eagle, H-E-B, New Seasons Market, Publix, Safeway, Sobey’s, Sprouts Farmers Market and Wegmans

LPKF Laser & Electronics (LPK GY)

Market cap: $627 million

German designer and producer of high-value laser systems that are critical to functions in the design of printed circuit boards, the manufacturing of solar panels and screen displays, and the hermetically-sealed welding of plastics (key in automotive and medical end markets). For a number of applications/solutions, LPK serves as the only game in town. For a company with de facto standard technologies in large, growing, and diverse end markets, we believe the market is completely underestimating the company’s growth profile. We also feel the market does not appreciate that LPK’s revenues going forward are expected to be increasingly recurring in nature, which should serve to reduce the cyclicality of the businesses.

Catalysts on the Horizon:

- Customer win announcements around LPK’s Laser Induced Deep Etching (or LIDE) technology and continued business wins in solar.

Conclusion

The COVID-19 crisis has enhanced an exceptional special situations investment environment in Europe.

The market today, we believe, offers investors the most compelling opportunity set that we have witnessed since Q1 2009.

The confluence of the bottom-up and top-down catalysts is unprecedented in our view. Now, as so many investors are giving up on international investing, especially in Europe, is precisely the time to get out there, be very aggressive and scoop up these situations where we have Value / Growth / Catalysts / Exceptional Management and Entrepreneurialism as we have never seen internationally.

The Evermore Focused Europe Fund, L.P. was formed to take advantage of this environment.

We remain steadfast in our belief that the time to invest in Europe is now, and that the volume and magnitude of opportunities will evaporate with continued economic recovery.

The post Evermore Global Advisor: Opportunity In Europe appeared first on ValueWalk.

bonds pandemic covid-19 equities blockchain euro otc stock marketsGovernment

Supreme Court Rules Public Officials May Block Their Constituents On Social Media

Supreme Court Rules Public Officials May Block Their Constituents On Social Media

Authored by Matthew Vadum via The Epoch Times (emphasis…

Share this:

Authored by Matthew Vadum via The Epoch Times (emphasis ours),

Public officials may block people on social media in certain situations, the Supreme Court ruled unanimously on March 15.

At the same time, the court held that public officials who post about topics pertaining to their work on their personal social media accounts are acting on behalf of the government. But such officials can be found liable for violating the First Amendment only when they have been properly authorized by the government to communicate on its behalf.

The case is important because nowadays public officials routinely reach out to voters through social media on the same pages where they discuss personal matters unrelated to government business.

“When a government official posts about job-related topics on social media, it can be difficult to tell whether the speech is official or private,” Justice Amy Coney Barrett wrote for the nation’s highest court.

The case is separate from but brings to mind a lawsuit that several individuals previously filed against former President Donald Trump after he blocked them from accessing his social media account on Twitter, which was later renamed X. The Supreme Court dismissed that case, Biden v. Knight First Amendment Institute, in April 2021 as moot because President Trump had already left office.

At the time of the ruling, the then-Twitter had banned President Trump. When Elon Musk took over the company he reversed that policy.

The new decision in Lindke v. Freed was written by Justice Amy Coney Barrett.

Respondent James Freed, the city manager of Port Huron, Michigan, used a public Facebook account to communicate with his constituents. Petitioner Kevin Lindke, a resident of Port Huron, criticized the municipality’s response to the COVID-19 pandemic, including accusations of hypocrisy by local officials.

Mr. Freed blocked Mr. Lindke and others and removed their comments, according to Mr. Lindke’s petition.

The U.S. Court of Appeals for the 6th Circuit ruled for Mr. Freed, finding that he was acting only in a personal capacity and that his activities did not constitute governmental action.

Mr. Freed’s attorney, Victoria Ferres, said during oral arguments before the Supreme Court on Oct. 31, 2023, that her client didn’t give up his rights when using social media.

“This country’s 21 million government employees should have the right to talk publicly about their jobs on personal social media accounts like their private-sector counterparts.”

The position advocated by the other side would unfairly punish government officials, and “will result in uncertainty and self-censorship for this country’s government employees despite this Court repeatedly finding that government employees do not lose their rights merely by virtue of public employment,” she said.

In Lindke v. Freed, the Supreme Court found that a public official who prevents a person from comments on the official’s social media pages engages in governmental action under Section 1983 only if the official had “actual authority” to speak on the government’s behalf on a specific matter and if the official claimed to exercise that authority when speaking in the relevant social media posts.

Section 1983 refers to Title 42, U.S. Code, Section 1983, which allows people to sue government actors for deprivation of civil rights.

Justice Barrett wrote that according to the so-called state action doctrine, the test for “actual authority” must be “rooted in written law or longstanding custom to speak for the State.”

“That authority must extend to speech of the sort that caused the alleged rights deprivation. If the plaintiff cannot make this threshold showing of authority, he cannot establish state action.”

“For social-media activity to constitute state action, an official must not only have state authority—he must also purport to use it,” the justice continued.

“State officials have a choice about the capacity in which they choose to speak.”

Citing previous precedent, Justice Barrett wrote that generally a public employee claiming to speak on behalf of the government acts with state authority when he speaks “in his official capacity or” when he uses his speech to carry out “his responsibilities pursuant to state law.”

“If the public employee does not use his speech in furtherance of his official responsibilities, he is speaking in his own voice.”

The Supreme Court remanded the case to the 6th Circuit with instructions to vacate its judgment and ordered it to conduct “further proceedings consistent with this opinion.”

Also on March 15, the Supreme Court ruled on O’Connor-Ratcliff v. Garnier, a related case. The court’s sparse, unanimous opinion was unsigned.

Petitioners Michelle O’Connor-Ratcliff and T.J. Zane were two elected members of the Poway Unified School District Board of Trustees in California who used their personal Facebook and Twitter accounts to communicate with the public.

Respondents Christopher Garnier and Kimberly Garnier, parents of local students, “spammed Petitioners’ posts and tweets with repetitive comments and replies” so the school board members blocked the respondents from the accounts, according to the petition filed by Ms. O’Connor-Ratcliff and Mr. Zane.

But the Garniers said they were acting in good faith.

“The Garniers left comments exposing financial mismanagement by the former superintendent as well as incidents of racism,” the couple said in a brief.

The U.S. Court of Appeals for the 9th Circuit found in favor of the Garniers, holding that elected officials using social media accounts were participating in a public forum.

The Supreme Court ruled in a three-page opinion that because the 9th Circuit deviated from the standard the high court articulated in Lindke v. Freed, the 9th Circuit’s decision must be vacated.

The case was remanded to the 9th Circuit “for further proceedings consistent with our opinion” in the Lindke case, the Supreme Court stated.

International

Home buyers must now navigate higher mortgage rates and prices

Rates under 4% came and went during the Covid pandemic, but home prices soared. Here’s what buyers and sellers face as the housing season ramps up.

Share this:

Springtime is spreading across the country. You can see it as daffodil, camellia, tulip and other blossoms start to emerge.

You can also see it in the increasing number of for sale signs popping up in front of homes, along with the painting, gardening and general sprucing up as buyers get ready to sell.

Which leads to two questions:

- How is the real estate market this spring?

- Where are mortgage rates?

What buyers and sellers face

The housing market is bedeviled with supply shortages, high prices and slow sales.

Mortgage rates are still high and may limit what a buyer can offer and a seller can expect.

Related: Analyst warns that a TikTok ban could lead to major trouble for Apple, Big Tech

And there's a factor not expected that may affect the sales process. Fixed commission rates on home sales are going away in July.

Reports this week and in a week will make the situation clearer for buyers and sellers.

The reports are:

- Housing starts from the U.S. Commerce Department due Tuesday. The consensus estimate is for a seasonally adjusted rate of about 1.4 million homes. These would include apartments, both rentals and condominiums.

- Existing home sales, due Thursday from the National Association of Realtors. The consensus estimate is for a seasonally adjusted sales rate of about 4 million homes. In 2023, some 4.1 million homes were sold, the worst sales rate since 1995.

- New-home sales and prices, due Monday from the Commerce Department. Analysts are expecting a sales rate of 661,000 homes (including condos), up 1.5% from a year ago.

Here is what buyers and sellers need to know about the situation.

Mortgage rates will stay above 5%

That's what most analysts believe. Right now, the rate on a 30-year mortgage is between 6.7% and 7%.

Rates peaked at 8% in October after the Federal Reserve signaled it was done raising interest rates.

The Freddie Mac Primary Mortgage Market Survey of March 14 was at 6.74%.

Freddie Mac buys mortgages from lenders and sells securities to investors. The effect is to replenish lenders' cash levels to make more loans.

A hotter-than-expected Producer Price Index released that day has pushed quotes to 7% or higher, according to data from Mortgage News Daily, which tracks mortgage markets.

TheStreet

On a median-priced home (price: $380,000) and a 20% down payment, that means a principal and interest rate payment of $2,022. The payment does not include taxes and insurance.

Last fall when the 30-year rate hit 8%, the payment would have been $2,230.

In 2021, the average rate was 2.96%, which translated into a payment of $1,275.

Short of a depression, that's a rate that won't happen in most of our lifetimes.

Most economists believe current rates will fall to around 6.3% by the end of the year, maybe lower, depending on how many times the Federal Reserve cuts rates this year.

If 6%, the payment on our median-priced home is $1,823.

But under 5%, absent a nasty recession, fuhgettaboutit.

Supply will be tight, keeping prices up

Two factors are affecting the supply of homes for sale in just about every market.

First: Homeowners who had been able to land a mortgage at 2.96% are very reluctant to sell because they would then have to find a home they could afford with, probably, a higher-cost mortgage.

More economic news:

- Fed members just hat-tipped what's next for interest rates

- Retail sales tumble clouds impact of inflation data

- Jobs report shocker: 353,000 hires crush forecasts, stokes inflation fears

Second, the combination of high prices and high mortgage rates are freezing out thousands of potential buyers, especially those looking for homes in lower price ranges.

Indeed, The Wall Street Journal noted that online brokerage Redfin said only about 20% of homes for sale in February were affordable for the typical household.

And here mortgage rates can play one last nasty trick. If rates fall, that means a buyer can afford to pay more. Sellers and their real-estate agents know this too, and may ask for a higher price.

Covid's last laugh: An inflation surge

Mortgage rates jumped to 8% or higher because since 2022 the Federal Reserve has been fighting to knock inflation down to 2% a year. Raising interest rates was the ammunition to battle rising prices.

In June 2022, the consumer price index was 9.1% higher than a year earlier.

The causes of the worst inflation since the 1970s were:

- Covid-19 pandemic, which caused the global economy to shut down in 2020. When Covid ebbed and people got back to living their lives, getting global supply chains back to normal operation proved difficult.

- Oil prices jumped to record levels because of the recovery from the pandemic recovery and Russia's invasion of Ukraine.

What the changes in commissions means

The long-standing practice of paying real-estate agents will be retired this summer, after the National Association of Realtors settled a long and bitter legal fight.

No longer will the seller necessarily pay 6% of the sale price to split between buyer and seller agents.

Both sellers and buyers will have to negotiate separately the services agents have charged for 100 years or more. These include pre-screening properties, writing sales contracts, and the like. The change will continue a trend of adding costs and complications to the process of buying or selling a home.

Already, interest rates are a complication. In addition, homeowners insurance has become very pricey, especially in communities vulnerable to hurricanes, tornadoes, and forest fires. Florida homeowners have seen premiums jump more than 102% in the last three years. A policy now costs three times more than the national average.

Related: Veteran fund manager picks favorite stocks for 2024

recession depression pandemic covid-19 stocks fed federal reserve home sales mortgage rates real estate mortgages housing market recovery interest rates oil russia ukraine

Uncategorized

Default: San Francisco Four Seasons Hotel Investors $3 Million Late On Loan As Foreclosure Looms

Default: San Francisco Four Seasons Hotel Investors $3 Million Late On Loan As Foreclosure Looms

Westbrook Partners, which acquired the San…

Share this:

{kind=link}

Westbrook Partners, which acquired the San Francisco Four Seasons luxury hotel building, has been served a notice of default, as the developer has failed to make its monthly loan payment since December, and is currently behind by more than $3 million, the San Francisco Business Times reports.

{kind=link}

Westbrook, which acquired the property at 345 California Center in 2019, has 90 days to bring their account current with its lender or face foreclosure.

Related

- Fed Fears "Notable" Financial System Vulnerability As Renowned CRE Investor Tells Team 'Stop All NYC Underwriting'

- The State Of Commercial Real Estate, In Charts

- "Who Could Be Next": Top Canadian Pension Fund Sells Manhattan Office Tower For $1, Sparking Firesale Panic

- "Heightened Risks": Goldman Points To Leading CRE Indicator That Shows Pain Train Not Over

As SF Gate notes, downtown San Francisco hotel investors have had a terrible few years - with interest rates higher than their pre-pandemic levels, and local tourism continuing to suffer thanks to the city's legendary mismanagement that has resulted in overlapping drug, crime, and homelessness crises (which SF Gate characterizes as "a negative media narrative).

Last summer, the owner of San Francisco’s Hilton Union Square and Parc 55 hotels abandoned its loan in the first major default. Industry insiders speculate that loan defaults like this may become more common given the difficult period for investors.

At a visitor impact summit in August, a senior director of hospitality analytics for the CoStar Group reported that there are 22 active commercial mortgage-backed securities loans for hotels in San Francisco maturing in the next two years. Of these hotel loans, 17 are on CoStar’s “watchlist,” as they are at a higher risk of default, the analyst said. -SF Gate

The 155-room Four Seasons San Francisco at Embarcadero currenly occupies the top 11 floors of the iconic skyscrper. After slow renovations, the hotel officially reopened in the summer of 2021.

"Regarding the landscape of the hotel community in San Francisco, the short term is a challenging situation due to high interest rates, fewer guests compared to pre-pandemic and the relatively high costs attached with doing business here," Alex Bastian, President and CEO of the Hotel Council of San Francisco, told SFGATE.

Heightened Risks

In January, the owner of the Hilton Financial District at 750 Kearny St. - Portsmouth Square's affiliate Justice Operating Company - defaulted on the property, which had a $97 million loan on the 544-room hotel taken out in 2013. The company says it proposed a loan modification agreement which was under review by the servicer, LNR Partners.

Meanwhile last year Park Hotels & Resorts gave up ownership of two properties, Parc 55 and Hilton Union Square - which were transferred to a receiver that assumed management.

In the third quarter of 2023, the most recent data available, the Hilton Financial District reported $11.1 million in revenue, down from $12.3 million from the third quarter of 2022. The hotel had a net operating loss of $1.56 million in the most recent third quarter.

Occupancy fell to 88% with an average daily rate of $218 in the third quarter compared with 94% and $230 in the same period of 2022. -SF Chronicle

According to the Chronicle, San Francisco's 2024 convention calendar is lighter than it was last year - in part due to key events leaving the city for cheaper, less crime-ridden places like Las Vegas.

Mistakes Were Made

Home buyers must now navigate higher mortgage rates and prices

Women’s basketball is gaining ground, but is March Madness ready to rival the men’s game?

Supreme Court Rules Public Officials May Block Their Constituents On Social Media

Gen Z, The Most Pessimistic Generation In History, May Decide The Election

“Extreme Events”: US Cancer Deaths Spiked In 2021 And 2022 In “Large Excess Over Trend”

Harvard Medical School Professor Was Fired Over Not Getting COVID Vaccine

Default: San Francisco Four Seasons Hotel Investors $3 Million Late On Loan As Foreclosure Looms

Correcting the Washington Post’s 11 Charts That Are Supposed to Tell Us How the Economy Changed Since Covid

-

Uncategorized3 weeks ago

Uncategorized3 weeks agoAll Of The Elements Are In Place For An Economic Crisis Of Staggering Proportions

-

International1 week ago

International1 week agoEyePoint poaches medical chief from Apellis; Sandoz CFO, longtime BioNTech exec to retire

-

Spread & Containment5 days ago

Spread & Containment5 days agoIFM’s Hat Trick and Reflections On Option-To-Buy M&A

-

Uncategorized1 month ago

Uncategorized1 month agoCalifornia Counties Could Be Forced To Pay $300 Million To Cover COVID-Era Program

-

Uncategorized3 weeks ago

Uncategorized3 weeks agoApparel Retailer Express Moving Toward Bankruptcy

-

Uncategorized1 month ago

Uncategorized1 month agoIndustrial Production Decreased 0.1% in January

-

International1 week ago

International1 week agoWalmart launches clever answer to Target’s new membership program

-

Uncategorized1 month ago

Uncategorized1 month agoRFK Jr: The Wuhan Cover-Up & The Rise Of The Biowarfare-Industrial Complex