“Being self-employed, I don’t like to add extra bills or burdens, and with a moratorium, there’s no guarantee that later I won’t be further into debt.”

Lucy, freelance photographer, Colorado – July 2020

Lucy’s concern about accumulating debt echoes across America. Millions of renters and homeowners are anxious about paying both their monthly housing bill and a ballooning debt balance.

Based on present missed payment rates, consumers will accumulate at least $100B in housing debt by January 2021. The following model describes a set of linked health, social and economic events. These events are likely to unfold in next 6 months. An uncontrolled wave of virus infections drives the cascading economic impact:

> personal income falls > consumers miss rent and mortgage payments

> rent and mortgage payment moratoriums fail > consumers use credit cards to make payments

> small business apartment landlords & homeowners default on mortgages (debt bubble bursts)

> consumer spending dives

Our analysis starts by examining the virus 3rd wave and a likely increase in lockdowns.

Virus Growth Uncontrolled

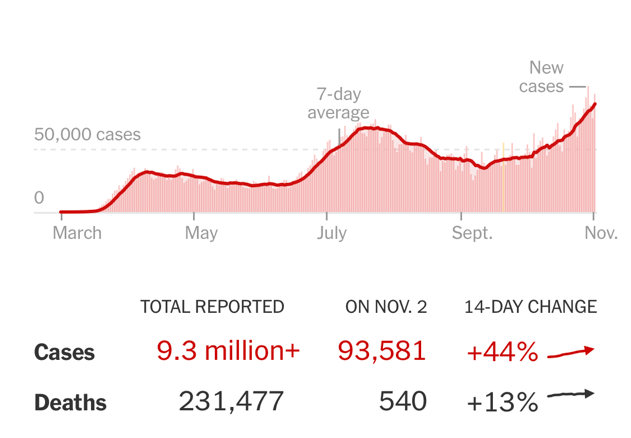

On November 2st the U.S. had a 44% increase in daily COVID-19 to 93,581. The chart below indicates the second wave of infections did not decline to the first wave low. Thus, experts forecast a third winter wave peak of cases will be higher than the second spring wave peak.

Source: New York Times – 11/3/20

Hospitalizations are rising in 42 states. Nineteen states report their highest hospitalization rate since the pandemic began in March. Uncontrolled virus infections will result in more partial or full lockdowns of intense social activity businesses including, hotels, restaurants, bars, theaters, sports stadiums, indoor arenas, offices, transit, airlines, hair salons, and personal services. An indication of what the U.S. may face soon is unfolding now in the United Kingdom, Germany, and France. These EU countries are tightening pandemic restrictions at levels not seen since last June. Meantime, U.S. businesses, such as internet entertainment, technology services, eCommerce and, socially distanced grocery stores, will continue to grow.

Economic Activity Contracts

The U.S. Economy is contracting according to the latest Sales Manager Index. The next chart shows a U.S. Sales Manager survey of national economic activity jumping in the 3rd quarter and then rolling over into contraction.

Source: World Economics, The Daily Shot – 10/22/20

Components of the Sales Manager Index that are falling or flat include business confidence contracting, market growth flat, sales growth flat, profit margins weakening, and staffing levels falling. Accordingly, staffing levels are critical to watch as more layoffs mean an increase in unemployment.

Unemployment Rises

The latest report from the Department of Labor for state unemployment claims and continuing benefits shows a high level of unemployment continuing. The trend chart below shows that while regular state benefits are declining, extended emergency benefits increase for long-term jobless workers.

Sources: Department of Labor, J.P. Morgan, The Daily Shot – 10/23/20

There are 22.6M workers on continuing unemployment assistance. This level of continuing unemployment is 22 times the level of 1M a year ago. Considering 2 -3M workers who have not qualified for extended benefits or have used up their extended benefits the number of eligible workers for unemployment is closer to 25 – 26M. Twenty-six million workers unemployed is about 17.3% of the labor force. Labor experts set the unemployment rate at 20% if other workers who did not apply for benefits are added. High unemployment rates are driving personal income down.

Personal Income Falls

Consumer personal income received a boost from several sources. The CARES Act provided $1,200 stimulus checks, enacted the Payroll Protection Program targeting small businesses, a $600 weekly increase in unemployment insurance, and other emergency loans. The following Oxford Economics analysis indicates that a budget squeeze began in October.

Sources: Oxford Economics, The Daily Shot – 10/8/20

Oxford forecasts that household income will fall by 3% below pre-COVID levels beginning in November. The model shows how tight household budgets will become by January 2021.

Consumers Miss Rent and Home Mortgage Payments

The Mortgage Bankers Association reports for the 2nd quarter of 2020 rental income losses of $9.1B and mortgage payments missed of $16.3B. For the 3rd quarter, rental losses were $9.1B and $19.4B in missed mortgage payments. For the 4th quarter, we forecast a continuing $35B total for both missed rental income and mortgage payments. The total forecast for both rental income losses and missed mortgage payments by 2021 is $90B.

However, Moody’s Analytics forecasts $70B in missed rental payments alone by 12.8M renters by January 2021. Confirming the 12.8M figure, a study by Joint Center For Housing Studies at Harvard reports that 12.1M renter households have at least one at-risk-industry worker. Due to thewide variance in estimates, we forecast at least $100B in rental and mortgage debt due in January 2021.

Our forecast of $100B in looming housing debt builds on our earlier analysis in a recent Executive – Employee Catch 22 post. In that post we identified two consumer segments, workers and professionals. We noted all homeowners reported no-confidence in making next month’s payment. The analysis indicates that 16% of professional homeowners reported little or no-confidence in making mortgage payments for September. Yet, workers reported twice the no-confidence rate of professionals at 34%.

The CARES Act mortgage and rent moratorium covered homes and apartment buildings secured with federal loans through July 31st. Renters obtained payment relief, while landlords continued to pay mortgage loans from their funds or relief act assistance. In mid-August, President Trump signed an executive order instructing the Centers for Disease Control and Prevention to identify households where infections may increase and mandate that household members be protected from eviction to ensure public safety. Since the federal moratorium ended and the CDC policy has been put into effect, thousands of landlords have filed suits challenging the CDC authority to protect renters from eviction.

Courts in some states are finding in favor of landlords causing evictions to rise. Moody’s Analytics forecasts that 16% of all renters will face eviction by January 2021. States like California and Washington passed blanket rent moratoriums in effect until January 1st, 2021. Rent debt is not erased in any case. The California moratorium calls for landlords to receive 25 % of the debt balance in January and 50% in February, followed by 25% increments to zero. With no stimulus assistance to renters and distressed homeowners, housing debt will likely continue to soar.

Consumers Use Credit Cards To Make Payments

Credit card usage by renters increased by 70% last spring. As renters received stimulus payments, the rate dipped to 50%. However, the credit card payment rate has risen to 65% due to the end of stimulus assistance.

Sources: The Philadelphia Federal Reserve, Census Bureau, The Wall Street Journal – 10/27/20

Consumers building credit card debt while unemployed or on reduced income assistance is unsustainable. Many consumers will be unable to make their credit card payments. Defaulting on their credit cards will hurt their credit score and make it more difficult to obtain other housing because they have an eviction record. A surge in credit card defaults will increase losses for credit card issuing banks as well. Today, missed rent payments force millions of small business landlords to fall behind in their mortgage payments.

Small Business Landlords Default on Mortgages

When renters miss payments, their landlords must continue to pay the mortgage on their building. Property corporations with access to low-interest bank loans or bond markets will have a cushion during this rent loss period. However, many small business landlords are financially stressed. Small business landlords own 22M properties, which are usually 1- 4 unit buildings Local small unit landlords finance their purchases with savings, other business profits, or family and friends. Only 12% of small unit buildings were covered by the CARES Act rent moratorium, which ended on July 31st. So, some small business landlords have taken action to evict tenants.

Facing a cash flow crunch, anxious small business landlords applied for CARES Act business emergency loans to mitigate income loss. The Terner Center for Housing Innovation at UC Berkeley survey of small business landlords found 40 % of owners are not confident they can pay operating costs over the next few months. So, small business landlords may evict tenants to find a paying renter. However, by 1st quarter of 2021, there are likely to be millions of people evicted or with poor credit so, finding another paying tenant could be problematic. Small business landlords facing declining income and poor prospects for new paying tenants will likely default on their mortgage. There is likely to be a surge in multi-unit buildings for sale, causing a decline in multi-unit building construction.

Home Owners Default on Mortgages

Homeowners enter into forbearance plans with their lenders to avoid penalties and fees when they are likely to be delinquent on their payments. Black Knight reports there are 3M mortgages in forbearance as of October 31st. This forbearance rate is ten times the 300k mortgages in forbearance in February of 2020. Most of these mortgages are approaching their six-month renewal date from last March and April. Homeowners can apply for a six-month renewal under the CARES Act. However, after March 2021, the forbearance period ends, and homeowners must begin paying their balance owned while continuing monthly payments.

Eighty percent of present forbearance payers have applied for a six-month extension. With unemployment increasing and lockdowns forecast, there may be an increase in the number of forbearance plans. Other homeowners who don’t qualify for forbearance are delinquent in making payments. Mortgage delinquencies outside of forbearance are up by 107% YTD as of October. By the end of 1st quarter, 2021 defaults are likely to rise significantly.

Consumer Spending Dives

A perfect economic storm is gathering strength from the health, social and financial forces we have identified in this post. The corona virus continues to penetrate all facets of American life, driving uncertainty in the economy. Until we have a national virus containment program implemented, the pandemic will force economic activity down. Without a stimulus package from Congress, millions of unemployed workers, renters, and small businesses will struggle. With the bottom 80% of consumers facing severe economic headwinds, consumer spending will likely dive in the first half of next year.

For investors, this is the time to prepare for a possible severe economic storm coming this winter. Scott Minerd, Global CIO at Guggenheim, observes that we have a pause now giving us time to prepare for an economic whirlwind:

“the relative calm we feel in the markets right now isn’t the end of the storm, it is just the eye, it may seem like there is no storm at all…yet the worst is yet to come.”

Patrick Hill is the Editor of The Progressive Ensign, https://theprogressiveensign.com/ writes from the heart of Silicon Valley, leveraging 20 years of experience as an executive at firms like HP, Genentech, Verigy, Informatica, and Okta to provide investment and economic insights. Twitter: @PatrickHill1677, email: patrickhill@theprogressiveensign.com

Former Project Veritas & O’Keefe Media Group operative and Pfizer formulation analyst scientist Justin Leslie revealed previously unpublished recordings showing Pfizer’s top vaccine researchers discussing major concerns surrounding COVID-19 vaccines. Leslie delivered these recordings to Veritas in late 2021, but they were never published:

Principal scientist at Pfizer, Kanwall Gill in 2021:

“We had no idea how it’s going to look like. MRNA vaccines have been there for 50 years, but nothing went to clinical trial because MRNA have been known to have side effects.”

Featured in Leslie’s footage is Kanwal Gill, a principal scientist at Pfizer. Gill was weary of MRNA technology given its long research history yet lack of approved commercial products. She called the vaccines “sneaky,” suggesting latent side effects could emerge in time.

Gill goes on to illustrate how the vaccine formulation process was dramatically rushed under the FDA’s Emergency Use Authorization and adds that profit incentives likely played a role:

Pfizer's principal scientist in 2021:

“It takes 10 year for a vaccine to come out. It takes years of observations... we are doing everything at the same time."

"It’s going to affect my heart, and I’m going to die. And nobody’s talking about that."

Leslie recorded another colleague, Pfizer’s pharmaceutical formulation scientist Ramin Darvari, who raised the since-validated concern that repeat booster intake could damage the cardiovascular system:

Pfizer's pharmaceutical formulation scientist, Ramin Darvari, in 2021:

“They’re engineering it specifically for me to take the next one, so increasing my consumption."

“It’s going to affect my heart, and I’m going to die. And nobody’s talking about that.”

None of these claims will be shocking to hear in 2024, but it is telling that high-level Pfizer researchers were discussing these topics in private while the company assured the public of “no serious safety concerns” upon the jab’s release:

Vaccine for Children is a Different Formulation

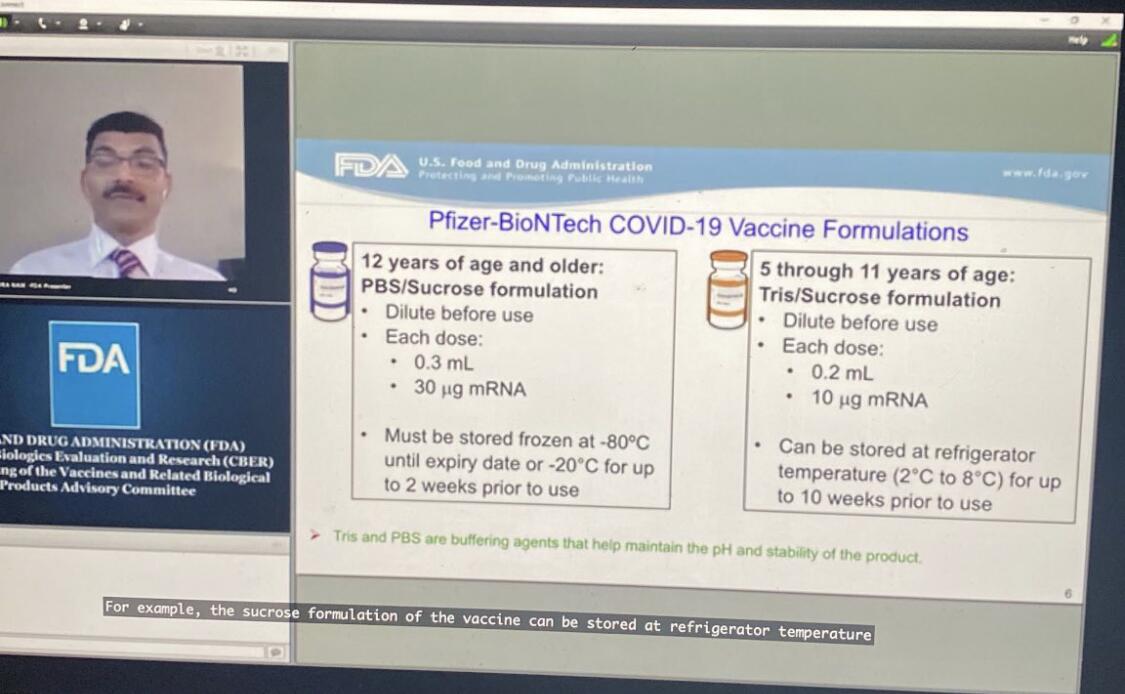

Leslie sent me a little-known FDA-Pfizer conference — a 7-hour Zoom meeting published in tandem with the approval of the vaccine for 5 – 11 year-olds — during which Pfizer’s vice presidents of vaccine research and development, Nicholas Warne and William Gruber, discussed a last-minute change to the vaccine’s “buffer” — from “PBS” to “Tris” — to improve its shelf life. For about 30 seconds of these 7 hours, Gruber acknowledged that the new formula was NOT the one used in clinical trials (emphasis mine):

“The studies were done using the same volume… but contained the PBS buffer. We obviously had extensive consultations with the FDA and it was determined that the clinical studies were not required because, again, the LNP and the MRNA are the same and the behavior — in terms of reactogenicity and efficacy — are expected to be the same.”

According to Leslie, the tweaked “buffer” dramatically changed the temperature needed for storage: “Before they changed this last step of the formulation, the formula was to be kept at -80 degrees Celsius. After they changed the last step, we kept them at 2 to 8 degrees celsius,” Leslie told me.

The claims are backed up in the referenced video presentation:

I’m no vaccinologist but an 80-degree temperature delta — and a 5x shelf-life in a warmer climate — seems like a significant change that might warrant clinical trials before commercial release.

Despite this information technically being public, there has been virtually no media scrutiny or even coverage — and in fact, most were told the vaccine for children was the same formula but just a smaller dose — which is perhaps due to a combination of the information being buried within a 7-hour jargon-filled presentation and our media being totally dysfunctional.

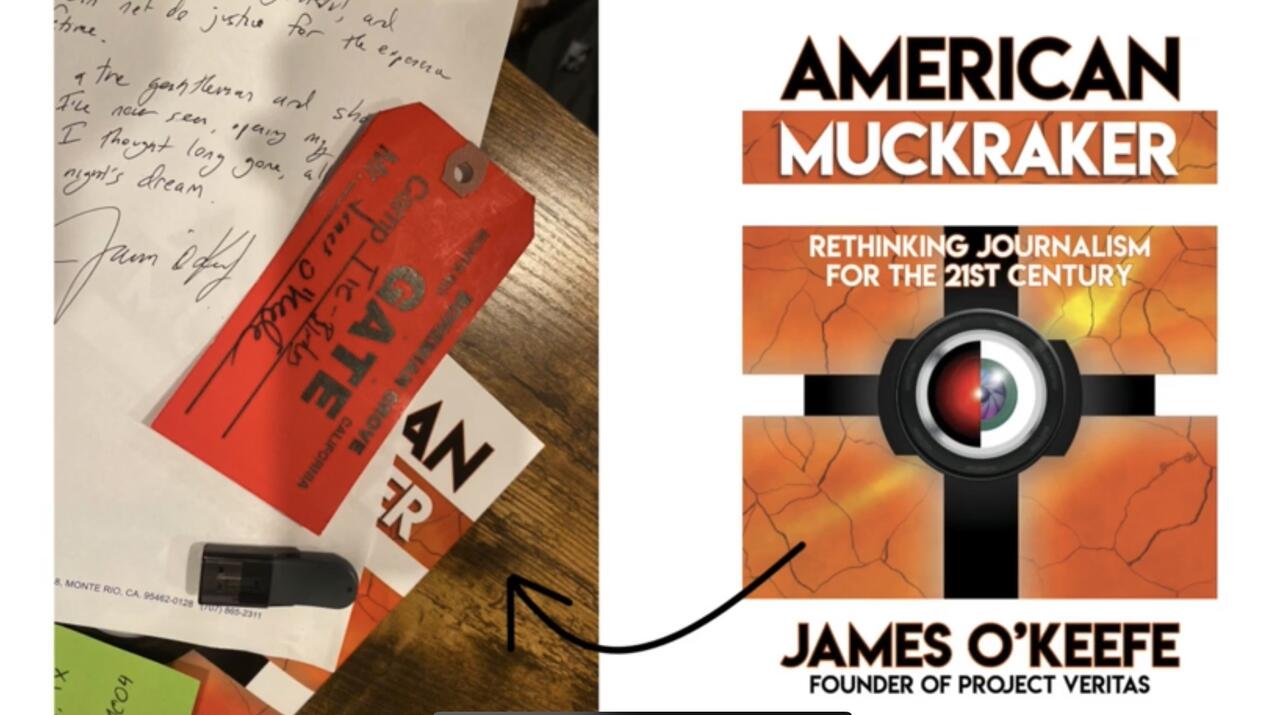

Bohemian Grove?

Leslie’s 2-hour long documentary on his experience at both Pfizer and O’Keefe’s companies concludes on an interesting note: James O’Keefe attended an outing at the Bohemian Grove.

Leslie offers this photo of James’ Bohemian Grove “GATE” slip as evidence, left on his work desk atop a copy of his book, “American Muckraker”:

My thoughts on the Bohemian Grove: my good friend’s dad was its general manager for several decades. From what I have gathered through that connection, the Bohemian Grove is not some version of the Illuminati, at least not in the institutional sense.

Do powerful elites hangout there? Absolutely. Do they discuss their plans for the world while hanging out there? I’m sure it has happened. Do they have a weird ritual with a giant owl? Yep, Alex Jones showed that to the world.

My perspective is based on conversations with my friend and my belief that his father is not lying to him. I could be wrong and am open to evidence — like if boxer Ryan Garcia decides to produce evidence regarding his rape claims — and I do find it a bit strange the club would invite O’Keefe who is notorious for covertly filming, but Occam’s razor would lead me to believe the club is — as it was under my friend’s dad — run by boomer conservatives the extent of whose politics include disliking wokeness, immigration, and Biden (common subjects of O’Keefe’s work).

Therefore, I don’t find O’Keefe’s visit to the club indicative that he is some sort of Operation Mockingbird asset as Leslie tries to depict (however Mockingbird is a 100% legitimate conspiracy). I have also met James several times and even came close to joining OMG. While I disagreed with James on the significance of many of his stories — finding some to be overhyped and showy — I never doubted his conviction in them.

As for why Leslie’s story was squashed… all my sources told me it was to avoid jail time for Veritas executives.

Feel free to watch Leslie’s full documentary here and decide for yourself.

Fun fact — Justin Leslie was also the operative behind this mega-viral Project Veritas story where Pfizer’s director of R&D claimed the company was privately mutating COVID-19 behind closed doors:

BREAKING: @Pfizer Exploring "Mutating" COVID-19 Virus For New Vaccines

"Don't tell anyone this...There is a risk...have to be very controlled to make sure this virus you mutate doesn't create something...the way that the virus started in Wuhan, to be honest."#DirectedEvolutionpic.twitter.com/xaRvlD5qTo

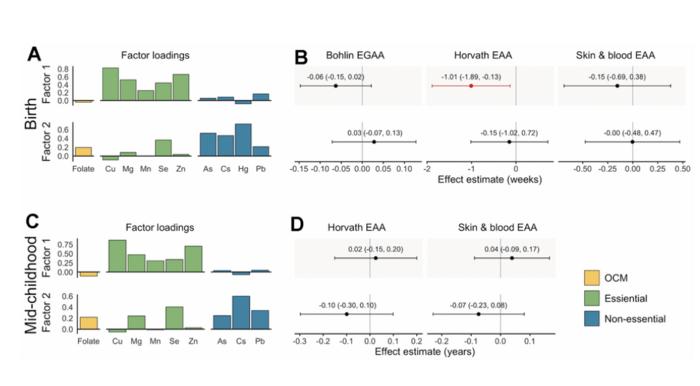

“[…] our findings support the hypothesis that the intrauterine environment, particularly essential and non-essential metals, affect epigenetic aging biomarkers across the life course.”

Credit: 2024 Bozack et al.

“[…] our findings support the hypothesis that the intrauterine environment, particularly essential and non-essential metals, affect epigenetic aging biomarkers across the life course.”

BUFFALO, NY- March 12, 2024 – A new research paper was published inAging (listed by MEDLINE/PubMed as “Aging (Albany NY)” and “Aging-US” by Web of Science) Volume 16, Issue 4, entitled, “Associations of prenatal one-carbon metabolism nutrients and metals with epigenetic aging biomarkers at birth and in childhood in a US cohort.”

Epigenetic gestational age acceleration (EGAA) at birth and epigenetic age acceleration (EAA) in childhood may be biomarkers of the intrauterine environment. In this new study, researchers Anne K. Bozack, Sheryl L. Rifas-Shiman, Andrea A. Baccarelli, Robert O. Wright, Diane R. Gold, Emily Oken, Marie-France Hivert, and Andres Cardenas from Stanford University School of Medicine, Harvard Medical School, Harvard T.H. Chan School of Public Health, Columbia University, and Icahn School of Medicine at Mount Sinai investigated the extent to which first-trimester folate, B12, 5 essential and 7 non-essential metals in maternal circulation are associated with EGAA and EAA in early life.

“[…] we hypothesized that OCM [one-carbon metabolism] nutrients and essential metals would be positively associated with EGAA and non-essential metals would be negatively associated with EGAA. We also investigated nonlinear associations and associations with mixtures of micronutrients and metals.”

Bohlin EGAA and Horvath pan-tissue and skin and blood EAA were calculated using DNA methylation measured in cord blood (N=351) and mid-childhood blood (N=326; median age = 7.7 years) in the Project Viva pre-birth cohort. A one standard deviation increase in individual essential metals (copper, manganese, and zinc) was associated with 0.94-1.2 weeks lower Horvath EAA at birth, and patterns of exposures identified by exploratory factor analysis suggested that a common source of essential metals was associated with Horvath EAA. The researchers also observed evidence of nonlinear associations of zinc with Bohlin EGAA, magnesium and lead with Horvath EAA, and cesium with skin and blood EAA at birth. Overall, associations at birth did not persist in mid-childhood; however, arsenic was associated with greater EAA at birth and in childhood.

“Prenatal metals, including essential metals and arsenic, are associated with epigenetic aging in early life, which might be associated with future health.”

Read the full paper: DOI:https://doi.org/10.18632/aging.205602

Corresponding Author: Andres Cardenas

Corresponding Email:andres.cardenas@stanford.edu

Keywords: epigenetic age acceleration, metals, folate, B12, prenatal exposures

Click here to sign up for free Altmetric alerts about this article.

About Aging:

Launched in 2009, Aging publishes papers of general interest and biological significance in all fields of aging research and age-related diseases, including cancer—and now, with a special focus on COVID-19 vulnerability as an age-dependent syndrome. Topics in Aging go beyond traditional gerontology, including, but not limited to, cellular and molecular biology, human age-related diseases, pathology in model organisms, signal transduction pathways (e.g., p53, sirtuins, and PI-3K/AKT/mTOR, among others), and approaches to modulating these signaling pathways.

Please visit our website at www.Aging-US.com and connect with us:

National insurance, income tax, VAT, capital gains tax, inheritance tax… it’s easy to get confused about the many different ways we contribute to the cost of running the country. The budget announcement is the key time each year when the government shares its financial plans with us all, and announces changes that may make a tangible difference to what you pay.

But you’ll likely be hearing a lot more about taxes in the coming months – promises to cut or raise them are an easy win (or lose) for politicians in an election year. We may even get at least one “mini-budget”.

If you’ve recently entered the workforce or the housing market, you may still be wrapping your mind around all of these terms. Here is what you need to know about the different types of taxes and how they affect you.

The UK broadly uses three ways to collect tax:

1. When you earn money

If you are an employee or own a business, taxes are deducted from your salary or profits you make. For most people, this happens in two ways: income tax, and national insurance contributions (or NICs).

If you are self-employed, you will have to pay your taxes via an annual tax return assessment. You might also have to pay taxes this way for interest you earn on savings, dividends (distribution of profits from a company or shares you own) received and most other forms of income not taxed before you get it.

VAT and excise duties are taxes on most goods and services you buy, with some exceptions like books and children’s clothing. About 20% of the total tax collected is VAT.

3. Taxes on wealth and assets

These are mainly taxes on the money you earn if you sell assets (like property or stocks) for more than you bought them for, or when you pass on assets in an inheritance. In the latter case in the UK, the recipient doesn’t pay this, it is the estate paying it out that must cover this if due. These taxes contribute only about 3% to the total tax collected.

You also likely have to pay council tax, which is set by the council you live in based on the value of your house or flat. It is paid by the user of the property, no matter if you own or rent. If you are a full-time student or on some apprenticeship schemes, you may get a deduction or not have to pay council tax at all.

This article is part of Quarter Life, a series about issues affecting those of us in our 20s and 30s. From the challenges of beginning a career and taking care of our mental health, to the excitement of starting a family, adopting a pet or just making friends as an adult. The articles in this series explore the questions and bring answers as we navigate this turbulent period of life.

Put together, these totalled almost £790 billion in 2022-23, which the government spends on public services such as the NHS, schools and social care. The government collects taxes from all sources and sets its spending plans accordingly, borrowing to make up any difference between the two.

Income tax

The amount of income tax you pay is determined by where your income sits in a series of “bands” set by the government. Almost everyone is entitled to a “personal allowance”, currently £12,570, which you can earn without needing to pay any income tax.

You then pay 20% in tax on each pound of income you earn (across all sources) from £12,570-£50,270. You pay 40% on each extra pound up to £125,140 and 45% over this. If you earn more than £100,000, the personal allowance (amount of untaxed income) starts to decrease.

If you are self-employed, the same rates apply to you. You just don’t have an employer to take this off your salary each month. Instead, you have to make sure you have enough money at the end of the year to pay this directly to the government.

The government can increase the threshold limits to adjust for inflation. This tries to ensure any wage rise you get in response to higher prices doesn’t lead to you having to pay a higher tax rate. However, the government announced in 2021 that they would freeze these thresholds until 2026 (extended now to 2028), arguing that it would help repay the costs of the pandemic.

Given wages are now rising for many to help with the cost of living crisis, this means many people will pay more income tax this coming year than they did before. This is sometimes referred to as “fiscal drag” – where lower earners are “dragged” into paying higher tax rates, or being taxed on more of their income.

National insurance

National insurance contributions (NICs) are a second “tax” you pay on your income – or to be precise, on your earned income (your salary). You don’t pay this on some forms of income, including savings or dividends, and you also don’t pay it once you reach state retirement age (currently 66).

While Jeremy Hunt, the current chancellor of the exchequer, didn’t adjust income tax meaningfully in this year’s budget, he did announce a cut to NICs. This was a surprise to many, as we had already seen rates fall from 12% to 10% on incomes higher than £242/week in January. It will now fall again to 8% from April.

While this is charged separately to income tax, in reality it all just goes into one pot with other taxes. Some, including the chancellor, say it is time to merge these two deductions and make this simpler for everyone. In his budget speech this year, Hunt said he’d like to see this tax go entirely. He thinks this isn’t fair on those who have to pay it, as it is only charged on some forms of income and on some workers.

I wouldn’t hold my breath for this to happen however, and even if it did, there are huge sums linked to NICs (nearly £180bn last year) so it would almost certainly have to be collected from elsewhere (such as via an increase in income taxes, or a lot more borrowing) to make sure the government could still balance its books.

There are likely to be further tweaks to the UK’s tax system soon, perhaps by the current government before the election – and almost certainly if there is a change of government.

Wealth taxes may be in line for a change. In the budget, the chancellor reduced capital gains taxes on sales of assets such as second properties (from 28% to 24%). These types of taxes provide only a limited amount of money to the government, as quite high thresholds apply for inheritance tax (up to £1 million if you are passing on a family home).

There are calls from many quarters though to look again at these types of taxes. Wealth inequality (the differences between total wealth held by the richest compared to the poorest) in the UK is very high (much higher than income inequality) and rising.

But how to do this effectively is a matter of much debate. A recent study suggested a one-off tax on total wealth held over a certain threshold might work. But wealth taxes are challenging to make work in practice, and both main political parties have already said this isn’t an option they are considering currently.

Andy Lymer and his colleagues at the Centre for Personal Financial Wellbeing at Aston University currently or have recently received funding for their research work from a variety of funding bodies including the UK's Money and Pension Service, the Aviva Foundation, Fair4All Finance, NEST Insight, the Gambling Commission, Vivid Housing and the ESRC, amongst others.

We use cookies on our website to give you the most relevant experience by remembering your preferences and repeat visits. By clicking “Accept”, you consent to the use of ALL the cookies.

This website uses cookies to improve your experience while you navigate through the website. Out of these, the cookies that are categorized as necessary are stored on your browser as they are essential for the working of basic functionalities of the website. We also use third-party cookies that help us analyze and understand how you use this website. These cookies will be stored in your browser only with your consent. You also have the option to opt-out of these cookies. But opting out of some of these cookies may affect your browsing experience.

Necessary cookies are absolutely essential for the website to function properly. These cookies ensure basic functionalities and security features of the website, anonymously.

Cookie

Duration

Description

cookielawinfo-checbox-analytics

11 months

This cookie is set by GDPR Cookie Consent plugin. The cookie is used to store the user consent for the cookies in the category "Analytics".

cookielawinfo-checbox-functional

11 months

The cookie is set by GDPR cookie consent to record the user consent for the cookies in the category "Functional".

cookielawinfo-checbox-others

11 months

This cookie is set by GDPR Cookie Consent plugin. The cookie is used to store the user consent for the cookies in the category "Other.

cookielawinfo-checkbox-necessary

11 months

This cookie is set by GDPR Cookie Consent plugin. The cookies is used to store the user consent for the cookies in the category "Necessary".

cookielawinfo-checkbox-performance

11 months

This cookie is set by GDPR Cookie Consent plugin. The cookie is used to store the user consent for the cookies in the category "Performance".

viewed_cookie_policy

11 months

The cookie is set by the GDPR Cookie Consent plugin and is used to store whether or not user has consented to the use of cookies. It does not store any personal data.

Functional cookies help to perform certain functionalities like sharing the content of the website on social media platforms, collect feedbacks, and other third-party features.

Performance cookies are used to understand and analyze the key performance indexes of the website which helps in delivering a better user experience for the visitors.

Analytical cookies are used to understand how visitors interact with the website. These cookies help provide information on metrics the number of visitors, bounce rate, traffic source, etc.

Advertisement cookies are used to provide visitors with relevant ads and marketing campaigns. These cookies track visitors across websites and collect information to provide customized ads.

{kind=link}