The 2020s Are Becoming Another Great Inflationary Decade: Stack Bitcoin Accordingly

As in the 1940s and ’70s, poor economic policy is driving rampant inflation and compelling investors to move wealth from cash to bitcoin.

Share this:

As in the 1940s and ’70s, poor economic policy is driving rampant inflation and compelling investors to move wealth from cash to bitcoin.

Central banks globally are fighting the deleveraging of the largest debt bubble in modern history. With inflation recently hitting its highest levels in 30 years, many have called for more responsible policy decisions from central banks, to tame the inflation that’s now ravaging the everyday person.

However, every time central banks attempt to taper and remove artificial stimulus injections into markets, assets begin cratering.

Central banks globally are stuck between a rock and a hard place. Continuing to print and run enormous fiscal deficits will only accelerate the already out-of-control inflation. Meanwhile, every time they stop printing and attempt to raise rates, assets begin selling off precipitously.

Many believe central banks are simply out of options in trying to combat this economic conundrum. Or, do they have a nuclear plan hidden up their sleeves that they’re about to unleash, making the unprecedented 2020 balance sheet expansion look trivial in comparison?

Global Debt Crisis!

Before we look at central banks’ nuclear “solution,” we need to understand why they’d consider such a move and why deleveraging is simply not an option.

The world has never been more indebted than today in the 2020s, as central banks are trying to avoid a repeat of the mass deleveraging event of the 1930s. The 90% correction in the Dow Jones in 1929 led to a decade-long period of high unemployment, suffering and starvation. The decade in the 1930s is today known as the Great Depression.

At this stage of a long-term debt cycle, with interest rates at zero and debt levels unsustainably high across the globe, central banks’ are desperately hoping to avoid a repeat of the 1930s.

Hirschmann Capital released a fascinating report which helps to explain the current day predicament facing central banks. Its work showed that since the year 1800, 51 out of 52 countries that have reached sovereign debt levels greater than 130% of GDP ended up defaulting on their debts within 15 years. Default came through either devaluation, inflation, restructuring, outright nominal default or an implicit default, like the one that was seen in 1971 during the Nixon Shock and the U.S. refusing to make good on its obligation to allow countries to redeem the U.S. dollar for the gold it was supposed to be backed by.

In simple terms, central banks normally choose to default through inflation and currency devaluation. They do this by embarking on irresponsible monetary policies, such as money printing, which devalues the currency so that they can pay back their massive debts with the devalued dollars.

Today, the U.S. has appeared to have crossed the rubicon, having just passed a 130% debt-to-GDP ratio. The previous time in history that the U.S. had debt levels as high as today was in the 1940s, at the conclusion of the previous 75- to 100-year long-term debt cycle. More on this later.

The 1930s Blueprint For Central Banks?

Figure six below highlights how the central banks pegged interest rates to 2.5% for the best part of a decade and broke their independence from the government. This separation of the Federal Reserve and U.S. Treasury allowed the government to run large fiscal deficits and enabled it to tackle the enormous debt that was built up through World War I.

This inevitably caused significant inflation throughout the 1940s, which devalued the currency and enabled the government to decrease its nominal debt/GDP levels from over 120% in 1945, to below 60% by the ’60s, highlighted by figure seven below.

Is what happened in the 1940s a blueprint that central banks are looking at today?

The International Monetary Fund (IMF), which serves as the central bank of central banks, appears to be well aware of how to deal with the debt. It wrote a working paper titled “The Liquidation Of Government Debt” in 2015, describing how it would use financial repression and inflate away the debt, similarly to what was done in the 1940s. We talked about this paper in more detail in this video.

Every time they try to tell the market that they’re not going to inflate away the debt and taper, the market has a tantrum.

Taper Or Taper Tantrum

Pressure has been mounting on the Federal Reserve to begin tapering, with inflation hitting 30-year highs and central banks around the world in the U.K., Canada and Australia all beginning tapering in Q3 2021.

Recently, Federal Reserve Chairman Jerome Powell begrudgingly announced that the U.S. would begin decreasing the $120 billion in quantitative easing (QE) it has been doing each month. Its plan is to decrease QE by $15 billion per month, which started recently, until it reaches zero in June 2022, when it would also then look to raise interest rates.

Many involved in the finance and macroeconomic worlds are watching this hawkish move with bated breath. In 2019, Powell tried to taper the Fed’s QE programs and normalize the balance sheet, in an attempt to restore faith in capitalism and the currency after the continued expansionary monetary policy. The unprecedented idea of QE in response to the 2008 Great Financial Crisis was supposed to be temporary, after all. The chart below shows how the stock markets reacted and sold off 22% only two months into tapering, forcing Powell to reverse course and prove that you “can’t taper a ponzi scheme.”

The stock markets are becoming increasingly fragile and reliant on stimulus to remain so artificially elevated. The ever-increasing size of bailouts needed and volatility in markets are vital signs that the currency is coming closer to collapse.

We discussed the concept of currency collapses when talking about German hyperinflation in this video.

This point of increasing fragility and volatility was further illustrated in early 2020 as the SPY, and stock markets globally, had their fastest 30% crash in history. The Fed responded by announcing the largest and fastest bailout in history in response to the global liquidity crisis.

2021 marks the 50th anniversary of the Nixon Shock and we’ve witnessed the unleashing of the most exuberant and unprecedented monetary policies in human history over those 50 years. With debts now at 5,000-year highs and interest rates at 5,000-year lows, what could possibly go wrong when central banks attempt to raise rates?

Will they taper or are we seeing signs that they’re seeking another avenue through which to tackle inflation?

Nuclear Option… Price Controls?

Inflation has to be the most hotly-debated topic in macroeconomics today and the chart below gives insights to why that is.

The recent surge in the price of Thanksgiving costs has also reminded us that inflation is continuing to be a massive issue, and proving to be anything but transitory.

Senator Elizabeth Warren, a former Democratic presidential candidate, recently suggested that consumers are paying higher prices for turkey because of excessive consolidation, price-fixing and "plain old corporate greed."

“The average cost of this year's classic Thanksgiving feast has jumped more than 14% from last year's average, according to the American Farm Bureau Federation's annual Thanksgiving dinner cost survey. That's in large part because the cost of a turkey is up nearly 24% from last year. The cost of chicken breasts, meanwhile, has jumped 26% over the past year, according to Labor Department data.”

Other sources claim that the turkey price has increased even more dramatically, which has sparked further heated debate over inflation in the corporate media.

In the same week that Warren went after corporations over inflation concerns, the Food Trade Commission (FTC) said that it was ordering Walmart, Amazon, Kroger and other large wholesalers and suppliers, including Procter & Gamble Co., Tyson Foods and Kraft Heinz Co., “to turn over information to help study causes of empty shelves and sky-high prices.”

To further flame the food-price inflation debate, a regular contributor to The Washington Post, Micheline Maynard, found the solution to the empty shelves:

“She says that we have come to expect too much for the economy. Ever since 1911, she says, we’ve been obsessed with getting stuff and getting it fast. That’s dumb, she says. Deprivation is not only the new normal; it’s the way things should be.”

Those words are particularly ominous as we appear to be entering a period of secular inflation akin to the decades of the 1940s or 1970s, when food and energy rationing was normalized in harsh economic environments.

2020s: A Repeat Of 1940s?

Now that Powell has recently ‘’retired the word ‘transitory,’’’ let’s draw from some historically-similar inflationary periods to gauge what we could be in for in the coming years.

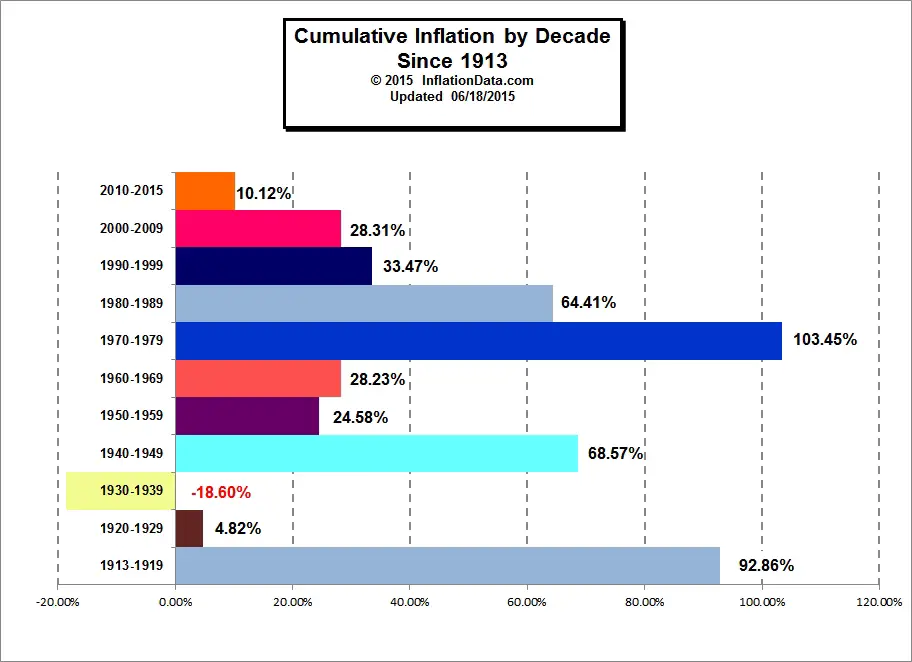

Prices of everyday items were highly volatile during this period of financial repression in the 1940s. Policies like yield curve control (YCC) and heavy fiscal deficits were enforced, as the government attempted to inflate away its debt.

Between 1941 and 1951, total inflation across the CPI inflation basket saw a 76.4% increase, which is a 5.9% annualized inflation rate. The highest yearly inflation print in that time period, which was over 18%, fell between 1946 and 1947.

Food was the component in the CPI basket most affected by the volatile inflation and it subsequently saw the largest price increase during this decade, experiencing an 8% annualized inflation rate.

From January 1941 to May 1943, food was rising at a rapid 18% rate and was similarly volatile between February 1946 and August 1948, experiencing annualized inflation of 19% over the two-year period. Imagine your grocery bill increasing from $100 to $140 in the space of only two years.

In response to the annualized 10% inflation that the U.S. saw in 1941, before the second world war, central planners did what central planners do: The Office of Price Administration (OPA), which became an independent agency in January 1942, was formed to oversee price controls and saw its powers extended and expanded in October of that year with the passage of the “Emergency Stabilization Act.”

The OPA had a busy schedule — many food items, and of course gasoline, were rationed in the early 1940s.

Of course, many items, such as automobiles and radios, were removed from the index and what remained in the CPI basket was heavily manipulated. Shrinkflation was rampant as the CPI index changed the size of a box of corn flakes from 8 ounces to 6 ounces, and many automobile measurements were changed to try and hide the inflation that the public felt during this period.

The price controls were temporarily lifted in 1946, only to be once again called upon in 1951. Both times that price controls were implemented, it only led to food shortages as producers had no incentive to produce large crops when their profits were cut and more pain was felt by the consumer as a result. Inflation only began to dissipate in the early 1950s as a result of the Fed’s tighter monetary policy.

Interest rates were allowed to rise and large fiscal deficits begun to decrease in the early ’50s. The decision to enforce tighter monetary policy also coincidentally led to 15 years of low inflation, highlighted by the green shaded box above in figure 21.

Oil Shortages And Oil Price Fixing

The FTC has had a busy end of year. It has not only been investigating food inflation and putting pressure on food corporations and monopolies like Walmart and Amazon, as we discussed earlier, but the energy producers are also under fire.

President Joe Biden is asking the Federal Trade Commission to look into behavior from energy companies as gas prices hover around a seven-year high.

The national average for a gallon of regular gas stood at $3.41 a month ago, according to data from AAA. That’s up from $2.16 as of one year ago.

Fuel prices aren’t just soaring in the U.S. The entire world is experiencing an energy crisis, as figure 23 below shows that energy prices in Iceland are up over 300% in the last year. The majority of Europe is in the same boat with electricity prices doubling since 2020.

The American Petroleum Institute called Biden’s calls on the FTC a “distraction from the fundamental market shift.”

“The American Petroleum Institute called Wednesday’s letter to the FTC a ‘distraction from the fundamental market shift’ that’s ongoing as economics emerge from the pandemic. The industry group said in a statement that ‘ill-advised government decisions’ are ‘exacerbating this challenging situation.’

‘Rather than launching investigations on markets that are regulated and closely monitored on a daily basis or pleading with OPEC to increase supply, we should be encouraging the safe and responsible development of American-made oil and natural gas,’ said Frank Macchiarola, API’s senior vice president of policy, economics and regulatory affairs.”

–CNBC

But what is he talking about and why is there a shortage of oil?

Well, you see, it’s Biden policies that are causing the oil shortage, which we covered in more detail in this video. In the same way that it was the expansionary monetary policy in the 1940s that caused the significant inflation in that era, massive fiscal deficits and poor policy decisions are similarly causing the inflation today.

Biden, and policy makers globally, are creating the perfect recipe for explosive inflation. Firstly, through over regulation, they’re causing serious supply shortages and then, by creating excess demand in the form of new money through irresponsible QE and fiscal spending, prices were always destined to rise.

Now all of Biden’s attempts to heavily regulate the oil industry have led to a 10% decrease in oil production in 2021.

12.2 million barrels of oil per day were produced in 2019 and today, only 11.7 million barrels are being produced. That’s a 10.6% decline in production which is the largest annual decline on record.

Americans alive today who lived through the oil and energy crisis of the 1970s don’t have fond memories of those times, as they know all too well the devastating effects of over regulation.

Earlier, we explored the inflationary decade of the 1940s and all of the price controls exercised in response. However, the inflation of the ’40s pales in comparison to the inflationary decade of the 1970s, and in response, the subsequent price controls were even more exuberant from our central planners in the ’70s.

Inflationary 1970s Food And Energy Rationing

Inflation remained very tame and low through the 1950s until the late 1960s, until the Federal Reserve began running fiscal deficits which it accelerated in size around 1966 to continue funding the Vietnam War.

The period of time around 1966, when the Fed began spending more than it received in tax receipts, is highlighted below in figure 28.

Subsequently, all Items in the CPI saw a total increase of 186.4%; or 7.3% inflation annually through the years of 1968 to 1983. The inflation of the late ’60s was a warning sign, which ultimately ended with the Nixon Shock, as mentioned above, which only accelerated inflation throughout the decade. Nixon actually won re-election in 1972 based upon his promise to implement price controls in an attempt to slow down inflation.

Nixon introduced a 90-day price freeze on all wages and prices in the economy in 1971, trying to combat the rampant inflation.

In the ’40s, it was food that was heaviest hit by inflation. This time, in the ’70s, it was oil being the driving force behind the rampant inflation.

Nixon issued Executive Order 11615 (pursuant to the “Economic Stabilization Act of 1970”), imposing a 90-day freeze on wages and prices in order to counter inflation.

In 1973, gasoline consumption by Tulsa city vehicles was cut more than 25% to preserve gasoline, and some workers lost their vehicle take-home privileges. Lightbulbs were removed from corporate buildings leaving workers in the dark and speed limits were lowered to 55 miles per hour in an attempt to preserve the scarce petroleum. Only the police and fire departments were exempt from rationing, leaving everyone else fighting over the limited supply.

This morbid video highlights some of the consequences to the price controls that occurred in the 1970s. Price controls on chickens, coupled with the rising cost of chicken feed, meant it was uneconomical for farmers to feed their chickens, leading to large swaths of livestock being wasted.

This article written by Stephen Roache, who was a Fed insider in the 1970s, explains how the Consumer Price Index (CPI) inflation basket was manipulated throughout the 70s. Countless items such as energy, food and housing were all systematically removed from the official CPI inflation basket and by the end of the decade, 75% of the items in the original basket at the beginning of the 1970 had been removed.

All of these price controls and overreaching government actions had no effect on stopping the inflation. It only caused shortages and black markets to emerge, which both wreaked havoc on the economy. The only thing that tamed inflation was more responsible monetary policy, highlighted below in figure 32. In 1981, Paul Volcker finally slowed down inflation after raising interest rates to 20%, in a desperate attempt to put an end to the most inflationary decade in U.S. economic history.

Notice the common theme that stopped rampant inflation in both the 1940s and the 1970s? Responsible monetary policy decisions. Price controls and further regulation failed in both decades and concerningly, policy makers at the helm today in the 2020s appear ignorant to history.

Price Controls Making A Comeback In The Great Inflationary Decade Of 2020s?

Are these recent suggestions and recent inquiries from Biden, Warren and the FTC clues that rent controls weren’t the first signs of policy makers planning on becoming a larger part of our economy in the near future?

Oregon and California were the first states in the U.S. to begin the trend of using rent controls in 2019, in an attempt to tackle housing affordability. Oregon introduced a statewide law that capped homeowners from raising their rents by 7% plus inflation, and California followed suit, introducing a 5%-plus-inflation-rent-increase cap on homeowners.

This trend of homeowners being blamed continued in early 2020, with the introduction of a housing moratorium for renters. Many lost their jobs as a result of the government mandated lockdowns and subsequently were unable to pay their rent.

As of mid-August 2021, 5.9 million renter households, 15% of all renters, were behind on their rent payments.

Again, the unaffordability of houses is a consequence of low interest rates and central banks globally continuing to engage in QE. The Fed now owns around 30% of the total mortgage-backed security market in the U.S.

The trend of more central planning in the U.S. seems to be accelerating of late, as Joe Biden, Elizabeth Warren and the FTC have all been calling for more government control in the last handful of weeks alone.

Central planning always fails, and one simple chart helps to explain this phenomenon:

Central banks claim their interference with the free market helps to smooth the business cycle. However, it’s very clear that since 1913, and the creation of the Fed, markets have only continued to get more and more volatile.

In each occasion that there was a slowdown in the short-term business cycle, the next crash is becoming larger and faster than the previous one. You can’t remove volatility from the markets, you can only push it further into the future, where it’s effects are compounded by magnitudes when they eventually arrive.

And the more that the central bankers try to fix things, the worse they become.

In a recent video, we discussed what the final stages of what von Mises called the ‘’crack-up boom’’ generally looks like.

“The course of a progressing inflation is this: At the beginning the inflow of additional money makes the prices of some commodities and services rise… There are still people in the country who have not yet become aware of the fact that they are confronted with a price revolution which will finally result in a considerable rise of all prices… These people still believe that prices one day will drop. Waiting for this day, they restrict their purchases and concomitantly increase their cash holdings…

But then, finally, the masses wake up. They become suddenly aware of the fact that inflation is a deliberate policy and will go on endlessly. A breakdown occurs. The crack-up boom appears. Everybody is anxious to swap his money against ‘real’ goods, no matter whether he needs them or not, no matter how much money he has to pay for them.

Within a very short time, within a few weeks or even days, the things which were used as money are no longer used as media of exchange. They become scrap paper. Nobody wants to give away anything against them.”

And this time is coming fast. Trust is a very fickle thing, and once it is lost, it is gone for good. Currently, trust is being lost in currency at an accelerated pace.

A recent survey with 11,000 participants in 76 countries found that 41% of people globally say they trust bitcoin over local currencies:

The time to buy insurance for your house is “before” the fire comes. And the time to protect yourself from the Federal Reserve induced “crack-up boom” by moving your wealth from cash to bitcoin is before the crack-up boom happens. Because once it happens, it will be too late.

The good news is you still have time, stack accordingly.

Additional Resources:

- “Biden Halts Oil And Gas Leases, Permits On U.S. Land And Water”

- “Why is Biden Halting Federal Oil And Gas Sales?”

- “Keystone XL Pipeline Halted As Biden Revokes Permit”

- “Biden Might Close Michigan Pipeline, WH Admits After Calling Report Bogus”

- “White House Confirms Biden Effort To Shut Down Another Major Pipeline”

- “Biden Shutting Down Line 5 Pipeline Could Send Gas Prices Surging”

- “Biden: OPEC And Russia Must Pump More Oil To Help America’s Working Class”

- “Biden’s Energy Idiocy: Kneecap U.S. Oil But Beg OPEC To Pump More”

- “U.S. Shale Has A Message For The Biden Administration: Ask Us To Increase Oil Production, Not OPEC”

This is a guest post by Mark Moss. Opinions expressed are entirely their own and do not necessarily reflect those of BTC Inc or Bitcoin Magazine.

yield curve pandemic dow jones bitcoin btc currencies commodities stock markets gold oilGovernment

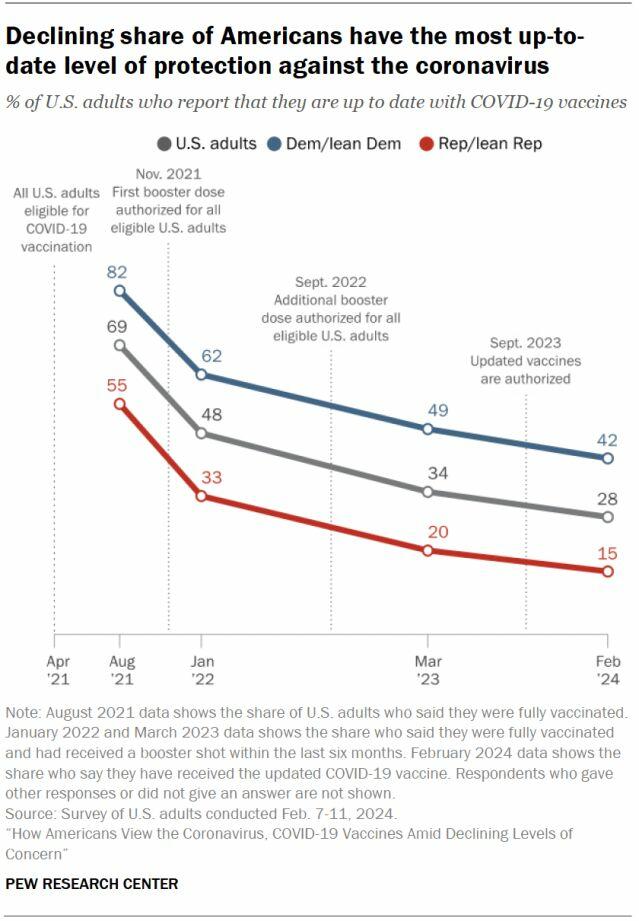

Survey Shows Declining Concerns Among Americans About COVID-19

Survey Shows Declining Concerns Among Americans About COVID-19

A new survey reveals that only 20% of Americans view covid-19 as "a major threat"…

Share this:

A new survey reveals that only 20% of Americans view covid-19 as "a major threat" to the health of the US population - a sharp decline from a high of 67% in July 2020.

What's more, the Pew Research Center survey conducted from Feb. 7 to Feb. 11 showed that just 10% of Americans are concerned that they will catch the disease and require hospitalization.

"This data represents a low ebb of public concern about the virus that reached its height in the summer and fall of 2020, when as many as two-thirds of Americans viewed COVID-19 as a major threat to public health," reads the report, which was published March 7.

According to the survey, half of the participants understand the significance of researchers and healthcare providers in understanding and treating long COVID - however 27% of participants consider this issue less important, while 22% of Americans are unaware of long COVID.

What's more, while Democrats were far more worried than Republicans in the past, that gap has narrowed significantly.

"In the pandemic’s first year, Democrats were routinely about 40 points more likely than Republicans to view the coronavirus as a major threat to the health of the U.S. population. This gap has waned as overall levels of concern have fallen," reads the report.

More via the Epoch Times;

The survey found that three in ten Democrats under 50 have received an updated COVID-19 vaccine, compared with 66 percent of Democrats ages 65 and older.

Moreover, 66 percent of Democrats ages 65 and older have received the updated COVID-19 vaccine, while only 24 percent of Republicans ages 65 and older have done so.

“This 42-point partisan gap is much wider now than at other points since the start of the outbreak. For instance, in August 2021, 93 percent of older Democrats and 78 percent of older Republicans said they had received all the shots needed to be fully vaccinated (a 15-point gap),” it noted.

COVID-19 No Longer an Emergency

The U.S. Centers for Disease Control and Prevention (CDC) recently issued its updated recommendations for the virus, which no longer require people to stay home for five days after testing positive for COVID-19.

The updated guidance recommends that people who contracted a respiratory virus stay home, and they can resume normal activities when their symptoms improve overall and their fever subsides for 24 hours without medication.

“We still must use the commonsense solutions we know work to protect ourselves and others from serious illness from respiratory viruses, this includes vaccination, treatment, and staying home when we get sick,” CDC director Dr. Mandy Cohen said in a statement.

The CDC said that while the virus remains a threat, it is now less likely to cause severe illness because of widespread immunity and improved tools to prevent and treat the disease.

“Importantly, states and countries that have already adjusted recommended isolation times have not seen increased hospitalizations or deaths related to COVID-19,” it stated.

The federal government suspended its free at-home COVID-19 test program on March 8, according to a website set up by the government, following a decrease in COVID-19-related hospitalizations.

According to the CDC, hospitalization rates for COVID-19 and influenza diseases remain “elevated” but are decreasing in some parts of the United States.

International

Rand Paul Teases Senate GOP Leader Run – Musk Says “I Would Support”

Rand Paul Teases Senate GOP Leader Run – Musk Says "I Would Support"

Republican Kentucky Senator Rand Paul on Friday hinted that he may jump…

Share this:

Republican Kentucky Senator Rand Paul on Friday hinted that he may jump into the race to become the next Senate GOP leader, and Elon Musk was quick to support the idea. Republicans must find a successor for periodically malfunctioning Mitch McConnell, who recently announced he'll step down in November, though intending to keep his Senate seat until his term ends in January 2027, when he'd be within weeks of turning 86.

So far, the announced field consists of two quintessential establishment types: John Cornyn of Texas and John Thune of South Dakota. While John Barrasso's name had been thrown around as one of "The Three Johns" considered top contenders, the Wyoming senator on Tuesday said he'll instead seek the number two slot as party whip.

Paul used X to tease his potential bid for the position which -- if the GOP takes back the upper chamber in November -- could graduate from Minority Leader to Majority Leader. He started by telling his 5.1 million followers he'd had lots of people asking him about his interest in running...

Thousands of people have been asking if I'd run for Senate leadership...

— Rand Paul (@RandPaul) March 8, 2024

...then followed up with a poll in which he predictably annihilated Cornyn and Thune, taking a 96% share as of Friday night, with the other two below 2% each.

????????️VOTE NOW ????️ ???? Who would you like to be the next Senate leader?

— Rand Paul (@RandPaul) March 8, 2024

Elon Musk was quick to back the idea of Paul as GOP leader, while daring Cornyn and Thune to follow Paul's lead by throwing their names out for consideration by the Twitter-verse X-verse.

I would support Rand Paul and suspect that other candidates will not actually run polls out of concern for the results, but let’s see if they will!

— Elon Musk (@elonmusk) March 8, 2024

Paul has been a stalwart opponent of security-state mass surveillance, foreign interventionism -- to include shoveling billions of dollars into the proxy war in Ukraine -- and out-of-control spending in general. He demonstrated the latter passion on the Senate floor this week as he ridiculed the latest kick-the-can spending package:

This bill is an insult to the American people. The earmarks are all the wasteful spending that you could ever hope to see, and it should be defeated. Read more: https://t.co/Jt8K5iucA4 pic.twitter.com/I5okd4QgDg

— Senator Rand Paul (@SenRandPaul) March 8, 2024

In February, Paul used Senate rules to force his colleagues into a grueling Super Bowl weekend of votes, as he worked to derail a $95 billion foreign aid bill. "I think we should stay here as long as it takes,” said Paul. “If it takes a week or a month, I’ll force them to stay here to discuss why they think the border of Ukraine is more important than the US border.”

Don't expect a Majority Leader Paul to ditch the filibuster -- he's been a hardy user of the legislative delay tactic. In 2013, he spoke for 13 hours to fight the nomination of John Brennan as CIA director. In 2015, he orated for 10-and-a-half-hours to oppose extension of the Patriot Act.

Among the general public, Paul is probably best known as Capitol Hill's chief tormentor of Dr. Anthony Fauci, who was director of the National Institute of Allergy and Infectious Disease during the Covid-19 pandemic. Paul says the evidence indicates the virus emerged from China's Wuhan Institute of Virology. He's accused Fauci and other members of the US government public health apparatus of evading questions about their funding of the Chinese lab's "gain of function" research, which takes natural viruses and morphs them into something more dangerous. Paul has pointedly said that Fauci committed perjury in congressional hearings and that he belongs in jail "without question."

Musk is neither the only nor the first noteworthy figure to back Paul for party leader. Just hours after McConnell announced his upcoming step-down from leadership, independent 2024 presidential candidate Robert F. Kennedy, Jr voiced his support:

Mitch McConnell, who has served in the Senate for almost 40 years, announced he'll step down this November.

— Robert F. Kennedy Jr (@RobertKennedyJr) February 28, 2024

Part of public service is about knowing when to usher in a new generation. It’s time to promote leaders in Washington, DC who won’t kowtow to the military contractors or…

In a testament to the extent to which the establishment recoils at the libertarian-minded Paul, mainstream media outlets -- which have been quick to report on other developments in the majority leader race -- pretended not to notice that Paul had signaled his interest in the job. More than 24 hours after Paul's test-the-waters tweet-fest began, not a single major outlet had brought it to the attention of their audience.

That may be his strongest endorsement yet.

Government

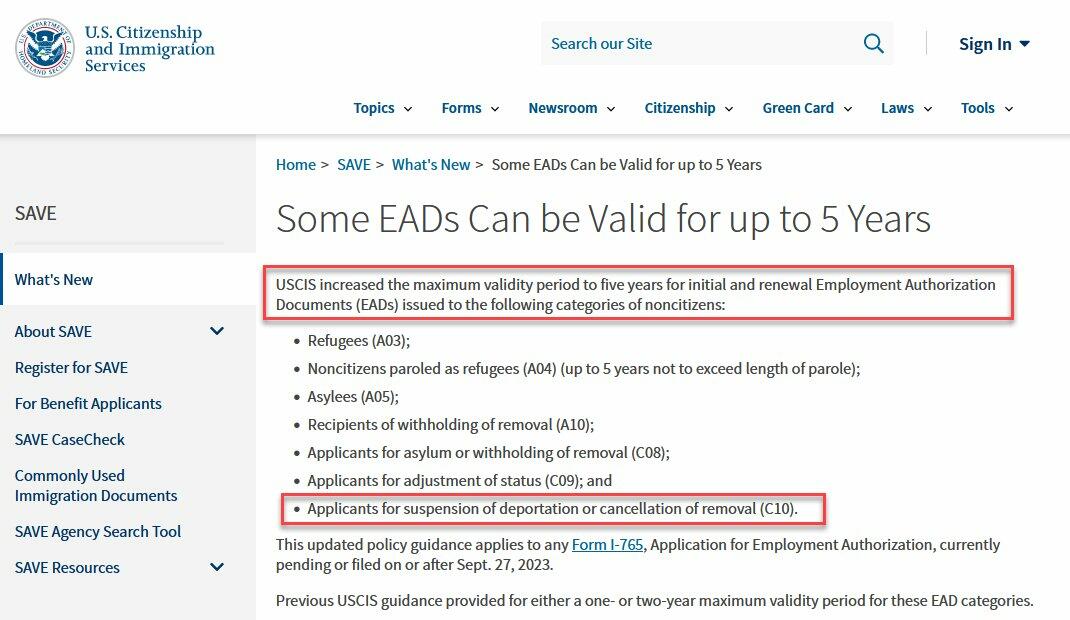

The Great Replacement Loophole: Illegal Immigrants Score 5-Year Work Benefit While “Waiting” For Deporation, Asylum

The Great Replacement Loophole: Illegal Immigrants Score 5-Year Work Benefit While "Waiting" For Deporation, Asylum

Over the past several…

Share this:

{kind=link}

{kind=link}

{kind=link}

{kind=link}

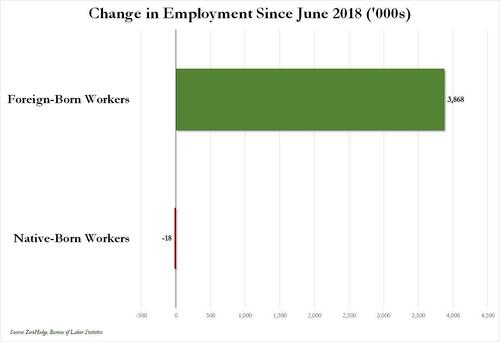

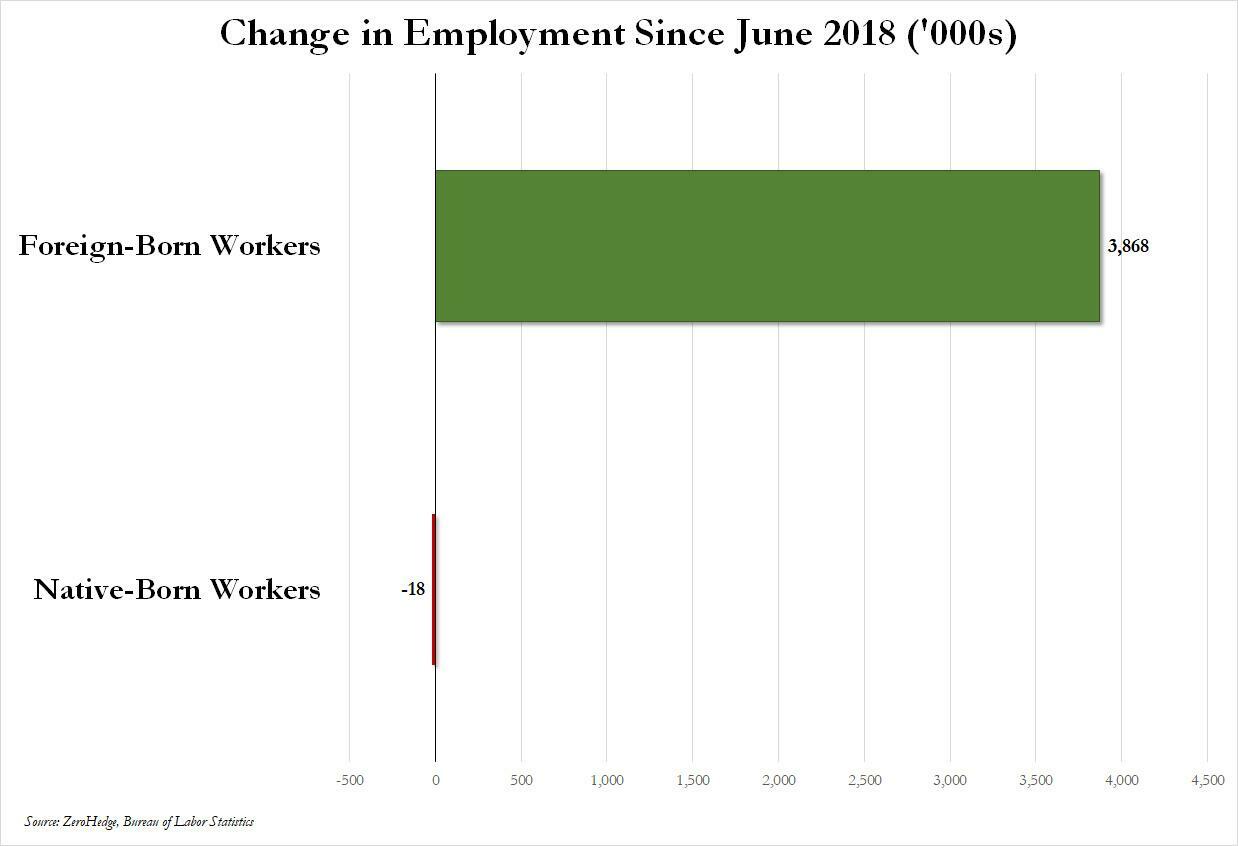

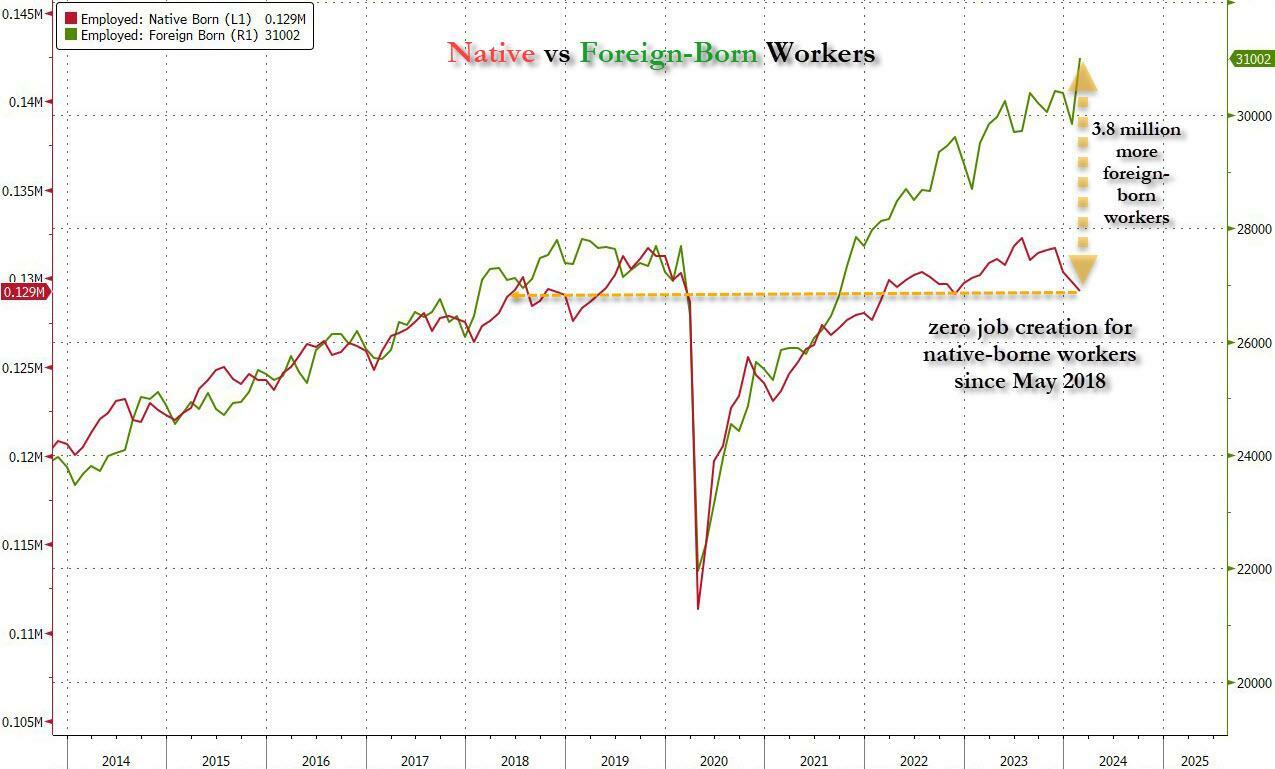

Over the past several months we've pointed out that there has been zero job creation for native-born workers since the summer of 2018...

{kind=link}

... and that since Joe Biden was sworn into office, most of the post-pandemic job gains the administration continuously brags about have gone foreign-born (read immigrants, mostly illegal ones) workers.

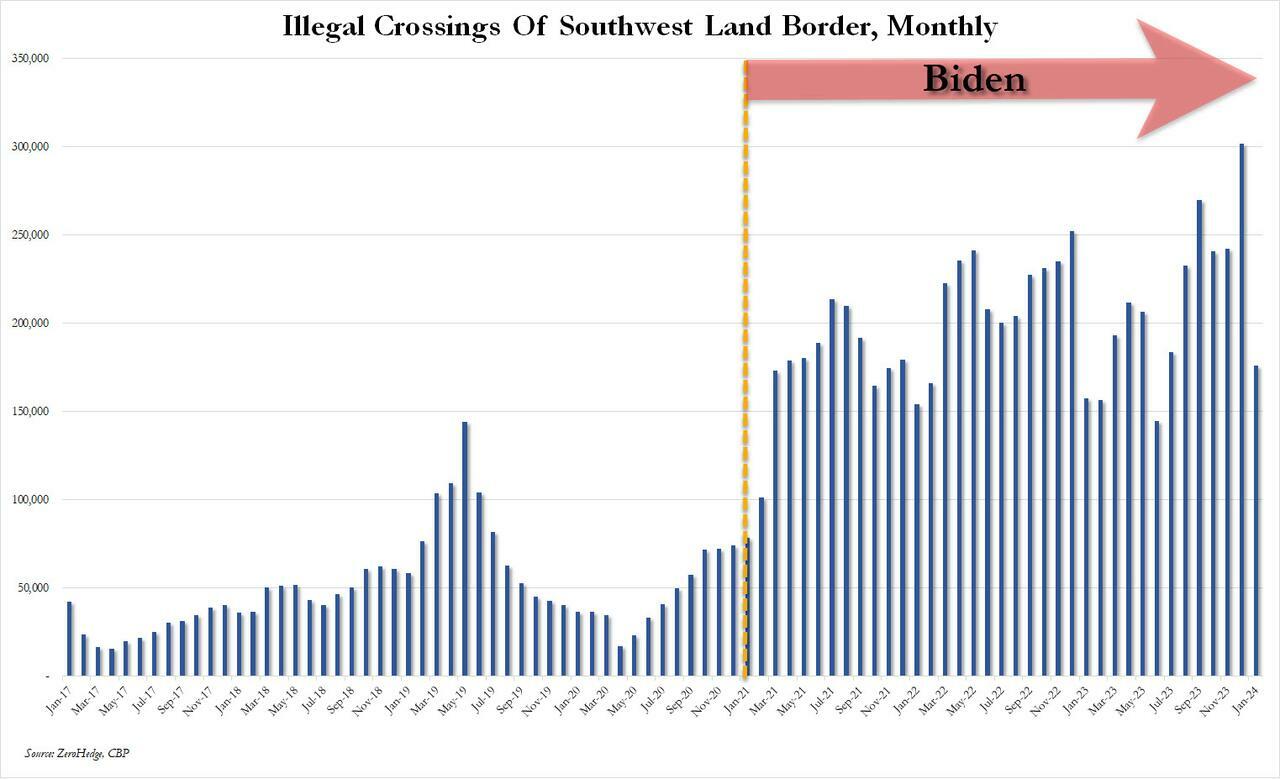

And while the left might find this data almost as verboten as FBI crime statistics - as it directly supports the so-called "great replacement theory" we're not supposed to discuss - it also coincides with record numbers of illegal crossings into the United States under Biden.

In short, the Biden administration opened the floodgates, 10 million illegal immigrants poured into the country, and most of the post-pandemic "jobs recovery" went to foreign-born workers, of which illegal immigrants represent the largest chunk.

'But Tyler, illegal immigrants can't possibly work in the United States whilst awaiting their asylum hearings,' one might hear from the peanut gallery. On the contrary: ever since Biden reversed a key aspect of Trump's labor policies, all illegal immigrants - even those awaiting deportation proceedings - have been given carte blanche to work while awaiting said proceedings for up to five years...

... something which even Elon Musk was shocked to learn.

Wow, learn something new every day https://t.co/8MDtEEZGam

— Elon Musk (@elonmusk) March 10, 2024

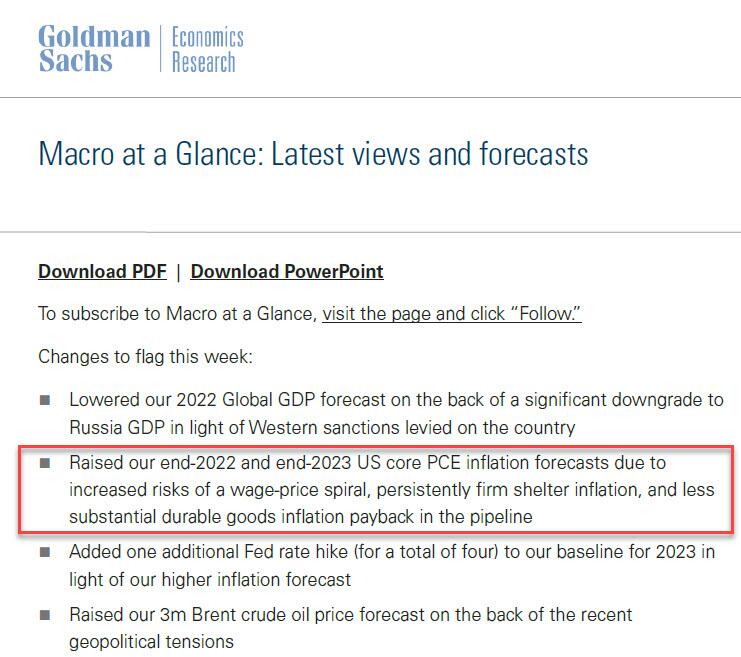

Which leads us to another question: recall that the primary concern for the Biden admin for much of 2022 and 2023 was soaring prices, i.e., relentless inflation in general, and rising wages in particular, which in turn prompted even Goldman to admit two years ago that the diabolical wage-price spiral had been unleashed in the US (diabolical, because nothing absent a major economic shock, read recession or depression, can short-circuit it once it is in place).

Well, there is one other thing that can break the wage-price spiral loop: a flood of ultra-cheap illegal immigrant workers. But don't take our word for it: here is Fed Chair Jerome Powell himself during his February 60 Minutes interview:

PELLEY: Why was immigration important?

POWELL: Because, you know, immigrants come in, and they tend to work at a rate that is at or above that for non-immigrants. Immigrants who come to the country tend to be in the workforce at a slightly higher level than native Americans do. But that's largely because of the age difference. They tend to skew younger.

PELLEY: Why is immigration so important to the economy?

POWELL: Well, first of all, immigration policy is not the Fed's job. The immigration policy of the United States is really important and really much under discussion right now, and that's none of our business. We don't set immigration policy. We don't comment on it.

I will say, over time, though, the U.S. economy has benefited from immigration. And, frankly, just in the last, year a big part of the story of the labor market coming back into better balance is immigration returning to levels that were more typical of the pre-pandemic era.

PELLEY: The country needed the workers.

POWELL: It did. And so, that's what's been happening.

Translation: Immigrants work hard, and Americans are lazy. But much more importantly, since illegal immigrants will work for any pay, and since Biden's Department of Homeland Security, via its Citizenship and Immigration Services Agency, has made it so illegal immigrants can work in the US perfectly legally for up to 5 years (if not more), one can argue that the flood of illegals through the southern border has been the primary reason why inflation - or rather mostly wage inflation, that all too critical component of the wage-price spiral - has moderated in in the past year, when the US labor market suddenly found itself flooded with millions of perfectly eligible workers, who just also happen to be illegal immigrants and thus have zero wage bargaining options.

None of this is to suggest that the relentless flood of immigrants into the US is not also driven by voting and census concerns - something Elon Musk has been pounding the table on in recent weeks, and has gone so far to call it "the biggest corruption of American democracy in the 21st century", but in retrospect, one can also argue that the only modest success the Biden admin has had in the past year - namely bringing inflation down from a torrid 9% annual rate to "only" 3% - has also been due to the millions of illegals he's imported into the country.

We would be remiss if we didn't also note that this so often carries catastrophic short-term consequences for the social fabric of the country (the Laken Riley fiasco being only the latest example), not to mention the far more dire long-term consequences for the future of the US - chief among them the trillions of dollars in debt the US will need to incur to pay for all those new illegal immigrants Democrat voters and low-paid workers. This is on top of the labor revolution that will kick in once AI leads to mass layoffs among high-paying, white-collar jobs, after which all those newly laid off native-born workers hoping to trade down to lower paying (if available) jobs will discover that hardened criminals from Honduras or Guatemala have already taken them, all thanks to Joe Biden.

Veterans Affairs Kept COVID-19 Vaccine Mandate In Place Without Evidence

The Coming Of The Police State In America

‘I couldn’t stand the pain’: the Turkish holiday resort that’s become an emergency dental centre for Britons who can’t get treated at home

Beloved mall retailer files Chapter 7 bankruptcy, will liquidate

February Employment Situation

Rand Paul Teases Senate GOP Leader Run – Musk Says “I Would Support”

Low Iron Levels In Blood Could Trigger Long COVID: Study

Walmart has really good news for shoppers (and Joe Biden)

Another beloved brewery files Chapter 11 bankruptcy

Walmart joins Costco in sharing key pricing news

-

Uncategorized2 weeks ago

Uncategorized2 weeks agoAll Of The Elements Are In Place For An Economic Crisis Of Staggering Proportions

-

Uncategorized1 month ago

Uncategorized1 month agoCathie Wood sells a major tech stock (again)

-

Uncategorized3 weeks ago

Uncategorized3 weeks agoCalifornia Counties Could Be Forced To Pay $300 Million To Cover COVID-Era Program

-

Uncategorized2 weeks ago

Uncategorized2 weeks agoApparel Retailer Express Moving Toward Bankruptcy

-

Uncategorized4 weeks ago

Uncategorized4 weeks agoIndustrial Production Decreased 0.1% in January

-

International3 days ago

International3 days agoWalmart launches clever answer to Target’s new membership program

-

International3 days ago

International3 days agoEyePoint poaches medical chief from Apellis; Sandoz CFO, longtime BioNTech exec to retire

-

Uncategorized3 weeks ago

Uncategorized3 weeks agoRFK Jr: The Wuhan Cover-Up & The Rise Of The Biowarfare-Industrial Complex