US Equity Futures Reverse Overnight Decline, Turn Positive As Oil Surges

US Equity Futures Reverse Overnight Decline, Turn Positive As Oil Surges

U.S. equity futures and European bourses stocks reversed modest…

Share this:

U.S. equity futures and European bourses stocks reversed modest overnight losses and turned higher as US traders got to their desks on Monday as crude oil extended a climb and investors monitored diplomatic efforts to bring an end to Russia’s almost month-old war in Ukraine. S&P futures rose 0.07% or 3 points after earlier sliding almost 30 points; Nasdaq futures were flat.

Focus on Monday will be on a speech by Fed Chair Jerome Powell after the central bank kicked off a rate-hiking cycle last week. Powell is set to speak at the annual meeting of the National Association for Business Economics at 12pm ET; text release and Q&A are expected.

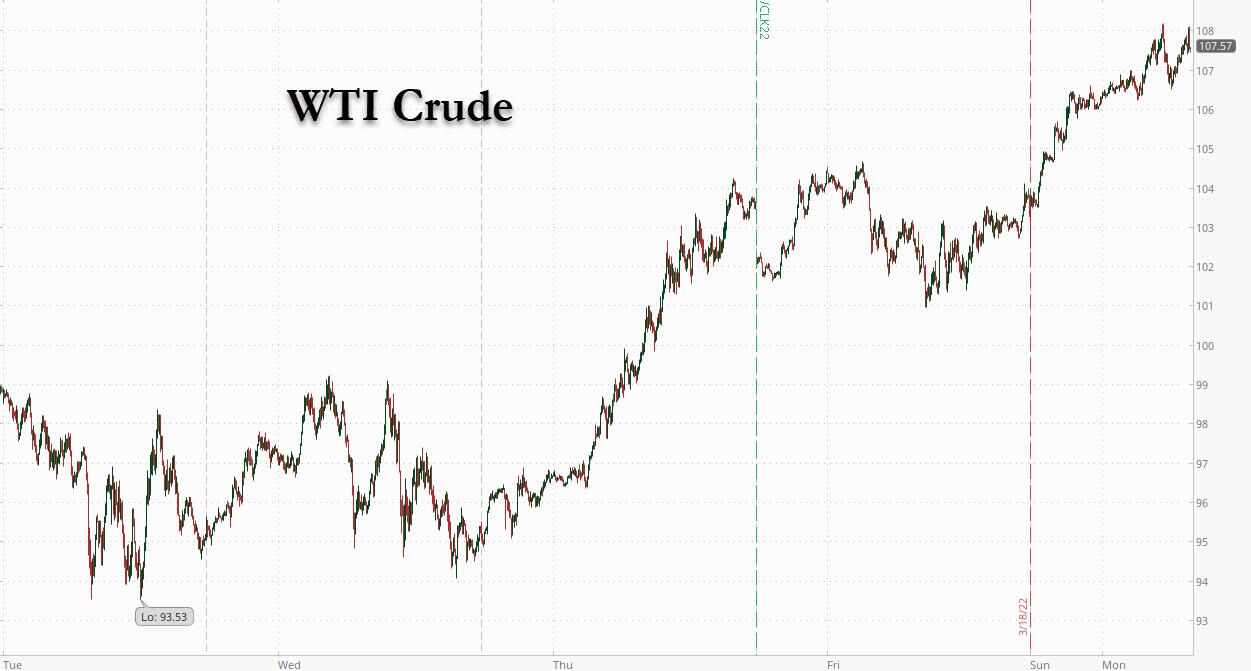

In addition to concerns about Russian crude supply, which Russia's deputy prime minister Novak said could surge to $300/bbl if Russian oil is shunned, also jumped after Saudi Arabia announced a “temporary reduction” in oil output at an Aramco facility after Yemen’s Houthi rebels launched multiple cross-border attacks on Sunday .A drone assault on the YASREF refinery, in the Yanbu Industrial City on the Red Sea, has “led to a temporary reduction in the refinery’s production, which will be compensated for from the inventory,” the energy ministry said in a statement. WTI rose as high as $108, surging $15 from prices hit last Tuesday, with Brent trading around $113.

The S&P 500 last week had its biggest gain since November 2020 and European equities recouped all of their losses triggered by Russia’s invasion of Ukraine nearly a month ago as peace negotiations and the lure of cheap valuations drew investors back. But that optimism may not be justified, given the “increasingly brutal measures that Russian forces are taking,” according to Michael Hewson, chief analyst at CMC Markets in London. “There appears to be a growing disconnect between what markets are doing and what is happening on the ground in Ukraine,” he said in a report. “Commodity markets continue to chop wildly” and “concerns about inflation are still posing awkward questions for central banks,” Hewson wrote.

A key question is whether last week’s stock rebound and drop in volatility are durable. European equities have recouped all of their losses triggered by Russia’s invasion of Ukraine nearly a month ago as optimism around peace negotiations and the lure of cheapened valuations draw investors back. But a historic spike in commodity prices on supply concerns shows little sign of easing, keeping traders on high alert over inflation and shaking their faith in the Federal Reserve to douse price pressures while keeping the economic recovery on track.

“The Fed comes out last week and basically tells you they have to do more -- into higher inflation but slowing growth,” Brian Weinstein, head of global fixed income at Morgan Stanley Investment Management, said in an interview with Bloomberg TV. “It certainly looks like the market is afraid of a traditional Fed goes too much, slows the economy down, and we don’t get the much-anticipated soft landing.”

In premarket trading, Boeing stock tumbled 6.6% after a China Eastern Airlines Boeing 737-800NG (yes, THE 737 MAX) plane carrying 132 people crashed in southwestern China.

Additionally, US-listed Chinese stocks slumped in premarket trading Monday, following their Asian peers lower, as investors were disappointed after Chinese banks left the loan prime rate unchanged despite expectations of some easing. Large-cap technology stocks are leading the decline including Alibaba -5.6%, JD.com -6%, NetEase -5.7%, Pinduoduo -5.6% and Baidu -3.4%. Among other China stocks listed in the U.S. that are lower this morning: Nio -2%, Li Auto -4.2%, XPeng -4.3%, Didi -5.9%, KE Holdings -6.4%, Lufax -3.2%, Trip.com -6.2%, Bilibili -7.6% and Tencent Music -7.5%. Other notable premarket movers:

- Anaplan (PLAN US) shares jump 27% in U.S. premarket after Thoma Bravo agreed to acquire U.S. enterprise software company in a deal valued at $10.7 billion, adding to a string of deals this year by cash-rich private equity firms.

- Nielsen Holdings (NLSN US) shares decline in U.S. premarket after it rejected an acquisition proposal from a private equity consortium, valuing the company at $25.40/share, a price that doesn’t “adequately compensate shareholders for Nielsen’s growth prospects.”

- Uber (UBER US) shares are slightly lower in U.S. premarket trading after price target is lowered at RBC Capital Markets, with broker less positive on the ride-hailing giant versus peer Lyft following proprietary driver supply analysis.

- Alleghany Corp. (Y US) shares could be active as Berkshire Hathaway Inc. is buying it for $11.6 billion in cash.

In the latest developments, Ukraine rejected a Russian demand that its forces lay down their arms Monday and leave the besieged southern port of Mariupol, which has been under intense Russian bombardment. Morgan Stanley’s chief U.S. equity strategist Michael Wilson said the recent rebound in U.S. stocks is an opportunity to sell and position more defensively. Meanwhile, U.S. President Joe Biden will speak with European leaders ahead of his trip to the continent this week. Senior U.S. officials will also meet with executives of Exxon Mobil Corp., JPMorgan Chase & Co. and other firms about the impact of the invasion and sanctions.

European equities had a subdued start to the week with most indexes opening flat. Euro Stoxx 50 and DAX rise slightly, while the FTSE MIB outperformed gaining 0.7%. Energy and mining stocks lead gains, tech and travel are in the red. Commodity-linked stocks are the biggest gainers on the Stoxx Europe 600 as prices rally with the war in Ukraine nearing the end of its first month with no conclusion in sight. The basic resources sub-index rises 1.8% as the energy sub-index gains 1.5%. Rio Tinto, Glencore and Anglo American are among the miners rising while Shell, BP and Equinor lead gains among energy stocks. Meanwhile, Europe’s formerly “unstoppable” luxury stocks are facing a swath of new challenges, from rising rates, war in Ukraine and China risks, leaving investors and analysts divided on whether valuations have fallen far enough yet. The MSCI Europe Textiles Apparel & Luxury Goods Index is down 14% this year, following three years of outsized gains. Hermes, the maker of $10,000 Birkin bags, is among top decliners, down 21% after a whopping 75% jump last year. Louis Vuitton owner LVMH, meanwhile, recently lost its crown as Europe’s biggest company to food giant Nestle. Investors were already dumping pricey luxury stocks in favor of cheaper shares amid concerns about rate hikes, while the war in Ukraine added further uncertainty. Valuation-wise, the group now trades at about a 60% premium to the broader market, near pre-pandemic levels and below its 5-year average.

Asia stocks fell after China’s lenders kept borrowing costs unchanged. The MSCI Asia Pacific Index was down 0.5% as of 3:13 p.m. in Singapore, erasing an earlier gain of 0.4%, weighed by declines in financials and communication services. The regional benchmark’s bumpy day followed its best week since February 2021. “Some may have clung to expectations for an LPR cut today, which I think will come later when they assess the growth drag from the outbreak,” said Wai Ho Leong, strategist at Modular Asset Management. “Peace talks and the Xi-Biden call also did not deliver substantive outcomes.” Stocks climbed last week as China pledged to stabilize its markets, and some traders had expected some help from banks’ loan prime rate announcement Monday. Talks between Xi Jinping and Joe Biden held Friday also failed to excite investors, although China’s top envoy to Washington pledged his country “will do everything” to de-escalate the war in Ukraine. Hong Kong Lifts Overseas Flight Ban; Cuts Hotel Quarantine Shares slid in China and Hong Kong, erasing earlier gains. Stocks in South Korea and Malaysia led declines in the region. Japanese markets were closed for a holiday.

India’s stocks took a breather on Monday after a sharp rally last week, as a drop in financial and consumer goods companies weighed on the indexes. The S&P BSE Sensex fell 1% to 57,292.49 in Mumbai, while the NSE Nifty 50 Index dropped by an equal measure. The gauges posted their biggest single-day drop since March 15. All but three of the 19 sector sub-indexes compiled by BSE Ltd fell, led by a gauge of utility companies. “Slowing rural sector is a risk even as urban consumption is showing signs of relatively better performance,” according to JM Financial analyst Dhananjay Sinha. Lower than expected growth and higher inflation are a key risk to Indian companies’ profitability, he added. Metal stocks were among gainers as Vedanta, Hindalco Industries and Coal India rose on the back of rising prices and worsening demand-supply scenario. ICICI Bank contributed the most to Sensex’s decline, decreasing 1.3%. Out of 30 shares in the Sensex, 25 fell, while 5 declined.

In FX, most FX majors are range-bound, as the DXY hovers on 98.000 handle awaiting speeches from Fed’s Bostic and chair Powell. Loonie underpinned by strong oil prices -Usd/Cad straddling 1.2600. Franc firm ahead of SNB policy assessment as Swiss sight deposits suggest less intervention; USD/CHF near 0.9300 and EUR/CHF sub-1.0300. Euro straddles 1.1050 with hawkish ECB commentary supportive, but hefty option expiries capping the upside (almost 2.8bln at 1.1100) Aussie unwinding recent gains on technical grounds and in wake of defeat for PM Morrison’s liberal party in local election - Aud/Usd back below 0.7400. Sterling still smarting after last week’s dovish BoE hike - Cable around 1.3150 and Eur/Gbp probing 100 DMA at 0.8415.

In rates, Treasuries followed wider losses across gilts while front-end leads the move lower, flattening the curve. 2Y-5Y yields cheaper by ~4bp, flattening 5s30s spread by ~3bp; 10-year yields around 2.18%, higher by ~2bp vs ~4bp for U.K. 10- year. Bunds and gilts bear steepen, cheapening roughly 3bps across the back end. Cash USTs open bear flatter with short dated yields up close to 5bps. Peripheral spreads are slightly wider to core.

In commodities, crude futures extend Asia’s gains; WTI adds ~4% to trade just shy of a 109-handle. Spot gold trades a narrow range in small positive territory near $1,924/oz. Base metals are mixed; LME nickel trades limit down for the fourth straight session. LME aluminum gains 3.8%, trading just off the late-Asia highs after Australia, the world’s biggest exporter of alumina, announced a ban on shipments to Russia.

Bitcoin is modestly pressured but contained within last week's parameters overall, holding above USD 41k.

Today's calendar is relatively quiet, with just the Chicago Fed National Activity Index on dex (exp 0.5, down from 0.69). Powell speaks at NABE at 12pm although it is unlikely he will make any monetary policy comments.

Market Snapshot

- S&P 500 futures up 0.1% to 4,448.75

- STOXX Europe 600 little changed at 455.00

- MXAP down 0.5% to 177.54

- MXAPJ down 0.7% to 579.14

- Nikkei up 0.7% to 26,827.43

- Topix up 0.5% to 1,909.27

- Hang Seng Index down 0.9% to 21,221.34

- Shanghai Composite little changed at 3,253.69

- Sensex down 0.8% to 57,428.60

- Australia S&P/ASX 200 down 0.2% to 7,278.55

- Kospi down 0.8% to 2,686.05

- Brent Futures up 3.8% to $112.03/bbl

- Gold spot up 0.2% to $1,924.77

- U.S. Dollar Index little changed at 98.27

- German 10Y yield little changed at 0.39%

- Euro little changed at $1.1048

- Brent Futures up 3.8% to $112.03/bbl

Top Overnight News from Bloomberg

- Ukraine rejected a Russian demand to surrender of the embattled southern port city of Mariupol, and an aide to President Volodymyr Zelenskiy said Russian forces are using “more destructive artillery.” More talks on ending the war are expected on Monday after Turkey said the two sides had made progress on key points

- Chinese banks left borrowing costs unchanged in line with expectations as the focus shifts to other possible easing measures from the central bank after top leaders pledged to boost the economy

- European Central Bank Vice President Luis de Guindos has yet to see any indication that soaring inflation rates are leading to higher wage demands, according to an interview with Handelsblatt

- Oil rose for a third day as the war in Ukraine neared the end of its first month with no end in sight, and Iranian-backed rebels attacked energy facilities in key exporter Saudi Arabia

- Hong Kong will lift a ban on flights from nine countries including the U.S. as of April 1, and cut the time incoming travelers need to spend in hotel quarantine in half provided they test negative, Chief Executive Carrie Lam said

- China and Russia’s trade relationship has become more complicated since the war started more than three weeks ago, raising questions about the future flow of energy, metals and crops between the two powerhouses

A more detailed look at global markets courtesy of Newsquawk

Asia-Pac stocks were choppy with sentiment clouded amid the uncertain geopolitical climate and higher oil prices. ASX 200 was indecisive as outperformance in tech was offset by losses in financials and with PM Morrison’s Liberal Party defeated in South Australia's state election, raising concerns for the government ahead of the federal election in two months Nikkei 225 was closed for the Vernal Equinox holiday. Hang Seng and Shanghai Comp. swung between gains and losses with an early surge in Hong Kong tech stocks ahead of a widely speculated relaxation to COVID restrictions after the city’s daily cases fell to a threeweek low and with China’s tech hub of Shenzhen resuming normal work output. However, the gains were wiped out with the mainland hampered as Shanghai tussles with a COVID-19 outbreak, while the PBoC also kept its Loan Prime Rates unchanged, as expected.

Top Asian News

- Indonesia Ends Quarantine Requirement for Overseas Travelers

- Asia Stocks Edge Down as Concerns Linger on China Policy Support

- Russia’s War Lifts Default Risk for Distressed Economies

- China Confirms Ambassador Met With Russian Defense Official

European bourses are contained and haven't differed too far from the unchanged mark overall, Euro Stoxx 50 +0.1%, as we await updates on Russia-Ukraine. Developments throughout the morning have been limited, and commentary from the Kremlin is predominantly infitting with last-week's/weekend updates. US futures are pressured, ES -0.2%, awaiting geopolitical catalysts with Fed speak, including Chair Powell, ahead. China Eastern airlines passenger jet flying from Kunming to Guangzhou on Monday experienced an accident in Guangxi, via State Media; unknown injuries/deaths from the accident. Craft was a Boeing (BA) 737 . Subsequently, China's Aviation Regulator confirms the crash of the China Eastern airlines passenger jet carrying 132 people. Boeing -8.3% in the pre-market Berkshire Hathaway (BRK/B) is to purchase Alleghany Corp (Y) for USD 848.02/shr (vs. close USD 676.75 /shr) in a USD 11.6bln transaction.

Top European News

- ECB’s Lagarde Says She’s Not Seeing Elements of Stagflation Now

- LSE Group to Sell BETA+ to Motive Partners, Clearlake: Sky

- S&T CEO’s Grosso Tech to Offer EU15.30/Shr for ~5.5m S&T Shares

- Julius Baer Says Sanctioned Clients in ‘Low Single Digits’

In FX, DXY hovers on 98.000 handle awaiting speeches from Fed’s Bostic and chair Powell. Loonie underpinned by strong oil prices -Usd/Cad straddling 1.2600. Franc firm ahead of SNB policy assessment as Swiss sight deposits suggest less intervention; USD/CHF near 0.9300 and EUR/CHF sub-1.0300. Euro straddles 1.1050 with hawkish ECB commentary supportive, but hefty option expiries capping the upside (almost 2.8bln at 1.1100) Aussie unwinding recent gains on technical grounds and in wake of defeat for PM Morrison’s liberal party in local election - Aud/Usd back below 0.7400. Sterling still smarting after last week’s dovish BoE hike - Cable around 1.3150 and Eur/Gbp probing 100 DMA at 0.8415.

In commodities, WTI and Brent have been dipping from best-levels, but remain underpinned on the session amid weekend geopolitical premia.; albeit, the European morning's developments have been more limited. WTI May resides around USD 107/bbl (vs high ~108.20/bbl) while its Brent counterpart trades just under USD 112 /bbl (vs high ~112.75/bbl). Saudi-led coalition reported that Yemen Houthis targeted a gas station in Khamis Mushait on Saturday which resulted in material damage to civilian cars and homes but no casualties, according to the state news agency. Saudi-led coalition also said it destroyed an explosive-laden boat to thwart an attack on shipping in the Red Sea, while it was also reported that Aramco’s petroleum products distribution plant in Jeddah was attacked and production at a Saudi oil refinery in Yanbu declined momentarily after an attack by Houthis. Saudi Aramco reported FY net income USD 110.0bln vs prev. USD 49.0bln Y/Y, while the CEO expects oil demand to return to pre-pandemic levels by year-end and said they are seeing healthy demand especially in Asia. Saudi Aramco's CEO also noted that there is limited spare capacity which is declining every month with global spare capacity around 2mln bpd and that the market is very tight in terms of available barrels.

US Event Calendar and Central Bank speakers

- 8am: Fed’s Bostic Gives Speech at NABE Conference

- 8:30am: Feb. Chicago Fed Nat Activity Index, est. 0.50, prior 0.69

- 12pm: Fed Chair Powell speaks at NABE

DB's Jim Reid concludes the overnight wrap

After a few weekends with some dramatic news of late, this weekend was relatively sparse in terms of new incremental news flow. The conflict and negotiations continue but without any major developments. Last week was the best for US and European equities since November 2020’s US election week; so markets are coming to terms with the current state of the conflict.

Over the weekend, Ukrainian officials rejected an offer given by the Russian military for its forces and civilians to surrender the city of Mariupol as shelling continued in Kyiv. Separately, the White House announced that President Joe Biden will travel to Poland in his upcoming trip to Europe for urgent talks with NATO and European allies. Mr. Biden is also hosting a call with his counterparts in the UK, Germany and Italy today at 11am UK time.

Overnight, Turkey’s Foreign Minister Mevlut Cavusoglu indicated that Ukraine and Russia are close to an agreement following progress in peace talks and is hopeful for a ceasefire if both the sides do not backtrack from their current positions. However there is no other developments on the current state of negotiations.

Asian equity markets have started the week on a weaker footing with the Hang Seng (-0.69%), reversing its early morning gains after it rose more than 1%. Mainland Chinese stocks are also dipping as I type with the CSI (-0.66%) and Shanghai Composite (-0.10%) lower after the PBOC kept the one-year loan prime rate unchanged at 3.7%. Elsewhere, markets in Japan are closed for a holiday. Moving on, stock futures in the DMs are also falling, as contracts on the S&P 500 (-0.42%), Nasdaq (-0.60%) and DAX (-0.58%) are all down.

Oil prices are up this morning with Brent futures advancing +3.08% to $111.25/bbl while WTI futures are up +3.23% at $108.08/bbl, as I type. Elsewhere, today's holiday in Japan means no USTs trading in Asia.

One of the key events this week will be Thursday’s March flash PMIs from around the world where we’ll see the first impact of the Russia/Ukraine conflict on activity, especially in Europe.

Outside of that, UK CPI data on Wednesday is going to be very interesting after the BoE warned on both growth and inflation last week in their surprisingly dovish hike. See our UK economist’s review here. There is also the Spring UK (Budget) Statement on Wednesday (preview here) where all things fiscal will be in focus.

Wednesday's new home sales, Friday's pending home sales and Thursday's durable goods are the main economic releases in the US.

There's plenty of Fed speak to sharpen up the message from last week's FOMC but don't expect a chorus line singing from the same song sheet. The dot plot showed the range of YE '22 Fed funds rates, as forecast by the committee, was a historically wide 1.4% to 3.1%. Boston (non-voter hawk) and Chair Powell himself are up today with the latter also on the docket on Wednesday. Williams (dove) will be on a panel tomorrow but also gives a speech on Friday. Daly (non-voter / dove) speaks tomorrow, Wednesday and Friday. Mester (voter / hawk) speaks tomorrow. Bullard (voter / hawk) is up on Wednesday and remember he was the lone 50bps dissenter last week. Kashkari (non-voter / dove), Governor Waller (hawk) and Chicago President Evans (non-voter / dove) speak on Thursday. Barkin (non-voter / hawk) concludes the Fed's business for the week on Friday.

Looking back at last week now and the conflict raged on but peace negotiations between Ukraine and Russia continued, with the headlines presenting a staccato back and forth about Ukrainian and Russian leaders’ current perceptions of the negotiation outlook. Markets seemed to look through this back-and-forth and took solace that negotiations were even happening, which was a material step up from where we were but a short time ago. In particular, both sides reported common ground on Ukraine’s neutral status and lack of NATO membership as a positive.

Another positive came on Friday after Presidents Biden and Xi Jinping spoke. China’s support for Russia remained a key unknown, but following the call both sides expressed aspirations for a peaceful resolution to the conflict, and for tensions to not escalate any further. Ahead of the meeting, US diplomatic officials warned that the US would impose costs on China were it to support the Russian invasion.

Russian sovereign bond payments made their way to creditors via custodians, despite some uncertainty, avoiding a default. Nevertheless, S&P cut the rating on Russian sovereign debt another notch, considering it at high risk of default. However, Russia’s remaining interest repayments this month will keep investors anxious as a $447 million payment is due on March 31, followed by a $2 billion payment as a bond comes due on April 4.

Dragging on sentiment were American intelligence reports that President Putin was prepared to re-engage in nuclear sabre rattling should the conflict drag on. That drove futures lower at the time of release but was not enough to drag risk negative on the week.

That said it was a good week for risk with the S&P 500 and STOXX 600 gaining +6.16% (+1.17% Friday) and +5.43% (+0.91% Friday) over the week, respectively. That marked the best weekly performance for both indices since the week of the US Presidential election in November 2020. Financials and mega cap tech stocks performed even better. The S&P and STOXX bank indices gained +6.60% (-0.15% Friday) and +8.72% (+0.22% Friday), respectively, while the FANG+ gained +13.61% (+3.37%). That was the best weekly performance ever for the FANG+, which also put in its best daily performance ever on Wednesday following the Fed meeting, and more positive Chinese state support news (the index contains Baidu and Alibaba), gaining +10.19%.

Speaking of the Fed, after two years at the zero lower bound, the FOMC raised policy rates by 25 basis points, with the dots projecting an additional 150 basis points of tightening this year, in line with DB expectations. Further, the Fed’s projections put policy into an explicitly restrictive stance by 2023. Despite the tightening, Chair Powell did not place particularly high risks on a recession occurring in the next year, which was apparently enough to help equities, with the S&P gaining +2.24% the day of the meeting in addition to the gangbusters day for the FANG+ index.

The Fed also announced plans to start reducing their bond holdings at a coming meeting. Chair Powell noted the asset holding reductions would roughly equate to an additional 25 basis points of tightening this year and could commence as early as the FOMC’s next meeting in May.

Money markets ended the week pricing around 167 basis points of additional policy rate tightening, suggesting some probability of a 50 basis point hike this year, which the Chair did not rule out. 10yr Treasury yields gained +15.8bps (-2.1bps Friday) on the week, driven entirely by real yields, which increased +22.7bps (+1.5bps Friday). The 2s10s yield curve continued its flattening, as 2yr yields gained +18.8bps (+2.2bps Friday), bringing the level to 20.5bps, the lowest since early March 2020.

The Bank of England also hiked rates, raising the Bank Rate by 25 basis points in an 8-1 decision. The lone dissenter preferred to keep policy rates on hold, in contrast to the four dissenters in the February meeting which voted for a 50 basis point increase.

Forward guidance added to the dovish tone, as it emphasised two-sided risks around the outlook, with downside impacts to growth featuring as prominent as upside risks to inflation, in contrast with recent advanced economy central bank communications. In line, 10yr gilt yields lagged other DM yields, gaining +0.6bps (-6.8bps Friday), as 10yr bunds increased +12.4bps (-1.2bps Friday). 2yr gilt yields priced out hikes, falling -10.9bps (-8.9bps Friday). Markets are pricing the Bank Rate to end the year at 1.87%, as opposed to 2.0% a week ago.

Meanwhile, the Bank of Japan left policy unchanged, and warned of downside risks to growth stemming from the invasion of Ukraine, picking up the BoE’s dovish mantle.

In line with the improvement in risk sentiment, crude oil prices fell a modest -3.97% over the week (+1.21% Friday), but still put in some large intraday swings. Prices also eased following reports that progress on the Iran nuclear deal would not be handcuffed by sanctions on Russia. European natural gas also fell -23.42% (-0.65% Friday). Given the volatility in energy markets, French President Macron warned the state may need to seize control of some energy firms.

Elsewhere, sentiment was boosted by reports that China would actively introduce policies that benefit markets and take steps to avoid the most spartan lockdown measures.

International

Beloved mall retailer files Chapter 7 bankruptcy, will liquidate

The struggling chain has given up the fight and will close hundreds of stores around the world.

Share this:

It has been a brutal period for several popular retailers. The fallout from the covid pandemic and a challenging economic environment have pushed numerous chains into bankruptcy with Tuesday Morning, Christmas Tree Shops, and Bed Bath & Beyond all moving from Chapter 11 to Chapter 7 bankruptcy liquidation.

In all three of those cases, the companies faced clear financial pressures that led to inventory problems and vendors demanding faster, or even upfront payment. That creates a sort of inevitability.

Related: Beloved retailer finds life after bankruptcy, new famous owner

When a retailer faces financial pressure it sets off a cycle where vendors become wary of selling them items. That leads to barren shelves and no ability for the chain to sell its way out of its financial problems.

Once that happens bankruptcy generally becomes the only option. Sometimes that means a Chapter 11 filing which gives the company a chance to negotiate with its creditors. In some cases, deals can be worked out where vendors extend longer terms or even forgive some debts, and banks offer an extension of loan terms.

In other cases, new funding can be secured which assuages vendor concerns or the company might be taken over by its vendors. Sometimes, as was the case with David's Bridal, a new owner steps in, adds new money, and makes deals with creditors in order to give the company a new lease on life.

It's rare that a retailer moves directly into Chapter 7 bankruptcy and decides to liquidate without trying to find a new source of funding.

Image source: Getty Images

The Body Shop has bad news for customers

The Body Shop has been in a very public fight for survival. Fears began when the company closed half of its locations in the United Kingdom. That was followed by a bankruptcy-style filing in Canada and an abrupt closure of its U.S. stores on March 4.

"The Canadian subsidiary of the global beauty and cosmetics brand announced it has started restructuring proceedings by filing a Notice of Intention (NOI) to Make a Proposal pursuant to the Bankruptcy and Insolvency Act (Canada). In the same release, the company said that, as of March 1, 2024, The Body Shop US Limited has ceased operations," Chain Store Age reported.

A message on the company's U.S. website shared a simple message that does not appear to be the entire story.

"We're currently undergoing planned maintenance, but don't worry we're due to be back online soon."

That same message is still on the company's website, but a new filing makes it clear that the site is not down for maintenance, it's down for good.

The Body Shop files for Chapter 7 bankruptcy

While the future appeared bleak for The Body Shop, fans of the brand held out hope that a savior would step in. That's not going to be the case.

The Body Shop filed for Chapter 7 bankruptcy in the United States.

"The US arm of the ethical cosmetics group has ceased trading at its 50 outlets. On Saturday (March 9), it filed for Chapter 7 insolvency, under which assets are sold off to clear debts, putting about 400 jobs at risk including those in a distribution center that still holds millions of dollars worth of stock," The Guardian reported.

After its closure in the United States, the survival of the brand remains very much in doubt. About half of the chain's stores in the United Kingdom remain open along with its Australian stores.

The future of those stores remains very much in doubt and the chain has shared that it needs new funding in order for them to continue operating.

The Body Shop did not respond to a request for comment from TheStreet.

bankruptcy pandemic canadaGovernment

Are Voters Recoiling Against Disorder?

Are Voters Recoiling Against Disorder?

Authored by Michael Barone via The Epoch Times (emphasis ours),

The headlines coming out of the Super…

Share this:

Authored by Michael Barone via The Epoch Times (emphasis ours),

The headlines coming out of the Super Tuesday primaries have got it right. Barring cataclysmic changes, Donald Trump and Joe Biden will be the Republican and Democratic nominees for president in 2024.

With Nikki Haley’s withdrawal, there will be no more significantly contested primaries or caucuses—the earliest both parties’ races have been over since something like the current primary-dominated system was put in place in 1972.

The primary results have spotlighted some of both nominees’ weaknesses.

Donald Trump lost high-income, high-educated constituencies, including the entire metro area—aka the Swamp. Many but by no means all Haley votes there were cast by Biden Democrats. Mr. Trump can’t afford to lose too many of the others in target states like Pennsylvania and Michigan.

Majorities and large minorities of voters in overwhelmingly Latino counties in Texas’s Rio Grande Valley and some in Houston voted against Joe Biden, and even more against Senate nominee Rep. Colin Allred (D-Texas).

Returns from Hispanic precincts in New Hampshire and Massachusetts show the same thing. Mr. Biden can’t afford to lose too many Latino votes in target states like Arizona and Georgia.

When Mr. Trump rode down that escalator in 2015, commentators assumed he’d repel Latinos. Instead, Latino voters nationally, and especially the closest eyewitnesses of Biden’s open-border policy, have been trending heavily Republican.

High-income liberal Democrats may sport lawn signs proclaiming, “In this house, we believe ... no human is illegal.” The logical consequence of that belief is an open border. But modest-income folks in border counties know that flows of illegal immigrants result in disorder, disease, and crime.

There is plenty of impatience with increased disorder in election returns below the presidential level. Consider Los Angeles County, America’s largest county, with nearly 10 million people, more people than 40 of the 50 states. It voted 71 percent for Mr. Biden in 2020.

Current returns show county District Attorney George Gascon winning only 21 percent of the vote in the nonpartisan primary. He’ll apparently face Republican Nathan Hochman, a critic of his liberal policies, in November.

Gascon, elected after the May 2020 death of counterfeit-passing suspect George Floyd in Minneapolis, is one of many county prosecutors supported by billionaire George Soros. His policies include not charging juveniles as adults, not seeking higher penalties for gang membership or use of firearms, and bringing fewer misdemeanor cases.

The predictable result has been increased car thefts, burglaries, and personal robberies. Some 120 assistant district attorneys have left the office, and there’s a backlog of 10,000 unprosecuted cases.

More than a dozen other Soros-backed and similarly liberal prosecutors have faced strong opposition or have left office.

St. Louis prosecutor Kim Gardner resigned last May amid lawsuits seeking her removal, Milwaukee’s John Chisholm retired in January, and Baltimore’s Marilyn Mosby was defeated in July 2022 and convicted of perjury in September 2023. Last November, Loudoun County, Virginia, voters (62 percent Biden) ousted liberal Buta Biberaj, who declined to prosecute a transgender student for assault, and in June 2022 voters in San Francisco (85 percent Biden) recalled famed radical Chesa Boudin.

Similarly, this Tuesday, voters in San Francisco passed ballot measures strengthening police powers and requiring treatment of drug-addicted welfare recipients.

In retrospect, it appears the Floyd video, appearing after three months of COVID-19 confinement, sparked a frenzied, even crazed reaction, especially among the highly educated and articulate. One fatal incident was seen as proof that America’s “systemic racism” was worse than ever and that police forces should be defunded and perhaps abolished.

2020 was “the year America went crazy,” I wrote in January 2021, a year in which police funding was actually cut by Democrats in New York, Los Angeles, San Francisco, Seattle, and Denver. A year in which young New York Times (NYT) staffers claimed they were endangered by the publication of Sen. Tom Cotton’s (R-Ark.) opinion article advocating calling in military forces if necessary to stop rioting, as had been done in Detroit in 1967 and Los Angeles in 1992. A craven NYT publisher even fired the editorial page editor for running the article.

Evidence of visible and tangible discontent with increasing violence and its consequences—barren and locked shelves in Manhattan chain drugstores, skyrocketing carjackings in Washington, D.C.—is as unmistakable in polls and election results as it is in daily life in large metropolitan areas. Maybe 2024 will turn out to be the year even liberal America stopped acting crazy.

Chaos and disorder work against incumbents, as they did in 1968 when Democrats saw their party’s popular vote fall from 61 percent to 43 percent.

Views expressed in this article are opinions of the author and do not necessarily reflect the views of The Epoch Times or ZeroHedge.

Government

Veterans Affairs Kept COVID-19 Vaccine Mandate In Place Without Evidence

Veterans Affairs Kept COVID-19 Vaccine Mandate In Place Without Evidence

Authored by Zachary Stieber via The Epoch Times (emphasis ours),

The…

Share this:

{kind=link}

{kind=link}

Authored by Zachary Stieber via The Epoch Times (emphasis ours),

The U.S. Department of Veterans Affairs (VA) reviewed no data when deciding in 2023 to keep its COVID-19 vaccine mandate in place.

{kind=link}

VA Secretary Denis McDonough said on May 1, 2023, that the end of many other federal mandates “will not impact current policies at the Department of Veterans Affairs.”

He said the mandate was remaining for VA health care personnel “to ensure the safety of veterans and our colleagues.”

Mr. McDonough did not cite any studies or other data. A VA spokesperson declined to provide any data that was reviewed when deciding not to rescind the mandate. The Epoch Times submitted a Freedom of Information Act for “all documents outlining which data was relied upon when establishing the mandate when deciding to keep the mandate in place.”

The agency searched for such data and did not find any.

“The VA does not even attempt to justify its policies with science, because it can’t,” Leslie Manookian, president and founder of the Health Freedom Defense Fund, told The Epoch Times.

“The VA just trusts that the process and cost of challenging its unfounded policies is so onerous, most people are dissuaded from even trying,” she added.

The VA’s mandate remains in place to this day.

The VA’s website claims that vaccines “help protect you from getting severe illness” and “offer good protection against most COVID-19 variants,” pointing in part to observational data from the U.S. Centers for Disease Control and Prevention (CDC) that estimate the vaccines provide poor protection against symptomatic infection and transient shielding against hospitalization.

There have also been increasing concerns among outside scientists about confirmed side effects like heart inflammation—the VA hid a safety signal it detected for the inflammation—and possible side effects such as tinnitus, which shift the benefit-risk calculus.

President Joe Biden imposed a slate of COVID-19 vaccine mandates in 2021. The VA was the first federal agency to implement a mandate.

President Biden rescinded the mandates in May 2023, citing a drop in COVID-19 cases and hospitalizations. His administration maintains the choice to require vaccines was the right one and saved lives.

“Our administration’s vaccination requirements helped ensure the safety of workers in critical workforces including those in the healthcare and education sectors, protecting themselves and the populations they serve, and strengthening their ability to provide services without disruptions to operations,” the White House said.

Some experts said requiring vaccination meant many younger people were forced to get a vaccine despite the risks potentially outweighing the benefits, leaving fewer doses for older adults.

“By mandating the vaccines to younger people and those with natural immunity from having had COVID, older people in the U.S. and other countries did not have access to them, and many people might have died because of that,” Martin Kulldorff, a professor of medicine on leave from Harvard Medical School, told The Epoch Times previously.

The VA was one of just a handful of agencies to keep its mandate in place following the removal of many federal mandates.

“At this time, the vaccine requirement will remain in effect for VA health care personnel, including VA psychologists, pharmacists, social workers, nursing assistants, physical therapists, respiratory therapists, peer specialists, medical support assistants, engineers, housekeepers, and other clinical, administrative, and infrastructure support employees,” Mr. McDonough wrote to VA employees at the time.

“This also includes VA volunteers and contractors. Effectively, this means that any Veterans Health Administration (VHA) employee, volunteer, or contractor who works in VHA facilities, visits VHA facilities, or provides direct care to those we serve will still be subject to the vaccine requirement at this time,” he said. “We continue to monitor and discuss this requirement, and we will provide more information about the vaccination requirements for VA health care employees soon. As always, we will process requests for vaccination exceptions in accordance with applicable laws, regulations, and policies.”

The version of the shots cleared in the fall of 2022, and available through the fall of 2023, did not have any clinical trial data supporting them.

A new version was approved in the fall of 2023 because there were indications that the shots not only offered temporary protection but also that the level of protection was lower than what was observed during earlier stages of the pandemic.

Ms. Manookian, whose group has challenged several of the federal mandates, said that the mandate “illustrates the dangers of the administrative state and how these federal agencies have become a law unto themselves.”

Veterans Affairs Kept COVID-19 Vaccine Mandate In Place Without Evidence

The Coming Of The Police State In America

When Military Rule Supplants Democracy

Mortgage rates fall as labor market normalizes

Economic Earthquake Ahead? The Cracks Are Spreading Fast

February Employment Situation

Low Iron Levels In Blood Could Trigger Long COVID: Study

Walmart has really good news for shoppers (and Joe Biden)

Another beloved brewery files Chapter 11 bankruptcy

Beloved mall retailer files Chapter 7 bankruptcy, will liquidate

-

Uncategorized2 weeks ago

Uncategorized2 weeks agoAll Of The Elements Are In Place For An Economic Crisis Of Staggering Proportions

-

Uncategorized1 month ago

Uncategorized1 month agoCathie Wood sells a major tech stock (again)

-

Uncategorized3 weeks ago

Uncategorized3 weeks agoCalifornia Counties Could Be Forced To Pay $300 Million To Cover COVID-Era Program

-

Uncategorized2 weeks ago

Uncategorized2 weeks agoApparel Retailer Express Moving Toward Bankruptcy

-

Uncategorized3 weeks ago

Uncategorized3 weeks agoIndustrial Production Decreased 0.1% in January

-

International2 days ago

International2 days agoWalmart launches clever answer to Target’s new membership program

-

International2 days ago

International2 days agoEyePoint poaches medical chief from Apellis; Sandoz CFO, longtime BioNTech exec to retire

-

Uncategorized3 weeks ago

Uncategorized3 weeks agoRFK Jr: The Wuhan Cover-Up & The Rise Of The Biowarfare-Industrial Complex