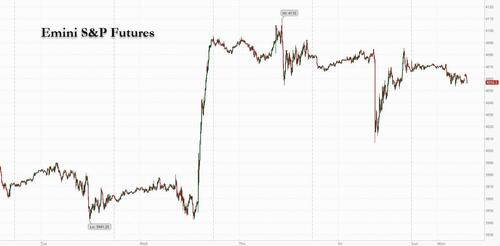

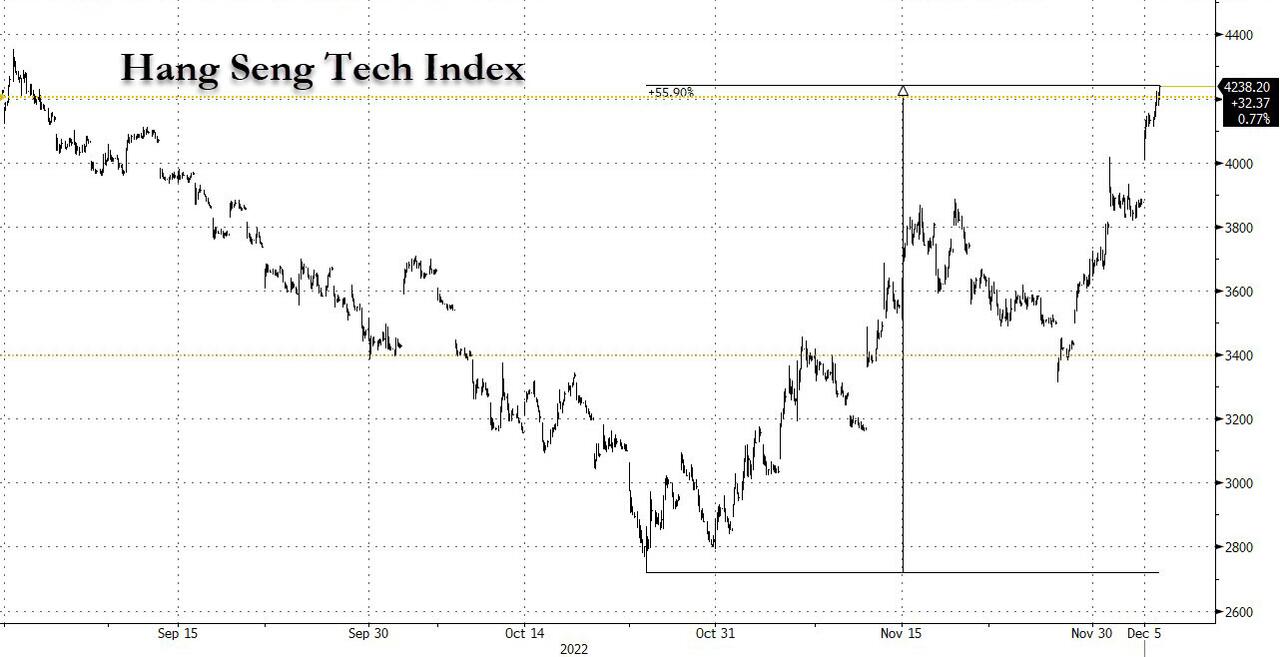

US Futures Drop As Chinese Stocks Soar On Reopening Optimism

US stock futures fell on Monday as investors weighed the outlook for economic growth against the possibility of a softening in the Federal Reserve’s policy, or in other words, whether bad news is again bad news. At the same time, and just one week after China was swept by violent anti-covid zero protests, Chinese stocks in listed in the US rose sharply after Hong Kong-listed peers rallied and the offshore yuan strengthened past the key 7.00 level after Chinese authorities eased Covid testing requirements across major cities over the weekend. The financial hub of Shanghai scrapped PCR testing requirements to enter outdoor public venues such as parks or use public transportation starting Monday. Hangzhou, home to tech giant Alibaba dropped obligations to enter most public venues including offices and supermarkets, while Shanghai also eased rules. As a result, Hong Kong’s Hang Seng Tech Index closed at session highs, soaring some 9.2%, the biggest jump since Nov. 11, after China eased Covid testing requirements across major cities over the weekend.

Meanwhile in the US, Nasdaq 100 futures were down 0.4% by 7:30 a.m. in New York, while S&P 500 futures dipped 0.5%. The indexes shrugged off a hotter-than-expected jobs report on Friday as investors and erased almost all early losses as they remained optimistic that the Fed would slow the pace of interest rate hikes at its meeting this month. The dollar remained near session lows, boosting most Group-of-10 currencies. Treasury yields climbed across the curve. Oil advanced after OPEC+ kept its 2 million production cut and amid growing signs China is reopening, while gold was little changed. Bitcoin rose more than 1%, gaining for a second day.

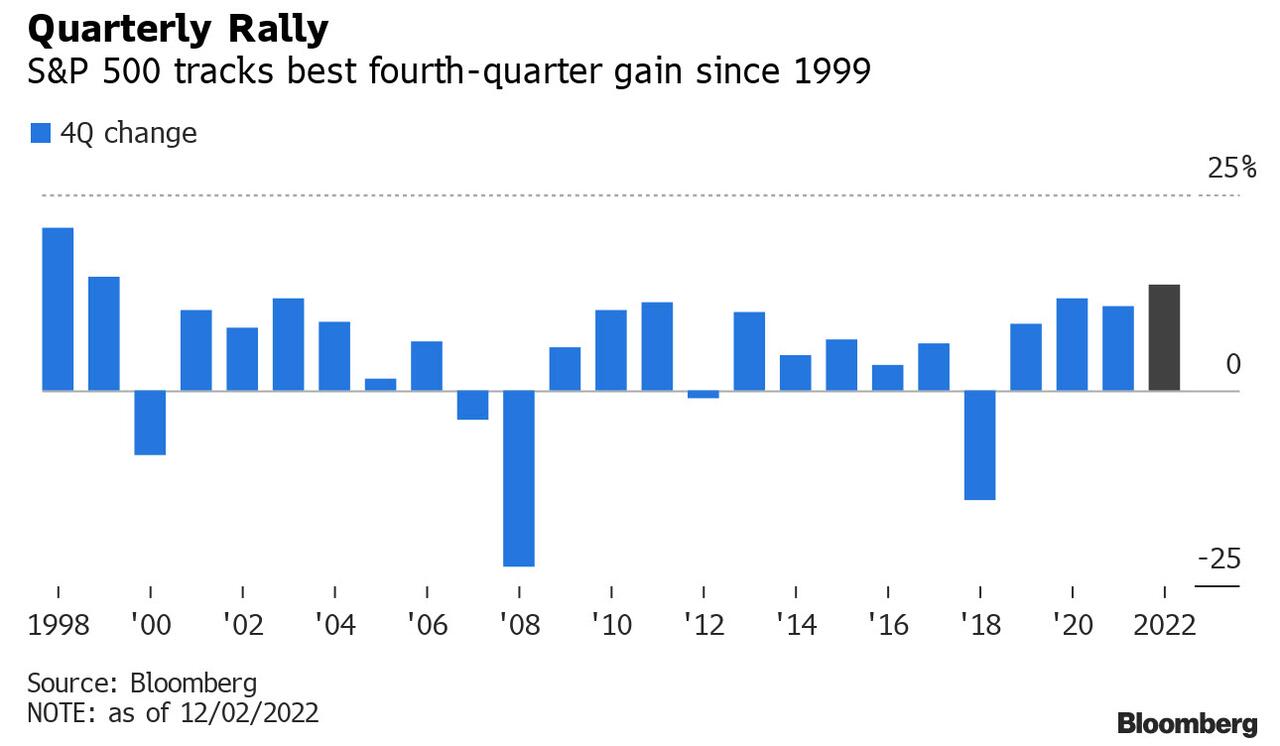

The S&P 500 is on course for its biggest fourth-quarter gain since 1999 as signs of a cooling in US inflation have led to a pullback in bond yields, but market participants warn the outlook for next year remains uncertain amid the risk to corporate earnings from the specter of a recession.

Among notable moves in premarket trading, US-listed Chinese stocks extended their torrid rally as easing Covid curbs in major Chinese cities fueled optimism that Beijing is hastening the shift away from its Covid Zero strategy; Alibaba rose 5.2%, Baidu +5.6%, Pinduoduo +5%, JD.com +5.6%, Bilibili +16%, Nio +6.3%, XPeng +11%. Cryptocurrency-exposed stocks rose as Bitcoin extended gains for a second day. Tesla slipped as much as 4.8% after a Bloomberg News report said that the electric vehicle maker planned to lower production at its Shanghai factory. Here are the other notable premarket movers:

Activision Blizzard rises 2.3% after Bloomberg News reported that Microsoft is ready to fight for its $69 billion acquisition of the video gaming company if the US Federal Trade Commission files a lawsuit seeking to block the deal.

Marathon Digital and Riot Blockchain lead cryptocurrency-exposed stocks higher as Bitcoin extends gains for a second day. Marathon Digital +4.9%, Riot Blockchain (RIOT US) +2.8% and Coinbase +2.3%

Keep an eye on airlines’ shares as Morgan Stanley says 2023 could be a “Goldilocks” year for air travel, boosting earnings beyond current expectations, as the broker upgrades United Airlines to overweight and cuts Allegiant Travel to equal-weight.

Alaska Air is initiated with a buy recommendation at Citi, saying the carrier has attributes to offset headwinds facing domestic airlines in 2023. Additionally, the broker begins coverage on JetBlue with a neutral rating.

Watch Terex as Deutsche Bank cut its rating to hold from buy on recent outperformance, saying that it’s best to stay defensively-positioned on US industrial stocks into 2023.

Keep an eye on Ameris Bancorp and Atlantic Union (AUB US) as Piper Sandler resumed coverage on US mid-Atlantic and southeast banks, saying the two lenders are its preferred larger-cap names with both at attractive entry points.

“Despite an increasingly optimistic end to the year, the main indexes seem unlikely to recover their lost ground and the current rally may be too little, too late,” said Richard Hunter, head of markets at Interactive Investor. Moreover, “doubts still linger” on how much more the Fed will still need to raise interest rates and the impact of higher-for-longer inflation, he said.

Morgan Stanley strategist Michael Wilson said the year-end rally he had predicted had now run its course and investors are better off booking profits from here on. He sees an “absolute upside” for the S&P 500 at 4,150 points -- about 2% above current levels -- which could be achieved “over the next week or so.”

Notable other US headlines:

WSJ's Timiraos writes that Fed officials have signalled plans to hike by 50bp at the December gathering, though elevated wage pressures could lead them to continue increasing rates to levels higher than investors currently expect.

Delta Air Lines (DAL) confirmed it reached an agreement in principle for a new pilot contract after it offered a 34% pay increase to pilots over 3 years, according to Reuters.

Apple (AAPL) supplier Foxconn (2317 TT) expects full production at its COVID-hit plant in China to resume from late December to early January, while the Co. and the local government are pushing hard on the plant's recruitment drive but many uncertainties remain, according to sources cited by Reuters.

Moldova’s central bank is to conduct an extraordinary meeting on Monday to assess its main policy indicators including the policy rate, according to Reuters.

Iran’s Attorney General announced that Iran abolished its morality police and is considering changing hijab laws following the protests, according to WSJ.

Euro Stoxx 50 falls 0.2%. FTSE 100 outperforms peers, adding 0.3%. Here are some of the biggest European movers today:

Tech investors Naspers and Prosus both gain more than 5% in Johannesburg trading Monday after Chinese authorities accelerate a shift toward reopening the economy.

European mining stocks in focus as metals advance after Chinese authorities eased Covid testing requirements across major cities over the weekend. Rio Tinto and Glencore shares rise as much as 3.7% and 2.4% respectively.

Credit Suisse shares climb as much as 3.7% in early trading after the Wall Street Journal reported that Saudi Arabia’s Crown Prince Mohammed bin Salman is preparing to invest in the Swiss lender’s investment-bank unit.

Grifols shares rise as much as 6.5% in early trading after Morgan Stanley raised to overweight from equal-weight on the expectation that 2023 will be a “strong growth year” supported by accelerating plasma collections and early signs of declining donor fees.

Bayer shares slide as much as 2.8%, the most in about a month, after Bank of America cut its recommendation for the German agropharmaceutical giant to neutral on the company’s lack of catalysts after a 2022 outperformance.

FlatexDEGIRO shares fall as much as 38%, the biggest intraday drop since its 2009 listing, after the online brokerage firm cut its revenue forecast and said it was working on measures to address shortcomings in some business practices and governance identified by a BaFin audit.

German catering equipment company Rational sinks as much as 9%, making them the worst performer in the Stoxx 600, after Bank of America initiated coverage on the stock with an underperform recommendation, citing a “demand crunch” in 2023.

Swedish Orphan Biovitrum shares drop as much as 2.2% after Morgan Stanley downgrades the stock to equal-weight from overweight.

Asian stocks rebounded, inching closer to bull market territory, as Chinese equities resumed their rally on further relaxation of Covid rules in Asia’s biggest economy. The MSCI Asia Pacific Index climbed as much as 1.4%, led by communication services and consumer discretionary shares. Benchmarks in Hong Kong led gains in the region with the Hang Seng Tech Index soaring more than 9% and the Hang Seng China Enterprises Index up roughly 5%. Morgan Stanley upgraded China to overweight.

Investors cheered latest signs of China pivoting from its strict virus rules as authorities eased Covid testing requirements across major cities over the weekend, including the financial hub of Shanghai. The move fueled gains in reopening stocks in China and its neighboring countries such as South Korea. Markets were closed in Thailand for a holiday. The moves coincided with growing bullish calls from Wall Street banks on Chinese equities, with more market watchers calling a bottom in the nation’s shares. Morgan Stanley upgraded China stocks to overweight from an equal-weight position held since January 2021, while abrdn’s Asia Pacific chief executive Rene Buehlmann urged investors to “go back” into Chinese markets.

Elsewhere, stock benchmarks were mixed with gauges in Japan and South Korea trading lower while those in Australia, Singapore and Vietnam rose. After falling for much of the year, Asian stocks staged a dramatic rally in the past few weeks with a surge in foreign inflows into emerging Asian shares, supported by the dollar’s weakness and expectations for a slowdown in the Fed’s hikes. The key Asian stock benchmark still remains about 17% lower so far this year, on course for its worst annual performance in more than a decade.

A closer look at Japanese stocks reveals that they ended mixed as investors gauged the impact of China’s shift toward reopening and US employment data. The Topix fell 0.3% to close at 1,947.90, while the Nikkei advanced 0.2% to 27,820.40. Toyota Motor Corp. contributed the most to the Topix decline, decreasing 1%. Out of 2,164 stocks in the index, 741 rose and 1,304 fell, while 119 were unchanged. “Japanese stocks are a bit weak at the moment as economic indicators are becoming a little more globally skewed,” said Mamoru Shimode, a chief strategist at Resona Asset Management.

Australian stocks rose: the S&P/ASX 200 index rose 0.3% to close at 7,325.60, led by gains in mining and real estate shares, as traders bet on further reopening of the Chinese economy from Covid restrictions. Shares of iron ore miners and steel companies were among top performers advancing as commodity prices rallied on China reopening bets. In New Zealand, the S&P/NZX 50 index rose 0.3% to 11,677.75.

Stocks in India ended flat on Monday as investors likely took profits in recent outperformers, while the focus shifts to the central bank’s monetary policy announcement later this week. The S&P BSE Sensex ended flat at 62,834.60 in Mumbai, while the NSE Nifty 50 Index was also little changed, as both indexes overcame declines of as much as 0.6% each. The key gauges rose for eight consecutive sessions before declining on Friday. The Reserve Bank of India’s rate-setting panel will commenced its three-day meet Monday for the monetary policy to be announced on Wednesday. All of the economists surveyed by Bloomberg expect the benchmark lending rate to be increased, with the median estimate for a 35 basis points hike. Polls in India’s Gujarat, also the home state to Prime Minister Narendra Modi, end today and results will be announced on Dec. 8. Investors will be watchful of the outcome as the results will indicate Modi’s popularity for national elections next in 2024.

In rates, treasuries are mixed as the curve bear flattens with 2s10s narrowing 1.6bps as US trading day begins, extending the flattening move unleashed Friday by stronger-than-estimated November employment data. All Treasuries apart from the very long end fell, with the largest decline seen in the belly of the curve, as traders added to Fed hike wagers ahead of US ISM services numbers for November. Yields remain inside Friday’s ranges, though inverted 2s10s reached -81.4bp, new low for the cycle. 2- to 7-year yields higher by 3bp-4bp on the day, 30-year lower by ~1bp; 10-year higher by ~2bp at 3.50% Most European 10-year yields are lower, led by UK as expectations for BOE rate hikes are pared. IG credit issuance slate blank so far, however dealers expect $10b-$15b this week and $20b for December. Three-month dollar Libor fell for a third straight day, longest streak since February, to 4.72343%.

The Bloomberg Dollar Spot Index snapped a four-day drop as the greenback rose 0.1%. CAD and AUD are the strongest performers in G-10 FX, JPY and GBP underperform. ZAR (1.7%) leads gains in EMFX.

The yen underperformed all its Group-of-10 peers while the Australian and Canadian dollar were the top gainers as commodities got a boost on hopes that China is engineering a gradual shift away from its strict Covid Zero policy. Chinese stocks and the yuan also rallied.

The yuan strengthened past the key 7 per dollar level after Shanghai and Hangzou relaxed Covid testing rules. Hong Kong dollar surged to the strongest level since June 2021. Te onshore yuan extended gain to 1.5% to 6.9450 per dollar, the most since Nov. 11 as reopening optimism continues to boost the currency.

The euro steadied after rising to a fresh five-month high of $1.0585. Euro options bets suggest a run above $1.06 before FOMC meeting. Bunds, Italian bonds swung between modest gains and losses amid a slew of ECB speeches.

The pound slipped after posting four consecutive weeks of gains. Money markets eased BOE rate-hike wagers after policy-maker Swati Dhingra said in a newspaper interview that interest rates should peak below 4.5%. The central bank will conduct bond sales later on Monday

In commoidties, Crude benchmarks have been choppy, but are ultimately firmer post-OPEC+ and as the Russian oil cap comes into effect at USD 60/bbl. Brent rises 1.8% near $87.15 while WTI Jan was at 81.50/bbl, with the latest easing of China's COVID controls also factoring. OPEC+ ministers formally endorsed the output policy rollover and will hold the next JMMC meeting on February 1st, while it vowed to stand ready to adjust oil output to stabilize markets. Russian Deputy PM Novak said they will not operate under the oil price cap even if they have to cut production and the price cap may affect other countries as well, while he added that they are working on mechanisms to ban supplies which are capped. Russia is analysing the price cap imposed by G7 and allies on its oil and made preparations for this, while it will not accept the oil price cap, according to state news agencies citing the Kremlin. Russia's Kremlin, on price cap, said Russia is preparing a decision and will not recognise the price cap; price cap will destabilise global energy market but will not affect Russia's ability to sustain the military operation in Ukraine.

US economic data include November final S&P Global US services and composite PMIs (9:45am), October factory orders and November ISM services (10am)

Market Snapshot

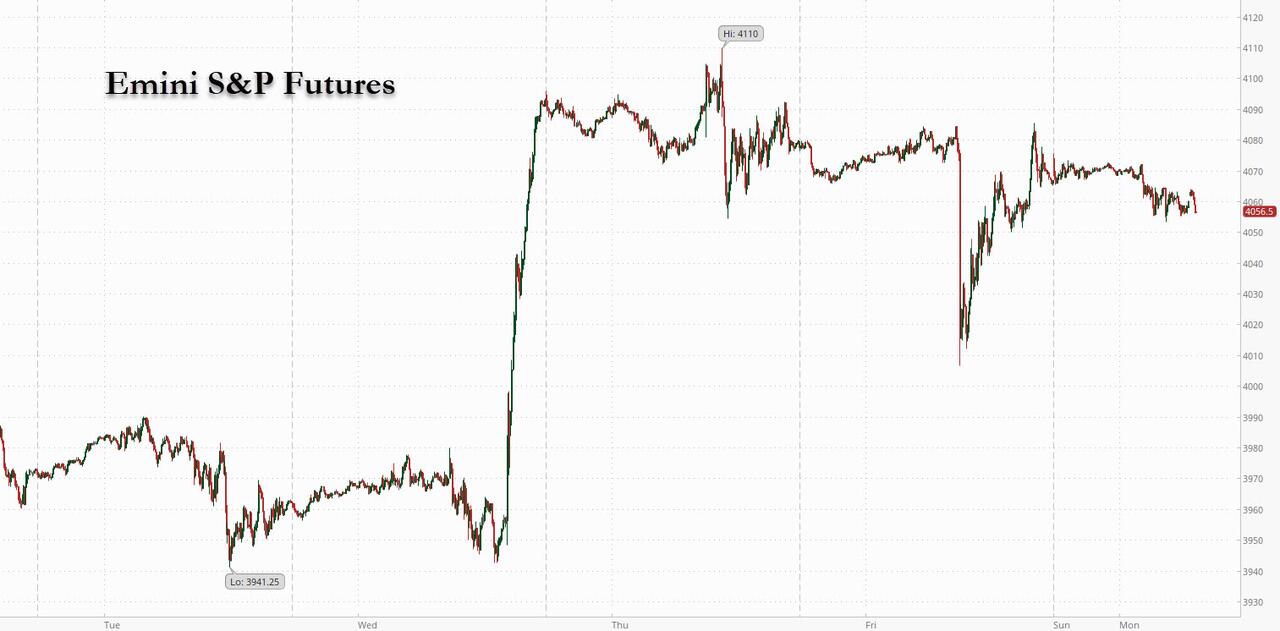

S&P 500 futures down 0.3% to 4,062.75

STOXX Europe 600 little changed at 442.85

MXAP up 1.1% to 159.66

MXAPJ up 1.7% to 521.41

Nikkei up 0.2% to 27,820.40

Topix down 0.3% to 1,947.90

Hang Seng Index up 4.5% to 19,518.29

Shanghai Composite up 1.8% to 3,211.81

Sensex down 0.1% to 62,798.89

Australia S&P/ASX 200 up 0.3% to 7,325.60

Kospi down 0.6% to 2,419.32

German 10Y yield little changed at 1.85%

Euro up 0.2% to $1.0555

Brent Futures up 1.9% to $87.16/bbl

Gold spot down 0.0% to $1,797.23

US Dollar Index little changed at 104.47

Top US News From Bloomberg

ECB Governing Council member Francois Villeroy de Galhau said it’s too early to discuss where interest rates will peak, saying the monetary-tightening process should be carried out at the appropriate pace

The ECB should raise borrowing costs by at least a half-point this month to curb surging consumer prices, according to Governing Council member Gabriel Makhlouf

ECB Governing Council Member Mario Centeno said “everything indicates” that the peak of inflation may be reached in the fourth quarter

“Decisive monetary tightening must continue” as inflation persists above target, Croatian Central Bank Governor Boris Vujcic told the newspaper Jutarnji List, weeks before the Balkan nation joins the euro zone

The US dollar has erased more than half of this year’s gains amid growing expectations the Federal Reserve will temper its aggressive rate hikes, and as optimism grows over China’s reopening plans

Swedish central bankers are divided on the prospects for bringing inflation back to its target after a string of interest-rate increases, minutes from the bank’s latest policy meeting show

Emerging-market central banks face a Catch-22 where plunging economic growth means they can’t keep monetary conditions tight, but elevated inflation doesn’t allow them to halt rate hikes either

OPEC+ responded to surging volatility and growing market uncertainty by keeping its oil production unchanged

The world’s worst- performing major currency looks poised for an impressive turnaround in 2023 as its two key drivers -- a hawkish Federal Reserve and dovish Bank of Japan -- swap places in the eyes of some investors

The BOJ may achieve its inflation target in 2023 as the cost of living has consistently exceeded market expectations this year, according to Takatoshi Ito, a contender to replace Governor Haruhiko Kuroda in April

The PBOC injected a record monthly amount into state policy banks in November to help spur infrastructure spending and boost a struggling economy

Turkish inflation slowed for the first time in over a year-and-a-half, though measures to revive the economy ahead of elections in 2023 may keep it elevated for some time

A more detailed look at global markets courtesy of Newsquawk

Asia-Pacific stocks traded mostly positive as Chinese markets led the advances on reopening optimism after several large cities further loosened COVID-19 restrictions, although the gains for the rest of the region were limited after Friday’s mixed post-NFP performance on Wall St and a further deterioration in Chinese Caixin Services and Composite PMI data. ASX 200 was higher with the index supported by strength in mining and energy as underlying commodity prices benefitted from the China reopening play. Nikkei 225 was indecisive and just about kept afloat throughout the session with price action contained by a lack of pertinent drivers to propel the index closer to the 28,000 level. Hang Seng and Shanghai Comp shrugged off the weak Chinese PMI data with risk appetite supported by reopening hopes and as the PBoC’s previously announced RRR cut took effect, while developers were boosted after reports last week that China's top four banks intend to issue loans for domestic developers’ overseas debt repayments.

Top Asian News

Chinese Caixin Services PMI (Nov) 46.7 vs. Exp. 48.0 (Prev. 48.4); Composite PMI (Nov) 47.0 (Prev. 48.3)

Several Chinese cities accelerated the loosening of COVID-19 restrictions over the weekend including Shanghai and Shenzhen which scrapped requirements for commuters to present PCR tests for travelling on public transport, while apartment complexes in Beijing indicated that those that tested positive could quarantine at home, according to FT.

China could announce 10 supplementary COVID measures as soon as Wednesday, via Reuters citing sources; could downgrade COVID to category B management as early as January. Subsequently, Shanghai scraps COVID testing requirement at more public venues from Tuesday, according to Bloomberg.

PBoC is reportedly expected to reduce the amount of open market operations towards the end of the year to avoid excess liquidity, according to China Securities Journal.

Morgan Stanley upgraded MSCI China to overweight from equal weight and said the ROE is likely to rise to 11.1% by end-2023, according to Reuters.

European bourses are under modest pressure, Euro Stoxx 50 -0.2%, following on from fairly contained action in futures overnight. In APAC hours, Chinese stocks were the marked outpeformers given the loosening of COVID restrictions, though the region's PMIs slipped. Stateside, futures are are in-fitting with European peers and are under slight pressure, ES -0.3%, with specific developments light during the Fed blackout window. Tesla (TSLA) reduced Shanghai output by up to 20% due to sluggish demand, according to Bloomberg; output cuts set to take effect as soon as this week, sources state. Foxconn (2317 TT) November sales -11.4% YY. Q4 outlook expected in-line with consensus. November was the month most affected by COVID; due to off-peak seasonality and COVID November revenue declined MM.

Top European News

BoE’s Dhingra said higher interest rates could lead to a deeper and longer recession which is what she thinks they should all be worried about, while she sees few signs that demands for higher wages are raising the risk of a wage-price spiral, according to the Observer.

Confederation of British Industry warned the UK will fall into a year-long recession next year as a combination of rising inflation, negative growth and declining business investment weigh on the economy, according to FT.

UK Conservative Party Chairman and Minister without Portfolio in the Cabinet Office Zahawi said the government is looking at bringing in the military if strikes go ahead in various sectors including the health sector, according to Reuters and Sky News.

UK RMT union rejected the Rail Delivery Group offer and demanded a meeting on Monday to resolve the dispute, while UK Transport Secretary Harper said the situation is disappointing and unfair to the public, according to Reuters.

ECB’s Villeroy said that inflation should peak in H1 next year and that he favours a 50bps rate hike at the December 15th meeting, while he added that rate hikes will continue after that but cannot say when they will stop and he expects to beat inflation by 2024-2025, according to Reuters.

ECB's Makhlouf sees a 50bps increase at a minimum at the December (15th) meeting, expects the eventual magntude to be 50bp; have to be open to policy rates moving into restrictive territory for a period in 2023; pre-mature to be talking about the endpoint for rates

EU Commission President von der Leyen said the US Inflation Reduction Act is raising concerns in Europe and there is a risk it could lead to unfair competition, close markets and fragment supply chains that have already been tested by the pandemic, while she added that competition is good but it must be a level playing field and that they must take action to rebalance the playing field where the IRA or other measures conduct distortions, according to Reuters.

FX

DXY bid despite an earlier move to 104.10 lows, with the index recovering to 104.75+ parameters amid favourable technical levels US yields.

Action which has been felt most keenly against the JPY, USD/JPY testing 135.50 at best from an initial 134.10 low, action which has offset the Yuan's impact on the USD.

Yuan outperforms given the latest easing of COVID restrictions and source reports pointing to additional measures being forthcoming.

AUD the next-best ahead of the RBA policy announcement with a 25bp hike expected.

Both EUR and GBP were unreactive to the latest PMIs, with hefty OpEx in EUR/USD of note for the NY Cut; though, GBP has felt the USD's bid more keenly, sub-1.2250 at worst.

PBoC set USD/CNY mid-point at 7.0384 vs exp. 7.0368 (prev. 7.0542)

Fixed Income

Core benchmarks are experiencing choppy trade, but retain an underlying bid with Bunds surpassing touted 142.17 resistance and Gilts briefly breaching 106.00.

A move which leaves USTs lagging slightly with corresponding yields bid, though the curve is mixed and action is once again most pronounced at the short-end ahead of ISM & Factory Orders.

Commodities

Crude benchmarks have been choppy, but are ultimately firmer post-OPEC+ and as the Russian oil cap comes into effect at USD 60/bbl.

Currently, WTI Jan & Brent Fed are pivoting USD 81.50/bbl and USD 87/bbl respectively, with the latest easing of China's COVID controls also factoring.

OPEC+ ministers formally endorsed the output policy rollover and will hold the next JMMC meeting on February 1st, while it vowed to stand ready to adjust oil output to stabilise markets, according to Reuters and FT.

Iraqi Oil Minister said OPEC members are committed to the agreed production rates until the end of 2023 and the Algerian Energy Minister said the decision to keep output unchanged is appropriate to market fluctuations. Kuwaiti Oil Minister said OPEC+ decisions are based on market data and ensure its stability, while he added the impact of slow global economic growth on oil demand is a cause for continuous caution, according to Reuters.

G7 and Australia announced on Friday that a consensus was reached on a price cap for Russian seaborne oil at USD 60/bbl which will enter into force on December 5th or very soon thereafter and they will ‘grandfather’ any revision of the price cap to allow compliant transactions concluded beforehand. Furthermore, US Treasury Secretary Yellen said that the price cap will immediately cut into Russia’s most important source of revenue and preserve stable global energy supplies, while a senior Treasury official stated that the price cap will create an anchor for Russian oil and has already driven prices lower, according to Reuters.

Ukrainian President Zelensky’s chief of staff commented that the price cap on Russian oil should be capped to USD 30/bbl, according to Reuters.

Russian Deputy PM Novak said they will not operate under the oil price cap even if they have to cut production and the price cap may affect other countries as well, while he added that they are working on mechanisms to ban supplies which are capped.

Russia is analysing the price cap imposed by G7 and allies on its oil and made preparations for this, while it will not accept the oil price cap, according to state news agencies citing the Kremlin.

Russia's Kremlin, on price cap, said Russia is preparing a decision and will not recognise the price cap; price cap will destabilise global energy market but will not affect Russia's ability to sustain the military operation in Ukraine.

EU countries cut their gas demand by a quarter last month despite a fall in temperature which shows an effort in reducing the reliance on Russian energy, according to FT.

Moldova’s Deputy PM Spinu said they will not pay a 50% advance to Gasprom by December 20th for its December gas supplies, according to Reuters.

Spot gold has pulled back below USD 1800/oz and now resides in proximity to its 200-DMA at USD 1795/oz while base metals remain bid, but have eased from initial best levels.

Geopolitics

US Defense Secretary Austin accused Russia of deliberate cruelty in its war in Ukraine and that it was intentionally targeting civilians, according to Reuters.

US Director of National Intelligence Haines said they expect a reduced tempo in Ukraine fighting to continue in the coming months, while she added that Russia is not capable of indigenously producing munitions they are expending, according to Reuters.

US Indo-Pacific Commander Aquilino said it is in China’s strategy to encourage nations like North Korea to create problems for the US and he is not optimistic about China doing anything helpful to stabilise the Indo-Pacific region, according to Reuters.

N.Korea has fired around 130 artillery shots off its East & West Coast, via Yonhap; Subsequently, N. Korean military says the firing of artillery shells was a warning to S. Korean military action, via KCNA.

US Event Calendar

09:45: Nov. S&P Global US Composite PMI, est. 46.3, prior 46.3

09:45: Nov. S&P Global US Services PMI, est. 46.1, prior 46.1

10:00: Oct. Durable Goods Orders, est. 1.0%, prior 1.0%

Durables-Less Transportation, est. 0.5%, prior 0.5%

Cap Goods Ship Nondef Ex Air, prior 1.3%

Cap Goods Orders Nondef Ex Air, prior 0.7%

10:00: Oct. Factory Orders, est. 0.7%, prior 0.3%

Factory Orders Ex Trans, prior -0.1%

10:00: Nov. ISM Services Index, est. 53.3, prior 54.4

DB's Jim Reid concludes the overnight wrap

Although there is little question that I feel fully aware that someone has cut my back open with a knife within the last few days and sawed off some bone inside, I feel remarkably mobile and spritely. However, I'm trying not to appear too mobile as I've been signed off housework for a few weeks as I'm not supposed to bend, twist or lift. Don't waste a crisis as they say. I also resisted any urge to celebrate England waltzing into the last 8 of World Cup last night. Still plenty of time for it to go spectacularly wrong. No need to stress the back needlessly at this stage!

As the World Cup builds to the business end of the tournament, we welcome in a week with limited US data and one with the Fed now on their blackout period ahead of next week's FOMC. In fact, could it actually be quite a quiet week ahead? Famous last words in a year like this, but next week should be much more interesting than this week given that we also have US CPI and the ECB meeting to go alongside the Fed.

The data we do see in the US starts today with the ISM services index (DB forecast 53.9 vs 54.4 in October) and ends with PPI and the UoM consumer confidence number on Friday with the latest inflation expectations numbers included.

Elsewhere we’ll also get CPI and PPI from China (Friday), industrial production from Germany (Wednesday) and trade data from key economies.

While central bank speak will be sparse, Lagarde speaks today and for this week some attention will shift to Canada and Australia. The former meet on Wednesday and as a reminder, their last meeting's dovish tilt spurred a pivot trade in the US on the back of expectations the Fed would mimic the message. So this meeting may be a driver of sentiment more broadly. The consensus is split on Bloomberg between 25bps and 50bps which makes it interesting. The Reserve Bank of Australia will also decide on policy tomorrow, and consensus expects a 25bp rate hike that takes the cash rate to 3.1%. Wednesday will also likely see the Reserve Bank of India downshift to 25bps after three 50bps hikes. So by midweek we’ll have a better feel for whether these central banks are trying to downshift. The full day-by-day week ahead is at the end as usual on a Monday.

Staying on the topic of where central bank rates are going, payrolls from last Friday merit some closer attention. The headline (263k vs 284k last and 200k consensus) and private (221k vs. 248k last and 185k consensus) payrolls numbers beat with unemployment steady at 3.7%. However, market focus was squarely on the upside surprise to average hourly earnings (+0.6% vs. +0.5% last and +0.3% consensus) which boosted the year-over-year growth rate by a couple of tenths to 5.1% vs consensus at only 4.6%. This big upside miss got our economists digging into the data and they found that the response rate for the establishment survey, which measures nonfarm payrolls, hours and earnings, was just 49.4%, well below the normal 65-70% range and the lowest since 2002. So it feels like you could see decent sized revisions. In addition, our economists found that most of the upside surprise to AHEs was due to the transportation and warehouse sector, which showed a +2.5% monthly gain - over five standard deviations above the average and by far a record increase. Information services AHEs (+1.6% vs. Unch.) also showed an unusually large gain that was about 2.5 standard deviations outside of the average. Combined, the unusually large increases in these two sectors likely boosted overall AHEs by around one to two tenths in their view.

Nevertheless, income growth from our economists’ payroll proxy was still up 7.6% compared to a year ago and inflation is not going to be coming down to trend with labour markets like this. There is more and more evidence that the supply side is normalising on the inflation front but it's seems inconceivable that inflation can normalise overall when we see the type of employment numbers we saw last week, not just from the employment report but also from the JOLTS data which still pointed towards a tight labour market.

Indeed, in Powell's mid-week speech which caused a major bond/rates rally, he did cite the latest JOLTS data as still showing a large imbalance between supply and demand for labour, referencing the roughly 1.7 job openings for every unemployed worker. Powell also noted that for "the principal wage measures that we look at, I would say that you're one and half or two percent above that (which is consistent with two percent inflation over time)". So it's fascinating that at the moment the market is focusing squarely on the very strong likelihood that we'll ratchet down to 'only' a 50bps hike next week and extrapolating that level of dovishness rather than focus on any risks that the terminal rate could end up being nearer say 6% than 5%. Indeed Larry Summers was doing the rounds over the weekend suggesting that markets were likely under-pricing terminal and seemingly being more comfortable suggesting a peak nearer 6 than 5%, even if he wasn't specific over a particular number.

In terms of weekend news OPEC+ decided to keep production at current levels as expected. This follows the EU decision on Friday, after months of negotiations, to cap the price of Russian crude at $60 per barrel, starting today. This morning in Asia trading hours, oil prices are trading higher with Brent crude futures (+0.82%) trading at $86.27/bbl and WTI futures (+0.83%) at $80.64/bbl following China’s further easing of its Covid Curbs.

Elsewhere, Shanghai and Hangzhou have followed other Chinese cities in easing some Covid restrictions over the weekend. They announced that from tomorrow, they will remove the requirement to have a PCR test to enter outdoor public venues and to use public transport. Chinese equities surged on the news with the Hang Seng rising +3.3% in early trading to its highest since mid-September, leading gains across the region with the CSI (+1.60%) and the Shanghai Composite (+1.55%) also rallying. Outside of China, the Nikkei (+0.01%) is struggling to gain traction this morning whilst the KOSPI (-0.51%) is slipping back slightly. In overnight trading, US stock futures are indicating a negative start with contracts tied to S&P 500 (-0.14%) and the NASDAQ 100 (-0.17%) edging lower. Meanwhile, yields on 10yr USTs (+4.55 bps) have climbed higher, trading at 3.53% with the 2s10s curve at -79.15 bps as we go to press.

Data out from China today showed that services activity contracted further in November as Covid restrictions continued to restrain growth, with the Caixin China services PMI falling to a six-month low of 46.7 from 48.4 in October. Elsewhere, the final estimate of Japan’s services PMI fell to 50.3 from October's 53.2, hitting the lowest since August as cost pressures remained acute. The composite PMI contracted to 48.9 in November from 51.8 a month earlier.

In FX, the Chinese currency strengthened to 6.96 against the US dollar, moving below 7 for the first time since mid-September on hopes of reopening.

Recapping last week now and for the second week running major sovereign bond markets and equity indices rallied, after perceived dovishness from Fed Chair Powell in his last remarks before the December FOMC communications blackout period, troubling global growth data, and further confirmation of China moving on from the strictest form zero Covid policies that have plagued global supply chains.

Treasury and Bund yields fell over the week, a largely parallel shock to the already inverted US yield curve while Bund yields flattened slightly. All told, 2yr Treasuries fell -18.1bps (+4.4bps Friday) while 10yr yields were -19.1bps lower (-1.9bps Friday). 2yr Bunds fell -8.7bps, though climbed +8.0bps Friday, while 10yr yields were -11.8bps lower after climbing +4.2bps Friday following the US jobs report. But note that 10yr US yields fell c.7bps after the European close and c.15bps lower than their highs for the day just after payrolls were released.

Terminal Fed Funds fell c.8bps on the week but were first c.6bps higher pre-Powell's speech and then c.22bps lower into payrolls, before climbing 8bps after and into the close for the week.

A second straight week of falling discount rates led to a second straight week of decent equity performance. The S&P 500 climbed +1.13% (-0.12% Friday) with the more rate-sensitive NASDAQ outperforming, up +2.09% (-0.18% Friday). One area of weakness was bank stocks, where the S&P 500 banks sector fell -2.03% (-1.04% Friday) as slower growth and flatter curves weighed. Performance was more mixed in Europe, but the STOXX 600 still managed to post a +0.58% weekly gain (-0.15% Friday), while the regional indices took their cues from the World Cup: the DAX fell -0.08% (+0.27% Friday) with Germany failing to reach the knockout round again while the CAC and FTSE 100 increased +0.44% (-0.17% Friday) and +0.93% (-0.03% Friday), respectively.

Meet the Bitcoinetas, a fleet of transformative vehicles on a mission to spread the bitcoin message everywhere they go. From Argentina to South Africa,…

You may have seen that picture of Michael Saylor in a bitcoin-branded van, with a cheerful guy right next to the car door. This one:

Ariel Aguilar and La Bitcoineta European Edition at BTC Prague.

That car is the Bitcoineta European Edition, and the cheerful guy is Ariel Aguilar. Ariel is part of the European Bitcoineta team, and has previously driven another similar car in Argentina. In fact, there are currently five cars around the world that carry the name Bitcoineta (in some cases preceded with the Spanish definite article “La”).

Argentina: the original La Bitcoineta

The story of Bitcoinetas begins with the birth of 'La Bitcoineta' in Argentina, back in 2017. Inspired by the vibrancy of the South American Bitcoin community, the original Bitcoineta was conceived after an annual Latin American Conference (Labitconf), where the visionaries behind it recognized a unique opportunity to promote Bitcoin education in remote areas. Armed with a bright orange Bitcoin-themed exterior and a mission to bridge the gap in financial literacy, La Bitcoineta embarked on a journey to bring awareness of Bitcoin's potential benefits to villages and towns that often remained untouched by mainstream financial education initiatives. Operated by a team of dedicated volunteers, it was more than just a car; it was a symbol of hope and empowerment for those living on the fringes of financial inclusion.

The concept drawing for La Bitcoineta from December 2017.

Ariel was part of that initial Argentinian Bitcoineta team, and spent weeks on the road when the car became a reality. The original dream to bring bitcoin education even to remote areas within Argentina and other South American countries came true, and the La Bitcoineta team took part in dozens of local bitcoin meetups in the subsequent years.

The original La Bitcoineta from Argentina.

One major hiccup came in late 2018, when the car was crashed into while parked in Puerto Madryn. The car was pretty much destroyed, but since the team was possessed by a honey badger spirit, nothing could stop them from keeping true to their mission. It is a testament to the determination and resilience of the Argentinian team that the car was quickly restored and returned on its orange-pilling quest soon after.

Argentinian Bitcoineta after a major accident (no-one got hurt); the car was restored shortly after.

Over the more than 5 years that the Argentinian Bitcoineta has been running, it has traveled more than 80,000 kilometers - and as we’ll see further, it inspired multiple similar initiatives around the world.

In early 2021, the president of El Salvador passed the Bitcoin Law, making bitcoin legal tender in the country. The Labitconf team decided to celebrate this major step forward in bitcoin adoption by hosting the annual conference in San Salvador, the capital city of El Salvador. And correspondingly, the Argentinian Bitcoineta team made plans for a bold 7000-kilometer road trip to visit the Bitcoin country with the iconic Bitcoin car.

However, it proved to be impossible to cross so many borders separating Argentina and Salvador, since many governments were still imposing travel restrictions due to a Covid pandemic. So two weeks before the November event, the Labitconf team decided to fund a second Bitcoineta directly in El Salvador, as part of the Bitcoin Beach circular economy. Thus the second Bitcoineta was born.

Salvadoran’s Bitcoineta operates in the El Zonte region, where the Bitcoin Beach circular economy is located.

The eye-catching Volkswagen minibus has been donated to the Bitcoin Beach team, which uses the car for the needs of its circular economy based in El Zonte.

Late 2021 saw one other major development in terms of grassroots bitcoin adoption. On the other side of the planet, in South Africa, Hermann Vivier initiated the Bitcoin Ekasi project. “Ekasi” is a colloquial term for a township, and a township in the South African context is an underdeveloped urban area with a predominantly black population, a remnant of the segregationist apartheid regime. Bitcoin Ekasi emerged as an attempt to introduce bitcoin into the economy of the JCC Camp township located in Mossel Bay, and has gained a lot of success on that front.

Bitcoin Ekasi was in large part inspired by the success of the Bitcoin Beach circular economy back in El Salvador, and the respect was mutual. The Bitcoin Beach team thus decided to pass on the favor they received from the Argentinian Bitcoineta team, and provided funds to Bitcoin Ekasi for them to build a Bitcoineta of their own.

Bitcoin Ekasi’s Bitcoineta as seen at the Adopting Bitcoin Cape Town conference.Bitcoin Ekasi’s Bitcoineta as seen at the Adopting Bitcoin Cape Town conference. Hermann Vivier is seen in the background. South African Bitcoineta serves the needs of Bitcoin Ekasi, a local bitcoin circular economy in the JCC Camp township.

Bitcoin Ekasi emerged as a sister organization of Surfer Kids, a non-profit organization with a mission to empower marginalized youths through surfing. The Ekasi Bitcoineta thus partially serves as a means to get the kids to visit various surfer competitions in South Africa. A major highlight in this regard was when the kids got to meet Jordy Smith, one of the most successful South African surfers worldwide.

Coincidentally, South African surfers present an intriguing demographic for understanding Bitcoin due to their unique circumstances and needs. To make it as a professional surfer, the athletes need to attend competitions abroad; but since South Africa has tight currency controls in place, it is often a headache to send money abroad for travel and competition expenses. The borderless nature of Bitcoin offers a solution to these constraints, providing surfers with an alternative means of moving funds across borders without any obstacles.

Photo taken at the South African Junior Surfing Championships 2023. Back row, left to right:

Mbasa, Chuma, Jordy Smith, Sandiso. Front, left to right: Owethu, Sibulele.

To find out more about Bitcoineta South Africa and the non-profit endeavors it serves, watch Lekker Feeling, a documentary by Aubrey Strobel:

The European Bitcoineta started its journey in early 2023, with Ariel Aguilar being one of the main catalysts behind the idea. Unlike its predecessors in El Salvador and South Africa, the European Bitcoineta was not funded by a previous team but instead secured support from individual donors, reflecting a grassroots approach to spreading financial literacy.

European Bitcoineta sports a hard-to-overlook bitcoin logo along with the message “Bitcoin is Work. Bitcoin is Time. Bitcoin is Hope.”

The European Bitcoineta is a Mercedes box van adorned with a prominent Bitcoin logo and inspiring messages, and serves as a mobile hub for education and discussion at numerous European Bitcoin conferences and local meetups. Inside its spacious interior, both notable bitcoiners and bitcoin plebs share their insights on the walls, fostering a sense of camaraderie and collaboration.

Inside the European Bitcoineta, one can find the wall of fame, where visitors can read messages from prominent bitcoiners such as Michael Saylor, Uncle Rockstar, Javier Bastardo, Hodlonaut, and many others.On the “pleb wall”, any bitcoiner can share their message (as long as space permits).

Introduced in December 2023 at the Africa Bitcoin Conference in Ghana, the fifth Bitcoineta was donated to the Ghanaian Bitcoin Cowries educational initiative as part of the Trezor Academy program.

Bitcoineta West Africa was launched in December 2023 at the Africa Bitcoin Conference. Among its elements, it bears the motto of the Trezor Academy initiative: Bitcoin. Education. Freedom.

Bitcoineta West Africa was funded by the proceeds from the bitcoin-only limited edition Trezor device, which was sold out within one day of its launch at the Bitcoin Amsterdam conference.

With plans for an extensive tour spanning Ghana, Togo, Benin, Nigeria, and potentially other countries within the ECOWAS political and economic union, Bitcoineta West Africa embodies the spirit of collaboration and solidarity in driving Bitcoin adoption and financial inclusion throughout the Global South.

Bitcoineta West Africa surrounded by a group of enthusiastic bitcoiners at the Black Star Square, Accra, Ghana.

All the Bitcoineta cars around the world share one overarching mission: to empower their local communities through bitcoin education, and thus improve the lives of common people that might have a strong need for bitcoin without being currently aware of such need. As they continue to traverse borders and break down barriers, Bitcoinetas serve as a reminder of the power of grassroots initiatives and the importance of financial education in shaping a more inclusive future. The tradition of Bitcoinetas will continue to flourish, and in the years to come we will hopefully encounter a brazenly decorated bitcoin car everywhere we go.

If the inspiring stories of Bitcoinetas have ignited a passion within you to make a difference in your community, we encourage you to take action! Reach out to one of the existing Bitcoineta teams for guidance, support, and inspiration on how to start your own initiative. Whether you're interested in spreading Bitcoin education, promoting financial literacy, or fostering empowerment in underserved areas, the Bitcoineta community is here to help you every step of the way. Together, we will orange pill the world!

This is a guest post by Josef Tetek. Opinions expressed are entirely their own and do not necessarily reflect those of BTC Inc or Bitcoin Magazine.

Over the last few years, digital currencies and gold have become decent barometers of speculative investor appetite. Such isn’t surprising given the evolution…

Over the last few years, digital currencies and gold have become decent barometers of speculative investor appetite. Such isn’t surprising given the evolution of the market into a “casino” following the pandemic, where retail traders have increased their speculative appetites.

“Such is unsurprising, given that retail investors often fall victim to the psychological behavior of the “fear of missing out.” The chart below shows the “dumb money index” versus the S&P 500. Once again, retail investors are very long equities relative to the institutional players ascribed to being the “smart money.””

“The difference between “smart” and “dumb money” investors shows that, more often than not, the “dumb money” invests near market tops and sells near market bottoms.”

That enthusiasm has increased sharply since last November as stocks surged in hopes that the Federal Reserve would cut interest rates. As noted by Sentiment Trader:

“Over the past 18 weeks, the straight-up rally has moved us to an interesting juncture in the Sentiment Cycle. For the past few weeks, the S&P 500 has demonstrated a high positive correlation to the ‘Enthusiasm’ part of the cycle and a highly negative correlation to the ‘Panic’ phase.”

That frenzy to chase the markets, driven by the psychological bias of the “fear of missing out,” has permeated the entirety of the market. As noted in “This Is Nuts:”

“Since then, the entire market has surged higher following last week’s earnings report from Nvidia (NVDA). The reason I say “this is nuts” is the assumption that all companies were going to grow earnings and revenue at Nvidia’s rate. There is little doubt about Nvidia’s earnings and revenue growth rates. However, to maintain that growth pace indefinitely, particularly at 32x price-to-sales, means others like AMD and Intel must lose market share.”

Of course, it is not just a speculative frenzy in the markets for stocks, specifically anything related to “artificial intelligence,” but that exuberance has spilled over into gold and cryptocurrencies.

Birds Of A Feather

There are a couple of ways to measure exuberance in the assets. While sentiment measures examine the broad market, technical indicators can reflect exuberance on individual asset levels. However, before we get to our charts, we need a brief explanation of statistics, specifically, standard deviation.

“Like a rubber band that has been stretched too far – it must be relaxed in order to be stretched again. This is exactly the same for stock prices that are anchored to their moving averages. Trends that get overextended in one direction, or another, always return to their long-term average. Even during a strong uptrend or strong downtrend, prices often move back (revert) to a long-term moving average.”

The idea of “stretching the rubber band” can be measured in several ways, but I will limit our discussion this week to Standard Deviation and measuring deviation with “Bollinger Bands.”

“Standard Deviation” is defined as:

“A measure of the dispersion of a set of data from its mean. The more spread apart the data, the higher the deviation. Standard deviation is calculated as the square root of the variance.”

In plain English,this meansthat the further away from the average that an event occurs, the more unlikely it becomes. As shown below, out of 1000 occurrences, only three will fall outside the area of 3 standard deviations. 95.4% of the time, events will occur within two standard deviations.

A second measure of “exuberance” is “relative strength.”

“In technical analysis, the relative strength index (RSI) is a momentum indicator that measures the magnitude of recent price changes to evaluate overbought or oversold conditions in the price of a stock or other asset. The RSI is displayed as an oscillator (a line graph that moves between two extremes) and can read from 0 to 100.

Traditional interpretation and usage of the RSI are that values of 70 or above indicate that a security is becoming overbought or overvalued and may be primed for a trend reversal or corrective pullback in price. An RSI reading of 30 or below indicates an oversold or undervalued condition.” – Investopedia

With those two measures, let’s look at Nvidia (NVDA), the poster child of speculative momentum trading in the markets. Nvidia trades more than 3 standard deviations above its moving average, and its RSI is 81. The last time this occurred was in July of 2023 when Nvidia consolidated and corrected prices through November.

Interestingly, gold also trades well into 3 standard deviation territory with an RSI reading of 75. Given that gold is supposed to be a “safe haven” or “risk off” asset, it is instead getting swept up in the current market exuberance.

The same is seen with digital currencies. Given the recent approval of spot, Bitcoin exchange-traded funds (ETFs), the panic bid to buy Bitcoin has pushed the price well into 3 standard deviation territory with an RSI of 73.

In other words, the stock market frenzy to “buy anything that is going up” has spread from just a handful of stocks related to artificial intelligence to gold and digital currencies.

It’s All Relative

We can see the correlation between stock market exuberance and gold and digital currency, which has risen since 2015 but accelerated following the post-pandemic, stimulus-fueled market frenzy. Since the market, gold and cryptocurrencies, or Bitcoin for our purposes, have disparate prices, we have rebased the performance to 100 in 2015.

Gold was supposed to be an inflation hedge. Yet, in 2022, gold prices fell as the market declined and inflation surged to 9%. However, as inflation has fallen and the stock market surged, so has gold. Notably, since 2015, gold and the market have moved in a more correlated pattern, which has reduced the hedging effect of gold in portfolios. In other words, during the subsequent market decline, gold will likely track stocks lower, failing to provide its “wealth preservation” status for investors.

The same goes for cryptocurrencies. Bitcoin is substantially more volatile than gold and tends to ebb and flow with the overall market. As sentiment surges in the S&P 500, Bitcoin and other cryptocurrencies follow suit as speculative appetites increase. Unfortunately, for individuals once again piling into Bitcoin to chase rising prices, if, or when, the market corrects, the decline in cryptocurrencies will likely substantially outpace the decline in market-based equities. This is particularly the case as Wall Street can now short the spot-Bitcoin ETFs, creating additional selling pressure on Bitcoin.

Just for added measure, here is Bitcoin versus gold.

Not A Recommendation

There are many narratives surrounding the markets, digital currency, and gold. However, in today’s market, more than in previous years, all assets are getting swept up into the investor-feeding frenzy.

Sure, this time could be different. I am only making an observation and not an investment recommendation.

However, from a portfolio management perspective, it will likely pay to remain attentive to the correlated risk between asset classes. If some event causes a reversal in bullish exuberance, cash and bonds may be the only place to hide.

BUFFALO, NY- March 11, 2024 – Impact Journals publishes scholarly journals in the biomedical sciences with a focus on all areas of cancer and aging research. Aging is one of the most prominent journals published by Impact Journals.

Credit: Impact Journals

BUFFALO, NY- March 11, 2024 – Impact Journals publishes scholarly journals in the biomedical sciences with a focus on all areas of cancer and aging research. Aging is one of the most prominent journals published by Impact Journals.

Impact Journals will be participating as an exhibitor at the American Association for Cancer Research (AACR) Annual Meeting 2024 from April 5-10 at the San Diego Convention Center in San Diego, California. This year, the AACR meeting theme is “Inspiring Science • Fueling Progress • Revolutionizing Care.”

Visit booth #4159 at the AACR Annual Meeting 2024 to connect with members of the Agingteam.

About Aging-US:

Agingpublishes research papers in all fields of aging research including but not limited, aging from yeast to mammals, cellular senescence, age-related diseases such as cancer and Alzheimer’s diseases and their prevention and treatment, anti-aging strategies and drug development and especially the role of signal transduction pathways such as mTOR in aging and potential approaches to modulate these signaling pathways to extend lifespan. The journal aims to promote treatment of age-related diseases by slowing down aging, validation of anti-aging drugs by treating age-related diseases, prevention of cancer by inhibiting aging. Cancer and COVID-19 are age-related diseases.

Agingis indexed and archived byPubMed/Medline (abbreviated as “Aging (Albany NY)”), PubMed Central, Web of Science: Science Citation Index Expanded (abbreviated as “Aging‐US” and listed in the Cell Biology and Geriatrics & Gerontology categories), Scopus (abbreviated as “Aging” and listed in the Cell Biology and Aging categories), Biological Abstracts, BIOSIS Previews, EMBASE, META (Chan Zuckerberg Initiative) (2018-2022), and Dimensions (Digital Science).

Please visit our website at www.Aging-US.com and connect with us:

We use cookies on our website to give you the most relevant experience by remembering your preferences and repeat visits. By clicking “Accept”, you consent to the use of ALL the cookies.

This website uses cookies to improve your experience while you navigate through the website. Out of these, the cookies that are categorized as necessary are stored on your browser as they are essential for the working of basic functionalities of the website. We also use third-party cookies that help us analyze and understand how you use this website. These cookies will be stored in your browser only with your consent. You also have the option to opt-out of these cookies. But opting out of some of these cookies may affect your browsing experience.

Necessary cookies are absolutely essential for the website to function properly. These cookies ensure basic functionalities and security features of the website, anonymously.

Cookie

Duration

Description

cookielawinfo-checbox-analytics

11 months

This cookie is set by GDPR Cookie Consent plugin. The cookie is used to store the user consent for the cookies in the category "Analytics".

cookielawinfo-checbox-functional

11 months

The cookie is set by GDPR cookie consent to record the user consent for the cookies in the category "Functional".

cookielawinfo-checbox-others

11 months

This cookie is set by GDPR Cookie Consent plugin. The cookie is used to store the user consent for the cookies in the category "Other.

cookielawinfo-checkbox-necessary

11 months

This cookie is set by GDPR Cookie Consent plugin. The cookies is used to store the user consent for the cookies in the category "Necessary".

cookielawinfo-checkbox-performance

11 months

This cookie is set by GDPR Cookie Consent plugin. The cookie is used to store the user consent for the cookies in the category "Performance".

viewed_cookie_policy

11 months

The cookie is set by the GDPR Cookie Consent plugin and is used to store whether or not user has consented to the use of cookies. It does not store any personal data.

Functional cookies help to perform certain functionalities like sharing the content of the website on social media platforms, collect feedbacks, and other third-party features.

Performance cookies are used to understand and analyze the key performance indexes of the website which helps in delivering a better user experience for the visitors.

Analytical cookies are used to understand how visitors interact with the website. These cookies help provide information on metrics the number of visitors, bounce rate, traffic source, etc.

Advertisement cookies are used to provide visitors with relevant ads and marketing campaigns. These cookies track visitors across websites and collect information to provide customized ads.

{kind=link}

{kind=link}