US Futures Ignore China Implosion, Reverse Overnight Losses as Oil Tumbles

US Futures Ignore China Implosion, Reverse Overnight Losses as Oil Tumbles

Welcome to another rollercoaster session where US equity futures…

Share this:

Welcome to another rollercoaster session where US equity futures first tumbled alongside the second consecutive day of stocks plunging in China, which also dragged Europe lower, only to hit a U-turn around 5am at which point sentiment reversed higher, ahead of tomorrow’s expected Federal Reserve rate hike and amid mounting risks from the war in Ukraine and a Chinese equity rout. Nasdaq 100 contracts trade 0.5% higher at 7:15 a.m. after earlier slumping as much as 0.8% following the first bear-market close for the first time since March 2020. S&P 500 futures also turned 0.3% green, as did Dow futures.

Much of the reversal in sentiment has been attributed to the latest drop in oil which tumbled over $8/bbl or 5.5%, sliding as low as $98 after hitting $139 one week ago. WTI crude oil also fell below $100 a barrel a barrel as traders reassessed the potential impact of disruptions in Russian oil supplies and a decline in demand from China. Iron ore futures fell for a sixth day, the longest streak since September. In other words, commodities are not sliding because of hopes for Russia peace, but because of fears about a global recession, but try explaining it all to algos. Treasuries gained, though the 10-year yield remains near the highest level since 2019. Yields across the euro region also declined. The dollar slipped, while the euro pushed higher and bitcoin dropped again.

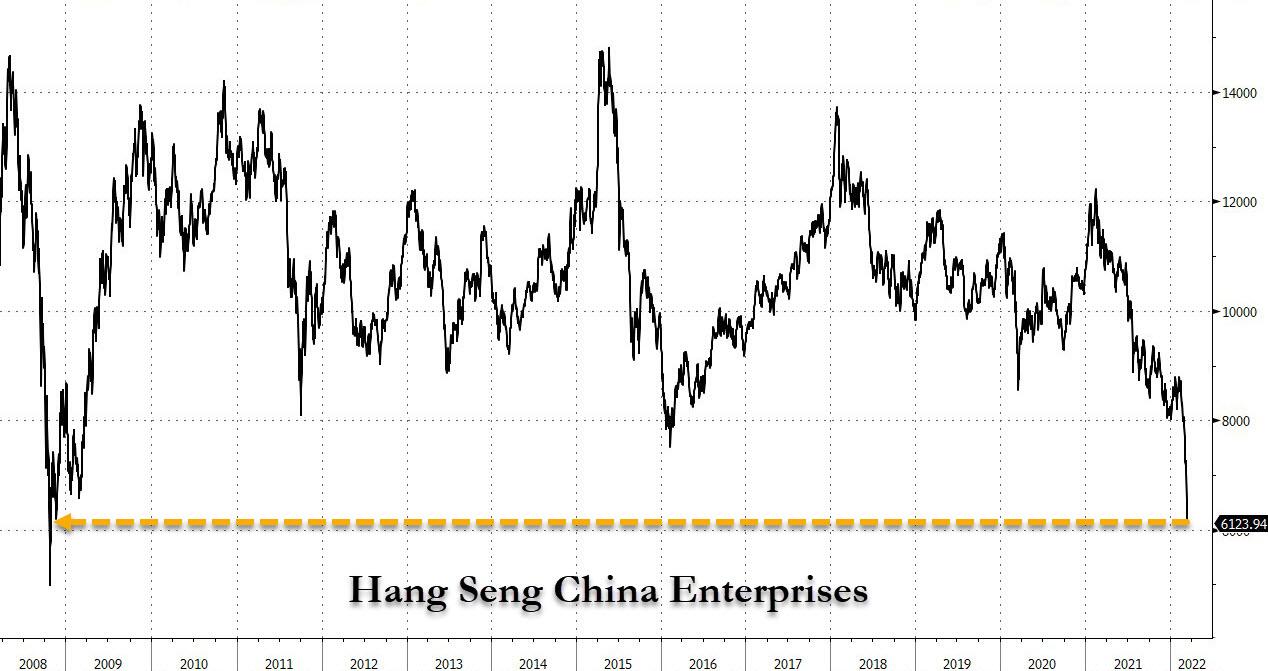

Earlier in the session, a selloff across Chinese equities deepened as concerns about ties with Russia, a growing covid crisis, and persistent regulatory pressure sent a key index to its lowest level since 2008. The Hang Seng China Enterprises Index, which tracks Chinese shares listed in Hong Kong, sank 6.6%, following a plunge in the previous session that was the biggest since the global financial crisis.

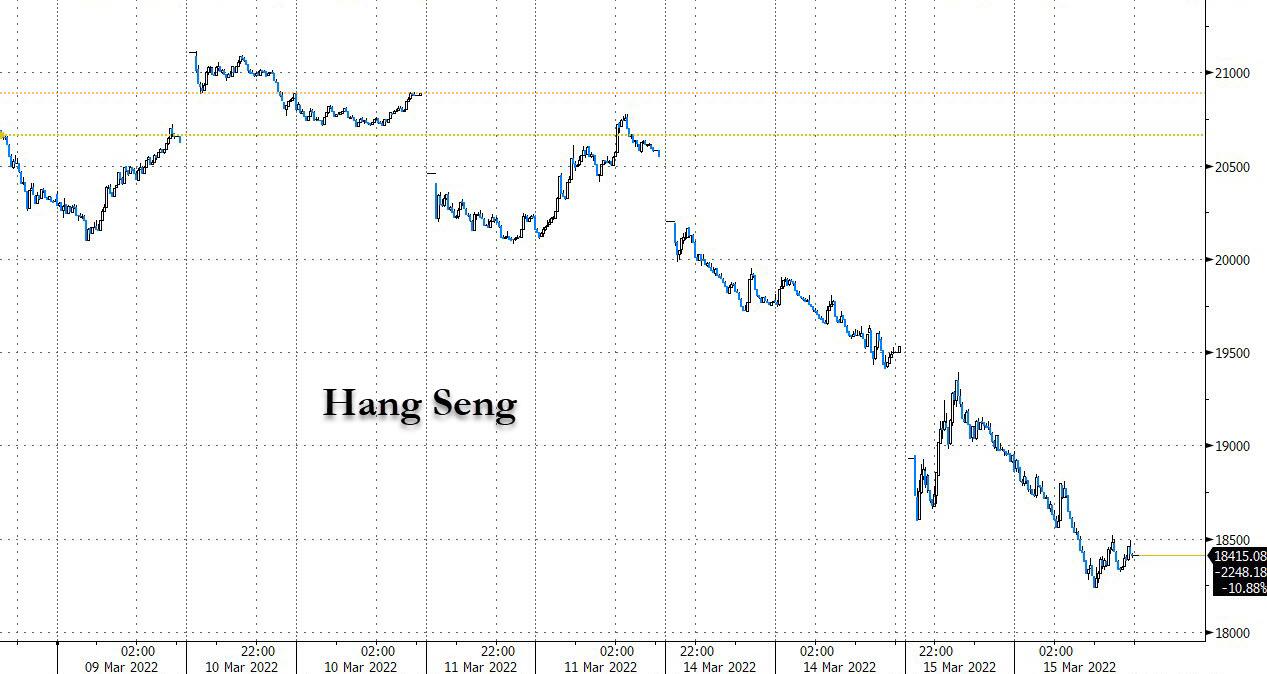

The Hang Seng index tumbled Tech giants Alibaba Group Holding Ltd. and Tencent Holdings Ltd. led the decline. Hong Kong’s benchmark Hang Seng Index slumped 5.7%, its biggest fall since July 2015.

China’s equities are looking increasingly risky on concerns that Beijing’s ties with Russia could spark new U.S. sanctions. That’s adding to worries from regulatory developments including a possible delisting from the U.S. exchanges. While upbeat economic data was a rare bright spot in the market, growing lockdowns in major Chinese cities are dimming the outlook.

"The selloff is overdone, but so is everything else,” said Andy Maynard, head of equities at China Renaissance Securities. "The market is crazy -- there’s no fundamentals anymore. This might be worse than the 2008 financial crisis."

“Risk-off sentiment stemming from both the Russia-Ukraine war and the current wave of Covid-19 in China has driven equity markets sharply weaker this morning,” Siobhan Redford, an analyst at Rand Merchant Bank in Johannesburg, said in a client note. “This has been compounded by falling commodity prices as the intersection between limited supply -- given sanctions on Russia and the war in Ukraine -- and a weaker demand trajectory -- given further waves of the pandemic -- create a perfect storm of sorts.”

With zero liquidity, and trigger happy traders looking to sell any rally, swings in S&P 500 and Nasdaq 100 futures signaled another volatile day ahead for U.S. stocks. U.S.-listed Chinese stocks sank again on Tuesday, following a brutal rout in Asia, amid concerns that China’s ties with Russia may bring sanctions to Beijing, while persistent regulatory pressures also weighed. Alibaba (BABA US) fell 6.5% in premarket trading, while rival JD.com (JD US) declined 4.5%. Apple Inc. inched lower, heading toward a bear market -- defined as a 20% drop from recent highs -- on worries that lockdowns in China to contain a surge in Covid-19 cases could worsen supply-chain constraints. Other notable premarket movers:

- Shares in big U.S. energy companies slide in premarket trading as crude price fall, declining after last week’s rally as worries over growing coronavirus cases in top crude importer China weigh. Exxon Mobil (XOM US) -3.1% and Chevron (CVX US) -3.7%.

- Coupa Software (COUP US) slides 30% in postmarket trading after the company’s revenue forecast for the first quarter misses the average analyst estimate.

- Gitlab (GTLB US) shares rose 12% in extended trading on Monday, after the software company reported fourth-quarter revenue that beat expectations and gave a full-year forecast that is stronger than the analyst consensus.

U.S. technology stocks have been particularly hard hit in the past week with the Federal Reserve expected to begin a rate-hike cycle on Wednesday, another negative for growth stocks valued on future profits. Investors are also looking for cues from the central bank about how aggressively it plans to continue tightening monetary policy as Russia’s invasion of Ukraine sent commodity prices soaring when inflation was already running high. A reading on the producer price index is due on Tuesday.

“If we are entering a world of above-target inflation for several years to come, investors should ditch the easy answers,” said Sahil Mahtani, strategist at Ninety One. “Conventional 60-40 type portfolios are likely to struggle. Investors should reflect about what specifically is driving the inflationary process and invest in equities that have pricing power but are not at frothy valuations.”

The Stoxx Europe 600 index fell more than 1.5%, with basic resources, consumer and technology stocks leading a broad-based decline. All sectors are in the red. Euro Stoxx 50 slumps 2.4%. IBEX outperforms peers but still trades off ~1.5%. Here are some of the biggest European movers today:

- Ahold Delhaize shares gain as much as 3.2%, the best performer in the Stoxx 600’s personal care, drug and grocery stores subgroup, after being upgraded to buy from neutral at UBS, which says the stock is at an “attractive entry point.”

- S&T rallied in Frankfurt, climbing as much as 18%, after the Austrian company said a forensic audit by Deloitte found allegations by short seller Viceroy Research were almost completely inaccurate.

- Sensirion shares spike as much as 13%, the most since June 2020, after the Swiss sensor manufacturer reported full- year sales and gave a revenue forecast that blew past analysts’ estimates. Stifel says the company’s growth is driven by all end markets and the performance of new environmental sensors looks “impressive.”

- Wacker Chemie shares gain as much as 6.9%, as Baader sees dividend proposal 56% above and midpoint ‘22 Ebitda guidance 3% ahead of consensus.

- Tecan falls as much as 16% after reporting sales for the full year that missed the average analyst estimate, and as the outlook disappointed.

- Dr. Martens shares tumble as much as 11% to the lowest since listing in January 2021 after RBC cut its price target to a Street-low, citing the bootmaker’s growth outlook.

- Swedish Match drops as much as 8.4%, the most intraday since February 2021, after the company suspended the spinoff of its U.S. cigar business. The move highlights regulatory risk, according to JPMorgan.

Meanwhile, Russia has started the payment process of two bond coupons due this week. Investors are waiting to see if the nation defaults after the U.S. and its allies froze Russia’s foreign-currency reserves. The ruble gained in Moscow trading.

Asian stocks plunged, on track for a third-straight daily loss, as the selloff in Chinese technology stocks continued after Monday’s plunge, while traders tried to gauge the impact of an imminent interest-rate hike by the Federal Reserve. The MSCI Asia Pacific Index fell as much as 1.9%, heading for its lowest close since August 2020. Tencent and Alibaba Group were among the biggest drags on the regional index, along with TSMC. The sustained selling pressure came as investors mulled the potential consequences of China’s assistance for Russia’s war in Ukraine and delisting risk for Chinese stocks traded in the U.S. Hong Kong’s benchmark Hang Seng Index tumbled 5.7%, its biggest fall since July 2015, while the Hang Seng Tech Index lost 8.1% following a wild intraday swing. Read: Relentless Selling in China Stocks Evokes Memories of 2008 Crash China’s CSI 300 Index slumped 4.6% as the nation’s strong set of economic data failed to lift sentiment amid market jitters on the rising case numbers of Covid-19. Japanese stocks rose for a second day as a weaker yen boosted the outlook for the nation’s exporters. “There are plenty of storms blowing through China right now,” said Jeffrey Halley, senior market analyst at Oanda Asia Pacific. “Fears continue to dog stock markets, that lockdowns could spread, which would severely impact China’s growth.” The risk of tighter monetary policies globally remained on investors’ minds as the Fed this week is expected to announce its first interest rate hike in three years in a bid to curb rising inflation amid surging commodity prices. Markets are now pricing in as many as seven quarter-point hikes for the full year.

Lockdowns in major Chinese cities are dimming the outlook for economic growth and posing risks for energy and raw-materials demand, just as concerns about the country’s relationship with Russia stoke a relentless stock selloff. The virus is also making a comeback in Europe: Germany on Tuesday set a fresh record for infection rates for the four straight day. Austria has also reached new highs, while cases in the Netherlands have doubled since lifting curbs on Feb. 25.

Japanese equities rose, extending their rebound to a second day, supported by gains in exporters on a weaker yen. Auto and chemical makers were the biggest boosts to the Topix, which climbed 0.8%. KDDI and Recruit were the biggest contributors to a 0.2% rise in the Nikkei 225, while Fast Retailing fell. The Japanese currency extended its loss against the dollar to a seventh-straight session, weakening more than 3% in that span. Despite its “haven” status,” the yen has dropped as Russia’s war in Ukraine has driven up prices of oil and other raw materials which Japan imports. “The market has already factored in a lot of bad news” regarding Russia and Ukraine, said Hajime Sakai, chief fund manager at Mito Securities. “The weakening of the yen is positive for exporting, but looking further on we need to think of the negative effect from import costs.”

In rates, Treasuries unwound a portion of Monday’s sharp selloff with yields richer by up to 4.5bp across front-end of the curve into early U.S. session. U.S. 10-year yield near 2.12% is down ~2bp vs Monday’s close, outperforming bunds and gilts in the sector by ~1bp; 2-year yield drop back to ~1.83% after topping near 1.89% during Asia session. Gilts and bund curves bull-flatten while Treasuries bull-steepen; short-dated USTs outperform bunds and gilts by roughly 2bps.

In FX, the Bloomberg Dollar Spot Index fell 0.1% after rising to its highest level since July 2020 in early Asian trade. Treasury yields fell by up to 4bps led by the front-end after rising in early Asian session, when the 10-year yield climbed to 2.17%, the highest since June 2019. Antipodean currencies as well as the Canadian dollar and Norwegian krone were steady to lower as commodities extended losses. The euro extended an Asia session gain, to touch $1.1020 before paring. European benchmark bond yields also fell, yet underperforming Treasuries. Sweden’s krona advanced after inflation expectations rose considerably for the coming two years. Australia’s dollar pares reased an intraday loss, in part on short covering seen after Chinese economic data beat estimates. Reserve Bank said Russia’s invasion of Ukraine has the potential to prolong a period of elevated consumer-price growth and is clouding the economic outlook, minutes of its March 1 policy meeting showed. The yen whipsawed in the spot market as stocks and oil turned south, but options wagers suggest fresh lows versus the dollar may be in store. Whether the greenback can extend its recent rally and maintain its bullish momentum for long depends on options pricing changing course.

In commodities, crude futures decline. WTI drifts 5.3% lower to trade around $97.50. Brent falls 5.3% but holds above $101. Most base metals trade in the red; LME aluminum falls 2.3%, underperforming peers. LME tin outperforms, adding 0.4%. Spot gold falls roughly $17 to trade near $1,934/oz. Elsewhere, nickel trading will resume on the London Metal Exchange on Wednesday, over a week after being suspended amid a historic short squeeze.

Looking to the day ahead now, markets have PPI for February in the US. In Europe, Germany’s ZEW survey expectations, UK jobless claims change, ILO unemployment rate 3 months, Eurozone ZEW survey expectations and industrial production are all due. Elsewhere, housing starts and manufacturing sales in Canada will be released. Earnings include Volkswagen, RWE and Generali.

Market Snapshot

- S&P 500 futures down 0.4% to 4,154.75

- STOXX Europe 600 down 1.7% to 429.03

- MXAP down 1.7% to 165.53

- MXAPJ down 2.9% to 531.41

- Nikkei up 0.2% to 25,346.48

- Topix up 0.8% to 1,826.63

- Hang Seng Index down 5.7% to 18,415.08

- Shanghai Composite down 5.0% to 3,063.97

- Sensex down 1.4% to 55,702.16

- Australia S&P/ASX 200 down 0.7% to 7,097.45

- Kospi down 0.9% to 2,621.53

- Brent Futures down 5.7% to $100.79/bbl

- Gold spot down 0.9% to $1,934.19

- U.S. Dollar Index down 0.21% to 98.79

- German 10Y yield little changed at 0.33%

- Euro up 0.5% to $1.0995

Top Overnight News from Bloomberg

- Germany is preparing to boost the supply of a scarce bond entangled in Russian sanctions, a move that will likely ease pockets of tension in European repo markets. The nation is looking to sell on Tuesday an additional 5.5 billion euros ($6.1 billion) of the notes maturing 2024, which the German government believed became difficult to source after sanctions were imposed against some bondholders

- Chinese stocks suffered another deep selloff on Tuesday as concerns about the country’s ties with Russia and persistent regulatory pressure sent shares on a downward spiral. The Hang Seng China Enterprises Index, which tracks Chinese shares listed in Hong Kong, sank 6.6%, following a plunge in the previous session that was the biggest since the global financial crisis

- Fund managers are leery of buying Chinese stocks as the country’s close ties to Russia, extreme Covid-19 curbs and lack of clarity on the end of regulatory crackdowns overwhelm the dip buying opportunity presented by the 75% plunge from their peak

- China wants to avoid being impacted by U.S. sanctions over Russia’s war, Foreign Minister Wang Yi said, in one of Beijing’s most explicit statements yet on American penalties that are contributing to a historic market selloff

- The global economy is bracing for greater disruption as China scrambles to contain its worst outbreak of Covid-19 since the pandemic began

- Russia’s economy is fraying, its currency has collapsed, and its debt is junk. Next up is a potential default that could cost investors billions and shut the country out of most funding markets

- The dollar has powered ahead of every major currency over the past nine months due to the prospect of Federal Reserve interest-rate hikes but the end of its rally may be in sight, if history is any guide. The U.S. currency has weakened by an average of 4.1% during the Federal Open Market Committee’s four previous tightening cycles

- Traders are ramping up their bets on the amount of Federal Reserve rate hikes in 2022 but are still toying with the possibility of a rate cut as soon as next year

- U.K. unemployment dropped below its pre- pandemic level for the first time as companies generated more jobs and granted higher wages than expected. The jobless rate fell to 3.9% in the three months through January, the lowest since the start of 2020

US Event Calendar

- 8:30am: Feb. PPI Final Demand YoY, est. 10.0%, prior 9.7%; MoM, est. 0.9%, prior 1.0%

- 8:30am: Feb. PPI Ex Food and Energy YoY, est. 8.7%, prior 8.3%; MoM, est. 0.6%, prior 0.8%

- 8:30am: March Empire Manufacturing, est. 6.1, prior 3.1

- 4pm: Jan. Total Net TIC Flows, prior -$52.4b

DB's Jim Reid concludes the overnight wrap

Some hints of positive diplomatic developments in the Ukraine crisis that materialised on Sunday night helped contribute to another major sell-off in bonds and a mild risk on move in European equities yesterday. While in the States, the reality of the impending Fed tightening cycle pushed yields higher and drove equities lower.

Bonds are in a strange situation at the moment as we seem to have reached a point where higher energy prices are deemed to be signalling recessionary risks and encourage flight to quality flows that push nominal yields lower, outweighing the potentially savage inflationary impact. Conversely, the collapse in the likes of oil and gas since early last week has led to a huge rise in yields as it appears policy tightening is back on the central bank menu. Brent is around -25% from its intra-day highs last Tuesday and 10yr bunds are +46.6bps higher since hitting -0.10% last Monday morning. Meanwhile, 1-month futures on Dutch Gas have fallen from a high of 335 last Monday morning to 110.50 at the close last night. Remarkable moves.

On the conflict, Russia and Ukraine finished a fourth day of negotiations yesterday and decided to take a pause to assess outcomes. Still, it seems that negotiations are making some progress. Meanwhile, President Zelensky is set to address the US Congress tomorrow, while there were reports that President Biden was considering a trip to Europe to express the US’s steadfast support for NATO allies.

Overnight in Asia, most equity markets are down with Hong Kong and Chinese stocks leading regional losses. The Hang Seng (-3.56%) opened sharply lower, slipping more than 4% before recovering slightly as a resurgence of Covid-19 in Hong Kong and China and potential delisting of Chinese stocks from US exchanges weighed on sentiment. The Shanghai Composite (-2.18%) and CSI (-1.75%) are also down even if losses were pared following the release of stronger-than-anticipated economic data. A fresh lockdown in China’s Jilin province of 24 million people is offsetting this. Elsewhere, the Nikkei (+0.33%) is advancing while the Kospi (-0.56%) is lagging. Moving forward, equity futures on the S&P 500 (+0.17%) and Nasdaq (+0.47%) are higher while DAX contracts (-0.45%) are weak.

On that China data, industrial output rose a more-than-expected +7.5% y/y in January and February, (vs market estimates of +4.0%) and against a +9.6% gain in December while retail sales grew +6.7% y/y in the same period compared with analyst estimates of a +3.0% increase amid rising demand during the Lunar New Year holidays and the Winter Olympic Games. Meanwhile, fixed asset investment also beat, up by +12.2% y/y YTD in February and well above the forecast for a +5.0% increase. Separately, the People’s Bank of China (PBOC) unexpectedly kept the one-year medium-term lending facility rate (MLF) at 2.85%, resulting in a net injection of 100 billion yuan in fresh funds. The central banks’ action dashed hopes of a rate cut as the policymakers may want to avoid widening policy divergence with the US ahead of their expected hike tomorrow.

Oil prices have extended their recent declines this morning with Brent futures sliding -4.0% to trade at $102.64/bbl and with WTI futures -4.2%, breaking below $100/bbl. It saw a similar fall yesterday after opening the week above $109/bbl. Elsewhere, the yield on the 10-year US Treasury note is roughly flat at 2.138%.

As discussed at the top, the calm in yields overnight followed a rout yesterday. 10yr bunds eventually rose +11.9bps yesterday as risk premium eased, and to the highest level since November 2018. With a modest +2.2bps uptick in breakevens, most of the move was in real yields. Note that page 24 of the “Dislocations” chart book shows that 10yr real bund yields last week hit all-time low levels. Since those lows last week we’ve backed up +48.8bps. The move in other European sovereign yields was remarkably similar to bunds yesterday with BTPs (+11.3bps), Spanish (+11.0bps) and even Greek (+11.8bps) bonds seeing hardly any change in spreads.

US Treasury yields sold even more (10yr +14.1bps) and unlike in Europe, higher yields were met with falling breakevens (-2.3bps) with real yields +16.4bps putting in their biggest daily move since February 2021. No small feat given the considerable sell-off in real rates that marked the beginning of this year. The 2s10s (+2.8bps) curve steepened a little which might be welcomed by the Fed. Yields across the US curve notched fresh cycle highs, with those on 2y (+11.3bps) and 10y reaching the highest levels since summer 2019.

Notably, US futures moved to fully price in 7 Fed hikes in 2022 for the first time this cycle, in line with our US econ team’s view. While there were reports of incoming corporate issuance and hedging flows driving the Treasury rate sell-off, it appears markets are waking up to the magnitude of tightening the Fed is about to embark on, starting this week. If the war wasn’t enough to get the ECB to strike a dovish tone, the Fed will be all the more emboldened given fewer direct linkages to growth shocks from the conflict and the higher starting point for inflation. Indeed, in a new periodical we launched yesterday, Questions for the Chair, link here, DB Research personnel offer the questions they would ask Chair Powell at his FOMC press conference. A common question was wouldn’t policy rates need to be higher than current forecasts given the inflationary outlook. It seems markets are coming around to that view.

That line of thinking passed through to US equities, where the S&P 500 slid -0.74%. The tech-heavy NASDAQ, which is more exposed to rising rates, underperformed, falling -2.04%. Sector-wise, amid plummeting oil prices energy stocks (-2.93%) performed the worst after a sustained run of outperformance, while financials (+1.23%) were the top performers in the S&P 500 amid a steeper yield curve.

European stocks outperformed their American counterparts, with the positive geopolitical noise outweighing a tighter monetary policy path to push major indices into positive territory. The STOXX 600 rallied +1.20%, but gains in country-level benchmarks like the German DAX (+2.21%) and the French CAC 40 (+1.75%) were even more startling amid recent sharp underperformance relative to their US counterparts.

The same positive risk sentiment pushed commodity prices lower. We've already mentioned the slump in Oil but European gas prices also fell, with front month Dutch TTF contracts losing -17.29%. Oil prices fell despite no additional supply via Iran, US, Venezuela, or OPEC appearing likely. Instead, it seems as though Russian supply may make its way to buyers such as China and India with fewer frictions than were previously feared. As a secondary consideration, reports of Covid-19 lockdowns in China may have pushed prices lower due to potential lower demand needs.

Industrial metals lost steam as well, with aluminium and copper falling -4.69% and -2.24%, respectively, while gold lost -1.89% as markets revised geopolitical risks downwards.

One developing story with unclear implications so far is Russia’s request for Chinese support of its invasion. There have been conflicting reports about the veracity of the original claims. We do know that the US National Security Advisor met with his Chinese counterpart yesterday to try and dissuade China from offering any such support. One to keep a very close eye on.

To the day ahead now. In today’s data releases, markets have PPI for February in the US. In Europe, Germany’s ZEW survey expectations, UK jobless claims change, ILO unemployment rate 3 months, Eurozone ZEW survey expectations and industrial production are all due. Elsewhere, housing starts and manufacturing sales in Canada will be released. Earnings include Volkswagen, RWE and Generali.

Uncategorized

Homes listed for sale in early June sell for $7,700 more

New Zillow research suggests the spring home shopping season may see a second wave this summer if mortgage rates fall

The post Homes listed for sale in…

Share this:

- A Zillow analysis of 2023 home sales finds homes listed in the first two weeks of June sold for 2.3% more.

- The best time to list a home for sale is a month later than it was in 2019, likely driven by mortgage rates.

- The best time to list can be as early as the second half of February in San Francisco, and as late as the first half of July in New York and Philadelphia.

Spring home sellers looking to maximize their sale price may want to wait it out and list their home for sale in the first half of June. A new Zillow® analysis of 2023 sales found that homes listed in the first two weeks of June sold for 2.3% more, a $7,700 boost on a typical U.S. home.

The best time to list consistently had been early May in the years leading up to the pandemic. The shift to June suggests mortgage rates are strongly influencing demand on top of the usual seasonality that brings buyers to the market in the spring. This home-shopping season is poised to follow a similar pattern as that in 2023, with the potential for a second wave if the Federal Reserve lowers interest rates midyear or later.

The 2.3% sale price premium registered last June followed the first spring in more than 15 years with mortgage rates over 6% on a 30-year fixed-rate loan. The high rates put home buyers on the back foot, and as rates continued upward through May, they were still reassessing and less likely to bid boldly. In June, however, rates pulled back a little from 6.79% to 6.67%, which likely presented an opportunity for determined buyers heading into summer. More buyers understood their market position and could afford to transact, boosting competition and sale prices.

The old logic was that sellers could earn a premium by listing in late spring, when search activity hit its peak. Now, with persistently low inventory, mortgage rate fluctuations make their own seasonality. First-time home buyers who are on the edge of qualifying for a home loan may dip in and out of the market, depending on what’s happening with rates. It is almost certain the Federal Reserve will push back any interest-rate cuts to mid-2024 at the earliest. If mortgage rates follow, that could bring another surge of buyers later this year.

Mortgage rates have been impacting affordability and sale prices since they began rising rapidly two years ago. In 2022, sellers nationwide saw the highest sale premium when they listed their home in late March, right before rates barreled past 5% and continued climbing.

Zillow’s research finds the best time to list can vary widely by metropolitan area. In 2023, it was as early as the second half of February in San Francisco, and as late as the first half of July in New York. Thirty of the top 35 largest metro areas saw for-sale listings command the highest sale prices between May and early July last year.

Zillow also found a wide range in the sale price premiums associated with homes listed during those peak periods. At the hottest time of the year in San Jose, homes sold for 5.5% more, a $88,000 boost on a typical home. Meanwhile, homes in San Antonio sold for 1.9% more during that same time period.

| Metropolitan Area | Best Time to List | Price Premium | Dollar Boost |

| United States | First half of June | 2.3% | $7,700 |

| New York, NY | First half of July | 2.4% | $15,500 |

| Los Angeles, CA | First half of May | 4.1% | $39,300 |

| Chicago, IL | First half of June | 2.8% | $8,800 |

| Dallas, TX | First half of June | 2.5% | $9,200 |

| Houston, TX | Second half of April | 2.0% | $6,200 |

| Washington, DC | Second half of June | 2.2% | $12,700 |

| Philadelphia, PA | First half of July | 2.4% | $8,200 |

| Miami, FL | First half of June | 2.3% | $12,900 |

| Atlanta, GA | Second half of June | 2.3% | $8,700 |

| Boston, MA | Second half of May | 3.5% | $23,600 |

| Phoenix, AZ | First half of June | 3.2% | $14,700 |

| San Francisco, CA | Second half of February | 4.2% | $50,300 |

| Riverside, CA | First half of May | 2.7% | $15,600 |

| Detroit, MI | First half of July | 3.3% | $7,900 |

| Seattle, WA | First half of June | 4.3% | $31,500 |

| Minneapolis, MN | Second half of May | 3.7% | $13,400 |

| San Diego, CA | Second half of April | 3.1% | $29,600 |

| Tampa, FL | Second half of June | 2.1% | $8,000 |

| Denver, CO | Second half of May | 2.9% | $16,900 |

| Baltimore, MD | First half of July | 2.2% | $8,200 |

| St. Louis, MO | First half of June | 2.9% | $7,000 |

| Orlando, FL | First half of June | 2.2% | $8,700 |

| Charlotte, NC | Second half of May | 3.0% | $11,000 |

| San Antonio, TX | First half of June | 1.9% | $5,400 |

| Portland, OR | Second half of April | 2.6% | $14,300 |

| Sacramento, CA | First half of June | 3.2% | $17,900 |

| Pittsburgh, PA | Second half of June | 2.3% | $4,700 |

| Cincinnati, OH | Second half of April | 2.7% | $7,500 |

| Austin, TX | Second half of May | 2.8% | $12,600 |

| Las Vegas, NV | First half of June | 3.4% | $14,600 |

| Kansas City, MO | Second half of May | 2.5% | $7,300 |

| Columbus, OH | Second half of June | 3.3% | $10,400 |

| Indianapolis, IN | First half of July | 3.0% | $8,100 |

| Cleveland, OH | First half of July | 3.4% | $7,400 |

| San Jose, CA | First half of June | 5.5% | $88,400 |

The post Homes listed for sale in early June sell for $7,700 more appeared first on Zillow Research.

federal reserve pandemic home sales mortgage rates interest ratesGovernment

Survey Shows Declining Concerns Among Americans About COVID-19

Survey Shows Declining Concerns Among Americans About COVID-19

A new survey reveals that only 20% of Americans view covid-19 as "a major threat"…

Share this:

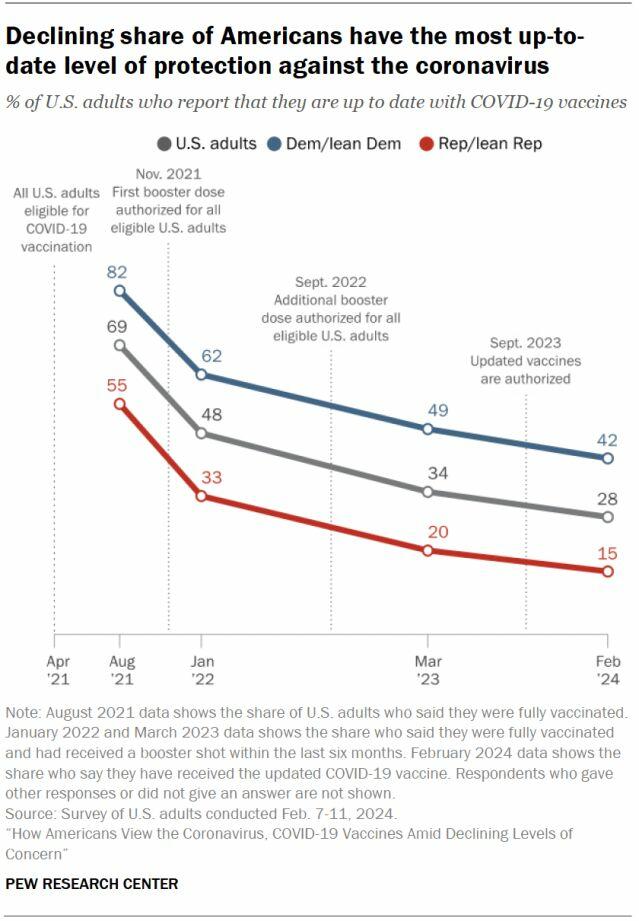

A new survey reveals that only 20% of Americans view covid-19 as "a major threat" to the health of the US population - a sharp decline from a high of 67% in July 2020.

What's more, the Pew Research Center survey conducted from Feb. 7 to Feb. 11 showed that just 10% of Americans are concerned that they will catch the disease and require hospitalization.

"This data represents a low ebb of public concern about the virus that reached its height in the summer and fall of 2020, when as many as two-thirds of Americans viewed COVID-19 as a major threat to public health," reads the report, which was published March 7.

According to the survey, half of the participants understand the significance of researchers and healthcare providers in understanding and treating long COVID - however 27% of participants consider this issue less important, while 22% of Americans are unaware of long COVID.

What's more, while Democrats were far more worried than Republicans in the past, that gap has narrowed significantly.

"In the pandemic’s first year, Democrats were routinely about 40 points more likely than Republicans to view the coronavirus as a major threat to the health of the U.S. population. This gap has waned as overall levels of concern have fallen," reads the report.

More via the Epoch Times;

The survey found that three in ten Democrats under 50 have received an updated COVID-19 vaccine, compared with 66 percent of Democrats ages 65 and older.

Moreover, 66 percent of Democrats ages 65 and older have received the updated COVID-19 vaccine, while only 24 percent of Republicans ages 65 and older have done so.

“This 42-point partisan gap is much wider now than at other points since the start of the outbreak. For instance, in August 2021, 93 percent of older Democrats and 78 percent of older Republicans said they had received all the shots needed to be fully vaccinated (a 15-point gap),” it noted.

COVID-19 No Longer an Emergency

The U.S. Centers for Disease Control and Prevention (CDC) recently issued its updated recommendations for the virus, which no longer require people to stay home for five days after testing positive for COVID-19.

The updated guidance recommends that people who contracted a respiratory virus stay home, and they can resume normal activities when their symptoms improve overall and their fever subsides for 24 hours without medication.

“We still must use the commonsense solutions we know work to protect ourselves and others from serious illness from respiratory viruses, this includes vaccination, treatment, and staying home when we get sick,” CDC director Dr. Mandy Cohen said in a statement.

The CDC said that while the virus remains a threat, it is now less likely to cause severe illness because of widespread immunity and improved tools to prevent and treat the disease.

“Importantly, states and countries that have already adjusted recommended isolation times have not seen increased hospitalizations or deaths related to COVID-19,” it stated.

The federal government suspended its free at-home COVID-19 test program on March 8, according to a website set up by the government, following a decrease in COVID-19-related hospitalizations.

According to the CDC, hospitalization rates for COVID-19 and influenza diseases remain “elevated” but are decreasing in some parts of the United States.

Government

Rand Paul Teases Senate GOP Leader Run – Musk Says “I Would Support”

Rand Paul Teases Senate GOP Leader Run – Musk Says "I Would Support"

Republican Kentucky Senator Rand Paul on Friday hinted that he may jump…

Share this:

{kind=link}

{kind=link}

Republican Kentucky Senator Rand Paul on Friday hinted that he may jump into the race to become the next Senate GOP leader, and Elon Musk was quick to support the idea. Republicans must find a successor for periodically malfunctioning Mitch McConnell, who recently announced he'll step down in November, though intending to keep his Senate seat until his term ends in January 2027, when he'd be within weeks of turning 86.

So far, the announced field consists of two quintessential establishment types: John Cornyn of Texas and John Thune of South Dakota. While John Barrasso's name had been thrown around as one of "The Three Johns" considered top contenders, the Wyoming senator on Tuesday said he'll instead seek the number two slot as party whip.

Paul used X to tease his potential bid for the position which -- if the GOP takes back the upper chamber in November -- could graduate from Minority Leader to Majority Leader. He started by telling his 5.1 million followers he'd had lots of people asking him about his interest in running...

Thousands of people have been asking if I'd run for Senate leadership...

— Rand Paul (@RandPaul) March 8, 2024

...then followed up with a poll in which he predictably annihilated Cornyn and Thune, taking a 96% share as of Friday night, with the other two below 2% each.

????????️VOTE NOW ????️ ???? Who would you like to be the next Senate leader?

— Rand Paul (@RandPaul) March 8, 2024

Elon Musk was quick to back the idea of Paul as GOP leader, while daring Cornyn and Thune to follow Paul's lead by throwing their names out for consideration by the Twitter-verse X-verse.

I would support Rand Paul and suspect that other candidates will not actually run polls out of concern for the results, but let’s see if they will!

— Elon Musk (@elonmusk) March 8, 2024

Paul has been a stalwart opponent of security-state mass surveillance, foreign interventionism -- to include shoveling billions of dollars into the proxy war in Ukraine -- and out-of-control spending in general. He demonstrated the latter passion on the Senate floor this week as he ridiculed the latest kick-the-can spending package:

This bill is an insult to the American people. The earmarks are all the wasteful spending that you could ever hope to see, and it should be defeated. Read more: https://t.co/Jt8K5iucA4 pic.twitter.com/I5okd4QgDg

— Senator Rand Paul (@SenRandPaul) March 8, 2024

In February, Paul used Senate rules to force his colleagues into a grueling Super Bowl weekend of votes, as he worked to derail a $95 billion foreign aid bill. "I think we should stay here as long as it takes,” said Paul. “If it takes a week or a month, I’ll force them to stay here to discuss why they think the border of Ukraine is more important than the US border.”

Don't expect a Majority Leader Paul to ditch the filibuster -- he's been a hardy user of the legislative delay tactic. In 2013, he spoke for 13 hours to fight the nomination of John Brennan as CIA director. In 2015, he orated for 10-and-a-half-hours to oppose extension of the Patriot Act.

{kind=link}

Among the general public, Paul is probably best known as Capitol Hill's chief tormentor of Dr. Anthony Fauci, who was director of the National Institute of Allergy and Infectious Disease during the Covid-19 pandemic. Paul says the evidence indicates the virus emerged from China's Wuhan Institute of Virology. He's accused Fauci and other members of the US government public health apparatus of evading questions about their funding of the Chinese lab's "gain of function" research, which takes natural viruses and morphs them into something more dangerous. Paul has pointedly said that Fauci committed perjury in congressional hearings and that he belongs in jail "without question."

Musk is neither the only nor the first noteworthy figure to back Paul for party leader. Just hours after McConnell announced his upcoming step-down from leadership, independent 2024 presidential candidate Robert F. Kennedy, Jr voiced his support:

Mitch McConnell, who has served in the Senate for almost 40 years, announced he'll step down this November.

— Robert F. Kennedy Jr (@RobertKennedyJr) February 28, 2024

Part of public service is about knowing when to usher in a new generation. It’s time to promote leaders in Washington, DC who won’t kowtow to the military contractors or…

In a testament to the extent to which the establishment recoils at the libertarian-minded Paul, mainstream media outlets -- which have been quick to report on other developments in the majority leader race -- pretended not to notice that Paul had signaled his interest in the job. More than 24 hours after Paul's test-the-waters tweet-fest began, not a single major outlet had brought it to the attention of their audience.

That may be his strongest endorsement yet.

Veterans Affairs Kept COVID-19 Vaccine Mandate In Place Without Evidence

The Coming Of The Police State In America

Beloved mall retailer files Chapter 7 bankruptcy, will liquidate

‘I couldn’t stand the pain’: the Turkish holiday resort that’s become an emergency dental centre for Britons who can’t get treated at home

February Employment Situation

Low Iron Levels In Blood Could Trigger Long COVID: Study

Rand Paul Teases Senate GOP Leader Run – Musk Says “I Would Support”

Walmart has really good news for shoppers (and Joe Biden)

Another beloved brewery files Chapter 11 bankruptcy

Walmart joins Costco in sharing key pricing news

-

Uncategorized3 weeks ago

Uncategorized3 weeks agoAll Of The Elements Are In Place For An Economic Crisis Of Staggering Proportions

-

Uncategorized1 month ago

Uncategorized1 month agoCathie Wood sells a major tech stock (again)

-

Uncategorized3 weeks ago

Uncategorized3 weeks agoCalifornia Counties Could Be Forced To Pay $300 Million To Cover COVID-Era Program

-

Uncategorized2 weeks ago

Uncategorized2 weeks agoApparel Retailer Express Moving Toward Bankruptcy

-

Uncategorized4 weeks ago

Uncategorized4 weeks agoIndustrial Production Decreased 0.1% in January

-

International3 days ago

International3 days agoWalmart launches clever answer to Target’s new membership program

-

International3 days ago

International3 days agoEyePoint poaches medical chief from Apellis; Sandoz CFO, longtime BioNTech exec to retire

-

Uncategorized3 weeks ago

Uncategorized3 weeks agoRFK Jr: The Wuhan Cover-Up & The Rise Of The Biowarfare-Industrial Complex