US Futures Fade Asian Rally On Fears ECB Will Take Away The Punchbowl

US Futures Fade Asian Rally On Fears ECB Will Take Away The Punchbowl

European bourses dipped in the red and a rally in US equity futures which traded near all-time highs after the Labor Day holiday fizzled, as investors weighed China’s…

US Futures Fade Asian Rally On Fears ECB Will Take Away The Punchbowl

European bourses dipped in the red and a rally in US equity futures which traded near all-time highs after the Labor Day holiday fizzled, as investors weighed China’s better-than-forecast trade data against the growing likelihood of fading central-bank support. S&P500 futures traded fractionally in the green and Nasdaq 100 indexes slipped and equity gains in China and Japan were followed by losses in Europe as investors speculated the ECB may get ready to roll back stimulus. The dollar and Treasuries yields rose, gold and cryptos dropped.

Tech gigacaps such as Microsoft, Amazon.com and Facebook eased about 0.2% each, while Apple and Google were slightly higher. Tracking benchmark bond yields higher, banks including Wells Fargo, Goldman Sachs, Citigroup and JP Morgan rose between 0.4% and 0.5%. Among meme stocks, IronNet more than doubled in value in premarket trading after the cybersecurity company was touted on Reddit and StockTwits. Chinese technology stocks listed in the U.S. rose premarket, amid surprisingly strong trade data (see below), renewed demand for technology shares, the lack of new regulatory announcements and Tencent’s plans to buy back more shares. Alibaba (BABA) was up 2.6% and Didi (DIDI) gained 2.8%, while Baidu (BIDU) gains 3.4%. Here are some of the other biggest movers today:

Alcoa (AA) shares rise 2.9% premarket, catching up with the jump in aluminum prices seen on Monday when U.S. markets were closed.

Farfetch (FTCH) drops 0.7% after Arete downgraded the stock to sell, citing China risks along with a drag to gross margin from Tmall fees.

Columbia Property Trust Inc (CXP) jumped 15.8% after Pacific Investment Management Company said it would buy the company for $2.2 billion.

InflaRx (IFRX) shares rally 23% after it was among the companies awarded grants in Germany for Covid-19 drug development.

IronNet (IRNT) shares soar 106% with the stock being touted on Reddit and StockTwits.

Match Group (MTCH) surges 14% on being named to the S&P 500 Index.

Moderna (MRNA) declines 1.6% after report that Japan’s health ministry said that a man in his 40s died after receiving the biotech’s Covid-19 vaccine from production lots that are being recalled due to possible contamination

Vertex Pharmaceuticals fell 1.8% in early New York trading after Morgan Stanley cut its stock recommendation to underweight.

The world’s biggest economy remains “in good health” despite a recent increase in Covid-19 infections, according to Mark Haefele, chief investment officer at UBS Global Wealth. “This will support stocks, in our view, especially in cyclical industries like energy and financials,” Haefele said. “We continue to advise investors to position for reopening and recovery.”

Another thing that supports stocks is that the market is no longer expecting a Fed announcement about tapering in September, Esty Dwek, a global market strategist at Natixis Investment Managers, told Bloomberg Television. “Tapering doesn’t matter that much for markets. It’s priced in, it’s expected. But the reality is that interest rate hikes matter.” Justifying this view was Goldman's latest GDP forecast cut on Monday, its third in the past month, which saw the bank trim its full-year 2021 GDP forecast to 5.7% from 6.0%.

The S&P 500 and the Nasdaq have gained around 1.5% each since Aug. 27 following dovish commentary from Fed Chair Jerome Powell at the Jackson Hole Symposium where he again said that a stable job market was an essential goal for the central bank to start pulling back monetary support.

Optimism that the Fed will delay tapering was offset by concerns that the ECB could turn hawkish at its meeting this week: “There is a growing expectation that the European Central Bank could start talking about tapering its bond purchases sooner rather than later,” Ipek Ozkardeskaya, a senior analyst at Swissquote Group Holdings, wrote in a note. “The ECB hawks who have been in a retreat for the past year won’t stay quiet for longer facing the rising inflation threat.”

Sure enough, Europe's Stoxx 600 index dropped as investors focused on the ECB’s Thursday meeting where the central bank will decide if it will dial down emergency stimulus. Bank of America said it sees the “Goldilocks combination” of accelerating growth and lower real yields coming to an end. As Bloomberg notes, European stocks pushing to regain a record high against a more muted macro backdrop turned cautious, with investing sectors and styles favoring growth and quality. The Stoxx 600 hasn’t hit a record high since Aug 13. The gauge’s decline of ~0.5% since then is hardly indicative of a rout. But as Bloomberg notes, traders have shied away from blatantly cyclical sectors like consumer products, autos and miners and most notably bought a classic growth industry in tech, even if it’s pricey. This comes amid a global backdrop of rising delta cases, higher inflation, supply chain bottlenecks and a slowdown in the economic recovery. In Europe, unfilled orders rose to an unprecedented level in August, and Germany’s key business sentiment gauge weakened. In terms of styles, quality and growth are holding up better than overall European stocks or factors such as value.

The MSCI Europe Quality Net Return index has risen almost 25% this year through Monday, compared with ~19% for the MSCI Europe. Quality has also outperformed in the past month. The ratio of the MSCI Europe Quality to the MSCI Europe is near the highest ever. The MSCI Europe Growth index has also beaten both the MSCI Europe and the MSCI Europe Value in particular. The European growth/value index is at the highest since November. Here are some of the biggest European movers today:

Vistry Group shares climb as much as 5.6% after its 1H results are better than expected, driven by a beat on margins, Liberum (buy) writes in a note.

Marks & Spencer shares gain as much as 3.6% after being upgraded to buy from neutral at UBS, which notes “strong progress” in the U.K. retailer’s clothing & home business along with food.

DS Smith shares rise as much as 2.4% after reporting “excellent volume growth” and good progress toward recovering the significant increasing costs of production through higher prices.

Danone shares lose as much as 2.4% after BofA Global Research cut its recommendation to underperform from neutral.

Allegro shares drop as much as 2.1% after Wiadomosci Handlowe and Reuters reported that Singapore’s Sea plans to expand its marketplace Shopee to Poland.

Holcim shares fall as much as 1.9%, declining for a second day on investor worries about legal consequences from past conduct of the company’s Lafarge unit in Syria.

Deutsche Telekom said it will use proceeds from the sale of its Dutch unit to acquire a greater stake in T-Mobile US.

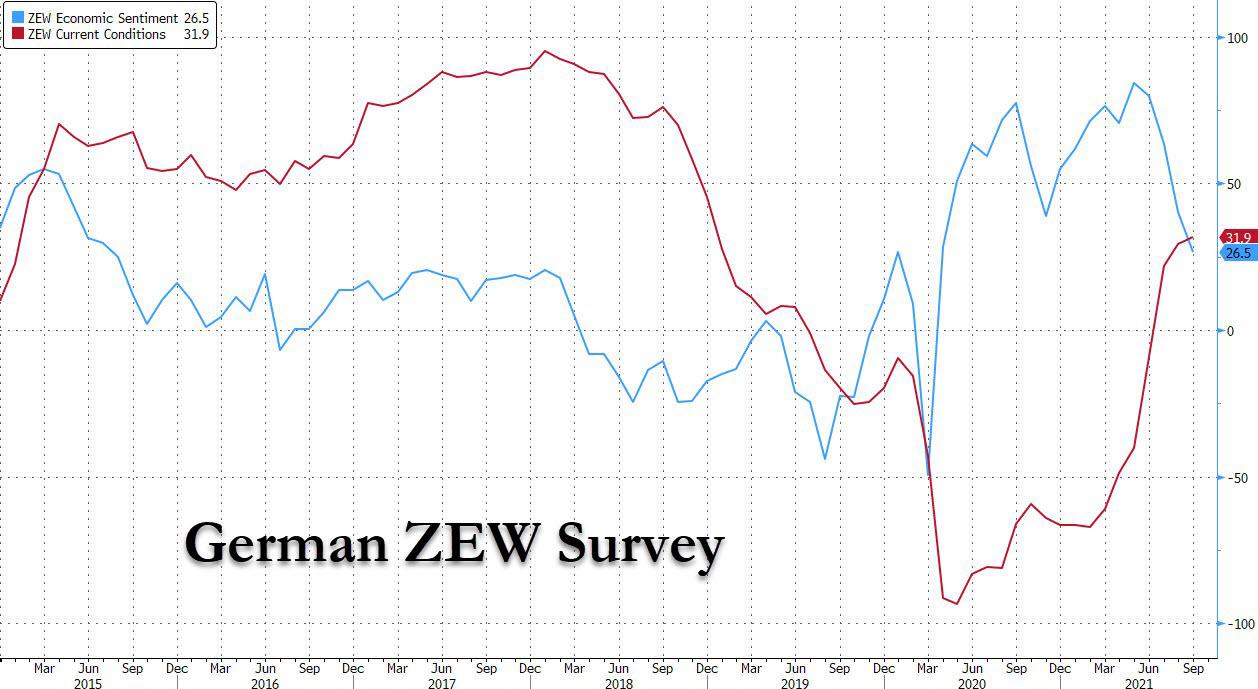

And speaking of ECB tapering, it would come just as the Germany economy continues to roll over with the latest ZEW Economic Sentiment missing, dropping from 40.4 to 26.5, below the 30.0 expected; current conditions also missed, printing at 31.9 vs 34.0 exp.

Asian stocks climbed, driven by Japanese shares that extended a rally after the prime minister’s resignation announcement and a surge in Hong Kong-traded tech names. The MSCI Asia Pacific Index advanced as much as 0.5%, led by the communication-services and consumer-discretionary sectors. Japan’s Nikkei 225 Stock Average briefly broke above the 30,000 level for the first time since April as a reshuffle of the blue-chip gauge added to optimism stoked by potential policy changes that could come under a new national leader. Japanese Finance Minister Aso said they will consider compiling a budget with focus on digital, environmental policies, regional economies and ageing population. Furthermore, he doubts if Japan's finances would risk a weaker JPY and inflation, while he suggested it would be good for the next PM to boost government revenue and restrain spending (yes, he really said that). Meanwhile, tech stocks jumped in Hong Kong as Tencent repurchased shares and regulatory announcements related to crackdowns on the sector appeared to take a breather.

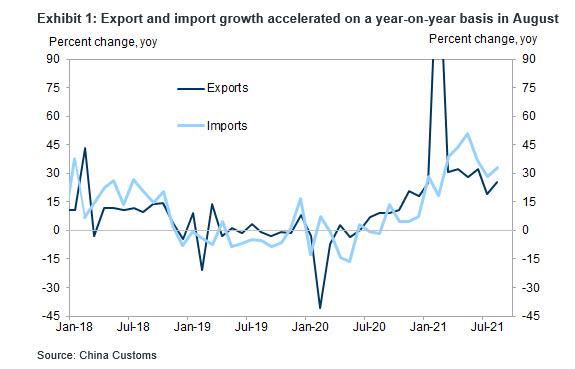

Adding to the good news was the report that Chinese export growth unexpectedly surged in August, allaying concerns the pandemic is delaying economic reopening and creating supply-chain bottlenecks. China's exports accelerated to 25.6% yoy in August, a sequential rebound of 3.3% in August vs. -0.3% in July. Imports rose 33.1% yoy in August, and grew 2.1% mom sa non-annualized in August (vs. -6.4% in July). Both exports and imports surprised to the upside despite the disruptions to operations at Ningbo port in August due to the local outbreak. Monthly trade surplus rose to $58.3bn in August.

Adding to the positive mood, Hong Kong said it will start allowing visitors from the mainland to skip the strict quarantine process. Equities rose in the mainland and offshore. The Asian stock gauge entered its eighth-straight session of gains as concerns related to U.S. monetary policy tightening and the delta variant’s effects on global growth appeared to ease. A ninth day in the green would put the measure on track for its longest winning streak since November.

In FX, the Bloomberg Dollar Spot Index erased losses as a rally in regional equities stalled and the greenback traded mixed versus its Group-of-10 peers, though most moves were relatively small. Australia’s dollar was the worst G-10 performer as it reversed an earlier gain after the central bank said it will maintain its debt purchases until at least-mid February, instead of an earlier target of November this year. Ten of 16 economists surveyed by Bloomberg had expected the RBA to defer scaling back quantitative easing. The central bank held its cash rate at 0.1% at the meeting. The euro was little changed, shrugging off data that showed investor confidence in the German economy declining for a fourth month amid worsening infection rates and global supply disruptions. The pound hovered ahead of U.K. Prime Minister Boris Johnson announcing a long-awaited plan to reform social care. If the “key interest rate does rise in the next year or so, it’s likely that any rise would be relatively limited,” Bank of England policy maker Michael Saunders said in a speech on Tuesday. Japanese government bond futures rose after a smooth auction of 30-year debt soothed sentiment toward the nation’s debt market. The yen traded in a narrow range. Emerging-market currencies weakened for the first time in three days as the dollar climbed along with U.S. yields. Higher-yielding currencies, including the South African rand and Russian ruble, led declines after outperforming peers last week on expectations for continuing monetary support from the Federal Reserve.

In rates, Treasury yields were cheaper by up to 4bp across 7- to 20-year sectors, with 10-year yields sit around 1.36%, mildly outperforming bunds while gilts trade slightly richer. Treasuries were pressured lower with losses led by intermediates out to long-end ahead of this week’s supply, which kicks off Tuesday with $58b 3-year note sale. Mild risk-on in Asia spurred by China trade data beat saw stocks close higher and Treasuries trade heavy, adding to auction concessions. U.S. auction cycle includes 10- and 30-year offerings Wednesday and Thursday. Peripheral spreads have a marginal tightening bias to core; Spain underperformed slightly with focus today on issuance of the sovereign’s inaugural green bond.

In commodities, crude futures drift within Monday’s trading range. WTI hovers near $69. Brent near $72.50. Spot gold drops ~$10 to trade near $1,813/oz. LME copper underperforms peers with a 1% decline.

Looking at the day ahead, it’s another quiet day on the calendar ahead, with nothing on the US econ calendar. Meanwhile from central banks, the BoE’s Saunders will be speaking.

Market Snapshot

S&P 500 futures little changed at 4,538.25

STOXX Europe 600 down 0.1% to 474.60

MXAP up 0.3% to 207.14

MXAPJ little changed at 674.43

Nikkei up 0.9% to 29,916.14

Topix up 1.1% to 2,063.38

Hang Seng Index up 0.7% to 26,353.63

Shanghai Composite up 1.5% to 3,676.59

Sensex up 0.3% to 58,458.54

Australia S&P/ASX 200 little changed at 7,530.34

Kospi down 0.5% to 3,187.42

Brent Futures up 0.4% to $72.53/bbl

Gold spot down 0.4% to $1,815.21

U.S. Dollar Index up 0.29% to 92.30

German 10Y yield rose 2.6 bps to -0.341%

Euro little changed at $1.1863

Brent Futures up 0.4% to $72.52/bbl

Top Overnight News from Bloomberg

The euro-area economy expanded faster than previously reported in the second quarter, bolstered by a surge in consumer spending. Output increased 2.2% in the three months through June, more than the 2% initially estimated by Eurostat. Household consumption was up 3.7%, with government outlays and investment also contributing to growth

U.K. house prices picked up momentum in August, with the tapering of a tax break on purchases doing little to dent demand for property, according to Halifax. The average value of a home rose 0.7% to 262,954 pounds ($364,000), the mortgage lender said Tuesday. That followed a 0.4% gain in July. The annual pace of increase slowed marginally to 7.1%

The Swiss National Bank’s pile of foreign exchange increased to 929.3 billion francs ($1 trillion) in August, suggesting officials used interventions to depress the value of their currency

China’s export growth unexpectedly surged in August as suppliers likely boosted orders ahead of the year-end shopping season, offsetting any port disruptions due to fresh outbreaks of the delta strain

Spain is the latest European nation turning to a hot market for green debt as it seeks to fund projects that mitigate climate change. The nation is seeking to raise 5 billion euros ($5.9 billion) by offering a bond maturing in 2042 via banks Tuesday

President Joe Biden needs Democrats in Congress to give him a political boost by passing his $4 trillion economic agenda, but deepening divisions in the party threaten the chances of that happening any time soon.

A deeper look at global markets courtesy of Newsquawk

Asia-Pac stocks traded cautiously as the region struggled for direction after a non-existent lead due to the holiday closure in the US and tentativeness amid key announcements including the RBA policy decision and Chinese trade data. ASX 200 (Unch) remained pressured by underperformance in the mining sector after Dalian iron ore futures slumped around 5% near the open and with losses across the industry heavyweights BHP, Rio and Fortescue, while participants also lacked commitment heading into the RBA policy decision where the RBA announced it is to proceed with tapering whilst also extended the period to at least February from mid-November. Nikkei 225 (+0.9%) continued to benefit from the upcoming leadership transition which helped the index shrug off disappointing household spending data to briefly reclaim the 30k level with shares of Keyence and Murata boosted on their looming inclusion to the benchmark index, while the addition of Nintendo also underpinned its shares albeit to a lesser extent. Hang Seng (+0.7%) and Shanghai Comp. (+1.5%) gradually shrugged off the early indecision as participants awaited the latest Chinese trade data which topped estimates in USD terms including a 25.6% jump in exports. However, the market reaction to the data was muted with the CNY-denominated trade figures less convincing and amid mixed regulatory-focused headlines including reports that China will strengthen regulations to prevent a disorderly expansion of capital but will also support Chinese companies to list in Hong Kong and will step up monitoring of cross-border capital flows to maintain market stability. Finally, 10yr JGBs recouped some of the recent losses and re-approached the 152.00 level amid weak Household Spending data and continued gains in Japanese stocks, but with upside limited after relatively stable/slightly softer metrics from the 30yr JGB auction including a lower b/c and accepted prices.

Top Asian News

Soros Calls BlackRock’s China Investment a ‘Tragic Mistake’

BOJ Needs More Realistic Price Goal, Ex-Deputy Governor Says

Gold Declines as Treasury Yields Push Higher After Long Weekend

Hong Kong’s Move to Reopen China Border Boosts Stocks

Bourses in Europe have retained the uninspiring price action seen at the cash open (Euro Stoxx 50 -0.1%; Stoxx 600 -0.1%) amidst a lack of fresh catalysts and ahead of the US' return from its Labor Day holiday. The tone this morning thus far has remained tentative, with participants keeping powder dry as Thursday's ECB looms, whilst a plethora of post-NFP Fed speakers are scattered between Wednesday and Friday. US equity futures have traded on either side of the flat mark but with mild underperformance seen in the RTY (-0.1%) vs its ES (+0.1%), YM (+0.1%) and NQ (+0.1%) peers. This morning has also seen some positive omens out of banks on equities – Barclays raised its SPX price target to 4600 from 4400 (vs 4535 close on Friday), whilst UBS raised its Stoxx 600 target to 510 from 470 (vs current ~474) and upped its 2021 EPS growth forecast to 60% & forecast 15% growth in '22. The Swiss bank continues to see an earnings-driven market & expect P/E multiples to modestly derate to 16x 12m forward by year-end. Sticking with Europe, sectors are primarily negative with no discernible bias and the breadth of price action narrow. Still, the Telecoms sector has retained the top spot, albeit to a lesser magnitude vs the open. Deutsche Telekom (+0.7%) is the driving force behind the Telecom outperformance after opening higher by around 3% following its agreement with Tele2 (-0.1%) to sell their shares (25% and 75%respectively) in T-Mobile Netherlands to the Apax funds and Warburg Pincus. Furthermore, Deutsche Telekom also entered a long-term strategic partnership and share swap agreement with Softbank. Additionally, Deutsche Telekom CEO noted that the Co. is looking at options for its BT (+0.9%) stake and expects something to happen within the next 12 months. Deutsche Telekom owns a 12.06% stake in BT. The former divestment of the Dutch T-Mobile unit has also given rival KPN (+4.1%) a lift, potentially on sector consolidation tailwinds. In terms of individual movers, Allianz (-0.3%) remains mildly pressured after German watchdog BaFin has reportedly launched a probe into Allianz over structured Alpha Investment Funds. Meanwhile, Salzgitter (+3.4%) was bolstered after another guidance upgrade – citing sustained upbeat development in prices and demand

Top European News

Euro-Area Economy Grew Faster Than Expected in Second Quarter

Merkel Confidant Dies Days After Becoming China Ambassador

Merkel Endorses Laschet, Takes Swipe at Scholz in Election Pitch

Nord Stream 2 Gas Link Moves Closer to Start as Last Pipe Welded

In FX, some relative calm after the overnight storm for the Aussie that knee-jerked higher on the back of the RBA’s decision to press ahead with plans to trim bond purchases to Aud 4 bn/week from Aud 5 bn before recoiling in response to the decision to extend the QE timeframe to at least mid-February 2022 from mid-November this year due to a delay in the economic recovery and increased uncertainty associated with the Delta outbreak. To recap, markets were finely divided over the possibility of the Board aborting its planned tapering altogether or ploughing on, so a decent reaction in Aud/Usd and Aud/Nzd was almost guaranteed, but the headline pair is pulling back a bit further from circa 0.7469 to under 0.7400 and the cross is eyeing 1.0400 compared to just above 1.0450 at one stage even though the Kiwi is slipping back in sympathy between 0.7153-10 parameters after spiking alongside 10 year NZ yields vs its US peer.

DXY/CAD - Having dipped a solitary tick under Monday’s 92.105 Labor Day low, the index subsequently regained composure and sufficient momentum to notch a marginally higher high at 92.324 vs 92.314 against the backdrop of more pronounced bear-steepening in US Treasuries and other global bonds in the run up to this week’s heavy supply schedule. Moreover, the Greenback gleaned traction from the inability of several major counterparts to cash in when the pendulum was swinging in their favour. In terms of fundamentals, employment trends for August are rather obsolete given Friday’s official jobs data, so the Usd 58 bn 3 year note auction is likely to warrant more attention before the rest of the refunding and the US agenda picks up in general from tomorrow with the latest Fed Beige Book and speakers. Meanwhile, the Loonie has lost a bit more of its oil-powered impetus as WTI crude meanders and is also heading into Wednesday’s BoC policy meeting cautiously within a 1.2582-19 band.

EUR/CHF/GBP/JPY - All narrowly mixed against the Dollar and rangy, as the Euro continues to hold above 1.1850, but beneath 1.1900 irrespective of Eurozone surveys (like a weak ZEW) or data and is probably keeping counsel for the ECB instead, while the Franc is pivoting 0.9150 and hardly reacted to softer than expected Swiss jobless rates. Elsewhere, Sterling derived some support from BoE’s Saunders underlining his more hawkish leanings (see 8.34BST post on the Headline Feed for bullets), but not enough to revisit 1.3850+ peaks and is now probing the 1.3800 handle following a breach of the 200 DMA and 50 DMA. Similarly, the Yen is striving to keep afloat of 110.00 in wake of Japanese household spending missing consensus by a mile and before attention switches to Q2 GDP, Jule trade and current account balances plus August’s Economy Watchers Poll.

In commodities, WTI and Brent front month futures are choppy after the overnight upside momentum petered out as European players entered the fray. Prices had been hovering just above USD 69/bbl and USD 72.50/bbl, respectively before losing both levels with newsflow for the complex on the lighter side. Participants will notice a dichotomy between the intraday price changes due to the lack of WTI futures settlement yesterday on account of the US Labor Day holiday – with the weekly Private Inventory data also delayed until later today, whilst the EIA Weekly Petroleum Status Report is deferred to Thursday 16:00BST/11:00EDT. Over in the GoM, BSEE estimated approximately 83.9% of oil production in the Gulf of Mexico shut-in (prev. 88.3%), and about 80.8% of the gas production in the Gulf of Mexico has been shut-in (prev. 82.7%), while a total of 99 oil and gas production platforms remain evacuated. It was also reported that the US Coast Guard was investigating nearly 350 reports of oil spills in and along the Gulf of Mexico following Hurricane Ida, albeit this is unlikely to affect policy in the near term as things stand. Elsewhere, spot gold and silver have been drifting lower in tandem with the rise in the Buck, although with technicals also bearing some weight in the absence of fresh catalysts. Spot gold fell back below its 100 DMA (USD 1,815/oz) and has sights on the 200 DMA (1,809.59/oz) at the time of writing. Similarly, spot silver hit a ceiling at its 50 DMA around 24.80/oz. Meanwhile, copper prices declined overnight – with LME still subdued and back under USD 9,500/t -as Chinese copper imports fell to over a 2yr low, whilst Chinese iron ore imports rose for the first time in five months. However, analysts believe this is short-lived given China's steel target reduction.

US Event Calendar

No major releases scheduled

DB's Jim Reid concludes the overnight wrap

It may have been a quiet session with the US out on holiday, but markets continued their upward ascent once again yesterday thanks to investor hopes that the weak US jobs data would reduce the likelihood that the Fed would shortly begin to withdraw their monetary stimulus. Global equities were buoyant across the board, with the STOXX 600 (+0.69%) closing only -0.13% away from its all-time closing high last month, the MSCI World index (+0.18%) advancing to a new record, and futures on the S&P 500 (+0.11% this morning) edging up and similarly pointing to record highs for that index as well. In Asia, risk appetite has continued to remain firm with the Nikkei (+0.75%), Hang Seng (+0.61%) and Shanghai Comp (+0.77%) all up. Bucking the trend is the Kospi which is down -0.70%.

Back to Europe yesterday and equity gains were pretty broad-based across Europe, with the DAX (+0.96%), the CAC 40 (+0.80%) and the FTSE 100 (+0.68%) all moving higher across the continent, though Spain’s IBEX 35 (+0.21%) put in a relatively weaker performance. At the sectoral level, tech stocks led the gains, with the STOXX Technology Index up +1.85%, which comes off the back of having advanced for 10 of the last 11 weeks, and brings the index to its highest level since 2000.

Elsewhere, sovereign bond yields in Europe generally moved lower yesterday ahead of this week’s ECB decision, with those on 10yr bunds (-0.5bps), OATs (-0.9bps) and BTPs (-1.6bps) all falling. That said, there was a very big rise in inflation expectations across the continent, with German 10yr breakevens (+5.1bps) rising to their highest level since 2013, at 1.57%, just as Italian (+6.7bps) 10yr breakevens rose to their own post-2013 high of 1.53 %.

Speaking of that ECB decision, our chief European economist Mark Wall discusses the issue in a new podcast out yesterday (link here), and makes the point that whether the slowing in purchase is done in September or December is besides the point. A slower pace of PEPP purchases, and hence peak asset purchases, is inevitable, though his view is that a September announcement is slightly more likely than December. You can read his written preview here as well (link here).

Sentiment this morning is being aided by positive trade data out of China as exports came in stronger than expectations at +25.6% (vs. +17.3% expected) while imports came in at +33.1% (vs. +26.9% expected). In Fx, the Australian dollar is up +0.29 % after the RBA stuck with its decision to taper bond purchases to AUD4bn a week and added that it will continue the purchases at this rate until at least mid-February 2022. The RBA left its policy rate and yield target unchanged. The central bank said that it views the setback to economy on account of the lockdowns as temporary. The RBA also committed to lower rates for longer as it said that conditions for rate rises will not be met before 2024 under the central scenario. Overall while the taper was a close call in terms of expectations it seems the language used by the RBA is relatively dovish.

The RBA decision seems to have caused Aussie yields to rally a couple of bps from before the announcement and that may have dragged 10yr USTs yields down a touch as they have rallied off their highs for the session and stand +1.7bps at 1.3393%. In terms of other overnight data releases, Japan’s July labour cash earnings printed at a stronger +1.0% yoy (vs. +0.4% yoy expected) while the previous month’s reading was revised up by +0.2pp to +0.1% yoy.

One area that we might be seeing some fresh inflationary pressures soon are in aluminium prices, which hit their highest level in over a decade yesterday after the coup in Guinea raised concerns that the supply of bauxite (which is used to make aluminium) could be affected. Though the country’s population is estimated to be around 13-14 million people, they are a major supplier of bauxite, supplying around a quarter of the world’s total, so any disruption there could have profound effects on the global market. More broadly however, it was a fairly subdued day for commodities, with Brent crude (-0.54%) oil prices losing ground, whilst gold (-0.24%) also fell back following 4 successive weekly gains.

Turning to the pandemic, the picture is definitely brightening at the global level, and the latest John Hopkins University data is showing that last week saw the first weekly decline in new cases since early June. That said, a number of places are still tightening restrictions, with Singapore taking fresh action yesterday, which includes more extensive testing in higher-risk environments, and a ban on workplace social gatherings from September 8. Elsewhere, in a move that is likely to be world’s first, the Chilean government has approved the Sinovac Biotech’s vaccine for use on children as young as six, with shots being administered beginning this month.

There wasn’t much data yesterday either with the US on holiday, though German factory orders unexpectedly grew by +3.4% in July (vs. -0.7% expected). However, the country’s construction PMI for August fell back to a three-month low of 44.6. Meanwhile in the UK, the construction PMI there fell back to a five-month low of 55.2 (vs. 56.0 expected).

It’s another quiet day on the calendar ahead, though data highlights will include German industrial production for July and the ZEW survey for September. Meanwhile from central banks, the BoE’s Saunders will be speaking.

It was Jan. 11, 2024 when software giant Microsoft (MSFT) briefly passed Apple (AAPL) as the most valuable company in the world.

Microsoft's stock closed 0.5% higher, giving it a market valuation of $2.859 trillion.

It rose as much as 2% during the session and the company was briefly worth $2.903 trillion. Apple closed 0.3% lower, giving the company a market capitalization of $2.886 trillion.

"It was inevitable that Microsoft would overtake Apple since Microsoft is growing faster and has more to benefit from the generative AI revolution," D.A. Davidson analyst Gil Luria said at the time, according to Reuters.

The two tech titans have jostled for top spot over the years and Microsoft was ahead at last check, with a market cap of $3.085 trillion, compared with Apple's value of $2.684 trillion.

Analysts noted that Apple had been dealing with weakening demand, including for the iPhone, the company’s main source of revenue.

Demand in China, a major market, has slumped as the country's economy makes a slow recovery from the pandemic and competition from Huawei.

Sales in China of Apple's iPhone fell by 24% in the first six weeks of 2024 compared with a year earlier, according to research firm Counterpoint, as the company contended with stiff competition from a resurgent Huawei "while getting squeezed in the middle on aggressive pricing from the likes of OPPO, vivo and Xiaomi," said senior Analyst Mengmeng Zhang.

“Although the iPhone 15 is a great device, it has no significant upgrades from the previous version, so consumers feel fine holding on to the older-generation iPhones for now," he said.

A man scrolling through Netflix on an Apple iPad Pro. Photo by Phil Barker/Future Publishing via Getty Images.

Counterpoint said that the first six weeks of 2023 saw abnormally high numbers with significant unit sales being deferred from December 2022 due to production issues.

Apple is planning to open its eighth store in Shanghai – and its 47th across China – on March 21.

The company also plans to expand its research centre in Shanghai to support all of its product lines and open a new lab in southern tech hub Shenzhen later this year, according to the South China Morning Post.

Meanwhile, over in Europe, Apple announced changes to comply with the European Union's Digital Markets Act (DMA), which went into effect last week, Reuters reported on March 12.

Beginning this spring, software developers operating in Europe will be able to distribute apps to EU customers directly from their own websites instead of through the App Store.

"To reflect the DMA’s changes, users in the EU can install apps from alternative app marketplaces in iOS 17.4 and later," Apple said on its website, referring to the software platform that runs iPhones and iPads.

"Users will be able to download an alternative marketplace app from the marketplace developer’s website," the company said.

Apple has also said it will appeal a $2 billion EU antitrust fine for thwarting competition from Spotify (SPOT) and other music streaming rivals via restrictions on the App Store.

The company's shares have suffered amid all this upheaval, but some analysts still see good things in Apple's future.

Bank of America Securities confirmed its positive stance on Apple, maintaining a buy rating with a steady price target of $225, according to Investing.com.

The firm's analysis highlighted Apple's pricing strategy evolution since the introduction of the first iPhone in 2007, with initial prices set at $499 for the 4GB model and $599 for the 8GB model.

BofA said that Apple has consistently launched new iPhone models, including the Pro/Pro Max versions, to target the premium market.

Analyst says Apple selloff 'overdone'

Concurrently, prices for previous models are typically reduced by about $100 with each new release.

This strategy, coupled with installment plans from Apple and carriers, has contributed to the iPhone's installed base reaching a record 1.2 billion in 2023, the firm said.

Apple has effectively shifted its sales mix toward higher-value units despite experiencing slower unit sales, BofA said.

This trend is expected to persist and could help mitigate potential unit sales weaknesses, particularly in China.

BofA also noted Apple's dominance in the high-end market, maintaining a market share of over 90% in the $1,000 and above price band for the past three years.

The firm also cited the anticipation of a multi-year iPhone cycle propelled by next-generation AI technology, robust services growth, and the potential for margin expansion.

On Monday, Evercore ISI analysts said they believed that the sell-off in the iPhone maker’s shares may be “overdone.”

The firm said that investors' growing preference for AI-focused stocks like Nvidia (NVDA) has led to a reallocation of funds away from Apple.

In addition, Evercore said concerns over weakening demand in China, where Apple may be losing market share in the smartphone segment, have affected investor sentiment.

And then ongoing regulatory issues continue to have an impact on investor confidence in the world's second-biggest company.

“We think the sell-off is rather overdone, while we suspect there is strong valuation support at current levels to down 10%, there are three distinct drivers that could unlock upside on the stock from here – a) Cap allocation, b) AI inferencing, and c) Risk-off/defensive shift," the firm said in a research note.

Major typhoid fever surveillance study in sub-Saharan Africa indicates need for the introduction of typhoid conjugate vaccines in endemic countries

There is a high burden of typhoid fever in sub-Saharan African countries, according to a new study published today in The Lancet Global Health. This high…

There is a high burden of typhoid fever in sub-Saharan African countries, according to a new study published today in The Lancet Global Health. This high burden combined with the threat of typhoid strains resistant to antibiotic treatment calls for stronger prevention strategies, including the use and implementation of typhoid conjugate vaccines (TCVs) in endemic settings along with improvements in access to safe water, sanitation, and hygiene.

Credit: IVI

There is a high burden of typhoid fever in sub-Saharan African countries, according to a new study published today in The Lancet Global Health. This high burden combined with the threat of typhoid strains resistant to antibiotic treatment calls for stronger prevention strategies, including the use and implementation of typhoid conjugate vaccines (TCVs) in endemic settings along with improvements in access to safe water, sanitation, and hygiene.

The findings from this 4-year study, the Severe Typhoid in Africa (SETA) program, offers new typhoid fever burden estimates from six countries: Burkina Faso, Democratic Republic of the Congo (DRC), Ethiopia, Ghana, Madagascar, and Nigeria, with four countries recording more than 100 cases for every 100,000 person-years of observation, which is considered a high burden. The highest incidence of typhoid was found in DRC with 315 cases per 100,000 people while children between 2-14 years of age were shown to be at highest risk across all 25 study sites.

There are an estimated 12.5 to 16.3 million cases of typhoid every year with 140,000 deaths. However, with generic symptoms such as fever, fatigue, and abdominal pain, and the need for blood culture sampling to make a definitive diagnosis, it is difficult for governments to capture the true burden of typhoid in their countries.

“Our goal through SETA was to address these gaps in typhoid disease burden data,” said lead author Dr. Florian Marks, Deputy Director General of the International Vaccine Institute (IVI). “Our estimates indicate that introduction of TCV in endemic settings would go to lengths in protecting communities, especially school-aged children, against this potentially deadly—but preventable—disease.”

In addition to disease incidence, this study also showed that the emergence of antimicrobial resistance (AMR) in Salmonella Typhi, the bacteria that causes typhoid fever, has led to more reliance beyond the traditional first line of antibiotic treatment. If left untreated, severe cases of the disease can lead to intestinal perforation and even death. This suggests that prevention through vaccination may play a critical role in not only protecting against typhoid fever but reducing the spread of drug-resistant strains of the bacteria.

There are two TCVs prequalified by the World Health Organization (WHO) and available through Gavi, the Vaccine Alliance. In February 2024, IVI and SK bioscience announced that a third TCV, SKYTyphoid™, also achieved WHO PQ, paving the way for public procurement and increasing the global supply.

Alongside the SETA disease burden study, IVI has been working with colleagues in three African countries to show the real-world impact of TCV vaccination. These studies include a cluster-randomized trial in Agogo, Ghana and two effectiveness studies following mass vaccination in Kisantu, DRC and Imerintsiatosika, Madagascar.

Dr. Birkneh Tilahun Tadesse, Associate Director General at IVI and Head of the Real-World Evidence Department, explains, “Through these vaccine effectiveness studies, we aim to show the full public health value of TCV in settings that are directly impacted by a high burden of typhoid fever.” He adds, “Our final objective of course is to eliminate typhoid or to at least reduce the burden to low incidence levels, and that’s what we are attempting in Fiji with an island-wide vaccination campaign.”

As more countries in typhoid endemic countries, namely in sub-Saharan Africa and South Asia, consider TCV in national immunization programs, these data will help inform evidence-based policy decisions around typhoid prevention and control.

###

About the International Vaccine Institute (IVI)

The International Vaccine Institute (IVI) is a non-profit international organization established in 1997 at the initiative of the United Nations Development Programme with a mission to discover, develop, and deliver safe, effective, and affordable vaccines for global health.

IVI’s current portfolio includes vaccines at all stages of pre-clinical and clinical development for infectious diseases that disproportionately affect low- and middle-income countries, such as cholera, typhoid, chikungunya, shigella, salmonella, schistosomiasis, hepatitis E, HPV, COVID-19, and more. IVI developed the world’s first low-cost oral cholera vaccine, pre-qualified by the World Health Organization (WHO) and developed a new-generation typhoid conjugate vaccine that is recently pre-qualified by WHO.

IVI is headquartered in Seoul, Republic of Korea with a Europe Regional Office in Sweden, a Country Office in Austria, and Collaborating Centers in Ghana, Ethiopia, and Madagascar. 39 countries and the WHO are members of IVI, and the governments of the Republic of Korea, Sweden, India, Finland, and Thailand provide state funding. For more information, please visit https://www.ivi.int.

Incidence of typhoid fever in Burkina Faso, Democratic Republic of the Congo, Ethiopia, Ghana, Madagascar, and Nigeria (the Severe Typhoid in Africa programme): a population-based study

We’ve added 60% to national debt since 2018. Germany - a country with major economic woes - added ‘just’ 32%.

Maybe it will never matter. Maybe MMT is real. Maybe we just cancel or inflate it out. Maybe career real estate borrowers or career politicians aren’t the answer.

I have no idea. Only time will tell. But it’s going to be fascinating to watch it play out.

He is right: it will be fascinating, and the latest budget deficit data simply confirmed that the day of reckoning will come very soon, certainly sooner than the two years that One River's Eric Peters predicted this weekend for the coming "US debt sustainability crisis."

According to the US Treasury, in February, the US collected $271 billion in various tax receipts, and spent $567 billion, more than double what it collected.

The two charts below show the divergence in US tax receipts which have flatlined (on a trailing 6M basis) since the covid pandemic in 2020 (with occasional stimmy-driven surges)...

... and spending which is about 50% higher compared to where it was in 2020.

The end result is that in February, the budget deficit rose to $296.3 billion, up 12.9% from a year prior, and the second highest February deficit on record.

And the punchline: on a cumulative basis, the budget deficit in fiscal 2024 which began on October 1, 2023 is now $828 billion, the second largest cumulative deficit through February on record, surpassed only by the peak covid year of 2021.

But wait there's more: because in a world where the US is spending more than twice what it is collecting, the endgame is clear: debt collapse, and while it won't be tomorrow, or the week after, it is coming... and it's also why the US is now selling $1 trillion in debt every 100 days just to keep operating (and absorbing all those millions of illegal immigrants who will keep voting democrat to preserve the socialist system of the US, so beloved by the Soros clan).

... having already surpassed total US defense spending and soon to surpass total health spending and, finally all social security spending, the largest spending category of all, which means that US debt will now rise exponentially higher until the inevitable moment when the US dollar loses its reserve status and it all comes crashing down.

We conclude with another observation by CNBC's Brian Sullivan, who quotes an email by a DC strategist...

.. which lays out the proposed Biden budget as follows:

The budget deficit will growth another $16 TRILLION over next 10 years. Thats *with* the proposed massive tax hikes.

Without them the deficit will grow $19 trillion.

That's why you will hear the "deficit is being reduced by $3 trillion" over the decade.

No family budget or business could exist with this kind of math.

Of course, in the long run, neither can the US... and since neither party will ever cut the spending which everyone by now is so addicted to, the best anyone can do is start planning for the endgame.

We use cookies on our website to give you the most relevant experience by remembering your preferences and repeat visits. By clicking “Accept”, you consent to the use of ALL the cookies.

This website uses cookies to improve your experience while you navigate through the website. Out of these, the cookies that are categorized as necessary are stored on your browser as they are essential for the working of basic functionalities of the website. We also use third-party cookies that help us analyze and understand how you use this website. These cookies will be stored in your browser only with your consent. You also have the option to opt-out of these cookies. But opting out of some of these cookies may affect your browsing experience.

Necessary cookies are absolutely essential for the website to function properly. These cookies ensure basic functionalities and security features of the website, anonymously.

Cookie

Duration

Description

cookielawinfo-checbox-analytics

11 months

This cookie is set by GDPR Cookie Consent plugin. The cookie is used to store the user consent for the cookies in the category "Analytics".

cookielawinfo-checbox-functional

11 months

The cookie is set by GDPR cookie consent to record the user consent for the cookies in the category "Functional".

cookielawinfo-checbox-others

11 months

This cookie is set by GDPR Cookie Consent plugin. The cookie is used to store the user consent for the cookies in the category "Other.

cookielawinfo-checkbox-necessary

11 months

This cookie is set by GDPR Cookie Consent plugin. The cookies is used to store the user consent for the cookies in the category "Necessary".

cookielawinfo-checkbox-performance

11 months

This cookie is set by GDPR Cookie Consent plugin. The cookie is used to store the user consent for the cookies in the category "Performance".

viewed_cookie_policy

11 months

The cookie is set by the GDPR Cookie Consent plugin and is used to store whether or not user has consented to the use of cookies. It does not store any personal data.

Functional cookies help to perform certain functionalities like sharing the content of the website on social media platforms, collect feedbacks, and other third-party features.

Performance cookies are used to understand and analyze the key performance indexes of the website which helps in delivering a better user experience for the visitors.

Analytical cookies are used to understand how visitors interact with the website. These cookies help provide information on metrics the number of visitors, bounce rate, traffic source, etc.

Advertisement cookies are used to provide visitors with relevant ads and marketing campaigns. These cookies track visitors across websites and collect information to provide customized ads.

{kind=link}

{kind=link}