Just recently in our “Daily Market Commentary”(subscribe for free), we discussed Wall Street setting its sights on S&P 5000.

“Wells Fargo’s Chris Harvey raised his year-end S&P 500 price target to 4,825 from 3,850, as reported by Bloomberg’s Lu Wang. This move follows a weekend note by David Lefkowitz, head of equities for the Americas at UBS Wealth Management, who raised his year-end price target for the S&P 500 to 4,600 from 4,500.

Lefkowitz also raised his June 2022 price target to 4,800 from 4,650, with the real headline coming from his year-end 2022 S&P 500 price target — 5,000.

‘Yes, the rally off the COVID-19 bottom in March 2020 has been extraordinary, but we think there are further gains ahead,’ Lefkowitz writes. ‘Solid economic and corporate profit growth, in conjunction with a still-accommodative Fed, means that the environment for stocks remains favorable. As a result of our higher EPS estimates, we raise our targets for the S&P 500 for December 2021 by 100 points to 4,600 and June 2022 by 150 points to 4,800. We initiate our December 2022 target of 5,000, representing about 13% price appreciation from current levels.’” – Yahoo

The Race To 5000

Considering the marketalready doubled from the pandemic lows, the escalation of price targets is not surprising. Such is particularly the case when Wall Street needs to sell products to retail investors.

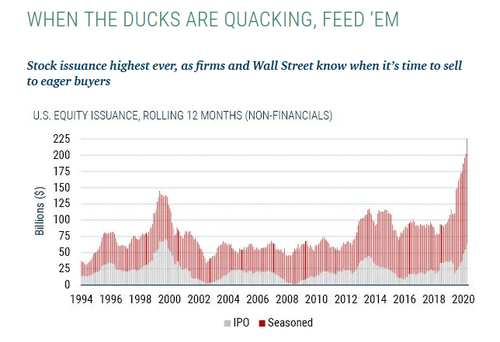

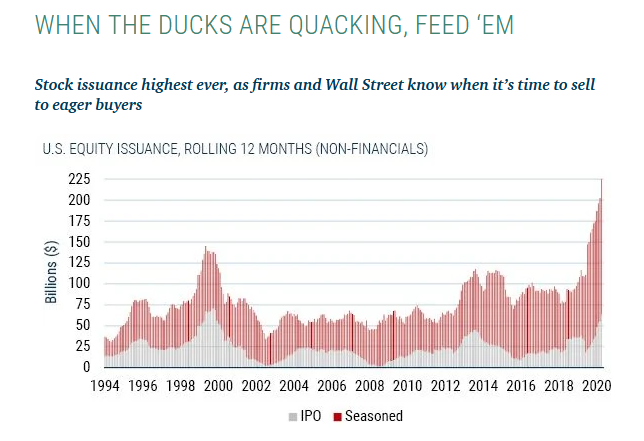

“The following graph and commentary from GMO, show that over the last year corporations took advantage of higher share prices. Interestingly, IPO issuance is currently running at the same pace as the market peak in 2000. Massive issuance from existing stocks is largely responsible for the big difference between total issuance today versus 2000.” – Michael Lebowitz

Like roaches in the kitchen, when there is one, there are always others. Credit Suisse also hiked price targets suggesting that earnings growth is the driving factor. To wit:

With this 2022 outlook, Lefkowitz joins Credit Suisse’s Jonathan Golub who earlier this month put a price target of 5,000 on the S&P 500 for the end of 2022. The equity strategy team at Goldman Sachs also garnered headlines earlier this month in raising their year-end price target to 4,700 from 4,300 while putting a year-end 2022 price target on the benchmark index of 4,900.

Lefkowitz sees earnings growth, not multiple expansion, as the driving force behind the market’s rally in the year ahead.

‘Our price targets assume a forward P/E multiple of about 20x, slightly below current levels of 21x. We expect valuations to remain above historical averages mostly due to the very low interest rate environment. Said another way, stocks continue to look appealing relative to bonds.’” – Yahoo

Rationalizing The Increase

The problem with the analysis is that it is based on rationalizations rather than reality. We discussed previously there is no precedent supporting the view thatlow rates justify high valuations.

“The primary argument is that when inflation or interest rates fall, the present value of future cash flows from equities rises, and subsequently, so should their valuation. While true, assuming all else is equal, a falling discount rate does suggest a higher valuation. However, when inflation declines, future nominal cash flow from equities also falls, this can offset the effect of lower discount rates. Lower discount rates are applied to lower expected cash flows.

In other words, without adjusting for inflation and, in no small degree, economic growth, suggesting low rates justify overpaying for cash flows is a very flawed premise.

‘Instead of regarding stocks as a fixed-rate bond with known nominal coupons, one must think of stocks as a floating-rate bond whose coupons will float with nominal earnings growth. In this analogy, the stock market’s P/E is like the price of a floating-rate bond. In most cases, despite moves in interest rates, the price of a floating-rate bond changes little, and likewise the rational P/E for the stock market moves little.’ – Cliff Asness“

Let’s set aside the “low rate rationalization” and focus on the “earnings growth” side of the valuation argument.

Earnings Growth A Reflection Of Economic Growth

The biggest problem for the S&P 5000 target is underlying earnings. There is an obvious correlation between economic growth and corporate earnings. Such is because over the long term the economy is what generates corporate revenues. While analysts ramped up earnings expectations following the massive liquidity injections from the Government, the payback is coming.

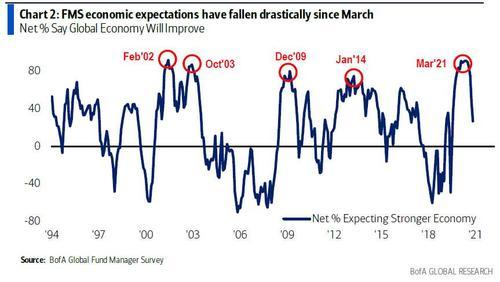

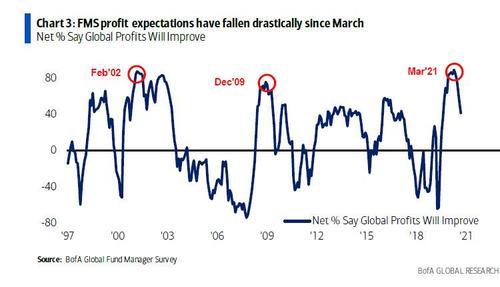

“As BofA recently noted, global expectations are beginning to roll over from very high levels.“

The first problem with Wall Street analysis is several:

Historically, earnings estimates are roughly 30% higher than what turns out to be reality.

As reporting dates approach, analysts revise down estimates below reported levels (assuring a high beat rate), and

Analysts are never held accountable to their orginal estimates.

Given the lack of accountability, it is not surprising analysts are always overly optimistic in their initial estimates which gives them plenty of room to downgrade in the future.

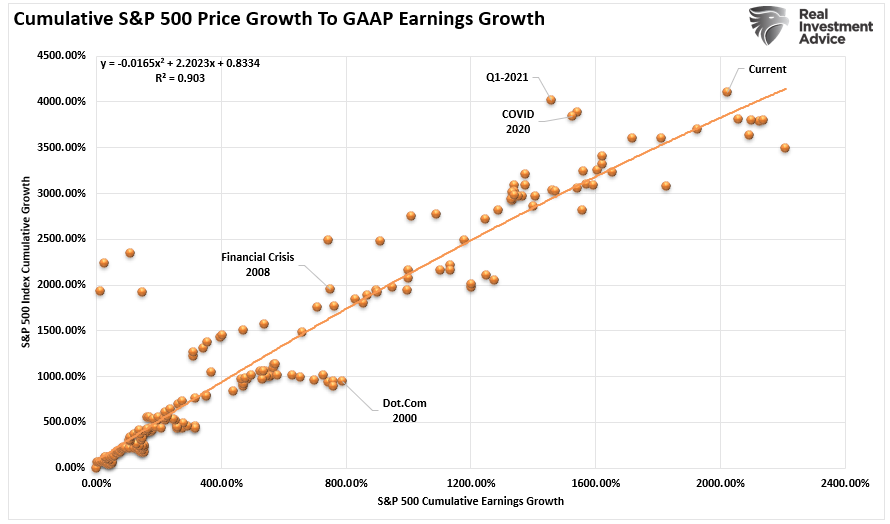

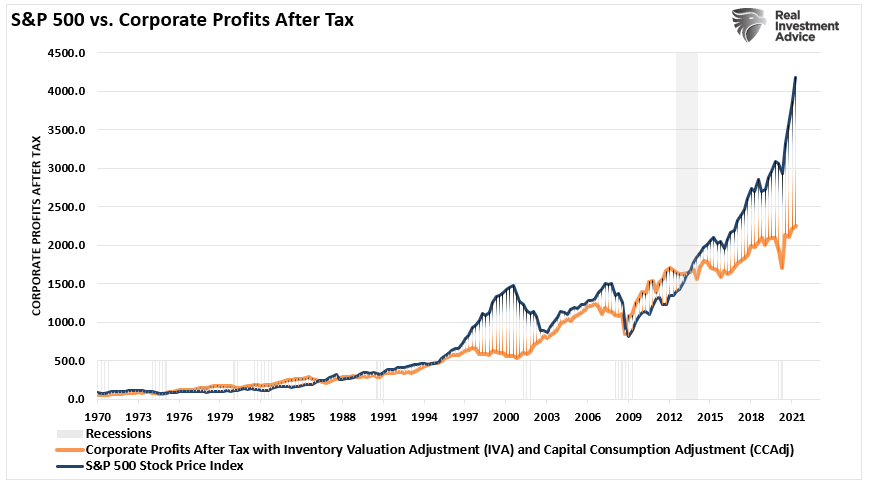

However, there is roughly a 90% correlation between the stock market and GAAP earnings growth. Therefore, if earnings do decline, as profit expectations fall, then the S&P will have a more difficult time hitting a high target.

Furthermore, the current gap between corporate profits and the market has historically not ended well for investors.

Valuations Will Remain Elevated

The problem currently is even with the estimated increase in earnings, the QE-driven price increase keeps valuations extended well above historical ranges.

While that statement comes with the caveat that “valuations are terrible market timing metrics,” they do imply lofty expectations are likely to be disappointed.

I previously quoted Carl Swenlin on earnings. As Carl noted, there is nothing normal with GAAP earnings. But, of course, today, most companies report “operating” earnings which obfuscate profitability by excluding all the “bad stuff.”

The following table shows the expectations for reported earnings growth:

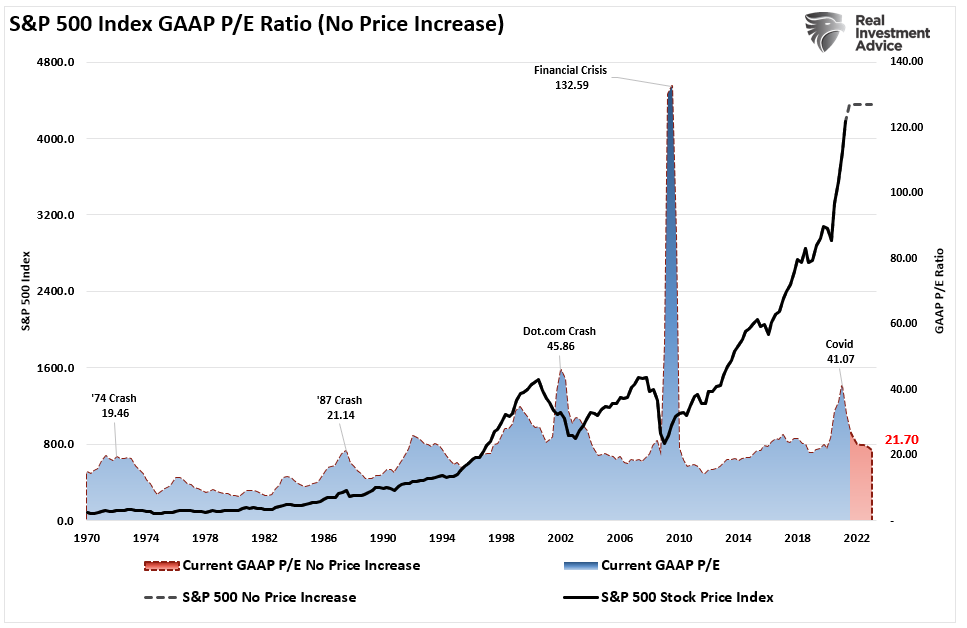

2020 (actual) = $94.13 / share

2021 (estimate) = $185.49 (Increase of 97% over 2020)

2022 (estimate) = $200.62 (Increase of 113% over 2020)

The chart below uses these earnings estimates and assumes NO price increase for the S&P 500 through 2022. Such would reduce valuations from 41x earnings in 2020 to roughly 22x earnings in 2022. (That valuation level remains near previous bull market peak valuations.)

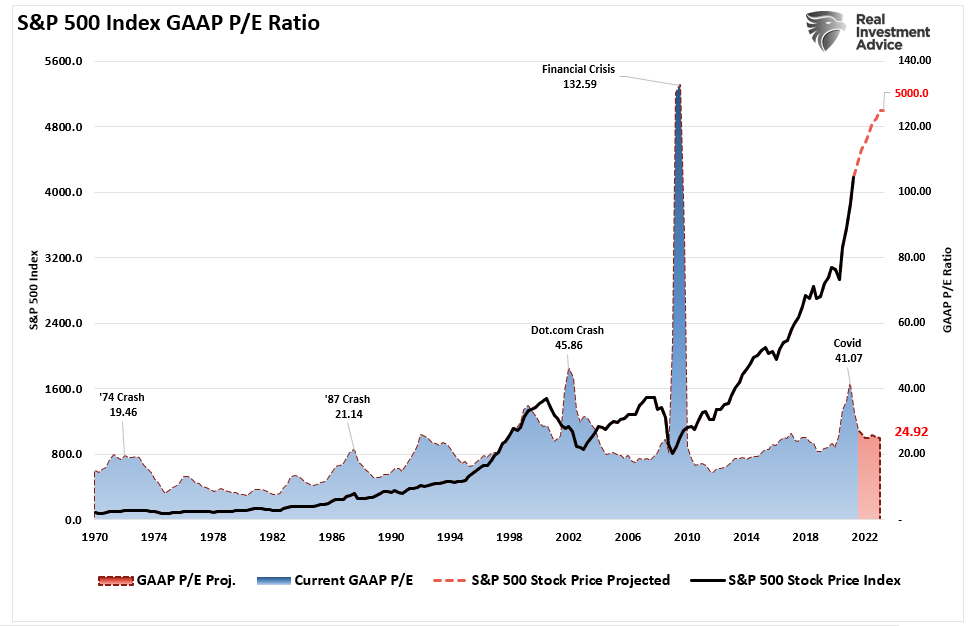

However, if analysts are correct and the market hits 5000, valuations remain elevated. Instead of valuations declining, the increase in price keeps valuations hovering near 25x earnings.

Given that markets are already trading well above historical valuation ranges, such suggests that outcomes will likely not be as “bullish” as many currently expect.

“Historically, price has usually remained below the top of the normal value range (red line); however, since about 1998, it has not been uncommon for price to exceed normal overvalue levels, sometimes by a lot. The market has been mostly overvalued since 1992, and it has not been undervalued since 1984. We could say that this is the ‘new normal,’ except that it isn’t normal by GAAP (Generally Accepted Accounting Principles) standards.” – Carl Swenlin

S&P 5000 Is Likely

We don’t disagree the S&P 500 could well hit a target of 5000. But, let us be honest about the reasons why:

$120 billion a month in liquidity,

Zero interest rates, and

A substantial amount of speculative market fervor.

Like a snowball, the current market momentum could very well carry the S&P higher over the next year.

Such does not preclude a “round-trip” ticket in the future.

Throughout history, overvaluations of markets have never been resolved by earnings catching up with the price. Secondly, the two-fold problem of the temporary nature of the stimulus and inflation leaves the market vulnerable to a downward shift in earnings expectations over the next few quarters. As noted, Wall Street has ratcheted up expectations to try and justify current prices.

While monetary interventions allow market participants to ignore the reality of the economic ties to the market, such does not preclude hair-raising volatility and significant declines, as we saw in March 2020.

More importantly, if the Fed backs off, whether by its design or due to inflation, slower economic growth, or massive debt overhead, rich valuations will matter.

The risk of disappointment is high. And so are the costs of investing based on analysis without all of the facts.

Mathematicians use AI to identify emerging COVID-19 variants

Scientists at The Universities of Manchester and Oxford have developed an AI framework that can identify and track new and concerning COVID-19 variants…

Scientists at The Universities of Manchester and Oxford have developed an AI framework that can identify and track new and concerning COVID-19 variants and could help with other infections in the future.

Scientists at The Universities of Manchester and Oxford have developed an AI framework that can identify and track new and concerning COVID-19 variants and could help with other infections in the future.

The framework combines dimension reduction techniques and a new explainable clustering algorithm called CLASSIX, developed by mathematicians at The University of Manchester. This enables the quick identification of groups of viral genomes that might present a risk in the future from huge volumes of data.

The study, presented this week in the journal PNAS, could support traditional methods of tracking viral evolution, such as phylogenetic analysis, which currently require extensive manual curation.

Roberto Cahuantzi, a researcher at The University of Manchester and first and corresponding author of the paper, said: “Since the emergence of COVID-19, we have seen multiple waves of new variants, heightened transmissibility, evasion of immune responses, and increased severity of illness.

“Scientists are now intensifying efforts to pinpoint these worrying new variants, such as alpha, delta and omicron, at the earliest stages of their emergence. If we can find a way to do this quickly and efficiently, it will enable us to be more proactive in our response, such as tailored vaccine development and may even enable us to eliminate the variants before they become established.”

Like many other RNA viruses, COVID-19 has a high mutation rate and short time between generations meaning it evolves extremely rapidly. This means identifying new strains that are likely to be problematic in the future requires considerable effort.

Currently, there are almost 16 million sequences available on the GISAID database (the Global Initiative on Sharing All Influenza Data), which provides access to genomic data of influenza viruses.

Mapping the evolution and history of all COVID-19 genomes from this data is currently done using extremely large amounts of computer and human time.

The described method allows automation of such tasks. The researchers processed 5.7 million high-coverage sequences in only one to two days on a standard modern laptop; this would not be possible for existing methods, putting identification of concerning pathogen strains in the hands of more researchers due to reduced resource needs.

Thomas House, Professor of Mathematical Sciences at The University of Manchester, said: “The unprecedented amount of genetic data generated during the pandemic demands improvements to our methods to analyse it thoroughly. The data is continuing to grow rapidly but without showing a benefit to curating this data, there is a risk that it will be removed or deleted.

“We know that human expert time is limited, so our approach should not replace the work of humans all together but work alongside them to enable the job to be done much quicker and free our experts for other vital developments.”

The proposed method works by breaking down genetic sequences of the COVID-19 virus into smaller “words” (called 3-mers) represented as numbers by counting them. Then, it groups similar sequences together based on their word patterns using machine learning techniques.

Stefan Güttel, Professor of Applied Mathematics at the University of Manchester, said: “The clustering algorithm CLASSIX we developed is much less computationally demanding than traditional methods and is fully explainable, meaning that it provides textual and visual explanations of the computed clusters.”

Roberto Cahuantzi added: “Our analysis serves as a proof of concept, demonstrating the potential use of machine learning methods as an alert tool for the early discovery of emerging major variants without relying on the need to generate phylogenies.

“Whilst phylogenetics remains the ‘gold standard’ for understanding the viral ancestry, these machine learning methods can accommodate several orders of magnitude more sequences than the current phylogenetic methods and at a low computational cost.”

Journal

Proceedings of the National Academy of Sciences

DOI

10.1073/pnas.2317284121

Article Title

Unsupervised identification of significant lineages of SARS-CoV-2 through scalable machine learning methods

While the size of the United States makes it hard for it to compete with the inter-city train access available in places like Japan and many European countries, Amtrak trains are a very popular transportation option in certain pockets of the country — so much so that the country’s national railway company is expanding its Northeast Corridor by more than one million seats.

Running from Boston all the way south to Washington, D.C., the route is one of the most popular as it passes through the most densely populated part of the country and serves as a commuter train for those who need to go between East Coast cities such as New York and Philadelphia for business.

Veronika Bondarenko captured this photo of New York’s Moynihan Train Hall.

Veronika Bondarenko

Amtrak launches new routes, promises travelers ‘additional travel options’

Earlier this month, Amtrak announced that it was adding four additional Northeastern routes to its schedule — two more routes between New York’s Penn Station and Union Station in Washington, D.C. on the weekend, a new early-morning weekday route between New York and Philadelphia’s William H. Gray III 30th Street Station and a weekend route between Philadelphia and Boston’s South Station.

According to Amtrak, these additions will increase Northeast Corridor’s service by 20% on the weekdays and 10% on the weekends for a total of one million additional seats when counted by how many will ride the corridor over the year.

“More people are taking the train than ever before and we’re proud to offer our customers additional travel options when they ride with us on the Northeast Regional,” Amtrak Executive Vice President and Chief Commercial Officer Eliot Hamlisch said in a statement on the new routes. “The Northeast Regional gets you where you want to go comfortably, conveniently and sustainably as you breeze past traffic on I-95 for a more enjoyable travel experience.”

Here are some of the other Amtrak changes you can expect to see

Amtrak also said that, in the 2023 financial year, the Northeast Corridor had nearly 9.2 million riders — 8% more than it had pre-pandemic and a 29% increase from 2022. The higher demand, particularly during both off-peak hours and the time when many business travelers use to get to work, is pushing Amtrak to invest into this corridor in particular.

To reach more customers, Amtrak has also made several changes to both its routes and pricing system. In the fall of 2023, it introduced a type of new “Night Owl Fare” — if traveling during very late or very early hours, one can go between cities like New York and Philadelphia or Philadelphia and Washington. D.C. for $5 to $15.

As travel on the same routes during peak hours can reach as much as $300, this was a deliberate move to reach those who have the flexibility of time and might have otherwise preferred more affordable methods of transportation such as the bus. After seeing strong uptake, Amtrak added this type of fare to more Boston routes.

The largest distances, such as the ones between Boston and New York or New York and Washington, are available at the lowest rate for $20.

I am a conservation biologist who studies emerging infectious diseases. When people ask me what I think the next pandemic will be I often say that we are in the midst of one – it’s just afflicting a great many species more than ours.

I am referring to the highly pathogenic strain of avian influenza H5N1 (HPAI H5N1), otherwise known as bird flu, which has killed millions of birds and unknown numbers of mammals, particularly during the past three years.

This is the strain that emerged in domestic geese in China in 1997 and quickly jumped to humans in south-east Asia with a mortality rate of around 40-50%. My research group encountered the virus when it killed a mammal, an endangered Owston’s palm civet, in a captive breeding programme in Cuc Phuong National Park Vietnam in 2005.

How these animals caught bird flu was never confirmed. Their diet is mainly earthworms, so they had not been infected by eating diseased poultry like many captive tigers in the region.

This discovery prompted us to collate all confirmed reports of fatal infection with bird flu to assess just how broad a threat to wildlife this virus might pose.

This is how a newly discovered virus in Chinese poultry came to threaten so much of the world’s biodiversity.

Until December 2005, most confirmed infections had been found in a few zoos and rescue centres in Thailand and Cambodia. Our analysis in 2006 showed that nearly half (48%) of all the different groups of birds (known to taxonomists as “orders”) contained a species in which a fatal infection of bird flu had been reported. These 13 orders comprised 84% of all bird species.

We reasoned 20 years ago that the strains of H5N1 circulating were probably highly pathogenic to all bird orders. We also showed that the list of confirmed infected species included those that were globally threatened and that important habitats, such as Vietnam’s Mekong delta, lay close to reported poultry outbreaks.

Mammals known to be susceptible to bird flu during the early 2000s included primates, rodents, pigs and rabbits. Large carnivores such as Bengal tigers and clouded leopards were reported to have been killed, as well as domestic cats.

Our 2006 paper showed the ease with which this virus crossed species barriers and suggested it might one day produce a pandemic-scale threat to global biodiversity.

In the past couple of years, bird flu has spread rapidly across Europe and infiltrated North and South America, killing millions of poultry and a variety of bird and mammal species. A recent paper found that 26 countries have reported at least 48 mammal species that have died from the virus since 2020, when the latest increase in reported infections started.

Not even the ocean is safe. Since 2020, 13 species of aquatic mammal have succumbed, including American sea lions, porpoises and dolphins, often dying in their thousands in South America. A wide range of scavenging and predatory mammals that live on land are now also confirmed to be susceptible, including mountain lions, lynx, brown, black and polar bears.

The UK alone has lost over 75% of its great skuas and seen a 25% decline in northern gannets. Recent declines in sandwich terns (35%) and common terns (42%) were also largely driven by the virus.

Scientists haven’t managed to completely sequence the virus in all affected species. Research and continuous surveillance could tell us how adaptable it ultimately becomes, and whether it can jump to even more species. We know it can already infect humans – one or more genetic mutations may make it more infectious.

At the crossroads

Between January 1 2003 and December 21 2023, 882 cases of human infection with the H5N1 virus were reported from 23 countries, of which 461 (52%) were fatal.

Of these fatal cases, more than half were in Vietnam, China, Cambodia and Laos. Poultry-to-human infections were first recorded in Cambodia in December 2003. Intermittent cases were reported until 2014, followed by a gap until 2023, yielding 41 deaths from 64 cases. The subtype of H5N1 virus responsible has been detected in poultry in Cambodia since 2014. In the early 2000s, the H5N1 virus circulating had a high human mortality rate, so it is worrying that we are now starting to see people dying after contact with poultry again.

It’s not just H5 subtypes of bird flu that concern humans. The H10N1 virus was originally isolated from wild birds in South Korea, but has also been reported in samples from China and Mongolia.

Recent research found that these particular virus subtypes may be able to jump to humans after they were found to be pathogenic in laboratory mice and ferrets. The first person who was confirmed to be infected with H10N5 died in China on January 27 2024, but this patient was also suffering from seasonal flu (H3N2). They had been exposed to live poultry which also tested positive for H10N5.

Species already threatened with extinction are among those which have died due to bird flu in the past three years. The first deaths from the virus in mainland Antarctica have just been confirmed in skuas, highlighting a looming threat to penguin colonies whose eggs and chicks skuas prey on. Humboldt penguins have already been killed by the virus in Chile.

How can we stem this tsunami of H5N1 and other avian influenzas? Completely overhaul poultry production on a global scale. Make farms self-sufficient in rearing eggs and chicks instead of exporting them internationally. The trend towards megafarms containing over a million birds must be stopped in its tracks.

To prevent the worst outcomes for this virus, we must revisit its primary source: the incubator of intensive poultry farms.

Diana Bell does not work for, consult, own shares in or receive funding from any company or organisation that would benefit from this article, and has disclosed no relevant affiliations beyond their academic appointment.

We use cookies on our website to give you the most relevant experience by remembering your preferences and repeat visits. By clicking “Accept”, you consent to the use of ALL the cookies.

This website uses cookies to improve your experience while you navigate through the website. Out of these, the cookies that are categorized as necessary are stored on your browser as they are essential for the working of basic functionalities of the website. We also use third-party cookies that help us analyze and understand how you use this website. These cookies will be stored in your browser only with your consent. You also have the option to opt-out of these cookies. But opting out of some of these cookies may affect your browsing experience.

Necessary cookies are absolutely essential for the website to function properly. These cookies ensure basic functionalities and security features of the website, anonymously.

Cookie

Duration

Description

cookielawinfo-checbox-analytics

11 months

This cookie is set by GDPR Cookie Consent plugin. The cookie is used to store the user consent for the cookies in the category "Analytics".

cookielawinfo-checbox-functional

11 months

The cookie is set by GDPR cookie consent to record the user consent for the cookies in the category "Functional".

cookielawinfo-checbox-others

11 months

This cookie is set by GDPR Cookie Consent plugin. The cookie is used to store the user consent for the cookies in the category "Other.

cookielawinfo-checkbox-necessary

11 months

This cookie is set by GDPR Cookie Consent plugin. The cookies is used to store the user consent for the cookies in the category "Necessary".

cookielawinfo-checkbox-performance

11 months

This cookie is set by GDPR Cookie Consent plugin. The cookie is used to store the user consent for the cookies in the category "Performance".

viewed_cookie_policy

11 months

The cookie is set by the GDPR Cookie Consent plugin and is used to store whether or not user has consented to the use of cookies. It does not store any personal data.

Functional cookies help to perform certain functionalities like sharing the content of the website on social media platforms, collect feedbacks, and other third-party features.

Performance cookies are used to understand and analyze the key performance indexes of the website which helps in delivering a better user experience for the visitors.

Analytical cookies are used to understand how visitors interact with the website. These cookies help provide information on metrics the number of visitors, bounce rate, traffic source, etc.

Advertisement cookies are used to provide visitors with relevant ads and marketing campaigns. These cookies track visitors across websites and collect information to provide customized ads.

{kind=link}