International

Destinations for portfolio investment in emerging economies: China is different

Since the 2008-2009 global financial crisis, international investors have shown increased appetite for bonds issued by emerging market and developing economies….

Share this:

By Gian Maria Milesi-Ferretti

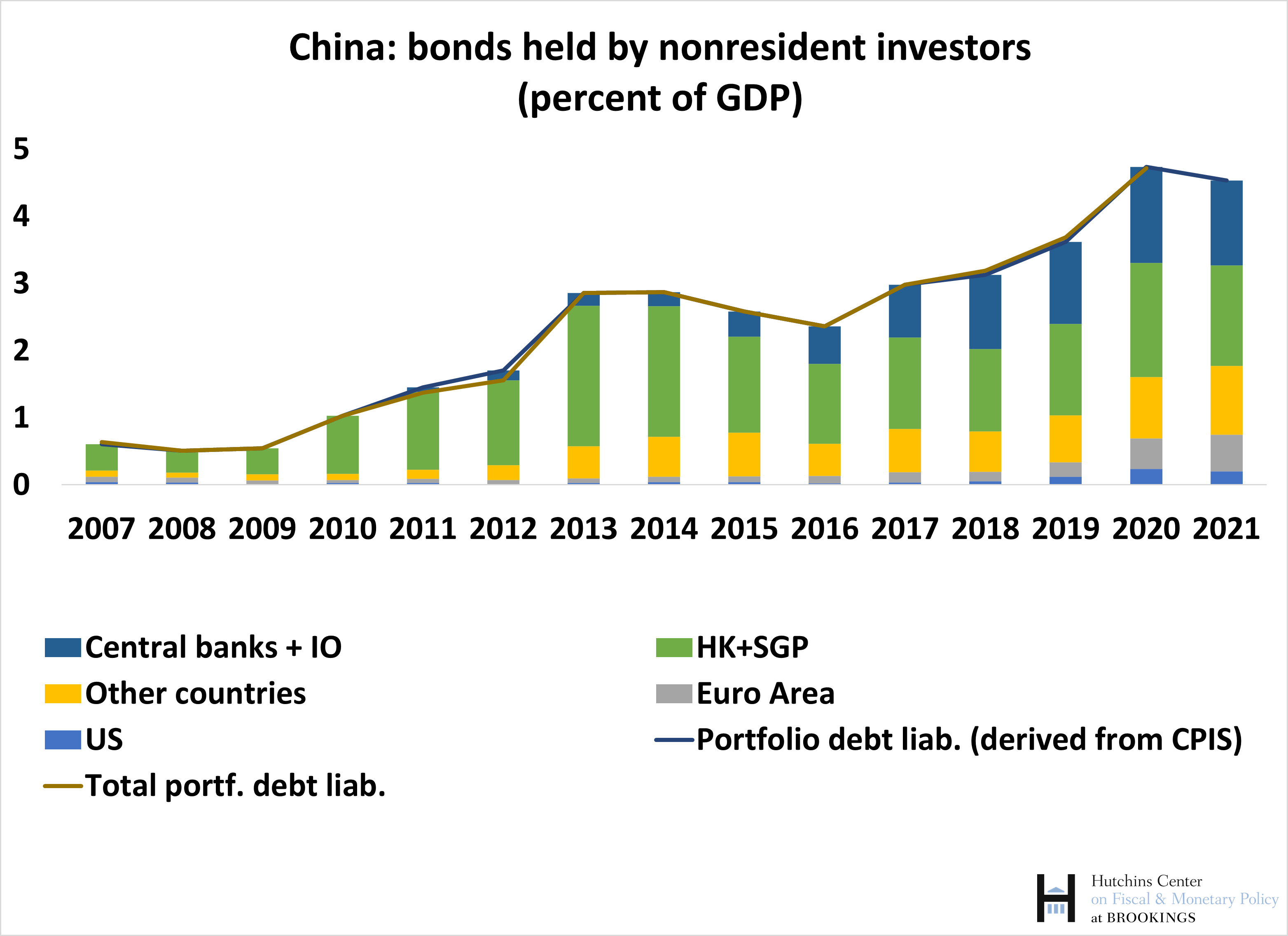

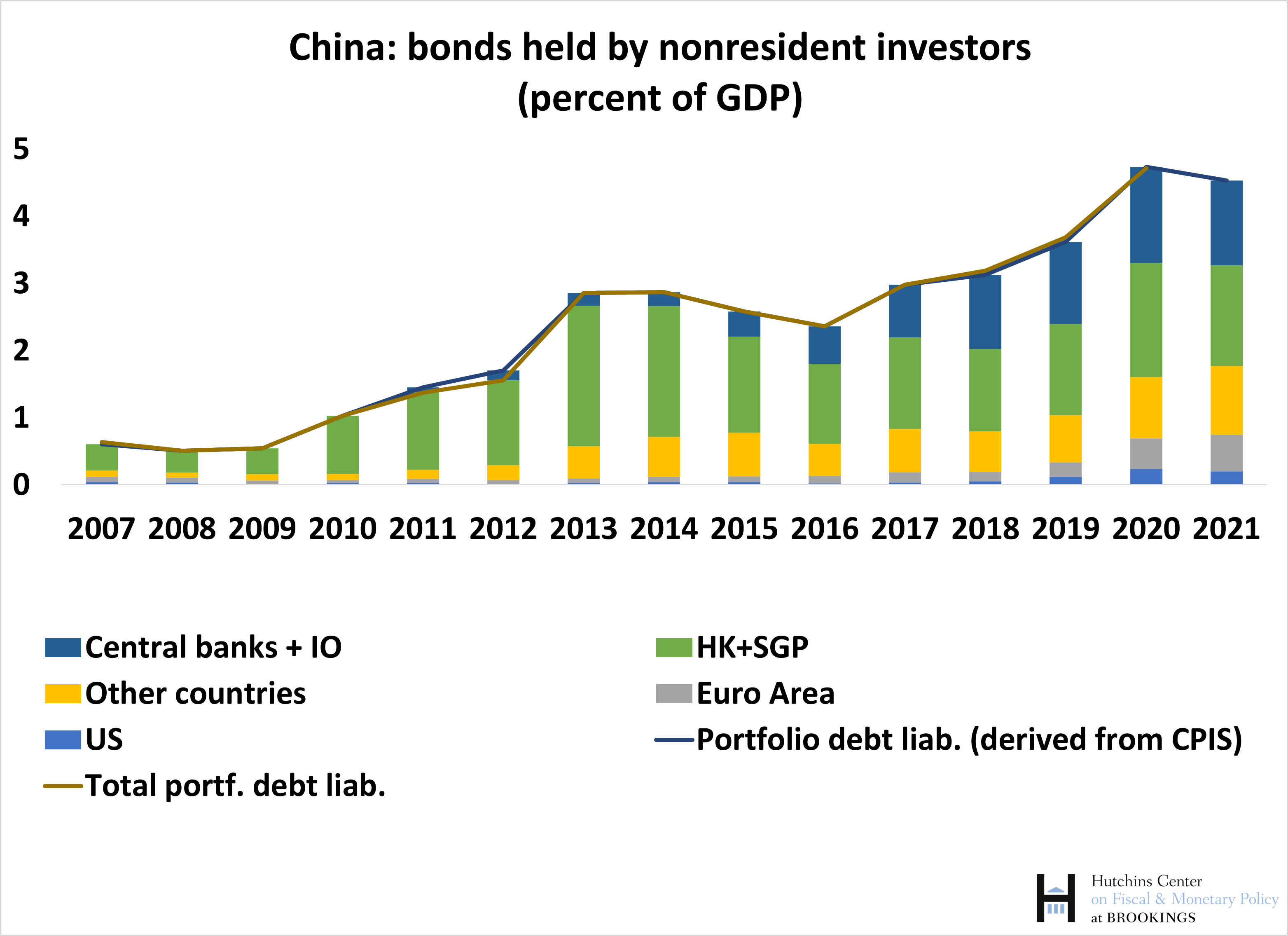

Since the 2008-2009 global financial crisis, international investors have shown increased appetite for bonds issued by emerging market and developing economies. The stock of bonds issued by their governments and corporations in the hands of international investors has risen from less than $1 trillion in 2009 to $3.5 trillion in 2021, according to our External Wealth of Nations database. Of particular note is the boom in international holdings of bonds issued by China, which were negligible in 2009 ($9 billion) and reached $788 billion at the end of 2021.

In a paper with Katharina Bergant and Martin Schmitz, we show that the largest holders of Chinese debt are Asian financial centers (especially Hong Kong and Singapore) and foreign central banks, including importantly Russia’s (chart).

The largest international investors—the United States and the euro area—play instead a much more modest role, even though their holdings have been increasing rapidly as well. The increase in foreign purchases of Chinese bonds—notable even as a share of rapidly rising Chinese GDP—reflect both the increased use of the Chinese renminbi as a reserve currency, following its inclusion in the International Monetary Fund’s SDR basket in 2016, and the increase in purchases of Chinese equities and bonds following China’s inclusion in major international indices in 2019.[1] Clearly holdings of international financial centers such as Hong Kong and Singapore will likely be on behalf of investors from other countries, and hence uncertainty remains on the nationality of the ultimate holders of these bonds.

In contrast, the majority of investment in bonds issued by countries such as Mexico, Brazil, Indonesia, Poland, and the Gulf states comes from advanced economies, with the euro area being the largest investor, followed by the United States (chart).

These holdings rose rapidly during the decade 2009-2019 and are higher in absolute terms ($2.7 trillion at end-2021, of which $2 trillion tracked by the CPIS) and as a share of the recipient countries’ GDP compared to holdings in China.

Using detailed information on sectors holding portfolio instruments including bonds shows the differences in the investors who hold Chinese bonds and those who hold bonds issued by other EMs. Estimates for holdings as of December of 2020 (chart) suggest that the largest investors are foreign central banks, followed by banks, while the shares held by investment funds and banks are broadly similar.[2]

In contrast, investment funds are by far the largest sector investing in bonds issued by EMs excluding China, followed by insurance companies and pension funds and then banks (chart).

The much lower presence of foreign central banks indicates that virtually the entirety of global foreign exchange reserves is held in advanced economies’ currencies or in renminbi.[3]

Offshore finance

Chinese corporate entities also issue a large amount of bonds through affiliates domiciled in financial centers (such as the Cayman Islands or the British Virgin Islands).[4] In general, firms choose this strategy for tax and regulatory reasons. For China, an additional incentive is the presence of capital controls that affect foreign access to local bond markets. The funds raised by these offshore affiliates are then channeled to the parent company via intercompany loans. Corporate bonds issued through offshore affiliates are mostly denominated in foreign currency (with a primary role for U.S. dollar issues), while bonds issued directly by onshore entities and held by nonresidents include government bonds, which are at least in part denominated in the domestic currency of the issuing country.

The stock of outstanding bonds issued through offshore affiliates exceeded $1 trillion as of December 2020, according to data from the Bank of International Settlements. This amount exceeds total foreign holdings of bonds issued directly by domestic Chinese entities, and is an order of magnitude larger than the amounts issued by Brazil, Russia, South Africa, and Gulf states (chart).

It is difficult to establish general patterns of ownership for those bonds—in surveys such as the CPIS, they are classified as bonds issued by, say, the Cayman Islands rather than China. However, data for the U.S. (as described in Bertaut, Bressler, and Curcuru, 2019) and the euro area (as shown in our paper) suggest that their holdings of bonds issued by offshore affiliates of Chinese corporate entities are broadly of the same order of magnitude as holdings of bonds issued directly by domestic Chinese entities, and therefore represent a relatively modest fraction of China’s offshore-issued bonds.[5] This relatively small share may have to do with the characteristics of the bonds, including the extent of disclosure required by major U.S. and European investment vehicles. It also raises the question of who the main investors in those instruments are, and whether they include resident Chinese investors as well.

In conclusion, foreign investors have been increasing their exposure to emerging market bonds over the past decade. At the same time, the investor base for Chinese bonds held overseas appears to be quite different from the one of the other main issuers, such as Brazil, Indonesia, Mexico, and Poland. Specifically, the weight of U.S. and euro area investors among all foreign investors is much smaller for China, where instead investors from Asia as well as foreign central banks (notably the Central Bank of Russia) play a larger role. Chinese corporate entities also issue a large amount of bonds through offshore affiliates. While it is difficult to establish general patterns of ownership for those bonds, existing data suggest that U.S. and euro area investors do not play a major role in that market either.

The evidence presented in this blog is a small slice of the work in the underlying paper. There we provide stylized facts on nonresident holdings of emerging market bonds and analyze the determinants of euro area investors’ purchases of such securities, using a comprehensive security-level dataset to track net transactions by euro area residents of individual bonds issued by emerging market economies. Euro area investors show a preference for euro-denominated and sovereign EM bonds. Net purchases tend to be higher when the macroeconomic outlook of the respective EMs improves, and U.S. monetary policy is loosened. Conversely, euro area investors—in particular, investment funds—sell emerging market debt when global financial stress is high. In a case study for the BRICS countries, we find that euro area investors treat EM bonds issued through offshore affiliates differently from onshore securities, likely reflecting differences in currency composition. The sell-offs of EM debt in 2018 as well as during the COVID-19 shock only affected securities issued directly by domestic entities, primarily in local currency, while euro area investors held on to securities issued through offshore affiliates.

[1] To link countries investing in EM bonds—and their investor sectors—to destination countries, we make use of data from the International Monetary Fund’s Coordinated Portfolio Investment Survey (CPIS) to help identify the residence of investors in emerging market securities. Countries participating to the survey, conducted annually between 2001 and 2012 and every 6 months thereafter, provide a breakdown by geographical destination of their holdings of foreign equities and bonds. The survey also provides the same breakdown for a group including participating central banks and international organizations. Aggregating investor holdings for each destination country enables us to construct a “derived” measure of bonds held by nonresidents (“portfolio debt liabilities” in balance of payments statistics). These derived liabilities are typically a bit lower than the corresponding liabilities reported by the destination country, given the incomplete investor coverage by the survey. At the same time, the participation to the survey of almost all large investor countries makes the data quite representative.

[2] Data for China rely on reported or estimated sectoral breakdowns for about 85 percent of total holdings identified in the CPIS. The calculation requires several assumptions. The most consequential one for China concerns Hong Kong (the largest investor in Chinese bonds). For that economy we don’t have a sectoral breakdown of its portfolio investment by country in CPIS, but we do have an aggregate breakdown of its total portfolio investment in bonds in its reported IIP. We apply the ratios derived from that breakdown to holdings in each individual destination country, including China. In particular, that breakdown indicates that deposit money banks account for 2/3 of total reported portfolio investment in bonds.

[3] For this group of countries, we can track or estimate investing sectors for over 90 percent of total bond holdings identified in the CPIS.

[4] Bonds may be issued on domestic markets or on international markets. What matters for their classification is the residence of the issuer—bonds issued by the government or a resident corporate entity and bought by a nonresident are classified as portfolio debt liabilities of the issuing country, while bonds issued by an affiliate of an EM corporate entity domiciled offshore are liabilities of the offshore center.

[5] Maggiori et al (2023) discuss in more detail the use of offshore affiliates by Chinese entities for equity and bond finance.

The Brookings Institution is financed through the support of a diverse array of foundations, corporations, governments, individuals, as well as an endowment. A list of donors can be found in our annual reports published online here. The findings, interpretations, and conclusions in this report are solely those of its author(s) and are not influenced by any donation.

bonds government bonds corporate bonds covid-19 equities monetary policy link currencies euro gdp singapore africa brazil mexico hong kong european poland russia chinaInternational

There will soon be one million seats on this popular Amtrak route

“More people are taking the train than ever before,” says Amtrak’s Executive Vice President.

Share this:

While the size of the United States makes it hard for it to compete with the inter-city train access available in places like Japan and many European countries, Amtrak trains are a very popular transportation option in certain pockets of the country — so much so that the country’s national railway company is expanding its Northeast Corridor by more than one million seats.

Related: This is what it's like to take a 19-hour train from New York to Chicago

Running from Boston all the way south to Washington, D.C., the route is one of the most popular as it passes through the most densely populated part of the country and serves as a commuter train for those who need to go between East Coast cities such as New York and Philadelphia for business.

Veronika Bondarenko

Amtrak launches new routes, promises travelers ‘additional travel options’

Earlier this month, Amtrak announced that it was adding four additional Northeastern routes to its schedule — two more routes between New York’s Penn Station and Union Station in Washington, D.C. on the weekend, a new early-morning weekday route between New York and Philadelphia’s William H. Gray III 30th Street Station and a weekend route between Philadelphia and Boston’s South Station.

More Travel:

- A new travel term is taking over the internet (and reaching airlines and hotels)

- The 10 best airline stocks to buy now

- Airlines see a new kind of traveler at the front of the plane

According to Amtrak, these additions will increase Northeast Corridor’s service by 20% on the weekdays and 10% on the weekends for a total of one million additional seats when counted by how many will ride the corridor over the year.

“More people are taking the train than ever before and we’re proud to offer our customers additional travel options when they ride with us on the Northeast Regional,” Amtrak Executive Vice President and Chief Commercial Officer Eliot Hamlisch said in a statement on the new routes. “The Northeast Regional gets you where you want to go comfortably, conveniently and sustainably as you breeze past traffic on I-95 for a more enjoyable travel experience.”

Here are some of the other Amtrak changes you can expect to see

Amtrak also said that, in the 2023 financial year, the Northeast Corridor had nearly 9.2 million riders — 8% more than it had pre-pandemic and a 29% increase from 2022. The higher demand, particularly during both off-peak hours and the time when many business travelers use to get to work, is pushing Amtrak to invest into this corridor in particular.

To reach more customers, Amtrak has also made several changes to both its routes and pricing system. In the fall of 2023, it introduced a type of new “Night Owl Fare” — if traveling during very late or very early hours, one can go between cities like New York and Philadelphia or Philadelphia and Washington. D.C. for $5 to $15.

As travel on the same routes during peak hours can reach as much as $300, this was a deliberate move to reach those who have the flexibility of time and might have otherwise preferred more affordable methods of transportation such as the bus. After seeing strong uptake, Amtrak added this type of fare to more Boston routes.

The largest distances, such as the ones between Boston and New York or New York and Washington, are available at the lowest rate for $20.

stocks pandemic japan europeanInternational

The next pandemic? It’s already here for Earth’s wildlife

Bird flu is decimating species already threatened by climate change and habitat loss.

Share this:

I am a conservation biologist who studies emerging infectious diseases. When people ask me what I think the next pandemic will be I often say that we are in the midst of one – it’s just afflicting a great many species more than ours.

I am referring to the highly pathogenic strain of avian influenza H5N1 (HPAI H5N1), otherwise known as bird flu, which has killed millions of birds and unknown numbers of mammals, particularly during the past three years.

This is the strain that emerged in domestic geese in China in 1997 and quickly jumped to humans in south-east Asia with a mortality rate of around 40-50%. My research group encountered the virus when it killed a mammal, an endangered Owston’s palm civet, in a captive breeding programme in Cuc Phuong National Park Vietnam in 2005.

How these animals caught bird flu was never confirmed. Their diet is mainly earthworms, so they had not been infected by eating diseased poultry like many captive tigers in the region.

This discovery prompted us to collate all confirmed reports of fatal infection with bird flu to assess just how broad a threat to wildlife this virus might pose.

This is how a newly discovered virus in Chinese poultry came to threaten so much of the world’s biodiversity.

The first signs

Until December 2005, most confirmed infections had been found in a few zoos and rescue centres in Thailand and Cambodia. Our analysis in 2006 showed that nearly half (48%) of all the different groups of birds (known to taxonomists as “orders”) contained a species in which a fatal infection of bird flu had been reported. These 13 orders comprised 84% of all bird species.

We reasoned 20 years ago that the strains of H5N1 circulating were probably highly pathogenic to all bird orders. We also showed that the list of confirmed infected species included those that were globally threatened and that important habitats, such as Vietnam’s Mekong delta, lay close to reported poultry outbreaks.

Mammals known to be susceptible to bird flu during the early 2000s included primates, rodents, pigs and rabbits. Large carnivores such as Bengal tigers and clouded leopards were reported to have been killed, as well as domestic cats.

Our 2006 paper showed the ease with which this virus crossed species barriers and suggested it might one day produce a pandemic-scale threat to global biodiversity.

Unfortunately, our warnings were correct.

A roving sickness

Two decades on, bird flu is killing species from the high Arctic to mainland Antarctica.

In the past couple of years, bird flu has spread rapidly across Europe and infiltrated North and South America, killing millions of poultry and a variety of bird and mammal species. A recent paper found that 26 countries have reported at least 48 mammal species that have died from the virus since 2020, when the latest increase in reported infections started.

Not even the ocean is safe. Since 2020, 13 species of aquatic mammal have succumbed, including American sea lions, porpoises and dolphins, often dying in their thousands in South America. A wide range of scavenging and predatory mammals that live on land are now also confirmed to be susceptible, including mountain lions, lynx, brown, black and polar bears.

The UK alone has lost over 75% of its great skuas and seen a 25% decline in northern gannets. Recent declines in sandwich terns (35%) and common terns (42%) were also largely driven by the virus.

Scientists haven’t managed to completely sequence the virus in all affected species. Research and continuous surveillance could tell us how adaptable it ultimately becomes, and whether it can jump to even more species. We know it can already infect humans – one or more genetic mutations may make it more infectious.

At the crossroads

Between January 1 2003 and December 21 2023, 882 cases of human infection with the H5N1 virus were reported from 23 countries, of which 461 (52%) were fatal.

Of these fatal cases, more than half were in Vietnam, China, Cambodia and Laos. Poultry-to-human infections were first recorded in Cambodia in December 2003. Intermittent cases were reported until 2014, followed by a gap until 2023, yielding 41 deaths from 64 cases. The subtype of H5N1 virus responsible has been detected in poultry in Cambodia since 2014. In the early 2000s, the H5N1 virus circulating had a high human mortality rate, so it is worrying that we are now starting to see people dying after contact with poultry again.

It’s not just H5 subtypes of bird flu that concern humans. The H10N1 virus was originally isolated from wild birds in South Korea, but has also been reported in samples from China and Mongolia.

Recent research found that these particular virus subtypes may be able to jump to humans after they were found to be pathogenic in laboratory mice and ferrets. The first person who was confirmed to be infected with H10N5 died in China on January 27 2024, but this patient was also suffering from seasonal flu (H3N2). They had been exposed to live poultry which also tested positive for H10N5.

Species already threatened with extinction are among those which have died due to bird flu in the past three years. The first deaths from the virus in mainland Antarctica have just been confirmed in skuas, highlighting a looming threat to penguin colonies whose eggs and chicks skuas prey on. Humboldt penguins have already been killed by the virus in Chile.

How can we stem this tsunami of H5N1 and other avian influenzas? Completely overhaul poultry production on a global scale. Make farms self-sufficient in rearing eggs and chicks instead of exporting them internationally. The trend towards megafarms containing over a million birds must be stopped in its tracks.

To prevent the worst outcomes for this virus, we must revisit its primary source: the incubator of intensive poultry farms.

Diana Bell does not work for, consult, own shares in or receive funding from any company or organisation that would benefit from this article, and has disclosed no relevant affiliations beyond their academic appointment.

genetic pandemic mortality spread deaths south korea south america europe uk chinaInternational

This is the biggest money mistake you’re making during travel

A retail expert talks of some common money mistakes travelers make on their trips.

Share this:

{kind=link}

Travel is expensive. Despite the explosion of travel demand in the two years since the world opened up from the pandemic, survey after survey shows that financial reasons are the biggest factor keeping some from taking their desired trips.

Airfare, accommodation as well as food and entertainment during the trip have all outpaced inflation over the last four years.

Related: This is why we're still spending an insane amount of money on travel

But while there are multiple tricks and “travel hacks” for finding cheaper plane tickets and accommodation, the biggest financial mistake that leads to blown travel budgets is much smaller and more insidious.

This is what you should (and shouldn’t) spend your money on while abroad

“When it comes to traveling, it's hard to resist buying items so you can have a piece of that memory at home,” Kristen Gall, a retail expert who heads the financial planning section at points-back platform Rakuten, told Travel + Leisure in an interview. “However, it's important to remember that you don't need every souvenir that catches your eye.”

More Travel:

- A new travel term is taking over the internet (and reaching airlines and hotels)

- The 10 best airline stocks to buy now

- Airlines see a new kind of traveler at the front of the plane

According to Gall, souvenirs not only have a tendency to add up in price but also weight which can in turn require one to pay for extra weight or even another suitcase at the airport — over the last two months, airlines like Delta (DAL) , American Airlines (AAL) and JetBlue Airways (JBLU) have all followed each other in increasing baggage prices to in some cases as much as $60 for a first bag and $100 for a second one.

While such extras may not seem like a lot compared to the thousands one might have spent on the hotel and ticket, they all have what is sometimes known as a “coffee” or “takeout effect” in which small expenses can lead one to overspend by a large amount.

‘Save up for one special thing rather than a bunch of trinkets…’

“When traveling abroad, I recommend only purchasing items that you can't get back at home, or that are small enough to not impact your luggage weight,” Gall said. “If you’re set on bringing home a souvenir, save up for one special thing, rather than wasting your money on a bunch of trinkets you may not think twice about once you return home.”

Along with the immediate costs, there is also the risk of purchasing things that go to waste when returning home from an international vacation. Alcohol is subject to airlines’ liquid rules while certain types of foods, particularly meat and other animal products, can be confiscated by customs.

While one incident of losing an expensive bottle of liquor or cheese brought back from a country like France will often make travelers forever careful, those who travel internationally less frequently will often be unaware of specific rules and be forced to part with something they spent money on at the airport.

“It's important to keep in mind that you're going to have to travel back with everything you purchased,” Gall continued. “[…] Be careful when buying food or wine, as it may not make it through customs. Foods like chocolate are typically fine, but items like meat and produce are likely prohibited to come back into the country.

Related: Veteran fund manager picks favorite stocks for 2024

stocks pandemic france

‘I couldn’t stand the pain’: the Turkish holiday resort that’s become an emergency dental centre for Britons who can’t get treated at home

Beloved mall retailer files Chapter 7 bankruptcy, will liquidate

Is the National Guard a solution to school violence?

Rand Paul Teases Senate GOP Leader Run – Musk Says “I Would Support”

The next pandemic? It’s already here for Earth’s wildlife

There will soon be one million seats on this popular Amtrak route

Chinese migration to US is nothing new – but the reasons for recent surge at Southern border are

The Grinch Who Stole Freedom

As the pandemic turns four, here’s what we need to do for a healthier future

This is the biggest money mistake you’re making during travel

-

Uncategorized3 weeks ago

Uncategorized3 weeks agoAll Of The Elements Are In Place For An Economic Crisis Of Staggering Proportions

-

Uncategorized1 month ago

Uncategorized1 month agoCathie Wood sells a major tech stock (again)

-

Uncategorized3 weeks ago

Uncategorized3 weeks agoCalifornia Counties Could Be Forced To Pay $300 Million To Cover COVID-Era Program

-

Uncategorized2 weeks ago

Uncategorized2 weeks agoApparel Retailer Express Moving Toward Bankruptcy

-

International3 days ago

International3 days agoEyePoint poaches medical chief from Apellis; Sandoz CFO, longtime BioNTech exec to retire

-

Uncategorized4 weeks ago

Uncategorized4 weeks agoIndustrial Production Decreased 0.1% in January

-

International3 days ago

International3 days agoWalmart launches clever answer to Target’s new membership program

-

Uncategorized3 weeks ago

Uncategorized3 weeks agoRFK Jr: The Wuhan Cover-Up & The Rise Of The Biowarfare-Industrial Complex