Spread & Containment

The ECB’s Financial Suttee

The ECB’s Financial Suttee

Authored by Alasdair Macleod via GoldMoney.com,

The European Commission is failing. Its response to Brexit and the pandemic, where it is now threatening emergency powers in order to secure vaccines is a latest…

Share this:

Authored by Alasdair Macleod via GoldMoney.com,

The European Commission is failing. Its response to Brexit and the pandemic, where it is now threatening emergency powers in order to secure vaccines is a latest throw of the political dice. Even before this development markets were getting the message with capital flight worsening.

The only thing that holds the Commission together is the magic money tree that is the ECB.

Following the recent change in the Commission’s leadership, the political dysfunction in Brussels is a new challenge for the ECB. It is already juggling with overindebted member states, a global rise in bond yields, a rotten settlement system and commercial banks both over-leveraged and with mounting pandemic-related bad debts.

It really is a horror show in the making.

Introduction

This week, the ECB took the next step towards its inevitable destruction of itself, its system and its currency. This ending, a sort of financial suttee where it joins the failing EU Commission on it funeral pyre, is plainly inevitable, and will increasingly be seen to be so.

On 3 March, Bloomberg reported “European Central Bank policy makers are downplaying concerns over rising bond yields, suggesting they can manage the risk to the euro-area economy with verbal interventions including a pledge to accelerate bond-buying if needed.”

Then last week, the story changed: the ECB vowed that: “Based on a joint assessment of financing conditions and the inflation outlook, the Governing Council expects purchases under the PEPP over the next quarter to be conducted at a significantly higher pace than during the first months of this year”.

What had happened is that bond yields had started to rise, threatening to bankrupt the whole Eurozone network if the trend continued. That network is like a basket of rotten apples. It is the consequence not just of a flawed system, but of policies introduced to rescue Spain from soaring bond yields in 2012. That was when Mario Draghi, the ECB’s President said he was ready to do whatever it takes to save the euro, adding, “Believe me, it will be enough”.

It was. The threat of intervention was enough to drive Spanish bond yields down and is probably behind the complacent thinking in the 3 March statement. But as the other bookend to Draghi’s promise to deploy bond purchasing programmes, Lagarde’s promised intervention is of necessity far larger. And there is the market problem, encapsulated in the saying, “fool me once, shame on you; fool me twice shame on me”. Does the ECB really think it is above this logic?

The euro started with the promise of being a far more stable currency replacement for national currencies, particularly the Italian lira, the Spanish peseta, the French franc, and the Greek drachma. The first president of the ECB, Wim Duisenberg, resigned halfway during his term to make way for Jean-Claude Trichet, who was a French statist from the École Nationale d’Administration and a career civil servant. His was a political appointment, promoted by the French on a mixture of nationalism and a determination to neutralise the sound money advocates in Germany.

From the outset, the ECB pursued inflationist policies. Unlike the Bundesbank which closely monitored the money supply and paid attention to little else, the ECB adopted a wide range of economic indicators, allowing it to shift its focus from money to employment, confidence polls, long-term interest rates, output measures and others, allowing a fully flexible attitude to money. Unlike the independent Bundesbank, the ECB is intensely political, masquerading as an independent institution. But there is now no question that its primary purpose is to ensure Eurozone governments’ profligate spending is always financed, “whatever it takes”. Our attention returns to the statement from the ECB this week, because rising bond yields threaten the ability of the ECB to finance in perpetuity increasing government deficits in the PIGS and France. Fool us once…

Business and money is beginning to leave

Traditionally, big business has loved big government. Not only is it a source of funds and preferences but it is an opportunity to lobby for regulations to the disadvantage of smaller competitors. In short, Brussels is the centre of European crony capitalism, which is why big business was set against Brexit. The CBI, representing big British industrial interests, lobbied hard to remain.

But since Brexit, the EU has advertised its own insecurity by waging a trade war against British imports, tying them up in needless bureaucracy. At the same time, the successful fast-tracking of the Oxford vaccine and its rapid deployment in the UK along with the Pfizer equivalent, compares with the abject failure of the Commission to roll them out across its member states, leading to a panicked reaction. On 27 January, officials raided AstraZeneca’s facility in Brussels, following production problems which had reduced the amount of its yet to be approved supply to the EU.

The message sent to all big businesses was clear. Investing in EU production facilities had become less attractive due to the implied threat to property rights. The Brussels lobbying game fundamentally changed for both European and international corporations. At the same time, the Commission attempted to move financial market clearing services out of London. The threat to freedom of capital flows in future became obvious to financial entities. According to HSBC, capital outflows reached €500bn in the fourth quarter of last year, representing an annualised pace of 20% of GDP, with half of it in December alone.

It is said that when you are in a hole you should stop digging. Not a bit of it: only yesterday, the Commission’s President threatened to invoke Article 122, allowing the EU to seize AstraZeneca’s factories and ban vaccine exports to the UK. There could hardly be a clearer threat to property rights for any multinational with offices and production facilities in Europe. Not only has the EU become a no-go for future industrial investment, but portfolio outflows seem sure to continue and accelerate further. And not only is the socialising Commission a failing organisation, but its downfall is becoming increasingly obvious for its member states to see.

The socialist ideal is coming unstuck

It is easy to not fully appreciate that the EU has turned into an intensely socialistic project, with a supranational commission overriding national governments, forcing them to conform to a centralised political ideal. Easy to forget, because the EU’s embedded socialism is almost never mentioned. Financially, it follows from redistribution policies whereby the majority of the Eurozone population is subsidised by savers in the Northern countries, centred on German’s savers.

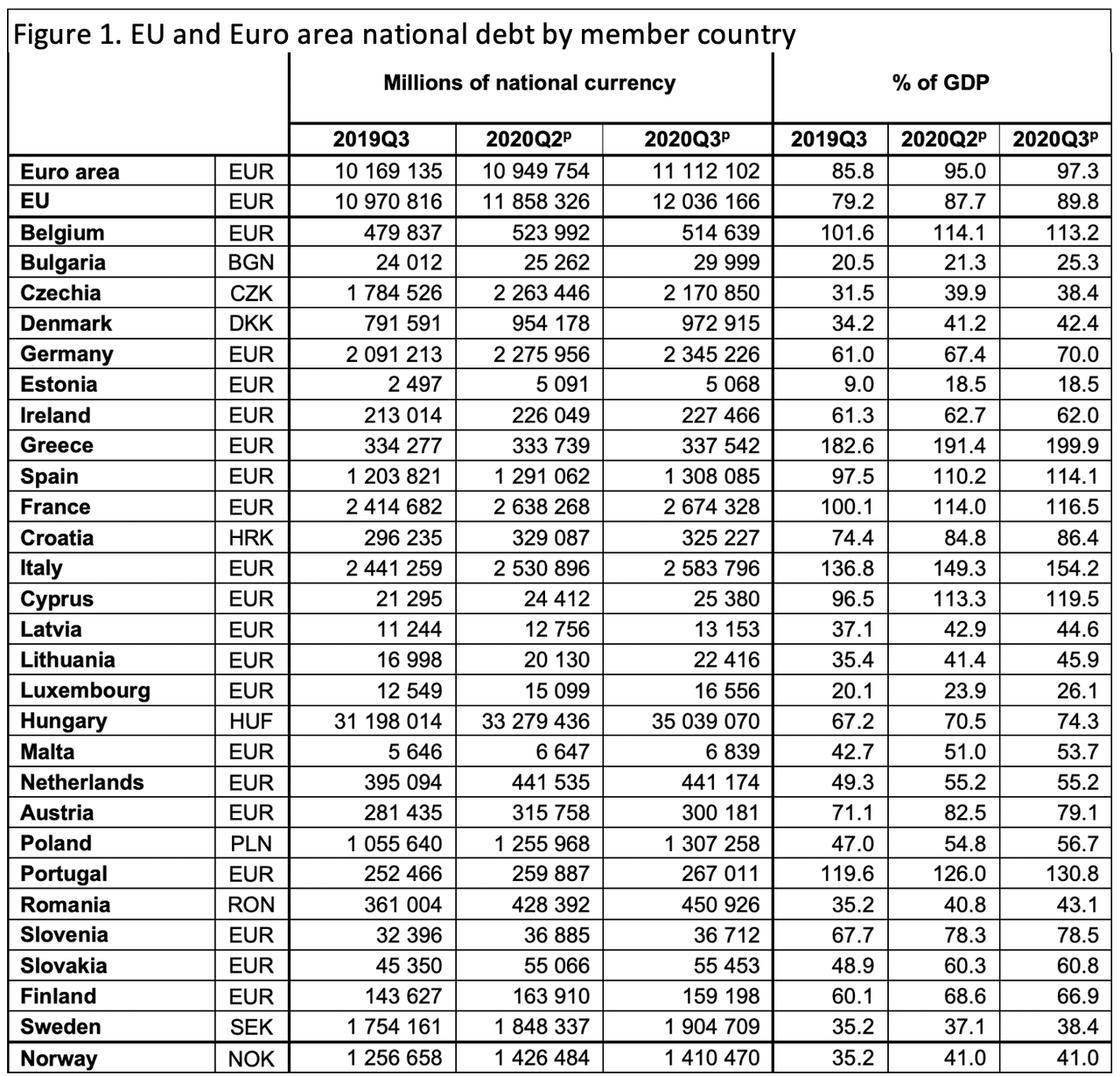

From 2000, Eurozone debt has risen from €5.2 trillion to €12.04 trillion in the third quarter of 2020, representing 97.3% of euro area GDP. Debt to GDP ratios are still soaring for two simple reasons: the EU economy is drifting into a deepening slump, and the important debtor nations of France and Italy have governments whose spending is already larger than their private sectors and other nations are getting close.

According to the Statista website, French government expenditure is about 63% of the economy, leaving only 37% of the economy in productive private sector hands. And of that 37%, an unknown but significant portion is comprised of government entities which are off balance sheet. In Italy, government expenditure is 60% of GDP, leaving a bare 40% in the private sector to pay the taxes and service the debt. A high proportion of the private sector is insolvent, with non-performing loans hidden in the euro system.

Over the last year, the greatest debt to GDP increases were in Cyprus 22.9%, Italy 17.4%, Greece 17.3%, Spain 16.6% and France 16.5%. And as the pandemic enters its third wave, national finances are still deteriorating.

The most recent figures for all EU states are shown in Figure 1, extracted from Eurostat.

The damage done to the government finances of Greece, Italy, Portugal, Cyprus, Spain, France and Belgium by pandemic shutdowns has been substantial. The failure to distribute vaccines means that even on a best hopes’ basis, emerging from the crisis will face considerable delays with lockdowns likely to continue into next winter.

The damage the coronavirus has done around the world, even to relatively free markets, is unprecedented. Free markets can be expected to recover more rapidly with the virus’s passing than those dominated by the state. Where free markets are supressed and the profit motive despised by the general population, which is the case in socialistic countries such as France and Italy, recovery is likely to be very slow. Forget the mollifying words about economic growth in the future. Along with most of the Eurozone members, France and Italy require accelerating bond sales to balance the books which are deteriorating by the day. They are already deeply ensnared in a debt trap, it being impossible to fund mountainous government debt on such small tax bases.

It is therefore no wonder that the ECB is sensitive to rising bond yields and that it is determined that they are kept as low as possible. The degree of suppression was illustrated yesterday, when a Greek 30-year bond sold out at a yield of 1.93% — half a per cent less than the US Treasury equivalent. It is plainly wrong for a country with a deteriorating government debt to GDP ratio of 200%, and with an appalling track record.

With the level of interest rate suppression this deal implies, even a moderate correction towards proper market pricing of bond yields threatens a systemic collapse of the whole euro system.

Why bond yields are rising

With the ECB firmly in control of financial markets, the inherent weaknesses and increasingly certain collapse of the euro system is for now generally ignored. Consequently, current troubles inflicting euro-denominated debt are more immediately associated with the sharp rise in dollar bond yields. Nevertheless, they share a common factor, which is that global markets are reassessing inflation prospects.

The official story, propagated by the financial establishment, is the following. As nations emerge from the coronavirus, business activity will return to normal. This outlook is guaranteed by the various stimulus packages and furlough support given to workers along with subsidies to businesses. And with consumers having been unable to spend more or less for a whole year, on the back of unleashed consumption the initial recovery will be strong. Consequently, there will be a temporary rise in prices which could exceed the 2% inflation target while pent up spending is absorbed. After that, conditions will return to normal, and the 2% inflation target will be achieved in the longer term without having to raise interest rates significantly. But even on this basis, one can see bond yields rising ahead of the increase in consumption. And the financial establishment is assuming that it is simply evidence of markets adjusting to the near-term inflation risk.

Even this Panglossian interpolation has the ECB panicking. The panic confirms that for the ECB there is no planned exit from its negative deposit rates, because with a post-covid recovery, some government finances at a national level cannot absorb any increase in bond financing costs at all.

Let us now consider a more realistic outcome, shorn of establishment wishful thinking. As mentioned above, it is likely that pandemic lockdowns throughout Europe will continue for much, if not all of this year. Consequently, on a best-case basis, economic recovery will badly lag that of the rest of the developed world. We have noted the debt traps already sprung on major EU nations by the pandemic and can readily conclude that the centralised government funding system being managed by the ECB will run into existential difficulties. But so far, we have not challenged the assumption that after lockdowns normality of a sort will return.

Even if normality does return in other major economies, the Eurozone’s banking system is preoccupied with funding national debts and dealing with non-performing loans. And being on average much more highly leveraged than the US banks, eurozone commercial banks are unable to expand the bank credit upon which economic recovery depends. But having already been damaged by the ending of the global bank credit cycle’s expansionary phase and the malign effects of a tariff war between the US and China, the global economic outlook has significantly worsened from the beginning of 2020 — only to be concealed by the pandemic crisis and the inflationary responses to it.

Not only is the Eurozone’s banking system unable to provide new credit for businesses, nor can the US banking system do so for its more dynamic economy. The reference to the bank credit cycle is not made lightly, because bankers now find that their balance sheets are at their most stretched — even beyond regulatory limits. They are being hit by widespread bankruptcies. American bank lending to the private sector is rapidly becoming a disaster as losses from non-performing loans are magnified by balance sheet leverage at the equity level, averaging 10.5 times for the big banks. So not only is the new Biden administration faced with financing a recovery from the coronavirus, but it might have to shore up the entire US economy from a cyclical depression whose driving factors are similar to those of the early 1930s.

The mounting evidence of this outcome has implications for global interest rates. A text-book Keynesian economist viewing consumer demand as the economic driver believes that a depression means lower interest rates, which is why he is confident that rising bond yields herald a more positive economic future. The error is to not understand that in a depression both consumption and production contract. And being more forward looking, producers will reduce capacity when they see the outlook deteriorating ahead of reductions in consumer spending. That being the case, monetary stimulation into a failing economy quickly ends up undermining the purchasing power of its fiat currency, instead of increasing it and threatening deflation, as a Keynesian analysis might suppose.

For the possessor of a fiat currency, there comes a growing realisation that its purchasing power will fall, whatever the economic outcome. If, as we are to suppose, the risk of a negative economic outcome increases, then the debasement will only escalate. To compensate, the offset in the form of interest paid on his monetary capital must increase if currency balances are to be maintained, reflected in higher interest rates and bond yields.

The crucial point is that our currency holder’s understanding of the outcome of inflationary central bank policies is markedly different from that of the policy planners. And even if Mr Pangloss at the Fed or the ECB is right, then the purchasing power of dollars or euros will fall anyway and those who possess it will still expect higher interest compensation to justify holding on to them. Alternatively, if the owner of a fiat currency concludes that accelerated monetary inflation will not save the economy from a slump, then because it is unbacked and not convertible into a sounder form of money, he will abandon it altogether.

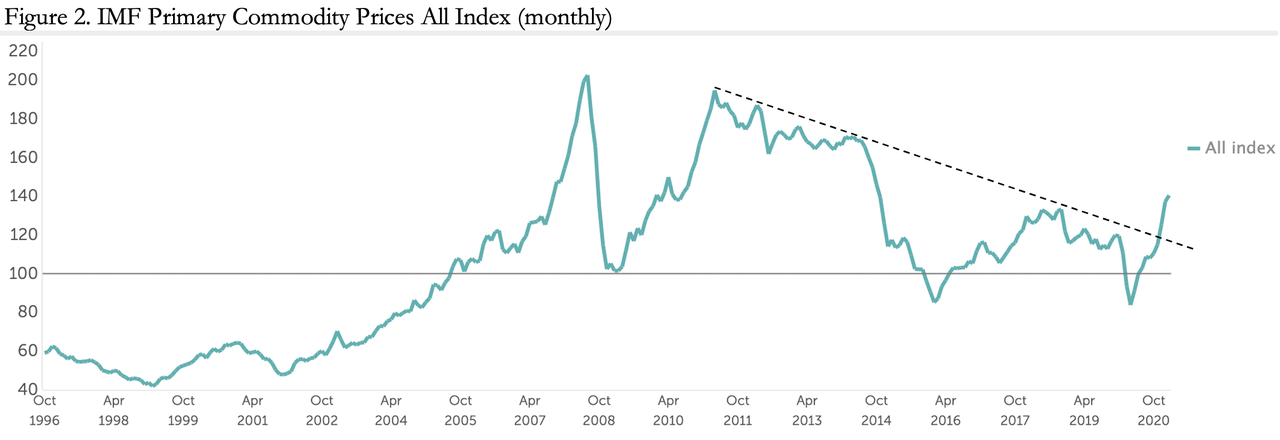

The evidence of the loss of purchasing power for fiat currencies is already visible in commodity prices, shown in Figure 2.

After a decade of consolidation, which ended in March 2020 with a dip down to 83.97, the IMF’s index has risen 67% in eleven months to 140.65. The turning point was the Fed cutting its funds rate to zero and increasing QE to $120bn per month in March 2020. Clearly, the commodity markets responded by discounting increased monetary inflation. Commodity prices in euros rose less due to the rise in its rate against the dollar, but that rise is still a substantial 55%. For genuine industrial users, keeping their excess liquidity in dollars or euros and to have not reduced currency ownership has been a costly error.

While macroeconomic commentators view the swings in commodity prices as cyclical, a more relevant interpretation is provided by understanding their users’ point of view. For manufacturers it is simple: the purchasing power of a currency measured against commodities has declined, in the case of the euro by over a third. And with monetary inflation increasing, it is a trend certain to continue, having little or nothing to do with levels of commodity demand.

Commodities are one of several economic inputs. Labour is another. And if a manufacturer is not competitive, the sensible recourse is to increase investment in automation, which requires monetary capital. The circulating element is provided by the banks, but as we have seen banks are now maxed out, risk averse, and in the eurozone fully committed to funding governments. For the eurozone banks there is an additional problem. Their balance sheets are weighted towards assets designated by the regulators as risk free or very low risk, such as government bills and bonds. An allocation into industrial and consumer lending carries extra risk, necessitating a reduction in balance sheet gearing. It is not going to happen easily or willingly.

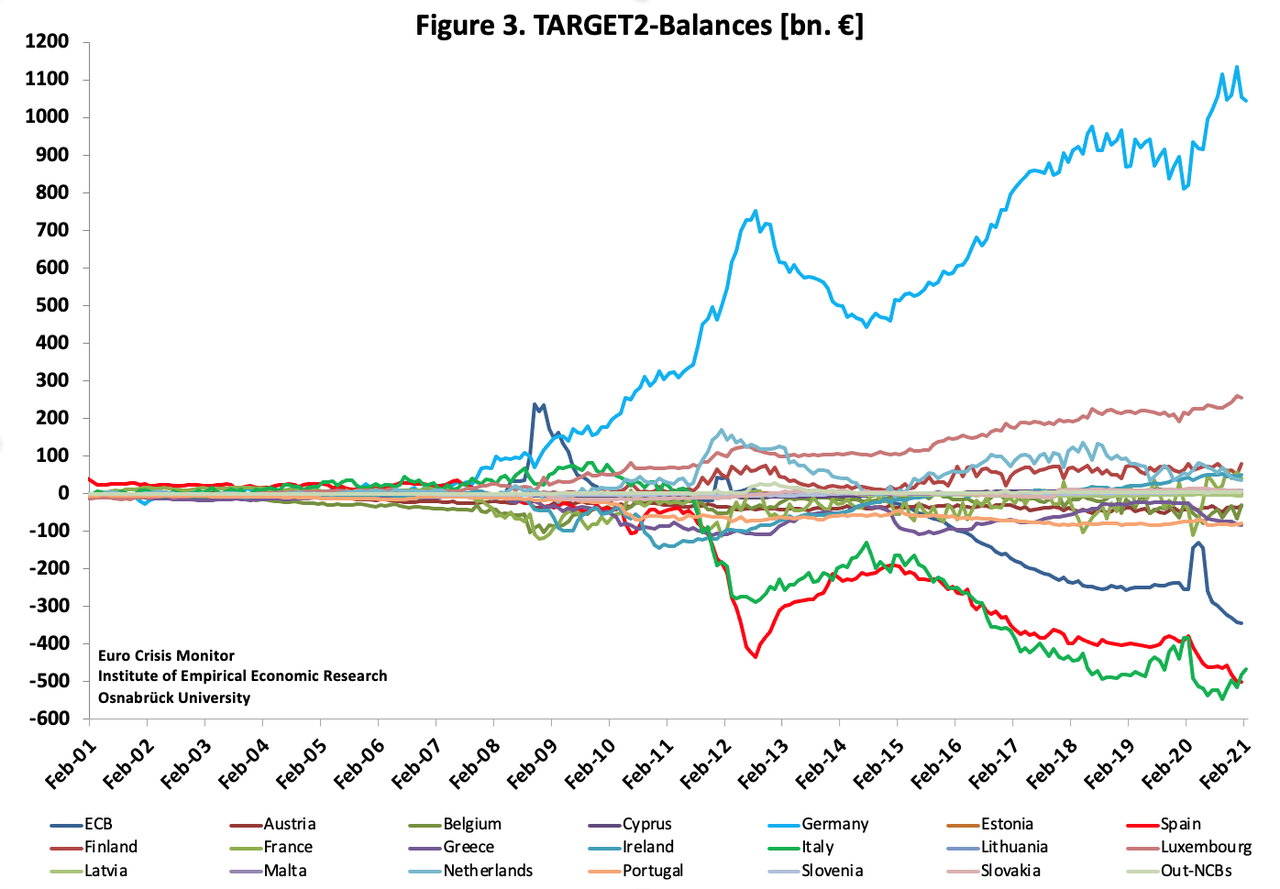

Target 2 imbalances

Figure 3 illustrates the imbalances in the TARGET2 settlement system between the national central banks and between them and the ECB. It reveals three features. Germany and Luxembourg between them are owed a net €1.3 trillion. Italy and Spain between them owe the system €968bn. And the ECB owes the national central banks €345bn. The effect of the ECB deficit, which arises from bond purchases conducted on its behalf by the national central banks, is to artificially reduce the TARGET2 balances of debtors and creditors in the system to the extent the ECB has bought their government bonds.

After allowing for the ECB’s bond purchases, the combined debts of Italy and Spain to the other national central banks easily exceed €1 trillion, and the money owed to Germany’s Bundesbank is greater than the chart shows by the extent of German debt bought by the Bundesbank on the ECB’s behalf and unpaid. The ECB’s dealings also affect France’s balance, which last March stood at a deficit of €109.4bn compared with a surplus of €40bn in January, which can only be due to payments by the ECB for French bonds, window dressing France’s position.

In theory, these imbalances should not exist. The fact that they do and that from 2015 they have been increasing is due partly to accumulating bad debts, particularly in Portugal, Italy, Greece and Spain. Local regulators are incentivised to declare non-performing bank loans as performing, so that they can be used as collateral for repurchase agreements with the local central bank. This has the effect of reducing non-performing loans at the national level, encouraging the view that there is no bad debt problem. But the problem has merely been removed from national banking systems and lost in the euro system.

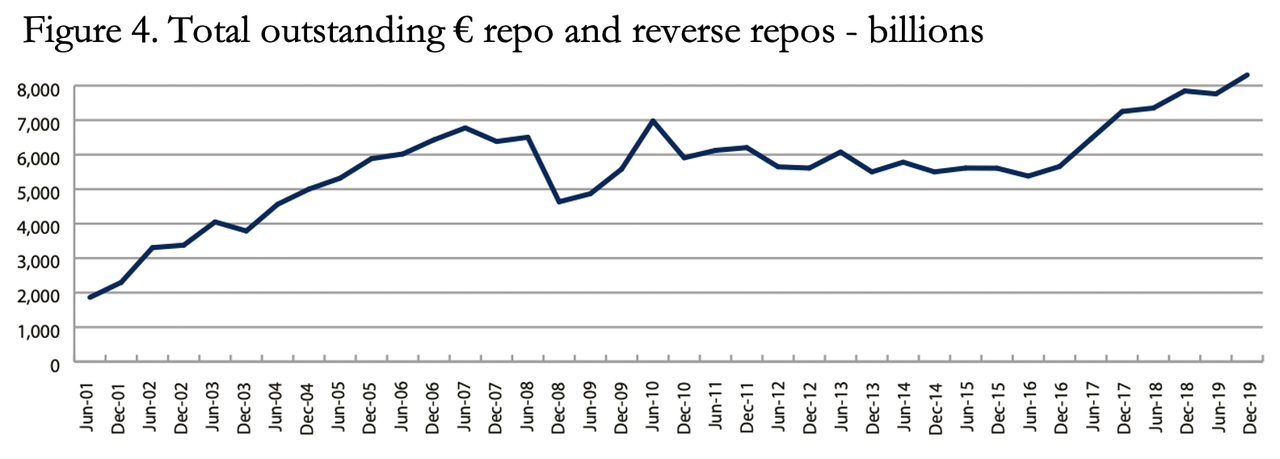

Demand for collateral against which to obtain liquidity has led to significant monetary expansion, with the repo market acting not as a marginal liquidity provider as is the case in other banking systems, but as an accumulating supply of raw money. This is shown in Figure 4, which is the result of a survey of 58 leading institutions in the euro system.

The total for this form of short-term financing grew to €8.31 trillion in outstanding contracts by December 2019. The collateral includes everything from government bonds and bills to pre-packaged national commercial bank debt. According to the survey, double counting, whereby repos are offset by reverse repos, is minimal. This is important when one considers that a reverse repo is the other side of a repo, so that with repos being additional to the reverse repos recorded, the sum of the two is a valid measure of the size of the market outstanding. The value of repos transacted with central banks as part of official monetary policy operations are not included in the survey and continue to be “very substantial”. But repos with central banks in the ordinary course of financing are included.

Today, even excluding central bank repos connected with monetary policy operations, this figure probably exceeds €10 trillion, taking into account the underlying growth in this market, and when one includes participants beyond the 58 dealers in the survey.

While the US Fed only accepts very high-quality securities as repo collateral, with the eurozone national banks and the ECB almost anything is accepted — it had to be when Greece was bailed out. High quality debt represents most of the repo collateral, but the hidden bailouts of Italian banks by taking dodgy loans off their books could not continue to this day without them being posted as repo collateral rolled into the TARGET2 system.

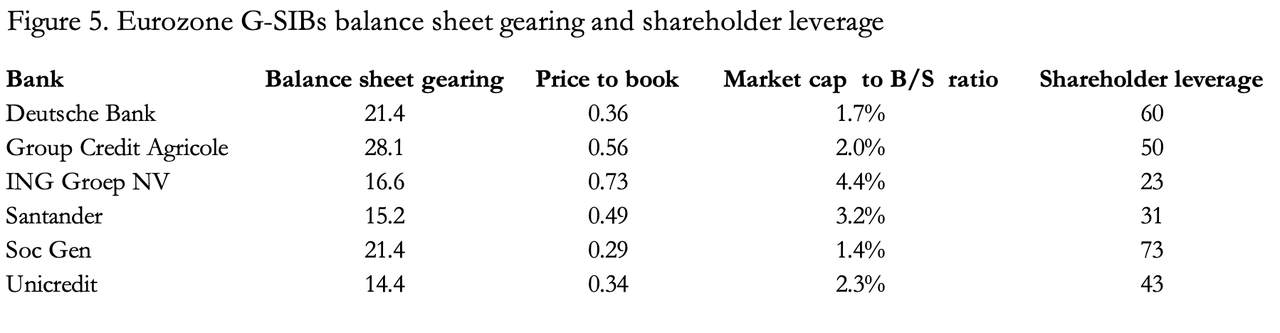

But there is a limit to this expansion, expressed in the relationship between a commercial bank’s capital and its equity. Figure 5 shows balance sheet gearing and shareholder leverage for the six listed Eurozone global systemically important banks (G-SIBs). Other eurozone banks do not have to carry the extra buffers to a G-SIB’s capital, and it is for sure that within their numbers there are even more highly leveraged banks, the failure of any one of which could lead to a system-wide run.

Without exception, the balance sheet gearing between total assets and shareholder’s tier-1 equity of all these banks is very high, given that a more normal level of balance sheet gearing is in the region of eight to twelve times at the height of a bank’s credit expansion cycle. It compares with the average ratio for the six US G-SIBs of 10.5, and even they are demonstrably tight on balance sheet capacity.

Market ratings for eurozone G-SIBs, with the arguable exception of ING, deeply discount shareholders’ equity, with Société Generale bearing the worst rating at a 71% discount. Moreover, these dismal ratings are at a time of buoyant stock markets near their all-time highs: the CAC 40 in Paris is up 60% over a year, the Dax in Frankfurt is up 73%, and the FTSE MIB in Milan up 64%. Like a party of drunks staggering to raise themselves from the gutter, Eurozone bank share prices have risen with the general markets, but it is their ratings which remain so appalling.

Conclusions

The EU is showing all the signs of a failing state, embarrassingly exposed by Brexit and the EU’s political response. Politically, it is still prepared to cut off its nose despite its face, clearly demonstrated over the vaccine debacle, aimed at the Oxford based AstraZeneca vaccine as a cover-up for the failure of Brussels to source and distribute vaccines of any manufacture around the member states. At a time of emerging lockdowns in the rest of the world, the EU is badly behind in its vaccination programme and is unlikely to fully emerge from its lockdowns before next winter, and possibly beyond. The economic consequences for the EU are going to be more devastating than for any other region outside the developing world, with third waves now emerging in Italy, France, Germany and Poland.

With the burden of financing the inevitable surge in covid-related bad debts, particularly in the PIGS but really everywhere, and with major EU nations’ national debts spiralling out of control, the financing of it all by the ECB will become increasingly difficult. As a central bank committed to financing socialising ideals by monetary inflation, the ECB has had no option but to accelerate its inflationary financing for some time. But today, the limitations placed on its inflationism are a lethal combination of the inherent rottenness of TARGET2 and rising bond yields.

Even on an optimistic (Keynesian) analysis, rising bond yields appear to be discounting a rise in post-lockdown spending, leading to a temporary burst in price inflation. The deeper truth revealed by the performance of commodity markets combined with an unprecedented increase in global money supply is that a far deeper loss of purchasing power in fiat currencies is in prospect. Furthermore, optimism over the wider economic outlook is confined to inflated numbers, with large sections of the global economy in a state of collapse.

The EU is a tail-end Charlie in this global environment, which is why it could not afford to mess up its emergence from pandemic lockdowns. And because the financing of it all falls on the ECB’s shoulders, that is where the EU’s crisis is sure to emerge. It will take out the banking system for sure; on slender equity bases, it will not take much of a rise in bond yields to wipe them out. And then all that ropey collateral in the repo system will be exposed for what it’s worth. Which is mostly nothing.

International

Four Years Ago This Week, Freedom Was Torched

Four Years Ago This Week, Freedom Was Torched

Authored by Jeffrey Tucker via The Brownstone Institute,

"Beware the Ides of March,” Shakespeare…

Share this:

Authored by Jeffrey Tucker via The Brownstone Institute,

"Beware the Ides of March,” Shakespeare quotes the soothsayer’s warning Julius Caesar about what turned out to be an impending assassination on March 15. The death of American liberty happened around the same time four years ago, when the orders went out from all levels of government to close all indoor and outdoor venues where people gather.

It was not quite a law and it was never voted on by anyone. Seemingly out of nowhere, people who the public had largely ignored, the public health bureaucrats, all united to tell the executives in charge – mayors, governors, and the president – that the only way to deal with a respiratory virus was to scrap freedom and the Bill of Rights.

And they did, not only in the US but all over the world.

The forced closures in the US began on March 6 when the mayor of Austin, Texas, announced the shutdown of the technology and arts festival South by Southwest. Hundreds of thousands of contracts, of attendees and vendors, were instantly scrapped. The mayor said he was acting on the advice of his health experts and they in turn pointed to the CDC, which in turn pointed to the World Health Organization, which in turn pointed to member states and so on.

There was no record of Covid in Austin, Texas, that day but they were sure they were doing their part to stop the spread. It was the first deployment of the “Zero Covid” strategy that became, for a time, official US policy, just as in China.

It was never clear precisely who to blame or who would take responsibility, legal or otherwise.

This Friday evening press conference in Austin was just the beginning. By the next Thursday evening, the lockdown mania reached a full crescendo. Donald Trump went on nationwide television to announce that everything was under control but that he was stopping all travel in and out of US borders, from Europe, the UK, Australia, and New Zealand. American citizens would need to return by Monday or be stuck.

Americans abroad panicked while spending on tickets home and crowded into international airports with waits up to 8 hours standing shoulder to shoulder. It was the first clear sign: there would be no consistency in the deployment of these edicts.

There is no historical record of any American president ever issuing global travel restrictions like this without a declaration of war. Until then, and since the age of travel began, every American had taken it for granted that he could buy a ticket and board a plane. That was no longer possible. Very quickly it became even difficult to travel state to state, as most states eventually implemented a two-week quarantine rule.

The next day, Friday March 13, Broadway closed and New York City began to empty out as any residents who could went to summer homes or out of state.

On that day, the Trump administration declared the national emergency by invoking the Stafford Act which triggers new powers and resources to the Federal Emergency Management Administration.

In addition, the Department of Health and Human Services issued a classified document, only to be released to the public months later. The document initiated the lockdowns. It still does not exist on any government website.

The White House Coronavirus Response Task Force, led by the Vice President, will coordinate a whole-of-government approach, including governors, state and local officials, and members of Congress, to develop the best options for the safety, well-being, and health of the American people. HHS is the LFA [Lead Federal Agency] for coordinating the federal response to COVID-19.

Closures were guaranteed:

Recommend significantly limiting public gatherings and cancellation of almost all sporting events, performances, and public and private meetings that cannot be convened by phone. Consider school closures. Issue widespread ‘stay at home’ directives for public and private organizations, with nearly 100% telework for some, although critical public services and infrastructure may need to retain skeleton crews. Law enforcement could shift to focus more on crime prevention, as routine monitoring of storefronts could be important.

In this vision of turnkey totalitarian control of society, the vaccine was pre-approved: “Partner with pharmaceutical industry to produce anti-virals and vaccine.”

The National Security Council was put in charge of policy making. The CDC was just the marketing operation. That’s why it felt like martial law. Without using those words, that’s what was being declared. It even urged information management, with censorship strongly implied.

The timing here is fascinating. This document came out on a Friday. But according to every autobiographical account – from Mike Pence and Scott Gottlieb to Deborah Birx and Jared Kushner – the gathered team did not meet with Trump himself until the weekend of the 14th and 15th, Saturday and Sunday.

According to their account, this was his first real encounter with the urge that he lock down the whole country. He reluctantly agreed to 15 days to flatten the curve. He announced this on Monday the 16th with the famous line: “All public and private venues where people gather should be closed.”

This makes no sense. The decision had already been made and all enabling documents were already in circulation.

There are only two possibilities.

One: the Department of Homeland Security issued this March 13 HHS document without Trump’s knowledge or authority. That seems unlikely.

Two: Kushner, Birx, Pence, and Gottlieb are lying. They decided on a story and they are sticking to it.

Trump himself has never explained the timeline or precisely when he decided to greenlight the lockdowns. To this day, he avoids the issue beyond his constant claim that he doesn’t get enough credit for his handling of the pandemic.

With Nixon, the famous question was always what did he know and when did he know it? When it comes to Trump and insofar as concerns Covid lockdowns – unlike the fake allegations of collusion with Russia – we have no investigations. To this day, no one in the corporate media seems even slightly interested in why, how, or when human rights got abolished by bureaucratic edict.

As part of the lockdowns, the Cybersecurity and Infrastructure Security Agency, which was and is part of the Department of Homeland Security, as set up in 2018, broke the entire American labor force into essential and nonessential.

They also set up and enforced censorship protocols, which is why it seemed like so few objected. In addition, CISA was tasked with overseeing mail-in ballots.

Only 8 days into the 15, Trump announced that he wanted to open the country by Easter, which was on April 12. His announcement on March 24 was treated as outrageous and irresponsible by the national press but keep in mind: Easter would already take us beyond the initial two-week lockdown. What seemed to be an opening was an extension of closing.

This announcement by Trump encouraged Birx and Fauci to ask for an additional 30 days of lockdown, which Trump granted. Even on April 23, Trump told Georgia and Florida, which had made noises about reopening, that “It’s too soon.” He publicly fought with the governor of Georgia, who was first to open his state.

Before the 15 days was over, Congress passed and the president signed the 880-page CARES Act, which authorized the distribution of $2 trillion to states, businesses, and individuals, thus guaranteeing that lockdowns would continue for the duration.

There was never a stated exit plan beyond Birx’s public statements that she wanted zero cases of Covid in the country. That was never going to happen. It is very likely that the virus had already been circulating in the US and Canada from October 2019. A famous seroprevalence study by Jay Bhattacharya came out in May 2020 discerning that infections and immunity were already widespread in the California county they examined.

What that implied was two crucial points: there was zero hope for the Zero Covid mission and this pandemic would end as they all did, through endemicity via exposure, not from a vaccine as such. That was certainly not the message that was being broadcast from Washington. The growing sense at the time was that we all had to sit tight and just wait for the inoculation on which pharmaceutical companies were working.

By summer 2020, you recall what happened. A restless generation of kids fed up with this stay-at-home nonsense seized on the opportunity to protest racial injustice in the killing of George Floyd. Public health officials approved of these gatherings – unlike protests against lockdowns – on grounds that racism was a virus even more serious than Covid. Some of these protests got out of hand and became violent and destructive.

Meanwhile, substance abuse rage – the liquor and weed stores never closed – and immune systems were being degraded by lack of normal exposure, exactly as the Bakersfield doctors had predicted. Millions of small businesses had closed. The learning losses from school closures were mounting, as it turned out that Zoom school was near worthless.

It was about this time that Trump seemed to figure out – thanks to the wise council of Dr. Scott Atlas – that he had been played and started urging states to reopen. But it was strange: he seemed to be less in the position of being a president in charge and more of a public pundit, Tweeting out his wishes until his account was banned. He was unable to put the worms back in the can that he had approved opening.

By that time, and by all accounts, Trump was convinced that the whole effort was a mistake, that he had been trolled into wrecking the country he promised to make great. It was too late. Mail-in ballots had been widely approved, the country was in shambles, the media and public health bureaucrats were ruling the airwaves, and his final months of the campaign failed even to come to grips with the reality on the ground.

At the time, many people had predicted that once Biden took office and the vaccine was released, Covid would be declared to have been beaten. But that didn’t happen and mainly for one reason: resistance to the vaccine was more intense than anyone had predicted. The Biden administration attempted to impose mandates on the entire US workforce. Thanks to a Supreme Court ruling, that effort was thwarted but not before HR departments around the country had already implemented them.

As the months rolled on – and four major cities closed all public accommodations to the unvaccinated, who were being demonized for prolonging the pandemic – it became clear that the vaccine could not and would not stop infection or transmission, which means that this shot could not be classified as a public health benefit. Even as a private benefit, the evidence was mixed. Any protection it provided was short-lived and reports of vaccine injury began to mount. Even now, we cannot gain full clarity on the scale of the problem because essential data and documentation remains classified.

After four years, we find ourselves in a strange position. We still do not know precisely what unfolded in mid-March 2020: who made what decisions, when, and why. There has been no serious attempt at any high level to provide a clear accounting much less assign blame.

Not even Tucker Carlson, who reportedly played a crucial role in getting Trump to panic over the virus, will tell us the source of his own information or what his source told him. There have been a series of valuable hearings in the House and Senate but they have received little to no press attention, and none have focus on the lockdown orders themselves.

The prevailing attitude in public life is just to forget the whole thing. And yet we live now in a country very different from the one we inhabited five years ago. Our media is captured. Social media is widely censored in violation of the First Amendment, a problem being taken up by the Supreme Court this month with no certainty of the outcome. The administrative state that seized control has not given up power. Crime has been normalized. Art and music institutions are on the rocks. Public trust in all official institutions is at rock bottom. We don’t even know if we can trust the elections anymore.

In the early days of lockdown, Henry Kissinger warned that if the mitigation plan does not go well, the world will find itself set “on fire.” He died in 2023. Meanwhile, the world is indeed on fire. The essential struggle in every country on earth today concerns the battle between the authority and power of permanent administration apparatus of the state – the very one that took total control in lockdowns – and the enlightenment ideal of a government that is responsible to the will of the people and the moral demand for freedom and rights.

How this struggle turns out is the essential story of our times.

CODA: I’m embedding a copy of PanCAP Adapted, as annotated by Debbie Lerman. You might need to download the whole thing to see the annotations. If you can help with research, please do.

* * *

Jeffrey Tucker is the author of the excellent new book 'Life After Lock-Down'

Government

Fauci Deputy Warned Him Against Vaccine Mandates: Email

Fauci Deputy Warned Him Against Vaccine Mandates: Email

Authored by Zachary Stieber via The Epoch Times (emphasis ours),

Mandating COVID-19…

Share this:

Authored by Zachary Stieber via The Epoch Times (emphasis ours),

Mandating COVID-19 vaccination was a mistake due to ethical and other concerns, a top government doctor warned Dr. Anthony Fauci after Dr. Fauci promoted mass vaccination.

“Coercing or forcing people to take a vaccine can have negative consequences from a biological, sociological, psychological, economical, and ethical standpoint and is not worth the cost even if the vaccine is 100% safe,” Dr. Matthew Memoli, director of the Laboratory of Infectious Diseases clinical studies unit at the U.S. National Institute of Allergy and Infectious Diseases (NIAID), told Dr. Fauci in an email.

“A more prudent approach that considers these issues would be to focus our efforts on those at high risk of severe disease and death, such as the elderly and obese, and do not push vaccination on the young and healthy any further.”

Employing that strategy would help prevent loss of public trust and political capital, Dr. Memoli said.

The email was sent on July 30, 2021, after Dr. Fauci, director of the NIAID, claimed that communities would be safer if more people received one of the COVID-19 vaccines and that mass vaccination would lead to the end of the COVID-19 pandemic.

“We’re on a really good track now to really crush this outbreak, and the more people we get vaccinated, the more assuredness that we’re going to have that we’re going to be able to do that,” Dr. Fauci said on CNN the month prior.

Dr. Memoli, who has studied influenza vaccination for years, disagreed, telling Dr. Fauci that research in the field has indicated yearly shots sometimes drive the evolution of influenza.

Vaccinating people who have not been infected with COVID-19, he said, could potentially impact the evolution of the virus that causes COVID-19 in unexpected ways.

“At best what we are doing with mandated mass vaccination does nothing and the variants emerge evading immunity anyway as they would have without the vaccine,” Dr. Memoli wrote. “At worst it drives evolution of the virus in a way that is different from nature and possibly detrimental, prolonging the pandemic or causing more morbidity and mortality than it should.”

The vaccination strategy was flawed because it relied on a single antigen, introducing immunity that only lasted for a certain period of time, Dr. Memoli said. When the immunity weakened, the virus was given an opportunity to evolve.

Some other experts, including virologist Geert Vanden Bossche, have offered similar views. Others in the scientific community, such as U.S. Centers for Disease Control and Prevention scientists, say vaccination prevents virus evolution, though the agency has acknowledged it doesn’t have records supporting its position.

Other Messages

Dr. Memoli sent the email to Dr. Fauci and two other top NIAID officials, Drs. Hugh Auchincloss and Clifford Lane. The message was first reported by the Wall Street Journal, though the publication did not publish the message. The Epoch Times obtained the email and 199 other pages of Dr. Memoli’s emails through a Freedom of Information Act request. There were no indications that Dr. Fauci ever responded to Dr. Memoli.

Later in 2021, the NIAID’s parent agency, the U.S. National Institutes of Health (NIH), and all other federal government agencies began requiring COVID-19 vaccination, under direction from President Joe Biden.

In other messages, Dr. Memoli said the mandates were unethical and that he was hopeful legal cases brought against the mandates would ultimately let people “make their own healthcare decisions.”

“I am certainly doing everything in my power to influence that,” he wrote on Nov. 2, 2021, to an unknown recipient. Dr. Memoli also disclosed that both he and his wife had applied for exemptions from the mandates imposed by the NIH and his wife’s employer. While her request had been granted, his had not as of yet, Dr. Memoli said. It’s not clear if it ever was.

According to Dr. Memoli, officials had not gone over the bioethics of the mandates. He wrote to the NIH’s Department of Bioethics, pointing out that the protection from the vaccines waned over time, that the shots can cause serious health issues such as myocarditis, or heart inflammation, and that vaccinated people were just as likely to spread COVID-19 as unvaccinated people.

He cited multiple studies in his emails, including one that found a resurgence of COVID-19 cases in a California health care system despite a high rate of vaccination and another that showed transmission rates were similar among the vaccinated and unvaccinated.

Dr. Memoli said he was “particularly interested in the bioethics of a mandate when the vaccine doesn’t have the ability to stop spread of the disease, which is the purpose of the mandate.”

The message led to Dr. Memoli speaking during an NIH event in December 2021, several weeks after he went public with his concerns about mandating vaccines.

“Vaccine mandates should be rare and considered only with a strong justification,” Dr. Memoli said in the debate. He suggested that the justification was not there for COVID-19 vaccines, given their fleeting effectiveness.

Julie Ledgerwood, another NIAID official who also spoke at the event, said that the vaccines were highly effective and that the side effects that had been detected were not significant. She did acknowledge that vaccinated people needed boosters after a period of time.

The NIH, and many other government agencies, removed their mandates in 2023 with the end of the COVID-19 public health emergency.

A request for comment from Dr. Fauci was not returned. Dr. Memoli told The Epoch Times in an email he was “happy to answer any questions you have” but that he needed clearance from the NIAID’s media office. That office then refused to give clearance.

Dr. Jay Bhattacharya, a professor of health policy at Stanford University, said that Dr. Memoli showed bravery when he warned Dr. Fauci against mandates.

“Those mandates have done more to demolish public trust in public health than any single action by public health officials in my professional career, including diminishing public trust in all vaccines.” Dr. Bhattacharya, a frequent critic of the U.S. response to COVID-19, told The Epoch Times via email. “It was risky for Dr. Memoli to speak publicly since he works at the NIH, and the culture of the NIH punishes those who cross powerful scientific bureaucrats like Dr. Fauci or his former boss, Dr. Francis Collins.”

Government

Trump “Clearly Hasn’t Learned From His COVID-Era Mistakes”, RFK Jr. Says

Trump "Clearly Hasn’t Learned From His COVID-Era Mistakes", RFK Jr. Says

Authored by Jeff Louderback via The Epoch Times (emphasis ours),

President…

Share this:

{kind=link}

{kind=link}

Authored by Jeff Louderback via The Epoch Times (emphasis ours),

President Joe Biden claimed that COVID vaccines are now helping cancer patients during his State of the Union address on March 7, but it was a response on Truth Social from former President Donald Trump that drew the ire of independent presidential candidate Robert F. Kennedy Jr.

{kind=link}

During the address, President Biden said: “The pandemic no longer controls our lives. The vaccines that saved us from COVID are now being used to help beat cancer, turning setback into comeback. That’s what America does.”

President Trump wrote: “The Pandemic no longer controls our lives. The VACCINES that saved us from COVID are now being used to help beat cancer—turning setback into comeback. YOU’RE WELCOME JOE. NINE-MONTH APPROVAL TIME VS. 12 YEARS THAT IT WOULD HAVE TAKEN YOU.”

An outspoken critic of President Trump’s COVID response, and the Operation Warp Speed program that escalated the availability of COVID vaccines, Mr. Kennedy said on X, formerly known as Twitter, that “Donald Trump clearly hasn’t learned from his COVID-era mistakes.”

“He fails to recognize how ineffective his warp speed vaccine is as the ninth shot is being recommended to seniors. Even more troubling is the documented harm being caused by the shot to so many innocent children and adults who are suffering myocarditis, pericarditis, and brain inflammation,” Mr. Kennedy remarked.

“This has been confirmed by a CDC-funded study of 99 million people. Instead of bragging about its speedy approval, we should be honestly and transparently debating the abundant evidence that this vaccine may have caused more harm than good.

“I look forward to debating both Trump and Biden on Sept. 16 in San Marcos, Texas.”

Mr. Kennedy announced in April 2023 that he would challenge President Biden for the 2024 Democratic Party presidential nomination before declaring his run as an independent last October, claiming that the Democrat National Committee was “rigging the primary.”

Since the early stages of his campaign, Mr. Kennedy has generated more support than pundits expected from conservatives, moderates, and independents resulting in speculation that he could take votes away from President Trump.

Many Republicans continue to seek a reckoning over the government-imposed pandemic lockdowns and vaccine mandates.

President Trump’s defense of Operation Warp Speed, the program he rolled out in May 2020 to spur the development and distribution of COVID-19 vaccines amid the pandemic, remains a sticking point for some of his supporters.

Operation Warp Speed featured a partnership between the government, the military, and the private sector, with the government paying for millions of vaccine doses to be produced.

President Trump released a statement in March 2021 saying: “I hope everyone remembers when they’re getting the COVID-19 Vaccine, that if I wasn’t President, you wouldn’t be getting that beautiful ‘shot’ for 5 years, at best, and probably wouldn’t be getting it at all. I hope everyone remembers!”

President Trump said about the COVID-19 vaccine in an interview on Fox News in March 2021: “It works incredibly well. Ninety-five percent, maybe even more than that. I would recommend it, and I would recommend it to a lot of people that don’t want to get it and a lot of those people voted for me, frankly.

“But again, we have our freedoms and we have to live by that and I agree with that also. But it’s a great vaccine, it’s a safe vaccine, and it’s something that works.”

On many occasions, President Trump has said that he is not in favor of vaccine mandates.

An environmental attorney, Mr. Kennedy founded Children’s Health Defense, a nonprofit that aims to end childhood health epidemics by promoting vaccine safeguards, among other initiatives.

Last year, Mr. Kennedy told podcaster Joe Rogan that ivermectin was suppressed by the FDA so that the COVID-19 vaccines could be granted emergency use authorization.

He has criticized Big Pharma, vaccine safety, and government mandates for years.

Since launching his presidential campaign, Mr. Kennedy has made his stances on the COVID-19 vaccines, and vaccines in general, a frequent talking point.

“I would argue that the science is very clear right now that they [vaccines] caused a lot more problems than they averted,” Mr. Kennedy said on Piers Morgan Uncensored last April.

“And if you look at the countries that did not vaccinate, they had the lowest death rates, they had the lowest COVID and infection rates.”

Additional data show a “direct correlation” between excess deaths and high vaccination rates in developed countries, he said.

President Trump and Mr. Kennedy have similar views on topics like protecting the U.S.-Mexico border and ending the Russia-Ukraine war.

COVID-19 is the topic where Mr. Kennedy and President Trump seem to differ the most.

Former President Donald Trump intended to “drain the swamp” when he took office in 2017, but he was “intimidated by bureaucrats” at federal agencies and did not accomplish that objective, Mr. Kennedy said on Feb. 5.

Speaking at a voter rally in Tucson, where he collected signatures to get on the Arizona ballot, the independent presidential candidate said President Trump was “earnest” when he vowed to “drain the swamp,” but it was “business as usual” during his term.

John Bolton, who President Trump appointed as a national security adviser, is “the template for a swamp creature,” Mr. Kennedy said.

Scott Gottlieb, who President Trump named to run the FDA, “was Pfizer’s business partner” and eventually returned to Pfizer, Mr. Kennedy said.

Mr. Kennedy said that President Trump had more lobbyists running federal agencies than any president in U.S. history.

“You can’t reform them when you’ve got the swamp creatures running them, and I’m not going to do that. I’m going to do something different,” Mr. Kennedy said.

During the COVID-19 pandemic, President Trump “did not ask the questions that he should have,” he believes.

President Trump “knew that lockdowns were wrong” and then “agreed to lockdowns,” Mr. Kennedy said.

He also “knew that hydroxychloroquine worked, he said it,” Mr. Kennedy explained, adding that he was eventually “rolled over” by Dr. Anthony Fauci and his advisers.

MaryJo Perry, a longtime advocate for vaccine choice and a Trump supporter, thinks votes will be at a premium come Election Day, particularly because the independent and third-party field is becoming more competitive.

Ms. Perry, president of Mississippi Parents for Vaccine Rights, believes advocates for medical freedom could determine who is ultimately president.

She believes that Mr. Kennedy is “pulling votes from Trump” because of the former president’s stance on the vaccines.

“People care about medical freedom. It’s an important issue here in Mississippi, and across the country,” Ms. Perry told The Epoch Times.

“Trump should admit he was wrong about Operation Warp Speed and that COVID vaccines have been dangerous. That would make a difference among people he has offended.”

President Trump won’t lose enough votes to Mr. Kennedy about Operation Warp Speed and COVID vaccines to have a significant impact on the election, Ohio Republican strategist Wes Farno told The Epoch Times.

President Trump won in Ohio by eight percentage points in both 2016 and 2020. The Ohio Republican Party endorsed President Trump for the nomination in 2024.

“The positives of a Trump presidency far outweigh the negatives,” Mr. Farno said. “People are more concerned about their wallet and the economy.

“They are asking themselves if they were better off during President Trump’s term compared to since President Biden took office. The answer to that question is obvious because many Americans are struggling to afford groceries, gas, mortgages, and rent payments.

“America needs President Trump.”

Multiple national polls back Mr. Farno’s view.

As of March 6, the RealClearPolitics average of polls indicates that President Trump has 41.8 percent support in a five-way race that includes President Biden (38.4 percent), Mr. Kennedy (12.7 percent), independent Cornel West (2.6 percent), and Green Party nominee Jill Stein (1.7 percent).

A Pew Research Center study conducted among 10,133 U.S. adults from Feb. 7 to Feb. 11 showed that Democrats and Democrat-leaning independents (42 percent) are more likely than Republicans and GOP-leaning independents (15 percent) to say they have received an updated COVID vaccine.

The poll also reported that just 28 percent of adults say they have received the updated COVID inoculation.

The peer-reviewed multinational study of more than 99 million vaccinated people that Mr. Kennedy referenced in his X post on March 7 was published in the Vaccine journal on Feb. 12.

It aimed to evaluate the risk of 13 adverse events of special interest (AESI) following COVID-19 vaccination. The AESIs spanned three categories—neurological, hematologic (blood), and cardiovascular.

The study reviewed data collected from more than 99 million vaccinated people from eight nations—Argentina, Australia, Canada, Denmark, Finland, France, New Zealand, and Scotland—looking at risks up to 42 days after getting the shots.

Three vaccines—Pfizer and Moderna’s mRNA vaccines as well as AstraZeneca’s viral vector jab—were examined in the study.

Researchers found higher-than-expected cases that they deemed met the threshold to be potential safety signals for multiple AESIs, including for Guillain-Barre syndrome (GBS), cerebral venous sinus thrombosis (CVST), myocarditis, and pericarditis.

A safety signal refers to information that could suggest a potential risk or harm that may be associated with a medical product.

The study identified higher incidences of neurological, cardiovascular, and blood disorder complications than what the researchers expected.

President Trump’s role in Operation Warp Speed, and his continued praise of the COVID vaccine, remains a concern for some voters, including those who still support him.

Krista Cobb is a 40-year-old mother in western Ohio. She voted for President Trump in 2020 and said she would cast her vote for him this November, but she was stunned when she saw his response to President Biden about the COVID-19 vaccine during the State of the Union address.

“I love President Trump and support his policies, but at this point, he has to know they [advisers and health officials] lied about the shot,” Ms. Cobb told The Epoch Times.

“If he continues to promote it, especially after all of the hearings they’ve had about it in Congress, the side effects, and cover-ups on Capitol Hill, at what point does he become the same as the people who have lied?” Ms. Cobb added.

“I think he should distance himself from talk about Operation Warp Speed and even admit that he was wrong—that the vaccines have not had the impact he was told they would have. If he did that, people would respect him even more.”

Red Candle In The Wind

‘I couldn’t stand the pain’: the Turkish holiday resort that’s become an emergency dental centre for Britons who can’t get treated at home

Four Years Ago This Week, Freedom Was Torched

Beloved mall retailer files Chapter 7 bankruptcy, will liquidate

Is the National Guard a solution to school violence?

Rand Paul Teases Senate GOP Leader Run – Musk Says “I Would Support”

Trump “Clearly Hasn’t Learned From His COVID-Era Mistakes”, RFK Jr. Says

The next pandemic? It’s already here for Earth’s wildlife

Fauci Deputy Warned Him Against Vaccine Mandates: Email

Vaccine-skeptical mothers say bad health care experiences made them distrust the medical system

-

Uncategorized3 weeks ago

Uncategorized3 weeks agoAll Of The Elements Are In Place For An Economic Crisis Of Staggering Proportions

-

International4 days ago

International4 days agoEyePoint poaches medical chief from Apellis; Sandoz CFO, longtime BioNTech exec to retire

-

Uncategorized3 weeks ago

Uncategorized3 weeks agoCalifornia Counties Could Be Forced To Pay $300 Million To Cover COVID-Era Program

-

Uncategorized2 weeks ago

Uncategorized2 weeks agoApparel Retailer Express Moving Toward Bankruptcy

-

Uncategorized4 weeks ago

Uncategorized4 weeks agoIndustrial Production Decreased 0.1% in January

-

International4 days ago

International4 days agoWalmart launches clever answer to Target’s new membership program

-

Uncategorized3 weeks ago

Uncategorized3 weeks agoRFK Jr: The Wuhan Cover-Up & The Rise Of The Biowarfare-Industrial Complex

-

Uncategorized3 weeks ago

Uncategorized3 weeks agoGOP Efforts To Shore Up Election Security In Swing States Face Challenges