Do Antiviral Pills Negate The Need For Vaccine Mandates?

Do Antiviral Pills Negate The Need For Vaccine Mandates?

Authored by Red Jahncke via RealClearPolicy.com,

The Biden Administration’s generals are fighting the last war. Last Thursday, they mandated that large businesses and health care…

Share this:

Authored by Red Jahncke via RealClearPolicy.com,

The Biden Administration’s generals are fighting the last war. Last Thursday, they mandated that large businesses and health care facilities require that their workers get vaccinated for COVID-19. On Friday, Pfizer announced an antiviral pill to treat the virus. Pfizer’s pill is 89% effective. A Merck antiviral pill for COVID-19 (with only about 50% effectiveness) is already in use in Britain.

COVID-19 treatment pills destroy any vestige of logic or justification for the new mandates.

No matter how someone contracts the virus, these pills prevent serious illness — hospitalization and death. With double lines of defense against the coronavirus — vaccination, and, now, these new antiviral treatment pills — mandates have become unnecessary.

On Saturday, the Fifth U.S. Court of Appeals issued an emergency stay of the Biden business mandate, saying it raises “grave statutory and constitutional issues.”

Quite apart for the legal issues, the mandates ignore science and logic.

The logic of a vaccine mandate has always been weak and self-contradictory insofar as their implied purpose of protecting vaccinated people from unvaccinated people. If vaccines are effective (95% effective in Pfizer’s case), then, vaccinated people face little risk from unvaccinated people.

If the vaccines are ineffective, then why should anyone get them?

Naturally, there are minor exceptions to this logic.

-

First, a vaccine that is 95% effective is 5% ineffective.

-

Second, there have been “breakthrough cases” of largely unknown number and origin. They could represent the 5% ineffectiveness factor, and they could demonstrate that the vaccines are less effective against variants of the virus.

-

Third, studies suggest that the efficacy of vaccines diminish over time.

All three of these minor exceptions are addressed by booster shots — in the same fashion as annual vaccines protect against the seasonal flu. Flu shots are in effect boosters, after the effectiveness of the prior season’s flu shot has waned. Each year flu shots are recalibrated for recurring and potential new variants, and, each year, they are less than 100% effective. There is always some risk.

There is a critical difference between flu shots and COVID-19 vaccines. The flu shots have no back-up. There is no flu pill.

The new antiviral treatment pills for COVID-19 dramatize further the original illogic of mandates: If vaccines and boosters and treatment pills are even more effective — as science and logic say they are, then unvaccinated people pose virtually no threat to vaccinated people. Now add the new corollary: Unvaccinated people do not even endanger themselves, because they can take the Merck or Pfizer pill (once approved) if they do contract COVID-19. They don’t even burden the healthcare system — remember “bending the curve” — since the pills are intended for home use.

Now, most Americans got vaccinated as soon as they could. Most consider the vaccines a virtual godsend, an amazing demonstration of American scientific and pharmaceutical prowess. Most don’t really understand why someone would not get vaccinated.

But we live in a country where people can do what they want if they aren’t threatening anyone else, don’t we? Without pretending to litigate the legal issues, vaccine mandates appear to be an unnecessary violation of personal liberty. What could be more invasive than the government dictating what you must do with your own body — your life and your life only?

Parsing the issue further, there is a vast difference between government dictating vaccine policy and a business — or any organization — establishing an organizational vaccine policy. If an organization adopts a vaccine mandate, an anti-vaccine employee can quit and find another job.

Beyond these observations, let’s leave the Fifth Circuit to begin the process of sorting out the legal and constitutional issues. The Court has ordered the Biden Administration to file its arguments to lift the stay by yesterday afternoon.

Yet, science and basic logic would seem to be enough to decide the issue. No one who gets vaccinated, gets a booster shot and has available antiviral pills is at appreciable risk from exposure to unvaccinated people.

That is not to say that vaccinated people will not contract the virus, nor to say that some vaccinated people will not get seriously ill and die. Until there is a life-long vaccine, such as the polio vaccine, COVID-19 will be a part of our lives.

In the meantime, the real danger comes from a frustrated Biden Administration misusing urgent emergency powers under existing occupational health and safety law to exercise extraordinary powers. For Biden & Co., the already dissipating 20-month-old pandemic is not receding fast enough. That is neither urgent nor an emergency. It manifests that the Administration is fighting yesterday’s COVID-19 battle, without realizing that the antiviral pills have radically altered the war.

Like it or not, COVID-19 has taken hold and is here to stay, but not as the threat to which we were originally defenseless. Biden’s COVID-19 vaccine mandates would set a dangerous precedent. They should never take hold. Who’s to say what the next “emergency” would be that government might use as a pretext to exercise such overriding power.

Spread & Containment

There Goes The Fed’s Inflation Target: Goldman Sees Terminal Rate 100bps Higher At 3.5%

There Goes The Fed’s Inflation Target: Goldman Sees Terminal Rate 100bps Higher At 3.5%

Two years ago, we first said that it’s only a matter…

Share this:

Two years ago, we first said that it's only a matter of time before the Fed admits it is unable to rsolve the so-called "last mile" of inflation and that as a result, the old inflation target of 2% is no longer viable.

At some point Fed will concede it has no control over supply. That's when we will start getting leaks of raising the inflation target

— zerohedge (@zerohedge) June 21, 2022

Then one year ago, we correctly said that while everyone was paying attention elsewhere, the inflation target had already been hiked to 2.8%... on the way to even more increases.

The new inflation target has been set to 2.8%. The rest is just narrative fill for the next 2 years. https://t.co/X1xYkecyPy

— zerohedge (@zerohedge) February 21, 2023

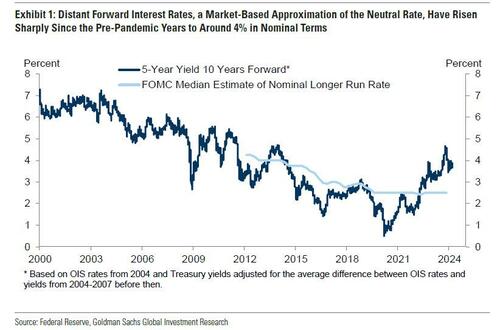

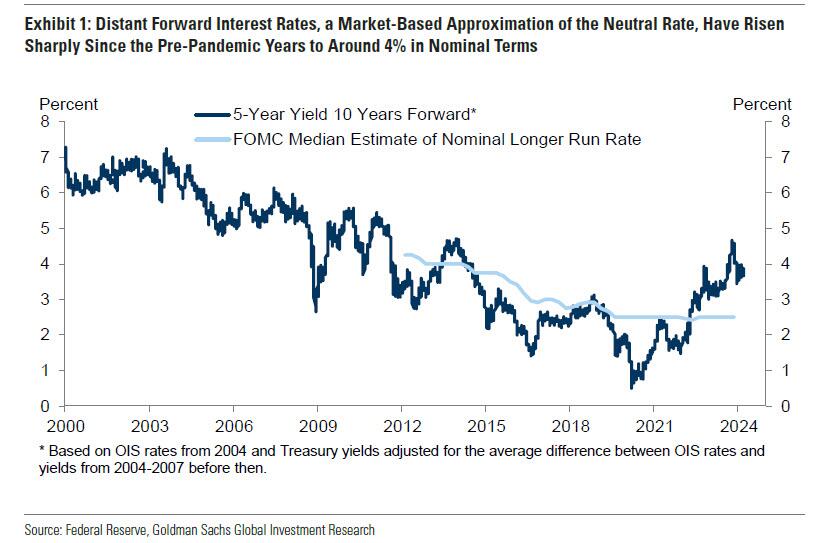

And while the Fed still pretends it can one day lower inflation to 2% even as it prepares to cut rates as soon as June, moments ago Goldman published a note from its economics team which had to balls to finally call a spade a spade, and concluded that - as party of the Fed's next big debate, i.e., rethinking the Neutral rate - both the neutral and terminal rate, a polite euphemism for the inflation target, are much higher than conventional wisdom believes, and that as a result Goldman is "penciling in a terminal rate of 3.25-3.5% this cycle, 100bp above the peak reached last cycle."

There is more in the full Goldman note, but below we excerpt the key fragments:

We argued last cycle that the long-run neutral rate was not as low as widely thought, perhaps closer to 3-3.5% in nominal terms than to 2-2.5%. We have also argued this cycle that the short-run neutral rate could be higher still because the fiscal deficit is much larger than usual—in fact, estimates of the elasticity of the neutral rate to the deficit suggest that the wider deficit might boost the short-term neutral rate by 1-1.5%. Fed economists have also offered another reason why the short-term neutral rate might be elevated, namely that broad financial conditions have not tightened commensurately with the rise in the funds rate, limiting transmission to the economy.

Over the coming year, Fed officials are likely to debate whether the neutral rate is still as low as they assumed last cycle and as the dot plot implies....

...Translation: raising the neutral rate estimate is also the first step to admitting that the traditional 2% inflation target is higher than previously expected. And once the Fed officially crosses that particular Rubicon, all bets are off.

... Their thinking is likely to be influenced by distant forward market rates, which have risen 1-2pp since the pre-pandemic years to about 4%; by model-based estimates of neutral, whose earlier real-time values have been revised up by roughly 0.5pp on average to about 3.5% nominal and whose latest values are little changed; and by their perception of how well the economy is performing at the current level of the funds rate.

The bank's conclusion:

We expect Fed officials to raise their estimates of neutral over time both by raising their long-run neutral rate dots somewhat and by concluding that short-run neutral is currently higher than long-run neutral. While we are fairly confident that Fed officials will not be comfortable leaving the funds rate above 5% indefinitely once inflation approaches 2% and that they will not go all the way back to 2.5% purely in the name of normalization, we are quite uncertain about where in between they will ultimately land.

Because the economy is not sensitive enough to small changes in the funds rate to make it glaringly obvious when neutral has been reached, the terminal or equilibrium rate where the FOMC decides to leave the funds rate is partly a matter of the true neutral rate and partly a matter of the perceived neutral rate. For now, we are penciling in a terminal rate of 3.25-3.5% this cycle, 100bps above the peak reached last cycle. This reflects both our view that neutral is higher than Fed officials think and our expectation that their thinking will evolve.

Not that this should come as a surprise: as a reminder, with the US now $35.5 trillion in debt and rising by $1 trillion every 100 days, we are fast approaching the Minsky Moment, which means the US has just a handful of options left: losing the reserve currency status, QEing the deficit and every new dollar in debt, or - the only viable alternative - inflating it all away. The only question we had before is when do "serious" economists make the same admission.

Meanwhile, nothing changes: total US debt jumps $57BN on March 15, to a record $34.543 trillion.

— zerohedge (@zerohedge) March 19, 2024

Three ways this ends: inflate it away, QE it all, or reserve status collapse

They now have.

And while we have discussed the staggering consequences of raising the inflation target by just 1% from 2% to 3% on everything from markets, to economic growth (instead of doubling every 35 years at 2% inflation target, prices would double every 23 years at 3%), and social cohesion, we will soon rerun the analysis again as the implications are profound. For now all you need to know is that with the US about to implicitly hit the overdrive of dollar devaluation, anything that is non-fiat will be much more preferable over fiat alternatives.

Much more in the full Goldman note available to pro subs in the usual place.

Spread & Containment

Household Net Interest Income Falls As Rates Spike

A Bloomberg article from this morning offered an excellent array of charts detailing the shifts in interest payment flows amid rising rates. The historical…

Share this:

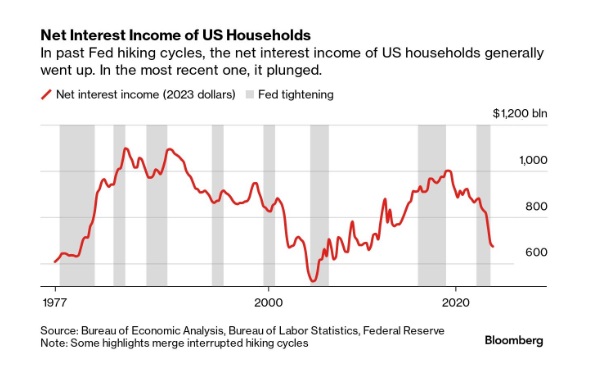

A Bloomberg article from this morning offered an excellent array of charts detailing the shifts in interest payment flows amid rising rates. The historical anomaly was both surprising and contradicted our priors.

10 Key Points:

- Historical Anomaly: This is the first time in the last fifty years that a Federal Reserve rate hike cycle has led to a significant drop in household net interest income.

- Interest Expense Increase: Since the Fed began raising rates in March 2022, Americans’ annual interest expenses on debts like mortgages and credit cards have surged by nearly $420 billion.

- Interest Income Lag: The increase in interest income during the same period was only about $280 billion, resulting in a net decline in household interest income, a departure from past trends.

- Consumer Debt Influence: The recent rate hikes impacted household finances more because of a higher proportion of consumer credit, which adjusts more quickly to rate changes, increasing interest costs.

- Banks and Savers: Banks have been slow to pass on higher interest rates to depositors, and the prolonged period of low rates before 2022 may have discouraged savers from actively seeking better returns.

- Shift in Wealth: There’s been a shift from interest-bearing assets to stocks, with dividends surpassing interest payments as a source of unearned income during the pandemic.

- Distributional Discrepancy: Higher interest rates benefit wealthier individuals who own interest-earning assets, whereas lower-income earners face the brunt of increased debt servicing costs, exacerbating economic inequality.

- Job Market Impact: Typically, Fed rate hikes affect households through the job market, as businesses cut costs, potentially leading to layoffs or wage suppression, though this hasn’t occurred yet in the current cycle.

- Economic Impact: The distribution of interest income and debt servicing means that rate increases transfer money from those more likely to spend (and thus stimulate the economy) to those less likely to increase consumption, potentially dampening economic activity.

- No Immediate Relief: Expectations for the Fed to reduce rates have diminished, indicating that high-interest expenses for households may persist.

Uncategorized

One more airline cracks down on lounge crowding in a way you won’t like

Qantas Airways is increasing the price of accessing its network of lounges by as much as 17%.

Share this:

{kind=link}

{kind=link}

Over the last two years, multiple airlines have dealt with crowding in their lounges. While they are designed as a luxury experience for a small subset of travelers, high numbers of people taking a trip post-pandemic as well as the different ways they are able to gain access through status or certain credit cards made it difficult for some airlines to keep up with keeping foods stocked, common areas clean and having enough staff to serve bar drinks at the rate that customers expect them.

In the fall of 2023, Delta Air Lines (DAL) caught serious traveler outcry after announcing that it was cracking down on crowding by raising how much one needs to spend for lounge access and limiting the number of times one can enter those lounges.

Related: Competitors pushed Delta to backtrack on its lounge and loyalty program changes

Some airlines saw the outcry with Delta as their chance to reassure customers that they would not raise their fees while others waited for the storm to pass to quietly implement their own increases.

Shutterstock

This is how much more you'll have to pay for Qantas lounge access

Australia's flagship carrier Qantas Airways (QUBSF) is the latest airline to announce that it would raise the cost accessing the 24 lounges across the country as well as the 600 international lounges available at airports across the world through partner airlines.

More Travel:

- A new travel term is taking over the internet (and reaching airlines and hotels)

- The 10 best airline stocks to buy now

- Airlines see a new kind of traveler at the front of the plane

Unlike other airlines which grant access primarily after reaching frequent flyer status, Qantas also sells it through a membership — starting from April 18, 2024, prices will rise from $600 Australian dollars ($392 USD) to $699 AUD ($456 USD) for one year, $1,100 ($718 USD) to $1,299 ($848 USD) for two years and $2,000 AUD ($1,304) to lock in the rate for four years.

Those signing up for lounge access for the first time also currently pay a joining fee of $99 AUD ($65 USD) that will rise to $129 AUD ($85 USD).

The airline also allows customers to purchase their membership with Qantas Points they collect through frequent travel; the membership fees are also being raised by the equivalent amount in points in what adds up to as much as 17% — from 308,000 to 399,900 to lock in access for four years.

Airline says hikes will 'cover cost increases passed on from suppliers'

"This is the first time the Qantas Club membership fees have increased in seven years and will help cover cost increases passed on from a range of suppliers over that time," a Qantas spokesperson confirmed to Simple Flying. "This follows a reduction in the membership fees for several years during the pandemic."

The spokesperson said the gains from the increases will go both towards making up for inflation-related costs and keeping existing lounges looking modern by updating features like furniture and décor.

While the price increases also do not apply for those who earned lounge access through frequent flyer status or change what it takes to earn that status, Qantas is also introducing even steeper increases for those renewing a membership or adding additional features such as spouse and partner memberships.

In some cases, the cost of these features will nearly double from what members are paying now.

stocks pandemic

Google’s A.I. Fiasco Exposes Deeper Infowarp

Home buyers must now navigate higher mortgage rates and prices

Greenback Surges after BOJ Hikes and Ends YCC and RBA Delivers a Dovish Hold

Supreme Court Rules Public Officials May Block Their Constituents On Social Media

Manufacturing and construction vs. the still-inverted yield curve

Student loan borrowers may finally get answers to loan forgiveness issues

When words make you sick

You can strike gold and silver investment opportunities at Costco

Bolsonaro Indicted By Brazilian Police For Falsifying Covid-19 Vaccine Records

Germany Is Running Out Of Money And Debt Levels Are Exploding, Finance Minister Warns

-

Spread & Containment7 days ago

Spread & Containment7 days agoIFM’s Hat Trick and Reflections On Option-To-Buy M&A

-

Uncategorized4 weeks ago

Uncategorized4 weeks agoAll Of The Elements Are In Place For An Economic Crisis Of Staggering Proportions

-

International2 weeks ago

International2 weeks agoEyePoint poaches medical chief from Apellis; Sandoz CFO, longtime BioNTech exec to retire

-

Uncategorized1 month ago

Uncategorized1 month agoCalifornia Counties Could Be Forced To Pay $300 Million To Cover COVID-Era Program

-

Uncategorized4 weeks ago

Uncategorized4 weeks agoApparel Retailer Express Moving Toward Bankruptcy

-

Uncategorized1 month ago

Uncategorized1 month agoIndustrial Production Decreased 0.1% in January

-

International2 weeks ago

International2 weeks agoWalmart launches clever answer to Target’s new membership program

-

Uncategorized1 month ago

Uncategorized1 month agoRFK Jr: The Wuhan Cover-Up & The Rise Of The Biowarfare-Industrial Complex