Uncategorized

The homebuilders got lucky this time

The homebuilders got lucky in the current recession since they don’t have to compete with millions of existing homes.

Share this:

Looking at the latest NAHB/Wells Fargo homebuilder confidence data and builder stock prices, I can say the homebuilders got very lucky this time around in the middle of a housing recession. There is one simple reason for this: it’s not 2008. They have less competition as they are working from low sales levels in today’s housing market.

The truth is that if mortgage rates fell below 5.875% and kept going lower, everyone’s housing predictions would need to be revised this year because the builders can sell their homes with lower mortgage rates. However, the glaring difference today versus the recession of 2008, is that in 2007 the builders had to deal with over 4 million active listings as competition for their pricey new homes.

Last year we had monthly existing home sales collapse back to 2007 levels, except this time around, NAR has total inventory at 970,000 and not over 4 million.

In an odd twist of fate, the delays due to COVID-19 are currently an infrastructure and jobs program for Americans in the construction industry. Let me explain my logic with today’s housing starts report.

Building permits

From Census: Building Permits: Privately-owned housing units authorized by building permits in January were at a seasonally adjusted annual rate of 1,339,000. This is 0.1 percent above the revised December rate of 1,337,000, but is 27.3 percent below the January 2022 rate of 1,841,000. Single-family authorizations in January were at a rate of 718,000; this is 1.8 percent below the revised December figure of 731,000. Authorizations of units in buildings with five units or more were at a rate of 563,000 in January.

As you can see in the chart below, housing permits are falling, new home sales are down, supply is up, and you don’t issue more housing permits in this environment. Homebuilders will only permit new housing when they don’t have excess supply and they know they can grow sales.

Housing starts: Privately-owned housing starts in January were at a seasonally adjusted annual rate of 1,309,000. This is 4.5 percent (±15.9 percent)* below the revised December estimate of 1,371,000 and is 21.4 percent (±10.6 percent) below the January 2022 rate of 1,666,000. Single-family housing starts in January were at a rate of 841,000; this is 4.3 percent (±16.4 percent)* below the revised December figure of 879,000. The January rate for units in buildings with five units or more was 457,000.

As housing permits fall, as you can see below, housing starts also fall, so nothing is abnormal here with the housing data while in a recession.

Now comes the abnormal data line: housing completions. This is so slow my tortoise would look like the flash against this data line.

Housing completions: Privately-owned housing completions in January were at a seasonally adjusted annual rate of 1,406,000. This is 1.0 percent (±9.8 percent)* above the revised December estimate of 1,392,000 and is 12.8 percent (±13.0 percent)* above the January 2022 rate of 1,247,000. Single-family housing completions in January were at a rate of 1,040,000; this is 4.4 percent (±10.4 percent)* above the revised December rate of 996,000. The January rate for units in buildings with five units or more was 349,000.

As you can see below, housing completions are slowly moving along; the homebuilders have more new homes under construction that they haven’t even started yet than active new homes for sale. While the two charts above are falling noticeably, housing completion data is slowly moving up. This is why construction workers haven’t been laid off while other jobs in the housing market have been.

Let me be honest here: we got lucky as a country. If the homebuilders and homebuyers knew rates would hit 7% in 2022, many would not have taken those contracts they’re canceling now. This means the builders would not have even considered taking permits out for those homes. So, for now, we are simply working through that backlog, which means we have more housing supply and construction workers are still employed.

However, to my first point, the builders are lucky that total housing inventory is near all-time lows because this means their product holds more value. Buyers have fewer choices than normal in the past eight years — but in reality, since 1982.

Homebuilders confidence

The homebuilder’s confidence index has picked up in the last two months, and three months ago, their forward-looking survey looked positive. I am not shocked that forward-looking housing data works again. As I have tried to highlight in my economic work, the housing market started to improve on Nov. 9, so we have three months of positive data trends filtering into the monthly housing reports now.

However, I tried to bring some context into this discussion on CNBC last Monday. Even though the housing data has improved, it needs to be understood in context from working off a historical dive in 2022.

Historically speaking, when you see a bounce in the homebuilder’s index like this, it tells us the economic recession is ending, or at least the housing recession has ended. However, I caution people not to look at it this way since the U.S. economy isn’t in recession today, and mortgage rates have risen almost 1% from the recent lows.

New home sales

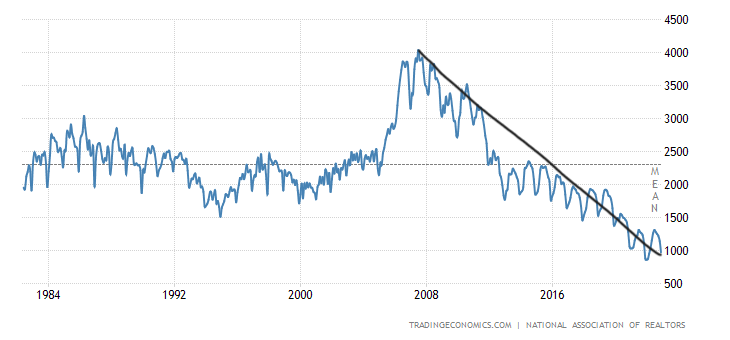

Next up is the new home sales report that comes out next week, so let’s check on how the monthly supply for the builders looks before the report. In the last report, the builders had 9.0 months’ supply, as the chart below shows.

Here’s the breakout:

- 71,000 new homes have been completed: 1.4 months of supply.

- 291,000 homes are still under construction: 5.7 months of supply

- 99,000 homes have yet to be started: 1.9 months of supply

My rule of thumb for anticipating builder behavior is based on the three-month supply average. This has nothing to do with the existing home sales market; this monthly supply data only applies to the new home sales market, and the current nine months are too high for them to issue new permits.

- When supply is 4.3 months, and below, this is an excellent market for builders.

- When supply is 4.4 to 6.4 months, this is an OK market for the builders. They will build as long as new home sales are growing.

- The builders will pull back on construction when the supply is 6.5 months and above.

Still, the builders have some work to do, and thankfully they’re keeping construction workers employed while working off their backlog.

Homebuilders are efficient sellers of homes because it’s like a commodity to them; they don’t have to look for shelter after they sell or have a 3% mortgage rate they have to give up after they sell.

Back to the basics

Lower mortgage rates are good for the housing market, and higher rates are bad; we are back to basic affordability demand here. Just look at the chart below and how bad credit looked from 2005 to 2008, then the job loss recession happened. This chart is a direct link to the excess supply that the homebuilders don’t have to deal with today.

Also, look how small the data looks in the bottom corner right If you need your glasses, I don’t blame you.

Today, homeowners look great on paper. In an inflationary environment of rising wages they have fixed long-term debt. The American home and its fixed long-term debt cost has been the best hedge against inflation.

Now, the question is: How much longer can this last? People buy and sell homes every year and total inventory growth can happen over time as homes stay on the market longer and longer. With mortgage rates up again, this can lead to inventory growing higher when homes take longer to sell.

Last year new listing growth turned negative year over year when rates got over 6%; now with rates rising into the spring season, we will see a lack of enthusiasm from sellers.

recession covid-19 link home sales mortgage rates housing market recessionUncategorized

One city held a mass passport-getting event

A New Orleans congressman organized a way for people to apply for their passports en masse.

Share this:

While the number of Americans who do not have a passport has dropped steadily from more than 80% in 1990 to just over 50% now, a lack of knowledge around passport requirements still keeps a significant portion of the population away from international travel.

Over the four years that passed since the start of covid-19, passport offices have also been dealing with significant backlog due to the high numbers of people who were looking to get a passport post-pandemic.

Related: Here is why it is (still) taking forever to get a passport

To deal with these concurrent issues, the U.S. State Department recently held a mass passport-getting event in the city of New Orleans. Called the "Passport Acceptance Event," the gathering was held at a local auditorium and invited residents of Louisiana’s 2nd Congressional District to complete a passport application on-site with the help of staff and government workers.

'Come apply for your passport, no appointment is required'

"Hey #LA02," Rep. Troy A. Carter Sr. (D-LA), whose office co-hosted the event alongside the city of New Orleans, wrote to his followers on Instagram (META) . "My office is providing passport services at our #PassportAcceptance event. Come apply for your passport, no appointment is required."

More Travel:

- A new travel term is taking over the internet (and reaching airlines and hotels)

- The 10 best airline stocks to buy now

- Airlines see a new kind of traveler at the front of the plane

The event was held on March 14 from 10 a.m. to 1 p.m. While it was designed for those who are already eligible for U.S. citizenship rather than as a way to help non-citizens with immigration questions, it helped those completing the application for the first time fill out forms and make sure they have the photographs and identity documents they need. The passport offices in New Orleans where one would normally have to bring already-completed forms have also been dealing with lines and would require one to book spots weeks in advance.

These are the countries with the highest-ranking passports in 2024

According to Carter Sr.'s communications team, those who submitted their passport application at the event also received expedited processing of two to three weeks (according to the State Department's website, times for regular processing are currently six to eight weeks).

While Carter Sr.'s office has not released the numbers of people who applied for a passport on March 14, photos from the event show that many took advantage of the opportunity to apply for a passport in a group setting and get expedited processing.

Every couple of months, a new ranking agency puts together a list of the most and least powerful passports in the world based on factors such as visa-free travel and opportunities for cross-border business.

In January, global citizenship and financial advisory firm Arton Capital identified United Arab Emirates as having the most powerful passport in 2024. While the United States topped the list of one such ranking in 2014, worsening relations with a number of countries as well as stricter immigration rules even as other countries have taken strides to create opportunities for investors and digital nomads caused the American passport to slip in recent years.

A UAE passport grants holders visa-free or visa-on-arrival access to 180 of the world’s 198 countries (this calculation includes disputed territories such as Kosovo and Western Sahara) while Americans currently have the same access to 151 countries.

stocks pandemic covid-19 grantsUncategorized

Fast-food chain closes restaurants after Chapter 11 bankruptcy

Several major fast-food chains recently have struggled to keep restaurants open.

Share this:

Competition in the fast-food space has been brutal as operators deal with inflation, consumers who are worried about the economy and their jobs and, in recent months, the falling cost of eating at home.

Add in that many fast-food chains took on more debt during the covid pandemic and that labor costs are rising, and you have a perfect storm of problems.

It's a situation where Restaurant Brands International (QSR) has suffered as much as any company.

Related: Wendy's menu drops a fan favorite item, adds something new

Three major Burger King franchise operators filed for bankruptcy in 2023, and the chain saw hundreds of stores close. It also saw multiple Popeyes franchisees move into bankruptcy, with dozens of locations closing.

RBI also stepped in and purchased one of its key franchisees.

"Carrols is the largest Burger King franchisee in the United States today, operating 1,022 Burger King restaurants in 23 states that generated approximately $1.8 billion of system sales during the 12 months ended Sept. 30, 2023," RBI said in a news release. Carrols also owns and operates 60 Popeyes restaurants in six states."

The multichain company made the move after two of its large franchisees, Premier Kings and Meridian, saw multiple locations not purchased when they reached auction after Chapter 11 bankruptcy filings. In that case, RBI bought select locations but allowed others to close.

Image source: Chen Jianli/Xinhua via Getty

Another fast-food chain faces bankruptcy problems

Bojangles may not be as big a name as Burger King or Popeye's, but it's a popular chain with more than 800 restaurants in eight states.

"Bojangles is a Carolina-born restaurant chain specializing in craveable Southern chicken, biscuits and tea made fresh daily from real recipes, and with a friendly smile," the chain says on its website. "Founded in 1977 as a single location in Charlotte, our beloved brand continues to grow nationwide."

Like RBI, Bojangles uses a franchise model, which makes it dependent on the financial health of its operators. The company ultimately saw all its Maryland locations close due to the financial situation of one of its franchisees.

Unlike. RBI, Bojangles is not public — it was taken private by Durational Capital Management LP and Jordan Co. in 2018 — which means the company does not disclose its financial information to the public.

That makes it hard to know whether overall softness for the brand contributed to the chain seeing its five Maryland locations after a Chapter 11 bankruptcy filing.

Bojangles has a messy bankruptcy situation

Even though the locations still appear on the Bojangles website, they have been shuttered since late 2023. The locations were operated by Salim Kakakhail and Yavir Akbar Durranni. The partners operated under a variety of LLCs, including ABS Network, according to local news channel WUSA9.

The station reported that the owners face a state investigation over complaints of wage theft and fraudulent W2s. In November Durranni and ABS Network filed for bankruptcy in New Jersey, WUSA9 reported.

"Not only do former employees say these men owe them money, WUSA9 learned the former owners owe the state, too, and have over $69,000 in back property taxes."

Former employees also say that the restaurant would regularly purchase fried chicken from Popeyes and Safeway when it ran out in their stores, the station reported.

Bojangles sent the station a comment on the situation.

"The franchisee is no longer in the Bojangles system," the company said. "However, it is important to note in your coverage that franchisees are independent business owners who are licensed to operate a brand but have autonomy over many aspects of their business, including hiring employees and payroll responsibilities."

Kakakhail and Durranni did not respond to multiple requests for comment from WUSA9.

bankruptcy pandemicUncategorized

Industrial Production Increased 0.1% in February

From the Fed: Industrial Production and Capacity Utilization

Industrial production edged up 0.1 percent in February after declining 0.5 percent in January. In February, the output of manufacturing rose 0.8 percent and the index for mining climbed 2.2 p…

Share this:

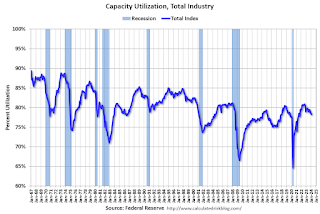

Industrial production edged up 0.1 percent in February after declining 0.5 percent in January. In February, the output of manufacturing rose 0.8 percent and the index for mining climbed 2.2 percent. Both gains partly reflected recoveries from weather-related declines in January. The index for utilities fell 7.5 percent in February because of warmer-than-typical temperatures. At 102.3 percent of its 2017 average, total industrial production in February was 0.2 percent below its year-earlier level. Capacity utilization for the industrial sector remained at 78.3 percent in February, a rate that is 1.3 percentage points below its long-run (1972–2023) average.Click on graph for larger image.

emphasis added

{kind=link}

This graph shows Capacity Utilization. This series is up from the record low set in April 2020, and above the level in February 2020 (pre-pandemic).

Capacity utilization at 78.3% is 1.3% below the average from 1972 to 2022. This was below consensus expectations.

Note: y-axis doesn't start at zero to better show the change.

The second graph shows industrial production since 1967.

The second graph shows industrial production since 1967.Industrial production increased to 102.3. This is above the pre-pandemic level.

Industrial production was above consensus expectations.

Key shipping company files for Chapter 11 bankruptcy

These Cities Have The Highest (And Lowest) Share Of Unaffordable Neighborhoods In 2024

The Question You Should Ask Whenever You’re Wrong

Tight inventory and frustrated buyers challenge agents in Virginia

Industrial Production Increased 0.1% in February

Your financial plan may be riskier without bitcoin

Key shipping company files Chapter 11 bankruptcy

One city held a mass passport-getting event

Southwest and United Airlines have bad news for passengers

The hostility Black women face in higher education carries dire consequences

-

Uncategorized3 weeks ago

Uncategorized3 weeks agoAll Of The Elements Are In Place For An Economic Crisis Of Staggering Proportions

-

International1 week ago

International1 week agoEyePoint poaches medical chief from Apellis; Sandoz CFO, longtime BioNTech exec to retire

-

Uncategorized4 weeks ago

Uncategorized4 weeks agoCalifornia Counties Could Be Forced To Pay $300 Million To Cover COVID-Era Program

-

Uncategorized3 weeks ago

Uncategorized3 weeks agoApparel Retailer Express Moving Toward Bankruptcy

-

Uncategorized4 weeks ago

Uncategorized4 weeks agoIndustrial Production Decreased 0.1% in January

-

International1 week ago

International1 week agoWalmart launches clever answer to Target’s new membership program

-

Spread & Containment3 days ago

Spread & Containment3 days agoIFM’s Hat Trick and Reflections On Option-To-Buy M&A

-

Uncategorized4 weeks ago

Uncategorized4 weeks agoRFK Jr: The Wuhan Cover-Up & The Rise Of The Biowarfare-Industrial Complex