Uncategorized

Venturing A Perspective On The Drug Pricing Debate

Venturing A Perspective On The Drug Pricing Debate

Share this:

The perennial drug pricing debate has reached a fever pitch, as loud as it’s ever been over the past few decades. Politicians on both sides are bashing the drug industry with the typical talking points about exorbitant prices, countered of course by the expected talking points about innovation and impact from PhRMA and BIO. Even VC’s and biotech CEOs are actively engaged in letter-writing campaigns to support the industry.

This week Congress is considering a piece of proposed legislation, known as “The Lower Drug Costs Now Act” (or H.R.3), which is similar in form to many of the proposals from multiple presidential candidates (like Elizabeth Warren). Let there be no mistake: these proposals would fundamentally damage the landscape for biomedical innovation in the US.

Even the CBO models that these proposals would lead to a significant reduction in the development of new medicines. This is a very bad outcome for both society and the biopharma sector. I truly hope rational minds will prevail when the legislative process concludes.

Questions have been raised about whether these new pricing proposals will negatively affect early stage biotech venture capital flows and the behavior of the investment community (from causing a “nuclear winter” to those asking “well where else will VCs invest”). The answer is simple: of course they will affect investment.

As a front-line practitioner in early stage biotech venture capital, I can assure you that radical across-the-board cuts in the future pricing of innovative therapies will certainly affect both the scale and pace of investments in new biomedical startups.

I’d like to share my perspective in three sections. First, I’d like to frame some foundational assumptions about investing in new therapies and the implications of radical pricing changes. Second, before we can talk about solutions, we need to share a common understanding of the state of healthcare and how pharmaceuticals fit in. And lastly, I’ll close with my thoughts on a few real measures for pricing reform that make sense. Although far too many words, a nuanced topic like drug pricing needs context – so there’s plenty of it for those willing to read on.

First Principle

Over the last fifteen years, I’ve invested with one foundational assumption – a variant of the George Merck view that patients come before profits. It’s what I call the “first principle” of early stage biotech investing: if we can positively impact the lives of patients by discovering and developing an innovative new medicine, the system will reward that risk-taking with superlative investment returns.

We all know the talking points about biotech being long, costly, and risky: it takes an average of 15 years from idea to product, hundreds of millions of dollars in direct costs per program, and 90% of drugs fail before making it to market. These are the inconvenient truths of drug R&D, and I won’t go into them here.

But they markedly differentiate new therapeutic ventures from most other areas of venture capital; because of this challenging triad of features, early stage biotech venture investors can typically only really underwrite a portion of the R&D value chain. Most of us never see real revenues during the time course of our investment. If a company got started from scratch in drug discovery, we generally never even see new product launches within our 5-10 year investment cycle. I can’t even recall ever building a spreadsheet model with revenues and drug prices in it for any of our new biotech investments. You simply can’t model with any accuracy what the revenues will look like in 15 years when a future drug launches. When we start a drug discovery company, the time to market is too long, the costs to get there too big, and the unpredictability too vast to build a model that is remotely useful. What we do know, with some accuracy, is what the real world unmet needs are for patients, and how we might address their mortality or morbidity. Our new startup investment theses are usually framed purely with that in mind.

In line with that approach, venture investors like Atlas can aptly be called “risk capitalists”. We underwrite lots of different kinds of risk. Foremost is the science risk – making medicines is incredibly hard, as biology and chemistry are way more complicated than textbooks tell you. But there’s also team risk, execution risk, financing risk, competitive risk, etc… And we take on these risks over 5-10 year investment horizons.

Importantly, once we are in a private biotech investment, we also face real “exit risk” as we have no real liquidity in our portfolio. That is, the only way we can leave an investment and recycle profits into new funds (and thus new investments) is by truly exiting it: selling the company to a bigger biopharma, offering a share of the company to the public markets and trading out over time, or writing it off/walking away. Unlike traditional public investors, who can move their capital from one investment to the next, one sector to another, or even into cash on the sidelines – we can’t do any of that once our capital is deployed. This creates significant illiquidity, another form of long duration exit risk. All this means we must have real conviction about what the long range future looks like and the expectation that we’ll be compensated for locking up our capital for a decade or more. In short, we have to have confidence in our expectation that the “first principle” of early stage biotech investing will be intact.

Underwriting all of these risks, and appreciating where we operate in the ecosystem, early stage VC-backed biotechs typically aim to advance new drugs from idea to clinical proof of concept, and then pass the baton to downstream partners through an IPO or M&A to take the new potential medicine (and company) the rest of the way. These downstream partners are larger biopharma players and/or later stage investors like hedge and mutual funds. Because these new partners join us midway through the R&D journey, they are much closer to any potential product launch and market dynamics. These are the folks who rightfully do build spreadsheets, as any smart later stage player should. They do run NPVs from discounted cash flows. They run product launch scenarios. They take bets on late stage clinical outcomes and approvals. And, importantly, they model what drug pricing is likely to be.

This is where the ripple effects of poorly conceived drug pricing legislation can become a tsunami of risk for early stage investors like me. If these downstream partners see their models come down by 70% (like Warren’s explicit proposal or implied by H.R.3), it will have a huge impact on how they invest in (or not) our early stage biotechs. Without the availability of downstream capital, we can’t keep advancing new medicines. Even successful biotech companies will often burn capital without real revenues for 15-20 years. This means biotech, as a sector, is very sensitive to the actual and perceived availability of capital. These new pricing measures will almost certainly tighten capital flows and dramatically increase the risk profile of our early stage investments (especially financing risk, exit risk, illiquidity risk, etc) way beyond the already prodigious science risks we take.

As these aggregate risks go up, the required rate of return goes up to compensate for heightened probability of investment losses. And this leads to a more expensive “cost of capital”. In plain English, that means venture money will become scarcer and more expensive to raise in light of the elevated risks. This is the painful world we’ve been in before (as two examples, take the challenging periods of 2002-2004 and 2008-2010): the venture money supply tightened dramatically in those periods, after peaking exuberantly shortly before. Funding flows in venture-backed biotech have been exuberant over the past few years, but a step-change in risk will dramatically tighten available funding for biotechs; when VCs become more risk averse, it means less innovative science will be able to find adequate funding.

In light of all of these dynamics, in order to continue to invest in turning risky science into new medicines, we need to have faith that the future healthcare system in the US will respect the “first principle” of early stage biotech investing: if we deliver real value to patients we will be rewarded with outsized returns. Sadly, the current pricing legislation being debated raises real questions for me about its fidelity.

But only asserting that the current drug pricing proposals violate this first principle isn’t very constructive: what are some possible solutions to the challenge of rewarding innovation while addressing the cost of pharmaceuticals?

In order to get to that, we need to have a shared sense of the situation.

Observations about the US Healthcare System and Pharmaceuticals

Here are a dozen or so points about the US healthcare system and pharmaceuticals that are important to appreciate before discussing pricing reform. Many of these are well known, but I’ll try flesh out the less well-appreciated points.

- Healthcare has historically been growing as a share of GDP for decades, though has plateaued around 17-18% recently. Overall healthcare spending is a concern for many, and it’s a worthy debate to discuss whether in an affluent society we should be spending 18% of GDP on our healthcare. But that’s a broader point and not the topic at hand.

- Pharmaceuticals haven’t grown as a share of healthcare spend. Drugs remain 9-10% of total healthcare spend for decades. Recent data suggests aggregate drug prices actually went down for the first time in 40+ years in 2018, due to generics and pricing restraint. Although there are a number of egregious examples of price increases (which I’ll address below), the reality is aggregate national pharmaceutical spending is just not a major driver of healthcare spending in the US – its less then 10 cents of every dollar.

- Consumers have increasingly been paying larger share via out of pocket spending. Changes to health insurance, with larger copays and deductables, and “donut holes” in coverage, have created significant out of pocket costs to consumers. Much has already been described about this issue, and it’s an important one. This isn’t sustainable and needs to be addressed, especially for expensive specialty drugs.

- Pharmaceuticals are a more consistently priced and efficient tool for health impact than other medical interventions. Unlike health provider services, pharmaceutical products generally don’t dramatically vary in either cost or outcome in the same significant way other healthcare services do across the country. For example, the costs to a health care plan for an angioplasty/PCI after a heart attack can vary by 500% even in the same metro geography, depending on which hospital does the surgery (here). This massive variation doesn’t happen at the pharmacy, but is seen across a vast number of healthcare services (more examples from the Kaiser Family Foundation). If you aren’t near a top academic medical center, you may not get a best-in-class surgery or treatment; but if you are near a pharmacy and have insurance, as the vast majority of Americans do, you will typically be able to get best-in-class medicines. Because of that, drugs have the potential to democratize healthcare. If drugs are truly effective and reduce visits, sickness, and system costs, there’s no reason prescription medicines shouldn’t actually be a higher proportion of healthcare costs vs far less efficient medical services.

- Unlike all other healthcare expenditures, pharmaceuticals commoditize rapidly once the products are beyond their patent-protected exclusivity period. The comparison of Lipitor in 2003 vs today is worth reviewing: in 2003, Lipitor was ~$3800/year for healthcare plans, today it’s about $50/year, over a 95%+ drop in cost. In contrast, laproscopic appendectomies, a very rote and common surgery, went from an average of $8.5K in 2003 to over $20K in 2016. Full knee replacement surgery from $19K to $34K, both according to the Kaiser Family Foundation. The reality is despite the maturity of the surgical technique, healthcare services don’t go generic – they actually get more expensive for most providers, and at a faster rate than inflation. This is yet another reason effective pharmaceuticals are a very cost-efficient long-term medical intervention; over longer time horizons, generic competition captures a huge amount of cost and delivers it as a dividend to society.

- Generics are a major boon to society and to the future innovators in the pharma industry. As noted above, the expiry of patents and the loss of market exclusivity herald a massive commoditization of prices for most pharmaceutical products. Genericization puts about 10-15% of total industry revenues at risk of significant price erosion in any given period, and has done so for several decades. This is what creates the room for new innovator products in healthcare budgets. Today, 90% of the ~6 billion monthly prescriptions written each year in the US are filled with generic drugs, all of which were at one time more expensive branded drugs. In healthcare, generics are the gift that keeps on giving – and a gift from the original innovator. But interchangeable, generic biologics haven’t yet happened despite a trickle of biosimilar approvals, even after 20 years of discussion. This has become a moral issue and affront to the industry’s social contract, especially when many of the older biologic drugs are taking double-digit price increases even after being on the market for 15+ years. These are, in my opinion, egregious drug pricing examples that need to be addressed.

- The US healthcare system is stacked against lower drug prices. Almost every player in the healthcare system is actually incentivized for higher drug costs (e.g., PBMs, physician practices, hospitals, distributors, etc) because they get paid a percentage of list price value, or get rebates off of those values, or mark them up when they pass the bill onto patients’ insurers. Most players in the healthcare value chain, whether they admit it or not, financially benefit from high-priced drugs: the higher, the better. This actually creates barriers to real price competition in crowded classes, as well as challenges for the adoption of lower cost drugs (like biosimilars) that might threaten those large rebates/discounts/mark-ups.

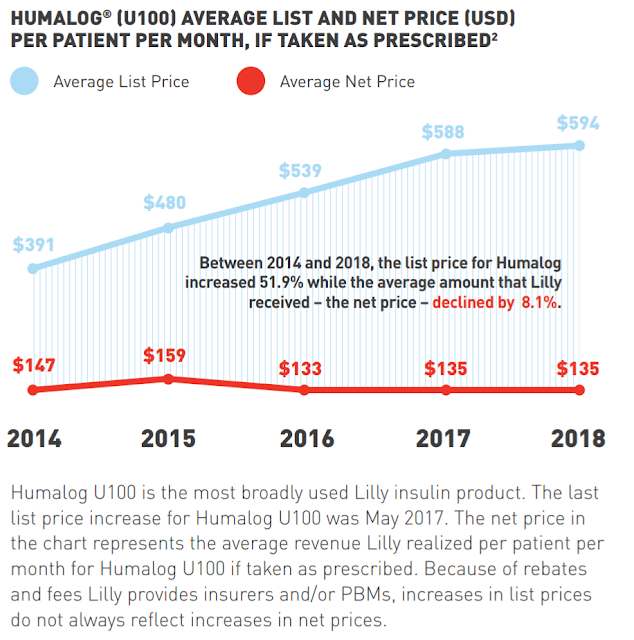

- List prices today do not transparently reflect pharmaceutical spending. The gross-to-net price differential distorts the market and has become a major issue. Pharmaceutical products have a list price for insurance companies, but this doesn’t reflect the value sent back to Pharma companies, as the system’s middleman extract their fees, rebates, and discounts. There is often a large (and lately increasing) delta between the list price of drugs and the net price back to the manufacturer. This has created a “gross-to-net bubble” that’s enormous, and is also enormously distorting to a discussion about drug prices. In the past few years, we have seen very small increases in net prices (1-2%). In fact, net prices increased only 0.3% in 2018, according to IQVIA; this is below the rate of consumer price inflation. As an example, branded insulin prices are commonly cited as having had egregious increases over time, and it’s true the list price increases have been very aggressive. But the net prices sent back to Pharma have often been very small if not negative. For a shocking image of this, check out the list-to-net price comparison of Humalog 100: $594 list price and a $135 net price after rebates. That captures the absurdity of the system. Adding insult to injury, that gross-to-net price differential isn’t passed on to consumers – it’s captured by the middleman usurpers in the healthcare system.

- Huge international price differentials exist for drugs across countries. It’s well appreciated that the US is paying more for most branded drugs, an average of 2.5x more according to Evercore. This reflects not only our higher GDP, but also a Faustian bargain that Pharma made around extracting marginal revenues decades ago (mentioned here). Pharma let smaller monopoly single payor systems drive down prices because they looked at it as incremental or marginal revenues after securing the largest market (the US). Unfortunately, the pricing gap is now so large that it’s no longer acceptable. It’s also a fact that the US has been subsidizing the world’s drug R&D engine, which is also likely why most of Pharma have relocated their R&D infrastructure to the US while shrinking their footprints elsewhere.

- Many innovators became addicted to US drug price increases. Over the past 20 years, Big Pharma revenue growth has become increasingly reliant on biannual US price increases, so much so the vast majority of revenue growth of the top 50 products last year was driven by price rather than volume. With industry branded drug volumes collapsing by 40% over the past six years (from 1B prescriptions in 2011 to 600M prescriptions in 2017), pricing in aggregate has been the only growth driver – either price increases of existing products, or higher pricing of new products. As I wrote in a 2016 blog on Innovators vs Exploiters, “The simple fact is the industry – including the Innovators – have gotten irresponsibly addicted to large biannual price increases for most of its products… Innovators need to take responsibility for these aggressive increases and justify them more clearly going forward.” These biannual price increases have moderated somewhat in recent years, with efforts like Brent Saunders’ price restraint pledge at Allergan. I’m very sympathetic to the claims that we need to see continued moderation in the price increases of older, existing branded drugs – unless there’s been meaningful changes to the drug’s clinical profile to justify the increase (from post-market clinical trials, for instance). And for the Exploiters who take old generic single-source products and jack up prices, in the words of Scott Gottlieb, there is no moral imperative to price gouge. It’s just not acceptable. I am hopeful with the FDA’s support of multi-source generics that these Exploiters go away.

- The mix of specialty vs primary care drugs has fundamentally changed the pharmaceutical landscape. High-priced, low-volume products are increasingly the norm. The majority of FDA approvals today now address only orphan drug populations, many of them are for ultra-orphan indications (below 10K in prevalence). This shift towards low volume products has changed the pricing paradigm, now often leading to inverse prevalence-based pricing. To me, the issue is less about the price and more about their cost effectiveness. If these new medicines truly change the lives of patients with serious orphan diseases, keeping them healthier and out of intensive hospital services or early mortality, it should be easy to justify the prices with a value-based pricing concept. With one-and-done gene therapies, this premise is even more clear. That said, the US healthcare system needs to figure out how to handle these new types of “curative” or near-curative single treatment therapies.

There are many other relevant observations that could be shared about the US healthcare system and role of pharmaceuticals, but these are certainly some of the important ones.

644371744

By laying out these points though, it helps to focus attention on the things that matter for drug pricing reform: delivering value-based pricing and cost effectiveness, improving price transparency in the US system, leveraging the power generics more broadly, and reducing global pricing differentials, among other things.

Unfortunately, it’s an election year and politicians are looking for political points. It doesn’t feel good to attack the hospital in your constituency, so politicians tend not to look at healthcare services. But Pharma is always an easy target, and so the same tired drug pricing levers come up as they have for two decades: direct price negotiation (aka. price controls by a monopoly purchaser), drug importation, and international reference pricing. These aren’t the right solutions.

I’m not a policy wonk, but here are my thoughts.

A Few Drug Pricing Policy Concepts (And Recommendations for Pharma)

Encourage value-based pricing models based on cost-effective therapies – and foster more experimentation in pricing models. Pricing “what the market will bear” isn’t a viable long-term strategy in a three-tiered demand system (i.e., where the user of the product is different from the decider of product choice who is different from the payor). Instead, Pharma needs to justify much more explicitly the pricing assumptions made using value-based principles: what’s the value of the drug to the patient, caregivers, healthcare system, and society. By definition that’s hard and somewhat subjective to measure, but we need to communicate more clearly on these value aspects. The industry also needs to support objective metrics for doing health technology assessments of cost-effectiveness. Good drugs can easily justify their prices. For example, the original ICER cost effectiveness assessment of SMA gene therapy Zolgensma, the world’s most expensive drug, said it was within the “upper bounds” of the cost effectiveness framework. Of course, where the rubber meets the road on the concept of value-based pricing is where the questions arise, so understanding the exact methodologies and cost-effectiveness benchmarks is critical. Pharma needs to be at the vanguard of thought leadership in the evolution of value-based pricing models, rather than ceding intellectual ownership of this space as just a recipient of the outputs; public-private engagement to work with groups like ICER feels like a positive step forward. More experimentation on drug pricing is important, with things like pay for performance guarantees, payer volume-linked pricing (like what Alnylam has recently done), and “all you can treat” models akin to the Netflix subscription model. Legislation is needed to open the flood gates for experimentation around these topics – which right now are often suffocated by bureaucratic rules around Medicare Best Price restrictions and the like.

Facilitate greater transparency on healthcare costs and money flows – for patients and for industry players. We need to cap out of pocket costs for patients; insurance companies need to protect patients from healthcare bankruptcies and huge out of pocket expenditures – this is the essence of insurance, to protect against catastrophic outcomes. We also need to pop the “gross to net bubble” on drug prices; sending scarce healthcare resources into the pocket of middlemen in the healthcare system, where they aren’t passed on to consumers, is wrong. Legislative action needs to consider addressing both runaway patient out-of-pocket payments (an insurance issue), at the same time forcing open some transparency on where the list price rebates and discounting “savings” actually go (linking them to help reduce out of pocket costs, perhaps).

Continue expanding more generic competition, especially to establish interchangeable generic biologics. Right now over 9 out of 10 prescriptions in the US are for generic drugs, and this is a good thing. But biologics now represent 70% of the revenues of the top 15 drugs in the US. So if we are to continue to secure the benefits of commodity-priced generics, we need truly generic biologics. Given their complexity, initiatives like compulsory cell bank technology transfer at the end of a patent life (to groups like ATCC or others) to enable generic manufacturers makes sense. RA Capital’s Jessica Sagers and Peter Kolchinsky recently wrote a piece suggesting that a new regulatory body could provide oversight to create the “go generic” pathway for complex biologics; this seems like a smart concept. If the social contract is a real concept in our industry, than we need to see commodity priced generic biologic drugs in the near future. Any new drug pricing legislation needs to ensure a clear pathway here.

Reduce global price differentials for pharmaceuticals. Drug importation isn’t the answer, especially from countries with price controls (enabled by the Faustian pricing bargain described above). But this gap in pricing is becoming a trade issue. While differential pricing is commonplace in many areas of commerce, and not wrong per se, it needs to be constructed in moderation – especially for countries with similar GDP-per-capita countries. Elderly consumers often get cheaper tickets to the movies; if, by example, Britain wants to be the elderly consumer of pharmaceutical innovation, then so be it – within moderation. That decision will likely have other unintended consequences around things like R&D jobs and the like. This issue isn’t easy to solve (e.g., witness the Vertex-UK price negotiations), but has to involve some combination of higher prices from European/Asian payors and lower prices in the US. This is as much a trade issue as a legislative issue.

Promote ways to reduce the cost of capital for loss-making enterprises. In the likely future where drug pricing policy at least in part hampers risk capital, we need to figure out additional and less expensive funding sources to support emerging biotech companies, including policy measures like R&D tax credits or trading net operating losses (where buyers purchase losses for their tax benefits, thus sellers access lower cost funding). With $15-20B spent per year for R&D by private venture-backed biotechs, these policy improvements could enable billions in additional risk capital to make up for the likely equity capital outflows. Legislation should consider these efforts in particular for loss-making pharma R&D expenditures.

Those are just a few things any comprehensive drug policy legislation should consider – while emphatically reinforcing the message that the “first principle” will be protected under any future outcome – which is, again paraphrasing George Merck, that if we deliver real value to patients, the returns will follow.

The post Venturing A Perspective On The Drug Pricing Debate appeared first on LifeSciVC.

Uncategorized

Airline, travel companies face Chapter 11 bankruptcy, default risk

New data from Creditsafe shows that three big-name brands face significant cash issues.

Share this:

It's actually fairly rare that a company files for Chapter 11 bankruptcy without throwing off signs that it's in deep financial trouble. Observant customers sometimes see the signs.

You might notice lower staffing levels or poor inventory in a retail setting. Restaurants facing financial troubles might drop the quality of their ingredients, cut portion sizes, or find other ways to cut corners.

Related: Fast-food chain closes restaurants after Chapter 11 bankruptcy

It's generally impossible to cut your way to a good financial position unless you were making huge mistakes in the first place. A company might find some savings by examining its operations and focuing on waste in areas customers don't see, but giving people less almost never works.

In many businesses, especially when companies are publicly traded, signs of upcoming financial trouble are obvious.

Public companies have to report their financial results and when there's more money going out than coming in, and cash balances get low, observant analysts can see a company likely to default on its bills that may be headed for bankruptcy well before it happens.

CreditSafe Head of Brand Ragini Bhalla recently shared her company's Financial & Bankruptcy Outlook: Transportation Report and some comments on it with TheStreet.

The report shows that three big-name companies in the travel/transportation space are facing significant financial risk, which is reflected in their stock prices. Bhalla gave some color as to why companies in those markets are struggling.

Image source: Shutterstock

The transportation industry faces a crisis

Bhalla shared her thoughts on what Creditsafe found.

"We are reflecting on the current challenges faced by transportation companies and the total industry outlook. During the pandemic, M&A activity in the industry soared, as transportation players and investors made deals to extend capabilities and acquire high-performing assets. To that end, deal values soared from $51 billion in 2020 to more than $150 billion in 2021, before it dipped to $95 billion in 2022," she said in an email to TheStreet.

Bhalla said she sees a different pattern in 2024.

"While M&A activity in the transportation industry cooled down in 2023, industry insiders are projecting that 2024 will be the year of consolidation. If that’s the case, then it will be more important than ever for both sides (sellers and buyers) to do their due diligence," she wrote.

Not every company that would benefit from being acquired will survive the M&A scrutiny.

"This should include various elements, such as running business credit checks on potential acquisitions to make sure they would be a good investment and aren’t in dire financial straits. It should also include running comprehensive compliance checks to make sure potential acquisitions aren’t violating sanctions, haven’t been convicted of regulatory violations, and aren’t involved in unethical practices like bribery, corruption, fraud, and the use of child/forced labor," she added.

One airline, two rental cars are at risk

Spirit Airlines (SAVE) has been on unofficial bankruptcy watch since the company's merger with JetBlue (JBLU) fell apart. There are real questions as to whether the super-low-cost airline model works, and Creditsafe sees a real risk of the airline ending up filing for Chapter 11 bankruptcy.

"Earlier this year, Spirit Airlines said it was looking to refinance its debt and hopes to refinance $1.1 billion of debt due in 2025," according to Creditsafe. "To make matters worse, the airline doesn’t have a stable track record of paying bills on time."

Not paying bills on time is often a sign that a company is running out of cash.

"Late payments increased over several months in 2023. For example, the number of late payments (1-30 days) rose from 7.00% in September 2023 to 30.87% in October 2023. A similar pattern occurred soon after when the number of late payments (1-30 days) rose from 6.37% in November 2023 to 30.54% in December 2023 and then again to 51.08% in January 2024," Creditsafe data showed.

Investors are shying from the stock. Shares were at $4.29 down 73.8% on the year as of Friday.

Two rental car companies, Avis Budget Group (CAR) and Hertz (HTZ) are facing similar woes.

"Avis Budget Group's long-term debt has consistently increased for the last three years, and how late the company paid its bills spiked drastically from 8 days late in March to 31 days in April and remained high until September 2023," Creditsafe shared.

Hertz has been following a similar path.

"The company’s number of delinquent payments (91+ days) increased consistently during the second half of 2023. For instance, the number of delinquent payments (91+ days) rose from 4.64% in August to 6.90% in September, then rose again to 10.73% in October 2023, indicating it is having trouble paying its bills," according to Creditsafe.

Avis Budget closed Friday at $107.70 and are down 39.2% this year. Hertz finished Friday at $7.58, down 25.7% on the year.

bankruptcy default pandemicUncategorized

Default: San Francisco Four Seasons Hotel Investors $3 Million Late On Loan As Foreclosure Looms

Default: San Francisco Four Seasons Hotel Investors $3 Million Late On Loan As Foreclosure Looms

Westbrook Partners, which acquired the San…

Share this:

Westbrook Partners, which acquired the San Francisco Four Seasons luxury hotel building, has been served a notice of default, as the developer has failed to make its monthly loan payment since December, and is currently behind by more than $3 million, the San Francisco Business Times reports.

Westbrook, which acquired the property at 345 California Center in 2019, has 90 days to bring their account current with its lender or face foreclosure.

Related

- Fed Fears "Notable" Financial System Vulnerability As Renowned CRE Investor Tells Team 'Stop All NYC Underwriting'

- The State Of Commercial Real Estate, In Charts

- "Who Could Be Next": Top Canadian Pension Fund Sells Manhattan Office Tower For $1, Sparking Firesale Panic

- "Heightened Risks": Goldman Points To Leading CRE Indicator That Shows Pain Train Not Over

As SF Gate notes, downtown San Francisco hotel investors have had a terrible few years - with interest rates higher than their pre-pandemic levels, and local tourism continuing to suffer thanks to the city's legendary mismanagement that has resulted in overlapping drug, crime, and homelessness crises (which SF Gate characterizes as "a negative media narrative).

Last summer, the owner of San Francisco’s Hilton Union Square and Parc 55 hotels abandoned its loan in the first major default. Industry insiders speculate that loan defaults like this may become more common given the difficult period for investors.

At a visitor impact summit in August, a senior director of hospitality analytics for the CoStar Group reported that there are 22 active commercial mortgage-backed securities loans for hotels in San Francisco maturing in the next two years. Of these hotel loans, 17 are on CoStar’s “watchlist,” as they are at a higher risk of default, the analyst said. -SF Gate

The 155-room Four Seasons San Francisco at Embarcadero currenly occupies the top 11 floors of the iconic skyscrper. After slow renovations, the hotel officially reopened in the summer of 2021.

"Regarding the landscape of the hotel community in San Francisco, the short term is a challenging situation due to high interest rates, fewer guests compared to pre-pandemic and the relatively high costs attached with doing business here," Alex Bastian, President and CEO of the Hotel Council of San Francisco, told SFGATE.

Heightened Risks

In January, the owner of the Hilton Financial District at 750 Kearny St. - Portsmouth Square's affiliate Justice Operating Company - defaulted on the property, which had a $97 million loan on the 544-room hotel taken out in 2013. The company says it proposed a loan modification agreement which was under review by the servicer, LNR Partners.

Meanwhile last year Park Hotels & Resorts gave up ownership of two properties, Parc 55 and Hilton Union Square - which were transferred to a receiver that assumed management.

In the third quarter of 2023, the most recent data available, the Hilton Financial District reported $11.1 million in revenue, down from $12.3 million from the third quarter of 2022. The hotel had a net operating loss of $1.56 million in the most recent third quarter.

Occupancy fell to 88% with an average daily rate of $218 in the third quarter compared with 94% and $230 in the same period of 2022. -SF Chronicle

According to the Chronicle, San Francisco's 2024 convention calendar is lighter than it was last year - in part due to key events leaving the city for cheaper, less crime-ridden places like Las Vegas.

Uncategorized

Correcting the Washington Post’s 11 Charts That Are Supposed to Tell Us How the Economy Changed Since Covid

The Washington Post made some serious errors or omissions in its 11 charts that are supposed to tell us how Covid changed the economy. Wages Starting with…

Share this:

{kind=link}

{kind=link}

The Washington Post made some serious errors or omissions in its 11 charts that are supposed to tell us how Covid changed the economy.

Wages

Starting with its second chart, the article gives us an index of average weekly wages since 2019. The index shows a big jump in 2020, which then falls off in 2021 and 2022, before rising again in 2023.

It tells readers:

“Many Americans got large pay increases after the pandemic, when employers were having to one-up each other to find and keep workers. For a while, those wage gains were wiped out by decade-high inflation: Workers were getting larger paychecks, but it wasn’t enough to keep up with rising prices.”

That actually is not what its chart shows. The big rise in average weekly wages at the start of the pandemic was not the result of workers getting pay increases, it was the result of low-paid workers in sectors like hotels and restaurants losing their jobs.

The number of people employed in the low-paying leisure and hospitality sector fell by more than 8 million at the start of the pandemic. Even at the start of 2021 it was still down by over 4 million.

Laying off low-paid workers raises average wages in the same way that getting the short people to leave raises the average height of the people in the room. The Washington Post might try to tell us that the remaining people grew taller, but that is not what happened.

The other problem with this chart is that it is giving us weekly wages. The length of the average workweek jumped at the start of the pandemic as employers decided to work the workers they had longer hours rather than hire more workers. In January of 2021 the average workweek was 34.9 hours, compared to 34.4 hours in 2019 and 34.3 hours in February.

This increase in hours, by itself, would raise weekly pay by 2.0 percent. As hours returned to normal in 2022, this measure would misleadingly imply that wages were falling.

It is also worth noting that the fastest wage gains since the pandemic have been at the bottom end of the wage distribution and the Black/white wage gap has fallen to its lowest level on record.

Saving Rates

The third chart shows the saving rate since 2019. It shows a big spike at the start of the pandemic, as people stopped spending on things like restaurants and travel and they got pandemic checks from the government. It then falls sharply in 2022 and is lower in the most recent quarters than in 2019.

The piece tells readers:

“But as the world reopened — and people resumed spending on dining out, travel, concerts and other things that were previously off-limits — savings rates have leveled off. Americans are also increasingly dip into rainy-day funds to pay more for necessities, including groceries, housing, education and health care. In fact, Americans are now generally saving less of their incomes than they were before the pandemic.

This is an incomplete picture due to a somewhat technical issue. As I explained in a blogpost a few months ago, there is an unusually large gap between GDP as measured on the output side and GDP measured on the income side. In principle, these two numbers should be the same, but they never come out exactly equal.

In recent quarters, the gap has been 2.5 percent of GDP. This is extraordinarily large, but it also is unusual in that the output side is higher than the income side, the opposite of the standard pattern over the last quarter century.

It is standard for economists to assume that the true number for GDP is somewhere between the two measures. If we make that assumption about the data for 2023, it would imply that income is somewhat higher than the data now show and consumption somewhat lower.

In that story, as I showed in the blogpost, the saving rate for 2023 would be 6.8 percent of disposable income, roughly the same as the average for the three years before the pandemic. This would mean that people are not dipping into their rainy-day funds as the Post tells us. They are spending pretty much as they did before the pandemic.

Credit Card Debt

The next graph shows that credit card debt is rising again, after sinking in the pandemic. The piece tells readers:

“But now, debt loads are swinging higher again as families try to keep up with rising prices. Total household debt reached a record $17.5 trillion at the end of 2023, according to the Federal Reserve Bank of New York. And, in a worrisome sign for the economy, delinquency rates on mortgages, car loans and credit cards are all rising, too.”

There are several points worth noting here. Credit card debt is rising, but measured relative to income it is still below where it was before the pandemic. It was 6.7 percent of disposable income at the end of 2019, compared to 6.5 percent at the end of last year.

The second point is that a major reason for the recent surge in credit card debt is that people are no longer refinancing mortgages. There was a massive surge in mortgage refinancing with the low interest rates in 2020-2021.

Many of the people who refinanced took additional money out, taking advantage of the increased equity in their home. This channel of credit was cut off when mortgage rates jumped in 2022 and virtually ended mortgage refinancing. This means that to a large extent the surge in credit card borrowing is simply a shift from mortgage debt to credit card debt.

The point about total household debt hitting a record can be said in most months. Except in the period immediately following the collapse of the housing bubble, total debt is almost always rising.

And the rise in delinquencies simply reflects the fact that they had been at very low levels in 2021 and 2022. For the most part, delinquency rates are just getting back to their pre-pandemic levels, which were historically low.

Grocery Prices and Gas Prices

The next two charts show the patterns in grocery prices and gas prices since the pandemic. It would have been worth mentioning that every major economy in the world saw similar run-ups in prices in these two areas. In other words, there was nothing specific to U.S. policy that led to a surge in inflation here.

The Missing Charts

There are several areas where it would have been interesting to see charts which the Post did not include. It would have been useful to have a chart on job quitters, the number of people who voluntarily quit their jobs during the pandemic. In the tight labor markets of 2021 and 2022 the number of workers who left jobs they didn’t like soared to record levels, as shown below.

The vast majority of these workers took other jobs that they liked better. This likely explains another item that could appear as a graph, the record level of job satisfaction.

In a similar vein there has been an explosion in the number of people who work from home at least part-time. This has increased by more than 17 million during the pandemic. These workers are saving themselves thousands of dollars a year on commuting costs and related expenses, as well as hundreds of hours spent commuting.

Finally, there has been an explosion in the use of telemedicine since the pandemic. At the peak, nearly one in four visits with a health care professional was a remote consultation. This saved many people with serious health issues the time and inconvenience associated with a trip to a hospital or doctor’s office. The increased use of telemedicine is likely to be a lasting gain from the pandemic.

The World Has Changed

The pandemic will likely have a lasting impact on the economy and society. The Washington Post’s charts captured part of this story, but in some cases misrepr

The post Correcting the Washington Post’s 11 Charts That Are Supposed to Tell Us How the Economy Changed Since Covid appeared first on Center for Economic and Policy Research.

federal reserve pandemic mortgage rates gdp interest rates

Women’s basketball is gaining ground, but is March Madness ready to rival the men’s game?

Default: San Francisco Four Seasons Hotel Investors $3 Million Late On Loan As Foreclosure Looms

Correcting the Washington Post’s 11 Charts That Are Supposed to Tell Us How the Economy Changed Since Covid

Airline, travel companies face Chapter 11 bankruptcy, default risk

-

Uncategorized4 weeks ago

Uncategorized4 weeks agoAll Of The Elements Are In Place For An Economic Crisis Of Staggering Proportions

-

International1 week ago

International1 week agoEyePoint poaches medical chief from Apellis; Sandoz CFO, longtime BioNTech exec to retire

-

Spread & Containment5 days ago

Spread & Containment5 days agoIFM’s Hat Trick and Reflections On Option-To-Buy M&A

-

Uncategorized1 month ago

Uncategorized1 month agoCalifornia Counties Could Be Forced To Pay $300 Million To Cover COVID-Era Program

-

Uncategorized3 weeks ago

Uncategorized3 weeks agoApparel Retailer Express Moving Toward Bankruptcy

-

Uncategorized1 month ago

Uncategorized1 month agoIndustrial Production Decreased 0.1% in January

-

International1 week ago

International1 week agoWalmart launches clever answer to Target’s new membership program

-

Uncategorized1 month ago

Uncategorized1 month agoRFK Jr: The Wuhan Cover-Up & The Rise Of The Biowarfare-Industrial Complex