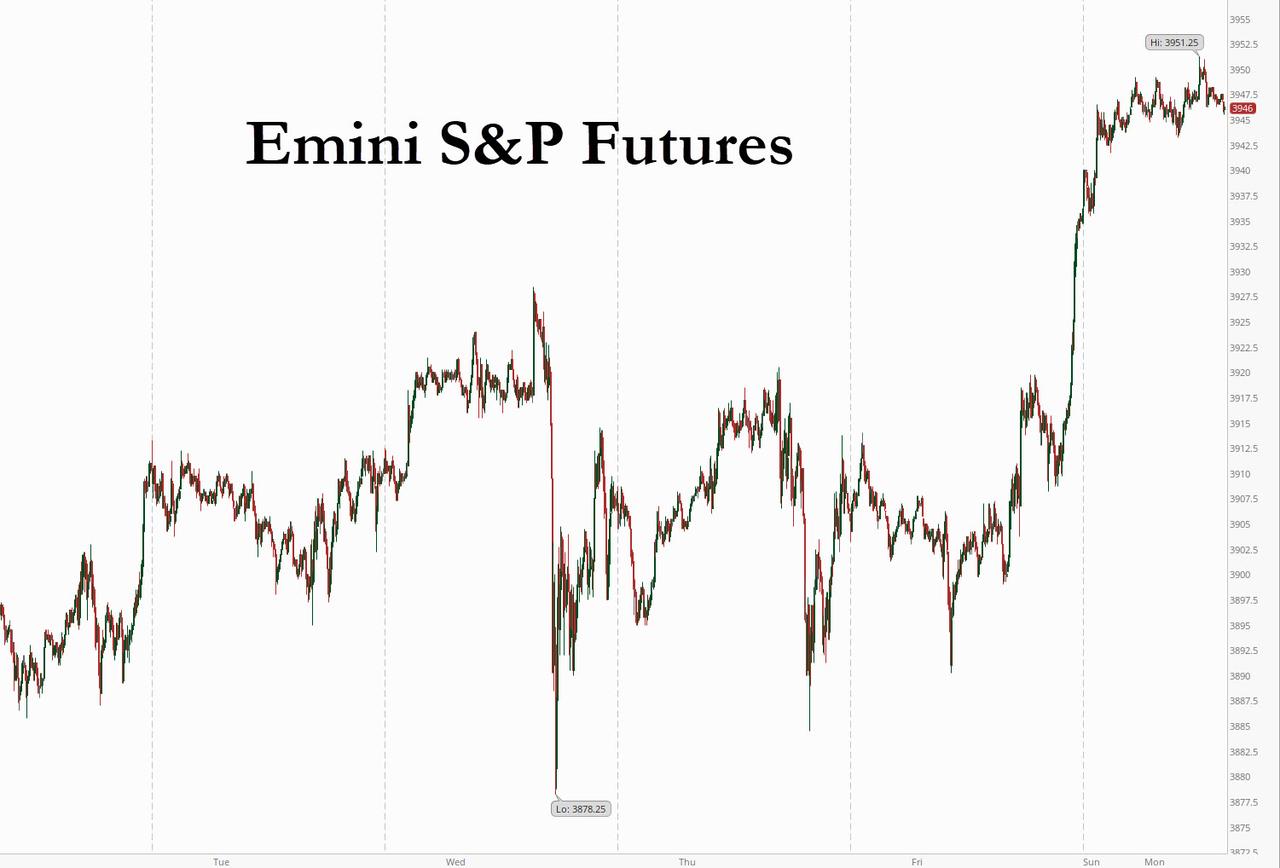

S&P Futures Hit Record High, WTI for Oil Soars Past $60

US cash markets may be closed for holiday (as is China and Hong Kong) but futures are up and running

Share this:

US cash markets may be closed for holiday (as is China and Hong Kong) but futures are up and running, and we mean up with EMinis bursting out of the gate late on Sunday and surging as high as 3,951, up 0.4%, to a new all time high, buoyed by vaccine rollout optimism, while energy names soared on a brutal polar vortex roiling energy markets across much of the US.

Global equities are on course to rise for 11 straight sessions -- the longest stretch since 2009 -- and the Treasury yield curve has tested the steepest levels in more than five years. Investors are betting on U.S. government spending and vaccines to drive the economy out of the pandemic.

“The reflation trade is set to continue to gather steam with vaccine deployment and massive fiscal spending by the Biden administration,” said Esty Dwek, head of global market strategy for Natixis Investment Managers Solutions. “Yields are likely to rise further and the catch-up of cyclical sectors should continue.”

Optimism was boosted after President Biden pushed for the first major legislative achievement of his term on Friday, turning to a bipartisan group of local officials for help on his $1.9 trillion coronavirus relief plan. “The long-awaited $1.9 trillion package has not been passed. As the latest U.S. job data hints at struggling labour market the relief package cannot come soon enough for some,” said Tamas Varga, oil analyst at London brokerage PVM Oil Associates. “The stimulus will likely be approved in some shape or form”, he added. Nasdaq futures underperformed with the reflation trade remains alive and well.

On Friday, VIX ended at its lowest level for nearly a year, dropping below 20 and helping drive a 0.4% gain for MSCI’s broadest measure of world stocks on Monday.

In Europe - which is not closed for holiday - the Stoxx 600 rose 1.1% as of 12:00 p.m. in London to a session high, led by media, basic resources and energy sectors amid optimism over the vaccine rollout and as freezing temperatures in Texas boost oil producers. Amid the reflationary thrust, media was the top-performing industry group +3.3%, followed by basic resources +3.1%; energy +2.9%, and banks +2.8%. All industry groups in the regional benchmark are in the green, with autos and health care the main laggards. FTSE 100 and IBEX outperform with gains of over 1.5%.

Asian stocks climbed to new heights in subdued trading with a number of key markets including China shut for holidays. Japanese stocks were strong, with the blue-chip Nikkei 225 closing above 30,000 for the first time since 1990 as the gauge continued its charge back up through levels not seen since the collapse of the bubble economy.

Information technology and financial stocks were the biggest boosts to the MSCI Asia Pacific Index, which reached another record. Samsung Electronics and SoftBank Group were the biggest individual contributors to the regional benchmark’s gains. South Korea’s Kospi led advances among key national indexes. Markets in China, Hong Kong, Taiwan and Vietnam, as well as the U.S., are closed for holidays on Monday.

In rates, cash Treasuries are closed for a local holiday and while Tsy futures trade a narrow range around Asia’s lows, inferring where the 30Y will trade means we are on the verge of 2.10% in the long bond.

Bloomberg notes that overnight, alarge Treasury options blocks printed, pointing to an unwind of bearish positions for April expiry. Over in Europe, yield curves bear steepen. Gilts underperform, trading ~3bps cheaper to bunds at the long end. Peripheral and semi-core spreads tighten with Italy narrower by ~2.5bps to core at the long end.

In FX, the Bloomberg dollar index briefly dipped below last week’s worst levels, while the NOK leads in G-10. Cable trades +0.4% breaching 1.39 to the upside. JPY lags with USD/JPY gains capped near 105.40 so far. TRY rises as much as 1% with USD/TRY back below 7.0. Crude futures drift off best levels. WTI remains ~2% higher, stalling just shy of a $61-handle during Asian trade.

In commodities, oil prices soared on Monday to their highest in about 13 months as vaccine rollouts promised to revive demand and producers kept supply reined in. Brent crude was up 92 cents, or 1.5%, at $63.35 a barrel, after climbing to a session high of $63.76, the highest since Jan. 22, 2020. WTI crude futures gained $1.20, or 2%, to $60.67 a barrel. It touched $60.95 - its highest since Jan. 8 last year, earlier in the session. Oil prices gained around 5% last week.

Prices have rallied more than 50% since the start of November as supplies tighten, due largely to production cuts from OPEC+. Russian Deputy Prime Minister Alexander Novak said the global oil market is on a recovery path and the oil price this year could average $45-$60 per barrel. “We’ve seen low volatility in the past few months. This means the market is balanced and the prices we are seeing today are in line with the market situation,” Novak was quoted as saying.

Meanwhile, an Arctic blast in the U.S. threatened to disrupt energy supplies, helping push crude oil to a 13-month high. Texas began rolling power blackouts for millions of households for the first time in a decade and traders estimate a few hundred thousand barrels a day of output in the state may be impacted by well shutdowns, traffic jams and power outages.

And in a move which could further tighten supply, workers will decide on Monday whether to strike this week at Norway’s largest oil loading terminal, action that could disrupt production at fields responsible for a third of the country’s crude output

Elsewhere, base metals trade well given better risk appetite, LME tin and lead gain over 0.5%. Platinum rallies 2.25% to outperform precious metals, rising above $1,300 for the first time since 2014.

Bitcoin, meanwhile, recovered some of its overnight weakness to trade down 1.4% at $47,984.96, below a record high of $49,714.66 hit just a few hours earlier. The cryptocurrency is benefiting from a wider embrace across the financial services industry, and over the weekend Bloomberg reported that a Morgan Stanley investing arm is considering adding Bitcoin to its list of possible bets.

Looking at the week ahead, all eyes will be on the release of minutes from the Fed's January meeting, where policymakers decided to leave rates unchanged, for hints to the likely direction of monetary policy. Those concerned about the impact of market exuberance on the outlook for inflation will also have fresh data to parse, with Britain, Canada and Japan all due to report. Friday will also see major economies, including the United States, release preliminary February purchasing managers’ indexes

A quick snapshot of global markets courtesy of Newsquawk

Asia-Pac equity markets began the week positively with sentiment underpinned as US equity futures extended to fresh record levels and amid improvements to the global COVID-19 situation on both sides of the Atlantic after the UK reached the 15mln vaccination milestone and with the 7-day average new infection cases in US recently declining to below 100k for the first time in more than 3 months. ASX 200 (+0.9%) traded higher with upside led by commodity names after WTI crude futures extended to above USD 60/bbl and with LME copper prices at their highest level since 2012. Furthermore, earnings results were a driving force among today’s biggest gainers and M&A news added to the constructive mood after Coca-Cola European Partners upped its offer for Coca-Cola Amatil and with Entain said to have offered AUD 3bln for Tabcorp’s wagering business. Nikkei 225 (+1.9%) climbed above the 30k milestone for the first time since August 1990 with the index buoyed by several bullish factors including a weaker currency and better than expected Q4 GDP data, while Japan also approved the Pfizer COVID-19 vaccine which is the first to be approved domestically and paves the way for vaccinations of medical workers this week. KOSPI (+1.4%) was lifted after South Korea eased COVID-19 restrictions which allows the reopening of nightclubs and karaoke bars from a 3-month closure, and with early February trade figures showing a surge in Exports and Imports which rose 69.1% and 71.9%, respectively, during the first 10 days of the month. As a reminder, US, Canada, China, Hong Kong, Taiwan and Vietnam are all closed for holiday on Monday. Finally, 10yr JGBs declined amid the rally in stocks and continued retreat in T-note futures which extended on Friday’s downturn, although the losses for Japan’s 10yr benchmark were cushioned by support near 151.50, better than expected GDP data and with the BoJ present in the market today for over JPY 1.2tln of JGBs mostly concentrated in 1yr-10yr maturities.

* * *

European equities kicked the week off modestly firmer across the board before extending on gains (Euro Stoxx 50 +0.9%), following on from the positive beginning to the APAC week (barring mass closures) which was underpinned as US equity futures reached fresh record levels. However, US cash players are away today in observations of US President’s Day (full desk schedule available on the Newsquawk headline feed), whilst China takes most of the week off due to the Spring Festival. Back to Europe, the DAX (+0.4%), CAC (+0.5%) and FTSE (+0.8%) all trade on a firmer footing as sentiment continues to be underpinned by stimulus hopes whilst mass vaccinations make further progress – with the UK benchmark cheering news that Britain has reached its target of inoculating around 15mln of its most vulnerable citizens against COVID-19, whilst also seeing tailwinds from higher crude prices and yields, alongside the housing sector providing support, as Barratt Developments (+1.6%), Taylor Wimpey (+2.2%), Redrow (+2.4%) and Rightmove (+1.8%) all trade firmer following reports that the UK is mulling an extension to the stamp duty holiday by six weeks to avoid buyers being stuck in a completion trap. Sectors in Europe are predominantly in the green – with the outperformers among those indicating a reflationary bias. The defensive Healthcare sector resides as the only negative mover and Consumer Staples and Utilities post only mild gains. The Media sector is the top gainer and is bolstered by Vivendi shares (+18.7%) amid news the Co. is mulling over the IPO of UMG by the end of the year. ING (+5.2%), Barclays (+5%), Investec (+4%) and ABN AMRO (+3.7%) all see gains amid higher yields, translating to strong banking sector performance. On the flip side, Travel & Leisure names are hit amid variant woes coupled with an update by Sanofi whereby it stated its EU-dependant mRNA vaccine will not be available in 2021, according to the CEO. As such Carnival (-3.7%), Tui (-3.5%), Air France (-2.3%) and Lufthansa (-2.2%) are all hit. In terms of individual movers, Lanxess (+4%) is firmer after the Co. signed a contract to acquire Emerland Kalama Chemical for USD 1.1bln to increase their presence in North America.

In FX, cable is cresting 1.3900 and Eur/Gbp is back below 0.8750 partly due to another downturn in the Dollar and relative Euro lethargy between key technical levels. However, Sterling is also bid in its own right and benefiting from the UK’s ongoing advanced progress in terms of vaccinating the population against COVID-19 that is keeping the PM on track to begin relaxing restrictions early next month. For the record, over 15 mn people have now been inoculated and the Government is aiming to have administered first jabs to 32 mn by April.

- NZD/NOK/AUD - The next best G10 currencies, as the Kiwi also takes advantage of its US counterpart’s failure to sustain recovery momentum, and claws back some lost ground vs its Antipodean rival even though NZ has suffered another mini pandemic outbreak resulting in a 3 day lockdown in Auckland and the rest of the nation moving up to level 2 alert status. Nzd/Usd is back up near 0.7250 and Aud/Nzd has retreated through 1.0750 as the Aussie fades into 0.7800 ahead of RBA minutes on Tuesday that are bound to be dovish given the unexpected Aud 100 bn QE extension and guidance for no change in rates until 2024, at the earliest. Meanwhile, a double dose of good news for the Norwegian Crown as oil prices continue to soar and the trade surplus swelled almost 2-fold in January to push Eur/Nok towards 10.2000.

- CAD/EUR/CHF - Also firmer vs the Greenback as the DXY meanders between 90.465-266 having failed to sustain Friday’s recovery momentum beyond the 21 DMA or 90.500 on a closing basis, with the Loonie also getting a boost from crude to retest recent peaks circa 1.2660, albeit in extra thin US Presidents’ Day trade due to Canada observing Family Day. Elsewhere, the Euro has reverted to a 1.2100-50 range after Friday’s false downside break, and from a chart perspective eyeing 21 and 50 DMAs yet again (1.2102 and 1.2158 respectively today), while the Franc is hovering just shy of 0.8900 and 1.0800 vs the single currency in wake of Swiss sight deposit balances showing another rise at domestic banks that indicates more SNB intervention.

- JPY - In stark contrast to the Norwegian Krona, Japanese data in the form of Q4 GDP and the Nikkei’s ascent through 30k have undermined the Yen, with Usd/Jpy now closer to the 200 DMA (105.51) than 21 or 100 that were both within touching distance last Tuesday and Wednesday. Moreover, risk appetite should get another fillip from news that Pfizer vaccine has been approved for use and PM Suga stating his intention to start injecting medical workers from February 17.

In commodities, WTI and Brent front month futures were bolstered at the electronic open, with the US benchmark narrowly outpacing its Brent counterpart as an Artic weather outbreak across central US and as far as the Gulf of Mexico raises short-term supply and logistical woes– including Texas issuing a state of disaster declaration whilst Oklahoma declared a weather disaster emergency. The National Weather Service warned that “extreme impacts are likely”. According to the EIA, a large number of energy infrastructures reside around the most impacted areas - Texas produced just under 5mln BPD in Nov 2020 according to the agency. Some also cite the stimulus-induced inflation narrative and rising geopolitical tensions as potential support for the complex, with the latter after Saudi reportedly intercepted another missile, albeit these attacks have been frequent. Meanwhile, weekend commentary from Russian Energy Minister Novak could also provide some positive omens for prices as he stated that oil markets are now rebalanced. Eyes now turn to the rhetoric among OPEC+ members in reference to the oil output cut quota, with higher prices seen as a temptation for some countries to increase production and exports (or at least call for these increases), and thus potentially causing a rift among members. WTI and Brent have waned off best levels but the former holds onto its USD 60/bbl handle (vs low 59.60/oz; high USD 60.92/bbl) and Brent hovers just north of USD 63/bbl (vs. low 62.82/bbl; high USD 63.74/bbl). Elsewhere, spot gold and silver see divergence with no stand-out fundamental explanations. Spot silver could be supported by the softer Buck, meanwhile from a technical standpoint, spot gold looks set for a “death cross” as its 50 DMA (1857.90) lines up with its 200 DMA (1857.59), potentially hindering upside for the yellow metal. Platinum prices have extended their rally amid expectations that the economic recovery could bolster demand for the metal used in autos and potentially lead to a supply shortfall. Elsewhere, while China remains closed for Lunar New Year, LME copper closes in on USD 8,500/oz as the red metal tracks the broader gains across the market alongside the inflationary narrative.

DB's Jim Reid concludes the overnight wrap

I hope you had a good weekend. If you were in Europe and you can remember much colder days than Saturday then you have a good memory. After a year of lobbying I finally persuaded my wife to huddle up over the cold Valentine’s weekend and try “The Last Dance”, the Michael Jordon / Chicago Bulls basketball documentary. After three episodes she’s absolutely hooked. So we both can’t wait to get through another long day to watch another episode tonight.

Before that don't expect that exciting a start to the week with half term well upon us, Chinese New Year, and a US Presidents’ Day holiday today. It has been a pretty eventful year so far with riots on Capitol Hill, the Georgia election results and huge associated potential stimulus numbers, the taper debate (becalmed for now), various bubble debates, Bitcoin up nearly five-fold since October, the EC vaccine saga, virus mutations, and who can forget the remarkable Reddit story. However over the last week or two markets have calmed down and returned to the liquidity/risk on trade. I still think this will be a very strong year for the global economy as I think life will look very different in the summer (even with some restrictions still), with an abundance of pent up demand. However that will likely bring its own issues with bond yields vulnerable if we see summer inflation (even if only transitory) and if the US technology bubble bursts as the “old” economy becomes relatively more attractive again and as day traders/retail have less time to invest in these chosen stocks. Before we get there the upcoming stimulus cheques may find their way into equity markets so if there is a bubble it may inflate more first before any correction. So I reiterate that I don’t think this will be a low vol year so enjoy the quiet period ahead while you can.

As for this week, on the data front, we’ll have to wait until Friday for the main event with the flash PMIs being published then. To be fair it’s probably going to be much more relevant where the economy will be once re-openings start than now but in this latest lockdown bout, most economies have held up better than expected so it’ll be interesting to see if this continues. January did see a divergence between the major economies though, as while a number of composite PMIs were below 50, including the Euro Area, the UK and Japan, the US economy continued to show promising signs, with their composite PMI rising to its highest level (58.7) since March 2015. Speaking of the US, the coming week will also see an increasing amount of hard data releases for January, including retail sales, industrial production, PPI (all Wednesday), housing starts and building permits (both Thursday).

From central banks, the next big round of monetary policy decisions won’t come until mid-March now, but we will get a number of meeting minutes released over the coming week, including from the Federal Reserve (Wednesday), the ECB (Thursday) and the Reserve Bank of Australia. Otherwise, the policy decisions will come from emerging market economies, with Bank Indonesia expected by DB’s economists to cut their policy rate by 25bps on Thursday, and the Central Bank of Turkey also deciding policy that same day.

Earnings season is starting to wind down now, with around three-quarters of the S&P 500 having reported. However, the coming week will still see a further 54 in the index report, as well as 67 from the STOXX 600. In terms of the highlights, today we’ll hear from BHP, before tomorrow sees CVS Health and AIG report. Then on Wednesday we’ll hear from Rio Tinto and British American Tobacco, followed by reports on Thursday from Walmart, Nestle, Applied Materials, Airbus, Daimler, Barclays and Credit Suisse. Finally on Friday, releases include Hermes International, Deere & Company, Allianz and NatWest Group.

On the stimulus package, the Senate will begin to debate the House's proposals this week. According to our economists it is possible that the Senate could move quickly towards a floor vote without making many changes to the House package. However their base case is that it will take a few weeks as moderate Democrats pare back Biden’s $1.9tn package through amendments. Indeed the House Ways and Means Committee last week took some steps to pare back the number of people eligible for stimulus checks, which lowered the cost of that part of the bill by $60bn.

Asian markets have started the week on the front foot with the Nikkei (+1.78%), Kospi (+1.76%), India’s Nifty (+0.92%) and Asx (+0.91%) all posting gains. The Nikkei is trading above the 30,000 mark for the first time since 1990 and is being helped by Japan’s Q4 GDP beat as the country posted an annualized growth of 12.7% qoq (vs. 10.1% qoq expected). Futures on the S&P are also up +0.39% while the US dollar index is down -0.17%. Meanwhile, WTI and Brent crude oil prices are up to a new post pandemic high of $60.82 (+2.27%) and $63.58 (+1.84%) per barrel respectively as a cold blast across some of America’s largest shale oil regions has caused crude flowing wells to slow or halt completely. Bitcoin prices are trading down -4.36% as we type after the cryptocurrency reached an all time intraday high of $49,694 during the weekend.

In terms of latest on the virus, the UK PM Johnson confirmed that his government has met its target of immunising everyone who wanted a jab over the age of 70, along with people who live or work in nursing homes, health service workers and those who are most vulnerable to Covid-19. Meanwhile, Japan is set to begin vaccinations on Wednesday with medical personnel being the first ones to receive the shots.

Back to last week and risk assets performed strongly with investor sentiment supported by positive developments around US fiscal stimulus and hopes over the vaccine rollout. Markets also received further affirmations of support from central bank officials as Fed Chair Powell and ECB president Lagarde both made comments of monetary policy needing to remain accommodative for the foreseeable future given the scars of the pandemic on the global economy. The S&P 500 gained +1.23% on the week (+0.47% Friday) while the NASDAQ composite rose a slightly stronger +1.73% (+0.50% Friday) to new record highs.

The cyclical trade again outperformed as rates rose and yield curves steepened on the week. US Banks rose +2.52% while their European counterparts gained +2.65% to take their YTD gains to +10.24% and +8.01% respectively. Energy stocks similarly picked up as Brent crude increased +5.21% and WTI moved +4.61% higher with both oil measures reaching yet another pandemic high and now back to late-January 2020 levels. With risk assets rallying and sentiment improving, the VIX volatility index fell -0.9pts over the course of the week to 19.97 – the lowest closing level since January 21 2020, the day before the first Coronavirus case was found in the US.

The STOXX 600 ended the week +1.09% higher (+0.64% Friday) at its pandemic highs while Italian assets continued to rally as Mario Draghi was able to gain the backing of the various political parties in Italy and will lay out his policy plans later this week. By the week’s end, the FTSE MIB rose +1.42%, while elsewhere the FTSE 100 also outperformed (+1.55%) even with the continued rally in Sterling.

US Treasury yields climbed +4.5bps to 1.208%, their highest level since late-February last year and the very early days of the pandemic’s spread. The sharp rise in 10yr yields steepened the 2y10y yield curve +3.9bps to 109.5bps, the steepest the curve has been since April 2017. The rise in inflation expectations helped as 10-year US breakevens rose to a 6-year high of 2.23% and 5yr breakevens to 2.38% (+7bps on the week and to an 8 year high) after being at 0.175% back in March last year. 10Yr Bund yields rose as well, increasing +2.0bps to -0.43%, while 10yr Gilt yields rose +3.5bps to 0.52%. Elsewhere in fixed income, high yield spreads are now at their tightest levels since 2018 as US HY cash spreads were -11bps tighter to 347bps, while in Europe they tightened -3bps to 263bps.

In terms of data from Friday the UK’s Q4 GDP reading showed that the economy grew by +1.0% (vs +0.5% expected) in the last three months of 2020, while shrinking by -7.8% (vs -8.1% expected) YoY. The gain comes despite partial lockdowns during the quarter, but given the tighter restrictions during the current quarter it will likely be hard to repeat. The other major economic data point was the University of Michigan’s preliminary consumer sentiment index for February which showed that sentiment may be rolling over. Sentiment declined in February to 76.2 (vs. 80.9 expected) from 79.0 reading the month prior, the drop could be largely attributed to a deterioration in confidence among Republicans and also households with incomes lower than $75k. The drop was also more stark in expectations (-4.2pts) rather than current conditions (-0.5pts).

Government

Are Voters Recoiling Against Disorder?

Are Voters Recoiling Against Disorder?

Authored by Michael Barone via The Epoch Times (emphasis ours),

The headlines coming out of the Super…

Share this:

Authored by Michael Barone via The Epoch Times (emphasis ours),

The headlines coming out of the Super Tuesday primaries have got it right. Barring cataclysmic changes, Donald Trump and Joe Biden will be the Republican and Democratic nominees for president in 2024.

With Nikki Haley’s withdrawal, there will be no more significantly contested primaries or caucuses—the earliest both parties’ races have been over since something like the current primary-dominated system was put in place in 1972.

The primary results have spotlighted some of both nominees’ weaknesses.

Donald Trump lost high-income, high-educated constituencies, including the entire metro area—aka the Swamp. Many but by no means all Haley votes there were cast by Biden Democrats. Mr. Trump can’t afford to lose too many of the others in target states like Pennsylvania and Michigan.

Majorities and large minorities of voters in overwhelmingly Latino counties in Texas’s Rio Grande Valley and some in Houston voted against Joe Biden, and even more against Senate nominee Rep. Colin Allred (D-Texas).

Returns from Hispanic precincts in New Hampshire and Massachusetts show the same thing. Mr. Biden can’t afford to lose too many Latino votes in target states like Arizona and Georgia.

When Mr. Trump rode down that escalator in 2015, commentators assumed he’d repel Latinos. Instead, Latino voters nationally, and especially the closest eyewitnesses of Biden’s open-border policy, have been trending heavily Republican.

High-income liberal Democrats may sport lawn signs proclaiming, “In this house, we believe ... no human is illegal.” The logical consequence of that belief is an open border. But modest-income folks in border counties know that flows of illegal immigrants result in disorder, disease, and crime.

There is plenty of impatience with increased disorder in election returns below the presidential level. Consider Los Angeles County, America’s largest county, with nearly 10 million people, more people than 40 of the 50 states. It voted 71 percent for Mr. Biden in 2020.

Current returns show county District Attorney George Gascon winning only 21 percent of the vote in the nonpartisan primary. He’ll apparently face Republican Nathan Hochman, a critic of his liberal policies, in November.

Gascon, elected after the May 2020 death of counterfeit-passing suspect George Floyd in Minneapolis, is one of many county prosecutors supported by billionaire George Soros. His policies include not charging juveniles as adults, not seeking higher penalties for gang membership or use of firearms, and bringing fewer misdemeanor cases.

The predictable result has been increased car thefts, burglaries, and personal robberies. Some 120 assistant district attorneys have left the office, and there’s a backlog of 10,000 unprosecuted cases.

More than a dozen other Soros-backed and similarly liberal prosecutors have faced strong opposition or have left office.

St. Louis prosecutor Kim Gardner resigned last May amid lawsuits seeking her removal, Milwaukee’s John Chisholm retired in January, and Baltimore’s Marilyn Mosby was defeated in July 2022 and convicted of perjury in September 2023. Last November, Loudoun County, Virginia, voters (62 percent Biden) ousted liberal Buta Biberaj, who declined to prosecute a transgender student for assault, and in June 2022 voters in San Francisco (85 percent Biden) recalled famed radical Chesa Boudin.

Similarly, this Tuesday, voters in San Francisco passed ballot measures strengthening police powers and requiring treatment of drug-addicted welfare recipients.

In retrospect, it appears the Floyd video, appearing after three months of COVID-19 confinement, sparked a frenzied, even crazed reaction, especially among the highly educated and articulate. One fatal incident was seen as proof that America’s “systemic racism” was worse than ever and that police forces should be defunded and perhaps abolished.

2020 was “the year America went crazy,” I wrote in January 2021, a year in which police funding was actually cut by Democrats in New York, Los Angeles, San Francisco, Seattle, and Denver. A year in which young New York Times (NYT) staffers claimed they were endangered by the publication of Sen. Tom Cotton’s (R-Ark.) opinion article advocating calling in military forces if necessary to stop rioting, as had been done in Detroit in 1967 and Los Angeles in 1992. A craven NYT publisher even fired the editorial page editor for running the article.

Evidence of visible and tangible discontent with increasing violence and its consequences—barren and locked shelves in Manhattan chain drugstores, skyrocketing carjackings in Washington, D.C.—is as unmistakable in polls and election results as it is in daily life in large metropolitan areas. Maybe 2024 will turn out to be the year even liberal America stopped acting crazy.

Chaos and disorder work against incumbents, as they did in 1968 when Democrats saw their party’s popular vote fall from 61 percent to 43 percent.

Views expressed in this article are opinions of the author and do not necessarily reflect the views of The Epoch Times or ZeroHedge.

Government

Veterans Affairs Kept COVID-19 Vaccine Mandate In Place Without Evidence

Veterans Affairs Kept COVID-19 Vaccine Mandate In Place Without Evidence

Authored by Zachary Stieber via The Epoch Times (emphasis ours),

The…

Share this:

Authored by Zachary Stieber via The Epoch Times (emphasis ours),

The U.S. Department of Veterans Affairs (VA) reviewed no data when deciding in 2023 to keep its COVID-19 vaccine mandate in place.

VA Secretary Denis McDonough said on May 1, 2023, that the end of many other federal mandates “will not impact current policies at the Department of Veterans Affairs.”

He said the mandate was remaining for VA health care personnel “to ensure the safety of veterans and our colleagues.”

Mr. McDonough did not cite any studies or other data. A VA spokesperson declined to provide any data that was reviewed when deciding not to rescind the mandate. The Epoch Times submitted a Freedom of Information Act for “all documents outlining which data was relied upon when establishing the mandate when deciding to keep the mandate in place.”

The agency searched for such data and did not find any.

“The VA does not even attempt to justify its policies with science, because it can’t,” Leslie Manookian, president and founder of the Health Freedom Defense Fund, told The Epoch Times.

“The VA just trusts that the process and cost of challenging its unfounded policies is so onerous, most people are dissuaded from even trying,” she added.

The VA’s mandate remains in place to this day.

The VA’s website claims that vaccines “help protect you from getting severe illness” and “offer good protection against most COVID-19 variants,” pointing in part to observational data from the U.S. Centers for Disease Control and Prevention (CDC) that estimate the vaccines provide poor protection against symptomatic infection and transient shielding against hospitalization.

There have also been increasing concerns among outside scientists about confirmed side effects like heart inflammation—the VA hid a safety signal it detected for the inflammation—and possible side effects such as tinnitus, which shift the benefit-risk calculus.

President Joe Biden imposed a slate of COVID-19 vaccine mandates in 2021. The VA was the first federal agency to implement a mandate.

President Biden rescinded the mandates in May 2023, citing a drop in COVID-19 cases and hospitalizations. His administration maintains the choice to require vaccines was the right one and saved lives.

“Our administration’s vaccination requirements helped ensure the safety of workers in critical workforces including those in the healthcare and education sectors, protecting themselves and the populations they serve, and strengthening their ability to provide services without disruptions to operations,” the White House said.

Some experts said requiring vaccination meant many younger people were forced to get a vaccine despite the risks potentially outweighing the benefits, leaving fewer doses for older adults.

“By mandating the vaccines to younger people and those with natural immunity from having had COVID, older people in the U.S. and other countries did not have access to them, and many people might have died because of that,” Martin Kulldorff, a professor of medicine on leave from Harvard Medical School, told The Epoch Times previously.

The VA was one of just a handful of agencies to keep its mandate in place following the removal of many federal mandates.

“At this time, the vaccine requirement will remain in effect for VA health care personnel, including VA psychologists, pharmacists, social workers, nursing assistants, physical therapists, respiratory therapists, peer specialists, medical support assistants, engineers, housekeepers, and other clinical, administrative, and infrastructure support employees,” Mr. McDonough wrote to VA employees at the time.

“This also includes VA volunteers and contractors. Effectively, this means that any Veterans Health Administration (VHA) employee, volunteer, or contractor who works in VHA facilities, visits VHA facilities, or provides direct care to those we serve will still be subject to the vaccine requirement at this time,” he said. “We continue to monitor and discuss this requirement, and we will provide more information about the vaccination requirements for VA health care employees soon. As always, we will process requests for vaccination exceptions in accordance with applicable laws, regulations, and policies.”

The version of the shots cleared in the fall of 2022, and available through the fall of 2023, did not have any clinical trial data supporting them.

A new version was approved in the fall of 2023 because there were indications that the shots not only offered temporary protection but also that the level of protection was lower than what was observed during earlier stages of the pandemic.

Ms. Manookian, whose group has challenged several of the federal mandates, said that the mandate “illustrates the dangers of the administrative state and how these federal agencies have become a law unto themselves.”

Spread & Containment

The Coming Of The Police State In America

The Coming Of The Police State In America

Authored by Jeffrey Tucker via The Epoch Times,

The National Guard and the State Police are now…

Share this:

{kind=link}

{kind=link}

Authored by Jeffrey Tucker via The Epoch Times,

The National Guard and the State Police are now patrolling the New York City subway system in an attempt to do something about the explosion of crime. As part of this, there are bag checks and new surveillance of all passengers. No legislation, no debate, just an edict from the mayor.

{kind=link}

Many citizens who rely on this system for transportation might welcome this. It’s a city of strict gun control, and no one knows for sure if they have the right to defend themselves. Merchants have been harassed and even arrested for trying to stop looting and pillaging in their own shops.

The message has been sent: Only the police can do this job. Whether they do it or not is another matter.

Things on the subway system have gotten crazy. If you know it well, you can manage to travel safely, but visitors to the city who take the wrong train at the wrong time are taking grave risks.

In actual fact, it’s guaranteed that this will only end in confiscating knives and other things that people carry in order to protect themselves while leaving the actual criminals even more free to prey on citizens.

The law-abiding will suffer and the criminals will grow more numerous. It will not end well.

When you step back from the details, what we have is the dawning of a genuine police state in the United States. It only starts in New York City. Where is the Guard going to be deployed next? Anywhere is possible.

If the crime is bad enough, citizens will welcome it. It must have been this way in most times and places that when the police state arrives, the people cheer.

We will all have our own stories of how this came to be. Some might begin with the passage of the Patriot Act and the establishment of the Department of Homeland Security in 2001. Some will focus on gun control and the taking away of citizens’ rights to defend themselves.

My own version of events is closer in time. It began four years ago this month with lockdowns. That’s what shattered the capacity of civil society to function in the United States. Everything that has happened since follows like one domino tumbling after another.

It goes like this:

1) lockdown,

2) loss of moral compass and spreading of loneliness and nihilism,

3) rioting resulting from citizen frustration, 4) police absent because of ideological hectoring,

5) a rise in uncontrolled immigration/refugees,

6) an epidemic of ill health from substance abuse and otherwise,

7) businesses flee the city

8) cities fall into decay, and that results in

9) more surveillance and police state.

The 10th stage is the sacking of liberty and civilization itself.

It doesn’t fall out this way at every point in history, but this seems like a solid outline of what happened in this case. Four years is a very short period of time to see all of this unfold. But it is a fact that New York City was more-or-less civilized only four years ago. No one could have predicted that it would come to this so quickly.

But once the lockdowns happened, all bets were off. Here we had a policy that most directly trampled on all freedoms that we had taken for granted. Schools, businesses, and churches were slammed shut, with various levels of enforcement. The entire workforce was divided between essential and nonessential, and there was widespread confusion about who precisely was in charge of designating and enforcing this.

It felt like martial law at the time, as if all normal civilian law had been displaced by something else. That something had to do with public health, but there was clearly more going on, because suddenly our social media posts were censored and we were being asked to do things that made no sense, such as mask up for a virus that evaded mask protection and walk in only one direction in grocery aisles.

Vast amounts of the white-collar workforce stayed home—and their kids, too—until it became too much to bear. The city became a ghost town. Most U.S. cities were the same.

As the months of disaster rolled on, the captives were let out of their houses for the summer in order to protest racism but no other reason. As a way of excusing this, the same public health authorities said that racism was a virus as bad as COVID-19, so therefore it was permitted.

The protests had turned to riots in many cities, and the police were being defunded and discouraged to do anything about the problem. Citizens watched in horror as downtowns burned and drug-crazed freaks took over whole sections of cities. It was like every standard of decency had been zapped out of an entire swath of the population.

Meanwhile, large checks were arriving in people’s bank accounts, defying every normal economic expectation. How could people not be working and get their bank accounts more flush with cash than ever? There was a new law that didn’t even require that people pay rent. How weird was that? Even student loans didn’t need to be paid.

By the fall, recess from lockdown was over and everyone was told to go home again. But this time they had a job to do: They were supposed to vote. Not at the polling places, because going there would only spread germs, or so the media said. When the voting results finally came in, it was the absentee ballots that swung the election in favor of the opposition party that actually wanted more lockdowns and eventually pushed vaccine mandates on the whole population.

The new party in control took note of the large population movements out of cities and states that they controlled. This would have a large effect on voting patterns in the future. But they had a plan. They would open the borders to millions of people in the guise of caring for refugees. These new warm bodies would become voters in time and certainly count on the census when it came time to reapportion political power.

Meanwhile, the native population had begun to swim in ill health from substance abuse, widespread depression, and demoralization, plus vaccine injury. This increased dependency on the very institutions that had caused the problem in the first place: the medical/scientific establishment.

The rise of crime drove the small businesses out of the city. They had barely survived the lockdowns, but they certainly could not survive the crime epidemic. This undermined the tax base of the city and allowed the criminals to take further control.

The same cities became sanctuaries for the waves of migrants sacking the country, and partisan mayors actually used tax dollars to house these invaders in high-end hotels in the name of having compassion for the stranger. Citizens were pushed out to make way for rampaging migrant hordes, as incredible as this seems.

But with that, of course, crime rose ever further, inciting citizen anger and providing a pretext to bring in the police state in the form of the National Guard, now tasked with cracking down on crime in the transportation system.

What’s the next step? It’s probably already here: mass surveillance and censorship, plus ever-expanding police power. This will be accompanied by further population movements, as those with the means to do so flee the city and even the country and leave it for everyone else to suffer.

As I tell the story, all of this seems inevitable. It is not. It could have been stopped at any point. A wise and prudent political leadership could have admitted the error from the beginning and called on the country to rediscover freedom, decency, and the difference between right and wrong. But ego and pride stopped that from happening, and we are left with the consequences.

The government grows ever bigger and civil society ever less capable of managing itself in large urban centers. Disaster is unfolding in real time, mitigated only by a rising stock market and a financial system that has yet to fall apart completely.

Are we at the middle stages of total collapse, or at the point where the population and people in leadership positions wise up and decide to put an end to the downward slide? It’s hard to know. But this much we do know: There is a growing pocket of resistance out there that is fed up and refuses to sit by and watch this great country be sacked and taken over by everything it was set up to prevent.

Walmart launches clever answer to Target’s new membership program

Wendy’s has a new deal for daylight savings time haters

Veterans Affairs Kept COVID-19 Vaccine Mandate In Place Without Evidence

The Coming Of The Police State In America

When Military Rule Supplants Democracy

Mortgage rates fall as labor market normalizes

United Airlines adds new flights to faraway destinations

Shipping company files surprise Chapter 7 bankruptcy, liquidation

February Employment Situation

Wendy’s teases new $3 offer for upcoming holiday

-

Uncategorized2 weeks ago

Uncategorized2 weeks agoAll Of The Elements Are In Place For An Economic Crisis Of Staggering Proportions

-

Uncategorized1 month ago

Uncategorized1 month agoCathie Wood sells a major tech stock (again)

-

Uncategorized3 weeks ago

Uncategorized3 weeks agoCalifornia Counties Could Be Forced To Pay $300 Million To Cover COVID-Era Program

-

Uncategorized2 weeks ago

Uncategorized2 weeks agoApparel Retailer Express Moving Toward Bankruptcy

-

Uncategorized3 weeks ago

Uncategorized3 weeks agoIndustrial Production Decreased 0.1% in January

-

International2 days ago

Walmart launches clever answer to Target’s new membership program

-

International2 days ago

International2 days agoEyePoint poaches medical chief from Apellis; Sandoz CFO, longtime BioNTech exec to retire

-

Uncategorized3 weeks ago

Uncategorized3 weeks agoRFK Jr: The Wuhan Cover-Up & The Rise Of The Biowarfare-Industrial Complex