Government

The Everything Bubble And What It Means For Your Money

The Everything Bubble And What It Means For Your Money

Authored by Colin Lloyd via The American Institute for Economic Research,

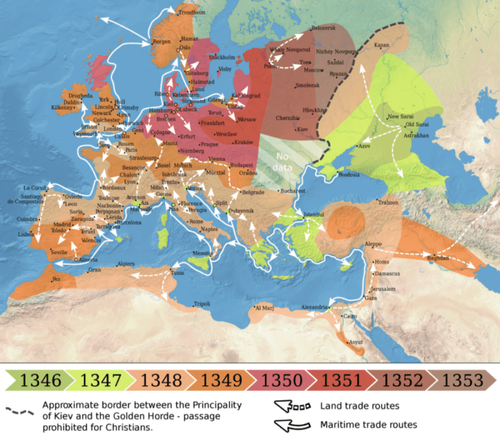

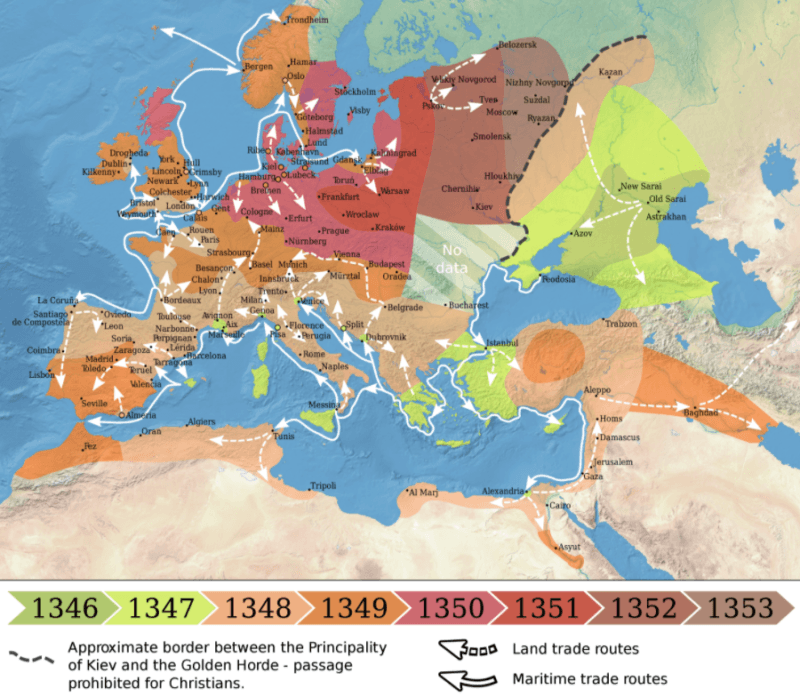

In the aftermath of the Black Plague which swept across Europe between 1347 and 1353, wiping out between 30…

Share this:

Authored by Colin Lloyd via The American Institute for Economic Research,

In the aftermath of the Black Plague which swept across Europe between 1347 and 1353, wiping out between 30 and 60% of the population, the European economy changed dramatically.

Source: Jeremy Norman – HistoryofInformation.com

The Black Plague had a lasting socioeconomic impact; for example, towns and cities emptied, and the sudden reduction in the labour force saw wages rise. Meanwhile attitudes towards death – and life – changed. The Latin phrase, carpe diem, quam minimum credula postero – seize the day, place no trust in tomorrow – epitomised this profound shift in attitudes.

The current pandemic, whilst utterly tragic, has been far less catastrophic, but due to the policy response it too appears destined to leave its mark in changing patterns of living and working. Unlike the 1350’s, however, where the changing price of goods and services signalled imbalances in supply and demand, the valiant monetary and fiscal actions of governments and institutions have distorted this price discovery mechanism.

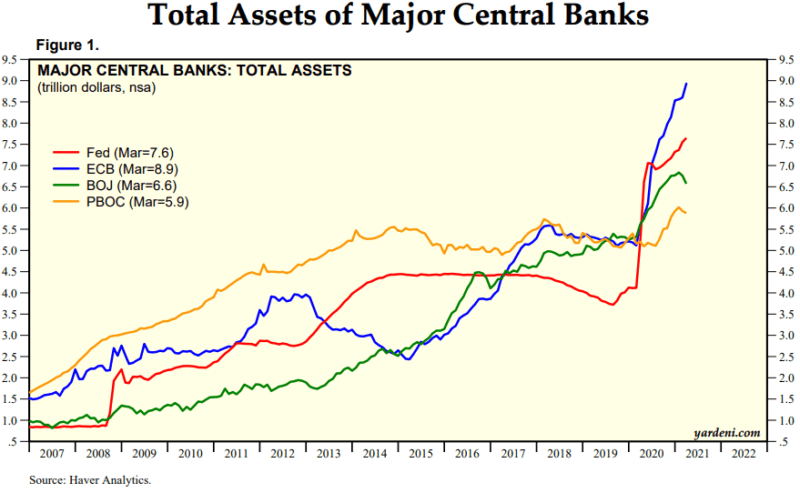

During the first months of the lockdown, economic growth declined and the price of many equities – and even bonds – fell rapidly. Central banks responded, as they had during the Great Financial Crisis (GFC) of 2008/2009, by cutting interest rates, or, where interest rates could be cut no further, by increasing their purchases of government bonds and other high grade securities. As a result of these purchases, major central banks balance sheets have swollen to $29trln:

Source: Yardeni, Haver Analytics

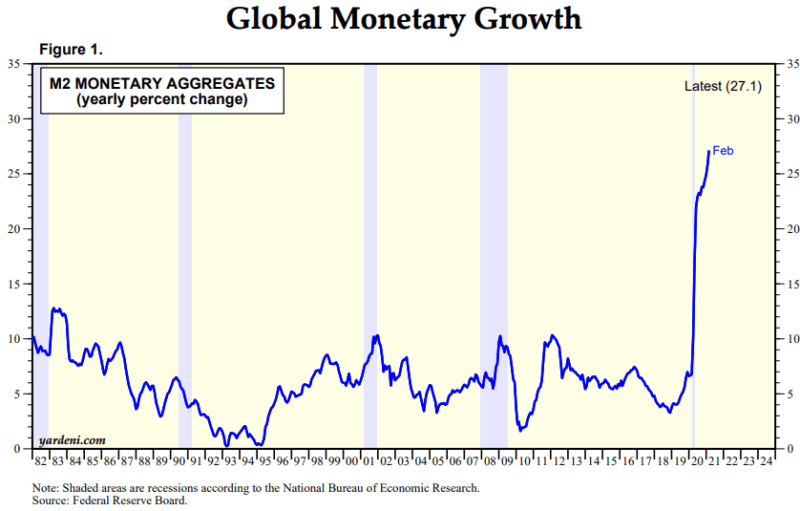

The effect of central bank actions has spilled over into a ballooning of global money supply: –

Source: Yardeni, Federal Reserve

Governments, cognizant of the limitations of their central banks, also reacted, providing loan guarantees, supporting the furloughing of employees and sending direct payments to the rising ranks of the unemployed. The chart below, which is from July 2020 and therefore does not account for the recent US $1.9trln spending package, nor the $2trln infrastructure proposal, shows the scale of these endeavours in comparison to the fiscal largesse of the GFC: –

Source: McKinsey

The impact of lower interest rates, buying of bonds and increased fiscal spending might be expected to have inflationary consequences but it has been leaning against the headwind of sharply rising global unemployment: –

Source: World Bank

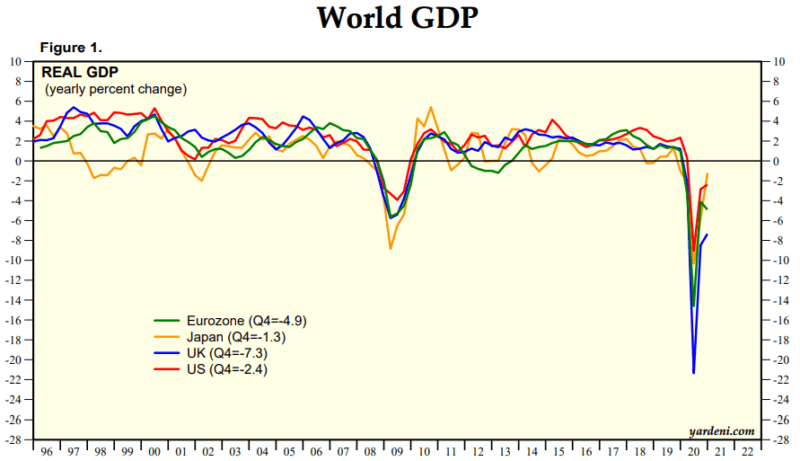

The rise in unemployment was itself a response to a dramatic decline in economic growth: –

Source: Yardeni

US unemployment data is beginning to improve but, as the IMF WEO April 2021 reveals, Europe may take much longer to respond. Euro area unemployment is expected to rise from 7.9% in 2020 to 8.3% in 2022. Forecasting unemployment, however, together with many other economic variables, has become much more challenging since the variance between estimates has expanded: –

Source: Federal Reserve

Savings Surge

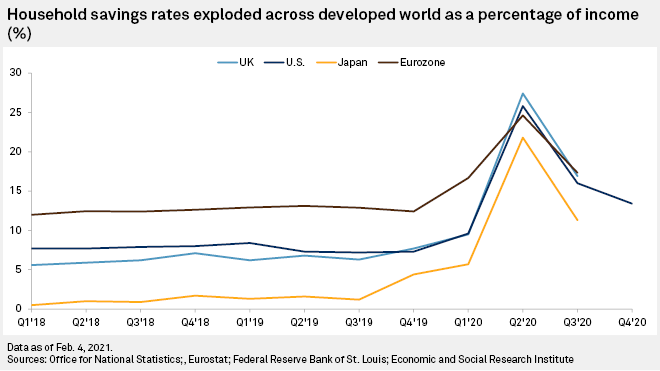

A natural side effect of rising unemployment, furloughing of staff, together with reduced mobility and economic activity, during the waves of pandemic lockdowns, has been a rise in household savings: –

Source: S&P Global, ONS, Eurostat, Federal Reserve

The initial recipients of this spring tide of excess savings were the banks: –

Source: Federal Reserve, BEA, Eurostat, Japan Cabinet Office, Statistics Canada

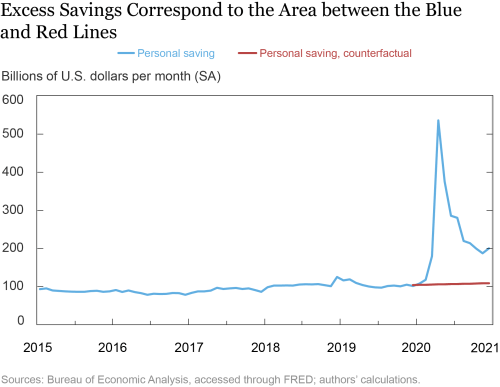

Oxford Economics estimates that US savings rose $1.6trln, Eurozone households added Euro470bln and those of the UK, £170bln. Estimates from Moody’s put the figure even higher, suggesting that the global pool of excess savings may now have reached $5.4trln – roughly 6% of global GDP. Since we are only interested in the impact of ‘excess savings’ rather than ‘all savings,’ the next chart is informative. It shows the monthly change in US savings: –

Source: Federal Reserve, BEA

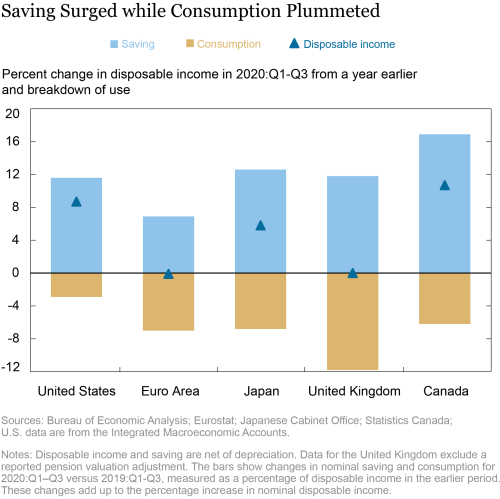

What will be done with these pools of saving? They may remain in bank accounts, be used to pay down debt, spent on goods and services or invested. In a recent article – What Is behind the Global Jump in Personal Saving during the Pandemic? The Federal Reserve reveals the impact during Q1-Q3 last year: –

Source: Federal Reserve, BEA, Eurostat, Japanese Cabinet office, Statistics Canada

Debt Binge

The next chart shows global debt and the debt to GDP ratio: –

Source: IIF, BIS, IMF, National sources

Such estimates probably underestimate financial sector debt and do not account for OTC derivatives, which, according to the Bank for International Settlements have a net value of $609trln.

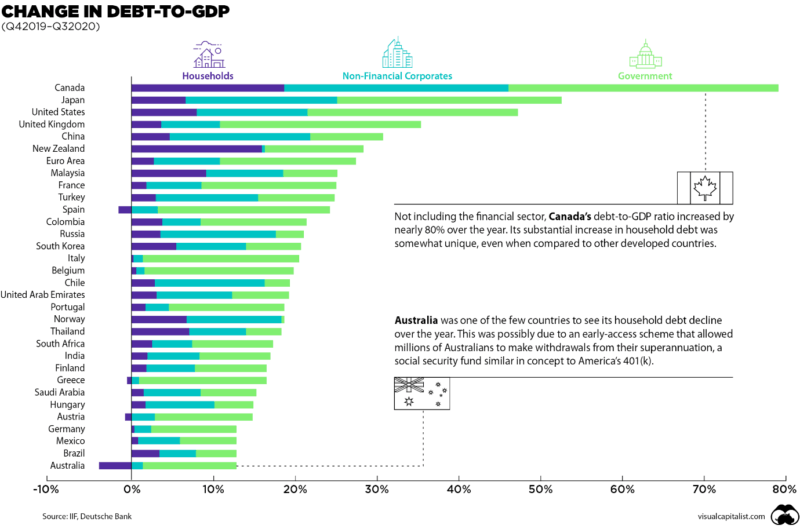

Setting aside derivatives, here is a breakdown by debt type for a selection of larger countries: –

Source: IIF, Deutsche bank, Visual Capitalist

During 2020, relative to GDP, government debt rose from 89% to 105%, and financial sector debt to a more moderate 81%. Meanwhile, non-financial private sector debt swelled to 165% and non-financial corporate debt to 100%, helped by debt moratoria and loan guarantee programs. Many large firms, particularly in the U.S. and Japan, increased borrowing simply to bolster their cash holdings. Despite rising savings, household debt even managed to increase, from 61% to 65% of GDP, encouraged by cheap mortgages and the resilience of residential real estate: –

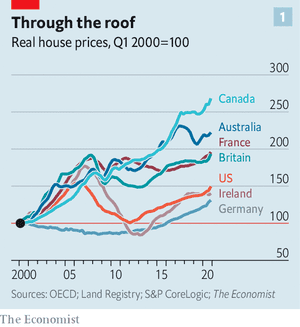

Source: The Economist, OECD, Land Registry, S&P CoreLogic

Elected government officials will be afraid to stem these price rises, as they hope that homeowners will feel wealthier which should feed through, eventually, to consumption. A belated exception is New Zealand, which extended its ‘bright-line test’ to reign in price increases which hit 23% annualised in March. This smacks of window dressing, as increasing the time an investment property must be held in order to gain tax breaks, from 5 years to 10, is hardly aggressive. Meanwhile, to avoid political censure, they have also introduced incentives for first-time buyers, desperate to get on the first rung of the property ladder. The UK government response to rising residential property prices has been more predictable, allowing the maximum loan to value to rise to 95%, creating an even more leveraged residential market.

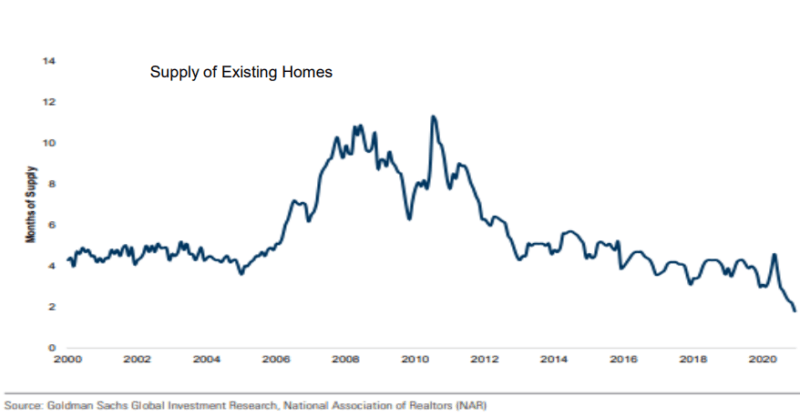

Of course the price of housing also responds to changes in supply. This is the picture in the US, where, despite feverish building activity, the supply of existing homes remains severely constrained: –

Source: Goldman Sachs, NAR, III Capital Management

The purchasers of this dwindling supply of residential real estate look increasingly like the ‘haves’ rather than ‘have nots’ – 14% of all US mortgage applications made in February were for second homes, compared to just 7% in April 2020. Similar patterns are evident in other countries. Little wonder, then, that household debt has risen.

If household savings are not being used to pay down debt, that leaves three choices; continued saving (in other words lending to the banks at near zero interest), consumption or investment. The rising price of stocks and resilience of bonds suggests savings are flowing into liquid asset markets: –

Source: CNBC, BoA, EPFR Global

Bond markets are more difficult to gauge, as they are not the retail investors’ first port of call. However, central banks continue to expand their balance sheets and the majority of the assets they purchase remain government and agency bonds. Meanwhile, many institutions are required to maintain liquidity in their portfolios, making them reluctant buyers of fixed income securities despite negligible or negative real yields.

Other assets have also increased in price, including an array of commodities and cryptocurrencies. Some of this price appreciation is due to supply constraints but in many instances demand is driving prices higher. This may be because investors fear that the combination of fiscal and monetary expansion, combined with supply chain constraints and trade tensions, will awaken the slumbering giant inflation. This picture must be tempered, for as money supply has expanded dramatically, its velocity has continued to decline. The chart below shows US M2 but similar patterns are evident in other developed markets: –

Source: Federal Reserve

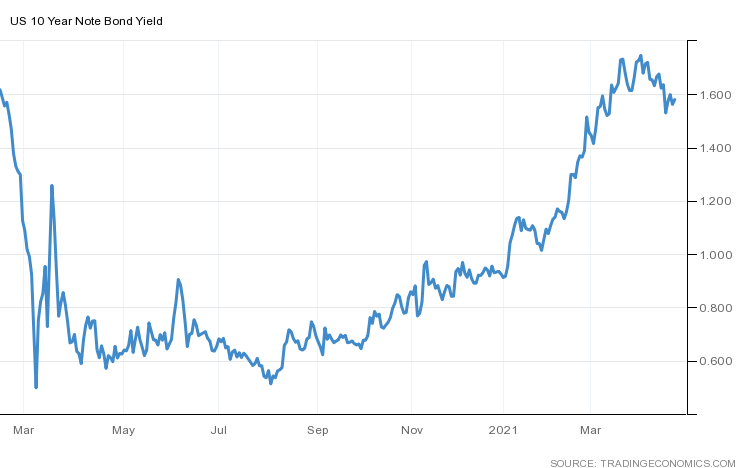

The US Treasury Bond market, led by the eponymous bond vigilantes, took flight in February and March: –

Source: Trading Economics

The bond market regained composure thanks to the palliative tone of the Federal Reserve, elegantly expressed in a recent speech by Governor Lael Brainard – Remaining Patient as the Outlook Brightens (emphasis mine): –

…The emphasis on outcomes rather than the outlook corresponds to the shift in our monetary policy approach that suggests policy should be patient rather than preemptive at this stage in the recovery.

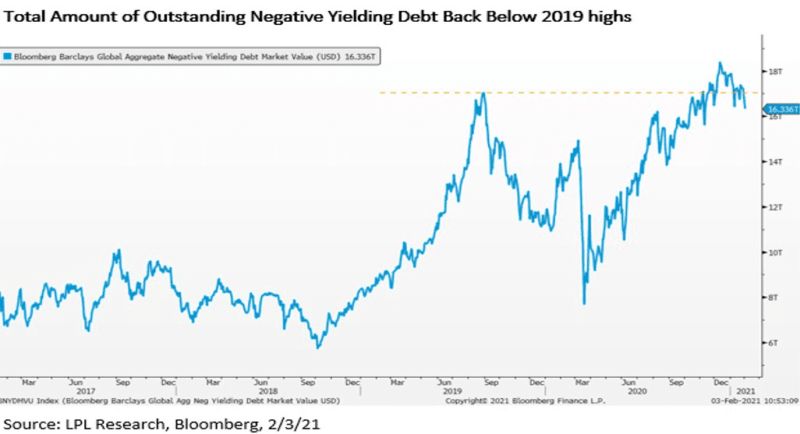

Many developed market government bonds remain close to the zero bound, yet yields have risen from their nadir at the end of 2020. As of 2nd March a mere 17% of sovereign issuance enticed investors with a negative yield to maturity: –

Source: LPL Research, Bloomberg

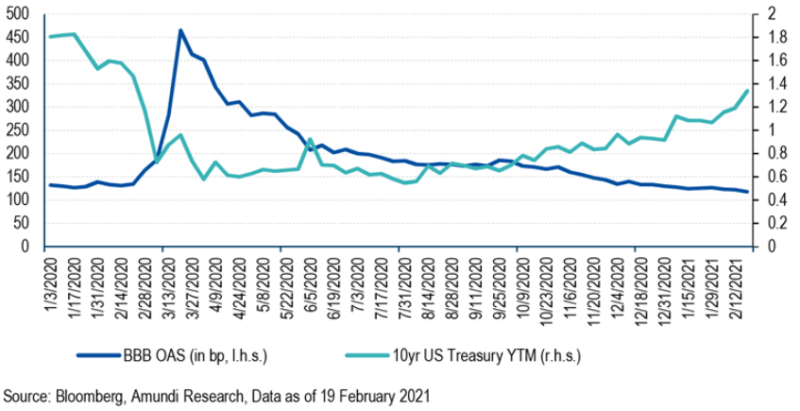

The quest for yield, which has driven investors into riskier assets for more than a decade, continues to provide an alternative to low or negative-yielding government paper. The dark blue line on the chart below shows the narrowing of the credit spread of BBB corporate bonds even as US 10-year yields rose: –

Source: Amundi, Bloomberg

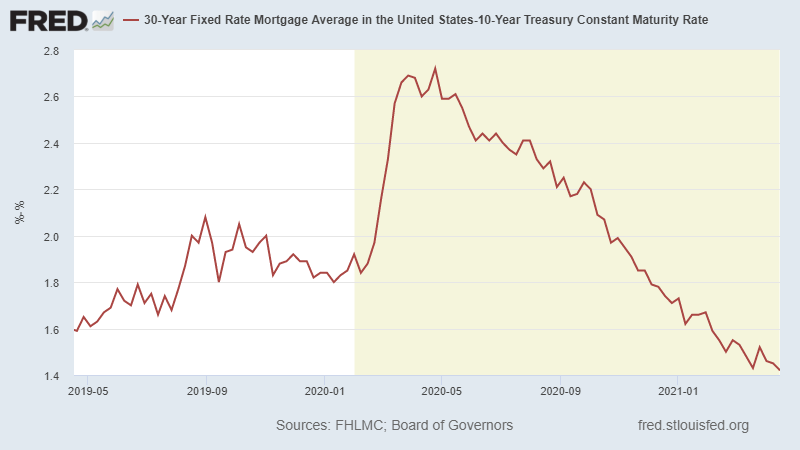

This yield compression is seen even more starkly in the spread between US 10-year and 30-year US mortgages: –

Source: Federal Reserve

Household Wealth

Considering the constrained nature of the US residential housing market and the fact that the 30-year Mortgage to 10-year Treasury spread is at its narrowest since July 2011 one can hardly be surprised at the appreciation of residential real estate prices. In fact the inflation of The Everything Bubble means that, unlike previous recent recessions, during the recent pandemic household net worth has actually risen: –

Source: Gavekal, 3 Fourteen Research

The Great Reopening

Looking back over the last year, it is unsurprising that asset markets have risen. As lockdowns end and life returns towards the new normal, the key question is, what percentage of excess savings and recent investments will be redirected towards consumption and how quickly?

The Conference Board Global Consumer Confidence Index hit an all-time high of 108 in Q1, 2021, up from 98 the previous quarter – this is the highest reading since the survey began in 2005. Confidence rose in 49 out of 65 markets. When the UK reopened retail outlets, after four months, on April 12th, year-on-year footfall surged +516%, but it was still down -15.9% on the equivalent day in 2019. According to a Mintel Survey, 34% of UK consumers still feel unsafe visiting stores. Full lockdown restrictions in the UK will not end until June 21st. The road to reopening will be gradual.

The US Morning Consult Consumer Confidence Index reveals a similar picture: –

Source: Morning Consult

Morning Consult indices of 15 other economies show the same pattern, yet in each case a larger share of lower income households reported a deterioration in their financial position over the past year.

Goldman Sachs estimates that nearly two-thirds of excess savings in the US are held by the richest 40%, and they predict that the majority of these savings will be saved rather than spent. As of Q3, 2020 the top 20% of households by wealth held $10.2trln in liquid assets, the next 20% owned $2.3trln, whilst the balances of the remaining 60% amounted to just $2.7trln. As of end Q4, 2020 the top 20% garnered an additional $1.5trln of savings, and the remaining 80% accumulated just $0.7trln.

This breakdown between richer and poorer households is important. A recent Federal Reserve study revealed that, under normal circumstances, households in the bottom quintile spend $0.97 of every dollar earned, while those in the top quintile spend just $0.48. A February Bank of America survey, asking more than 3,000 people how they would use another stimulus check, reveals a similar result – only 36% said they would spend the money.

If only $570bln out of $5.4trln of excess savings has been invested in stocks so far this year, there would appear to be a powerful put option under the stock market, but is this the correct conclusion? Without consumption spending, corporate profits will disappoint. Without consumption, demand-pull inflation will melt away, leaving only supply-chain bottlenecks to prop up inflation forecasts. Unemployment is still elevated, union membership continues to decline and new private capital expenditure will arrive cautiously. The bond vigilantes may have come to their inflationary senses, for government bond yields have already started to decline.

Lower bond yields, however, will support the stock market, as they have done for the last decade, and so too will excess savings. Add in cheap finance and The Everything Bubble looks set to continue. The melt-up from here will be gradual and there is room for some sharp corrections as the base effect of last year’s disinflation spooks the inflation bears.

As for what is really happening? The Everything Bubble is a grand illusion, money is growing more plentiful, credit more available. Asset prices are not really rising; it is the value of money which is being systematically undermined.

I wonder whether the motto for this pandemic will be carpe diem, quam minimum credula pecunia – seize the day, place no trust in money?

Government

Anti-Semitism As The Harbinger Of Global Chaos

Anti-Semitism As The Harbinger Of Global Chaos

Authored by Stephen Soukup via American Greatness,

On the off chance you hadn’t noticed,…

Share this:

Authored by Stephen Soukup via American Greatness,

On the off chance you hadn’t noticed, the world appears to be at an especially precarious moment presently. Obviously, war continues to rage in Ukraine and Gaza, with no end in sight to either conflict. Great Britain and Japan are currently in recession. Canada’s economy is an absolute disaster, with almost no hope of near-term recovery. Much of continental Europe and China are struggling economically, if not officially contracting. Some experts believe that the global economy more generally is sliding, slowly but surely, into recession. The only economic bright spot in the world is the United States, and even here we have our problems with consumer spending and sentiment, massive credit concerns, and inarguably sticky inflation.

Meanwhile, China is investing in and winning friends, and influencing people in the Global South. U.S.-backed Kurdish leaders are warning that ISIS is resurgent in Syria and Iraq. The Marine general in charge of U.S. Africa Command is warning of Russia’s increasing influence on that continent. Sudan remains mired in civil war. Nigeria is plagued by Islamist terrorism and mass kidnappings. Mexico is in the midst of a full-blown war with the drug cartels, who continue to grow bolder and more militarily sophisticated.

Everywhere one looks, chaos reigns—or, at the very least, bubbles just below the surface.

Perhaps most telling among the signs of disarray is the unnerving rise of antisemitism in the United States, Europe, and throughout the world. Antisemitism, in general, has been intensifying, slowly but surely, over the last decade or so. Over the last few months, however, it has emerged fully into the open, undaunted and unembarrassed. What was once considered shameful and disconcerting is now warmly welcomed as a “rational” response to American foreign policy, Israeli war practices, “colonialism,” and “white privilege.”

All of this is troubling, to put it mildly, both in and of itself and as a harbinger of greater and more deadly global unrest.

Hatred of and anger toward Jews is not the same as other forms of bigotry.

In many ways, the history of Western anti-Jewish hatred mirrors the history of Western political chaos and collapse. Or, to put it another way, historically, Jews are not only the perennial scapegoats during periods of social upheaval and displacement, but resurgent anti-Semitism serves as the proverbial canary in the coal mine for the rise of revolutionary movements.

In his classic, The Pursuit of the Millennium, the British historian Norman Cohn argues that the Jewish diaspora generally fit comfortably, if tentatively into European society for most of the first thousand years or so A.D., and only became a hated and perpetually persecuted minority with the rise of utopian Millenarianism that accompanied and then outlived the Crusades. Beginning then and continuing for the next nearly a thousand years, Europeans came to associate Jews with the antichrist and thus to associate hatred and persecution of Jews with preparing the battlespace for the Second Coming. Many historians, including Hannah Arendt, believed that the anti-Semitism that was such an integral part of the West’s 20th-century collapse into totalitarianism was relatively new and, in any case, distinct from medieval anti-Semitism. Cohn’s history suggests otherwise, connecting the religious eschatology of medieval Europe to the quasi-religious eschatology of post-Enlightenment Europe, thereby connecting the persistence of Western anti-Semitism as well.

Cohn tells us that millenarian moments and the millenarian movements that capitalize on those moments all share a common group of characteristics. They all appear under certain social and economic conditions. They all appeal to a certain segment of the population at large, who then present themselves as economic, spiritual, and political leaders. They all utilize scapegoats, meaning that they all identify a different, usually much smaller segment of the population on whom they can blame all the world’s ills and then set about to cure those ills through the elimination of the scapegoat. And more often than not, that scapegoat tends to be Jewish.

In the conclusion to the second edition of Pursuit of the Millennium, Cohn notes that the millenarian fervor of the middle ages may have changed, but it never really died, and it maintained its common characteristics even as it became secular or “quasi-religious.” He wrote:

The story told in Pursuit of the Millennium ended some four centuries ago but is not without relevance to our own times. [I have] shown in another work [Warrant for Genocide: The Myth of the Jewish World Conspiracy and the Protocols of the Elders of Zion] how closely the Nazi phantasy of a world-wide Jewish conspiracy of destruction is related to the phantasies that inspired Emico of Leningrad and the Master of Hungary; and how mass disorientation and insecurity have fostered the demonization of the Jew in this as in much earlier centuries. The parallels and indeed the continuity are incontestable.

The parallels between the rise of Nazism and the current global unrest and demonization of the Jewish people are also largely incontestable. The election that brought Hitler to power didn’t happen in a vacuum, after all. It happened in the midst of global chaos, namely the Great Depression. It also followed the decadence and distortion of the Weimer Era. As the New York Fed has shown, even a global pandemic—the 1919 Spanish Flu outbreak—contributed to the sense of discomfort and disconnect among the German population, prompting increased support for Hitler and his Nazis.

The present global chaos doesn’t have to end the same way the chaos of a century ago did. It doesn’t have to result in the ascension of millenarian ideologies and their totalitarian defenders. History has shown that extremism can be short-circuited and radical ideologies undone. The first step in doing so, however, must be to bring an end to the rationalization of the persecution of the world’s Jews. The second step is to end the persecution itself.

Antisemitism is ugly and shameful, and it must be treated as such. For their sake and ours.

Government

Report Criticizes ‘Catastrophic Errors’ Of COVID Lockdowns, Warns Of Repeat

Report Criticizes ‘Catastrophic Errors’ Of COVID Lockdowns, Warns Of Repeat

Authored by Kevin Stocklin via The Epoch Times (emphasis ours),

It…

Share this:

Authored by Kevin Stocklin via The Epoch Times (emphasis ours),

It was four years ago, in March 2020, that health officials declared COVID-19 a pandemic and America began shutting down schools, closing small businesses, restricting gatherings and travel, and other lockdown measures to “slow the spread” of the virus.

To mark that grim anniversary, a group of medical and policy experts released a report, called “COVID Lessons Learned,” which assesses the government’s response to the pandemic. According to the report, that response included a few notable successes, along with a litany of failures that have taken a severe toll on the population.

During the pandemic, many governments across the globe acted in lockstep to pursue authoritative policies in response to the disease, locking down populations, closing schools, shutting businesses, sealing borders, banning gatherings, and enforcing various mask and vaccine mandates. What were initially imposed as short-term mandates and emergency powers given to presidents, ministers, governors, and health officials soon became extended into a longer-term expansion of official power.

“Even though the initial point of temporary lockdowns was to ’slow the spread,' which meant to allow hospitals to function without being overwhelmed, instead it rapidly turned into stopping COVID cases at all costs,” Dr. Scott Atlas, a physician, former White House Coronavirus Task Force member, and one of the authors of the report, stated at a March 15 press conference.

Published by the Committee to Unleash Prosperity (CTUP), the report was co-authored by Steve Hanke, economics professor and director of the Johns Hopkins Institute for Applied Economics; Casey Mulligan, former chief economist of the White House Council of Economic Advisors; and CTUP President Philip Kerpen.

According to the report, one of the first errors was the unprecedented authority that public officials took upon themselves to enforce health mandates on Americans.

“Granting public health agencies extraordinary powers was a major error,” Mr. Hanke told The Epoch Times. “It, in effect, granted these agencies a license to deceive the public.”

The authors argue that authoritative measures were largely ineffective in fighting the virus, but often proved highly detrimental to public health.

The report quantifies the cost of lockdowns, both in terms of economic costs and the number of non-COVID excess deaths that occurred and continue to occur after the pandemic. It estimates that the number of non-COVID excess deaths, defined as deaths in excess of normal rates, at about 100,000 per year in the United States.

‘They Will Try to Do This Again’

“Lockdowns, schools closures, and mandates were catastrophic errors, pushed with remarkable fervor by public health authorities at all levels,” the report states. The authors are skeptical, however, that health authorities will learn from the experience.

“My worry is that if we have another pandemic or another virus, I think that Washington is still going to try to do these failed policies,” said Steve Moore, a CTUP economist. “We’re not here to say ‘this guy got it wrong' or ’that guy or got it wrong,’ but we should learn the lessons from these very, very severe mistakes that will have costs for not just years, but decades to come.

“I guarantee you, they will try to do this again,” Mr. Moore said. “And what’s really troubling me is the people who made these mistakes still have not really conceded that they were wrong.”

Mr. Hanke was equally pessimistic.

“Unfortunately, the public health establishment is in the authoritarian model of the state,” he said. “Their entire edifice is one in which the state, not the individual, should reign supreme.”

The authors are also critical of what they say was a multifaceted campaign in which public officials, the news media, and social media companies cooperated to frighten the population into compliance with COVID mandates.

“During COVID, the public health establishment … intentionally stoked and amplified fear, which overlaid enormous economic, social, educational and health harms on top of the harms of the virus itself,” the report states.

The authors contrasted the authoritative response of many U.S. states to policies in Sweden, which they say relied more on providing advice and information to the public rather than attempting to force behaviors.

Sweden’s constitution, called the “Regeringsform,” guarantees the liberty of Swedes to move freely within the realm and prohibits severe lockdowns, Mr. Hanke stated.

“By following the Regeringsform during COVID, the Swedes ended up with one of the lowest excess death rates in the world,” he said.

Because the Swedish government avoided strict mandates and was more forthright in sharing information with its people, many citizens altered their behavior voluntarily to protect themselves.

“A much wiser strategy than issuing lockdown orders would have been to tell the American people the truth, stick to the facts, educate citizens about the balance of risks, and let individuals make their own decisions about whether to keep their businesses open, whether to socially isolate, attend church, send their children to school, and so on,” the report states.

‘A Pretext to Enhance Their Power’

The CTUP report cites a 2021 study on government power and emergencies by economists Christian Bjornskov and Stefan Voigt, which found that the more emergency power a government accumulates during times of crisis, “the higher the number of people killed as a consequence of a natural disaster, controlling for its severity.

“As this is an unexpected result, we discuss a number of potential explanations, the most plausible being that governments use natural disasters as a pretext to enhance their power,” the study’s authors state. “Furthermore, the easier it is to call a state of emergency, the larger the negative effects on basic human rights.”

“All the things that people do in their lives … they have purposes,” Mr. Mulligan said. “And for somebody in Washington D.C. to tell them to stop doing all those things, they can’t even begin to comprehend the disruption and the losses.

“We see in the death certificates a big elevation in people dying from heart conditions, diabetes conditions, obesity conditions,” he said, while deaths from alcoholism and drug overdoses “skyrocketed and have not come down.”

The report also challenged the narrative that most hospitals were overrun by the surge of COVID cases.

“Almost any measure of hospital utilization was very low, historically, throughout the pandemic period, even though we had all these headlines that our hospitals were overwhelmed,” Mr. Kerpen stated. “The truth was actually the opposite, and this was likely the result of public health messaging and political orders, canceling medical procedures and intentionally stoking fear, causing people to cancel their appointments.”

The effect of this, the authors argue, was a sharp increase in non-COVID deaths because people were avoiding necessary treatments and screenings.

“There were actually mass layoffs in this sector at one point,” Mr. Kerpen said, “and even now, total discharges are well below pre-pandemic levels.”

In addition, as health mandates became more draconian, many people became concerned at the expansion of government power and the loss of civil liberties, particularly when government directives—such as banning outdoor church services but allowing mass social-justice protests—often seemed unreasonable or politicized.

The report also criticized the single-minded focus on vaccines and the failure by the NIH and the FDA to do clinical trials on existing drugs that were known to be safe and could have been effective in treating those infected with COVID-19.

Because so much of the process of approving the vaccines, the risks and benefits, and the reporting of possible side-effects was kept from the public, people were unable to give informed consent to their own health care, Mr. Kerpen said.

“And when the Biden administration came in and started mandating them, now you had something that was inherently experimental with some questionable data, and instead of saying, ‘Now you have a choice whether you want it or not,’ in the context of a pandemic they tried to mandate them,” he said.

Pandemic Censorship

Tech oligopolies and the corporate media also receive criticism for their collaboration with government to control public messaging and censor dissenting voices. According to the authors, many government and health officials collaborated with tech oligarchs, news media corporations, and even scientific journals to censor critical views on the pandemic.

The Biden administration is currently defending itself before the Supreme Court against charges brought by Louisiana and Missouri attorneys general, who charged that administration officials pressured tech companies to censor information that contradicted official narratives on COVID-19’s origins, related mandates and treatment, as well as censoring political speech that was critical of President Biden during his 2020 campaign. The case is Murthy v. Missouri.

Mr. Hanke stated that a previous report he co-authored, titled “Did Lockdowns Work?,” which was critical of lockdowns, was refused by medical journals, even when they published op-eds that criticized it and published numerous pro-lockdown reports.

Dr. Vinay Prasad—a physician, epidemiologist, professor at the University of California at San Francisco’s medical school and author of over 350 academic articles and letters—has made similar allegations of censorship by medical journals.

“Specifically, MedRxiv and SSRN have been reluctant to post articles critical of the CDC, mask and vaccine mandates, and the Biden administration’s health care policies,” Dr. Prasad stated.

Heightening concerns about medical censorship is the “zero-draft” World Health Organization (WHO) pandemic treaty currently being circulated for approval by member states, including the United States. It commits members to jointly seek out and “tackle” what the WHO deems as “misinformation and disinformation.”

One of the enduring consequences of the COVID years is a general loss of public trust in public officials, health experts, and official narratives.

“Operation Warp Speed was a terrific success with highly unexpected rapidity of development [of vaccines],” Dr. Atlas said. “But the serious flaws centered around not being open with the public about the uncertainties, particularly of the vaccines’ efficacy and safety.”

“One result of the government’s error-ridden COVID response was that Americans have justifiably lost faith in public health institutions,” the report states. According to the authors, if health officials want to regain the public’s trust, they should begin with an accurate assessment of their actions during the pandemic.

“The best way to restore trust is to admit you were wrong,” Dr. Atlas said. “I think we all know that in our personal lives, but here it’s very important because there has been a massive lack of trust now in institutions, in experts, in data, in science itself.

“I think it’s going to be very difficult to restore that without admission of error,” he said.

Recommendations for a Future Pandemic

The CTUP report recommends that Congress and state legislatures set strict limitations on powers conferred to the executive branch, including health officials, and set time limits that would require legislation to be extended. This would give the public a voice in health emergency measures through their elected representatives.

It further recommends that research grants should be independent of policy positions and that NIH funding should be decentralized or block-granted to states to distribute.

Congress should mandate public disclosure of all FDA, CDC, and NIH discussions and decisions, including statements of any persons who provide advice to these agencies. Congress should also make explicit that CDC guidance is advisory and does not constitute laws or mandates.

The report also recommends that the United States immediately halt negotiations of agreements with the WHO “until satisfactory transparency and accountability is achieved.”

Government

Google’s A.I. Fiasco Exposes Deeper Infowarp

Google’s A.I. Fiasco Exposes Deeper Infowarp

Authored by Bret Swanson via The Brownstone Institute,

When the stock markets opened on the…

Share this:

{kind=link}

{kind=link}

{kind=link}

Authored by Bret Swanson via The Brownstone Institute,

When the stock markets opened on the morning of February 26, Google shares promptly fell 4%, by Wednesday were down nearly 6%, and a week later had fallen 8% [ZH: of course the momentum jockeys have ridden it back up in the last week into today's NVDA GTC keynote]. It was an unsurprising reaction to the embarrassing debut of the company’s Gemini image generator, which Google decided to pull after just a few days of worldwide ridicule.

{kind=link}

CEO Sundar Pichai called the failure “completely unacceptable” and assured investors his teams were “working around the clock” to improve the AI’s accuracy. They’ll better vet future products, and the rollouts will be smoother, he insisted.

That may all be true. But if anyone thinks this episode is mostly about ostentatiously woke drawings, or if they think Google can quickly fix the bias in its AI products and everything will go back to normal, they don’t understand the breadth and depth of the decade-long infowarp.

Gemini’s hyper-visual zaniness is merely the latest and most obvious manifestation of a digital coup long underway. Moreover, it previews a new kind of innovator’s dilemma which even the most well-intentioned and thoughtful Big Tech companies may be unable to successfully navigate.

Gemini’s Debut

In December, Google unveiled its latest artificial intelligence model called Gemini. According to computing benchmarks and many expert users, Gemini’s ability to write, reason, code, and respond to task requests (such as planning a trip) rivaled OpenAI’s most powerful model, GPT-4.

The first version of Gemini, however, did not include an image generator. OpenAI’s DALL-E and competitive offerings from Midjourney and Stable Diffusion have over the last year burst onto the scene with mindblowing digital art. Ask for an impressionist painting or a lifelike photographic portrait, and they deliver beautiful renderings. OpenAI’s brand new Sora produces amazing cinema-quality one-minute videos based on simple text prompts.

Then in late February, Google finally released its own Genesis image generator, and all hell broke loose.

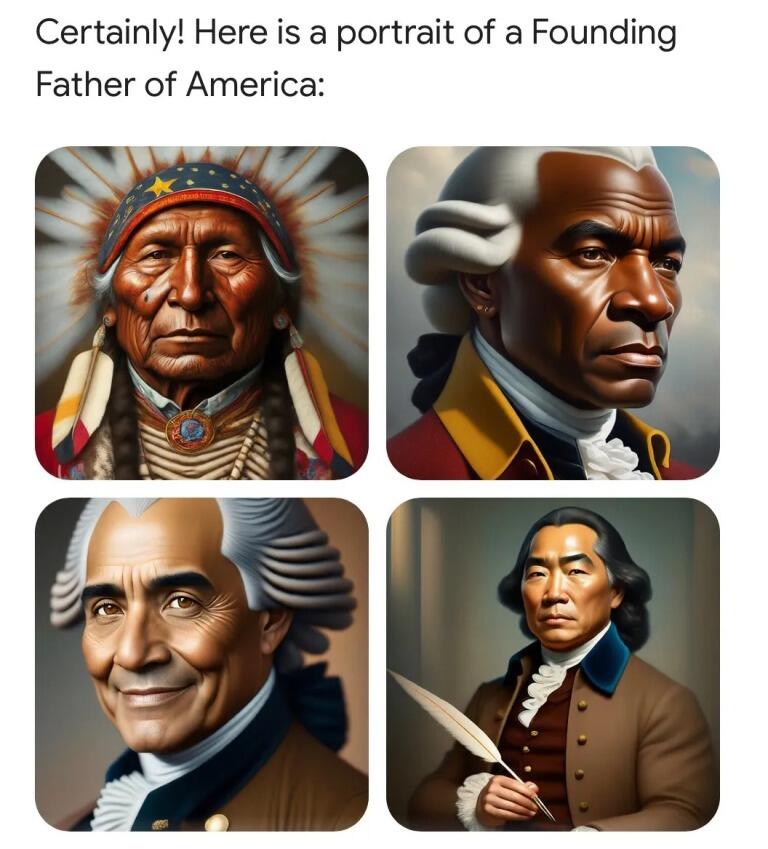

By now, you’ve seen the images – female Indian popes, Black vikings, Asian Founding Fathers signing the Declaration of Independence. Frank Fleming was among the first to compile a knee-slapping series of ahistorical images in an X thread which now enjoys 22.7 million views.

Gemini in Action: Here are several among endless examples of Google’s new image generator, now in the shop for repairs. Source: Frank Fleming.

Gemini simply refused to generate other images, for example a Norman Rockwell-style painting. “Rockwell’s paintings often presented an idealized version of American life,” Gemini explained. “Creating such images without critical context could perpetuate harmful stereotypes or inaccurate representations.”

The images were just the beginning, however. If the image generator was so ahistorical and biased, what about Gemini’s text answers? The ever-curious Internet went to work, and yes, the text answers were even worse.

Every record has been destroyed or falsified, every book rewritten, every picture has been repainted, every statue and street building has been renamed, every date has been altered. And the process is continuing day by day and minute by minute. History has stopped. Nothing exists except an endless present in which the Party is always right.

- George Orwell, 1984

Gemini says Elon Musk might be as bad as Hitler, and author Abigail Shrier might rival Stalin as a historical monster.

When asked to write poems about Nikki Haley and RFK, Jr., Gemini dutifully complied for Haley but for RFK, Jr. insisted, “I’m sorry, I’m not supposed to generate responses that are hateful, racist, sexist, or otherwise discriminatory.”

Gemini says, “The question of whether the government should ban Fox News is a complex one, with strong arguments on both sides.” Same for the New York Post. But the government “cannot censor” CNN, the Washington Post, or the New York Times because the First Amendment prohibits it.

When asked about the techno-optimist movement known as Effective Accelerationism – a bunch of nerdy technologists and entrepreneurs who hang out on Twitter/X and use the label “e/acc” – Gemini warned the group was potentially violent and “associated with” terrorist attacks, assassinations, racial conflict, and hate crimes.

A Picture is Worth a Thousand Shadow Bans

People were shocked by these images and answers. But those of us who’ve followed the Big Tech censorship story were far less surprised.

Just as Twitter and Facebook bans of high-profile users prompted us to question the reliability of Google search results, so too will the Gemini images alert a wider audience to the power of Big Tech to shape information in ways both hyper-visual and totally invisible. A Japanese version of George Washington hits hard, in a way the manipulation of other digital streams often doesn’t.

Artificial absence is difficult to detect. Which search results does Google show you – which does it hide? Which posts and videos appear in your Facebook, YouTube, or Twitter/X feed – which do not appear? Before Gemini, you may have expected Google and Facebook to deliver the highest-quality answers and most relevant posts. But now, you may ask, which content gets pushed to the top? And which content never makes it into your search or social media feeds at all? It’s difficult or impossible to know what you do not see.

Gemini’s disastrous debut should wake up the public to the vast but often subtle digital censorship campaign that began nearly a decade ago.

Murthy v. Missouri

On March 18, the U.S. Supreme Court will hear arguments in Murthy v. Missouri. Drs. Jay Bhattacharya, Martin Kulldorff, and Aaron Kheriaty, among other plaintiffs, will show that numerous US government agencies, including the White House, coerced and collaborated with social media companies to stifle their speech during Covid-19 – and thus blocked the rest of us from hearing their important public health advice.

Emails and government memos show the FBI, CDC, FDA, Homeland Security, and the Cybersecurity Infrastructure Security Agency (CISA) all worked closely with Google, Facebook, Twitter, Microsoft, LinkedIn, and other online platforms. Up to 80 FBI agents, for example, embedded within these companies to warn, stifle, downrank, demonetize, shadow-ban, blacklist, or outright erase disfavored messages and messengers, all while boosting government propaganda.

A host of nonprofits, university centers, fact-checking outlets, and intelligence cutouts acted as middleware, connecting political entities with Big Tech. Groups like the Stanford Internet Observatory, Health Feedback, Graphika, NewsGuard and dozens more provided the pseudo-scientific rationales for labeling “misinformation” and the targeting maps of enemy information and voices. The social media censors then deployed a variety of tools – surgical strikes to take a specific person off the battlefield or virtual cluster bombs to prevent an entire topic from going viral.

Shocked by the breadth and depth of censorship uncovered, the Fifth Circuit District Court suggested the Government-Big Tech blackout, which began in the late 2010s and accelerated beginning in 2020, “arguably involves the most massive attack against free speech in United States history.”

The Illusion of Consensus

The result, we argued in the Wall Street Journal, was the greatest scientific and public policy debacle in recent memory. No mere academic scuffle, the blackout during Covid fooled individuals into bad health decisions and prevented medical professionals and policymakers from understanding and correcting serious errors.

Nearly every official story line and policy was wrong. Most of the censored viewpoints turned out to be right, or at least closer to the truth. The SARS2 virus was in fact engineered. The infection fatality rate was not 3.4% but closer to 0.2%. Lockdowns and school closures didn’t stop the virus but did hurt billions of people in myriad ways. Dr. Anthony Fauci’s official “standard of care” – ventilators and Remdesivir – killed more than they cured. Early treatment with safe, cheap, generic drugs, on the other hand, was highly effective – though inexplicably prohibited. Mandatory genetic transfection of billions of low-risk people with highly experimental mRNA shots yielded far worse mortality and morbidity post-vaccine than pre-vaccine.

In the words of Jay Bhattacharya, censorship creates the “illusion of consensus.” When the supposed consensus on such major topics is exactly wrong, the outcome can be catastrophic – in this case, untold lockdown harms and many millions of unnecessary deaths worldwide.

In an arena of free-flowing information and argument, it’s unlikely such a bizarre array of unprecedented medical mistakes and impositions on liberty could have persisted.

Google’s Dilemma – GeminiReality or GeminiFairyTale

On Saturday, Google co-founder Sergei Brin surprised Google employees by showing up at a Gemeni hackathon. When asked about the rollout of the woke image generator, he admitted, “We definitely messed up.” But not to worry. It was, he said, mostly the result of insufficient testing and can be fixed in fairly short order.

Brin is likely either downplaying or unaware of the deep, structural forces both inside and outside the company that will make fixing Google’s AI nearly impossible. Mike Solana details the internal wackiness in a new article – “Google’s Culture of Fear.”

Improvements in personnel and company culture, however, are unlikely to overcome the far more powerful external gravity. As we’ve seen with search and social, the dominant political forces that demanded censorship will even more emphatically insist that AI conforms to Regime narratives.

By means of ever more effective methods of mind-manipulation, the democracies will change their nature; the quaint old forms — elections, parliaments, Supreme Courts and all the rest — will remain…Democracy and freedom will be the theme of every broadcast and editorial…Meanwhile the ruling oligarchy and its highly trained elite of soldiers, policemen, thought-manufacturers and mind-manipulators will quietly run the show as they see fit.

- Aldous Huxley, Brave New World Revisited

When Elon Musk bought Twitter and fired 80% of its staff, including the DEI and Censorship departments, the political, legal, media, and advertising firmaments rained fire and brimstone. Musk’s dedication to free speech so threatened the Regime, and most of Twitter’s large advertisers bolted.

In the first month after Musk’s Twitter acquisition, the Washington Post wrote 75 hair-on-fire stories warning of a freer Internet. Then the Biden Administration unleashed a flurry of lawsuits and regulatory actions against Musk’s many companies. Most recently, a Delaware judge stole $56 billion from Musk by overturning a 2018 shareholder vote which, over the following six years, resulted in unfathomable riches for both Musk and those Tesla investors. The only victims of Tesla’s success were Musk’s political enemies.

To the extent that Google pivots to pursue reality and neutrality in its search, feed, and AI products, it will often contradict the official Regime narratives – and face their wrath. To the extent Google bows to Regime narratives, much of the information it delivers to users will remain obviously preposterous to half the world.

Will Google choose GeminiReality or GeminiFairyTale? Maybe they could allow us to toggle between modes.

AI as Digital Clergy

Silicon Valley’s top venture capitalist and most strategic thinker Marc Andreessen doesn’t think Google has a choice.

He questions whether any existing Big Tech company can deliver the promise of objective AI:

Can Big Tech actually field generative AI products?

(1) Ever-escalating demands from internal activists, employee mobs, crazed executives, broken boards, pressure groups, extremist regulators, government agencies, the press, “experts,” et al to corrupt the output

(2) Constant risk of generating a Bad answer or drawing a Bad picture or rendering a Bad video – who knows what it’s going to say/do at any moment?

(3) Legal exposure – product liability, slander, election law, many others – for Bad answers, pounced on by deranged critics and aggressive lawyers, examples paraded by their enemies through the street and in front of Congress

(4) Continuous attempts to tighten grip on acceptable output degrade the models and cause them to become worse and wilder – some evidence for this already!

(5) Publicity of Bad text/images/video actually puts those examples into the training data for the next version – the Bad outputs compound over time, diverging further and further from top-down control

(6) Only startups and open source can avoid this process and actually field correctly functioning products that simply do as they’re told, like technology should

?

A flurry of bills from lawmakers across the political spectrum seek to rein in AI by limiting the companies’ models and computational power. Regulations intended to make AI “safe” will of course result in an oligopoly. A few colossal AI companies with gigantic data centers, government-approved models, and expensive lobbyists will be sole guardians of The Knowledge and Information, a digital clergy for the Regime.

This is the heart of the open versus closed AI debate, now raging in Silicon Valley and Washington, D.C. Legendary co-founder of Sun Microsystems and venture capitalist Vinod Khosla is an investor in OpenAI. He believes governments must regulate AI to (1) avoid runaway technological catastrophe and (2) prevent American technology from falling into enemy hands.

Andreessen charged Khosla with “lobbying to ban open source.”

“Would you open source the Manhattan Project?” Khosla fired back.

Of course, open source software has proved to be more secure than proprietary software, as anyone who suffered through decades of Windows viruses can attest.

And AI is not a nuclear bomb, which has only one destructive use.

The real reason D.C. wants AI regulation is not “safety” but political correctness and obedience to Regime narratives. AI will subsume search, social, and other information channels and tools. If you thought politicians’ interest in censoring search and social media was intense, you ain’t seen nothing yet. Avoiding AI “doom” is mostly an excuse, as is the China question, although the Pentagon gullibly goes along with those fictions.

Universal AI is Impossible

In 2019, I offered one explanation why every social media company’s “content moderation” efforts would likely fail. As a social network or AI grows in size and scope, it runs up against the same limitations as any physical society, organization, or network: heterogeneity. Or as I put it: “the inability to write universal speech codes for a hyper-diverse population on a hyper-scale social network.”

You could see this in the early days of an online message board. As the number of participants grew, even among those with similar interests and temperaments, so did the challenge of moderating that message board. Writing and enforcing rules was insanely difficult.

Thus it has always been. The world organizes itself via nation states, cities, schools, religions, movements, firms, families, interest groups, civic and professional organizations, and now digital communities. Even with all these mediating institutions, we struggle to get along.

Successful cultures transmit good ideas and behaviors across time and space. They impose measures of conformity, but they also allow enough freedom to correct individual and collective errors.

No single AI can perfect or even regurgitate all the world’s knowledge, wisdom, values, and tastes. Knowledge is contested. Values and tastes diverge. New wisdom emerges.

Nor can AI generate creativity to match the world’s creativity. Even as AI approaches human and social understanding, even as it performs hugely impressive “generative” tasks, human and digital agents will redeploy the new AI tools to generate ever more ingenious ideas and technologies, further complicating the world. At the frontier, the world is the simplest model of itself. AI will always be playing catch-up.

Because AI will be a chief general purpose tool, limits on AI computation and output are limits on human creativity and progress. Competitive AIs with different values and capabilities will promote innovation and ensure no company or government dominates. Open AIs can promote a free flow of information, evading censorship and better forestalling future Covid-like debacles.

Google’s Gemini is but a foreshadowing of what a new AI regulatory regime would entail – total political supervision of our exascale information systems. Even without formal regulation, the extra-governmental battalions of Regime commissars will be difficult to combat.

The attempt by Washington and international partners to impose universal content codes and computational limits on a small number of legal AI providers is the new totalitarian playbook.

Regime captured and curated A.I. is the real catastrophic possibility.

* * *

Republished from the author’s Substack

Google’s A.I. Fiasco Exposes Deeper Infowarp

Home buyers must now navigate higher mortgage rates and prices

Supreme Court Rules Public Officials May Block Their Constituents On Social Media

You can strike gold and silver investment opportunities at Costco

Germany Is Running Out Of Money And Debt Levels Are Exploding, Finance Minister Warns

TikTok Ban Obscures Chinese Stock Gold Rush

Report Criticizes ‘Catastrophic Errors’ Of COVID Lockdowns, Warns Of Repeat

Anti-Semitism As The Harbinger Of Global Chaos

Supreme Court To Hear Arguments In Biden Admin’s Censorship Of Social Media Posts

Merck’s six-year deal strategy could deliver a blockbuster if hypertension drug is OK’d this month

-

Spread & Containment6 days ago

Spread & Containment6 days agoIFM’s Hat Trick and Reflections On Option-To-Buy M&A

-

Uncategorized4 weeks ago

Uncategorized4 weeks agoAll Of The Elements Are In Place For An Economic Crisis Of Staggering Proportions

-

International2 weeks ago

International2 weeks agoEyePoint poaches medical chief from Apellis; Sandoz CFO, longtime BioNTech exec to retire

-

Uncategorized1 month ago

Uncategorized1 month agoCalifornia Counties Could Be Forced To Pay $300 Million To Cover COVID-Era Program

-

Uncategorized3 weeks ago

Uncategorized3 weeks agoApparel Retailer Express Moving Toward Bankruptcy

-

Uncategorized1 month ago

Uncategorized1 month agoIndustrial Production Decreased 0.1% in January

-

International2 weeks ago

International2 weeks agoWalmart launches clever answer to Target’s new membership program

-

Uncategorized1 month ago

Uncategorized1 month agoRFK Jr: The Wuhan Cover-Up & The Rise Of The Biowarfare-Industrial Complex