Uncategorized

Bitcoin And The Coming Energy Conundrum

Bitcoin And The Coming Energy Conundrum

Authored by ???????????????? “DR. DOOM” ????????₿???????????? via BombThrower.com,

Assessing…

Share this:

Authored by ???????????????? “DR. DOOM” ????????₿???????????? via BombThrower.com,

Assessing The Potential Of Bitcoin Mining In Energy Monetization

If trade is considered the lifeblood of an economy, then surely energy would mark the essence of life itself.

Without energy, then trade has no foundation to stand upon.

And yet, some seem intent on diminishing the capacity for the world to generate this very essence of an economy and of the world.

Thankfully, it seems that some are waking up and facing the music.

Woe Is We, Thx ESG

During the week of August 7th ratings agency S&P Global announced that it would no longer be using ESG scores to determine credit quality of public companies. A spokesperson for S&P Global also (quoted by Bloomberg) stated that their move to ‘not rely on ESG scores in credit ratings’ will not affect the company’s philosophies towards ESG goals, or how the organization assesses a firm’s creditworthiness.

This comes at an interesting time. After years of consistent aggravated PR campaigns against specifically oil and gas. With publicly stated concerted efforts to attempt to hamper O&G production and processing operations reality, it seems, is starting to finally set in. Time will tell what this pivot ultimately leads to with regards to the heightened polarity around ESG and the fixation on emissions and their implied impact on climate change.

There is one thing that I cannot help but get off my chest…

How boorishly cliche; to not be capable of seeing how irrational a tact may be, ignoring data and logic, until failure and mark-ed difficulty are staring us in the face. If there is a silver-lining here, I suppose it would be that this serves as evidence that we are still clutching on to our humanity. This capability of making silly mistakes that yield outlandish consequences proves that (at least so far) we haven’t completely turned into cyborgs yet. So… go us.

Now we not only need to undo all of the damage to public understanding that has been inflicted upon oil & gas, but we also need to explain how important hydrocarbons are to the production of renewables, and why a shortage in black gold is bad for everybody and has significant impacts on all forms of energy generation. Which it seems we are approaching more rapidly than we want to admit.

Choppy Waters for Oil

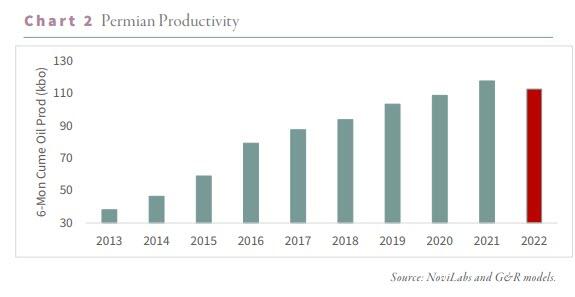

What really drives this point home is the report produced by Goehring & Rozencwajg (referred to as “G&R” going forward) on May 31st, 20233. Conventional non-OPEC oil production has markedly declined, while nonconventional non-OPEC (that basically means US Shale) production has stalled out, globally. The problem is that, according to G&R, the Permian Basin accounted for 75% of all nonconventional supply growth since 2016, globally – of the 7.4mm b/d the Permian supplied 5.4.

“Well, Mike, that’s just for non-OPEC production. You’re making it sound like it’s all doom and gloom, there’s still the OPEC producers.”

Yes you are correct. However, G&R are of the opinion that OPEC production has turned negative, an opinion that I have now heard from multiple different sources and also share (take that with a big helping of salt). This gives two reasons to be concerned about the previously stated production numbers:

1. If the majority of global supply growth was due to expansion in the Permian, and that has now passed, that suggests that supply and demand will continue to invert, and begin to pick up steam. Because, as G&R elaborate on, oil demand was forecasted to diminish after 2019 and instead has smacked back with a vengeance. And this isn’t just a “return to normal” situation, that demand is continuing to expand4. Meaning: energy prices should explode in such a scenario, making for the costs of quite literally everything more egregious. Ergo: the return of inflation and nauseating discussion volume over how real those measures are. Prepare yourselves.

2. If the supply growth stall is only on the non-OPEC side of the equation, that places America in a not-so-great tough spot. Our oil production has contributed to our prowess, and if we were to no longer be capable of continuing to expand access to our supply of oil, that removes a tool from our shed. And if you know anything about politik (and trade) you want every advantage at your disposal when things come to the negotiating table. NOW, lucky for the US is that (from my elementary understanding) we still have basins that we can lean on between California, Alaska, Louisiana, etc. However, these are much much smaller than Texas, and all together suggest by my back-of-the-napkin math ~20-25 billion barrels of potential production.

This leaves behind implications for everything as I stated with regards to the prices. But not just in the prices of goods like your food or the gasoline at the pump. This also has impacts on the expansion of all energy sources, both renewable and oil & gas. Solar panels and wind turbines require significant hydrocarbon inputs, let alone their batteries. The same goes for the production of transmission infrastructure – what brings the electricity to our homes and businesses. This further complicates the conversation around energy sourcing diversification as wind & solar have a problem with economics: they produce their greatest amounts of power outside of the peak demand window. This demand typically floods in between 2pm-8pm when families and individuals are returning home at the end of the day and powering on central air systems, TVs, computers, charging devices, video gaming systems, and various appliances.

Nuclear does not get away from this conversation either without taking some licks. Reactors require significant upfront investment, not just in capital but also in land and water. While reactors may not require nearly the amount of space as their solar and wind counterparts, they are still preferred to be built near water sources. As the power production does not come from the radiation from the fuel rods themselves, but by using that radiation to heat water and produce steam, which spins turbine blades, and those turbines generate the electricity. Oh and that water assists with heat dissipation. So yeah, you’re gonna want a lake or river nearby for that reactor… and building a manmade body of water is a feat that most would prefer to avoid.

Enter Bitcoin Mining, Stage Left.

Nuclear Mining

This is where the big orange “B” comes in with force. First, we will touch on the nuclear discussion as we were literally just there. Nuclear reactors can be limited in project viability as their prime locations can be quite the distance from communities and cities. Meaning that said operations would require significant transmission infrastructure investment to “tie in” to the grid and supply power. Which also means that it could be some time, and many hundreds of millions of $’s invested before the project is capable of earning a return, if the goldilocks environment is not available.

Bitcoin miners are uniquely positioned for this precise predicament. While a young reactor project is waiting for transmission infrastructure to be completed and connected, reactors could partner with bitcoin miners to “move in” and bunk-up on their operation by providing virtually immediate demand. Better yet, is that nuclear generation is consistent. Bitcoin mining’s energy demand is consistent. When operations are properly managed, and equipment is maintained, there is very little downtime required from either side of this equation.

What this provides is an avenue for rapid monetization of future nuclear projects. Things get even better when the grid gets tied-in to our generator; bitcoin miners can either be selected as persistent partners providing consistent demand and serving as a load balancer (like Riot and Marathon have been performing in Texas), or they can be asked to move on. Miners are effectively energy demand mercenaries.

CleanSpark (CLSK) serves as a great example of the success that is possible to an already established nuclear project that incorporates bitcoin mining as a service augmentation. Recently the CLSK team held their earnings call boasting great returns on the production of the bitcoin asset and their fully funded expansion project that will result in a 77% expansion in hashrate bringing the total forecasted hashrate to 16 EH/s5.

For those that are not versed in bitcoin mining terminology “hashrate” refers to the number of attempts that a bitcoin mining machine spits out in an attempt to discover the necessary solution to the current block of transactions. The vast majority of bitcoin miners utilize mining pools, a service that allows any number of mining organizations or individuals to dedicate their resources (hashrate) to work in a coordinated effort to discover that next fabled block. Because these services aggregate so much hashrate, and the likelihood of receiving a bitcoin subsidy is so much greater than working purely as individuals, these pools function by divvying up bitcoin returns according to the % of work done by each participant6. Providing a likelihood for a relatively consistent stream of income for the miners plugged in to said pools.

Now, another interesting aspect of CleanSpark’s latest earnings call was their numbers reported on their all-in power costs, coming in at a mere $0.041 kWh, which was an 11% reduction in their power costs from the prior quarter. CLSK attributes this cost reduction to their “active power management strategy.” Now, I do not know what that strategy could be in technical terms, but I am going to guess that it is a strategy that is effectively load balancing for the cities in which they operate; it only makes sense. That strategy would effectively reduce their cost of energy by not consuming during peak demand hours, also allowing for power prices to be reduced for the community during such timeframes.

CleanSpark even went so far as to further improve the quality of life for the community they have partnered with in Georgia. Matt Schultz, Vice Chairman at CleanSpark, shared that Washington, Georgia’s budget increased from $16 million to $30 million based solely on CleanSpark’s business activities7.

Wind & Solar Mining

There is little that actually needs to be said here. These energy sources are capable of benefiting from incorporating bitcoin mining in a very similar manner to nuclear. The difference being that, rather than responding strictly to demand, these renewables need to be capable of earning revenue outside of the peak power demand window. When your window of peak production is not matching up with the peak demand, additional strategies need to be sourced for revenue in order to cover the delta. Bitcoin mining covers that delta, and can go offline in response to any demands by the grid. Allowing the wind & solar operations to continue earning a solid revenue well outside of their locality’s peak demand window.

Conclusion

Look, I get it. Bitcoin has been an awfully cringe topic for almost everyone for the entirety of its existence. The community largely doesn’t help with that marketing and PR either. I get it. But we have to face the facts here, the world is changing and we are heading into a series of difficulties and complications that are going to require an upgrade to the incentivization of energy. I believe that mining bitcoin accomplishes that in ways that will change America, and the world, for the better. As I briefly described, mining the great orange asset provides a monetization strategy for all forms of energy generation, including oil and gas (which I have already touched on here). I very truly do not care if you call yourself a “bitcoiner.” I’ve never cared for tribalism or dogmas. But what I do care about is societal advancement and pushing towards a future of cheap and abundant energy.

It’s a world that I was promised as a child. And the world deserves its actualization. It may not be a “perfect” solution in your eyes, but I’ll be damned if it isn’t a better solution than everything else that is on offer currently.

Generate more energy, improve the condition of the world. Make some money while you’re at it.

* * *

Subscribe to the Bombthrower mailing list to get these posts as they come out (plus The CBDC Survival Guide when it’s ready), and follow Mike Hobart via his Substack and Twitter.

Uncategorized

February Employment Situation

By Paul Gomme and Peter Rupert The establishment data from the BLS showed a 275,000 increase in payroll employment for February, outpacing the 230,000…

Share this:

By Paul Gomme and Peter Rupert

The establishment data from the BLS showed a 275,000 increase in payroll employment for February, outpacing the 230,000 average over the previous 12 months. The payroll data for January and December were revised down by a total of 167,000. The private sector added 223,000 new jobs, the largest gain since May of last year.

Temporary help services employment continues a steep decline after a sharp post-pandemic rise.

Average hours of work increased from 34.2 to 34.3. The increase, along with the 223,000 private employment increase led to a hefty increase in total hours of 5.6% at an annualized rate, also the largest increase since May of last year.

The establishment report, once again, beat “expectations;” the WSJ survey of economists was 198,000. Other than the downward revisions, mentioned above, another bit of negative news was a smallish increase in wage growth, from $34.52 to $34.57.

The household survey shows that the labor force increased 150,000, a drop in employment of 184,000 and an increase in the number of unemployed persons of 334,000. The labor force participation rate held steady at 62.5, the employment to population ratio decreased from 60.2 to 60.1 and the unemployment rate increased from 3.66 to 3.86. Remember that the unemployment rate is the number of unemployed relative to the labor force (the number employed plus the number unemployed). Consequently, the unemployment rate can go up if the number of unemployed rises holding fixed the labor force, or if the labor force shrinks holding the number unemployed unchanged. An increase in the unemployment rate is not necessarily a bad thing: it may reflect a strong labor market drawing “marginally attached” individuals from outside the labor force. Indeed, there was a 96,000 decline in those workers.

Earlier in the week, the BLS announced JOLTS (Job Openings and Labor Turnover Survey) data for January. There isn’t much to report here as the job openings changed little at 8.9 million, the number of hires and total separations were little changed at 5.7 million and 5.3 million, respectively.

As has been the case for the last couple of years, the number of job openings remains higher than the number of unemployed persons.

Also earlier in the week the BLS announced that productivity increased 3.2% in the 4th quarter with output rising 3.5% and hours of work rising 0.3%.

The bottom line is that the labor market continues its surprisingly (to some) strong performance, once again proving stronger than many had expected. This strength makes it difficult to justify any interest rate cuts soon, particularly given the recent inflation spike.

unemployment pandemic unemploymentUncategorized

Mortgage rates fall as labor market normalizes

Jobless claims show an expanding economy. We will only be in a recession once jobless claims exceed 323,000 on a four-week moving average.

Share this:

Everyone was waiting to see if this week’s jobs report would send mortgage rates higher, which is what happened last month. Instead, the 10-year yield had a muted response after the headline number beat estimates, but we have negative job revisions from previous months. The Federal Reserve’s fear of wage growth spiraling out of control hasn’t materialized for over two years now and the unemployment rate ticked up to 3.9%. For now, we can say the labor market isn’t tight anymore, but it’s also not breaking.

The key labor data line in this expansion is the weekly jobless claims report. Jobless claims show an expanding economy that has not lost jobs yet. We will only be in a recession once jobless claims exceed 323,000 on a four-week moving average.

From the Fed: In the week ended March 2, initial claims for unemployment insurance benefits were flat, at 217,000. The four-week moving average declined slightly by 750, to 212,250

Below is an explanation of how we got here with the labor market, which all started during COVID-19.

1. I wrote the COVID-19 recovery model on April 7, 2020, and retired it on Dec. 9, 2020. By that time, the upfront recovery phase was done, and I needed to model out when we would get the jobs lost back.

2. Early in the labor market recovery, when we saw weaker job reports, I doubled and tripled down on my assertion that job openings would get to 10 million in this recovery. Job openings rose as high as to 12 million and are currently over 9 million. Even with the massive miss on a job report in May 2021, I didn’t waver.

Currently, the jobs openings, quit percentage and hires data are below pre-COVID-19 levels, which means the labor market isn’t as tight as it once was, and this is why the employment cost index has been slowing data to move along the quits percentage.

3. I wrote that we should get back all the jobs lost to COVID-19 by September of 2022. At the time this would be a speedy labor market recovery, and it happened on schedule, too

Total employment data

4. This is the key one for right now: If COVID-19 hadn’t happened, we would have between 157 million and 159 million jobs today, which would have been in line with the job growth rate in February 2020. Today, we are at 157,808,000. This is important because job growth should be cooling down now. We are more in line with where the labor market should be when averaging 140K-165K monthly. So for now, the fact that we aren’t trending between 140K-165K means we still have a bit more recovery kick left before we get down to those levels.

From BLS: Total nonfarm payroll employment rose by 275,000 in February, and the unemployment rate increased to 3.9 percent, the U.S. Bureau of Labor Statistics reported today. Job gains occurred in health care, in government, in food services and drinking places, in social assistance, and in transportation and warehousing.

Here are the jobs that were created and lost in the previous month:

In this jobs report, the unemployment rate for education levels looks like this:

- Less than a high school diploma: 6.1%

- High school graduate and no college: 4.2%

- Some college or associate degree: 3.1%

- Bachelor’s degree or higher: 2.2%

Today’s report has continued the trend of the labor data beating my expectations, only because I am looking for the jobs data to slow down to a level of 140K-165K, which hasn’t happened yet. I wouldn’t categorize the labor market as being tight anymore because of the quits ratio and the hires data in the job openings report. This also shows itself in the employment cost index as well. These are key data lines for the Fed and the reason we are going to see three rate cuts this year.

recession unemployment covid-19 fed federal reserve mortgage rates recession recovery unemploymentUncategorized

Inside The Most Ridiculous Jobs Report In History: Record 1.2 Million Immigrant Jobs Added In One Month

Inside The Most Ridiculous Jobs Report In History: Record 1.2 Million Immigrant Jobs Added In One Month

Last month we though that the January…

Share this:

{kind=link}

Last month we though that the January jobs report was the "most ridiculous in recent history" but, boy, were we wrong because this morning the Biden department of goalseeked propaganda (aka BLS) published the February jobs report, and holy crap was that something else. Even Goebbels would blush.

What happened? Let's take a closer look.

On the surface, it was (almost) another blockbuster jobs report, certainly one which nobody expected, or rather just one bank out of 76 expected. Starting at the top, the BLS reported that in February the US unexpectedly added 275K jobs, with just one research analyst (from Dai-Ichi Research) expecting a higher number.

{kind=link}

Some context: after last month's record 4-sigma beat, today's print was "only" 3 sigma higher than estimates. Needless to say, two multiple sigma beats in a row used to only happen in the USSR... and now in the US, apparently.

Before we go any further, a quick note on what last month we said was "the most ridiculous jobs report in recent history": it appears the BLS read our comments and decided to stop beclowing itself. It did that by slashing last month's ridiculous print by over a third, and revising what was originally reported as a massive 353K beat to just 229K, a 124K revision, which was the biggest one-month negative revision in two years!

Of course, that does not mean that this month's jobs print won't be revised lower: it will be, and not just that month but every other month until the November election because that's the only tool left in the Biden admin's box: pretend the economic and jobs are strong, then revise them sharply lower the next month, something we pointed out first last summer and which has not failed to disappoint once.

In the past month the Biden department of goalseeking stuff higher before revising it lower, has revised the following data sharply lower:

— zerohedge (@zerohedge) August 30, 2023

- Jobs

- JOLTS

- New Home sales

- Housing Starts and Permits

- Industrial Production

- PCE and core PCE

To be fair, not every aspect of the jobs report was stellar (after all, the BLS had to give it some vague credibility). Take the unemployment rate, after flatlining between 3.4% and 3.8% for two years - and thus denying expectations from Sahm's Rule that a recession may have already started - in February the unemployment rate unexpectedly jumped to 3.9%, the highest since February 2022 (with Black unemployment spiking by 0.3% to 5.6%, an indicator which the Biden admin will quickly slam as widespread economic racism or something).

And then there were average hourly earnings, which after surging 0.6% MoM in January (since revised to 0.5%) and spooking markets that wage growth is so hot, the Fed will have no choice but to delay cuts, in February the number tumbled to just 0.1%, the lowest in two years...

... for one simple reason: last month's average wage surge had nothing to do with actual wages, and everything to do with the BLS estimate of hours worked (which is the denominator in the average wage calculation) which last month tumbled to just 34.1 (we were led to believe) the lowest since the covid pandemic...

... but has since been revised higher while the February print rose even more, to 34.3, hence why the latest average wage data was once again a product not of wages going up, but of how long Americans worked in any weekly period, in this case higher from 34.1 to 34.3, an increase which has a major impact on the average calculation.

While the above data points were examples of some latent weakness in the latest report, perhaps meant to give it a sheen of veracity, it was everything else in the report that was a problem starting with the BLS's latest choice of seasonal adjustments (after last month's wholesale revision), which have gone from merely laughable to full clownshow, as the following comparison between the monthly change in BLS and ADP payrolls shows. The trend is clear: the Biden admin numbers are now clearly rising even as the impartial ADP (which directly logs employment numbers at the company level and is far more accurate), shows an accelerating slowdown.

But it's more than just the Biden admin hanging its "success" on seasonal adjustments: when one digs deeper inside the jobs report, all sorts of ugly things emerge... such as the growing unprecedented divergence between the Establishment (payrolls) survey and much more accurate Household (actual employment) survey. To wit, while in January the BLS claims 275K payrolls were added, the Household survey found that the number of actually employed workers dropped for the third straight month (and 4 in the past 5), this time by 184K (from 161.152K to 160.968K).

This means that while the Payrolls series hits new all time highs every month since December 2020 (when according to the BLS the US had its last month of payrolls losses), the level of Employment has not budged in the past year. Worse, as shown in the chart below, such a gaping divergence has opened between the two series in the past 4 years, that the number of Employed workers would need to soar by 9 million (!) to catch up to what Payrolls claims is the employment situation.

There's more: shifting from a quantitative to a qualitative assessment, reveals just how ugly the composition of "new jobs" has been. Consider this: the BLS reports that in February 2024, the US had 132.9 million full-time jobs and 27.9 million part-time jobs. Well, that's great... until you look back one year and find that in February 2023 the US had 133.2 million full-time jobs, or more than it does one year later! And yes, all the job growth since then has been in part-time jobs, which have increased by 921K since February 2023 (from 27.020 million to 27.941 million).

Here is a summary of the labor composition in the past year: all the new jobs have been part-time jobs!

But wait there's even more, because now that the primary season is over and we enter the heart of election season and political talking points will be thrown around left and right, especially in the context of the immigration crisis created intentionally by the Biden administration which is hoping to import millions of new Democratic voters (maybe the US can hold the presidential election in Honduras or Guatemala, after all it is their citizens that will be illegally casting the key votes in November), what we find is that in February, the number of native-born workers tumbled again, sliding by a massive 560K to just 129.807 million. Add to this the December data, and we get a near-record 2.4 million plunge in native-born workers in just the past 3 months (only the covid crash was worse)!

The offset? A record 1.2 million foreign-born (read immigrants, both legal and illegal but mostly illegal) workers added in February!

Said otherwise, not only has all job creation in the past 6 years has been exclusively for foreign-born workers...

... but there has been zero job-creation for native born workers since June 2018!

This is a huge issue - especially at a time of an illegal alien flood at the southwest border...

... and is about to become a huge political scandal, because once the inevitable recession finally hits, there will be millions of furious unemployed Americans demanding a more accurate explanation for what happened - i.e., the illegal immigration floodgates that were opened by the Biden admin.

Which is also why Biden's handlers will do everything in their power to insure there is no official recession before November... and why after the election is over, all economic hell will finally break loose. Until then, however, expect the jobs numbers to get even more ridiculous.

Wendy’s has a new deal for daylight savings time haters

Mortgage rates fall as labor market normalizes

Racial and Ethnic Wealth Inequality in the Post‑Pandemic Era

Wealth Inequality by Age in the Post‑Pandemic Era

People Who Received Ivermectin Were Better Off, Study Finds

Shipping company files surprise Chapter 7 bankruptcy, liquidation

Interest rates, the best it gets. It’s time to deploy cash

Is the biotech market rally real? Data suggest comeback in private, public markets

February Employment Situation

Wendy’s teases new $3 offer for upcoming holiday

-

Uncategorized2 weeks ago

Uncategorized2 weeks agoAll Of The Elements Are In Place For An Economic Crisis Of Staggering Proportions

-

Uncategorized1 month ago

Uncategorized1 month agoCathie Wood sells a major tech stock (again)

-

Uncategorized3 weeks ago

Uncategorized3 weeks agoCalifornia Counties Could Be Forced To Pay $300 Million To Cover COVID-Era Program

-

Uncategorized2 weeks ago

Uncategorized2 weeks agoApparel Retailer Express Moving Toward Bankruptcy

-

Uncategorized3 weeks ago

Uncategorized3 weeks agoIndustrial Production Decreased 0.1% in January

-

International2 days ago

International2 days agoWalmart launches clever answer to Target’s new membership program

-

International2 days ago

International2 days agoEyePoint poaches medical chief from Apellis; Sandoz CFO, longtime BioNTech exec to retire

-

Uncategorized3 weeks ago

Uncategorized3 weeks agoRFK Jr: The Wuhan Cover-Up & The Rise Of The Biowarfare-Industrial Complex