International

Three Generic Pharmaceutical Manufacturers to Buy for Profitable Investing

Three generic pharmaceutical manufacturers to buy for profitable investing opportunities feature companies that have risen near the top of that sector. The three generic pharmaceutical manufacturers to buy include two dividend payers and offer the potenti

Share this:

Three generic pharmaceutical manufacturers to buy for profitable investing opportunities feature companies that have risen near the top of that sector.

The three generic pharmaceutical manufacturers to buy include two dividend payers and offer the potential that they all could produce further growth organically and through acquisition. The trade-off is that the three generic pharmaceutical manufacturers to buy typically would not offer the potential blockbuster new drugs that could cause their share prices to soar.

One of the three generic pharmaceutical manufacturers to buy is from India, while the other two are based in the United States. The company based in India may have one of the most recognized brands in the generic industry because it was founded by a physician and named after him.

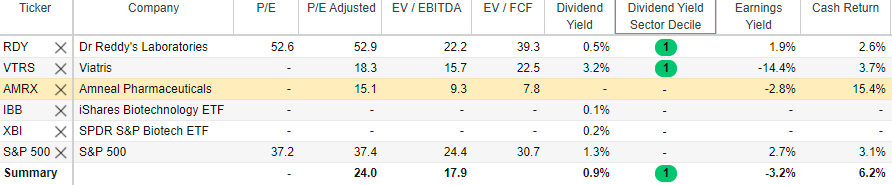

Source: Stock Rover. Click here to sign up for a free two-week trial.

For investors interested in gaining exposure to generic pharmaceutical companies, look to India, which has become a “global powerhouse” in the industry, said Bob Carlson, leader of the Retirement Watch investment newsletter.

Pension fund and Retirement Watch leader Bob Carlson answers questions from Paul Dykewicz.

Three Generic Pharmaceutical Manufacturers to Buy Include Dr. Reddy’s Laboratories

Among the top prospects for investors interested in companies that provide generic pharmaceuticals are Dr. Reddy’s Laboratories (NYSE:RDY), Sun Pharmaceutical industries (524715.India), Divi’s Laboratories (532488.India) and Cipla (500087.India). However, the generic sector of the pharmaceutical industry has had its problems, Carlson cautioned.

It also generally been under fire for overpricing generic drugs, Carlson continued. U.S. pharmacies and other buyers have consolidated further than in the past and are negotiating reduced prices with the generic drug makers as several government investigations have occurred in the sector, he continued.

Dr. Reddy reported in its fourth-quarter 6-K document filed with the U.S. Securities and Exchange Commission (SEC) that it is involved in disputes, lawsuits, claims, governmental and/or regulatory inspections, inquiries, investigations and proceedings, including patent and commercial matters that arise from time to time in the ordinary course of business. Most of the claims involve “complex issues” that are subject to uncertainties and the probability of a loss, the company added.

Dr. Reddy’s Headlines Three Generic Pharmaceutical Manufacturers to Buy

However, Dr. Reddy’s rising share price since the end of 2020 shows that the stock’s fortunes have not been ruined by those risks. Aside from manufacturing generic pharmaceuticals, Dr. Reddy partnered with the Russian Direct Investment Fund to cooperate on clinical trials and distribution of Sputnik V COVID-19 vaccine in India. Upon regulatory approval in India, RDIF agreed to supply Dr. Reddy’s with 100 million doses of the vaccine that is based on a well-studied human adenoviral vector platform to provide proven safety and to complete clinical trials to show its efficacy against COVID-19, the company announced.

Carlson commented that the coronavirus pandemic created supply shortages of compounds used to manufacture generic drugs. There are no U.S.-based locations that produce the compounds, which put American generic drug manufacturers at a disadvantage to those in India and China, he added.

A potential problem for the India-based companies is that as the pandemic wanes, the U.S. Food and Drug Administration (FDA) will have more extensive examinations of the factories in India than has been the case the last 18 months or so, Carlson said.

Three Generic Pharmaceutical Manufacturers to Buy Offer Diversified Revenues

Dr. Reddy’s operates three core segments: Pharmaceutical Services and Active Ingredients, Global Generics and Proprietary Products. Its management described its strengths as Chemical Synthesis, Formulation Development and Manufacturing; Clinical and Regulatory expertise; and robust global supply chain and strategic networks.

Analysts at Barclays PLC upgraded its rating of Dr. Reddy on Feb. 2 to “overweight” from an “equal weight” rating due to the company’s planned launch of its Sputnik vaccine. The heightened rating also included an increased price target of $70.00, up from $56.00. The stock subsequently showed those projections were conservative when the share price closed at $73.51 on July 13.

Chart courtesy of www.StockCharts.com

Money Manager Picks Two of Three Generic Pharmaceutical Manufacturers to Buy

“Pure generic drug investment opportunities have become scarce over the years because success in that business is either predicated on moving up the industry food chain into proprietary products or reaching scale via consolidation,” said Hilary Kramer, who heads the GameChangers and Value Authority advisory services. “Either way, the number of companies focused on off-patent drugs shrinks over time as leaders move on and laggards get bought out.”

Paul Dykewicz conducts a pre-COVID-19 interview with Hilary Kramer, whose premium advisory services include IPO Edge, 2-Day Trader, Turbo Trader and Inner Circle.

“One pure play I’d recommend right now: Amneal Pharmaceuticals Inc. (NYSE:AMRX), which shot into the market spotlight with generic epinephrine pens,” Kramer said. “But even though that initial surge is flattening out now, the stock is still interesting here below $5. You’re effectively paying under six times earnings for long-term EPS expansion of around 12% a year, which is classically an attractive price for that kind of growth profile.”

Three Generic Pharmaceutical Manufacturers to Buy Include Amneal

Amneal Pharmaceuticals, headquartered in Bridgewater, New Jersey, focuses on the development, manufacture and distribution of generic and specialty drug products. The company announced earlier this year that the Food and Drug Administration (FDA) has accepted the Biologics License Application (BLA) for its Bevacizumab, with a standard review goal date in second-quarter 2022, according to the BsUFA (Biosimilar User Fee Act).

Chart courtesy of www.StockCharts.com

On April 5, Amneal completed its previously announced acquisition of a 98% interest in Kashiv Specialty Pharmaceuticals, LLC. Kashiv Specialty Pharmaceuticals focused on the development of complex generics, innovative drug delivery platforms and novel 505(b)(2) drugs.

Viatris Emerges as One of Three Generic Pharmaceutical Manufacturers to Buy

Otherwise, investors probably are better off simply buying into a big pharmaceutical manufacturer like Viatris Inc. (NASDAQ:VTRS), a Canonsburg, Pennsylvania-based specialty and generics drug company that was formed by a merger between Pfizer’s (NYSE: PFE) Upjohn legacy brands business and Mylan, a generic and biosimilar drug manufacturer. Viatris has a “commanding franchise” and pays a 3% dividend as a bonus, Kramer counseled.

Chart courtesy of www.StockCharts.com

Funds Offer Alternative to Three Generic Pharmaceutical Manufacturers to Buy

Biotechnology stocks and funds have been doing well recently, and that’s likely to continue, Carlson said. Companies continue to announce breakthroughs, and a number of biotech companies are going public, he added.

It is tough to identify the best individual stocks in the sector to buy. He recommends a diversified exchange-traded fund (ETF) for most investors. But even that is difficult, because of differences in the stocks held by the leading ETFs. The best move for investors seeking alternatives to the three pharmaceutical manufacturing stocks to buy might be to hold positions in the two leading biotech ETFs.

iShares Biotechnology (IBB) aims to track the NASDAQ Biotechnology Index, so it holds only stocks listed on the NASDAQ and that are classified as either biotechnology or pharmaceutical companies. This tends to be the more volatile of the funds, and over some periods its returns can be substantially higher or lower than alternatives.

IBB Rose More Than 25% in Both 2019 and 2020

IBB returned 25.21% in 2019, 26.01% in 2020 and 6.35% so far in 2021. Its three-year annualized return is 14.24%, and its five-year return is 14.71%.

The other fund is SPDR S&P Biotech (XBI), which aims to track the S&P Biotechnology Select Industry Index. The sector index is derived from a U.S. total market composite, so it isn’t limited to S&P 500 stocks. But the fund uses a sampling strategy to try to track the index instead of holding all the stocks in the index. XBI tends to favor stocks with greater liquidity, so it does not own many smaller companies or those with limited trading volume.

XBI Carries Less Risk Than Three Generic Pharmaceutical Manufacturers to Buy

Though it is less volatile than IBB, XBI is more volatile than the market indexes and the health care sector. The fund returned 32.56% in 2019, 48.33% in 2020, but so far in 2021 is down 7.90%. The fund’s annualized returns are 13.01% over three years and 21.94% over five years.

The difficulty of categorizing stocks and funds in the sector is evidenced by Morningstar’s classification of these funds. IBB is in the Specialty-Technology category and XBI is in the Specialty-Health category.

IBB tends to hold larger capitalization companies than XBI. Despite their differences, Morningstar says the two funds have a correlation of 94%.

Five Biopharmaceutical Stocks to Buy as New Variants of COVID-19 Spread

The increasingly transmissible Delta variant of COVID-19 has spread to almost every state in America, raising concerns among health officials about potential spikes in cases. Genetic variants of SARS-CoV-2 have been emerging and circulating around the world throughout the COVID-19 pandemic, according to the Centers for Disease Control and Prevention (CDC).

A variant has one or more mutations that differentiate it from other variants in circulation. The Delta variant is expected to become the dominant coronavirus strain in the United States, the CDC director said. With more than half the U.S. population not fully vaccinated, public health officials caution that a resurgence of COVID-19 cases could occur in the fall when many unvaccinated children are expected to return to school.

Progress in the COVID-19 vaccination process lifts hope that new cases and deaths will keep falling. So far, 184,543,821 people, or 55.6% of the U.S. population, have received at least one dose of a COVID-19 vaccine. Those fully vaccinated total 159,675,163 people, or 48.1%, of the U.S. population, according to the CDC.

Plus, the Food and Drug Administration recently approved a third COVID-19 vaccine, manufactured by Johnson & Johnson (NYSE:JNJ), which requires only one dose rather than two, as needed with the first two vaccine providers: Pfizer (NYSE:PFE) and Moderna (NASDAQ:MRNA).

COVID-19 cases worldwide have hit 187,798,855 and caused 4,048,903 deaths, as of July 14, according to Johns Hopkins University. U.S. COVID-19 cases totaled 33,914,884 and have led to 607,771 deaths. America has the dubious distinction as the country with the most COVID-19 cases and deaths.

The three generic pharmaceutical stocks to buy offer ways for investors to profit amid the pandemic. Rising COVID-19 vaccine availability, improving economic data and a recent $1.9 trillion federal stimulus package should help to lift the valuations of the three generic pharmaceutical stocks to buy.

Paul Dykewicz, www.pauldykewicz.com, is an accomplished, award-winning journalist who has written for Dow Jones, the Wall Street Journal, Investor’s Business Daily, USA Today, the Journal of Commerce, Seeking Alpha, GuruFocus and other publications and websites. Paul, who can be followed on Twitter @PaulDykewicz, is the editor of StockInvestor.com and DividendInvestor.com, a writer for both websites and a columnist. He further is editorial director of Eagle Financial Publications in Washington, D.C., where he edits monthly investment newsletters, time-sensitive trading alerts, free e-letters and other investment reports. Paul previously served as business editor of Baltimore’s Daily Record newspaper. Paul also is the author of an inspirational book, “Holy Smokes! Golden Guidance from Notre Dame’s Championship Chaplain,” with a foreword by former national championship-winning football coach Lou Holtz. The book is great as a gift and is endorsed by Joe Montana, Joe Theismann, Ara Parseghian, “Rocket” Ismail, Reggie Brooks, Dick Vitale and many others. Call 202-677-4457 for special Father’s Day gift pricing!

The post Three Generic Pharmaceutical Manufacturers to Buy for Profitable Investing appeared first on Stock Investor.

stimulus pandemic coronavirus covid-19 dow jones sp 500 nasdaq stocks etf cdc disease control vaccine fda clinical trials genetic spread deaths new cases stimulus india chinaInternational

Riley Gaines Explains How Women’s Sports Are Rigged To Promote The Trans Agenda

Riley Gaines Explains How Women’s Sports Are Rigged To Promote The Trans Agenda

Is there a light forming when it comes to the long, dark and…

Share this:

Is there a light forming when it comes to the long, dark and bewildering tunnel of social justice cultism? Global events have been so frenetic that many people might not remember, but only a couple years ago Big Tech companies and numerous governments were openly aligned in favor of mass censorship. Not just to prevent the public from investigating the facts surrounding the pandemic farce, but to silence anyone questioning the validity of woke concepts like trans ideology.

From 2020-2022 was the closest the west has come in a long time to a complete erasure of freedom of speech. Even today there are still countries and Europe and places like Canada or Australia that are charging forward with draconian speech laws. The phrase "radical speech" is starting to circulate within pro-censorship circles in reference to any platform where people are allowed to talk critically. What is radical speech? Basically, it's any discussion that runs contrary to the beliefs of the political left.

Open hatred of moderate or conservative ideals is perfectly acceptable, but don't ever shine a negative light on woke activism, or you might be a terrorist.

Riley Gaines has experienced this double standard first hand. She was even assaulted and taken hostage at an event in 2023 at San Francisco State University when leftists protester tried to trap her in a room and demanded she "pay them to let her go." Campus police allegedly witnessed the incident but charges were never filed and surveillance footage from the college was never released.

It's probably the last thing a champion female swimmer ever expects, but her head-on collision with the trans movement and the institutional conspiracy to push it on the public forced her to become a counter-culture voice of reason rather than just an athlete.

For years the independent media argued that no matter how much we expose the insanity of men posing as women to compete and dominate women's sports, nothing will really change until the real female athletes speak up and fight back. Riley Gaines and those like her represent that necessary rebellion and a desperately needed return to common sense and reason.

In a recent interview on the Joe Rogan Podcast, Gaines related some interesting information on the inner workings of the NCAA and the subversive schemes surrounding trans athletes. Not only were women participants essentially strong-armed by colleges and officials into quietly going along with the program, there was also a concerted propaganda effort. Competition ceremonies were rigged as vehicles for promoting trans athletes over everyone else.

The bottom line? The competitions didn't matter. The real women and their achievements didn't matter. The only thing that mattered to officials were the photo ops; dudes pretending to be chicks posing with awards for the gushing corporate media. The agenda took precedence.

Lia Thomas, formerly known as William Thomas, was more than an activist invading female sports, he was also apparently a science project fostered and protected by the athletic establishment. It's important to understand that the political left does not care about female athletes. They do not care about women's sports. They don't care about the integrity of the environments they co-opt. Their only goal is to identify viable platforms with social impact and take control of them. Women's sports are seen as a vehicle for public indoctrination, nothing more.

The reasons why they covet women's sports are varied, but a primary motive is the desire to assert the fallacy that men and women are "the same" psychologically as well as physically. They want the deconstruction of biological sex and identity as nothing more than "social constructs" subject to personal preference. If they can destroy what it means to be a man or a woman, they can destroy the very foundations of relationships, families and even procreation.

For now it seems as though the trans agenda is hitting a wall with much of the public aware of it and less afraid to criticize it. Social media companies might be able to silence some people, but they can't silence everyone. However, there is still a significant threat as the movement continues to target children through the public education system and women's sports are not out of the woods yet.

The ultimate solution is for women athletes around the world to organize and widely refuse to participate in any competitions in which biological men are allowed. The only way to save women's sports is for women to be willing to end them, at least until institutions that put doctrine ahead of logic are made irrelevant.

International

Congress’ failure so far to deliver on promise of tens of billions in new research spending threatens America’s long-term economic competitiveness

A deal that avoided a shutdown also slashed spending for the National Science Foundation, putting it billions below a congressional target intended to…

Share this:

Federal spending on fundamental scientific research is pivotal to America’s long-term economic competitiveness and growth. But less than two years after agreeing the U.S. needed to invest tens of billions of dollars more in basic research than it had been, Congress is already seriously scaling back its plans.

A package of funding bills recently passed by Congress and signed by President Joe Biden on March 9, 2024, cuts the current fiscal year budget for the National Science Foundation, America’s premier basic science research agency, by over 8% relative to last year. That puts the NSF’s current allocation US$6.6 billion below targets Congress set in 2022.

And the president’s budget blueprint for the next fiscal year, released on March 11, doesn’t look much better. Even assuming his request for the NSF is fully funded, it would still, based on my calculations, leave the agency a total of $15 billion behind the plan Congress laid out to help the U.S. keep up with countries such as China that are rapidly increasing their science budgets.

I am a sociologist who studies how research universities contribute to the public good. I’m also the executive director of the Institute for Research on Innovation and Science, a national university consortium whose members share data that helps us understand, explain and work to amplify those benefits.

Our data shows how underfunding basic research, especially in high-priority areas, poses a real threat to the United States’ role as a leader in critical technology areas, forestalls innovation and makes it harder to recruit the skilled workers that high-tech companies need to succeed.

A promised investment

Less than two years ago, in August 2022, university researchers like me had reason to celebrate.

Congress had just passed the bipartisan CHIPS and Science Act. The science part of the law promised one of the biggest federal investments in the National Science Foundation in its 74-year history.

The CHIPS act authorized US$81 billion for the agency, promised to double its budget by 2027 and directed it to “address societal, national, and geostrategic challenges for the benefit of all Americans” by investing in research.

But there was one very big snag. The money still has to be appropriated by Congress every year. Lawmakers haven’t been good at doing that recently. As lawmakers struggle to keep the lights on, fundamental research is quickly becoming a casualty of political dysfunction.

Research’s critical impact

That’s bad because fundamental research matters in more ways than you might expect.

For instance, the basic discoveries that made the COVID-19 vaccine possible stretch back to the early 1960s. Such research investments contribute to the health, wealth and well-being of society, support jobs and regional economies and are vital to the U.S. economy and national security.

Lagging research investment will hurt U.S. leadership in critical technologies such as artificial intelligence, advanced communications, clean energy and biotechnology. Less support means less new research work gets done, fewer new researchers are trained and important new discoveries are made elsewhere.

But disrupting federal research funding also directly affects people’s jobs, lives and the economy.

Businesses nationwide thrive by selling the goods and services – everything from pipettes and biological specimens to notebooks and plane tickets – that are necessary for research. Those vendors include high-tech startups, manufacturers, contractors and even Main Street businesses like your local hardware store. They employ your neighbors and friends and contribute to the economic health of your hometown and the nation.

Nearly a third of the $10 billion in federal research funds that 26 of the universities in our consortium used in 2022 directly supported U.S. employers, including:

A Detroit welding shop that sells gases many labs use in experiments funded by the National Institutes of Health, National Science Foundation, Department of Defense and Department of Energy.

A Dallas-based construction company that is building an advanced vaccine and drug development facility paid for by the Department of Health and Human Services.

More than a dozen Utah businesses, including surveyors, engineers and construction and trucking companies, working on a Department of Energy project to develop breakthroughs in geothermal energy.

When Congress shortchanges basic research, it also damages businesses like these and people you might not usually associate with academic science and engineering. Construction and manufacturing companies earn more than $2 billion each year from federally funded research done by our consortium’s members.

Jobs and innovation

Disrupting or decreasing research funding also slows the flow of STEM – science, technology, engineering and math – talent from universities to American businesses. Highly trained people are essential to corporate innovation and to U.S. leadership in key fields, such as AI, where companies depend on hiring to secure research expertise.

In 2022, federal research grants paid wages for about 122,500 people at universities that shared data with my institute. More than half of them were students or trainees. Our data shows that they go on to many types of jobs but are particularly important for leading tech companies such as Google, Amazon, Apple, Facebook and Intel.

That same data lets me estimate that over 300,000 people who worked at U.S. universities in 2022 were paid by federal research funds. Threats to federal research investments put academic jobs at risk. They also hurt private sector innovation because even the most successful companies need to hire people with expert research skills. Most people learn those skills by working on university research projects, and most of those projects are federally funded.

High stakes

If Congress doesn’t move to fund fundamental science research to meet CHIPS and Science Act targets – and make up for the $11.6 billion it’s already behind schedule – the long-term consequences for American competitiveness could be serious.

Over time, companies would see fewer skilled job candidates, and academic and corporate researchers would produce fewer discoveries. Fewer high-tech startups would mean slower economic growth. America would become less competitive in the age of AI. This would turn one of the fears that led lawmakers to pass the CHIPS and Science Act into a reality.

Ultimately, it’s up to lawmakers to decide whether to fulfill their promise to invest more in the research that supports jobs across the economy and in American innovation, competitiveness and economic growth. So far, that promise is looking pretty fragile.

This is an updated version of an article originally published on Jan. 16, 2024.

Jason Owen-Smith receives research support from the National Science Foundation, the National Institutes of Health, the Alfred P. Sloan Foundation and Wellcome Leap.

economic growth covid-19 grants congress vaccine chinaInternational

What’s Driving Industrial Development in the Southwest U.S.

The post-COVID-19 pandemic pipeline, supply imbalances, investment and construction challenges: these are just a few of the topics address by a powerhouse…

Share this:

{kind=link}

The post-COVID-19 pandemic pipeline, supply imbalances, investment and construction challenges: these are just a few of the topics address by a powerhouse panel of executives in industrial real estate this week at NAIOP’s I.CON West in Long Beach, California. Led by Dawn McCombs, principal and Denver lead industrial specialist for Avison Young, the panel tackled some of the biggest issues facing the sector in the Western U.S.

Starting with the pandemic in 2020 and continuing through 2022, McCombs said, the industrial sector experienced a huge surge in demand, resulting in historic vacancies, rent growth and record deliveries. Operating fundamentals began to normalize in 2023 and construction starts declined, certainly impacting vacancy and absorption moving forward.

“Development starts dropped by 65% year-over-year across the U.S. last year. In Q4, we were down 25% from pre-COVID norms,” began Megan Creecy-Herman, president, U.S. West Region, Prologis, noting that all of that is setting us up to see an improvement of fundamentals in the market. “U.S. vacancy ended 2023 at about 5%, which is very healthy.”

Vacancies are expected to grow in Q1 and Q2, peaking mid-year at around 7%. Creecy-Herman expects to see an increase in absorption as customers begin to have confidence in the economy, and everyone gets some certainty on what the Fed does with interest rates.

“It’s an interesting dynamic to see such a great increase in rents, which have almost doubled in some markets,” said Reon Roski, CEO, Majestic Realty Co. “It’s healthy to see a slowing down… before [rents] go back up.”

Pre-pandemic, a lot of markets were used to 4-5% vacancy, said Brooke Birtcher Gustafson, fifth-generation president of Birtcher Development. “Everyone was a little tepid about where things are headed with a mediocre outlook for 2024, but much of this is normalizing in the Southwest markets.”

McCombs asked the panel where their companies found themselves in the construction pipeline when the Fed raised rates in 2022.

In Salt Lake City, said Angela Eldredge, chief operations officer at Price Real Estate, there is a typical 12-18-month lead time on construction materials. “As rates started to rise in 2022, lots of permits had already been pulled and construction starts were beginning, so those project deliveries were in fall 2023. [The slowdown] was good for our market because it kept rates high, vacancies lower and helped normalize the market to a healthy pace.”

A supply imbalance can stress any market, and Gustafson joked that the current imbalance reminded her of a favorite quote from the movie Super Troopers: “Desperation is a stinky cologne.” “We’re all still a little crazed where this imbalance has put us, but for the patient investor and owner, there will be a rebalancing and opportunity for the good quality real estate to pass the sniff test,” she said.

At Bircher, Gustafson said that mid-pandemic, there were predictions that one billion square feet of new product would be required to meet tenant demand, e-commerce growth and safety stock. That transition opened a great opportunity for investors to run at the goal. “In California, the entitlement process is lengthy, around 24-36 months to get from the start of an acquisition to the completion of a building,” she said. Fast forward to 2023-2024, a lot of what is being delivered in 2024 is the result of that chase.

“Being an optimistic developer, there is good news. The supply imbalance helped normalize what was an unsustainable surge in rents and land values,” she said. “It allowed corporate heads of real estate to proactively evaluate growth opportunities, opened the door for contrarian investors to land bank as values drop, and provided tenants with options as there is more product. Investment goals and strategies have shifted, and that’s created opportunity for buyers.”

“Developers only know how to run and develop as much as we can,” said Roski. “There are certain times in cycles that we are forced to slow down, which is a good thing. In the last few years, Majestic has delivered 12-14 million square feet, and this year we are developing 6-8 million square feet. It’s all part of the cycle.”

Creecy-Herman noted that compared to the other asset classes and opportunities out there, including office and multifamily, industrial remains much more attractive for investment. “That was absolutely one of the things that underpinned the amount of investment we saw in a relatively short time period,” she said.

Market rent growth across Los Angeles, Inland Empire and Orange County moved up more than 100% in a 24-month period. That created opportunities for landlords to flexible as they’re filling up their buildings. “Normalizing can be uncomfortable especially after that kind of historic high, but at the same time it’s setting us up for strong years ahead,” she said.

Issues that owners and landlords are facing with not as much movement in the market is driving a change in strategy, noted Gustafson. “Comps are all over the place,” she said. “You have to dive deep into every single deal that is done to understand it and how investment strategies are changing.”

Tenants experienced a variety of challenges in the pandemic years, from supply chain to labor shortages on the negative side, to increased demand for products on the positive, McCombs noted.

“Prologis has about 6,700 customers around the world, from small to large, and the universal lesson [from the pandemic] is taking a more conservative posture on inventories,” Creecy-Herman said. “Customers are beefing up inventories, and that conservatism in the supply chain is a lesson learned that’s going to stick with us for a long time.” She noted that the company has plenty of clients who want to take more space but are waiting on more certainty from the broader economy.

“E-commerce grew by 8% last year, and we think that’s going to accelerate to 10% this year. This is still less than 25% of all retail sales, so the acceleration we’re going to see in e-commerce… is going to drive the business forward for a long time,” she said.

Roski noted that customers continually re-evaluate their warehouse locations, expanding during the pandemic and now consolidating but staying within one delivery day of vast consumer bases.

“This is a generational change,” said Creecy-Herman. “Millions of young consumers have one-day delivery as a baseline for their shopping experience. Think of what this means for our business long term to help our customers meet these expectations.”

McCombs asked the panelists what kind of leasing activity they are experiencing as a return to normalcy is expected in 2024.

“During the pandemic, shifts in the ports and supply chain created a build up along the Mexican border,” said Roski, noting border towns’ importance to increased manufacturing in Mexico. A shift of populations out of California and into Arizona, Nevada, Texas and Florida have resulted in an expansion of warehouses in those markets.

Eldridge said that Salt Lake City’s “sweet spot” is 100-200 million square feet, noting that the market is best described as a mid-box distribution hub that is close to California and Midwest markets. “Our location opens up the entire U.S. to our market, and it’s continuing to grow,” she said.

The recent supply chain and West Coast port clogs prompted significant investment in nearshoring and port improvements. “Ports are always changing,” said Roski, listing a looming strike at East Coast ports, challenges with pirates in the Suez Canal, and water issues in the Panama Canal. “Companies used to fix on one port and that’s where they’d bring in their imports, but now see they need to be [bring product] in a couple of places.”

“Laredo, [Texas,] is one of the largest ports in the U.S., and there’s no water. It’s trucks coming across the border. Companies have learned to be nimble and not focused on one area,” she said.

“All of the markets in the southwest are becoming more interconnected and interdependent than they were previously,” Creecy-Herman said. “In Southern California, there are 10 markets within 500 miles with over 25 million consumers who spend, on average, 10% more than typical U.S. consumers.” Combined with the port complex, those fundamentals aren’t changing. Creecy-Herman noted that it’s less of a California exodus than it is a complementary strategy where customers are taking space in other markets as they grow. In the last 10 years, she noted there has been significant maturation of markets such as Las Vegas and Phoenix. As they’ve become more diversified, customers want to have a presence there.

In the last decade, Gustafson said, the consumer base has shifted. Tenants continue to change strategies to adapt, such as hub-and-spoke approaches. From an investment perspective, she said that strategies change weekly in response to market dynamics that are unprecedented.

McCombs said that construction challenges and utility constraints have been compounded by increased demand for water and power.

“Those are big issues from the beginning when we’re deciding on whether to buy the dirt, and another decision during construction,” Roski said. “In some markets, we order transformers more than a year before they are needed. Otherwise, the time comes [to use them] and we can’t get them. It’s a new dynamic of how leases are structured because it’s something that’s out of our control.” She noted that it’s becoming a bigger issue with electrification of cars, trucks and real estate, and the U.S. power grid is not prepared to handle it.

Salt Lake City’s land constraints play a role in site selection, said Eldridge. “Land values of areas near water are skyrocketing.”

The panelists agreed that a favorable outlook is ahead for 2024, and today’s rebalancing will drive a healthy industry in the future as demand and rates return to normalized levels, creating opportunities for investors, developers and tenants.

This post is brought to you by JLL, the social media and conference blog sponsor of NAIOP’s I.CON West 2024. Learn more about JLL at www.us.jll.com or www.jll.ca.

fed pandemic covid-19 real estate interest rates mexico

IFM’s Hat Trick and Reflections On Option-To-Buy M&A

Four Years Ago This Week, Freedom Was Torched

Red Candle In The Wind

Analyst reviews Apple stock price target amid challenges

The SNF Institute for Global Infectious Disease Research announces new advisory board

CDC Warns Thousands Of Children Sent To ER After Taking Common Sleep Aid

Economic Trends, Risks and the Industrial Market

Association of prenatal vitamins and metals with epigenetic aging at birth and in childhood

Riley Gaines Explains How Women’s Sports Are Rigged To Promote The Trans Agenda

SoCal Industrial Prioritizes Speed, Power and Sustainability

-

Uncategorized3 weeks ago

Uncategorized3 weeks agoAll Of The Elements Are In Place For An Economic Crisis Of Staggering Proportions

-

International5 days ago

International5 days agoEyePoint poaches medical chief from Apellis; Sandoz CFO, longtime BioNTech exec to retire

-

Uncategorized4 weeks ago

Uncategorized4 weeks agoCalifornia Counties Could Be Forced To Pay $300 Million To Cover COVID-Era Program

-

Uncategorized3 weeks ago

Uncategorized3 weeks agoApparel Retailer Express Moving Toward Bankruptcy

-

Uncategorized4 weeks ago

Uncategorized4 weeks agoIndustrial Production Decreased 0.1% in January

-

International5 days ago

International5 days agoWalmart launches clever answer to Target’s new membership program

-

Uncategorized4 weeks ago

Uncategorized4 weeks agoRFK Jr: The Wuhan Cover-Up & The Rise Of The Biowarfare-Industrial Complex

-

Uncategorized3 weeks ago

Uncategorized3 weeks agoGOP Efforts To Shore Up Election Security In Swing States Face Challenges