“World’s Most Bearish Hedge Fund” Goes Short Tech

"World’s Most Bearish Hedge Fund" Goes Short Tech

The world’s financial graveyards are covered with the career tombstones of those who, over the past decade, have called the end to a tech bubble that not only has yet to pop but has culminated

Share this:

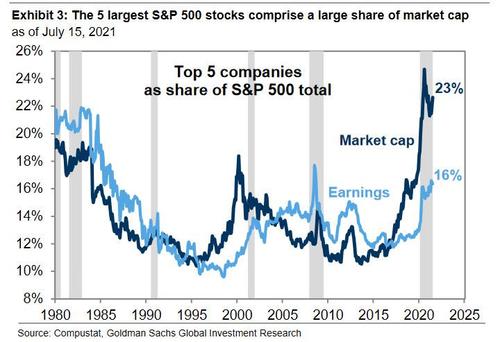

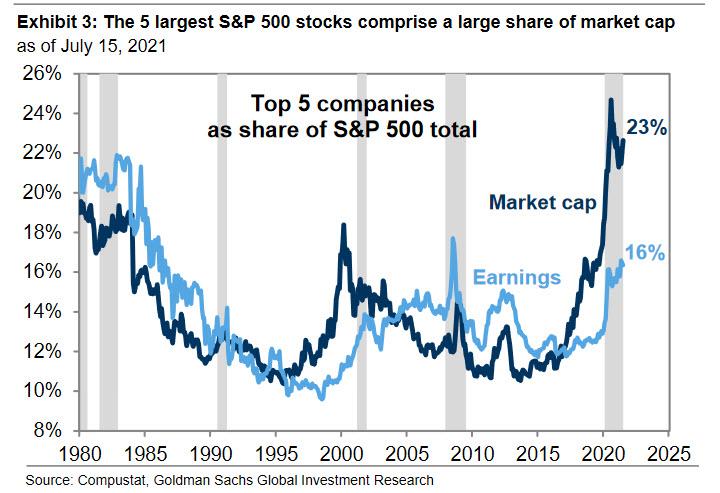

The world's financial graveyards are covered with the career tombstones of those who, over the past decade, have called the end to a tech bubble that not only has yet to pop but has culminated with just 5 tech names - the FAAMGs - comprising 23% of the S&P's market cap vastly surpassing the lofty dot com days, with a combined valuation of over $7 trillion.

Among those who were steamrolled by the tech juggernaut is Ned David Research, traditionally known for its accurate market timing calls if certainly not this time: two months ago it slapped a sell reco on tech right before it ripped the bears' faces off and embarked on a 14% rally. And then, just as the FAAMGs fell out of bed late last week, the firm’s strategists pulled a Gartman, and abandoned their underweight stance, expecting that the rotation out of reflation and into growth, coupled with a plunge in yields, will lead to more tech buying when we may well be facing the first market rout since March considering last week's coordinate selloff.

“The rapidly evolving COVID landscape, coupled with the Fed’s more hawkish tone at the June FOMC meeting” have “gone against cyclical Value sectors that tend to be positively correlated to interest rates and the yield curve,” said Ned Davis strategist Rob Anderson. “The progression of the virus will likely influence whether Growth or Value sectors gain the upper hand in the second half.”

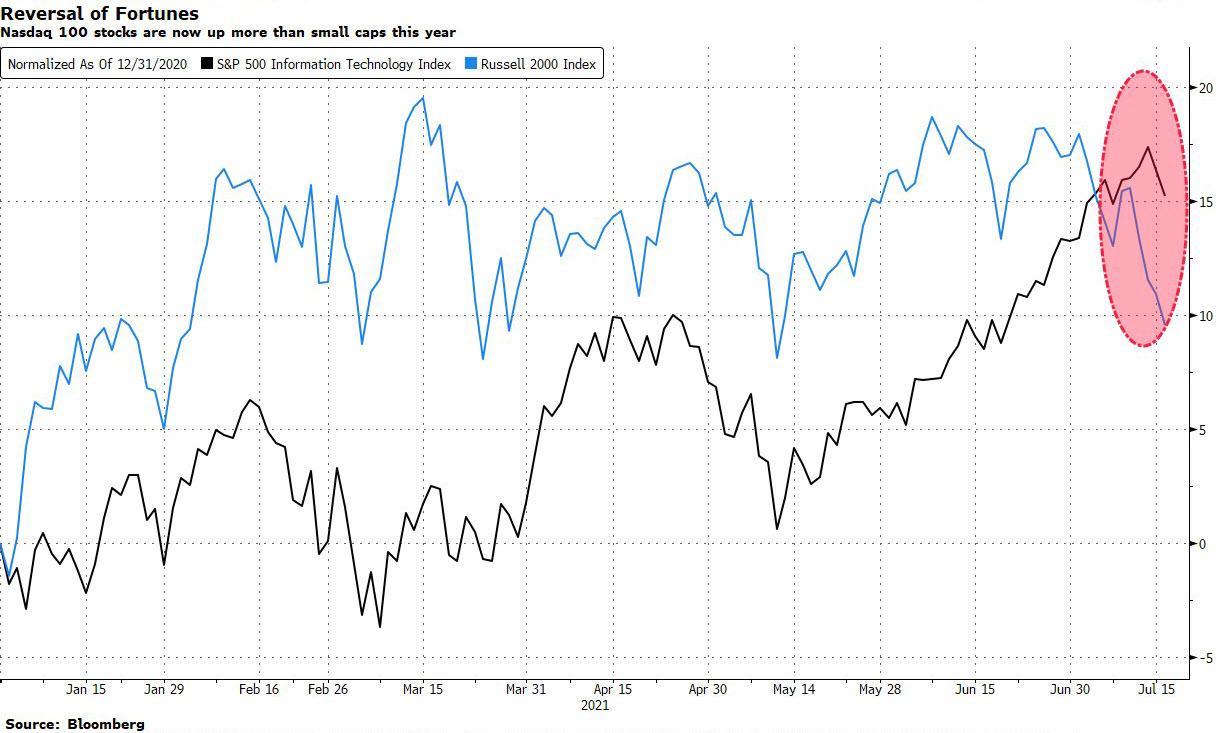

After trailing small-cap stocks which were the biggest beneficiaries of economic reopening, the Russell 100 Index erased its underperformance last Wednesday. The momentum continued this week, when small caps plunged 3.9%, while the Nasdaq 100 Index fell 0.2% and tech stocks in the S&P 500 added 0.4%.

As Bloomberg further notes, halfway into July, small caps trail their megacap peers by the most since March 2020, adding anxiety that a once-hot reflation trade is sputtering, with the delta variant of coronavirus quickly spreading and economic indicators moderating after a breakneck advance.

By abandonging its bearish bias, Ned Davis joins a host of Wall Street strategists who are currently bullish on tech including Goldman Sachs, Citigroup, UBS, Oppenheimer and JPMorgan, all of whom are overweight the sector while Deutsche Bank, Morgan Stanley, BMO, Bank of America and BTIG strategists are neutral on information technology.

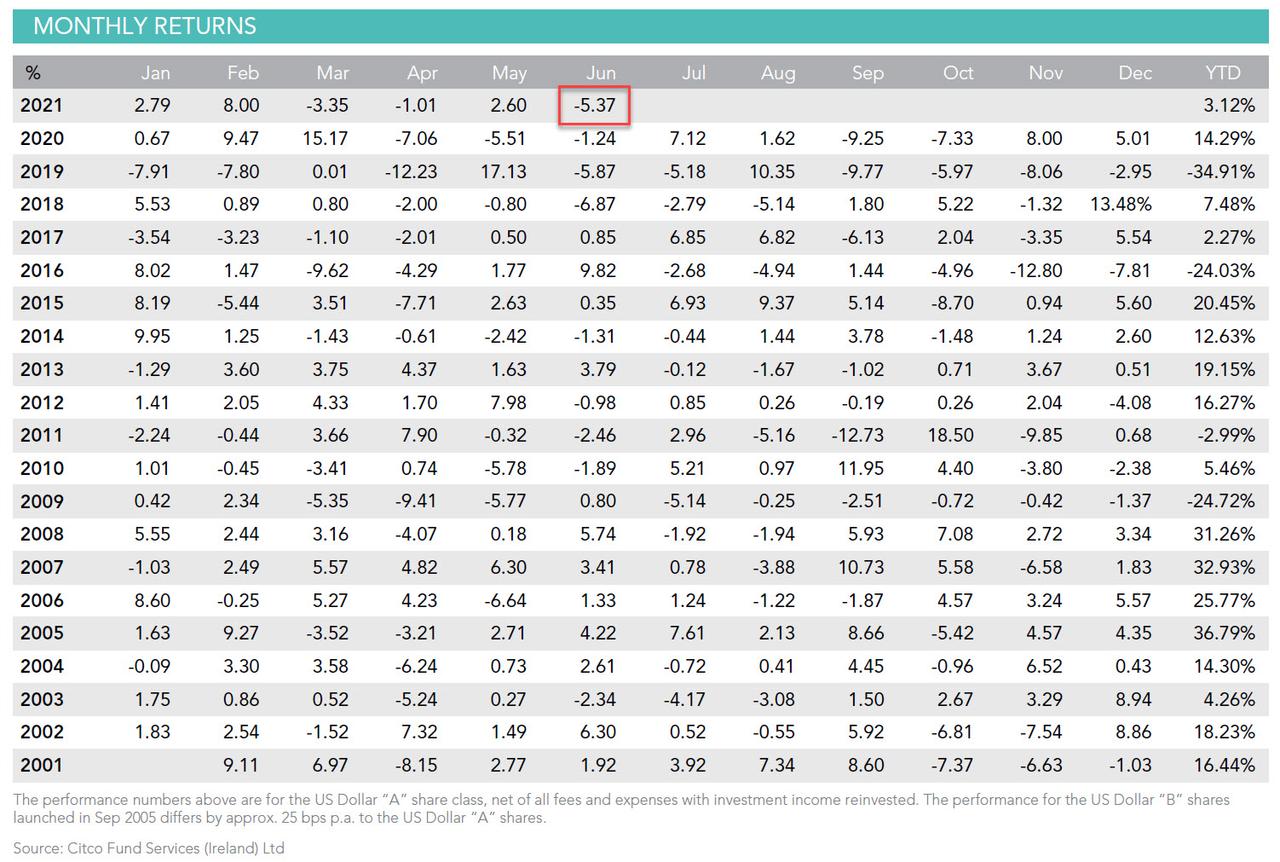

Yet as institutional strategists cover their bearish bets at the first sign of a substantial uptick, the mega bears crawl out of the woodwork, and in the world of bears (those that manage money) none is more familiar to our readers than Russell Clark, formerly of Horseman - which had earned the reputation of the world's most bearish hedge fund on these pages - and currently of Russell Clark Investment Management, who in his latest letter tells his patient investors that his fund, which is now down to just $296MM in AUM, had its worst month of the year in June when it dropped 5.37%...

... and may be en route to much more painful months if indeed the tech rally is just getting restarted. Why? Because as Clark says, "I am thinking of going net short in tech." The only question is where.

This is how Clark lays out the investment thesis:

First of all, I now understand why tech stocks, even loss-making ones, have been able to move such excessive valuations. Amazon showed that loss making companies capturing the consumer can build a monopoly position. Facebook shows even when firms abuse a monopoly position, the Federal Trade Commission (FTC) can only fine USD 5bn, and not force a breakup. A Supreme Court ruling in 2019 (Ohio v American Express) showed that the court only considers a company to be a monopoly if it raises prices to both its suppliers and its customers. In American Express’ case, it could charge high fees to retailers, but unless it could be proven that consumers suffered, the Supreme Court would do nothing to stop the abuse of market power. The potential implications of cases like these is that investors could find potential consumer facing monopolies, and force excessive valuations to make both capital raising and M&A easy (making it more likely companies are the dominant player). This has a knock-on effect of making M&A targets more attractive. You can see this effect in stocks like Tesla, Adobe, Slack, and it seems to be present in every 20 times sales loss making company I can find.

The question then, is "why should this end?"

Well, as mentioned last month, the US House of Representatives are keen to regulate big tech. But as mentioned above, the Supreme Court is still supportive of monopolies. So much so its dismissal of a lawsuit by the FTC against Facebook saw Facebook shares rally 5%. China has recently enacted very similar regulations against tech companies. And of course, in China government is king, with no Supreme Court to get in the way. The regulations, basically stop the two big tech oligopolies from favouring subsidiaries, has had a dramatic effect. Vipshop, TAL Education, Oriental Education and KE Holdings have all seen share prices break away from the Nasdaq, some falling 50% or more.

Taking this argument to its absurd extreme, Clark concludes that while Facebook, Amazon, Netflix and Facebook (FANG) stocks continue to rise, "it is beginning to look more difficult to invest in loss making stocks in the hope they can become a monopolist or be bought by a monopolist. The combination of the current US administration and the Chinese authoritarian government will ensure that every transaction will be scrutinised, and competition will be encouraged. For venture capital, this could be a disaster, particularly for those invested in Chinese start-ups. I am encouraged to take this view by the poor performance of Softbank, which has also diverged radically from the Nasdaq. The Softbank Vision Fund is the largest VC fund in the world, by quite a margin."

Going even further, Clark picks up on a point BofA CIO Michael Hartnett has been making for the past year, and claims that as China is attacking income inequality, he believes that Beijing is leading the world here, and is not an outlier:

Its policies are set to reduce liquidity in markets, keep a strong currency, whilst raising wages, and promote competition. These policies now seem to be taking hold, which means we are adjusting the fund’s portfolio.

In practical terms, this means that Clark has started to short Chinese tech, "as many of these companies seem to have no business strategy for making money" and he is also looking at loss making tech companies in the West whose exit strategy was M&A and shorting them as he believes that they are set to underperform.

At the same time, Clark will pair trade his growing tech short with agricultural related longs, "but we are going to hedge with liquidity driven assets that are being affected by Chinese monetary policy, namely crypto and gold."

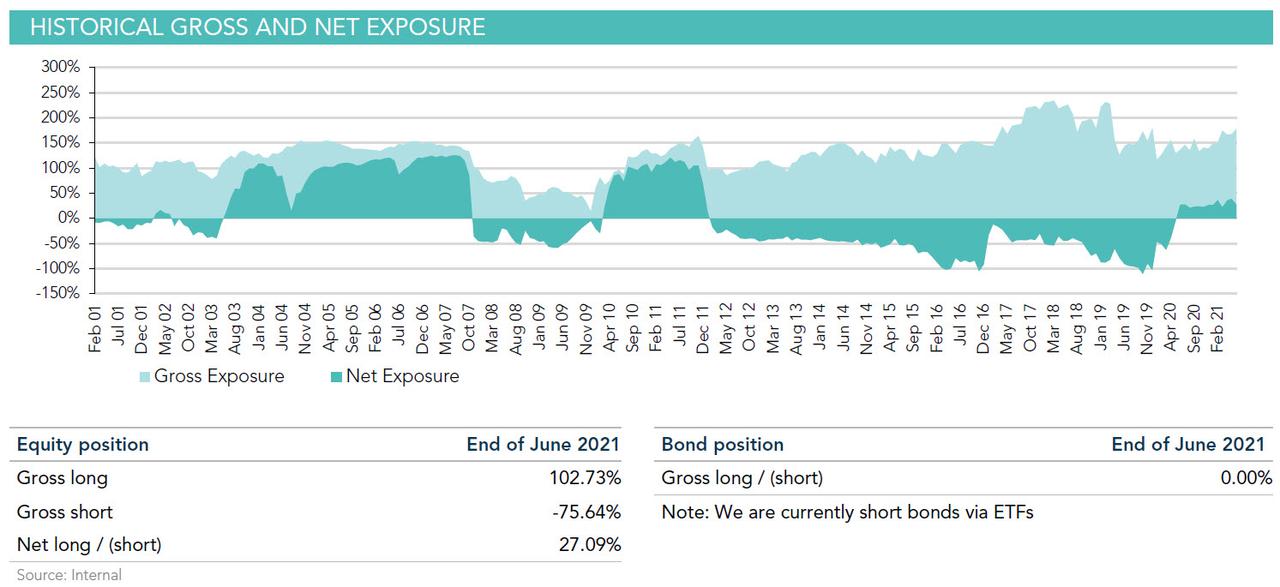

As a result, Clark concludes that he expects his fund - which has been net short for much of the past decade before briefly turning bullish around the time of the covid crisis helping its 14.3% return in 2020...

... once again "being mildly net short either this month or next month" as he is "long farmers, and short monopolists and proto monopolists."

While we wish Clark all the best, we would like to remind him that by going short tech he is not only fighting the central banks whose primary goal - above all else - is to prop up the wealth effect and nowhere do they have as much leverage as with the 5 companies which account for more than 20% of total market cap, but will also now be fighting the retail/reddit crowd which hones in like a heatseeker missile on any fund net short and then squeezes its biggest short holdings until the fund taps out (see Melvin). So while we wish Clark all the best - as we have for so many years - we can't help but wonder if the fund's AUM one year from now won't be in the double (or fewer) digits, if it's still around at all...

Spread & Containment

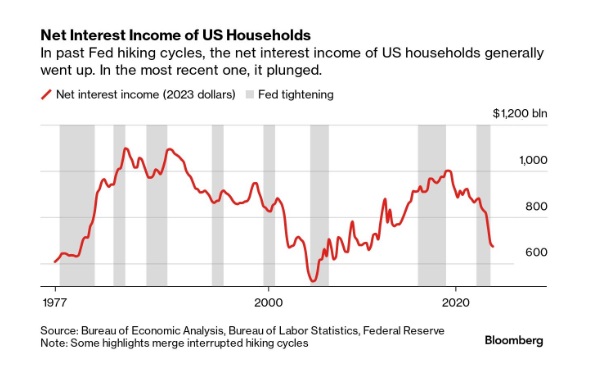

Household Net Interest Income Falls As Rates Spike

A Bloomberg article from this morning offered an excellent array of charts detailing the shifts in interest payment flows amid rising rates. The historical…

Share this:

A Bloomberg article from this morning offered an excellent array of charts detailing the shifts in interest payment flows amid rising rates. The historical anomaly was both surprising and contradicted our priors.

10 Key Points:

- Historical Anomaly: This is the first time in the last fifty years that a Federal Reserve rate hike cycle has led to a significant drop in household net interest income.

- Interest Expense Increase: Since the Fed began raising rates in March 2022, Americans’ annual interest expenses on debts like mortgages and credit cards have surged by nearly $420 billion.

- Interest Income Lag: The increase in interest income during the same period was only about $280 billion, resulting in a net decline in household interest income, a departure from past trends.

- Consumer Debt Influence: The recent rate hikes impacted household finances more because of a higher proportion of consumer credit, which adjusts more quickly to rate changes, increasing interest costs.

- Banks and Savers: Banks have been slow to pass on higher interest rates to depositors, and the prolonged period of low rates before 2022 may have discouraged savers from actively seeking better returns.

- Shift in Wealth: There’s been a shift from interest-bearing assets to stocks, with dividends surpassing interest payments as a source of unearned income during the pandemic.

- Distributional Discrepancy: Higher interest rates benefit wealthier individuals who own interest-earning assets, whereas lower-income earners face the brunt of increased debt servicing costs, exacerbating economic inequality.

- Job Market Impact: Typically, Fed rate hikes affect households through the job market, as businesses cut costs, potentially leading to layoffs or wage suppression, though this hasn’t occurred yet in the current cycle.

- Economic Impact: The distribution of interest income and debt servicing means that rate increases transfer money from those more likely to spend (and thus stimulate the economy) to those less likely to increase consumption, potentially dampening economic activity.

- No Immediate Relief: Expectations for the Fed to reduce rates have diminished, indicating that high-interest expenses for households may persist.

Uncategorized

One more airline cracks down on lounge crowding in a way you won’t like

Qantas Airways is increasing the price of accessing its network of lounges by as much as 17%.

Share this:

{kind=link}

Over the last two years, multiple airlines have dealt with crowding in their lounges. While they are designed as a luxury experience for a small subset of travelers, high numbers of people taking a trip post-pandemic as well as the different ways they are able to gain access through status or certain credit cards made it difficult for some airlines to keep up with keeping foods stocked, common areas clean and having enough staff to serve bar drinks at the rate that customers expect them.

In the fall of 2023, Delta Air Lines (DAL) caught serious traveler outcry after announcing that it was cracking down on crowding by raising how much one needs to spend for lounge access and limiting the number of times one can enter those lounges.

Related: Competitors pushed Delta to backtrack on its lounge and loyalty program changes

Some airlines saw the outcry with Delta as their chance to reassure customers that they would not raise their fees while others waited for the storm to pass to quietly implement their own increases.

Shutterstock

This is how much more you'll have to pay for Qantas lounge access

Australia's flagship carrier Qantas Airways (QUBSF) is the latest airline to announce that it would raise the cost accessing the 24 lounges across the country as well as the 600 international lounges available at airports across the world through partner airlines.

More Travel:

- A new travel term is taking over the internet (and reaching airlines and hotels)

- The 10 best airline stocks to buy now

- Airlines see a new kind of traveler at the front of the plane

Unlike other airlines which grant access primarily after reaching frequent flyer status, Qantas also sells it through a membership — starting from April 18, 2024, prices will rise from $600 Australian dollars ($392 USD) to $699 AUD ($456 USD) for one year, $1,100 ($718 USD) to $1,299 ($848 USD) for two years and $2,000 AUD ($1,304) to lock in the rate for four years.

Those signing up for lounge access for the first time also currently pay a joining fee of $99 AUD ($65 USD) that will rise to $129 AUD ($85 USD).

The airline also allows customers to purchase their membership with Qantas Points they collect through frequent travel; the membership fees are also being raised by the equivalent amount in points in what adds up to as much as 17% — from 308,000 to 399,900 to lock in access for four years.

Airline says hikes will 'cover cost increases passed on from suppliers'

"This is the first time the Qantas Club membership fees have increased in seven years and will help cover cost increases passed on from a range of suppliers over that time," a Qantas spokesperson confirmed to Simple Flying. "This follows a reduction in the membership fees for several years during the pandemic."

The spokesperson said the gains from the increases will go both towards making up for inflation-related costs and keeping existing lounges looking modern by updating features like furniture and décor.

While the price increases also do not apply for those who earned lounge access through frequent flyer status or change what it takes to earn that status, Qantas is also introducing even steeper increases for those renewing a membership or adding additional features such as spouse and partner memberships.

In some cases, the cost of these features will nearly double from what members are paying now.

stocks pandemicUncategorized

Star Wars icon gives his support to Disney, Bob Iger

Disney shareholders have a huge decision to make on April 3.

Share this:

Disney's (DIS) been facing some headwinds up top, but its leadership just got backing from one of the company's more prominent investors.

Star Wars creator George Lucas put out of statement in support of the company's current leadership team, led by CEO Bob Iger, ahead of the April 3 shareholders meeting which will see investors vote on the company's 12-member board.

"Creating magic is not for amateurs," Lucas said in a statement. "When I sold Lucasfilm just over a decade ago, I was delighted to become a Disney shareholder because of my long-time admiration for its iconic brand and Bob Iger’s leadership. When Bob recently returned to the company during a difficult time, I was relieved. No one knows Disney better. I remain a significant shareholder because I have full faith and confidence in the power of Disney and Bob’s track record of driving long-term value. I have voted all of my shares for Disney’s 12 directors and urge other shareholders to do the same."

Related: Disney stands against Nelson Peltz as leadership succession plan heats up

Lucasfilm was acquired by Disney for $4 billion in 2012 — notably under the first term of Iger. He received over 37 million in shares of Disney during the acquisition.

Lucas' statement seems to be an attempt to push investors away from the criticism coming from The Trian Partners investment group, led by Nelson Peltz. The group, owns about $3 million in shares of the media giant, is pushing two candidates for positions on the board, which are Peltz and former Disney CFO Jay Rasulo.

Peltz and Co. have called out a pair of Disney directors — Michael Froman and Maria Elena Lagomasino — for their lack of experience in the media space.

Related: Women's basketball is gaining ground, but is March Madness ready to rival the men's game?

Blackwells Capital is also pushing three of its candidates to take seats during the early April shareholder meeting, though Reuters has reported that the firm has been supportive of the company's current direction.

Disney has struggled in recent years amid the changes in media and the effects of the pandemic — which triggered the return of Iger at the helm in late 2022. After going through mass layoffs in the spring of 2023 and focusing on key growth brands, the company has seen a steady recovery with its stock up over 25% year-to-date and around 40% for the last six months.

Related: Veteran fund manager picks favorite stocks for 2024

stocks pandemic recovery

Google’s A.I. Fiasco Exposes Deeper Infowarp

Home buyers must now navigate higher mortgage rates and prices

Supreme Court Rules Public Officials May Block Their Constituents On Social Media

Greenback Surges after BOJ Hikes and Ends YCC and RBA Delivers a Dovish Hold

Manufacturing and construction vs. the still-inverted yield curve

When words make you sick

Student loan borrowers may finally get answers to loan forgiveness issues

You can strike gold and silver investment opportunities at Costco

Bolsonaro Indicted By Brazilian Police For Falsifying Covid-19 Vaccine Records

Germany Is Running Out Of Money And Debt Levels Are Exploding, Finance Minister Warns

-

Spread & Containment6 days ago

Spread & Containment6 days agoIFM’s Hat Trick and Reflections On Option-To-Buy M&A

-

Uncategorized4 weeks ago

Uncategorized4 weeks agoAll Of The Elements Are In Place For An Economic Crisis Of Staggering Proportions

-

International2 weeks ago

International2 weeks agoEyePoint poaches medical chief from Apellis; Sandoz CFO, longtime BioNTech exec to retire

-

Uncategorized1 month ago

Uncategorized1 month agoCalifornia Counties Could Be Forced To Pay $300 Million To Cover COVID-Era Program

-

Uncategorized4 weeks ago

Uncategorized4 weeks agoApparel Retailer Express Moving Toward Bankruptcy

-

Uncategorized1 month ago

Uncategorized1 month agoIndustrial Production Decreased 0.1% in January

-

International2 weeks ago

International2 weeks agoWalmart launches clever answer to Target’s new membership program

-

Uncategorized1 month ago

Uncategorized1 month agoRFK Jr: The Wuhan Cover-Up & The Rise Of The Biowarfare-Industrial Complex