International

Wall Street Reacts To Today’s Huge CPI Miss

Wall Street Reacts To Today’s Huge CPI Miss

“Remember that one month does not make a trend. But also remember that every trend starts with…

Share this:

“Remember that one month does not make a trend. But also remember that every trend starts with one month.” - Leon Brittan

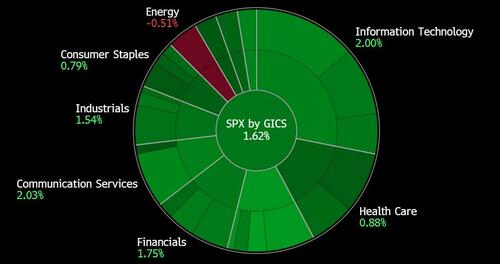

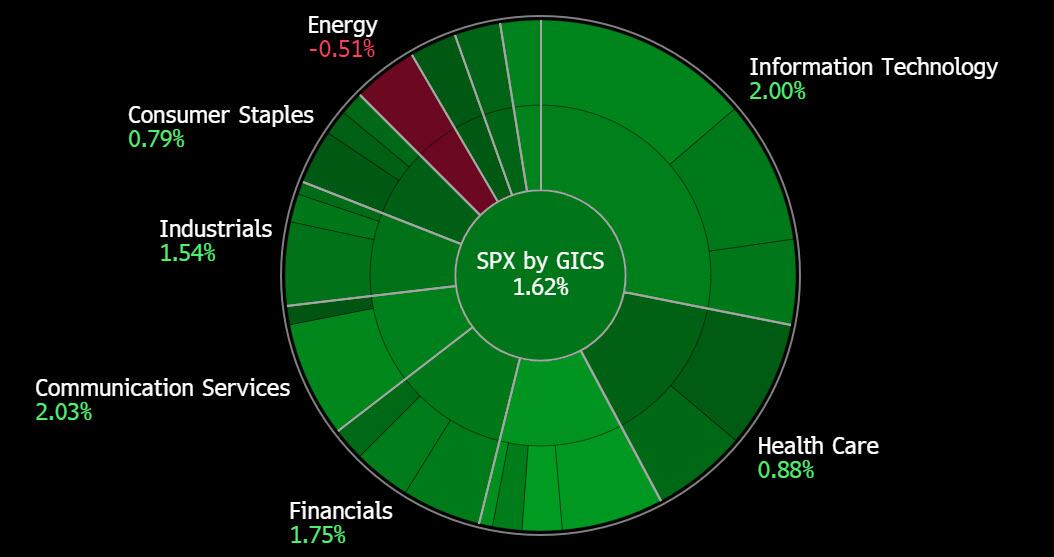

For a look at just how big of a surprise today's CPI miss (which we said would be a miss in our preview), look no further than the market where it's a sea of red with every asset class soaring (except energy)...

... and where the plight of the shorts - which these days is most hedge funds - can be summarized with one image:

Why this tremendous market reaction, where - when one strips away the rhetoric - all we have seen is one month's drop in energy prices, which will only rise now that the market is starting to anticipate a Fed pivot.

Bloomberg asks a similar question, namely "what’s behind the surprising slowdown in July?" and notes that according to a new Bloomberg Economics model, US inflation decomposes into four factors: supply, demand, energy prices and monetary policy.

The model found that lower energy costs and a slightly tighter Fed stance were the main drivers of the deceleration to 8.5% last month.

At the same time, sizzling demand paired with supply constraints continue to put upward pressure on inflation. With these last two factors harder to contain, Bloomberg writes that "the Fed has a tough task ahead of it and will likely need to be more hawkish then currently expected", or in other words, echoing what we said yesterday when we warned that "a miss will make Powell's life extremely hard."

Why? Well, here is a good thread summary from Dan Alpert:

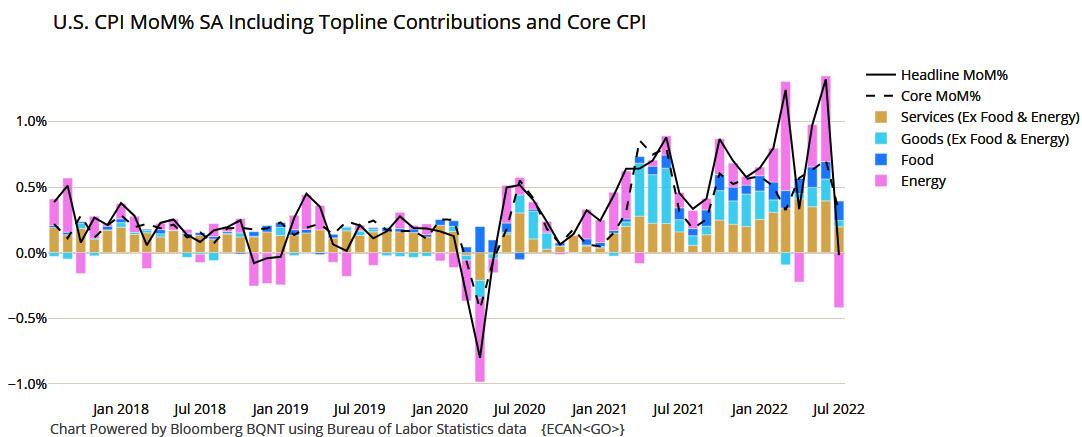

And the answer is: Headline: ZERO M/M; Core: 0.3%

The end is nigh!

That headline reading was with food UP 1.1% in July, offset by energy falling -4.9% on the month. (Energy commodities -7.6%)

Core commodities (goods) only rises 0.2% on the month as supply chains reopen and production inventories build to backlog. On the services side, the price rise falls to 0.4% driven by a -0.5 decline in transportation services in July.The shelter rise moderates a bit to +0.5% M/M on the back of a 2.7% monthly decline in lodging, which fell for the second straight month after pandemic reopening demand and supply squeezes (this will accelerate into the fall).

Rent and Owners Equivalent Rent of Primary Residences, the primary drivers of core inflation, remain high at 0.7% and 0.6% M/M respectively. But that is lagging data and the housing market has already been thrown into decline by Fed interest rate hikes and building oversupply.

Housing is, these days, the principal channel through which Fed monetary policy operates (the mortgage market). >>

While Fed hikes are not responsible for inflation slowing in this report (the prior inflation itself - "the cure for high prices is high prices", opening supply chains and lower global energy prices were), higher interest rates will have a huge impact on housing (and CPI) soon.

In October of last year, before Omicron and the Ukraine War disturbed pricing metrics around the world, I noted that inflation would be a first half of 2022 story (I said it would subside by Q2, but the foregoing events got in the way).

Yet here we are.

While these M/M sectoral declines will not be repeated every month, we will see housing costs gradually subside for sure, core goods stabilize and consumer purchases driven most by pandemic reopening "revenge spending" see material price retrenchment as inventories rebuild.

The only real wild cards are exogenous (not demand driven) supply risks associated with oil and gas, and their bleed over impact on food (think fertilizer and food transportation) costs.

All in all, this report is as I expected and the trend is reorienting itself.

We are at the point where the annual (Y/Y) CPI figures cease to have meaning. Prices are what they are now, as are wages and incomes. The only issue is where they go in the future. And that is not a function of expectations, it is the discipline of supply and demand.

One last data point FWIW: CPI All Items less Shelter fell by -0.3% in July.

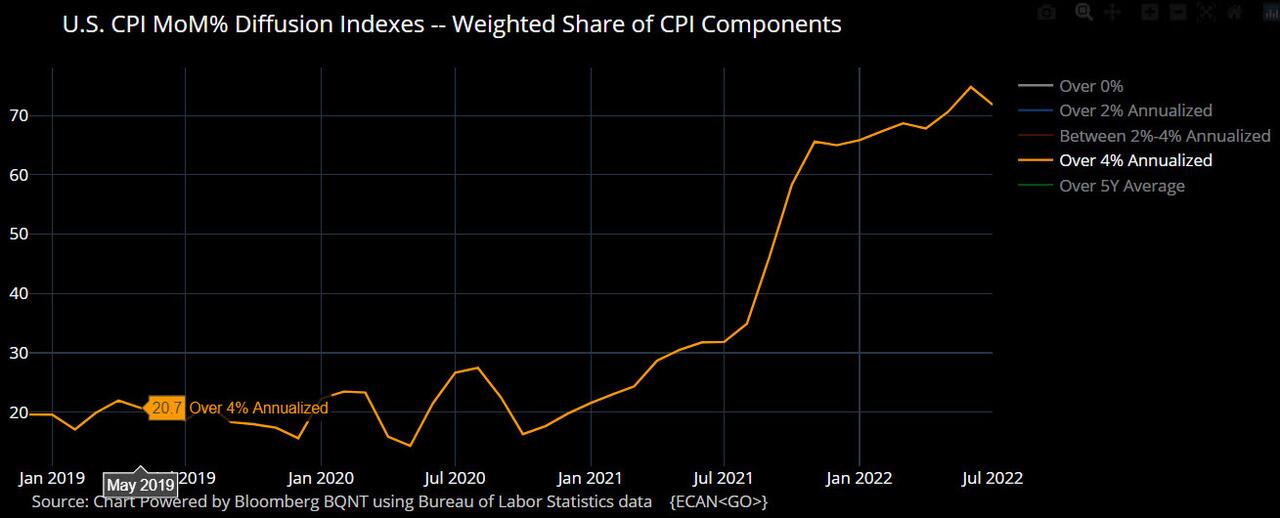

While we are confident that those who don't actually have a corporate charge card will disagree with Dan's cheerful take on today's inflation print, there was another reason for the market's euphoric reaction - the chart below from Bloomberg shows the breadth of inflation. The July reading of 71.8 is saying that 71.8% percent of the CPI basket is increasing in price at more than a 4% on an annualized basis from the MoM data, which represents relief for the Fed after June’s high of 74.8%.

What do other market watchers and strategists think? Below we summarize a handful of hot takes from across Wall Street:

- Peter Tchir, chief strategist at Academy Securities: "Slightly better than expected inflation across the board. Initial reaction lower yields, steeper curves (which I like). Higher stocks/risk assets - expected based on numbers, but 1) not sure number beat the whisper; 2) still high enough Fed not completely out of picture, which may lead us back to fixating on recession, inventories, semiconductors, warnings, etc. So fading this on risk side of the equation"

- Seema Shah, chief strategist at Principal Global Investors: “This is a textbook bear market rally -- technicals and sentiment drove the upturn and momentum is carrying it for now. Markets have become overly optimistic about the Fed outlook and even the economy. But as we get into Q4, earnings growth will show clear signs of struggles and inflation will be easing only slowly, giving markets an important reminder the further rate hikes are absolutely necessary.”

- Peter Boockvar, chief investment officer at Bleakley Financial Group: “We know there is another CPI figure, along with a jobs number before the Fed meets again. I’ll say again that they will be going 50 bps in September and I doubt much past that.”

- Eric Theoret, global macro strategist at Manulife Investment Management: "I'll be watching breakevens, and the challenge from here will be for markets to not celebrate too much and declare victory... Breakevens tend to be well correlated to market sentiment and the price of crude more specifically. A weaker USD and risk on tone would support the price of oil and lift breakevens, pulling them away from target. This is not something that markets or the Fed ultimately want.”

- Neil Dutta, head of US economic at Renaissance Macro: “This data point will fuel talk of a policy pivot. But, for me, the issue really does boil down to the labor market. Short-term inflation expectations and gasoline prices were the story in May and June. That’s not the story now. Wage growth is running red hot and absent a turn around in productivity this will ultimately fuel higher prices.”

- Anna Wong, Bloomberg chief economist: "Both headline and core CPI inflation were surprisingly soft in July, but with recent wage and productivity data signaling prices pressures ahead, the Federal Reserve is unlikely to step back from the inflation fight just yet. Another soft print is likely in August as gasoline prices have continued to decline."

- Ira Jersey, Bloomberg strategist: “Our analysis shows that the lower-volatility (read sticky) components of core CPI may have peaked in July, but the medium-volatility sector continues to jump higher. If the low-volatility cluster stabilizes at this higher level, these combined trends may keep core CPI underpinned and the Fed hawkish.... The better-than-expected core CPI print will be a strong positive for the Treasury market, particularly the long end, so the knee-jerk reaction is unsurprising. The strong steepening of the curve may not last, however, as the better-than-expected core still doesn’t mean it will fall. In fact, although better than expected, the core may be sticker than the market seems to be anticipating.”

- Ellen Zentner, Morgan Stanley economist: "Fed officials are unlikely to see this report as a signal to deviate from their steep tightening path we foresee through the end of this year. That said, this report makes a 50 basis points more likely at the September meeting rather than 75, but a lot will depend on the August CPI release next month.”

- Ian Lyngen, rates strategist at BMO Capital Markets: "post-CPI steepening in 2/10’s to around -40bps is a reentry point to add to a core flattener and expect that the incoming Fed-speak will emphasize the idea that the Fed will need to see more than one month of data for confirmation inflation has, in fact, peaked.”

- Ellen Gaske, G10 economist at PGIM Fixed Income: “The weaker-than-expected CPI print suggests the Fed could adopt a more cautious pace of tightening going forward.”

- Dennis DeBusschere, founder of 22V Research: "the report is obviously very positive for markets on the day -- rates are lower, rate-hike expectations are lower and worries about a too-hot CPI with very strong employment reduced.”

- Michael Pond, head of inflation strategy at Barclays: “This is a necessary print for the Fed, but it’s not sufficient. We need to see a lot more. You can think about this print sort of like the weather: it’s better today than it has been over the past few days. But it’s still summer. There’s still a lot of humidity.”

- Matt Maley, chief market strategist at Miller Tabak: “Some people were starting to think that we could get a 75 basis point hike in September or even a mid-meeting hike. This weaker than expected CPI number takes that off the table. In fact, it might even cause some people to look for a pause from the Fed.”

- Victoria Greene, chief investment officer at G Squared: “While this is to be celebrated, 8.5% inflation is still well above what the Fed wants to see. 50-75bps are still on the table for September, and more data will come in by that point."

- Jim Paulsen, chief investment strategist at the Leuthold Group: “Wow, finally the anecdotal evidence that inflation was easing has finally showed up in a mainstream inflation report. The Fed is rapidly losing its case for further tightening and this report reinforces for investors that either a new easing cycle has already begun or we are getting very close to one.”

- Han Hatzius, Goldman Sachs chief economist: "July core CPI rose by 0.31% month-over-month, below expectations and the slowest monthly pace since September. Declines in airfares and used car prices contributed to the slowdown, and we also note a sequentially slower but still elevated pace of shelter inflation."

International

Shakira’s net worth

After 12 albums, a tax evasion case, and now a towering bronze idol sculpted in her image, how much is Shakira worth more than 4 decades into her care…

Share this:

Shakira’s considerable net worth is no surprise, given her massive popularity in Latin America, the U.S., and elsewhere.

In fact, the belly-dancing contralto queen is the second-wealthiest Latin-America-born pop singer of all time after Gloria Estefan. (Interestingly, Estefan actually helped a young Shakira translate her breakout album “Laundry Service” into English, hugely propelling her stateside success.)

Since releasing her first record at age 13, Shakira has spent decades recording albums in both Spanish and English and performing all over the world. Over the course of her 40+ year career, she helped thrust Latin pop music into the American mainstream, paving the way for the subsequent success of massively popular modern acts like Karol G and Bad Bunny.

In December 2023, a 21-foot-tall beachside bronze statue of the “Hips Don’t Lie” singer was unveiled in her Colombian hometown of Barranquilla, making her a permanent fixture in the city’s skyline and cementing her legacy as one of Latin America’s most influential entertainers.

After 12 albums, a plethora of film and television appearances, a highly publicized tax evasion case, and now a towering bronze idol sculpted in her image, how much is Shakira worth? What does her income look like? And how does she spend her money?

How much is Shakira worth?

In late 2023, Spanish sports and lifestyle publication Marca reported Shakira’s net worth at $400 million, citing Forbes as the figure’s source (although Forbes’ profile page for Shakira does not list a net worth — and didn’t when that article was published).

Most other sources list the singer’s wealth at an estimated $300 million, and almost all of these point to Celebrity Net Worth — a popular but dubious celebrity wealth estimation site — as the source for the figure.

A $300 million net worth would make Shakira the third-richest Latina pop star after Gloria Estefan ($500 million) and Jennifer Lopez ($400 million), and the second-richest Latin-America-born pop singer after Estefan (JLo is Puerto Rican but was born in New York).

Shakira’s income: How much does she make annually?

Entertainers like Shakira don’t have predictable paychecks like ordinary salaried professionals. Instead, annual take-home earnings vary quite a bit depending on each year’s album sales, royalties, film and television appearances, streaming revenue, and other sources of income. As one might expect, Shakira’s earnings have fluctuated quite a bit over the years.

From June 2018 to June 2019, for instance, Shakira was the 10th highest-earning female musician, grossing $35 million, according to Forbes. This wasn’t her first time gracing the top 10, though — back in 2012, she also landed the #10 spot, bringing in $20 million, according to Billboard.

In 2023, Billboard listed Shakira as the 16th-highest-grossing Latin artist of all time.

How much does Shakira make from her concerts and tours?

A large part of Shakira’s wealth comes from her world tours, during which she sometimes sells out massive stadiums and arenas full of passionate fans eager to see her dance and sing live.

According to a 2020 report by Pollstar, she sold over 2.7 million tickets across 190 shows that grossed over $189 million between 2000 and 2020. This landed her the 19th spot on a list of female musicians ranked by touring revenue during that period. In 2023, Billboard reported a more modest touring revenue figure of $108.1 million across 120 shows.

In 2003, Shakira reportedly generated over $4 million from a single show on Valentine’s Day at Foro Sol in Mexico City. 15 years later, in 2018, Shakira grossed around $76.5 million from her El Dorado World Tour, according to Touring Data.

Related: RuPaul's net worth: Everything to know about the cultural icon and force behind 'Drag Race'

How much has Shakira made from her album sales?

According to a 2023 profile in Variety, Shakira has sold over 100 million records throughout her career. “Laundry Service,” the pop icon’s fifth studio album, was her most successful, selling over 13 million copies worldwide, according to TheRichest.

Exactly how much money Shakira has taken home from her album sales is unclear, but in 2008, it was widely reported that she signed a 10-year contract with LiveNation to the tune of between $70 and $100 million to release her subsequent albums and manage her tours.

How much did Shakira make from her Super Bowl and World Cup performances?

Shakira co-wrote one of her biggest hits, “Waka Waka (This Time for Africa),” after FIFA selected her to create the official anthem for the 2010 World Cup in South Africa. She performed the song, along with several of her existing fan-favorite tracks, during the event’s opening ceremonies. TheThings reported in 2023 that the song generated $1.4 million in revenue, citing Popnable for the figure.

A decade later, 2020’s Superbowl halftime show featured Shakira and Jennifer Lopez as co-headliners with guest performances by Bad Bunny and J Balvin. The 14-minute performance was widely praised as a high-energy celebration of Latin music and dance, but as is typical for Super Bowl shows, neither Shakira nor JLo was compensated beyond expenses and production costs.

The exposure value that comes with performing in the Super Bowl Halftime Show, though, is significant. It is typically the most-watched television event in the U.S. each year, and in 2020, a 30-second Super Bowl ad spot cost between $5 and $6 million.

How much did Shakira make as a coach on “The Voice?”

Shakira served as a team coach on the popular singing competition program “The Voice” during the show’s fourth and sixth seasons. On the show, celebrity musicians coach up-and-coming amateurs in a team-based competition that eventually results in a single winner. In 2012, The Hollywood Reporter wrote that Shakira’s salary as a coach on “The Voice” was $12 million.

Related: John Cena's net worth: The wrestler-turned-actor's investments, businesses, and more

How does Shakira spend her money?

Shakira doesn’t just make a lot of money — she spends it, too. Like many wealthy entertainers, she’s purchased her share of luxuries, but Barranquilla’s barefoot belly dancer is also a prolific philanthropist, having donated tens of millions to charitable causes throughout her career.

Private island

Back in 2006, she teamed up with Roger Waters of Pink Floyd fame and Spanish singer Alejandro Sanz to purchase Bonds Cay, a 550-acre island in the Bahamas, which was listed for $16 million at the time.

Along with her two partners in the purchase, Shakira planned to develop the island to feature housing, hotels, and an artists’ retreat designed to host a revolving cast of artists-in-residence. This plan didn’t come to fruition, though, and as of this article’s last update, the island was once again for sale on Vladi Private Islands.

Real estate and vehicles

Like most wealthy celebs, Shakira’s portfolio of high-end playthings also features an array of luxury properties and vehicles, including a home in Barcelona, a villa in Cyprus, a Miami mansion, and a rotating cast of Mercedes-Benz vehicles.

Philanthropy and charity

Shakira doesn’t just spend her massive wealth on herself; the “Queen of Latin Music” is also a dedicated philanthropist and regularly donates portions of her earnings to the Fundación Pies Descalzos, or “Barefoot Foundation,” a charity she founded in 1997 to “improve the education and social development of children in Colombia, which has suffered decades of conflict.” The foundation focuses on providing meals for children and building and improving educational infrastructure in Shakira’s hometown of Barranquilla as well as four other Colombian communities.

In addition to her efforts with the Fundación Pies Descalzos, Shakira has made a number of other notable donations over the years. In 2007, she diverted a whopping $40 million of her wealth to help rebuild community infrastructure in Peru and Nicaragua in the wake of a devastating 8.0 magnitude earthquake. Later, during the COVID-19 pandemic in 2020, Shakira donated a large supply of N95 masks for healthcare workers and ventilators for hospital patients to her hometown of Barranquilla.

Back in 2010, the UN honored Shakira with a medal to recognize her dedication to social justice, at which time the Director General of the International Labour Organization described her as a “true ambassador for children and young people.”

Shakira’s tax fraud scandal: How much did she pay?

In 2018, prosecutors in Spain initiated a tax evasion case against Shakira, alleging she lived primarily in Spain from 2012 to 2014 and therefore failed to pay around $14.4 million in taxes to the Spanish government. Spanish law requires anyone who is “domiciled” (i.e., living primarily) in Spain for more than half of the year to pay income taxes.

During the period in question, Shakira listed the Bahamas as her primary residence but did spend some time in Spain, as she was dating Gerard Piqué, a professional footballer and Spanish citizen. The couple’s first son, Milan, was also born in Barcelona during this period.

Shakira maintained that she spent far fewer than 183 days per year in Spain during each of the years in question. In an interview with Elle Magazine, the pop star opined that “Spanish tax authorities saw that I was dating a Spanish citizen and started to salivate. It's clear they wanted to go after that money no matter what."

Prosecutors in the case sought a fine of almost $26 million and a possible eight-year prison stint, but in November of 2023, Shakira took a deal to close the case, accepting a fine of around $8 million and a three-year suspended sentence to avoid going to trial. In reference to her decision to take the deal, Shakira stated, "While I was determined to defend my innocence in a trial that my lawyers were confident would have ruled in my favour [had the trial proceeded], I have made the decision to finally resolve this matter with the best interest of my kids at heart who do not want to see their mom sacrifice her personal well-being in this fight."

How much did the Shakira statue in Barranquilla cost?

In late 2023, a 21-foot-tall bronze likeness of Shakira was unveiled on a waterfront promenade in Barranquilla. The city’s then-mayor, Jaime Pumarejo, commissioned Colombian sculptor Yino Márquez to create the statue of the city’s treasured pop icon, along with a sculpture of the city’s coat of arms.

According to the New York Times, the two sculptures cost the city the equivalent of around $180,000. A plaque at the statue’s base reads, “A heart that composes, hips that don’t lie, an unmatched talent, a voice that moves the masses and bare feet that march for the good of children and humanity.”

Related: Taylor Swift net worth: The most successful entertainer joins the billionaire's club

bonds pandemic covid-19 real estate africa mexico spainInternational

Delta Air Lines adds a new route travelers have been asking for

The new Delta seasonal flight to the popular destination will run daily on a Boeing 767-300.

Share this:

Those who have tried to book a flight from North America to Europe in the summer of 2023 know just how high travel demand to the continent has spiked.

At 2.93 billion, visitors to the countries making up the European Union had finally reached pre-pandemic levels last year while North Americans in particular were booking trips to both large metropolises such as Paris and Milan as well as smaller cities growing increasingly popular among tourists.

Related: A popular European city is introducing the highest 'tourist tax' yet

As a result, U.S.-based airlines have been re-evaluating their networks to add more direct routes to smaller European destinations that most travelers would have previously needed to reach by train or transfer flight with a local airline.

Shutterstock

Delta Air Lines: ‘Glad to offer customers increased choice…’

By the end of March, Delta Air Lines (DAL) will be restarting its route between New York’s JFK and Marco Polo International Airport in Venice as well as launching two new flights to Venice from Atlanta. One will start running this month while the other will be added during peak demand in the summer.

More Travel:

- A new travel term is taking over the internet (and reaching airlines and hotels)

- The 10 best airline stocks to buy now

- Airlines see a new kind of traveler at the front of the plane

“As one of the most beautiful cities in the world, Venice is hugely popular with U.S. travelers, and our flights bring valuable tourism and trade opportunities to the city and the region as well as unrivalled opportunities for Venetians looking to explore destinations across the Americas,” Delta’s SVP for Europe Matteo Curcio said in a statement. “We’re glad to offer customers increased choice this summer with flights from New York and additional service from Atlanta.”

The JFK-Venice flight will run on a Boeing 767-300 (BA) and have 216 seats including higher classes such as Delta One, Delta Premium Select and Delta Comfort Plus.

Delta offers these features on the new flight

Both the New York and Atlanta flights are seasonal routes that will be pulled out of service in October. Both will run daily while the first route will depart New York at 8:55 p.m. and arrive in Venice at 10:15 a.m. local time on the way there, while leaving Venice at 12:15 p.m. to arrive at JFK at 5:05 p.m. on the way back.

According to Delta, this will bring its service to 17 flights from different U.S. cities to Venice during the peak summer period. As with most Delta flights at this point, passengers in all fare classes will have access to free Wi-Fi during the flight.

Those flying in Delta’s highest class or with access through airline status or a credit card will also be able to use the new Delta lounge that is part of the airline’s $12 billion terminal renovation and is slated to open to travelers in the coming months. The space will take up more than 40,000 square feet and have an outdoor terrace.

“Delta One customers can stretch out in a lie-flat seat and enjoy premium amenities like plush bedding made from recycled plastic bottles, more beverage options, and a seasonal chef-curated four-course meal,” Delta said of the new route. “[…] All customers can enjoy a wide selection of in-flight entertainment options and stay connected with Wi-Fi and enjoy free mobile messaging.”

stocks pandemic european europeInternational

Stock Market Today: Stocks turn lower as factory inflation spikes, retail sales miss target

Stocks will navigate the last major data releases prior to next week’s Fed rate meeting in Washington.

Share this:

{kind=link}

Check back for updates throughout the trading day

U.S. stocks edged lower Thursday following a trio of key economic releases that have added to the current inflation puzzle as investors shift focus to the Federal Reserve's March policy meeting next week in Washington.

Updated at 9:59 AM EDT

Red start

Stocks are now falling sharply following the PPI inflation data and retail sales miss, with the S&P 500 marked 18 points lower, or 0.36%, in the opening half hour of trading.

The Dow, meanwhile, was marked 92 points lower while the Nasdaq slipped 67 points.

Treasury yields are also on the move, with 2-year notes rising 5 basis points on the session to 4.679% and 10-year notes pegged 7 basis points higher at 4.271%.

The probability of a June rate cut has moved below 60% after the higher-than-expected CPI/PPI reports. A week ago this probability was 74% and a month ago it was 82%. pic.twitter.com/9W01oWU96G

— Charlie Bilello (@charliebilello) March 14, 2024

Updated at 9:44 AM EDT

Under Water

Under Armour (UAA) shares slumped firmly lower in early trading following the sportswear group's decision to bring back founder Kevin Plank as CEO, replacing the outgoing Stephanie Linnartz.

Plank, who founded Under Armour in 1996, left the group in May of 2021 just weeks before the group revealed that it was co-operating with investigations from both the Securities and Exchange Commission and the U.S. Department of Justice into the company's revenue recognition accounting.

Under Armour shares were marked 10.6% lower in early trading to change hands at $7.21 each.

Updated at 9:22 AM EDT

Steely resolve

U.S. Steel (X) shares extended their two-day decline Thursday, falling 5.75% in pre-market trading following multiple reports that suggest President Joe Biden will push to prevent Japan's Nippon Steel from buying the Pittsburgh-based group.

Both Reuters and the Associated Press have said Biden will express his views to Prime Minister Kishida Yuko ahead of a planned State Visit next month at the White House.

Related: US Steel soars on $15 billion Nippon Steel takeover; United Steelworkers slams deal

Updated at 8:52 AM EDT

Clear as mud

Retail sales rebounded last month, but the overall tally of $700.7 billion missed Street forecasts and suggests the recent uptick in inflation could be holding back discretionary spending.

A separate reading of factory inflation, meanwhile, showed prices spiking by 1.6%, on the year, and 0.6% on the month, amid a jump in goods prices.

U.S. stocks held earlier gains following the data release, with futures tied to the S&P 500 indicating an opening bell gain of 10 points, while the Dow was called 140 points higher. The Nasdaq, meanwhile, is looking at a more modest 40 point gain.

Benchmark 10-year Treasury note yields edged 3 basis points lower to 4.213% while two-year notes were little-changed at 4.626%.

The #PPI troughed 8 months ago, yet the economic consensus and even the #Fed believes #inflation has been conquered. Forget the forecasts for multiple rate cuts. pic.twitter.com/ZNIiKLWdFA

— Richard Bernstein Advisors (@RBAdvisors) March 14, 2024

Stock Market Today

Stocks finished lower last night, with the S&P 500 ending modestly in the red and the Nasdaq falling around 0.5%. The declines came amid an uptick in Treasury yields tied to concern that inflation pressures have failed to ease over the opening months of the year.

A better-than-expected auction of $22 billion in 30-year bonds, drawing the strongest overall demand since last June, steadied the overall market, but stocks still slipped into the close with an eye towards today's dataset.

The Commerce Department will publish its February reading of factory-gate inflation at 8:30 am Eastern Time. Analysts are expecting a slowdown in the key core reading, which feeds into the Fed's favored PCE price index.

Retail sales figures for the month are also set for an 8:30 am release as investors search for clues on consumer strength, tied to a resilient job market. Those factors could give the Fed more justification to wait until the summer months to begin the first of its three projected rate cuts.

"The case for a gradual but sustained slowdown in growth in consumers’ spending from 2023’s robust pace is persuasive," said Ian Shepherdson of Pantheon Macroeconomics.

"Most households have run down the excess savings accumulated during the pandemic, while the cost of credit has jumped and last year’s plunge in home sales has depressed demand housing-related retail items like furniture and appliances," he added.

Benchmark 10-year Treasury yields are holding steady at 4.196% heading into the start of the New York trading session, while 2-year notes were pegged at 4.628%.

With Fed officials in a quiet period, requiring no public comments ahead of next week's meeting in Washington, the U.S. dollar index is trading in a narrow range against its global peers and was last marked 0.06% higher at 102.852.

On Wall Street, futures tied to the S&P 500 are indicating an opening bell gain of around 19 points, with the Dow Jones Industrial Average indicating a 140-point advance.

The tech-focused Nasdaq, which is up 7.77% for the year, is priced for a gain of around 95 points, with Tesla (TSLA) once again sliding into the red after ending the Wednesday session at a 10-month low.

In Europe, the regionwide Stoxx 600 was marked 0.35% higher in early Frankfurt trading, while Britain's FTSE 100 slipped 0.09% in London.

Overnight in Asia, the Nikkei 225 gained 0.29% as investors looked to a key series of wage negotiation figures from key unions that are likely to see the biggest year-on-year pay increases in three decades.

The broader MSCI ex-Japan benchmark, meanwhile, rose 0.18% into the close of trading.

Related: Veteran fund manager picks favorite stocks for 2024

bonds pandemic dow jones sp 500 nasdaq ftse stocks rate cut fed federal reserve home sales white house japan europe

Net Zero, The Digital Panopticon, & The Future Of Food

For-profit nursing homes are cutting corners on safety and draining resources with financial shenanigans − especially at midsize chains that dodge public scrutiny

Trump nearly derailed democracy once − here’s what to watch out for in reelection campaign

Riley Gaines Explains How Women’s Sports Are Rigged To Promote The Trans Agenda

Health Officials: Man Dies From Bubonic Plague In New Mexico

MIPIM 2024 Reflects Mixed Feelings on CRE Recovery

Analyst reviews Apple stock price target amid challenges

Delta Air Lines adds a new route travelers have been asking for

Five Aerospace Investments to Buy as Wars Worsen Copy

Stock Market Today: Stocks turn lower as factory inflation spikes, retail sales miss target

-

Uncategorized3 weeks ago

Uncategorized3 weeks agoAll Of The Elements Are In Place For An Economic Crisis Of Staggering Proportions

-

International6 days ago

International6 days agoEyePoint poaches medical chief from Apellis; Sandoz CFO, longtime BioNTech exec to retire

-

Uncategorized4 weeks ago

Uncategorized4 weeks agoCalifornia Counties Could Be Forced To Pay $300 Million To Cover COVID-Era Program

-

Uncategorized3 weeks ago

Uncategorized3 weeks agoApparel Retailer Express Moving Toward Bankruptcy

-

Uncategorized4 weeks ago

Uncategorized4 weeks agoIndustrial Production Decreased 0.1% in January

-

International6 days ago

International6 days agoWalmart launches clever answer to Target’s new membership program

-

Uncategorized4 weeks ago

Uncategorized4 weeks agoRFK Jr: The Wuhan Cover-Up & The Rise Of The Biowarfare-Industrial Complex

-

Uncategorized3 weeks ago

Uncategorized3 weeks agoGOP Efforts To Shore Up Election Security In Swing States Face Challenges