"London calling to the Zombies of death, quit holding out and draw another breath”

Let’s talk about the Working from Home revolution – and what it might mean for markets and finance.

The City of London is the Capital of Global Finance. Together with satellites in the West End and Canary Wharf, Finance and The City employs some 500,000 of the highest paid workers in the UK, paying over £100 bln in taxes (business and personal) each year. There is more shiny bright new office space visible from our office windows in the Walkie Talkie, (which I bet still haven’t been cleaned since I last looked out of them in March), than you can shake a sharp pointy stick at.

The pandemic may be easing, but the City is still a Ghost Town. Tumbleweed blows down the streets. Lowest common denominator junk food vendor Greggs is about the only place open. (Seriously, their steak slices are to die for.) I’ve not been up myself, but She-who-is-Mrs-Blain was pretty shocked.

The news JP Morgan and the magic circle Law Firm Linklaters are ending the daily commute and telling staff to telework from work and in the office actually confirms the massive changes underway in how we work in global finance will be fairly limited. Staff will still be expected to come into the office regularly. Other firms, including Schroders, report work-from-home (WFH) has been a stunning success – with their business flourishing – they say. However, I’m told “freedom” for staff to WFH will be at their managers discretion.

On the other hand, a chum who runs an office-logistics firm tells me they are busy as London trading floors are being converted into flexible workspace while rows of desks are being consumed by new meeting rooms.

Although we hit peak WFH months ago, less than 35% of British office workers have returned to work. That compares to 83% of French employees de bureau. Personally, I suspect the main reason keeping staff from returning to their London offices is the misery of commuting. If WFJ works… then why take COVID risks on London’s dirty, filthy, unreliable and massively overcrowded rail and tube networks? When I go back to London I will relying on my Brompton bike for in-town travel.

However, I suspect the Pandemic will act as a catalyst to accelerate changes in Finance – which are going to have some long-term fairly unsettling effects on a large portion of the workforce. I expect the “accelerant” effect of COVID in changing/shaking industry and commerce will prove its most lasting bequest to us all.

Therefore, I award myself a “No Sh*t Sherlock”prize for realising the City is going to be massively changed by the Pandemic. We’ve seen predictions about the end of the modern office but its only now we’re beginning to see facts emerge. For instance, JP Morgan will be closing their Basinggrad office (Basingstoke to those of you who don’t commute) because they now know WFH makes recovery sites redundant.

Like most things in finance, the hyperbole and dystopian outlook of a permanently empty City is overblown. There will be changes, but it won’t be the end of everything. Over the last few days I’ve been asking clients and market contacts what they think the future holds for the Financial Industry, Teleworking, the Office and how Investments and the Market will be impacted by the coming evolution of the financial sector.

Let’s start with working from home.

Teleworking has pros and cons. It tends to be generational. Younger workers stuck in small London flats quickly went crazy and couldn’t wait to get back to work. Older workers have convinced themselves they’re working hard while finding time to go for long walks and do the garden.

When lockdown began there were serious regulatory concerns about how financial business could be conducted from home rather than controlled city locations. The head of one of the UK’s most important and influential institutions told me he’d been very concerned about trades being done in “another person’s shed” rather than the office, but that “after my hand was forced, I have to admit it’s worked rather well.” The same chap notes nothing will replace the “City Lunch” or the chance meeting as the sparks where business and ideas germinate.

I’ve written a few times about missing my “broker ear”, the ability to listen in to office conversations to sense what was occurring in the market, but to be honest, that was more 1980s-2010s. Since then offices have become far less energetic, and the language which conveyed the emotion of markets has been sensitised. I can learn what I need on calls.

On the other hand, humans are evolved social creatures. We thrive in company. We aren’t so good in solitary – which is why it’s a punishment. We need social impetus – the stimulus of discussions and arguments sparking ideas on the desk, driving the creativity and problem-solving that’s made the UK financial services sector such a success. No one is taught how to be a City financier – you learn through a process of osmosis in the office – “it can’t be learnt in half-hour Zoom calls”, said a client.

We also need threat – the knowledge that underperformance could cost us our jobs, and that younger staff want our salaries and to sit in our seats. If there is no sense of threat, people work less hard – fact. (That’s why bureaucracies ultimately kill economies.) I would argue competition with colleagues is the biggest driver of success in finance. Another client pointed out: “firms that pair back on analyst and associate programmes see a noticeable decline in output.” Fear of obsolescence and burn-out is a vital component of success.

Competition is also evident at firm level where the speed at which staff are returning to the office is a function of moral and the character of individual firms. It’s a form of resilience. I hear that over 50% of Goldman Sachs were back in the office the moment the doors opened – The Vampyre Squid is feeding them and offering free child-care. Smart. I reckon if we could chart returnees for each bank it would correlate directly with how successful the bank is perceived to be. (Please don’t tell me Deutsche Bank is already back in situ?)

At the other end of the scale, trying to get hold of a retail bank staff at high-street banks is still impossible – they were demotivated and bored before the crisis, and it’s just got even less interesting for them. If they can say they are anxious and stay at home, why wouldn’t they? I am so peeved with my bank making excuses blaming the virus as explaining why no one could help me chase missing money.

Then there is the importance of being present in an office. When it comes to awarding important new business, or investing in a fund, the principals are under a duty of care, which using includes “onsite due diligence” – meaning having a swanky office at a top City or Mayfair address that looks busy is still important.

WFH vs Office is bound to raise work-life balance questions. A senior European fund manager in London told me his younger European staff are seriously considering moving home – not because of Brexit, but because the whole point of being in London is because its so much more exciting than Frankfurt, Milan, Madrid or Paris. If it’s not, and London’s cultural menu is effectively zero at present, then working in Munchen - where a 10 min cycle gets you to a beer garden in the countryside - feels much more attractive.

On balance, WFH works, but isn’t ideal. I suspect we will all move towards an office/home mix. That will be determined through experimentation and common sense. My own intention is certainly to get back in the office regularly, and to resume face-to-face client meetings as soon as possible. (Meanwhile, you can see watch my videos on https://morningporridge.com/videoif you are missing my face!)

Technical issues reopening buildings

There are good reasons why more City staff haven’t yet returned. Technical problems about distancing have to be resolved before offices can reopen. Many clients tell me they have been unable to return to their offices because building owners haven’t figured out how to ramp up the air conditioning to cope with the number of people and new recommendations on ventilation, or how to get people to their working floors when lifts can only carry 3 passengers at a time. Its physically impossible to get 600 people onto a trading floor at 7.30 am when only 4 lifts service the floor.

The reality is London’s office towers were designed for a normal business environment. If the pandemic really means we have to keep social distancing and restrict numbers – then they just don’t work anymore. We will need a vaccine, or the bravery to agree the virus risks are manageable, the disease treatable, before we reopen them fully. Tower Block Offices don’t lend themselves to compromises. The future of the tower block office depends on what the post-Covid analysis says about the efficacy of lockdowns and distancing.

It’s clear there will be an impact on office demand. A senior banker told me he expects to cut the number of desks by 1/3rdand institute a hot-desk policy for rotating staff each day. If that’s replicated across the City, then demand for office space drops at least 1/3rd.

Perhaps the biggest loser is WeWork – they would have taken a thumping from cancelled desks at the start of Lockdown, but could have been marvellously positioned to reap rewards as small and mid-sized firms actually give up on offices completely. Perhaps it’s a business idea to think about: “WeWork2: this time we’re serious…”

The knock-on effects…

The services the City demands are massive. It’s not just shops and catering, but also supports such as travel. Bankers are not travelling to meet clients. Boards are doing meetings by Zoom. Conferences and Events have been cancelled. At least one senior city figure is delighted – “It all saves on the bottom line, and these fripperies never added to the bottom line. We did corporate hostility because everyone else did it.”

While losing the expertise of “event-managers” is unlikely to kill the City, the potential loss of skilled deal facilitators who become sidelined, like lawyers, accountants, media-advisors and digital IT geeks could prove highly significant. If they stay away in droves, choose to go elsewhere, or simply aren’t trained.. then London’s financial sector will be in serious crisis.

And then there are the cost implications. Large firms have the reserves to maintain their half-full trophy offices, but smaller firms being battered by the effects of the pandemic are going to struggle – leading to an inevitable glut of property as they fold or exit. The pandemic is culling smaller firms - which is a serious loss of future genetic diversity for the City.

The actual financial impact of WFH is going to be felt hardest in the Insurance Real Money sector – these firms have become the largest owners and funders of commercial property, although I’m hearing Chinese banks are going to take a serious bath as well. Landlords are doing rent deals because it’s better to have a tenanted office than an empty one! As they say: “The best tenant is the current tenant!” Expectations of high returns on prestige City Tower Blocks have tumbled. The effect is going to be most visible on UK pension and insurance companies performance – which means on the retirement savings of the workforce..

.. will change the Financial Industry

As I wrote earlier the Pandemic and teleworking are just accelerating trends that were already underway in finance.

The strengths of financial experience and creativity that led the boom in financial services has been under the regulatory cosh for the last 15 years. Don’t kid yourselves, but being a fund manager today isn’t the era of financial buccaneer spirit I encountered in the 1980s. Today, most City jobs are largely about box-ticking, regulatory oversight, and compliance – and the objective is to not be beaten by dumb indices. QE Infinity and ZIRP have dulled the game.

The fact most firms have apparently done well during lockdown could well expose a brutal truth:

“their basic worthlessness has been exposed by forced absenteeism without any consequence to the bottom line”, a fund manager told me.

Ouch.

It’s likely to get worse. We’ve known for years that automation and AI is going to eat into middle class professions. Bond salesmen are pretty much already dinosaurs in a market where the big funds have to buy everything anyway, and AI determines portfolio compositions to beat the indexes. Jobs are going to go – meaning the ecosystem of the City is going to contract. Even writers of financial commentary…. I can’t be replicated (!) but if no one is left to read me, I am equally redundant! (Perhaps I shall start to write the porridge in binary to make it easy for investment-bots?)

Using the cover of cost savings due to the pandemic, I expect to see at least 10% of City Staff culled by the end of the year. The numbers being let go will keep rising next year. That's a serious disincentive to new joiners, and the energy levels of the City will drop accordingly.

And then there is the effect of the Pandemic stifling innovation. Let’s assume you just had a brilliant idea that’s going to make Finance exciting, renumerative and deliver excellent above market returns, but you current employer can’t do it because “it’s not in mandate”, “compliance say no”, or “we are concerned about ESG/Mifid/SEC (delete where applicable)”. Your chances of funding and launching that brilliant idea aren’t looking good. Instead the older City dinosaurs that were being kept alive by regulatory constipation, will retain their dominance because the efforts to contain the pandemic enables them to survive when Darwin says they perish!

And we need brilliant ideas, because the challenge to the City today is simple. We exist In a global financial marketplace where returns have been minimised and risks maximised by interest rate repression and QE Infinity – how do you generate meaningful returns to finance retirement and growth?

"I Can't Even Save": Americans Are Getting Absolutely Crushed Under Enormous Debt Load

While Joe Biden insists that Americans are doing great - suggesting in his State of the Union Address last week that "our economy is the envy of the world," Americans are being absolutely crushed by inflation (which the Biden admin blames on 'shrinkflation' and 'corporate greed'), andof course - crippling debt.

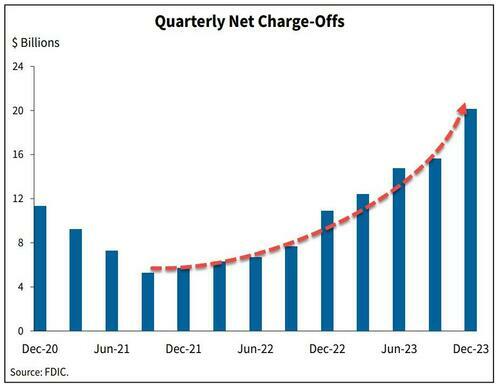

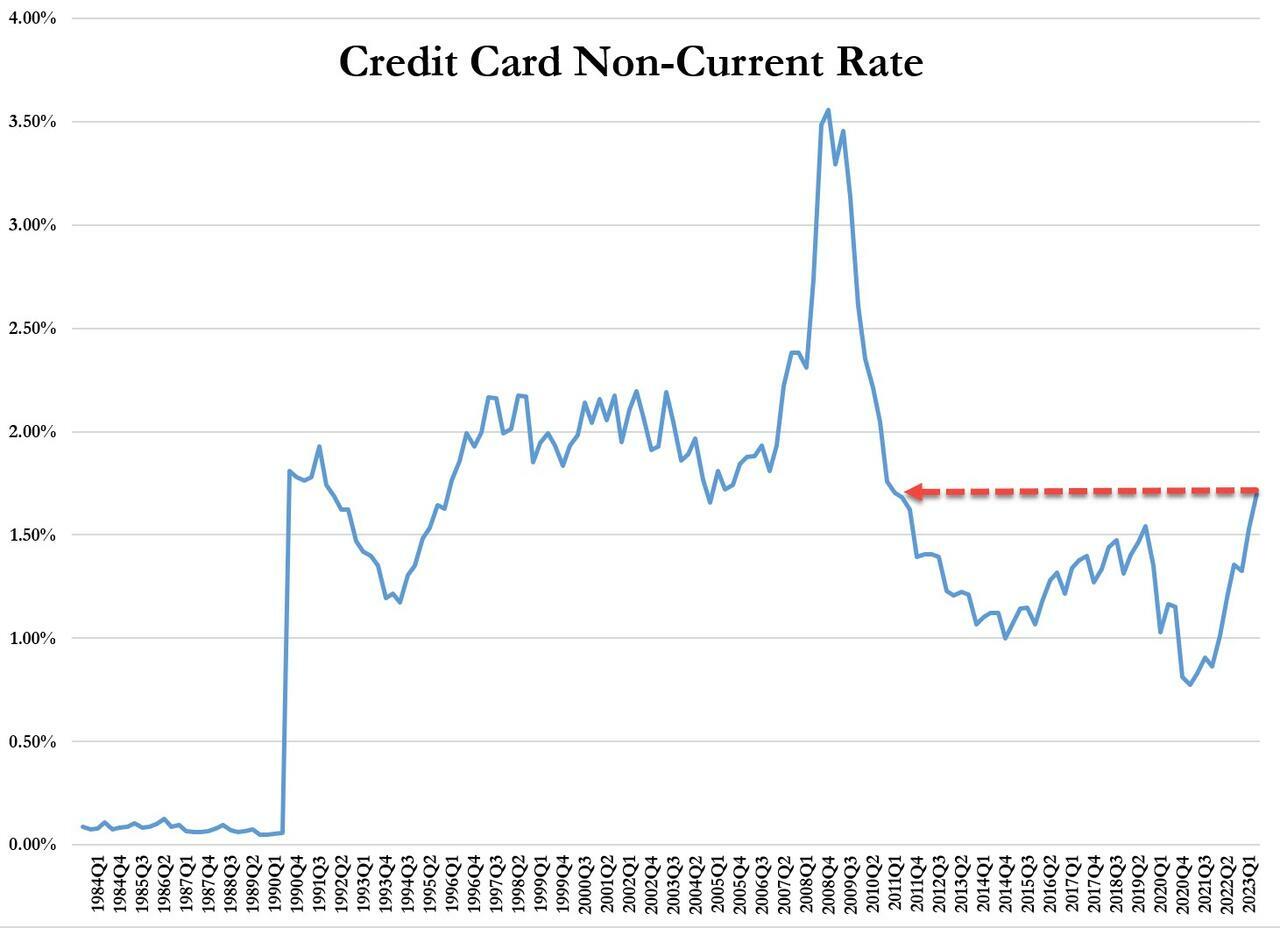

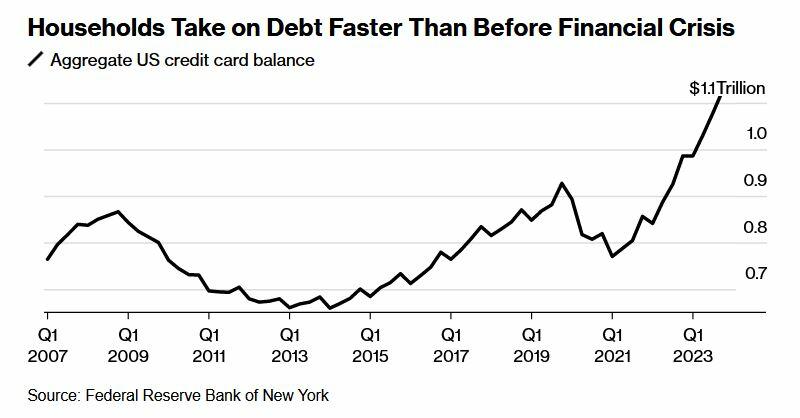

The signs are obvious. Last week we noted that banks' charge-offs are accelerating, and are now above pre-pandemic levels.

...and leading this increase are credit card loans - with delinquencies that haven't been this high since Q3 2011.

On top of that, while credit cards and nonfarm, nonresidential commercial real estate loans drove the quarterly increase in the noncurrent rate, residential mortgages drove the quarterly increase in the share of loans 30-89 days past due.

And while Biden and crew can spin all they want, an average of polls from RealClear Politics shows that just 40% of people approve of Biden's handling of the economy.

Crushed

On Friday, Bloomberg dug deeper into the effects of Biden's "envious" economy on Americans - specifically, how massive debt loads (credit cards and auto loans especially) are absolutely crushing people.

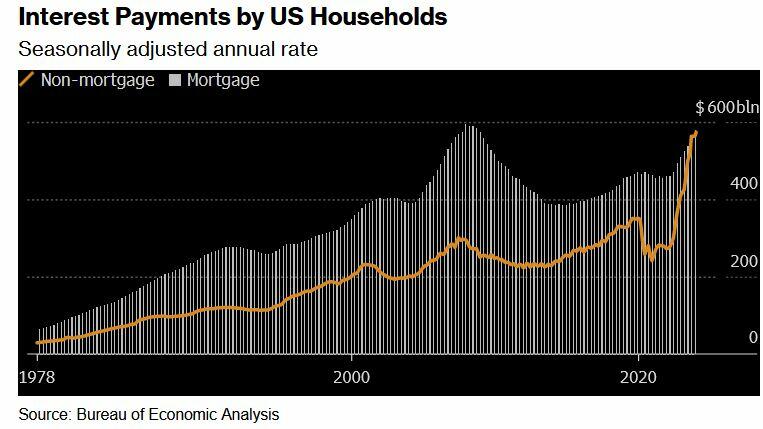

Two years after the Federal Reserve began hiking interest rates to tame prices, delinquency rates on credit cards and auto loans are the highest in more than a decade. For the first time on record, interest payments on those and other non-mortgage debts are as big a financial burden for US households as mortgage interest payments.

According to the report, this presents a difficult reality for millions of consumers who drive the US economy - "The era of high borrowing costs — however necessary to slow price increases — has a sting of its own that many families may feel for years to come, especially the ones that haven’t locked in cheap home loans."

The Fed, meanwhile, doesn't appear poised to cut rates until later this year.

According to a February paper from IMF and Harvard, the recent high cost of borrowing - something which isn't reflected in inflation figures, is at the heart of lackluster consumer sentiment despite inflation having moderated and a job market which has recovered (thanks to job gains almost entirely enjoyed by immigrants).

In short, the debt burden has made life under President Biden a constant struggle throughout America.

"I’m making the most money I've ever made, and I’m still living paycheck to paycheck," 40-year-old Denver resident Nikki Cimino told Bloomberg. Cimino is carrying a monthly mortgage of $1,650, and has $4,000 in credit card debt following a 2020 divorce.

"There's this wild disconnect between what people are experiencing and what economists are experiencing."

CBS: Do you attribute the inflation crisis to the pandemic or Biden?

WISCONSIN VOTER: "It's been YEARS now since the pandemic — I'm not buying that anymore. At first I did; I'm not buying that anymore because yogurt is STILL going up in price!" pic.twitter.com/apahb65scB

What's more, according to Wells Fargo, families have taken on debt at a comparatively fast rate - no doubt to sustain the same lifestyle as low rates and pandemic-era stimmies provided. In fact, it only took four years for households to set a record new debt level after paying down borrowings in 2021 when interest rates were near zero.

Meanwhile, that increased debt load is exacerbated by credit card interest rates that have climbed to a record 22%, according to the Fed.

[P]art of the reason some Americans were able to take on a substantial load of non-mortgage debt is because they’d locked in home loans at ultra-low rates, leaving room on their balance sheets for other types of borrowing. The effective rate of interest on US mortgage debt was just 3.8% at the end of last year.

Yet the loans and interest payments can be a significant strain that shapes families’ spending choices. -Bloomberg

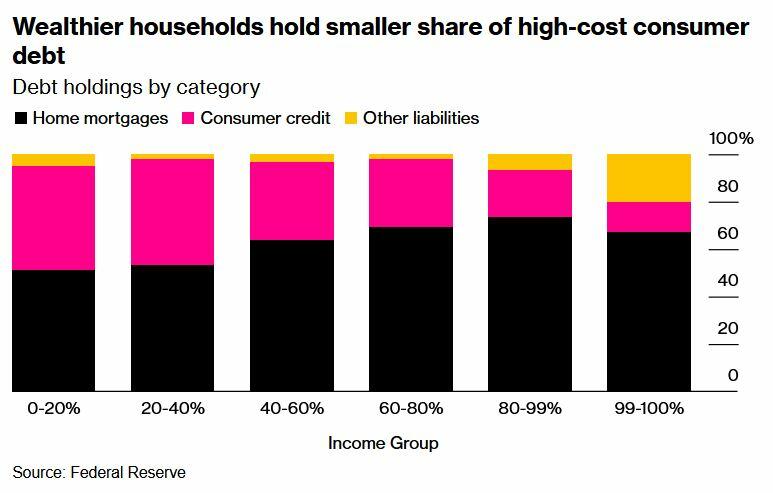

And of course, the highest-interest debt (credit cards) is hurting lower-income households the most, as tends to be the case.

The lowest earners also understandably had the biggest increase in credit card delinquencies.

"Many consumers are levered to the hilt — maxed out on debt and barely keeping their heads above water," Allan Schweitzer, a portfolio manager at credit-focused investment firm Beach Point Capital Management told Bloomberg. "They can dog paddle, if you will, but any uptick in unemployment or worsening of the economy could drive a pretty significant spike in defaults."

"We had more money when Trump was president," said Denise Nierzwicki, 69. She and her 72-year-old husband Paul have around $20,000 in debt spread across multiple cards - all of which have interest rates above 20%.

During the pandemic, Denise lost her job and a business deal for a bar they owned in their hometown of Lexington, Kentucky. While they applied for Social Security to ease the pain, Denise is now working 50 hours a week at a restaurant. Despite this, they're barely scraping enough money together to service their debt.

The couple blames Biden for what they see as a gloomy economy and plans to vote for the Republican candidate in November. Denise routinely voted for Democrats up until about 2010, when she grew dissatisfied with Barack Obama’s economic stances, she said. Now, she supports Donald Trump because he lowered taxes and because of his policies on immigration. -Bloomberg

Meanwhile there's student loans - which are not able to be discharged in bankruptcy.

"I can't even save, I don't have a savings account," said 29-year-old in Columbus, Ohio resident Brittany Walling - who has around $80,000 in federal student loans, $20,000 in private debt from her undergraduate and graduate degrees, and $6,000 in credit card debt she accumulated over a six-month stretch in 2022 while she was unemployed.

"I just know that a lot of people are struggling, and things need to change," she told the outlet.

The only silver lining of note, according to Bloomberg, is that broad wage gains resulting in large paychecks has made it easier for people to throw money at credit card bills.

Yet, according to Wells Fargo economist Shannon Grein, "As rates rose in 2023, we avoided a slowdown due to spending that was very much tied to easy access to credit ... Now, credit has become harder to come by and more expensive."

According to Grein, the change has posed "a significant headwind to consumption."

Then there's the election

"Maybe the Fed is done hiking, but as long as rates stay on hold, you still have a passive tightening effect flowing down to the consumer and being exerted on the economy," she continued. "Those household dynamics are going to be a factor in the election this year."

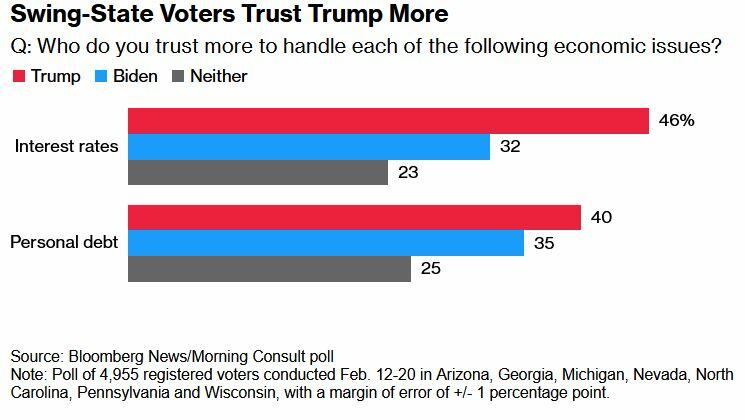

Meanwhile, swing-state voters in a February Bloomberg/Morning Consult poll said they trust Trump more than Biden on interest rates and personal debt.

Reverberations

These 'headwinds' have M3 Partners' Moshin Meghji concerned.

"Any tightening there immediately hits the top line of companies," he said, noting that for heavily indebted companies that took on debt during years of easy borrowing, "there's no easy fix."

Sylvester researchers, collaborators call for greater investment in bereavement care

MIAMI, FLORIDA (March 15, 2024) – The public health toll from bereavement is well-documented in the medical literature, with bereaved persons at greater…

MIAMI, FLORIDA (March 15, 2024) – The public health toll from bereavement is well-documented in the medical literature, with bereaved persons at greater risk for many adverse outcomes, including mental health challenges, decreased quality of life, health care neglect, cancer, heart disease, suicide, and death. Now, in a paper published in The Lancet Public Health, researchers sound a clarion call for greater investment, at both the community and institutional level, in establishing support for grief-related suffering.

Credit: Photo courtesy of Memorial Sloan Kettering Comprehensive Cancer Center

MIAMI, FLORIDA (March 15, 2024) – The public health toll from bereavement is well-documented in the medical literature, with bereaved persons at greater risk for many adverse outcomes, including mental health challenges, decreased quality of life, health care neglect, cancer, heart disease, suicide, and death. Now, in a paper published in The Lancet Public Health, researchers sound a clarion call for greater investment, at both the community and institutional level, in establishing support for grief-related suffering.

The authors emphasized that increased mortality worldwide caused by the COVID-19 pandemic, suicide, drug overdose, homicide, armed conflict, and terrorism have accelerated the urgency for national- and global-level frameworks to strengthen the provision of sustainable and accessible bereavement care. Unfortunately, current national and global investment in bereavement support services is woefully inadequate to address this growing public health crisis, said researchers with Sylvester Comprehensive Cancer Center at the University of Miami Miller School of Medicine and collaborating organizations.

They proposed a model for transitional care that involves firmly establishing bereavement support services within healthcare organizations to ensure continuity of family-centered care while bolstering community-based support through development of “compassionate communities” and a grief-informed workforce. The model highlights the responsibility of the health system to build bridges to the community that can help grievers feel held as they transition.

The Center for the Advancement of Bereavement Care at Sylvester is advocating for precisely this model of transitional care. Wendy G. Lichtenthal, PhD, FT, FAPOS, who is Founding Director of the new Center and associate professor of public health sciences at the Miller School, noted, “We need a paradigm shift in how healthcare professionals, institutions, and systems view bereavement care. Sylvester is leading the way by investing in the establishment of this Center, which is the first to focus on bringing the transitional bereavement care model to life.”

What further distinguishes the Center is its roots in bereavement science, advancing care approaches that are both grounded in research and community-engaged.

The authors focused on palliative care, which strives to provide a holistic approach to minimize suffering for seriously ill patients and their families, as one area where improvements are critically needed. They referenced groundbreaking reports of the Lancet Commissions on the value of global access to palliative care and pain relief that highlighted the “undeniable need for improved bereavement care delivery infrastructure.” One of those reports acknowledged that bereavement has been overlooked and called for reprioritizing social determinants of death, dying, and grief.

“Palliative care should culminate with bereavement care, both in theory and in practice,” explained Lichtenthal, who is the article’s corresponding author. “Yet, bereavement care often is under-resourced and beset with access inequities.”

Transitional bereavement care model

So, how do health systems and communities prioritize bereavement services to ensure that no bereaved individual goes without needed support? The transitional bereavement care model offers a roadmap.

“We must reposition bereavement care from an afterthought to a public health priority. Transitional bereavement care is necessary to bridge the gap in offerings between healthcare organizations and community-based bereavement services,” Lichtenthal said. “Our model calls for health systems to shore up the quality and availability of their offerings, but also recognizes that resources for bereavement care within a given healthcare institution are finite, emphasizing the need to help build communities’ capacity to support grievers.”

Key to the model, she added, is the bolstering of community-based support through development of “compassionate communities” and “upskilling” of professional services to assist those with more substantial bereavement-support needs.

The model contains these pillars:

Preventive bereavement care –healthcare teams engage in bereavement-conscious practices, and compassionate communities are mindful of the emotional and practical needs of dying patients’ families.

Ownership of bereavement care – institutions provide bereavement education for staff, risk screenings for families, outreach and counseling or grief support. Communities establish bereavement centers and “champions” to provide bereavement care at workplaces, schools, places of worship or care facilities.

Resource allocation for bereavement care – dedicated personnel offer universal outreach, and bereaved stakeholders provide input to identify community barriers and needed resources.

Upskilling of support providers – Bereavement education is integrated into training programs for health professionals, and institutions offer dedicated grief specialists. Communities have trained, accessible bereavement specialists who provide support and are educated in how to best support bereaved individuals, increasing their grief literacy.

Evidence-based care – bereavement care is evidence-based and features effective grief assessments, interventions, and training programs. Compassionate communities remain mindful of bereavement care needs.

Lichtenthal said the new Center will strive to materialize these pillars and aims to serve as a global model for other health organizations. She hopes the paper’s recommendations “will cultivate a bereavement-conscious and grief-informed workforce as well as grief-literate, compassionate communities and health systems that prioritize bereavement as a vital part of ethical healthcare.”

“This paper is calling for healthcare institutions to respond to their duty to care for the family beyond patients’ deaths. By investing in the creation of the Center for the Advancement of Bereavement Care, Sylvester is answering this call,” Lichtenthal said.

Follow @SylvesterCancer on X for the latest news on Sylvester’s research and care.

# # #

Article Title: Investing in bereavement care as a public health priority

DOI: 10.1016/S2468-2667(24)00030-6

Authors: The complete list of authors is included in the paper.

Funding: The authors received funding from the National Cancer Institute (P30 CA240139 Nimer) and P30 CA008748 Vickers).

Disclosures: The authors declared no competing interests.

# # #

Journal

The Lancet Public Health

DOI

10.1016/S2468-2667(24)00030-6

Article Title

Investing in bereavement care as a public health priority

Artificial intelligence (AI) cannot distinguish fact from fiction. It also isn’t creative or can create novel content but repeats, repackages, and reformulates what has already been said (but perhaps in new ways).

I am sure someone will disagree with the latter, perhaps pointing to the fact that AI can clearly generate, for example, new songs and lyrics. I agree with this, but it misses the point. AI produces a “new” song lyric only by drawing from the data of previous song lyrics and then uses that information (the inductively uncovered patterns in it) to generate what to us appears to be a new song (and may very well be one). However, there is no artistry in it, no creativity. It’s only a structural rehashing of what exists.

Of course, we can debate to what extent humans can think truly novel thoughts and whether human learning may be based solely or primarily on mimicry. However, even if we would—for the sake of argument—agree that all we know and do is mere reproduction, humans have limited capacity to remember exactly and will make errors. We also fill in gaps with what subjectively (not objectively) makes sense to us (Rorschach test, anyone?). Even in this very limited scenario, which I disagree with, humans generate novelty beyond what AI is able to do.

Both the inability to distinguish fact from fiction and the inductive tether to existent data patterns are problems that can be alleviated programmatically—but are open for manipulation.

Manipulation and Propaganda

When Google launched its Gemini AI in February, it immediately became clear that the AI had a woke agenda. Among other things, the AI pushed woke diversity ideals into every conceivable response and, among other things, refused to show images of white people (including when asked to produce images of the Founding Fathers).

Tech guru and Silicon Valley investor Marc Andreessen summarized it on X (formerly Twitter): “I know it’s hard to believe, but Big Tech AI generates the output it does because it is precisely executing the specific ideological, radical, biased agenda of its creators. The apparently bizarre output is 100% intended. It is working as designed.”

There is indeed a design to these AIs beyond the basic categorization and generation engines. The responses are not perfectly inductive or generative. In part, this is necessary in order to make the AI useful: filters and rules are applied to make sure that the responses that the AI generates are appropriate, fit with user expectations, and are accurate and respectful. Given the legal situation, creators of AI must also make sure that the AI does not, for example, violate intellectual property laws or engage in hate speech. AI is also designed (directed) so that it does not go haywire or offend its users (remember Tay?).

However, because such filters are applied and the “behavior” of the AI is already directed, it is easy to take it a little further. After all, when is a response too offensive versus offensive but within the limits of allowable discourse? It is a fine and difficult line that must be specified programmatically.

It also opens the possibility for steering the generated responses beyond mere quality assurance. With filters already in place, it is easy to make the AI make statements of a specific type or that nudges the user in a certain direction (in terms of selected facts, interpretations, and worldviews). It can also be used to give the AI an agenda, as Andreessen suggests, such as making it relentlessly woke.

Thus, AI can be used as an effective propaganda tool, which both the corporations creating them and the governments and agencies regulating them have recognized.

Misinformation and Error

States have long refused to admit that they benefit from and use propaganda to steer and control their subjects. This is in part because they want to maintain a veneer of legitimacy as democratic governments that govern based on (rather than shape) people’s opinions. Propaganda has a bad ring to it; it’s a means of control.

However, the state’s enemies—both domestic and foreign—are said to understand the power of propaganda and do not hesitate to use it to cause chaos in our otherwise untainted democratic society. The government must save us from such manipulation, they claim. Of course, rarely does it stop at mere defense. We saw this clearly during the covid pandemic, in which the government together with social media companies in effect outlawed expressing opinions that were not the official line (see Murthy v. Missouri).

AI is just as easy to manipulate for propaganda purposes as social media algorithms but with the added bonus that it isn’t only people’s opinions and that users tend to trust that what the AI reports is true. As we saw in the previous article on the AI revolution, this is not a valid assumption, but it is nevertheless a widely held view.

If the AI then can be instructed to not comment on certain things that the creators (or regulators) do not want people to see or learn, then it is effectively “memory holed.” This type of “unwanted” information will not spread as people will not be exposed to it—such as showing only diverse representations of the Founding Fathers (as Google’s Gemini) or presenting, for example, only Keynesian macroeconomic truths to make it appear like there is no other perspective. People don’t know what they don’t know.

Of course, nothing is to say that what is presented to the user is true. In fact, the AI itself cannot distinguish fact from truth but only generates responses according to direction and only based on whatever the AI has been fed. This leaves plenty of scope for the misrepresentation of the truth and can make the world believe outright lies. AI, therefore, can easily be used to impose control, whether it is upon a state, the subjects under its rule, or even a foreign power.

The Real Threat of AI

What, then, is the real threat of AI? As we saw in the first article, large language models will not (cannot) evolve into artificial general intelligence as there is nothing about inductive sifting through large troves of (humanly) created information that will give rise to consciousness. To be frank, we haven’t even figured out what consciousness is, so to think that we will create it (or that it will somehow emerge from algorithms discovering statistical language correlations in existing texts) is quite hyperbolic. Artificial general intelligence is still hypothetical.

As we saw in the second article, there is also no economic threat from AI. It will not make humans economically superfluous and cause mass unemployment. AI is productive capital, which therefore has value to the extent that it serves consumers by contributing to the satisfaction of their wants. Misused AI is as valuable as a misused factory—it will tend to its scrap value. However, this doesn’t mean that AI will have no impact on the economy. It will, and already has, but it is not as big in the short-term as some fear, and it is likely bigger in the long-term than we expect.

No, the real threat is AI’s impact on information. This is in part because induction is an inappropriate source of knowledge—truth and fact are not a matter of frequency or statistical probabilities. The evidence and theories of Nicolaus Copernicus and Galileo Galilei would get weeded out as improbable (false) by an AI trained on all the (best and brightest) writings on geocentrism at the time. There is no progress and no learning of new truths if we trust only historical theories and presentations of fact.

However, this problem can probably be overcome by clever programming (meaning implementing rules—and fact-based limitations—to the induction problem), at least to some extent. The greater problem is the corruption of what AI presents: the misinformation, disinformation, and malinformation that its creators and administrators, as well as governments and pressure groups, direct it to create as a means of controlling or steering public opinion or knowledge.

This is the real danger that the now-famous open letter, signed by Elon Musk, Steve Wozniak, and others, pointed to:

“Should we let machines flood our information channels with propaganda and untruth? Should we automate away all the jobs, including the fulfilling ones? Should we develop nonhuman minds that might eventually outnumber, outsmart, obsolete and replace us? Should we risk loss of control of our civilization?”

Other than the economically illiterate reference to “automat[ing] away all the jobs,” the warning is well-taken. AI will not Terminator-like start to hate us and attempt to exterminate mankind. It will not make us all into biological batteries, as in The Matrix. However, it will—especially when corrupted—misinform and mislead us, create chaos, and potentially make our lives “solitary, poor, nasty, brutish and short.”

We use cookies on our website to give you the most relevant experience by remembering your preferences and repeat visits. By clicking “Accept”, you consent to the use of ALL the cookies.

This website uses cookies to improve your experience while you navigate through the website. Out of these, the cookies that are categorized as necessary are stored on your browser as they are essential for the working of basic functionalities of the website. We also use third-party cookies that help us analyze and understand how you use this website. These cookies will be stored in your browser only with your consent. You also have the option to opt-out of these cookies. But opting out of some of these cookies may affect your browsing experience.

Necessary cookies are absolutely essential for the website to function properly. These cookies ensure basic functionalities and security features of the website, anonymously.

Cookie

Duration

Description

cookielawinfo-checbox-analytics

11 months

This cookie is set by GDPR Cookie Consent plugin. The cookie is used to store the user consent for the cookies in the category "Analytics".

cookielawinfo-checbox-functional

11 months

The cookie is set by GDPR cookie consent to record the user consent for the cookies in the category "Functional".

cookielawinfo-checbox-others

11 months

This cookie is set by GDPR Cookie Consent plugin. The cookie is used to store the user consent for the cookies in the category "Other.

cookielawinfo-checkbox-necessary

11 months

This cookie is set by GDPR Cookie Consent plugin. The cookies is used to store the user consent for the cookies in the category "Necessary".

cookielawinfo-checkbox-performance

11 months

This cookie is set by GDPR Cookie Consent plugin. The cookie is used to store the user consent for the cookies in the category "Performance".

viewed_cookie_policy

11 months

The cookie is set by the GDPR Cookie Consent plugin and is used to store whether or not user has consented to the use of cookies. It does not store any personal data.

Functional cookies help to perform certain functionalities like sharing the content of the website on social media platforms, collect feedbacks, and other third-party features.

Performance cookies are used to understand and analyze the key performance indexes of the website which helps in delivering a better user experience for the visitors.

Analytical cookies are used to understand how visitors interact with the website. These cookies help provide information on metrics the number of visitors, bounce rate, traffic source, etc.

Advertisement cookies are used to provide visitors with relevant ads and marketing campaigns. These cookies track visitors across websites and collect information to provide customized ads.

{kind=link}

{kind=link}