International

The Fate Of The Pound Sterling

The Fate Of The Pound Sterling

Share this:

Authored by Alasdair Macleod via GoldMoney.com,

This is the third in a series of articles focused on the outlook for major currencies. The first concluded that the US dollar is already on the path of monetary hyperinflation. The second concluded that the euro system is close to collapse as a consequence of a combination of the failure of commercial banks and the TARGET2 settlement system, likely to collapse the currency itself.

With its systemic exposure to the Eurozone, sterling is likely to be a casualty of the failure of the euro system and shares the monetary hyperinflation characteristics of the dollar. The Bank of England is copying US monetary policies and will find it increasingly difficult to prevent the pound from escaping the same fate as the dollar.

Main points

-

Adjusting out QE of £300bn since last March tells us that measured in 2019 pounds the UK economy contracted by 34% in 1H 2020, not the 9.3% headline figure. A further round of QE and government spending will be deployed in an attempt to support the private sector economy through a second covid wave, which will almost certainly be greater than the initial £300bn—£317bn so far.

-

The Bank of England has now accepted that a second round of stimulus is required and is exploring the possibility of introducing negative interest rates. It has yet to factor in the deterioration in the outlook for global trade which will force it into further rounds of QE, irrespective of the path of the virus.

-

Britain’s banks, themselves exceptionally highly leveraged on a market capitalisation to balance sheet assets basis, are heavily exposed to the Eurozone’s banking system, which as I showed in last week’s article is could collapse in the near future. Rescuing British banks will require the government to underwrite at least a further £5.3 trillion in balance sheet assets at a time of mounting bad debts in the economy.

-

Since the Lehman crisis the banks have supported zombie businesses rather than face crippling write-offs. These zombies, epitomised by the desire of the industrial establishment to remain in the EU customs union rather than grasp the opportunities offered by free trade, are the principal beneficiaries of yet more government support. The moment that that support falters, Schumpeter’s creative destruction will hit the UK economy with a vengeance.

-

The impending economic failure triggered by waves of covid will doubtless be incorrectly blamed on Brexit. Nevertheless, the government and the Bank are committed to ensuring the economy does not slump. This will lead to yet more monetary inflation, setting the UK’s pound on the same hyperinflationary course as that of the dollar.

Introduction

There was a time when the British pound bestrode the world. More correctly, it was the gold standard behind it, the pound acting as a gold substitute between the end of the Napoleonic Wars and the outbreak of the First World War. Its sound money was extended throughout the British Empire through commerce. Admittedly, the government financed a series of small wars, but these were never to conquer territory — rather they were to subjugate rebellion, mainly from forces that wanted to substitute power for commerce. Today it would be called US-style peacekeeping, but modern historians with an anti-imperialist axe to grind call it colonial oppression.

But the fact is that Britain brought civilisation and improved living standards to many people whose technology had not even advanced to the wheel. Following the First World War, Britain then began its decline and fall with a succession of weak socialistic governments which could only hang onto America’s coat tails until throwing her lot in with the Common Market. It has been the longest and most notable decline from prosperity and global commercial dominance in modern times — longer even that the failure of Soviet communism. For Britain the hundred years from the Great War to date have seen the reversal of the fortunes of the previous hundred years.

It is not as if this is a trend fuelled by ignorance — we know from our past how to become wealthy and successful. Margaret Thatcher knew it, and so did Boris Johnson. But both were overwhelmed by the system, Boris considerably more rapidly than Margaret. Already half forgotten, Boris’s plans were decent: the reduction of state bureaucracy, the creation of free ports and the restoration of Britain as an entrepôt — an acknowledgement of low taxes, free markets, and the opportunities of Brexit. They were quickly overwhelmed by fear of covid-19. Fear that the state health service, full of wonderful, dedicated people working in a bureaucratic organisation would be unable to cope.

The bureaucrats did what they always do, prioritise the organisation above its purpose. The dysfunctional national health system was eulogised with rainbow paintings and a weekly clap-for-carers. But because there were not enough masks, the public was told they were ineffective, while the NHS took for itself what was available. The surge in hospital numbers was managed by the sick being billeted in private sector care homes, infecting and killing their residents.

In the full knowledge of the likely economic consequences of the mismanagement of the pandemic there has been no suggestion that the state should rein in its spending. One would have thought that when the people are forced to economise, the state should as well to reduce its burden on the people. But no; to save the state’s employment record, spending on supposedly important causes with the intention of preserving jobs has gone off the Richter scale.

Civil servants in the Treasury, which has been brought under the Prime Minister’s direct control, still dream of a balanced budget, achieved not by cutting government spending, but by raising taxes. But others see that raising taxes too early risks destroying what’s left of the tax base. Meanwhile, the list of supplicants with good causes and their hands out for more and more money from the state grows even longer. The government’s problem is that after a hundred years of increasing socialism it finds itself accelerating on the road to yet more socialism instead of turning the tide towards Boris’s libertarian ideals.

Attempts to steer the economy back towards free markets and sound government finances were always going to be difficult. Boris is no de Gaulle, prepared to place national liberty and culture above foreign relations. Nor is he in a strong enough position to emulate Ludwig Erhard, who was empowered to ditch the status quo with a clear vision of the future. It is not necessarily Boris’s fault; it is the political reality.

If nothing else, covid has exposed Boris as relying on his advisors instead of ploughing his own furrow. It has exposed the British public’s wishful belief that a magic money tree exists ready to be defoliated, and that any government which doesn’t make full use of it is being monstrously unfair.

Covid is a crisis which has exposed the inadequacies of state planning. But the unsavoury fact is that given the scientific advice, from the political point of view the government had little alternative to locking down the entire nation on 23 March. Now that Europe and the UK are entering a second wave of the virus, all thoughts of a rapid return to normality have been debunked. The V-shaped recovery upon which financial and economic predictions were predicated has gone out of the window, and the establishment is only just realising it.

Brexit and continuing European ties

For the establishment there is the added pain of Brexit, where Britain can no longer hang onto its European nurse, for fear of something worse. As the habitual robber of its electorate’s freedom, the British establishment itself cannot easily come to terms with the prospect of its own freedom from Europe.

Brexit has already happened and the transition period, during which trade and other arrangements were meant to be finalised, ends on 31 December, so far without agreement. But at long last, the EU’s negotiating team realises that Britain means business over the remaining issues, principally fishing and sovereignty. From the British point of view, an understanding of proper economics tells us she should grasp the free market option, refuse to accept any trade deal and withhold any funds agreed as part of the withdrawal settlement. But the Westminster and Whitehall establishments, wooed by and in the pocket of vested interests, is wholly unable to embrace the sensibility of that outcome.

Whether it ends up with a trade deal or WTO terms is less relevant than the fact that with the exception of some cabinet ministers, Whitehall (civil service) and Westminster (politicians) establishments are solid Remainers — terrified of the economic consequences of Brexit. They are in the company of industry lobbyists, with their established European links and reluctance to explore new trade opportunities elsewhere. Any descent into a business slump will almost certainly be wrongly blamed on Brexit, ignoring the inadequacies of British business and the need for its fundamental reform — a need that can only be satisfied by allowing zombie businesses, mainly tied to European protectionism, to go to the wall and for capital of all forms to be freed and redirected towards profitable use.

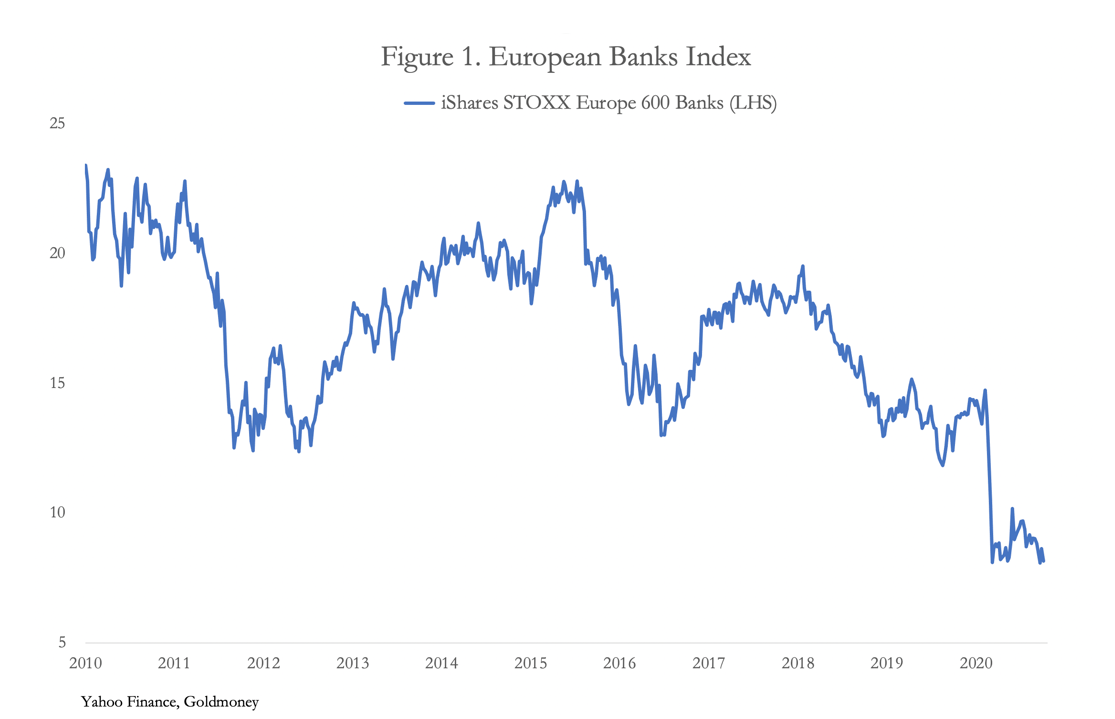

Whatever the outcome of Brexit, the ties with the EU will not suddenly cease. In the event of a financial and systemic failure, extra financial obligations will arise, and there are considerable counterparty risks between European and British banks. See here for my recent analysis of the Eurozone’s banking and monetary system. The likelihood of a Eurozone banking collapse is now a virtual certainty and could transpire any moment. Figure 1 shows the scale of the collapse in their share prices. And as measured by the STOXX Index Europe 600 banks, the sector is on the verge of setting new lows.

The STOXX Europe 600 banks includes Eurozone, British and other European banks. Over this calendar year, the index has fallen by 43% at a time when equities recovered strongly following the FOMC’s announcement of unlimited QE on 23 March 2020.

The severe actual and relative weaknesses in Eurozone banks come at a time of similar weakness in the British banks, and a banking failure in the Eurozone or elsewhere would collapse British banks like so many dominoes. The Treasury and Bank of England will then be forced to underwrite their banking systems with unlimited credit, supporting balance sheets amounting to more than £5.5 trillion — over twice UK GDP. Furthermore, the fig-leaf concealing monetary inflation through QE would be blown away, exposing the ghastly reality of government finances.

This is a global problem to which the UK is exceptionally exposed. Every ten years or so the cycle of bank credit expansion ends: that was first evidenced perhaps in September 2019 when the repo market in New York failed. The Fed had already begun to cut its funds rate the previous month; its antennae having detected a change in credit market conditions. By then, it was evident that international trade had stopped expanding, due to the trade tariff war between America and China. And because global trade is dollar based, the first impact was bound to affect US banks, their balance sheets and their lending policies.

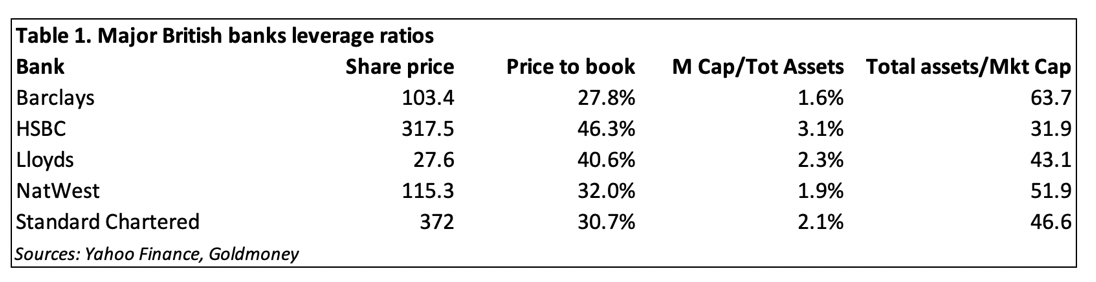

As the second most important international finance centre, London was bound to follow suit. In addition to the Eurozone exposure, and with the financial conflict between America and China escalating over Hong Kong, London faces risks from HSBC and Standard Chartered, two major British banks most of whose business is centred in Hong Kong and the Far East. And at over £2.6 trillion, these two banks have combined balance sheet liabilities that exceed Britain’s contracting 2020 GDP by nearly 40%. The full horror of the position of Britain’s banks is illustrated in Table 1 below.

By including the market’s rating of these banks (the price to book ratio), we end up with a better estimate of risk than by relying on balance sheet equity alone. This is because, for example, in the case of Barclays, the market is telling us that in a liquidation, shareholders will receive less than 28% pence in the pound: less, because in any share price there is also an enterprise value to consider as well as the option value of limited liability and unlimited upside. Even not allowing for these factors it is clear that none of the British banks, with combined balance sheet assets totalling £5.3 trillion, are in a position to withstand a Eurozone banking crisis.

Essentially, that was the position before covid wreaked its financial havoc, a factor which has only increased the certainty of a systemic banking crisis.

The financial and economic consequences of covid

In common with other nations the UK government moved quickly to prevent a surge in unemployment, fuelled by the belief that after lockdowns and with the right support from government the post-pandemic economy would quickly return to normal. The Bank of England stepped up to the plate with £300bn of quantitative easing, amounting to 13.6% of 2019 GDP and the equivalent of 34% of previously planned government spending.

At this juncture, it is important to understand something to which macroeconomists are generally blind: GDP is the sum total of all transactions, which without the addition of extra money is a static figure. Economic progress, or the lack of it, which is what GDP purports to measure cannot be measured, and an increase in GDP is simply an increase in the quantity of money in the economy. This is confirmed in Figure 1, where the quantity of UK broad money supply (M4) closely tracks annualised GDP, that is until this year, when the coronavirus hit — more about this divergence follows later in this article.

Another way of looking at the relationship is to understand that, apart from some minor variations in money retained for liquidity purposes, all money and profits earned are spent or saved, the latter being deferred consumption, supplying investment capital. With no change in the quantity of circulating currency there can be no change in the total spent and saved, and it is these totals that make up GDP, whether accounted for from the production or consumption sides. Therefore, if the central bank buys assets thereby pushing more money into the economy, or commercial banks expand credit out of thin air, GDP will rise accordingly by the amount of money created and credit expanded.

We can now consider the effects of monetary expansion on the UK’s national accounts. Since the Lehman crisis, which led to an emergency one-off £75bn round of QE, The BoE has been unable to resist the temptation of further rounds of inflationary financing, amounting to £745bn to date, which on a base of 2008’s nominal GDP of £1,589bn is an additional 47% of monetary inflation. [All GDP quantities in this analysis are of current price, or nominal GDP.]

By the end of 2019, annual GDP had increased to £2,214bn, including £445bn of QE, indicating that from 2008 the difference was made up by bank credit expansion totalling £180bn:

£1,589bn + £445bn + £180bn = £2,214bn.

In the first half of 2020, GDP was £1,031bn, after an injection of £300bn in QE. Putting to one side changes in levels of bank credit, without the £300bn QE, implied GDP in the first half of 2020 would have been £1,031bn less £300, or £731bn. This is an annualised rate of £1,462bn, implying an adjusted fall in annualised nominal GDP of 34%.

We can therefore conclude that the first wave of covid-19 reduced the monetary value of total transactions in the economy by 34% measured in pre-covid pounds, not the 9.3% headline figure, which includes the additional covid-related £300bn of QE. This leaves the question posed in Figure 1 about the relationship between a contracting GDP and increasing broad money supply, which we must now address.

Government lending schemes

As mentioned in the introduction, the government responded to the covid crisis by taking measures to restrict the effect on the level of employment. Clearly, with much of the economy locked down and running at only two-thirds of last year’s GDP there is a massive overhang not yet recorded in the 4.1% unemployment statistic. Furlough and other schemes to delay the impact were predicated on the hope that after the covid crisis things would quickly return to normal.

The normal to which the British planners hope to return is a post-Lehman crisis normal, where the ten-year expansion of bank lending has predominantly supported zombie businesses, which should have been allowed to fail[i]. Therefore, the government’s covid response is to extend zombie support by underwriting a range of bank loans for large, medium-sized and small business and relieve them of taxes and business rates. Banks are indemnified against all or most of the potential losses when acting as agents for government loans. Otherwise, it is clear that the banks would rather reduce their balance sheets at a time of escalating credit risk.

That explains why broad money, reflecting bank credit expansion of £243bn as well as £300m of QE, has increased. The difference with a contracting GDP exists because it has not yet worked through to prices, GDP itself being the product of the quantity of goods and services purchased and the prices paid. The bulk of covid support has been applied to business, the public sector and business tax reliefs, with only an estimated £83.7bn of the combined total of bank credit expansion and QE ending up in households, basically funding consumption.

If the money had been helicoptered into consumers’ bank accounts, the price effect would be more immediate. As it was, during the shutdown people were being paid somewhat less than they were earning before to do nothing, a condition of the furlough scheme, so overall consumption has declined, and so, therefore, has production.

So far, covid related government spending has led to an increase of government borrowing estimated £317.4bn[ii], slightly more than the Bank of England’s QE of £300bn. Before we move on to the effects of the second covid wave, we should note that the portion of bank credit not underwritten by the government will tend to contract. Already, there has been evidence of banks charging usurious rates of up to 40% on arranged overdrafts for individuals and the cutting of unused credit card limits. The squeeze on consumers’ and small businesses’ spending is bound to intensify. Businesses not qualifying for government support will find revolving credit virtually impossible to obtain, and businesses which have already drawn down on government guaranteed loans will find there is little further financial support available.

To the extent that the monetary stimulation from the Bank’s QE and government support schemes to the private sector is not neutralised by subsequent contractions of bank credit, the monetary inflation from these sources will lead to higher prices as the additions to broad money supply M4 circulates more widely. Furthermore, we can expect to see nominal GDP recover to close most of the gap between it and the level of M4 money supply as shown in Figure 1 above. While that will give the impression of economic recovery to slavish followers of statistics, it will misinform them. The reality is both production and consumption volumes and the purchasing power of the pound will have all declined.

Enter the second wave…

While statistically understating the negative effects of the inflation of money and credit on the general level of prices and of nominal GDP, there will be the additional effects of the second covid wave to consider. Already, plans to end the support given to business and households have been deferred with new support arrangements being introduced. As yet, these have not been fully disclosed and costed. But with the wreckage of the first round of shutdowns still in the works, the second covid round is likely to encourage the government into a second round of stimulus that will have to be greater than the first.

The government currently hopes that a refined version of complete lockdowns will limit the economic damage likely to be caused by the second wave. But pessimism mounts: only this week expectations that the second wave will lead to even greater strains on hospitals than those of the first wave have been reinforced by surging infection rates in Europe. “Second wave forecast to be more deadly than the first” was the lead story in yesterday’s Daily Telegraph.

It is becoming increasingly obvious to the government and the keeper of its money tree that the economic consequences are going to be at least as destructive as those of the first wave. In budgetary terms, The Institute for Government’s estimate of covid costs to September at £317bn will almost certainly be exceeded by a fair margin in the coming months.

Unsurprisingly, the Bank of England is preparing for yet more QE and in an attempt to lessen the impact on business is paving the way for negative interest rates. Commercial banks have been asked to report whether their systems are able to operate in a negative interest rate environment, and so far, only NatWest has replied that its systems cannot operate at or below the zero bound, but the deadline for replies is not until 12 November. The bigger issue is the sheer desperation that has led to the Bank to plan for their introduction.

The Bank of England plans unlimited inflation

While the committee’s members’ opinions vary, it is clear that the Monetary Policy Committee is collectively clueless — the MPC sets the bank rate and is the equivalent of the Fed’s FOMC. While firmly stuck on the belief that an interest rate is the cost of borrowing and not a reflection of time preference, the planners appear to ignore the fact that negative interest rates are a tax on the banks and their deposits, another form of wealth transfer from an embattled private sector to a voracious state. Then there is the hidden agenda of making limitless government borrowing affordable and thereby unleashing the prospect of unlimited monetary inflation.

The damage wreaked by negative rates is surely evident from the lack of their effectiveness in stimulating economies elsewhere, particularly that of neighbouring Euroland. If they were able to learn anything, the neo-Keynesians on the MPC would have understood that the interest rate structure can only be decided by free markets, and that as a committee they are therefore functionless. But if they have achieved anything, they have bought off the realities of a failing economy, overburdened by zombie businesses. And every day these realities are defrayed, the worse the eventual consequences become.

These are the endogenous economic and monetary realities. The exogenous ones, particularly the systemic risks of the Eurozone banking system, are factors no one appears to be taking seriously. The consequences of the contraction of global trade triggered by the tariff wars between America and China have rarely been taken into account.

So far, the foreign exchanges and general public, which ultimately decide the purchasing power of the state’s unbacked currency, only see the government’s response in terms of a currency which is fundamentally unaltered. A second round of QE, which is likely to exceed the first in terms of its size, can be expected to ring alarm bells, at least initially on the foreign exchanges, whose participants will then consider if the monetary dilution will be enough, and how much more will be needed to rescue the economy from a deepening slump. How these factors are reflected in dollar and euro exchange rates will depend on how similar factors affect those currencies. But it is easy to envisage, in the absence of the systemic risks mentioned above, sterling declining with the dollar, and its fall through parity with the euro being blamed on Brexit by Remainers in the establishment and the media. All currencies will then face the prospect of a slump in global trade being magnified by depreciating currencies measured in commodities, goods, and importantly essentials such as food.

If this leads to monetary inflation pushing up the general level of prices beyond the control of CPI methodologies, which seems certain to be the case, markets will take control of interest rates away from the MPC and America’s FOMC. The overt bankruptcy of the UK government will be reflected in a wider public rejection of faith in the currency, to the point where it will be disposed of rapidly for goods not necessarily needed immediately, in a crack-up boom.

That is the likely outcome of developments accelerated by the covid crisis and is in accordance with likely consequences for the dollar and the euro. It will take the characteristics of a monetary implosion instead of a quantity-related decline. In any event, sterling is already in a state of hyperinflation, which I have defined as the condition whereby monetary authorities accelerate the expansion of the quantity of money to the point where is proves impossible for them to regain control.

International

President Biden Delivers The “Darkest, Most Un-American Speech Given By A President”

President Biden Delivers The "Darkest, Most Un-American Speech Given By A President"

Having successfully raged, ranted, lied, and yelled through…

Share this:

Having successfully raged, ranted, lied, and yelled through the State of The Union, President Biden can go back to his crypt now.

Whatever 'they' gave Biden, every American man, woman, and the other should be allowed to take it - though it seems the cocktail brings out 'dark Brandon'?

Tl;dw: Biden's Speech tonight ...

-

Fund Ukraine.

-

Trump is threat to democracy and America itself.

-

Abortion is good.

-

American Economy is stronger than ever.

-

Inflation wasn't Biden's fault.

-

Illegals are Americans too.

-

Republicans are responsible for the border crisis.

-

Trump is bad.

-

Biden stands with trans-children.

-

J6 was the worst insurrection since the Civil War.

(h/t @TCDMS99)

Tucker Carlson's response sums it all up perfectly:

"that was possibly the darkest, most un-American speech given by an American president. It wasn't a speech, it was a rant..."

Carlson continued: "The true measure of a nation's greatness lies within its capacity to control borders, yet Bid refuses to do it."

"In a fair election, Joe Biden cannot win"

And concluded:

“There was not a meaningful word for the entire duration about the things that actually matter to people who live here.”

Victor Davis Hanson added some excellent color, but this was probably the best line on Biden:

"he doesn't care... he lives in an alternative reality."

— Tucker Carlson (@TuckerCarlson) March 8, 2024

* * *

Watch SOTU Live here...

* * *

Mises' Connor O'Keeffe, warns: "Be on the Lookout for These Lies in Biden's State of the Union Address."

On Thursday evening, President Joe Biden is set to give his third State of the Union address. The political press has been buzzing with speculation over what the president will say. That speculation, however, is focused more on how Biden will perform, and which issues he will prioritize. Much of the speech is expected to be familiar.

The story Biden will tell about what he has done as president and where the country finds itself as a result will be the same dishonest story he's been telling since at least the summer.

He'll cite government statistics to say the economy is growing, unemployment is low, and inflation is down.

Something that has been frustrating Biden, his team, and his allies in the media is that the American people do not feel as economically well off as the official data says they are. Despite what the White House and establishment-friendly journalists say, the problem lies with the data, not the American people's ability to perceive their own well-being.

As I wrote back in January, the reason for the discrepancy is the lack of distinction made between private economic activity and government spending in the most frequently cited economic indicators. There is an important difference between the two:

-

Government, unlike any other entity in the economy, can simply take money and resources from others to spend on things and hire people. Whether or not the spending brings people value is irrelevant

-

It's the private sector that's responsible for producing goods and services that actually meet people's needs and wants. So, the private components of the economy have the most significant effect on people's economic well-being.

Recently, government spending and hiring has accounted for a larger than normal share of both economic activity and employment. This means the government is propping up these traditional measures, making the economy appear better than it actually is. Also, many of the jobs Biden and his allies take credit for creating will quickly go away once it becomes clear that consumers don't actually want whatever the government encouraged these companies to produce.

On top of all that, the administration is dealing with the consequences of their chosen inflation rhetoric.

Since its peak in the summer of 2022, the president's team has talked about inflation "coming back down," which can easily give the impression that it's prices that will eventually come back down.

But that's not what that phrase means. It would be more honest to say that price increases are slowing down.

Americans are finally waking up to the fact that the cost of living will not return to prepandemic levels, and they're not happy about it.

The president has made some clumsy attempts at damage control, such as a Super Bowl Sunday video attacking food companies for "shrinkflation"—selling smaller portions at the same price instead of simply raising prices.

In his speech Thursday, Biden is expected to play up his desire to crack down on the "corporate greed" he's blaming for high prices.

In the name of "bringing down costs for Americans," the administration wants to implement targeted price ceilings - something anyone who has taken even a single economics class could tell you does more harm than good. Biden would never place the blame for the dramatic price increases we've experienced during his term where it actually belongs—on all the government spending that he and President Donald Trump oversaw during the pandemic, funded by the creation of $6 trillion out of thin air - because that kind of spending is precisely what he hopes to kick back up in a second term.

If reelected, the president wants to "revive" parts of his so-called Build Back Better agenda, which he tried and failed to pass in his first year. That would bring a significant expansion of domestic spending. And Biden remains committed to the idea that Americans must be forced to continue funding the war in Ukraine. That's another topic Biden is expected to highlight in the State of the Union, likely accompanied by the lie that Ukraine spending is good for the American economy. It isn't.

It's not possible to predict all the ways President Biden will exaggerate, mislead, and outright lie in his speech on Thursday. But we can be sure of two things. The "state of the Union" is not as strong as Biden will say it is. And his policy ambitions risk making it much worse.

* * *

The American people will be tuning in on their smartphones, laptops, and televisions on Thursday evening to see if 'sloppy joe' 81-year-old President Joe Biden can coherently put together more than two sentences (even with a teleprompter) as he gives his third State of the Union in front of a divided Congress.

President Biden will speak on various topics to convince voters why he shouldn't be sent to a retirement home.

The state of our union under President Biden: three years of decline. pic.twitter.com/Da1KOIb3eR

— Speaker Mike Johnson (@SpeakerJohnson) March 7, 2024

According to CNN sources, here are some of the topics Biden will discuss tonight:

Economic issues: Biden and his team have been drafting a speech heavy on economic populism, aides said, with calls for higher taxes on corporations and the wealthy – an attempt to draw a sharp contrast with Republicans and their likely presidential nominee, Donald Trump.

Health care expenses: Biden will also push for lowering health care costs and discuss his efforts to go after drug manufacturers to lower the cost of prescription medications — all issues his advisers believe can help buoy what have been sagging economic approval ratings.

Israel's war with Hamas: Also looming large over Biden's primetime address is the ongoing Israel-Hamas war, which has consumed much of the president's time and attention over the past few months. The president's top national security advisers have been working around the clock to try to finalize a ceasefire-hostages release deal by Ramadan, the Muslim holy month that begins next week.

An argument for reelection: Aides view Thursday's speech as a critical opportunity for the president to tout his accomplishments in office and lay out his plans for another four years in the nation's top job. Even though viewership has declined over the years, the yearly speech reliably draws tens of millions of households.

Sources provided more color on Biden's SOTU address:

The speech is expected to be heavy on economic populism. The president will talk about raising taxes on corporations and the wealthy. He'll highlight efforts to cut costs for the American people, including pushing Congress to help make prescription drugs more affordable.

Biden will talk about the need to preserve democracy and freedom, a cornerstone of his re-election bid. That includes protecting and bolstering reproductive rights, an issue Democrats believe will energize voters in November. Biden is also expected to promote his unity agenda, a key feature of each of his addresses to Congress while in office.

Biden is also expected to give remarks on border security while the invasion of illegals has become one of the most heated topics among American voters. A majority of voters are frustrated with radical progressives in the White House facilitating the illegal migrant invasion.

It is probable that the president will attribute the failure of the Senate border bill to the Republicans, a claim many voters view as unfounded. This is because the White House has the option to issue an executive order to restore border security, yet opts not to do so

Maybe this is why?

Most Americans are still unaware that the census counts ALL people, including illegal immigrants, for deciding how many House seats each state gets!

— Elon Musk (@elonmusk) March 7, 2024

This results in Dem states getting roughly 20 more House seats, which is another strong incentive for them not to deport illegals.

While Biden addresses the nation, the Biden administration will be armed with a social media team to pump propaganda to at least 100 million Americans.

"The White House hosted about 70 creators, digital publishers, and influencers across three separate events" on Wednesday and Thursday, a White House official told CNN.

Not a very capable social media team...

The State of Confusion https://t.co/C31mHc5ABJ

— zerohedge (@zerohedge) March 7, 2024

The administration's move to ramp up social media operations comes as users on X are mostly free from government censorship with Elon Musk at the helm. This infuriates Democrats, who can no longer censor their political enemies on X.

Meanwhile, Democratic lawmakers tell Axios that the president's SOTU performance will be critical as he tries to dispel voter concerns about his elderly age. The address reached as many as 27 million people in 2023.

"We are all nervous," said one House Democrat, citing concerns about the president's "ability to speak without blowing things."

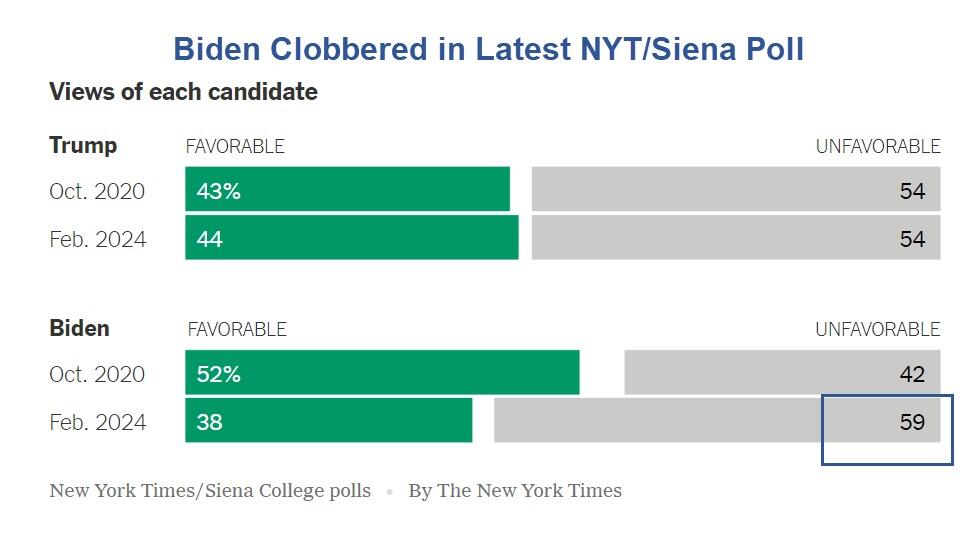

The SOTU address comes as Biden's polling data is in the dumps.

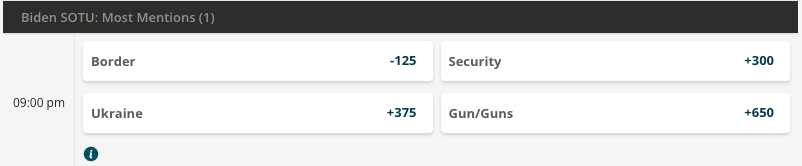

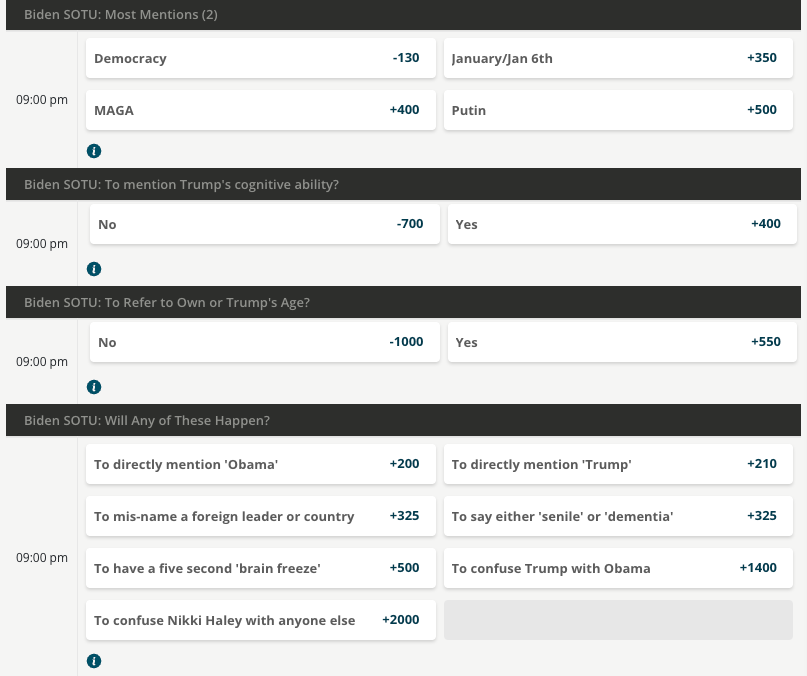

BetOnline has created several money-making opportunities for gamblers tonight, such as betting on what word Biden mentions the most.

As well as...

We will update you when Tucker Carlson's live feed of SOTU is published.

Fuck it. We’ll do it live! Thursday night, March 7, our live response to Joe Biden’s State of the Union speech. pic.twitter.com/V0UwOrgKvz

— Tucker Carlson (@TuckerCarlson) March 6, 2024

International

What is intersectionality and why does it make feminism more effective?

The social categories that we belong to shape our understanding of the world in different ways.

Share this:

The way we talk about society and the people and structures in it is constantly changing. One term you may come across this International Women’s Day is “intersectionality”. And specifically, the concept of “intersectional feminism”.

Intersectionality refers to the fact that everyone is part of multiple social categories. These include gender, social class, sexuality, (dis)ability and racialisation (when people are divided into “racial” groups often based on skin colour or features).

These categories are not independent of each other, they intersect. This looks different for every person. For example, a black woman without a disability will have a different experience of society than a white woman without a disability – or a black woman with a disability.

An intersectional approach makes social policy more inclusive and just. Its value was evident in research during the pandemic, when it became clear that women from various groups, those who worked in caring jobs and who lived in crowded circumstances were much more likely to die from COVID.

A long-fought battle

American civil rights leader and scholar Kimberlé Crenshaw first introduced the term intersectionality in a 1989 paper. She argued that focusing on a single form of oppression (such as gender or race) perpetuated discrimination against black women, who are simultaneously subjected to both racism and sexism.

Crenshaw gave a name to ways of thinking and theorising that black and Latina feminists, as well as working-class and lesbian feminists, had argued for decades. The Combahee River Collective of black lesbians was groundbreaking in this work.

They called for strategic alliances with black men to oppose racism, white women to oppose sexism and lesbians to oppose homophobia. This was an example of how an intersectional understanding of identity and social power relations can create more opportunities for action.

These ideas have, through political struggle, come to be accepted in feminist thinking and women’s studies scholarship. An increasing number of feminists now use the term “intersectional feminism”.

The term has moved from academia to feminist activist and social justice circles and beyond in recent years. Its popularity and widespread use means it is subjected to much scrutiny and debate about how and when it should be employed. For example, some argue that it should always include attention to racism and racialisation.

Recognising more issues makes feminism more effective

In writing about intersectionality, Crenshaw argued that singular approaches to social categories made black women’s oppression invisible. Many black feminists have pointed out that white feminists frequently overlook how racial categories shape different women’s experiences.

One example is hair discrimination. It is only in the 2020s that many organisations in South Africa, the UK and US have recognised that it is discriminatory to regulate black women’s hairstyles in ways that render their natural hair unacceptable.

This is an intersectional approach. White women and most black men do not face the same discrimination and pressures to straighten their hair.

“Abortion on demand” in the 1970s and 1980s in the UK and USA took no account of the fact that black women in these and many other countries needed to campaign against being given abortions against their will. The fight for reproductive justice does not look the same for all women.

Similarly, the experiences of working-class women have frequently been rendered invisible in white, middle class feminist campaigns and writings. Intersectionality means that these issues are recognised and fought for in an inclusive and more powerful way.

In the 35 years since Crenshaw coined the term, feminist scholars have analysed how women are positioned in society, for example, as black, working-class, lesbian or colonial subjects. Intersectionality reminds us that fruitful discussions about discrimination and justice must acknowledge how these different categories affect each other and their associated power relations.

This does not mean that research and policy cannot focus predominantly on one social category, such as race, gender or social class. But it does mean that we cannot, and should not, understand those categories in isolation of each other.

Ann Phoenix does not work for, consult, own shares in or receive funding from any company or organisation that would benefit from this article, and has disclosed no relevant affiliations beyond their academic appointment.

africa uk pandemicGovernment

Biden defends immigration policy during State of the Union, blaming Republicans in Congress for refusing to act

A rising number of Americans say that immigration is the country’s biggest problem. Biden called for Congress to pass a bipartisan border and immigration…

Share this:

{kind=link}

President Joe Biden delivered the annual State of the Union address on March 7, 2024, casting a wide net on a range of major themes – the economy, abortion rights, threats to democracy, the wars in Gaza and Ukraine – that are preoccupying many Americans heading into the November presidential election.

The president also addressed massive increases in immigration at the southern border and the political battle in Congress over how to manage it. “We can fight about the border, or we can fix it. I’m ready to fix it,” Biden said.

But while Biden stressed that he wants to overcome political division and take action on immigration and the border, he cautioned that he will not “demonize immigrants,” as he said his predecessor, former President Donald Trump, does.

“I will not separate families. I will not ban people from America because of their faith,” Biden said.

Biden’s speech comes as a rising number of American voters say that immigration is the country’s biggest problem.

Immigration law scholar Jean Lantz Reisz answers four questions about why immigration has become a top issue for Americans, and the limits of presidential power when it comes to immigration and border security.

1. What is driving all of the attention and concern immigration is receiving?

The unprecedented number of undocumented migrants crossing the U.S.-Mexico border right now has drawn national concern to the U.S. immigration system and the president’s enforcement policies at the border.

Border security has always been part of the immigration debate about how to stop unlawful immigration.

But in this election, the immigration debate is also fueled by images of large groups of migrants crossing a river and crawling through barbed wire fences. There is also news of standoffs between Texas law enforcement and U.S. Border Patrol agents and cities like New York and Chicago struggling to handle the influx of arriving migrants.

Republicans blame Biden for not taking action on what they say is an “invasion” at the U.S. border. Democrats blame Republicans for refusing to pass laws that would give the president the power to stop the flow of migration at the border.

2. Are Biden’s immigration policies effective?

Confusion about immigration laws may be the reason people believe that Biden is not implementing effective policies at the border.

The U.S. passed a law in 1952 that gives any person arriving at the border or inside the U.S. the right to apply for asylum and the right to legally stay in the country, even if that person crossed the border illegally. That law has not changed.

Courts struck down many of former President Donald Trump’s policies that tried to limit immigration. Trump was able to lawfully deport migrants at the border without processing their asylum claims during the COVID-19 pandemic under a public health law called Title 42. Biden continued that policy until the legal justification for Title 42 – meaning the public health emergency – ended in 2023.

Republicans falsely attribute the surge in undocumented migration to the U.S. over the past three years to something they call Biden’s “open border” policy. There is no such policy.

Multiple factors are driving increased migration to the U.S.

More people are leaving dangerous or difficult situations in their countries, and some people have waited to migrate until after the COVID-19 pandemic ended. People who smuggle migrants are also spreading misinformation to migrants about the ability to enter and stay in the U.S.

3. How much power does the president have over immigration?

The president’s power regarding immigration is limited to enforcing existing immigration laws. But the president has broad authority over how to enforce those laws.

For example, the president can place every single immigrant unlawfully present in the U.S. in deportation proceedings. Because there is not enough money or employees at federal agencies and courts to accomplish that, the president will usually choose to prioritize the deportation of certain immigrants, like those who have committed serious and violent crimes in the U.S.

The federal agency Immigration and Customs Enforcement deported more than 142,000 immigrants from October 2022 through September 2023, double the number of people it deported the previous fiscal year.

But under current law, the president does not have the power to summarily expel migrants who say they are afraid of returning to their country. The law requires the president to process their claims for asylum.

Biden’s ability to enforce immigration law also depends on a budget approved by Congress. Without congressional approval, the president cannot spend money to build a wall, increase immigration detention facilities’ capacity or send more Border Patrol agents to process undocumented migrants entering the country.

4. How could Biden address the current immigration problems in this country?

In early 2024, Republicans in the Senate refused to pass a bill – developed by a bipartisan team of legislators – that would have made it harder to get asylum and given Biden the power to stop taking asylum applications when migrant crossings reached a certain number.

During his speech, Biden called this bill the “toughest set of border security reforms we’ve ever seen in this country.”

That bill would have also provided more federal money to help immigration agencies and courts quickly review more asylum claims and expedite the asylum process, which remains backlogged with millions of cases, Biden said. Biden said the bipartisan deal would also hire 1,500 more border security agents and officers, as well as 4,300 more asylum officers.

Removing this backlog in immigration courts could mean that some undocumented migrants, who now might wait six to eight years for an asylum hearing, would instead only wait six weeks, Biden said. That means it would be “highly unlikely” migrants would pay a large amount to be smuggled into the country, only to be “kicked out quickly,” Biden said.

“My Republican friends, you owe it to the American people to get this bill done. We need to act,” Biden said.

Biden’s remarks calling for Congress to pass the bill drew jeers from some in the audience. Biden quickly responded, saying that it was a bipartisan effort: “What are you against?” he asked.

Biden is now considering using section 212(f) of the Immigration and Nationality Act to get more control over immigration. This sweeping law allows the president to temporarily suspend or restrict the entry of all foreigners if their arrival is detrimental to the U.S.

This obscure law gained attention when Trump used it in January 2017 to implement a travel ban on foreigners from mainly Muslim countries. The Supreme Court upheld the travel ban in 2018.

Trump again also signed an executive order in April 2020 that blocked foreigners who were seeking lawful permanent residency from entering the country for 60 days, citing this same section of the Immigration and Nationality Act.

Biden did not mention any possible use of section 212(f) during his State of the Union speech. If the president uses this, it would likely be challenged in court. It is not clear that 212(f) would apply to people already in the U.S., and it conflicts with existing asylum law that gives people within the U.S. the right to seek asylum.

Jean Lantz Reisz does not work for, consult, own shares in or receive funding from any company or organization that would benefit from this article, and has disclosed no relevant affiliations beyond their academic appointment.

congress senate trump pandemic covid-19 mexico ukraine

EyePoint poaches medical chief from Apellis; Sandoz CFO, longtime BioNTech exec to retire

Redefining Poverty: Towards a Transpartisan Approach

The Digest #187

Gather ’round the crystal ball: A multi-commodity outlook from PDAC 2024

Biden to call for first-time homebuyer tax credit, construction of 2 million homes

Is “Greedflation” Over?

Catastrophic Risk: Investing and Business Implications

Deterra Royalties half-yearly result: stable performance and growth Initiatives

Deflationary pressures in China – be careful what you wish for

Stock Market Today: Tech leads gains, S&P 500, Gold at record highs

-

Uncategorized2 weeks ago

Uncategorized2 weeks agoAll Of The Elements Are In Place For An Economic Crisis Of Staggering Proportions

-

Uncategorized1 month ago

Uncategorized1 month agoCathie Wood sells a major tech stock (again)

-

Uncategorized3 weeks ago

Uncategorized3 weeks agoCalifornia Counties Could Be Forced To Pay $300 Million To Cover COVID-Era Program

-

Uncategorized2 weeks ago

Uncategorized2 weeks agoApparel Retailer Express Moving Toward Bankruptcy

-

Uncategorized3 weeks ago

Uncategorized3 weeks agoIndustrial Production Decreased 0.1% in January

-

International1 month ago

International1 month agoWar Delirium

-

Uncategorized3 weeks ago

Uncategorized3 weeks agoRFK Jr: The Wuhan Cover-Up & The Rise Of The Biowarfare-Industrial Complex

-

Uncategorized3 weeks ago

Uncategorized3 weeks agoGOP Efforts To Shore Up Election Security In Swing States Face Challenges