Government

S&P Futures Jump To Five Month High, Dollar Spikes In Bullish Start To New Month

S&P Futures Jump To Five Month High, Dollar Spikes In Bullish Start To New Month

Share this:

World stocks rose and US futures jumped to the highest level since late February even as U.S. lawmakers struggled to agree on the next round of coronavirus aid while Covid cases around the globe continued to rise, while a squeeze on crowded short positions left the dollar clinging to a tentative bounce.

S&P 500 futures turned higher, reversing earlier losses with Microsoft rising in pre-market trading as it tried to salvage a deal for the U.S. operations of TikTok. Marathon Petroleum jumped after agreeing to sell its gasoline-station business for $21 billion. Still, investors remained jittery amid the lack of a progress on the stimulus package and White House Chief of Staff Mark Meadows not optimistic about a deal.

"Three months to go until the U.S. Presidential election! Surely Congress will want to get something over the line regarding new stimulus in the U.S. driven more by politics than necessarily economics," said Chris Bailey, European strategist at Raymond James.

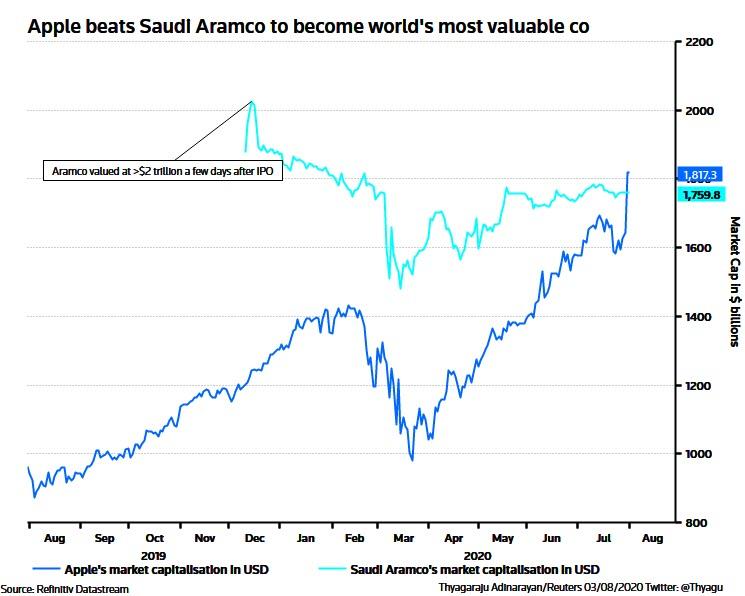

On Friday, Fitch Ratings cut the outlook on the United States’ triple-A credit rating to negative from stable and said the direction of fiscal policy depends in part on the November election and the resulting makeup of Congress, cautioning that policy gridlock could continue. However, as Reuters notes, those concerns have hardly hit the U.S. technology sector, evident in Friday’s record highs, with Apple overtaking Saudi Aramco to become the world’s most valuable company.

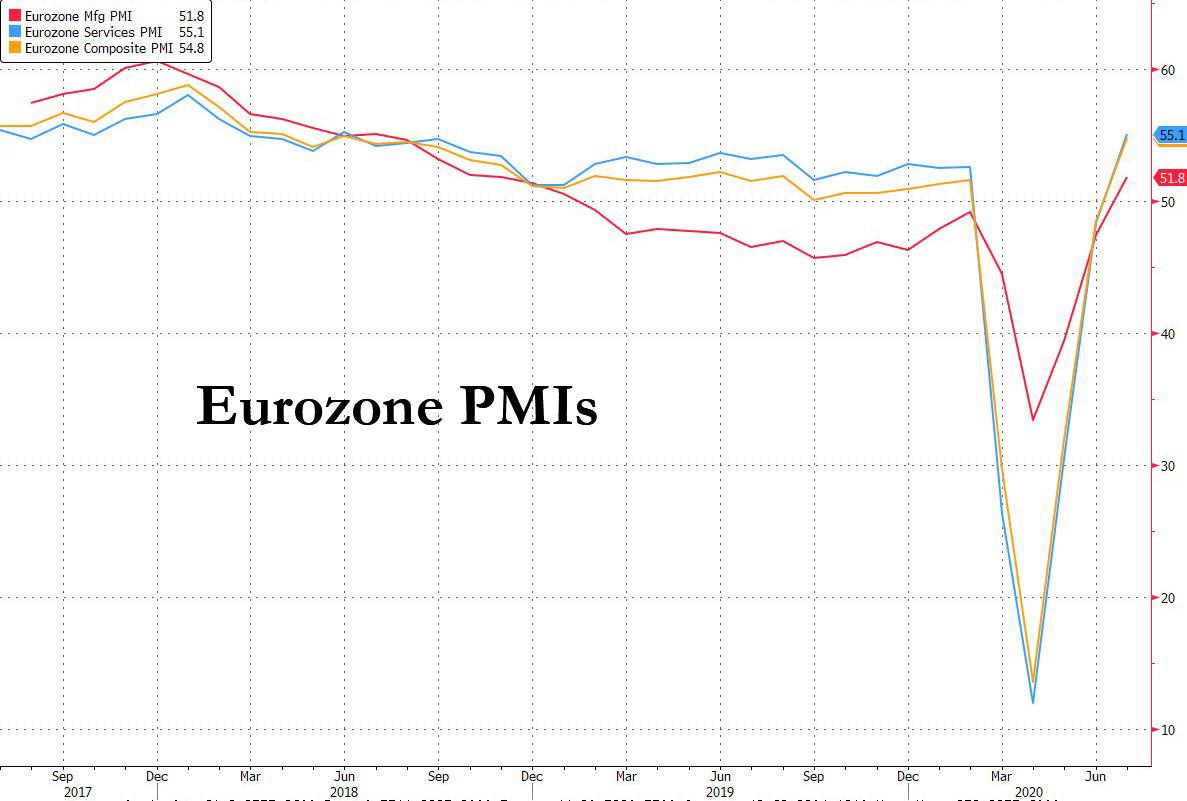

In Europe, stocks were up over 1% with all but four sector indexes advancing, with gains led by automakers, technology and chemicals sub- indexes, which are all up at least 1.7%. Travel and leisure stocks are the worst performers. Technology stocks rallied on positive read-across from peers on the other side of the Atlantic, while automobile shares jumped after the euro area recorded its first manufacturing expansion in one-and-a-half years when the final Eurozone mfg PMI printed at 51.8, above the 51.1 expected.

Spanish stocks, meanwhile, declined on Monday as the country saw the biggest jump in coronavirus cases since a national lockdown was lifted in June, while data showed international tourist arrivals to the country fell 98% year on year in June. “Second wave virus concerns are building in Australia, Europe etc. but no huge risk-aversion move,” said Bailey.

European gains were also limited by a selloff in big banks’ shares, with index heavyweight HSBC falling 5% to a fresh 11 year low after it warned that its bad debt charges could surge to as much as $13 billion, and France’s Societe Generale reported a 1.26 billion euro ($1.48 billion) second-quarter loss.

Earlier in the session, Asian stocks also gained, led by communications and health care, after falling in the last session. Most markets in the region were down, with Jakarta Composite dropping 2.8% and Singapore's Straits Times Index falling 1.9%, while Japan's Topix Index gained 1.8%. The Topix gained 1.8%, with ISB and ITmedia rising the most. The Shanghai Composite Index rose 1.8%, with Raytron Technology and Piesat Information Technology Co Ltd posting the biggest advances as investor margin debt resumed its climb.

Factory activity data from China showed the fastest pace of expansion in nearly a decade.

That helped China's blue chips rally 1.6%, offsetting worries about U.S.-China relations. Japan's Nikkei meanwhile added 2.2%, courtesy of a pullback in the yen.

"There is going to be a recovery -- we shouldn’t lose track of that as we go through this period,” Anne Anderson, head of fixed income at UBS Asset Management Australia, said on Bloomberg TV. “But returning to where we were before we started is going to be a real challenge and is going to require ongoing monetary and fiscal support. It’s a long way out of here."

Meanwhile, tension between the U.S. and China emerged as another threat to risk appetite. The Trump administration will announce measures shortly against “a broad array” of Chinese-owned software deemed to pose national-security risks, U.S. Secretary of State Michael Pompeo said. Even so, shares advanced in Japan and China, where mainland-listed technology stocks surged on expectations of support from Beijing in response to U.S. moves against Chinese-owned software companies.

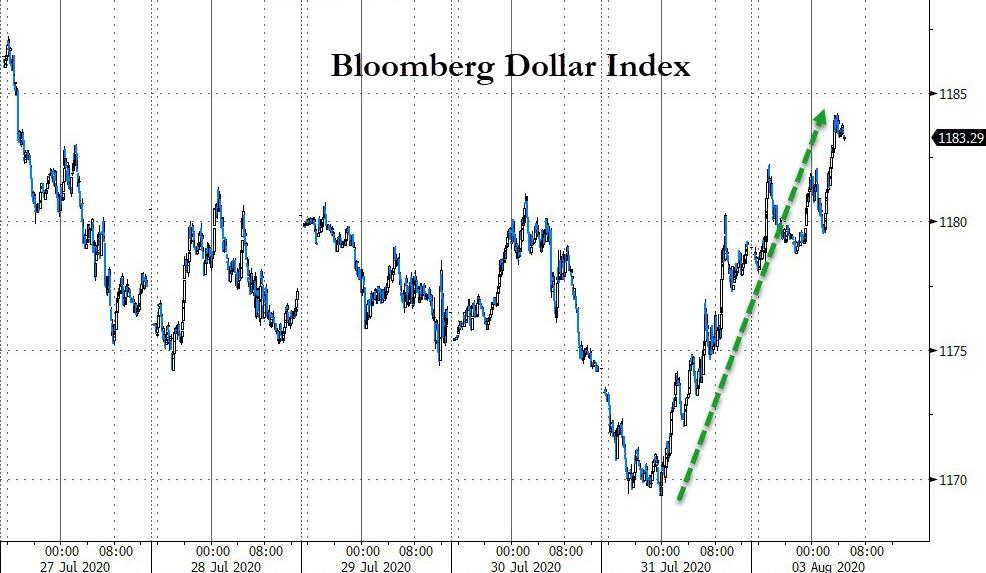

In FX, Dollar bears also took some profits as short positions hit an 11 year high, with the Bloomberg Dollar Spot Index heading for its biggest two-day gain in seven weeks, with the greenback rising against all Group-of-10 peers except the Swedish krona and the yen.

but any further gains were capped by the slowing U.S. economic recovery from COVID-19 and real rates breaking below -1% for the first time.

The real 10Y rate hit a record low amid a marked flattening of the yield curve as investors wager on more accommodation from the Federal Reserve.

The euro and the pound were down only slightly with the dollar at $1.1755 per euro and $1.3065 per pound. Both the currencies recorded their best monthly gain in nearly a decade in July.

“Amid improvements in business sentiment, signals are emerging that the initial boost from pent-up demand is fading and consumer confidence is slipping lower,” economists at Barclays wrote in a note. "Together with concerns about labour market and virus developments, this clouds the outlook and could be exacerbated if U.S. fiscal support is not renewed in time."

In rates, 10-year Treasury yields were higher at 0.5576% after touching the lowest level since March last week. German government bond yields rose slightly to -0.527%. Treasuries bear steepened as month-end support came out of the market and investors looked ahead to Wednesday’s supply announcement where record sales of notes and bonds are expected. Yields higher by up to 3bp across long-end of the curve with front-end broadly anchored, steepening 2s10s, 5s30s by ~1.5bp each; 10-year yields around 0.545%, cheaper by 1.5bp vs. Friday close while bunds, gilts outperform by ~2bp each. Yields on 30-year U.S. Treasuries are set for the biggest daily increase since June 30 as U.S. equity futures advance and the bond curve bear-steepens. As Bloomberg adds, a busy week of IG corporate issuance also expected, adding to downside pressure on Treasuries along with delta hedging large option package.

The recent decline in the dollar combined with super-low real bond yields has been a boon for gold, which hit $1,984 an ounce on Monday and seemed on track to take out $2,000 soon.

In other commodities, oil prices eased on concerns about oversupply as OPEC and its allies are due to pull back from production cuts in August while an increase in COVID-19 cases raised fears of slower pick-up in fuel demand. Brent crude futures dipped 46 cents to $43.06 a barrel, while U.S. crude eased 51 cents to $39.76.

On today's calendar, economic data include ISM and Markit manufacturing data. Ferrari is among today’s scheduled earnings.

Market Snapshot

- S&P 500 futures down 0.1% to 3,260.50

- STOXX Europe 600 up 0.4% to 357.57

- MXAP up 0.3% to 165.11

- MXAPJ down 0.4% to 549.24

- Nikkei up 2.2% to 22,195.38

- Topix up 1.8% to 1,522.64

- Hang Seng Index down 0.6% to 24,458.13

- Shanghai Composite up 1.8% to 3,367.97

- Sensex down 1.7% to 36,967.20

- Australia S&P/ASX 200 down 0.03% to 5,926.09

- Kospi up 0.07% to 2,251.04

- Brent Futures down 0.6% to $43.24/bbl

- Gold spot down 0.2% to $1,972.89

- U.S. Dollar Index up 0.1% to 93.44

- German 10Y yield rose 0.4 bps to -0.52%

- Euro down 0.03% to $1.1775

- Brent Futures down 0.6% to $43.24/bbl

- Italian 10Y yield rose 4.2 bps to 0.887%

- Spanish 10Y yield rose 0.2 bps to 0.342%

Top Overnight News from Bloomberg

- Factories across the euro area saw a stronger return to growth in July than initially reported, marking the region’s first manufacturing expansion in one-and-a-half years while economies from Germany to Italy beat expectations. In the U.K., although numbers were slightly below flash estimates, manufacturing grew at the fastest pace in almost three years as the nation’s lockdown eased

- Gold’s spot and futures prices opened the week by hitting records, with the metal for immediate delivery closing in on $2,000 an ounce as the search for haven assets continues amid the coronavirus pandemic

- Microsoft chief executive Satya Nadella attempted to salvage a deal for the U.S. operations of TikTok by speaking with President Donald Trump by phone

- Oil edged below $40 a barrel in New York as OPEC and allied producers started to unwind output cuts even as many countries are still struggling to contain the virus

Asian equity markets began the new trading month mixed after last Friday’s positive close on Wall St where the tech sector rallied following earnings from the industry giants including Apple which rose to a fresh record high, but with upside in the region restricted ahead of this week’s risk events and after continued stalemate in US coronavirus relief discussions. ASX 200 (flat) was subdued as gains in commodity related sectors were offset by underperformance in the top weighted financials and with trade hampered by reduced liquidity due to bank holiday in New South Wales, while risk appetite was also weighed by a state of disaster declaration in Victoria with the state capital of Melbourne to be subjected to tougher restrictions including a curfew through to at least September 13th. Nikkei 225 (+2.2%) was the stellar performer as it coat-tailed on recent favourable currency flows and after Q1 Final GDP topped estimates, although there were some notable losses seen in Shinsei Bank and Mazda post earnings, as well as Seven & I on news it is to acquire Speedway convenience stores from Marathon Petroleum in a deal valued around USD 18.9bln. Hang Seng (-0.6%) and Shanghai Comp. (+1.8%) were mixed after PBoC inaction resulted to a CNY 100bln liquidity drain and as participants digested a more than 50% drop in HSBC HY profits, as well as the highest Chinese Caixin Manufacturing PMI reading since 2011. There was also plenty of focus around tech after reports that President Trump is to allow 45 days for ByteDance to negotiate the sale of TikTok to Microsoft and will reportedly take action on Chinese software companies that threaten national security in the approaching days. Finally, 10yr JGBs were lower amid a surge in Japanese stocks and with the BoJ present in the market for JPY 450bln of JGBs predominantly focused on 1yr-3yr maturities, while the central bank recently announced its buying intentions for August in which it maintained the current pace of purchases for all maturities.

Top Asian News

- Why Investors Keep Losing Money Betting Against the Hong Kong Dollar Peg

- Goldman, BofA Left Off Ant IPO for Work With Alibaba Rivals

- SoftBank, Naver to Start Joint Tender Offer for Line on Aug. 4

Mixed trade in the European equity sphere (Euro Stoxx 50 +0.6%) after a similar lead from APAC markets, as participants remain on standby for this week’s key risk events - including US ISM and labour market report alongside any updates on fiscal stimulus talks. Core EU bourses saw some upside in the run-up to the Final Manufacturing PMIs, potentially on optimism for higher revisions, but indices have since remained contained. UK’s FTSE 100 lags the core markets on currency dynamics, and with the Financial sector hit on the back of dismal earnings from HSBC (-5.1%) where Q2 profit slumped and loan loss provisions rose almost seven-fold. Furthermore, SocGen (-3.1%) adds to the woes in the sector after posting a surprise loss due to pandemic impact on equity trading. Energy names have also lost steam amid price action in the complex, but overall European sectors remain mixed with no clear risk tone to be derived. The sectoral breakdown sees Travel and Leisure at the bottom as second wave fears materialise in the sector. Elsewhere of note, AI company Shanghai Zhizhen Network Technology is suing Apple for around USD 1.4bln over virtual assistant patent violations, WSJ reported.

Top European News

- U.K. Manufacturing Grows as Sector Starts Long Road to Recovery

- Euro-Area Factories Returned to Growth Amid Severe Jobs Cuts

- Real Estate Stocks Fall on Lockdown Concerns, Negative Sentiment

In FX, mixed macro impulses for the Franc as Swiss CPI was considerably firmer than forecast, but the manufacturing PMI fell short of expectations and the key 50.0 mark to leave Usd/Chf eyeing 0.9200 and Eur/Chf even closer to 1.0800 following yet another rise in weekly bank sight deposits. Moreover, the cross has rebounded amidst Eurozone manufacturing PMIs that beat consensus and underpinned EU stocks alongside economic recovery hopes. Conversely, the COVID-19 escalation in Melbourne, Victoria has prompted a state of disaster amidst tougher restrictions and a curfew in the capital until September 13, at the earliest, on the eve of the RBA policy meeting – full preview of the event available on the headline feed – to the detriment of the Aussie that is holding just above 0.7100 vs the Greenback compared to last Friday’s 0.7200+ new ytd peak.

- USD - The Dollar has handed back some of its pre-month end gains after the DXY rebounded further from fresh 2020 lows (92.546) to 93.708 and is now pivoting 93.500, with additional support coming via M&A flows due to deals amounting to Usd 16.4 bn and Usd 21 bn for US companies from German and Japanese rivals respectively. Ahead, the final Markit manufacturing PMI, ISM equivalent and construction spending before a duo of Fed speakers (Bullard and Evans).

- JPY/GBP/NZD - All intiailly firmer against the Buck, or off worst levels to be more precise, as the Yen regains composure following its aggressive reversal from the low 104.00 area to 106.40+, while Sterling revisited 1.3100 from not far off 1.3050 even though the final UK manufacturing PMI was revised down a tad and the coronavirus outbreak in Northern England has reached ‘major incident’ proportions in Greater Manchester. Elsewhere, the Kiwi is benefiting from the aforementioned Aussie travails to an extent given Aud/Nzd pulling back below 1.0750 to keep Nzd/Usd more buoyant on the 0.6600 handle despite reports that hedge funds are implementing bearish positions ahead of the RNBZ later in August.

- EUR/CAD/SEK/NOK - Some traction for the Euro within 1.1796-42 parameters vs the Greenback in wake of the better than prelim/anticipated Eurozone manufacturing PMIs, but no confirmed breach of resistance in the form of the 100 HMA (1.1779), while the Loonie is sub-1.3400 amidst another downturn in crude prices that is also hampering the Norwegian Krona relative to its Swedish counterpart after the manufacturing PMI reclaimed 50.0+ status and retail sales picked up pace. Indeed, Eur/Nok is hovering around 10.7500 in contrast to Eur/Sek testing 10.3100 vs highs of 10.7860 and 10.3515 respectively.

- EM - The Yuan is keeping its head above 7.0000 on the back of China’s Caixin manufacturing PMI exceeding forecast at 52.8 for the strongest print since January 2011 and the Rouble is consolidating off recent lows circa 74.0000 awaiting the latest CBR MPR, but the Rand is lagging near 17.3000 after a steep decline in SA tax receipts for the fy through end July.

In commodities, WTI and Brent front-month futures remain subdued in early European trade with little by way of fresh fundamental catalysts, but with that being said, OPEC+ are poised to ease the magnitude of the agreed-upon cuts this month which will see an additional 1.9mln BPD of supply entering the market – this was reflected by the Russian oil and gas condensate output for the first half of August. It is also worth bearing in mind that the extra supply comes against the backdrop of rising second-wave fears which have prompted some cities to re-enter lockdown, whilst others deferred their reopening plans. Elsewhere, spot gold remains uneventful after testing support at USD 1970/oz (vs. fresh high 1987.94), with the yellow metal decoupled from Dollar dynamics (for now) as prices remain near record highs. Spot silver sees similar lacklustre action sub 24.50/oz. Turning to base metals, Dalian iron ore futures rose in excess of 4% to hit 12-month highs on a firm demand outlook. Conversely, copper touched a three-week low despite the strong Chinese factory data, with some citing second wave fears.

US Event Calendar

- 9:45am: Markit US Manufacturing PMI, est. 51.3, prior 51.3

- 10am: ISM Manufacturing, est. 53.5, prior 52.6

- 10am: Construction Spending MoM, est. 1.0%, prior -2.1%

- Wards Total Vehicle Sales, est. 14m, prior 13.1m

DB's Jim Reid concludes the overnight wrap

A happy August to you all. This morning’s EMR is brought to you by the powers of paracetamol and ibuprofen as I played my one and only game of cricket this season over the weekend. It was President’s Day and I’m the President of my club so I couldn’t really avoid coming out of semi-retirement for a game I played pretty much every summer weekend from around 1983 to 2011. Running, diving, throwing, bowling, eating a big tea all took a big toll out of me.

My performance certainly wasn’t as good as markets were in July, unless the dollar was my benchmark. Craig (who is still in a state of shock after Arsenal won the FA Cup final on Saturday) has already published July’s performance review this morning (link here) where the highlights were a bumper month for Silver and Gold and a poor month for the dollar. Silver (c.+35%) had its best month since December 1979 and the dollar the worse for a decade. US equities had a good month in spite of rising virus caseloads due to a strong earnings season relative to expectations, especially in tech towards the end of the month. YTD Silver, Gold and the NASDAQ have been the three best performers while at the bottom of the leaderboard Brent, WTI and European Banks are all down at least 30%.

In terms of how August is faring so far, it’s been a mixed start in Asia with the Nikkei (+1.95%) and Shanghai Comp (+1.08%) both posting decent gains, the Hang Seng (-0.95%) down and the Kospi and ASX little changed. Meanwhile, yields on 10yr USTs are up +1.3bps and futures on the S&P 500 are down -0.08%. In terms of data releases, China’s June Caixin manufacturing PMI came in at 52.8 (vs. 51.1 expected) which was the highest reading since Jan 2011 while Japan’s final manufacturing PMI reading was confirmed at 45.2 (vs. 42.6 in preliminary read). We also got Japan’s final annualized 1Q GDP print this morning, printing at -2.2% qoq (vs. -2.8% qoq expected).

In terms of weekend news, US Secretary of State Michael Pompeo has said that the White House will announce measures against “a broad array” of Chinese-owned software deemed to pose national-security risks. This follows President Trump saying on Friday that he intends to ban music-video app TikTok from the US. Meanwhile, on the fiscal stimulus negotiations in the US, there are reports that Democrats and Republicans continue to remain far apart on the plan to restore a $600-per-week jobless benefit that expired last week. Negotiations will continue today.

Looking at coronavirus numbers for the weekend, growth rates for new cases slowed in the US to an average of 1.13% per day (vs. average growth of 1.70% over last 5 weekends). The same was true for the most populous states like Texas, Florida, California and Arizona. The fatalities growth rate also slowed in Texas (1.35% vs. 1.89%) and Arizona (0.96% vs. 2.45%) but continues to remain high in Florida (1.75% vs. 1.34%) and California (1.13% vs. 0.73%). Meanwhile, the White House coronavirus task force head Deborah Birx said the pandemic is in a “new phase” as it spreads across U.S. rural and urban areas. In Asia, Australia’s Victoria state declared a state of disaster and has ordered Melbourne’s residents to stay home except for work, medical care, provisions or exercise. The city is now under curfew between 8 p.m. and 5 a.m and the new restrictions will be in force for six weeks. The state reported 671 new cases in the past 24 hours. Please see the regular case and fatalities table in the PDF for more. Finally, the latest on a possible vaccine is that the Serum Institute of India received approval for conducting phase two and three clinical trials of the Covid-19 vaccine candidate developed by the University of Oxford and AstraZeneca in the country.

Looking ahead to this week now, the release of PMIs from around the world (today and Wednesday mostly) will set the tone, before the July US jobs report on Friday rounds out the week. On the central bank front, we will hear the monetary policy decision from the Bank of England and Governor Bailey’s ensuing press conference on Thursday. The market also enters the second half of Q2 earnings season, which has already seen a record number of beats in the S&P 500.

Going through in more detail now, the majority of manufacturing PMIs are out on today, before services and composite PMIs come out on Wednesday for the most part. There’ll also be the ISM manufacturing index from the US (today). The key here will be to see how differentiated PMIs are given that some governments around the world are cautiously easing restrictions with others needing to tighten. For the countries where we already have a flash PMI reading, they generally showed that the recovery has more momentum in Europe than in the US. Many of the flash European levels were the strongest in at least two years, while both manufacturing and services PMIs in the US failed to meet expectations. As ever caution is required as these are diffusion indices which simply monitor whether activity is better or worse than the previous month. Remember that the US was never as shutdown as Europe so momentum was always likely to be more in the latter’s favour regardless of the recent rise in cases.

In terms of payrolls on Friday, markets are generally expecting a third straight month of gains, though likely at a slower rate than we saw in June. DB are looking for a further +900k gain in the headline, below consensus estimates at +1.578m. This follows last month’s blowout +4.8m increase. Our economists also see the unemployment rate falling to 10.5% from 11.1%, in line with the median estimate. This data will give some insight into how the renewed spread of the coronavirus through the US, especially in the South and West have affected the US economy. The rest of the key data can be found in the day by day week ahead guide at the end.

On the central bank front, one highlight will be the Bank of England meeting and Governor Bailey’s ensuing press conference on Thursday. While our DB economists are not expecting any change to the policy rate this meeting, there is a chance for a dovish surprise on the overall commentary and tone. Focus will be on the central bank’s economic projections, the ongoing review of the effective lower bound, and the path of QE. See their preview here .

Elsewhere in central banks, India and Brazil are also releasing their policy decisions on Wednesday and Thursday, respectively. The two countries have the highest confirmed coronavirus caseloads outside the US, and are expected to lower interest rates in light of the continued economic impact of the pandemic. Following the FOMC last week and the lifting of the blackout period, we will hear from the Fed's Bullard, Evans, Mester and Kaplan.

Earnings will continue to be in focus, with 133 companies reporting from the S&P 500 and a further 95 from the STOXX 600. Among the releases include HSBC, Heineken, Siemens, Berkshire Hathaway, and Ferrari today. Then tomorrow markets will hear from Bayer, Diageo, Fidelity, BP, Walt Disney and Activision Blizzard. Wednesday will see Deutsche Post, Allianz, Humana, Bayerische Motoren, Regeneron Pharmaceuticals, CVS Health, MetLife and Fiserv release earnings. Following that, Thursday includes Merck, AXA, Siemens, adidas, Bristol-Myers Squibb, Novo Nordisk, Becton Dickinson & Co, Zoetis, T-Mobile, Illumina. Finally on Friday, Standard Life Aberdeen, Norwegian Cruise Line, Royal Caribbean Cruises and Ventas. So another busy week.

To review last week now, global equity markets were bifurcated with US stocks outperforming after beating low earning expectations, particularly in tech. The S&P 500 rose +1.73% (+0.77% Friday) led primarily by the mega cap tech stocks which reported towards the end of last week. With Apple, Facebook, and Amazon in particular surprising on earnings, the tech-focused Nasdaq outperformed this week as the index rose +3.69% (+1.49% Friday). Over 60% of the S&P have now reported and the index has seen a record of just under 85% of companies beat EPS estimates. Remember that the issue with this earnings season was that analysts didn’t increase their estimates in June as macro surprises beat. This left a great set up for earnings versus expectations.

Risk assets in Europe did not fare as well with European equities down -2.98% (-0.89%) over the 5 days, pushing the index down -1.11% for July. It was the first monthly loss since March as cyclical sectors led the declines following more concerns on the economic outlook and small rises in cases across the continent.

Even as US equities rose, core sovereign bonds fell with US 10yr Treasury yields falling -6.1bps (-1.8bps Friday) to a record closing low of 0.528%. Similarly, UK 10yr gilts rose +1.6bps on Friday to be just off Thursday’s all-time closing lows to fall -4.0bps overall on the week to 0.10%. German bunds fell -7.6bps to -0.52%, while a souring risk appetite saw wider peripheral spreads to bunds in Italy (+9.2bps), Spain (+6.3bps), Portugal (+7.1bps) and Greece (+9.7bps). The dollar fell over -1.0% on the week for the second week in a row, and has not seen a weekly rise since mid-June when economic data and US cases started getting worse again. With yields and the greenback falling, gold continued its breakneck rally. The metal rose +3.88% (+0.98% Friday) to another all-time record of $1975.86/oz.

On Friday, we received Q2 GDP data from the majority of Europe. This came following Thursday’s data out of the US, Germany and China. We learned that Euro Area quarterly GDP fell by -12.1%, right in-line with estimates and the largest decline on record. France GDP shrank -13.8% (vs. -15.2% expected), with the construction sector seeming to be hit the hardest after falling about -24% in the second quarter. Italy similarly showed a slightly ‘better’ GDP print than expected, coming in at -12.4% (vs. -15.5%). Unlike France and Italy, Spain’s data came in under projections with the economy contracting -18.5% (vs. -16.6% expected). In other data, German retail sales fell -1.6% MoM, better than the expected -3.3% drop, but somewhat expected given the +12.7% rise last month. In the US, July MNI Chicago PMI surprised by rising into expansionary territory at 51.9 vs 36.6 last month and well above the 44.0 estimate. Finally, the preliminary July University of Michigan survey showed sentiment fall -0.7pts to 72.5, just below estimates of 72.9. The slight drop in sentiment was driven by a -2.7pt move lower in current conditions even in light of a slight rise in expectations.

International

United Airlines adds new flights to faraway destinations

The airline said that it has been working hard to "find hidden gem destinations."

Share this:

Since countries started opening up after the pandemic in 2021 and 2022, airlines have been seeing demand soar not just for major global cities and popular routes but also for farther-away destinations.

Numerous reports, including a recent TripAdvisor survey of trending destinations, showed that there has been a rise in U.S. traveler interest in Asian countries such as Japan, South Korea and Vietnam as well as growing tourism traction in off-the-beaten-path European countries such as Slovenia, Estonia and Montenegro.

Related: 'No more flying for you': Travel agency sounds alarm over risk of 'carbon passports'

As a result, airlines have been looking at their networks to include more faraway destinations as well as smaller cities that are growing increasingly popular with tourists and may not be served by their competitors.

Shutterstock

United brings back more routes, says it is committed to 'finding hidden gems'

This week, United Airlines (UAL) announced that it will be launching a new route from Newark Liberty International Airport (EWR) to Morocco's Marrakesh. While it is only the country's fourth-largest city, Marrakesh is a particularly popular place for tourists to seek out the sights and experiences that many associate with the country — colorful souks, gardens with ornate architecture and mosques from the Moorish period.

More Travel:

- A new travel term is taking over the internet (and reaching airlines and hotels)

- The 10 best airline stocks to buy now

- Airlines see a new kind of traveler at the front of the plane

"We have consistently been ahead of the curve in finding hidden gem destinations for our customers to explore and remain committed to providing the most unique slate of travel options for their adventures abroad," United's SVP of Global Network Planning Patrick Quayle, said in a press statement.

The new route will launch on Oct. 24 and take place three times a week on a Boeing 767-300ER (BA) plane that is equipped with 46 Polaris business class and 22 Premium Plus seats. The plane choice was a way to reach a luxury customer customer looking to start their holiday in Marrakesh in the plane.

Along with the new Morocco route, United is also launching a flight between Houston (IAH) and Colombia's Medellín on Oct. 27 as well as a route between Tokyo and Cebu in the Philippines on July 31 — the latter is known as a "fifth freedom" flight in which the airline flies to the larger hub from the mainland U.S. and then goes on to smaller Asian city popular with tourists after some travelers get off (and others get on) in Tokyo.

United's network expansion includes new 'fifth freedom' flight

In the fall of 2023, United became the first U.S. airline to fly to the Philippines with a new Manila-San Francisco flight. It has expanded its service to Asia from different U.S. cities earlier last year. Cebu has been on its radar amid growing tourist interest in the region known for marine parks, rainforests and Spanish-style architecture.

With the summer coming up, United also announced that it plans to run its current flights to Hong Kong, Seoul, and Portugal's Porto more frequently at different points of the week and reach four weekly flights between Los Angeles and Shanghai by August 29.

"This is your normal, exciting network planning team back in action," Quayle told travel website The Points Guy of the airline's plans for the new routes.

stocks pandemic south korea japan hong kong europeanInternational

Walmart launches clever answer to Target’s new membership program

The retail superstore is adding a new feature to its Walmart+ plan — and customers will be happy.

Share this:

It's just been a few days since Target (TGT) launched its new Target Circle 360 paid membership plan.

The plan offers free and fast shipping on many products to customers, initially for $49 a year and then $99 after the initial promotional signup period. It promises to be a success, since many Target customers are loyal to the brand and will go out of their way to shop at one instead of at its two larger peers, Walmart and Amazon.

Related: Walmart makes a major price cut that will delight customers

And stop us if this sounds familiar: Target will rely on its more than 2,000 stores to act as fulfillment hubs.

This model is a proven winner; Walmart also uses its more than 4,600 stores as fulfillment and shipping locations to get orders to customers as soon as possible.

Sometimes, this means shipping goods from the nearest warehouse. But if a desired product is in-store and closer to a customer, it reduces miles on the road and delivery time. It's a kind of logistical magic that makes any efficiency lover's (or retail nerd's) heart go pitter patter.

Walmart rolls out answer to Target's new membership tier

Walmart has certainly had more time than Target to develop and work out the kinks in Walmart+. It first launched the paid membership in 2020 during the height of the pandemic, when many shoppers sheltered at home but still required many staples they might ordinarily pick up at a Walmart, like cleaning supplies, personal-care products, pantry goods and, of course, toilet paper.

It also undercut Amazon (AMZN) Prime, which costs customers $139 a year for free and fast shipping (plus several other benefits including access to its streaming service, Amazon Prime Video).

Walmart+ costs $98 a year, which also gets you free and speedy delivery, plus access to a Paramount+ streaming subscription, fuel savings, and more.

If that's not enough to tempt you, however, Walmart+ just added a new benefit to its membership program, ostensibly to compete directly with something Target now has: ultrafast delivery.

Target Circle 360 particularly attracts customers with free same-day delivery for select orders over $35 and as little as one-hour delivery on select items. Target executes this through its Shipt subsidiary.

We've seen this lightning-fast delivery speed only in snippets from Amazon, the king of delivery efficiency. Who better to take on Target, though, than Walmart, which is using a similar store-as-fulfillment-center model?

"Walmart is stepping up to save our customers even more time with our latest delivery offering: Express On-Demand Early Morning Delivery," Walmart said in a statement, just a day after Target Circle 360 launched. "Starting at 6 a.m., earlier than ever before, customers can enjoy the convenience of On-Demand delivery."

Walmart (WMT) clearly sees consumers' desire for near-instant delivery, which obviously saves time and trips to the store. Rather than waiting a day for your order to show up, it might be on your doorstep when you wake up.

Consumers also tend to spend more money when they shop online, and they remain stickier as paying annual members. So, to a growing number of retail giants, almost instant gratification like this seems like something worth striving for.

Related: Veteran fund manager picks favorite stocks for 2024

stocks pandemic mexicoGovernment

President Biden Delivers The “Darkest, Most Un-American Speech Given By A President”

President Biden Delivers The "Darkest, Most Un-American Speech Given By A President"

Having successfully raged, ranted, lied, and yelled through…

Share this:

Having successfully raged, ranted, lied, and yelled through the State of The Union, President Biden can go back to his crypt now.

Whatever 'they' gave Biden, every American man, woman, and the other should be allowed to take it - though it seems the cocktail brings out 'dark Brandon'?

{kind=link}

Tl;dw: Biden's Speech tonight ...

-

Fund Ukraine.

-

Trump is threat to democracy and America itself.

-

Abortion is good.

-

American Economy is stronger than ever.

-

Inflation wasn't Biden's fault.

-

Illegals are Americans too.

-

Republicans are responsible for the border crisis.

-

Trump is bad.

-

Biden stands with trans-children.

-

J6 was the worst insurrection since the Civil War.

(h/t @TCDMS99)

Tucker Carlson's response sums it all up perfectly:

"that was possibly the darkest, most un-American speech given by an American president. It wasn't a speech, it was a rant..."

Carlson continued: "The true measure of a nation's greatness lies within its capacity to control borders, yet Bid refuses to do it."

"In a fair election, Joe Biden cannot win"

And concluded:

“There was not a meaningful word for the entire duration about the things that actually matter to people who live here.”

Victor Davis Hanson added some excellent color, but this was probably the best line on Biden:

"he doesn't care... he lives in an alternative reality."

— Tucker Carlson (@TuckerCarlson) March 8, 2024

* * *

Watch SOTU Live here...

* * *

Mises' Connor O'Keeffe, warns: "Be on the Lookout for These Lies in Biden's State of the Union Address."

On Thursday evening, President Joe Biden is set to give his third State of the Union address. The political press has been buzzing with speculation over what the president will say. That speculation, however, is focused more on how Biden will perform, and which issues he will prioritize. Much of the speech is expected to be familiar.

The story Biden will tell about what he has done as president and where the country finds itself as a result will be the same dishonest story he's been telling since at least the summer.

He'll cite government statistics to say the economy is growing, unemployment is low, and inflation is down.

Something that has been frustrating Biden, his team, and his allies in the media is that the American people do not feel as economically well off as the official data says they are. Despite what the White House and establishment-friendly journalists say, the problem lies with the data, not the American people's ability to perceive their own well-being.

As I wrote back in January, the reason for the discrepancy is the lack of distinction made between private economic activity and government spending in the most frequently cited economic indicators. There is an important difference between the two:

-

Government, unlike any other entity in the economy, can simply take money and resources from others to spend on things and hire people. Whether or not the spending brings people value is irrelevant

-

It's the private sector that's responsible for producing goods and services that actually meet people's needs and wants. So, the private components of the economy have the most significant effect on people's economic well-being.

Recently, government spending and hiring has accounted for a larger than normal share of both economic activity and employment. This means the government is propping up these traditional measures, making the economy appear better than it actually is. Also, many of the jobs Biden and his allies take credit for creating will quickly go away once it becomes clear that consumers don't actually want whatever the government encouraged these companies to produce.

On top of all that, the administration is dealing with the consequences of their chosen inflation rhetoric.

Since its peak in the summer of 2022, the president's team has talked about inflation "coming back down," which can easily give the impression that it's prices that will eventually come back down.

But that's not what that phrase means. It would be more honest to say that price increases are slowing down.

Americans are finally waking up to the fact that the cost of living will not return to prepandemic levels, and they're not happy about it.

The president has made some clumsy attempts at damage control, such as a Super Bowl Sunday video attacking food companies for "shrinkflation"—selling smaller portions at the same price instead of simply raising prices.

In his speech Thursday, Biden is expected to play up his desire to crack down on the "corporate greed" he's blaming for high prices.

In the name of "bringing down costs for Americans," the administration wants to implement targeted price ceilings - something anyone who has taken even a single economics class could tell you does more harm than good. Biden would never place the blame for the dramatic price increases we've experienced during his term where it actually belongs—on all the government spending that he and President Donald Trump oversaw during the pandemic, funded by the creation of $6 trillion out of thin air - because that kind of spending is precisely what he hopes to kick back up in a second term.

If reelected, the president wants to "revive" parts of his so-called Build Back Better agenda, which he tried and failed to pass in his first year. That would bring a significant expansion of domestic spending. And Biden remains committed to the idea that Americans must be forced to continue funding the war in Ukraine. That's another topic Biden is expected to highlight in the State of the Union, likely accompanied by the lie that Ukraine spending is good for the American economy. It isn't.

It's not possible to predict all the ways President Biden will exaggerate, mislead, and outright lie in his speech on Thursday. But we can be sure of two things. The "state of the Union" is not as strong as Biden will say it is. And his policy ambitions risk making it much worse.

* * *

The American people will be tuning in on their smartphones, laptops, and televisions on Thursday evening to see if 'sloppy joe' 81-year-old President Joe Biden can coherently put together more than two sentences (even with a teleprompter) as he gives his third State of the Union in front of a divided Congress.

President Biden will speak on various topics to convince voters why he shouldn't be sent to a retirement home.

The state of our union under President Biden: three years of decline. pic.twitter.com/Da1KOIb3eR

— Speaker Mike Johnson (@SpeakerJohnson) March 7, 2024

According to CNN sources, here are some of the topics Biden will discuss tonight:

Economic issues: Biden and his team have been drafting a speech heavy on economic populism, aides said, with calls for higher taxes on corporations and the wealthy – an attempt to draw a sharp contrast with Republicans and their likely presidential nominee, Donald Trump.

Health care expenses: Biden will also push for lowering health care costs and discuss his efforts to go after drug manufacturers to lower the cost of prescription medications — all issues his advisers believe can help buoy what have been sagging economic approval ratings.

Israel's war with Hamas: Also looming large over Biden's primetime address is the ongoing Israel-Hamas war, which has consumed much of the president's time and attention over the past few months. The president's top national security advisers have been working around the clock to try to finalize a ceasefire-hostages release deal by Ramadan, the Muslim holy month that begins next week.

An argument for reelection: Aides view Thursday's speech as a critical opportunity for the president to tout his accomplishments in office and lay out his plans for another four years in the nation's top job. Even though viewership has declined over the years, the yearly speech reliably draws tens of millions of households.

Sources provided more color on Biden's SOTU address:

The speech is expected to be heavy on economic populism. The president will talk about raising taxes on corporations and the wealthy. He'll highlight efforts to cut costs for the American people, including pushing Congress to help make prescription drugs more affordable.

Biden will talk about the need to preserve democracy and freedom, a cornerstone of his re-election bid. That includes protecting and bolstering reproductive rights, an issue Democrats believe will energize voters in November. Biden is also expected to promote his unity agenda, a key feature of each of his addresses to Congress while in office.

Biden is also expected to give remarks on border security while the invasion of illegals has become one of the most heated topics among American voters. A majority of voters are frustrated with radical progressives in the White House facilitating the illegal migrant invasion.

It is probable that the president will attribute the failure of the Senate border bill to the Republicans, a claim many voters view as unfounded. This is because the White House has the option to issue an executive order to restore border security, yet opts not to do so

Maybe this is why?

Most Americans are still unaware that the census counts ALL people, including illegal immigrants, for deciding how many House seats each state gets!

— Elon Musk (@elonmusk) March 7, 2024

This results in Dem states getting roughly 20 more House seats, which is another strong incentive for them not to deport illegals.

While Biden addresses the nation, the Biden administration will be armed with a social media team to pump propaganda to at least 100 million Americans.

"The White House hosted about 70 creators, digital publishers, and influencers across three separate events" on Wednesday and Thursday, a White House official told CNN.

Not a very capable social media team...

The State of Confusion https://t.co/C31mHc5ABJ

— zerohedge (@zerohedge) March 7, 2024

The administration's move to ramp up social media operations comes as users on X are mostly free from government censorship with Elon Musk at the helm. This infuriates Democrats, who can no longer censor their political enemies on X.

Meanwhile, Democratic lawmakers tell Axios that the president's SOTU performance will be critical as he tries to dispel voter concerns about his elderly age. The address reached as many as 27 million people in 2023.

"We are all nervous," said one House Democrat, citing concerns about the president's "ability to speak without blowing things."

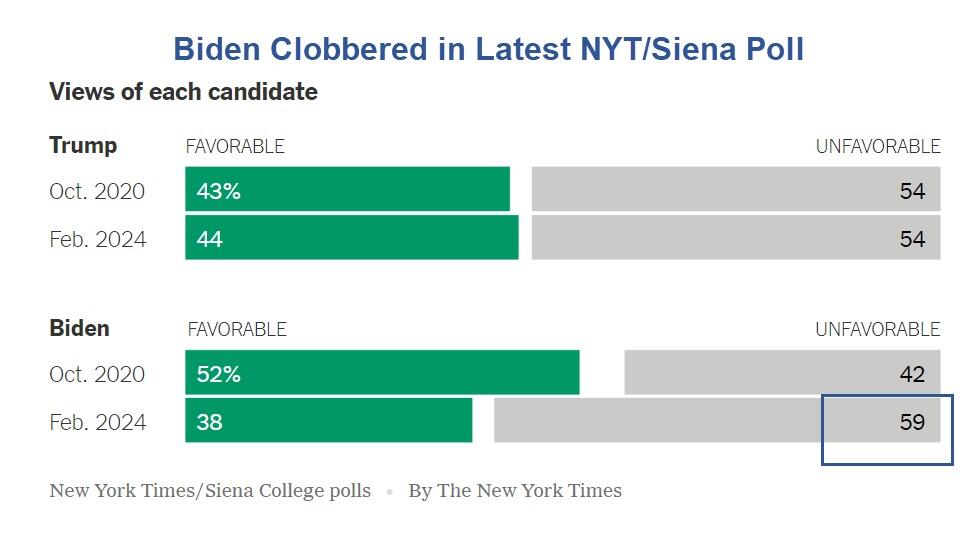

The SOTU address comes as Biden's polling data is in the dumps.

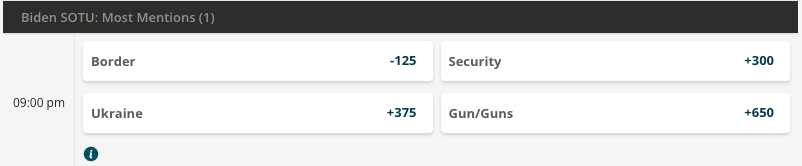

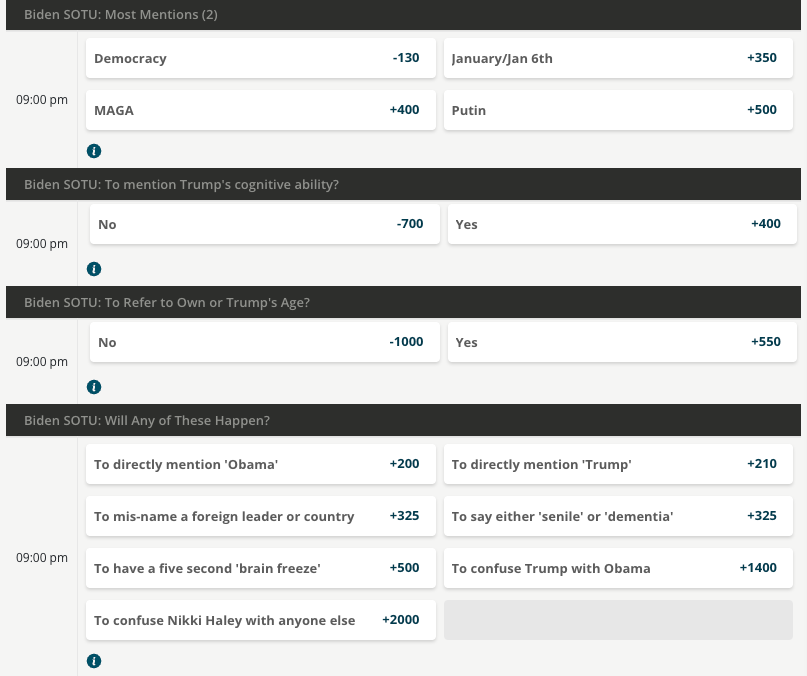

BetOnline has created several money-making opportunities for gamblers tonight, such as betting on what word Biden mentions the most.

As well as...

We will update you when Tucker Carlson's live feed of SOTU is published.

Fuck it. We’ll do it live! Thursday night, March 7, our live response to Joe Biden’s State of the Union speech. pic.twitter.com/V0UwOrgKvz

— Tucker Carlson (@TuckerCarlson) March 6, 2024

Walmart launches clever answer to Target’s new membership program

EyePoint poaches medical chief from Apellis; Sandoz CFO, longtime BioNTech exec to retire

Catastrophic Risk: Investing and Business Implications

Redefining Poverty: Towards a Transpartisan Approach

The Digest #187

Gather ’round the crystal ball: A multi-commodity outlook from PDAC 2024

Where Is R‑Star and the End of the Refi Boom: The Top 5 Posts of 2023

Deterra Royalties half-yearly result: stable performance and growth Initiatives

Deflationary pressures in China – be careful what you wish for

Revving up tourism: Formula One and other big events look set to drive growth in the hospitality industry

-

Uncategorized2 weeks ago

Uncategorized2 weeks agoAll Of The Elements Are In Place For An Economic Crisis Of Staggering Proportions

-

Uncategorized1 month ago

Uncategorized1 month agoCathie Wood sells a major tech stock (again)

-

Uncategorized3 weeks ago

Uncategorized3 weeks agoCalifornia Counties Could Be Forced To Pay $300 Million To Cover COVID-Era Program

-

Uncategorized2 weeks ago

Uncategorized2 weeks agoApparel Retailer Express Moving Toward Bankruptcy

-

Uncategorized3 weeks ago

Uncategorized3 weeks agoIndustrial Production Decreased 0.1% in January

-

International5 hours ago

Walmart launches clever answer to Target’s new membership program

-

International1 month ago

International1 month agoWar Delirium

-

Uncategorized3 weeks ago

Uncategorized3 weeks agoRFK Jr: The Wuhan Cover-Up & The Rise Of The Biowarfare-Industrial Complex