Government

Why Canada should be paying attention to the brawl over inflation in U.S. economics establishment

The economics establishment in the United States has been putting on a show worthy of World Wrestling Entertainment this month.

Lawrence Summers

…

Share this:

The economics establishment in the United States has been putting on a show worthy of World Wrestling Entertainment this month.

Lawrence Summers , the former Democratic treasury secretary, and Olivier Blanchard , a similarly famous economist who once led the International Monetary Fund’s research department, created waves by going public with their worries that President Joe Biden’s US$1.9-trillion stimulus plan could cause inflation to blow past the Federal Reserve’s target of two per cent.

That’s not what Janet Yellen, the current treasury secretary, needed to hear. Summers and Blanchard sounded like the Republican minority in the Senate that could curb the Biden administration’s ambitions. They were supposed to be on her side.

“As treasury secretary, I have to worry about all of the risks to the economy,” Yellen, who, as a former Fed chair, is an intellectual heavyweight in her own right, said on CNN. “And the most important risk is that we leave workers and communities scarred by the pandemic and the economic toll that it’s taken, that we don’t do enough to address the pandemic and the public health issues, that we don’t get our kids back to school.”

Canada’s economic community is also split on whether inflation is a serious threat. However, it lacks stars such as Summers, so its members are mostly talking amongst themselves. That probably should change.

William White, a retired Canadian central banker who now ranks as a respected critic of his former profession, this week warned against assuming that the low inflation of the past couple of decades was the new steady state. Bond yields have been drifting higher, a sign that traders anticipate inflation. Climate change could be an inflationary force, and globalization, which has exerted downward pressure on prices for decades, has been slowed by resurgent nationalism in important economies, he said.

In other words, inflation may look contained, but the lid isn’t as secure as it used to be. “You can’t extrapolate past performance to future performance,” White, now a senior fellow at the C.D. Howe Institute, said during a virtual event hosted by the Global Risk Institute on Feb. 18.

Bank of Canada governor Tiff Macklem is in Yellen’s camp. He has made it clear that he is far more concerned about disinflation than he is about losing his grip on prices, a stance that was supported by Statistics Canada’s latest update of the Consumer Price Index this week.

The agency on Feb. 17 said the CPI increased one per cent in January from a year earlier, well short of the Bank of Canada’s target of about two per cent. There isn’t even a hint in the data that inflationary pressures are building. The central bank’s three “core” price measures, which cancel out noisier items in the CPI basket, averaged 1.5 per cent, a level that is “unlikely to concern the central bank,” Charles St-Arnaud, chief economist at Alberta Central, said.

Statistics Canada on Feb. 19 reported that retail sales dropped 3.4 per cent in December from the previous month, and 1.4 per cent in 2020 compared with 2019, additional evidence that the pandemic’s second wave has interrupted the recovery from the COVID-19 crisis.

The U.S. debate over inflation is interesting because it is a family feud, rather than yet another squabble between dovish liberals and hawkish conservatives. Blanchard and Summers have effectively accepted to play the heels in this drama, former heroes who suddenly and unexpectedly turned on their fans.

Summers is best known these days for having reintroduced the idea of “secular stagnation,” a condition in which savings pile up for lack of decent investment opportunities, resulting in meagre economic growth. His solution to the problem is a big increase in public investment, which is one of the reasons his critique of Biden’s plan was so surprising.

Blanchard disrupted conventional thinking about government deficits in 2019 by showing that growth will erode the debt over time, as long as borrowing costs are lower than the rate at which the economy expands, negating the assumption that new spending must be matched by tax increases and/or spending cuts. It was the weapon liberal policy-makers needed in their fight against knee-jerk austerity. Chrystia Freeland, Canada’s finance minister, cited Blanchard when she made the intellectual case for Prime Minister Justin Trudeau’s deficits last year.

And yet, Summers and Blanchard are now calling on Biden to show restraint, lest he wreck all that was accomplished by finally harnessing runaway inflation in the 1980s and 1990s. Their critique is multi-faceted, but, essentially, they argue that sending US$1,400 cheques to most Americans is unnecessarily generous, given that Congress just approved a US$900-billion stimulus program in December.

Their math suggests the hole left by the COVID-19 crisis simply isn’t that big, so the excess cash risks supercharging the recovery and putting the Fed in the position of having to explain why it’s letting inflation run hotter than its target, or jacking up interest rates to cool the economy, risking another recession. “I’d rather not go there,” Blanchard said in a blog post on Feb. 18.

Biden’s fiscal policy will have repercussions around the world, which is probably why Gita Gopinath, the IMF’s current chief economist, joined the inflation debate on Feb. 19.

Gopinath came down on the side of Yellen, arguing that the global economy remains too weak to stoke inflation pressures. She also said that increased automation would allow companies to keep prices low, as would the growing dominance of larger companies, since their fat profit margins will help absorb any increase in input costs.

All told, the IMF reckons Biden’s plan might cause inflation to rise to 2.25 per cent in 2022, “which is nothing to be concerned about,” Gopinath said.

• Email: kcarmichael@postmedia.com | Twitter: CarmichaelKevin

recession pandemic covid-19 stimulus economic growth fed federal reserve congress senate governor recovery interest rates stimulus canada albertaInternational

A popular vacation destination is about to get much more expensive

The entry fee to this destination known for its fauna has been unchanged since 1998.

Share this:

When visiting certain islands and other remote parts of the world, travelers need to be prepared to pay more than just the plane ticket and accommodation costs.

Particularly for smaller places grappling with overtourism, local governments will often introduce "tourist taxes" to go toward things like reversing ecological degradation and keeping popular attractions clean and safe.

Related: A popular European city is introducing the highest 'tourist tax' yet

Located 900 kilometers off the coast of Ecuador and often associated with the many species of giant turtles who call it home, the Galápagos Islands are not easy to get to (visitors from the U.S. often pass through Quito and then get on a charter flight to the islands) but are often a dream destination for those interested in seeing rare animal species in an unspoiled environment.

Shutterstock

This is how much you'll have to pay to visit the Galápagos Islands

While local authorities have been charging a $100 USD entry fee for all visitors to the islands since 1998, Ecuador's Ministry of Tourism announced that this number would rise to $200 for adults starting from August 1, 2024.

More Travel:

- A new travel term is taking over the internet (and reaching airlines and hotels)

- The 10 best airline stocks to buy now

- Airlines see a new kind of traveler at the front of the plane

According to the local tourism board, the increase has been prompted by the fact that record numbers of visitors since the pandemic have started taking a toll on the local environment. The islands are home to just 30,000 people but have been seeing nearly 300,000 visitors each year.

"It is our collective responsibility to protect and preserve this unparalleled ecosystem for future generations," Ecuador's Minister of Tourism Niels Olsen said in a statement. "The adjustment in the entry fee, the first in 26 years, is a necessary measure to ensure that tourism in the Galápagos remains sustainable and mutually beneficial to both the environment and our local communities."

These are the other countries which are raising (or adding) their tourist taxes

While the $200 applies to most international adult arrivals, there are some exceptions that can make one eligible for a lower rate. Adult citizens of the countries that make up the South American treaty bloc Mercosur will pay a $100 fee while children from any country will also get a discounted rate that is currently set at $50. Children under the age of two will continue to get free access.

In recent years, multiple countries and destinations have either raised or introduced new taxes for visitors. Thailand recently started charging all international visitors between 150 and 300 baht (up to $9 USD) that are put toward a sustainability budget while the Italian city of Venice is running a test in which it charges those coming into the city during the most popular summer weekends five euros.

Places such as Bali, the Maldives and New Zealand have been charging international arrivals a fee for years while Iceland's Prime Minister Katrín Jakobsdóttir hinted at plans to introduce something similar at the United Nations Climate Ambition Summit in 2023.

"Tourism has really grown exponentially in Iceland in the last decade and that obviously is not just creating effects on the climate," Jakobsdóttir told a Bloomberg reporter. "Most of our guests visit our unspoiled nature and obviously that creates a pressure."

stocks pandemic europeanInternational

Merck’s six-year deal strategy could deliver a blockbuster if hypertension drug is OK’d this month

With an FDA decision expected next week for its blood pressure drug sotatercept, Merck is hoping that its bundle of acquisitions in recent years will lead…

Share this:

With an FDA decision expected next week for its blood pressure drug sotatercept, Merck is hoping that its bundle of acquisitions in recent years will lead to multiple approvals and late-stage clinical wins.

The regulator is set to decide whether to approve the pulmonary arterial hypertension drug known as sotatercept by March 26. If approved, the drug could generate $1.9 billion in sales in 2025, according to Leerink Partners analyst Daina Graybosch.

The subcutaneous treatment came to Merck by way of its $11.5 billion acquisition of Acceleron in 2021.

“We viewed [Acceleron] as a great Merck-type company to own, especially with their legacy of R&D,” Sunil Patel, Merck’s head of corporate development and business development & licensing, said in an interview.

For the past few years, the pharma giant has been amassing help from external biotechs to broaden its pipeline and prepare for the looming patent deadline for Keytruda, the cancer immunotherapy that had $25 billion in sales last year. It’s Merck’s most notable treatment to come from external innovation; Organon made the drug, known then as pembrolizumab, and was bought by Schering-Plough, which merged with Merck in 2009.

Now, Merck is once again hoping a drug that it bet billions of dollars on will lead a spate of approvals out of its promising late-stage pipeline. The company has put at least $50 billion toward business development since 2018. Aside from Covid-19 treatment Lagevrio, which was authorized in late 2021 and developed with Ridgeback Biotherapeutics, Merck’s dealmaking over the past few years has not produced another blockbuster medicine.

In three months, Merck could have another approval in patritumab deruxtecan, an antibody-drug conjugate it’s developing with Daiichi Sankyo, in certain forms of non-small cell lung cancer. The FDA set a decision date of June 26. As part of the $4 billion upfront deal, Merck is co-developing and co-commercializing three antibody-drug conjugates with the ADC powerhouse.

Merck also expects a late-stage race with Roche in the inflammatory market, stemming from its $10.8 billion acquisition of Prometheus Biosciences last year. It began a Phase III of Prometheus’ lead drug, now called tulisokibart or MK-7240, in ulcerative colitis last fall. Meanwhile, the company also bagged a Phase I/II cancer drug via its more relatively modest $680 million acquisition of Harpoon Therapeutics earlier this year.

The acquisitions are likely to keep coming. Merck CEO Rob Davis said earlier this year the pharma is willing to spend as much as $15 billion on M&A.

It’s made more than 20 biotech acquisitions in the past 10 years, and that has led to at least 17 compounds that have been approved or are in mid- and late-stage development, Patel said.

“This current management team is deeply rooted in the legacy of this company. They understand the importance of building a long-term sustainable future, and they’re just not afraid to make the bold scientific bets,” he said.

Last year, Merck adjusted the way it calculates R&D spending to factor in M&A and licensing costs, and doing so catapulted the company to the top of Endpoints News’ 2023 pharma R&D expenditure list.

But not all deals have been smooth. Merck discontinued a Covid-19 treatment candidate from its 2020 acquisition of OncoImmune. And a chronic cough drug that it gained through its 2016 acquisition of Afferent Pharmaceuticals has twice been rejected by the FDA. The drug has been approved in Europe, Switzerland and Japan.

All told, Merck inks about 80 to 100 business development transactions per year, Patel said. That includes licensing pacts and early-stage collaborations, like a $1 billion biobuck-loaded deal for new biologics with Pearl Bio that it announced last week.

“Once we get through the science, we act decisively and very rapidly to bring the right type of BD structure,” said Patel, who’s been at Merck Research Laboratories for 25 years.

Dean Li

Dean LiAbout 80 employees search and evaluate potential transactions, which are then presented to a committee led by Dean Li, president of Merck Research Laboratories. Li joined Merck in 2017 from the University of Utah Health, where he co-founded biotechs such as Recursion and Hydra Biosciences.

“It’s seamless between Merck Research Labs and the BD unit. We’re just one simple group that operates with the one pipeline mentality,” Patel said.

About 60% of the Acceleron team remains at Merck.

“That’s a testament to how we can integrate these teams and how we embrace the science that we’re acquiring,” he said.

treatment fda covid-19 japan europeInternational

Key Events This Week: Central Banks Galore Including A Historic Rate Hike By The BOJ

Key Events This Week: Central Banks Galore Including A Historic Rate Hike By The BOJ

According to DB’s Jim Reid, "this could be a landmark…

Share this:

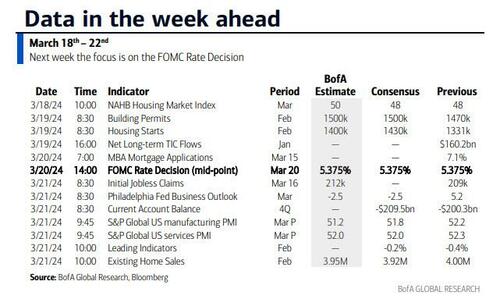

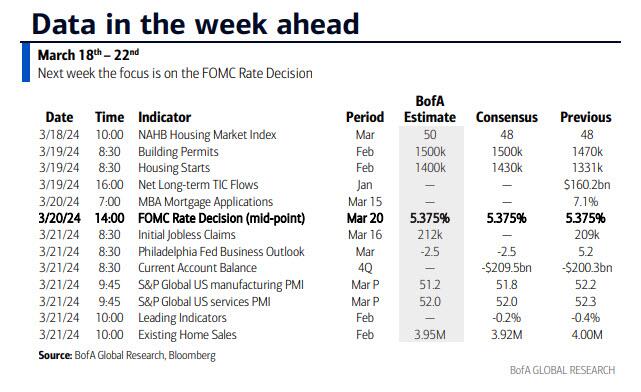

According to DB's Jim Reid, "this could be a landmark week in markets as the last global holdout on negative rates looks set to be removed as the BoJ likely hikes rates from -0.1% tomorrow." That will likely overshadow the FOMC that concludes on Wednesday that will have its own signalling intrigue given recent strong inflation. We also have the RBA meeting tomorrow and the SNB and BoE meetings on Thursday to close out a big week for global central bankers with many EM countries also deciding on policy. We’ll preview the main meetings in more depth below but outside of this we have the global flash PMIs on Thursday as well as inflation reports in Japan (Thursday) and the UK (Wednesday). US housing data also permeates through the week as you'll see in the full global day-by-day week ahead at the end as usual.

{kind=link}

Let’s go into detail now, starting with the BoJ tomorrow. We’ve had negative base rates now for 8 years which if is the longest run ever seen for any country in the history of mankind. In fact it is doubtful that pre-historic man was as generous as to charge negative interest rates on lending money prior to this! It also might be one of the longest global runs without any interest rate hikes given the 17 year run that could end tomorrow. So, as Reid puts it, a landmark event.

DB's Chief Japan economist expects the central bank to revise its policy and abandon both NIRP and the multi-tiered current account structure and set rates on all excess reserves at 0.1%. He also sees both the yield curve control (YCC) and the inflation-overshooting commitment ending, replaced by a benchmark for the pace of the bank’s JGB purchasing activity. The house view forecast of 50bps of hikes through 2025 is more hawkish than the market but risks are still tilted to the upside. On Friday, the Japan Trade Union Confederation (Rengo) announced the first tally of the results of this year's shunto spring wage negotiation. The wage increase rate, including the seniority-based wage hike, is 5.28%, which was significantly higher than expected. This year will probably see the highest wage settlements since 1991 which given Japan’s recent history is an incredible turnaround. This wage data news has firmed up expectations for tomorrow.

With regards to the FOMC which concludes on Wednesday, DB economists expect only minor revisions to the meeting statement that saw an overhaul last meeting. With regards to the SEP, the growth and unemployment forecasts are unlikely to change but the 2024 inflation forecasts potentially could; elsewhere, expect the Fed to revise up their 2024 core PCE inflation forecast by a tenth to 2.5%, although they see meaningful risks that it gets revised up even higher to 2.6%. In our economists' view, a 2.5% core PCE reading would allow just enough wiggle room to keep the 2024 fed funds rate at 4.6% (75bps of cuts). However, if core PCE inflation were revised up to 2.6%, it would likely entail the Fed moving their base case back to 50bps of cuts, as this would essentially reflect the same forecasts as the September 2023 SEP.

Beyond 2024, DB expect officials to build in less policy easing due to a higher r-star. If two of the eight officials currently at 2.5% move up by 25bps, then the long-run median forecast would edge up to 2.6%. This could be justified by a one-tenth upgrade to the long-run growth forecast. After all this information is released the presser from Powell will of course be heavily scrutinised, especially on how Powell sees recent inflation data. Powell should also provide an update on discussions around QT but it is unlikely they are ready yet to release updated guidance.

One additional global highlight this week might be a big fall in UK inflation on Wednesday, suggesting that headline CPI will slow to 3.4% (vs 4% in January) and core to 4.5% (5.1%). Elsewhere there is plenty of ECB speaker appearances including President Lagarde on Wednesday. They are all highlighted in the day-by-day guide at the end.

Courtesy of DB, here is a day-by-day calendar of events

Monday March 18

- Data: US March New York Fed services business activity, NAHB housing market index, China February retail sales, industrial production, property investment, Eurozone January trade balance, Canada February raw materials, industrial product price index, existing home sales

Tuesday March 19

- Data: US January total net TIC flows, February housing starts, building permits, Japan January capacity utilization, Germany and Eurozone March Zew survey, Eurozone Q4 labour costs, Canada February CPI

- Central banks: BoJ decision, ECB's Guindos speaks, RBA decision

- Auctions: US 20-yr Bond ($13bn, reopening)

Wednesday March 20

- Data: UK February CPI, PPI, RPI, January house price index, China 1-yr and 5-yr loan prime rates, Japan February trade balance, Italy January industrial production, Germany February PPI, Eurozone March consumer confidence, January construction output

- Central banks: Fed's decision, ECB's Lagarde, Lane, De Cos, Schnabel, Nagel and Holzmann speak, BoC summary of deliberations

- Earnings: Tencent, Micron

Thursday March 21

- Data: US, UK, Japan, Germany, France and Eurozone March PMIs, US March Philadelphia Fed business outlook, February leading index, existing home sales, Q4 current account balance, initial jobless claims, UK February public finances, Japan February national CPI, Italy January current account balance, France March manufacturing confidence, February retail sales, ECB January current account, EU27 February new car registrations

- Central banks: BoE decision, SNB decision

- Earnings: Nike, FedEx, Lululemon, BMW, Enel

- Auctions: US 10-yr TIPS ($16bn, reopening)

- Other: European Union summit, through March 22

Friday March 22

- Data: UK March GfK consumer confidence, February retail sales, Germany March Ifo survey, January import price index, Canada January retail sales

* * *

Finally, looking at just the US, Goldman notes that the key economic data releases this week are the Philadelphia Fed manufacturing index and existing home sales reports on Thursday. The March FOMC meeting is on Wednesday. The post-meeting statement will be released at 2:00 PM ET, followed by Chair Powell’s press conference at 2:30 PM. There are several speaking engagements from Fed officials this week, including Chair Powell, Vice Chair for Supervision Barr, and President Bostic.

Monday, March 18

- There are no major economic data releases scheduled.

Tuesday, March 19

- 08:30 AM Housing starts, February (GS +9.4%, consensus +7.4%, last -14.8%); Building permits, February (consensus +2.0%, last -0.3%)

Wednesday, March 20

- 02:00 PM FOMC statement, March 19 – March 20 meeting: As discussed in our FOMC preview, we continue to expect the committee to target a first cut in June, but we now expect 3 cuts in 2024 in June, September, and December (vs. 4 previously) given the slightly higher inflation path. We continue to expect 4 cuts in 2025 and now expect 1 final cut in 2026 to an unchanged terminal rate forecast of 3.25-3.5%. The main risk to our expectation is that FOMC participants might be more concerned about the recent inflation data and less convinced that inflation will resume its earlier soft trend. In that case, they might bump up their 2024 core PCE inflation forecast to 2.5% and show a 2-cut median.

Thursday, March 21

- 08:30 AM Current account balance, Q4 (consensus -$209.5bn, last -$200.3bn)

- 08:30 AM Philadelphia Fed manufacturing index, March (GS 3.2, consensus -1.3, last 5.2): We estimate that the Philadelphia Fed manufacturing index fell 2pt to 3.2 in March. While the measure is elevated relative to other surveys, we expect a boost from the rebound in foreign manufacturing activity and the pickup in US production and freight activity.

- 08:30 AM Initial jobless claims, week ended March 16 (GS 210k, consensus 215k, last 209k): Continuing jobless claims, week ended March 9 (consensus 1,815k, last 1,811k)

- 09:45 AM S&P Global US manufacturing PMI, March preliminary (consensus 51.8, last 52.2): S&P Global US services PMI, March preliminary (consensus 52.0, last 52.3)

- 10:00 AM Existing home sales, February (GS +1.2%, consensus -1.6%, last +3.1%)

- 02:00 PM Federal Reserve Vice Chair for Supervision Barr speaks: Federal Reserve Vice Chair Michael for Supervision Barr will participate in a fireside chat in Ann Arbor, MI with students and faculty. A moderated Q&A is expected. On February 14, Barr said the Fed is “confident we are on a path to 2% inflation,” but the recent report showing prices rose faster than anticipated in January “is a reminder that the path back to 2% inflation may be a bumpy one.” Barr also noted that “we need to see continued good data before we can begin the process of reducing the federal funds rate.”

Friday, March 22

- 09:00 AM Fed Reserve Chair Powell speaks: The Federal Reserve Board will host a Fed Listens event in Washington D.C. on “Transitioning to the Post-Pandemic Economy.” Chair Powell will deliver opening remarks. Vice Chair Phillip Jefferson and Fed Governor Michelle Bowman will moderate conversations with leaders from various organizations. On March 6, Chair Powell noted in his congressional testimony that if the economy evolves broadly as expected, it will likely be appropriate to begin dialing back policy restraint at some point this year.

- 12:00 PM Federal Reserve Vice Chair for Supervision Barr speaks: Federal Reserve Vice Chair for Supervision Michael Barr will participate in a virtual event on “International Economic and Monetary Design.” A moderated Q&A is expected.

- 04:00 PM Atlanta Fed President Bostic (FOMC voter) speaks: Atlanta Fed President Raphael Bostic will participate in a moderated conversation at the 2024 Household Finance Conference in Atlanta. On March 4, Bostic said, “I need to see more progress to feel fully confident that inflation is on a sure path to averaging 2% over time.” Bostic also noted, “I expect the first interest rate cut, which I have penciled in for the third quarter, will be followed by a pause in the following meeting.”

Source: DB, Goldman, BofA

Mistakes Were Made

Home buyers must now navigate higher mortgage rates and prices

Supreme Court Rules Public Officials May Block Their Constituents On Social Media

“Extreme Events”: US Cancer Deaths Spiked In 2021 And 2022 In “Large Excess Over Trend”

Harvard Medical School Professor Was Fired Over Not Getting COVID Vaccine

Germany Is Running Out Of Money And Debt Levels Are Exploding, Finance Minister Warns

You can strike gold and silver investment opportunities at Costco

TikTok Ban Obscures Chinese Stock Gold Rush

AI vs. elections: 4 essential reads about the threat of high-tech deception in politics

Free school meals for all may reduce childhood obesity, while easing financial and logistical burdens for families and schools

-

Uncategorized4 weeks ago

Uncategorized4 weeks agoAll Of The Elements Are In Place For An Economic Crisis Of Staggering Proportions

-

Spread & Containment5 days ago

Spread & Containment5 days agoIFM’s Hat Trick and Reflections On Option-To-Buy M&A

-

International1 week ago

International1 week agoEyePoint poaches medical chief from Apellis; Sandoz CFO, longtime BioNTech exec to retire

-

Uncategorized1 month ago

Uncategorized1 month agoCalifornia Counties Could Be Forced To Pay $300 Million To Cover COVID-Era Program

-

Uncategorized3 weeks ago

Uncategorized3 weeks agoApparel Retailer Express Moving Toward Bankruptcy

-

Uncategorized1 month ago

Uncategorized1 month agoIndustrial Production Decreased 0.1% in January

-

International1 week ago

International1 week agoWalmart launches clever answer to Target’s new membership program

-

Uncategorized1 month ago

Uncategorized1 month agoRFK Jr: The Wuhan Cover-Up & The Rise Of The Biowarfare-Industrial Complex