Charles Evans, president and chief executive officer of the Chicago Fed wants to run the economy hot.

The Benefits of Running Hot

In a headline that seems like it could be from The Onion or the Babylon Bee, please consider Chicago Fed president Charles Evans On the Benefits of Running the Economy Hot

In his speech Evans frequently refers to "r*" defined as the "equilibrium (or natural) real interest rate, or the rate consistent with full employment of the economy’s productive resources"

Let's now tune in to his thoughts. It was relatively lengthy speech by Evans. Here are the key snips.

It is an understatement to say that our current situation is complex: two years of Covid-19 distress; global supply chains in disarray; strong fiscal, monetary, and financial support; and 7-1/2 percent annual CPI inflation in the U.S.

But monetary policy is not the only game in town. Fiscal and regulatory policies will be crucial complementary tools in many cases—such as when aggregate demand is far too weak or financial excesses loom large. Importantly, these situations are more likely to arise in a low r* environment—when the proximity of the effective lower bound (ELB) reduces monetary policy capacity and investors’ views about potential returns may be at odds with the economy’s fundamentally lower average rate of return.

My view is that as long as the U.S. and global economies are in a low r* world, nominal interest rates will remain low and we will experience episodes close to or at the ELB. Unless the FOMC is to jettison our responsibility to promote maximum employment and price stability, the financial stability burden should be primarily on financial regulators.

Our present monetary policy setting is wrong-footed against the current, sharp increase in inflation. That is for sure. But the sources of these large relative price increases may be different from more typical cyclical inflation episodes. Furthermore, by my reading, underlying inflation appears to still be well anchored at levels consistent with the Fed’s average 2 percent objective, and so—unlike in the Volker and Greenspan eras—no extra monetary restraint is needed to bring trend inflation down. So I see our current policy situation as likely requiring less ultimate financial restrictiveness compared with past episodes and posing a smaller risk to the employment mandate than many times in the past.

As a monetary policymaker, I would cheer continued vibrancy for all segments of the labor market and hold off on potentially unnecessary policy restrictiveness until inflation began rising to levels that were incompatible with average 2 percent PCE inflation over time.

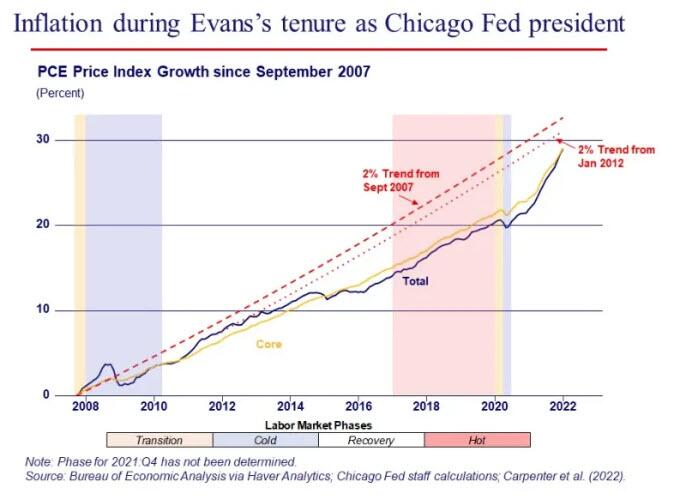

Indeed, as you can see from this chart [lead chart], we have been fighting this low inflation battle for nearly my entire tenure as Chicago Fed President. Even with the recent spike, the price level today is still 2-3/4 percent below a 2 percent trend line starting at 2007, when I got the job. It’s about 1-1/2 percent below a 2 percent trend line starting from 2012, when we formally adopted the 2 percent target. And this gap actually increased some during the “hot period” identified in the conference paper and shaded red on this chart.

This brings me to our current high inflation situation. Despite all the typical Evans dovishness I’ve just expounded, I agree the current stance of monetary policy is wrong-footed and needs substantial adjustment.

But how this plays out will be key for my monetary policy decision-making over the year. “Careful monitoring” will continue to be the watchwords.

Conclusion

So, to conclude, how should one come down on the question of whether running the economy hot is foolish—or when does it become foolish? Of course, the answer is it depends. It depends on how strong the relationship between growth and inflation is today, the dynamics of inflation expectations, the level of r*, and the associated proximity of the ELB. Or, if you don’t believe in Phillips curves, the question is largely moot because you aren’t going to worry about high employment generating inflation.

With regard to the policy situation today, I still see current inflation as largely being driven by unusual supply-side developments related to the Covid-19 shock. But inflation pressures clearly have widened in the broader economy to a degree that requires a substantial repositioning of monetary policy. What that repositioning ultimately will look like will depend a good deal on the same factors that enter the running-hot calculus.

Make Up for Past Insufficient Inflation

It's economic illiteracy to believe inflation is not running hot and has been for a long time.

Every person on the Fed is guilty of not understanding what inflation is. They are also all guilty of ignoring Fed-sponsored clear asset bubbles.

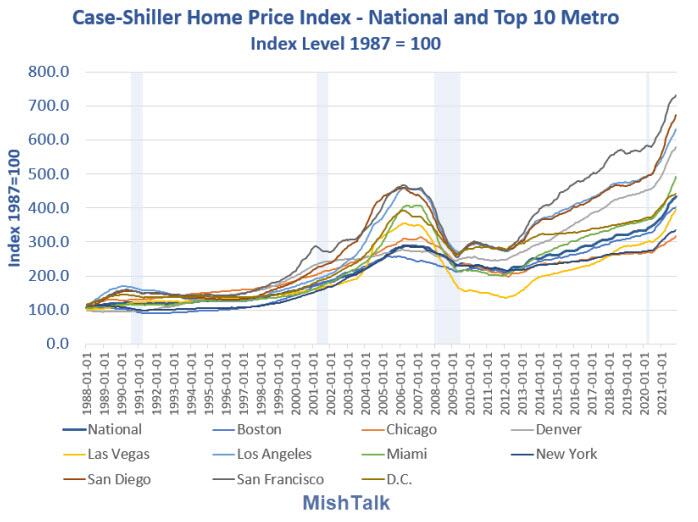

Case-Shiller Home Prices, data from Case-Shiller via St. Louis Fed, chart by Mish.

The Fed dunderheads do not count housing, crypto mania, or obvious stock market bubbles in their definition of inflation.

The fact is, we are currently in one of the four biggest bubbles of all time, the other three being 1929, the DotCom bubble in 2000, and the housing bubble in 2007.

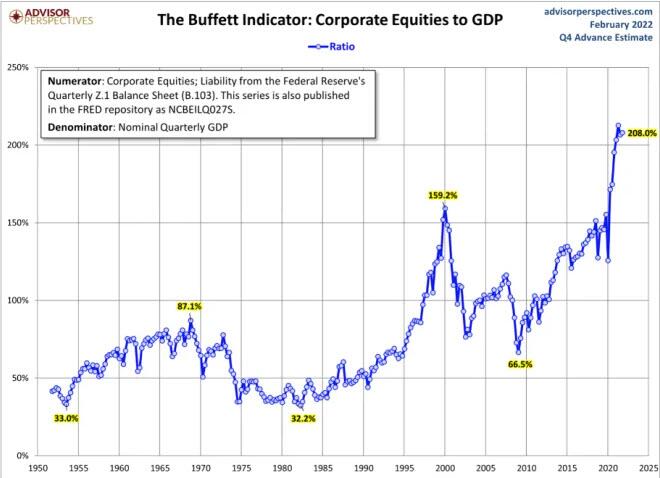

Buffett Indicator

The Buffett Indicator is a valuation multiple used to assess how expensive or cheap the aggregate stock market is at a given point in time. It was proposed as a metric by investor Warren Buffett in 2001, who called it "probably the best single measure of where valuations stand at any given moment", and its modern form compares the capitalization of the US Wilshire 5000 index to US GDP. It is widely followed by the financial media as a valuation measure for the US market in both its absolute, and detrended forms.

Former Fed chairs Janet Yellen and Ben Bernanke were both big Phillips Curve advocates despite the fact the theory never worked even according to Fed studies.

Concerns about deflation – falling prices of goods and services – are rooted in the view that it is very costly. We test the historical link between output growth and deflation in a sample covering 140 years for up to 38 economies. The evidence suggests that this link is weak and derives largely from the Great Depression. But we find a stronger link between output growth and asset price deflations, particularly during postwar property price deflations. We fail to uncover evidence that high debt has so far raised the cost of goods and services price deflations, in so-called debt deflations. The most damaging interaction appears to be between property price deflations and private debt.

Deflation may actually boost output. Lower prices increase real incomes and wealth. And they may also make export goods more competitive.

Once we control for persistent asset price deflations and country-specific average changes in growth rates over the sample periods, persistent goods and services (CPI ) deflations do not appear to be linked in a statistically significant way with slower growth even in the interwar period. They are uniformly statistically insignificant except for the first post-peak year during the postwar era – where, however, deflation appears to usher in stronger output growth. By contrast, the link of both property and equity price deflations with output growth is always the expected one, and is consistently statistically significant.

The Fed is hellbent on producing damaging inflation.

In the real world deflation boosts output. Falling prices make things more affordable and improve standards of living.

In one of the more accurate statements ever made by any Fed president, James Bullard, St. Louis Fed president recently stated "I think the inflation we are seeing is very bad for low and moderate-income households. Real wages are declining. People are unhappy. Consumer confidence is declining. This is not a good situation."

Bullard is no hero. He failed to dissent in any recent Fed meetings.

Asset Bubble Burst Coming

The Fed blew another enormous asset bubble, the biggest in history.

Payback is coming and the BIS described it well. The "link of both property and equity price deflations with output growth is always the expected one, and is consistently statistically significant."

S&P 500 - What is the Pain Threshold for the Fed and Traders?

ARPA-H appoints Etta Pisano to lead its Advancing Clinical Trials Readiness Initiative

The Advanced Research Projects Agency for Health (ARPA-H) has appointed Etta D. Pisano, MD, FACR, senior portfolio lead, to build the agency’s clinical…

The Advanced Research Projects Agency for Health (ARPA-H) has appointed Etta D. Pisano, MD, FACR, senior portfolio lead, to build the agency’s clinical trial portfolio and lead the ARPA-H Advancing Clinical Trials Readiness Initiative under ARPA-H Resilient Systems Mission Office Director Jennifer Roberts.

Credit: N/A

The Advanced Research Projects Agency for Health (ARPA-H) has appointed Etta D. Pisano, MD, FACR, senior portfolio lead, to build the agency’s clinical trial portfolio and lead the ARPA-H Advancing Clinical Trials Readiness Initiative under ARPA-H Resilient Systems Mission Office Director Jennifer Roberts.

The first radiologist to be appointed to such a role, Dr. Pisano is an internationally recognized expert in women’s health, breast cancer research, and the use of artificial intelligence in medical imaging applications.

“I am honored to be working for ARPA-H to identify and promote research that can improve healthcare quality, efficacy and delivery, and to improve patient care and access to clinical trials for all Americans, including women, rural residents, and the underserved,” said Dr. Pisano.

Dr. Pisano will continue to serve as study chair of the large-scale Tomosynthesis Mammographic Imaging Screening Trial (TMIST) for the ECOG-ACRIN Cancer Research Group (ECOG-ACRIN). TMIST is led by ECOG-ACRIN with funding from the National Cancer Institute, part of the National Institutes of Health. She will also continue to serve as the American College of Radiology® (ACR®) Chief Research Officer (CRO). Dr. Pisano previously served as the principal investigator of the landmark Digital Mammographic Imaging Screening Trial (DMIST).

The TMIST breast cancer screening study is among the fastest growing National Cancer Institute (NCI) trials of the COVID-19 era. Under Dr. Pisano’s leadership, TMIST is assembling one of the most diverse cancer screening trial populations ever. Approximately 21% of TMIST U.S. participants are Black—more than double the average rate for Black participation in NCI-funded clinical trials (9%).

With ARPA-H, Dr. Pisano will work to build underserved and minority participation in clinical trials—including identifying and onboarding rural facilities and those outside of large academic medical centers—such as emerging retail healthcare sites.

These duties are also very consistent with the missions of ECOG-ACRIN and ACR, which include promoting the exploration and identification of next-generation technologies that can benefit patients and providers.

“This is a great opportunity for Etta, and I’m excited about the impact she will make on our approach to clinical trials,” said Mitchell D. Schnall, MD, PhD, group co-chair of ECOG-ACRIN.

About ECOG-ACRIN

The ECOG-ACRIN Cancer Research Group (ECOG-ACRIN) is an expansive membership-based scientific organization that designs and conducts cancer research involving adults who have or are at risk of developing cancer. The Group comprises nearly 1400 member institutions and 21,000 research professionals in the United States and around the world. ECOG-ACRIN is known for advancing precision medicine and biomarker research through its leadership of major national clinical trials integrating cutting-edge genomic approaches. Member researchers and advocates collaborate across more than 40 scientific committees to design studies spanning the cancer care spectrum, from early detection to management of advanced disease. ECOG-ACRIN is funded primarily by the National Cancer Institute, part of the National Institutes of Health. Visit ecog-acrin.org, and follow us on X @eaonc, Facebook, LinkedIn, and Instagram.

Media Contact: Diane Dragaud, Director of Communications, communications@ecog-acrin.org.

Bacteria subtype linked to growth in up to 50% of human colorectal cancers, Fred Hutch researchers report

Researchers at Fred Hutchinson Cancer Center have found that a specific subtype of a microbe commonly found in the mouth is able to travel to the gut and…

Researchers at Fred Hutchinson Cancer Center have found that a specific subtype of a microbe commonly found in the mouth is able to travel to the gut and grow within colorectal cancer tumors. This microbe is also a culprit for driving cancer progression and leads to poorer patient outcomes after cancer treatment.

Credit: Fred Hutchinson Cancer Center

Researchers at Fred Hutchinson Cancer Center have found that a specific subtype of a microbe commonly found in the mouth is able to travel to the gut and grow within colorectal cancer tumors. This microbe is also a culprit for driving cancer progression and leads to poorer patient outcomes after cancer treatment.

The findings, published March 20 in the journal Nature, could help improve therapeutic approaches and early screening methods for colorectal cancer, which is the second most common cause of cancer deaths in adults in the U.S. according to the American Cancer Society.

Examining colorectal cancer tumors removed from 200 patients, the Fred Hutch team measured levels of Fusobacterium nucleatum, a bacterium known to infect tumors. In about 50% of the cases, they found that only a specific subtype of the bacterium was elevated in the tumor tissue compared to healthy tissue.

The researchers also found this microbe in higher numbers within stool samples of colorectal cancer patients compared with stool samples from healthy people.

“We’ve consistently seen that patients with colorectal tumors containing Fusobacterium nucleatum have poor survival and poorer prognosis compared with patients without the microbe,” explained Susan Bullman, Ph.D., Fred Hutch cancer microbiome researcher and co-corresponding study author. “Now we’re finding that a specific subtype of this microbe is responsible for tumor growth. It suggests therapeutics and screening that target this subgroup within the microbiota would help people who are at a higher risk for more aggressive colorectal cancer.”

In the study, Bullman and co-corresponding author Christopher D. Johnston, Ph.D., Fred Hutch molecular microbiologist, along with the study’s first author Martha Zepeda-Rivera, Ph.D., a Washington Research Foundation Fellow and Staff Scientist in the Johnston Lab, wanted to discover how the microbe moves from its typical environment of the mouth to a distant site in the lower gut and how it contributes to cancer growth.

First they found a surprise that could be important for future treatments. The predominant group of Fusobacterium nucleatum in colorectal cancer tumors, thought to be a single subspecies, is actually composed of two distinct lineages known as “clades.”

“This discovery was similar to stumbling upon the Rosetta Stone in terms of genetics,” Johnston explained. “We have bacterial strains that are so phylogenetically close that we thought of them as the same thing, but now we see an enormous difference between their relative abundance in tumors versus the oral cavity.”

By separating out the genetic differences between these clades, the researchers found that the tumor-infiltrating Fna C2 type had acquired distinct genetic traits suggesting it could travel from the mouth through the stomach, withstand stomach acid and then grow in the lower gastrointestinal tract. The analysis revealed 195 genetic differences between the clades.

Then, comparing tumor tissue with healthy tissue from patients with colorectal cancer, the researchers found that only the subtype Fna C2 is significantly enriched in colorectal tumor tissue and is responsible for colorectal cancer growth.

Further molecular analyses of two patient cohorts, including over 200 colorectal tumors, revealed the presence of this Fna C2 lineage in approximately 50% of cases.

The researchers also found in hundreds of stool samples from people with and without colorectal cancer that Fna C2 levels were consistently higher in colorectal cancer.

“We have pinpointed the exact bacterial lineage that is associated with colorectal cancer, and that knowledge is critical for developing effective preventive and treatment methods,” Johnston said.

He and Bullman believe their study presents significant opportunities for developing microbial cellular therapies, which use modified versions of bacterial strains to deliver treatments directly into tumors.

###

Fred Hutchinson Cancer Center unites individualized care and advanced research to provide the latest cancer treatment options while accelerating discoveries that prevent, treat and cure cancer and infectious diseases worldwide.

Based in Seattle, Fred Hutch is an independent, nonprofit organization and the only National Cancer Institute-designated cancer center in Washington. We have earned a global reputation for our track record of discoveries in cancer, infectious disease and basic research, including important advances in bone marrow transplantation, immunotherapy, HIV/AIDS prevention and COVID-19 vaccines. Fred Hutch operates eight clinical care sites that provide medical oncology, infusion, radiation, proton therapy and related services. Fred Hutch also serves as UW Medicine’s cancer program.

Journal

Nature

DOI

10.1038/s41586-024-07182-w

Method of Research

Observational study

Subject of Research

Human tissue samples

Article Title

A distinct Fusobacterium nucleatum clade dominates the colorectal cancer niche

Article Publication Date

20-Mar-2024

COI Statement

Note: Fred Hutch and its scientists who contributed to these discoveries may stand to benefit from their commercialization.

“Are you better off than you were four years ago?”

– by New Deal democratNo economic news today, so let me take a look at the supposed killer recent GOP meme that they claim is completely unanswerable:…

No economic news today, so let me take a look at the supposed killer recent GOP meme that they claim is completely unanswerable: “Are you better off today than you were four years ago?”

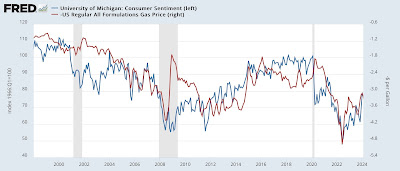

This is based primarily on consumer sentiment reading as well as polling that has consistently shown that most people think that the economy is poor, even though they rate their own situation as doing well. Dan Guild has a model comparing consumer sentiment with Presidential approval ratings. He concludes that Biden will lose re-election unless consumer sentiment as measured by the University of Michigan does not improve to the index level of 82.

As I’ve pointed out in the past, Presidential approval correlates quite well with the price of gas. Here’s the historical record updated through last month:

Except for those periods late in recessions and shortly thereafter, when the price of gas has typically declined sharply but the unemployment rate is very high, generally speaking, the lower the cost of gas, the higher the consumer sentiment. Interestingly, except for the early part of the 1990s, when gas prices were ridiculously low, the correlation holds better nominally than adjusted for income.

But perceptions aside, are most people in fact worse off than 4 years ago? Here are two ways of looking at that.

First, as I noted several months ago, Motio Research has produced very good monthly estimates of median household income, that track very well with the (unfortunately) annual measure, which is only reported in September of the next year (thus, for example, the most recent official report even now is for the year 2022). Here’s their update through February:

Note that they recommend (in the small print at the bottom) ignoring the results from March through October 2020, when response rates were very skewed. Leaving those out, only three months during Trump’s term were better than the current reading, and two of those, at 112.7, were equaled by January’s reading. Only February 2020 scored higher, at 112.9.

A second way of measuring is to compare real average and aggregate wages. Below I show average hourly wages (blue), average weekly wages (red), and aggregate payrolls divided by population (black), all deflated by the CPI, and normed to 100 as of February 2020:

Most of the surge in average hourly and weekly earnings in 2020 and early 2021 were compositional. That is, most of the workers laid off during the worst of the pandemic were low wage service workers, in places like restaurants, bars, and entertainment venues. When those workers were rehired during 2021 and 2022, the averages went down, with a very big assist from gas prices spiking to $5/gallon. Since then, both measures have exceeded their levels from just before the pandemic.

Aggregate payrolls, even divided by population, and so including everyone who is not working, and not even in the labor force, hit their pre-pandemic level late in 2021 and haven’t looked back. They are *not* affected by compositional issues. And they are currently 2.9% higher, even on this per capita basis, than they were just before the pandemic.

So the truthful answer for most people to “Are you better off than you were four years ago?” is by any reasonable measure, “Yes.”

We use cookies on our website to give you the most relevant experience by remembering your preferences and repeat visits. By clicking “Accept”, you consent to the use of ALL the cookies.

This website uses cookies to improve your experience while you navigate through the website. Out of these, the cookies that are categorized as necessary are stored on your browser as they are essential for the working of basic functionalities of the website. We also use third-party cookies that help us analyze and understand how you use this website. These cookies will be stored in your browser only with your consent. You also have the option to opt-out of these cookies. But opting out of some of these cookies may affect your browsing experience.

Necessary cookies are absolutely essential for the website to function properly. These cookies ensure basic functionalities and security features of the website, anonymously.

Cookie

Duration

Description

cookielawinfo-checbox-analytics

11 months

This cookie is set by GDPR Cookie Consent plugin. The cookie is used to store the user consent for the cookies in the category "Analytics".

cookielawinfo-checbox-functional

11 months

The cookie is set by GDPR cookie consent to record the user consent for the cookies in the category "Functional".

cookielawinfo-checbox-others

11 months

This cookie is set by GDPR Cookie Consent plugin. The cookie is used to store the user consent for the cookies in the category "Other.

cookielawinfo-checkbox-necessary

11 months

This cookie is set by GDPR Cookie Consent plugin. The cookies is used to store the user consent for the cookies in the category "Necessary".

cookielawinfo-checkbox-performance

11 months

This cookie is set by GDPR Cookie Consent plugin. The cookie is used to store the user consent for the cookies in the category "Performance".

viewed_cookie_policy

11 months

The cookie is set by the GDPR Cookie Consent plugin and is used to store whether or not user has consented to the use of cookies. It does not store any personal data.

Functional cookies help to perform certain functionalities like sharing the content of the website on social media platforms, collect feedbacks, and other third-party features.

Performance cookies are used to understand and analyze the key performance indexes of the website which helps in delivering a better user experience for the visitors.

Analytical cookies are used to understand how visitors interact with the website. These cookies help provide information on metrics the number of visitors, bounce rate, traffic source, etc.

Advertisement cookies are used to provide visitors with relevant ads and marketing campaigns. These cookies track visitors across websites and collect information to provide customized ads.

{kind=link}

{kind=link}