Uncategorized

Using blockchain technology to combat retail theft

Blockchain technology may be a solution when it comes to anti-theft measures for retailers.

The retail industry is one of the most…

Share this:

Blockchain technology may be a solution when it comes to anti-theft measures for retailers.

The retail industry is one of the most important sectors of the United States economy. Unfortunately, the COVID-19 pandemic has left the trillion-dollar retail sector vulnerable to in-store theft.

Findings from the National Retail Federation’s 2022 Retail Security Survey show that retail losses from stolen goods increased to $94.5 billion in 2021, up from $90.8 billion in 2020. Some retailers also have to lock away certain products to prevent theft, which may lead to decreased sales due to consumers’ inability to access goods.

Retailers look toward blockchain to solve retail theft

Given these extreme measures, many innovative retailers have started looking toward technology to combat retail theft. For example, Lowe’s, an American home improvement retailer, has recently implemented a proof-of-concept called Project Unlock, which uses radio frequency identification (RFID) chips, Internet of Things sensors and blockchain technology. The solution is currently being tested in several Lowe’s stores in the United States.

Josh Shabtai, senior director of ecosystem practice at Lowe’s Innovation Labs — Lowe’s tech wing that developed Project Unlock — told Cointelegraph that Project Unlock aims to explore emerging technology to help curb theft while creating better customer experiences.

Recent: What is institutional DeFi, and how can banks benefit?

To accomplish this, Shabtai explained that RFID chips are used to activate specific Lowes’ power tools at the point of purchase. “So if a customer steals a power tool, it won’t work,” he said.

Shabtai noted that RFID chips are a low-cost solution that many retailers use to prevent theft. According to the National Retail Federation’s 2022 Retail Security Survey, 38.6% of retailers already implement or plan to implement RFID systems. However, Shabtai explained that combining RFID systems with a blockchain network can provide retailers with a transparent, tamper-proof record to track in-store purchases. He said:

“Through Project Unlock, a unique ID is registered and assigned to each of our power tools. When that product is purchased, the RFID system activates the power tool for use. At the same time, the transaction can be viewed by anyone, since that information gets recorded to a public blockchain network.”

Mehdi Sarkeshi, lead project manager at Project Unlock, told Cointelegraph that Project Unlock is based on the Ethereum network. Sarkeshi elaborated that each product under Project Unlock is tied to a pre-minted nonfungible token (NFT), or a digital twin, that will receive a status change upon purchase.

“A product’s NFT undergoes a status change when it is either sold by Lowe’s, if it has been stolen, or if the status is unknown. All of this information is publicly visible to customers and resellers since it’s recorded on the Ethereum blockchain. We have essentially built a purchase authenticity provenance for Lowes’ power tools,” he said.

While the concept behind Project Unlock is innovative for a large retailer, David Menard, CEO of asset verification platform Real Items, told Cointelegraph that his firm has been exploring a similar solution. “Traditionally, RFID tags prevent theft, so this problem has already been solved,” he said. Given this, Menard noted that Real Items combines digital identity with physical products to ensure that stolen items can be accounted for. He said:

“If physical items are paired with digital twins, then retailers can know exactly what was stolen, from where and from which product batch. Retailers can understand this with more clarity versus information generated by RFID systems.”

According to Menard, Real Items currently has a memorandum of understanding with SmartLabel, a digital platform that generates QR codes for brands and retailers to provide consumers with detailed product information. He shared that Real Items plans to implement “digital product passports” with SmartLabel products in the future. “We view digital product passports as the foundation for storing information about a product throughout a product’s life cycle,” he said.

Menard further explained that Real Items uses the Polygon network to store product information. It’s important to point out that this model differs from Project Unlock since a blockchain network is only used here to record information about a certain item. “We use a product’s digital twin — also known as its NFT — for engagement. It can be tied to anti-theft, but it’s more about providing retailers with useful data.”

While the solutions being developed by Lowe’s Innovation Labs and Real Items could be a game-changer for retailers, the rise of the metaverse may also help curb retail theft. According to McKinsey’s “Value Creation in the Metaverse” report, by 2030, the metaverse could generate $4 trillion to $5 trillion across consumer and enterprise use cases. The report notes that this includes the retail sector.

Marjorie Hernandez, managing director of LUKSO — a digital lifestyle Web3 platform — told Cointelegraph that designer brands like Prada and Web3 marketplaces like The Dematerialised, where she is also CEO, are already using NFT redemption processes.

Hernandez explained that this allows communities to purchase a digital good in a metaverse-like environment, which can then be redeemed for a physical item in store. She said:

“This redemption process allows retailers to explore new ways to authenticate products on-chain and provide a more sustainable production process with made-to-order demand. This also creates a new and direct access channel between creators and consumers beyond point of sale.”

Hernandez believes that more retailers will explore digital identities for lifestyle goods in the coming year. “This allows brands, designers and users to finally have a transparent solution for many of the problems facing the retail industry today, like counterfeit goods and theft.”

Will retailers adopt blockchain solutions to combat theft?

Although blockchain could help solve in-store theft moving forward, retailers may be hesitant to adopt the technology for several reasons. For instance, blockchain’s association with cryptocurrency may be a pain point for enterprises. Recent events like the collapse of FTX reinforce this.

Yet, Shabtai remains optimistic, noting that Lowe’s Innovation Labs believes that it’s important to consider new technologies to better understand what is viable. “Through Project Unlock, we have proven that blockchain technology is valuable. We hope this can serve as a proof point for other retailers considering a similar solution,” he remarked. Shabtai added that Lowe’s Innovation Labs plans to evolve its solution beyond power tools moving forward.

Recent: Redeeming physical NFTs: Easier said than done?

While notable, Sarkeshi pointed out that it may be challenging for consumers to understand the value of using blockchain to record transactions. “For instance, if I’m a customer buying a second-hand product, why should I care if it was stolen,” he said. Given this, Sarkeshi believes that a shift in customer mindset must occur for such a solution to be entirely successful. He said:

“It’s a culture building challenge. Some customers will initially not feel good about buying a stolen product, but we need this to resonate across the board. We want customers to know that when a product is stolen, everyone across the supply chain gets hurt. Building that culture may be challenging, but I believe this will happen in the long term.”cryptocurrency ethereum blockchain pandemic covid-19

Uncategorized

One city held a mass passport-getting event

A New Orleans congressman organized a way for people to apply for their passports en masse.

Share this:

While the number of Americans who do not have a passport has dropped steadily from more than 80% in 1990 to just over 50% now, a lack of knowledge around passport requirements still keeps a significant portion of the population away from international travel.

Over the four years that passed since the start of covid-19, passport offices have also been dealing with significant backlog due to the high numbers of people who were looking to get a passport post-pandemic.

Related: Here is why it is (still) taking forever to get a passport

To deal with these concurrent issues, the U.S. State Department recently held a mass passport-getting event in the city of New Orleans. Called the "Passport Acceptance Event," the gathering was held at a local auditorium and invited residents of Louisiana’s 2nd Congressional District to complete a passport application on-site with the help of staff and government workers.

'Come apply for your passport, no appointment is required'

"Hey #LA02," Rep. Troy A. Carter Sr. (D-LA), whose office co-hosted the event alongside the city of New Orleans, wrote to his followers on Instagram (META) . "My office is providing passport services at our #PassportAcceptance event. Come apply for your passport, no appointment is required."

More Travel:

- A new travel term is taking over the internet (and reaching airlines and hotels)

- The 10 best airline stocks to buy now

- Airlines see a new kind of traveler at the front of the plane

The event was held on March 14 from 10 a.m. to 1 p.m. While it was designed for those who are already eligible for U.S. citizenship rather than as a way to help non-citizens with immigration questions, it helped those completing the application for the first time fill out forms and make sure they have the photographs and identity documents they need. The passport offices in New Orleans where one would normally have to bring already-completed forms have also been dealing with lines and would require one to book spots weeks in advance.

These are the countries with the highest-ranking passports in 2024

According to Carter Sr.'s communications team, those who submitted their passport application at the event also received expedited processing of two to three weeks (according to the State Department's website, times for regular processing are currently six to eight weeks).

While Carter Sr.'s office has not released the numbers of people who applied for a passport on March 14, photos from the event show that many took advantage of the opportunity to apply for a passport in a group setting and get expedited processing.

Every couple of months, a new ranking agency puts together a list of the most and least powerful passports in the world based on factors such as visa-free travel and opportunities for cross-border business.

In January, global citizenship and financial advisory firm Arton Capital identified United Arab Emirates as having the most powerful passport in 2024. While the United States topped the list of one such ranking in 2014, worsening relations with a number of countries as well as stricter immigration rules even as other countries have taken strides to create opportunities for investors and digital nomads caused the American passport to slip in recent years.

A UAE passport grants holders visa-free or visa-on-arrival access to 180 of the world’s 198 countries (this calculation includes disputed territories such as Kosovo and Western Sahara) while Americans currently have the same access to 151 countries.

stocks pandemic covid-19 grantsUncategorized

Fast-food chain closes restaurants after Chapter 11 bankruptcy

Several major fast-food chains recently have struggled to keep restaurants open.

Share this:

Competition in the fast-food space has been brutal as operators deal with inflation, consumers who are worried about the economy and their jobs and, in recent months, the falling cost of eating at home.

Add in that many fast-food chains took on more debt during the covid pandemic and that labor costs are rising, and you have a perfect storm of problems.

It's a situation where Restaurant Brands International (QSR) has suffered as much as any company.

Related: Wendy's menu drops a fan favorite item, adds something new

Three major Burger King franchise operators filed for bankruptcy in 2023, and the chain saw hundreds of stores close. It also saw multiple Popeyes franchisees move into bankruptcy, with dozens of locations closing.

RBI also stepped in and purchased one of its key franchisees.

"Carrols is the largest Burger King franchisee in the United States today, operating 1,022 Burger King restaurants in 23 states that generated approximately $1.8 billion of system sales during the 12 months ended Sept. 30, 2023," RBI said in a news release. Carrols also owns and operates 60 Popeyes restaurants in six states."

The multichain company made the move after two of its large franchisees, Premier Kings and Meridian, saw multiple locations not purchased when they reached auction after Chapter 11 bankruptcy filings. In that case, RBI bought select locations but allowed others to close.

Image source: Chen Jianli/Xinhua via Getty

Another fast-food chain faces bankruptcy problems

Bojangles may not be as big a name as Burger King or Popeye's, but it's a popular chain with more than 800 restaurants in eight states.

"Bojangles is a Carolina-born restaurant chain specializing in craveable Southern chicken, biscuits and tea made fresh daily from real recipes, and with a friendly smile," the chain says on its website. "Founded in 1977 as a single location in Charlotte, our beloved brand continues to grow nationwide."

Like RBI, Bojangles uses a franchise model, which makes it dependent on the financial health of its operators. The company ultimately saw all its Maryland locations close due to the financial situation of one of its franchisees.

Unlike. RBI, Bojangles is not public — it was taken private by Durational Capital Management LP and Jordan Co. in 2018 — which means the company does not disclose its financial information to the public.

That makes it hard to know whether overall softness for the brand contributed to the chain seeing its five Maryland locations after a Chapter 11 bankruptcy filing.

Bojangles has a messy bankruptcy situation

Even though the locations still appear on the Bojangles website, they have been shuttered since late 2023. The locations were operated by Salim Kakakhail and Yavir Akbar Durranni. The partners operated under a variety of LLCs, including ABS Network, according to local news channel WUSA9.

The station reported that the owners face a state investigation over complaints of wage theft and fraudulent W2s. In November Durranni and ABS Network filed for bankruptcy in New Jersey, WUSA9 reported.

"Not only do former employees say these men owe them money, WUSA9 learned the former owners owe the state, too, and have over $69,000 in back property taxes."

Former employees also say that the restaurant would regularly purchase fried chicken from Popeyes and Safeway when it ran out in their stores, the station reported.

Bojangles sent the station a comment on the situation.

"The franchisee is no longer in the Bojangles system," the company said. "However, it is important to note in your coverage that franchisees are independent business owners who are licensed to operate a brand but have autonomy over many aspects of their business, including hiring employees and payroll responsibilities."

Kakakhail and Durranni did not respond to multiple requests for comment from WUSA9.

bankruptcy pandemicUncategorized

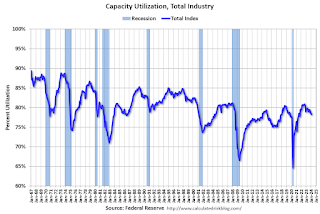

Industrial Production Increased 0.1% in February

From the Fed: Industrial Production and Capacity Utilization

Industrial production edged up 0.1 percent in February after declining 0.5 percent in January. In February, the output of manufacturing rose 0.8 percent and the index for mining climbed 2.2 p…

Share this:

Industrial production edged up 0.1 percent in February after declining 0.5 percent in January. In February, the output of manufacturing rose 0.8 percent and the index for mining climbed 2.2 percent. Both gains partly reflected recoveries from weather-related declines in January. The index for utilities fell 7.5 percent in February because of warmer-than-typical temperatures. At 102.3 percent of its 2017 average, total industrial production in February was 0.2 percent below its year-earlier level. Capacity utilization for the industrial sector remained at 78.3 percent in February, a rate that is 1.3 percentage points below its long-run (1972–2023) average.Click on graph for larger image.

emphasis added

{kind=link}

This graph shows Capacity Utilization. This series is up from the record low set in April 2020, and above the level in February 2020 (pre-pandemic).

Capacity utilization at 78.3% is 1.3% below the average from 1972 to 2022. This was below consensus expectations.

Note: y-axis doesn't start at zero to better show the change.

The second graph shows industrial production since 1967.

The second graph shows industrial production since 1967.Industrial production increased to 102.3. This is above the pre-pandemic level.

Industrial production was above consensus expectations.

Key shipping company files for Chapter 11 bankruptcy

These Cities Have The Highest (And Lowest) Share Of Unaffordable Neighborhoods In 2024

The Question You Should Ask Whenever You’re Wrong

Tight inventory and frustrated buyers challenge agents in Virginia

Futures Rise To New Record High Ahead Of Data Deluge

Walmart and Target make key self-checkout changes to fight theft

Industrial Production Increased 0.1% in February

Your financial plan may be riskier without bitcoin

Key shipping company files Chapter 11 bankruptcy

One city held a mass passport-getting event

-

Uncategorized3 weeks ago

Uncategorized3 weeks agoAll Of The Elements Are In Place For An Economic Crisis Of Staggering Proportions

-

International1 week ago

International1 week agoEyePoint poaches medical chief from Apellis; Sandoz CFO, longtime BioNTech exec to retire

-

Uncategorized4 weeks ago

Uncategorized4 weeks agoCalifornia Counties Could Be Forced To Pay $300 Million To Cover COVID-Era Program

-

Uncategorized3 weeks ago

Uncategorized3 weeks agoApparel Retailer Express Moving Toward Bankruptcy

-

Uncategorized4 weeks ago

Uncategorized4 weeks agoIndustrial Production Decreased 0.1% in January

-

International1 week ago

International1 week agoWalmart launches clever answer to Target’s new membership program

-

Spread & Containment3 days ago

Spread & Containment3 days agoIFM’s Hat Trick and Reflections On Option-To-Buy M&A

-

Uncategorized4 weeks ago

Uncategorized4 weeks agoRFK Jr: The Wuhan Cover-Up & The Rise Of The Biowarfare-Industrial Complex