Government

S&P Futures, Global Stocks Slump As European Banks Crash To All-Time Low

S&P Futures, Global Stocks Slump As European Banks Crash To All-Time Low

Share this:

US equity futures and European stocks slumped as investor skepticism for a new American stimulus deal grew against a sharp uptick in global coronavirus cases. Both bonds and the dollar advanced amid the flight from risk. The Emini was down 0.5% last, set to retest Thursday's lows.

Costco Wholesale Corp fell 2.5% as the warehouse chain recorded high coronavirus-related costs for the second straight quarter, overshadowing its better-than-expected results. The FAAMG tech mega-caps headed lower after leading gains on Wall Street in the previous session. Nikola fell another 5.2% in premarket trading, with the stock heading for the worst weekly performance on record, already being down 44% in a rout fueled by the resignation of its founder and executive chairman.

Boeing Co inched higher after Europe’s chief aviation safety regulator said the planemaker’s grounded 737 MAX could receive regulatory approval to resume flying in November and enter service by the end of the year. United Airlines, Southwest Airlines and Alaska Air Group were little changed in premarket trading even as airline unions hoped further aid would be announced before the current program ends on Oct. 1. After weeks of stalemate in talks over a fifth coronavirus relief bill, a key lawmaker said on Thursday Democrats in the U.S. House of Representatives were working on a $2.2 trillion package that could be voted on next week. Failure to reach a deal by then would result in another round of mass furloughs.

As futures slid, the VIX spiked above 30 with amid fears it could surge even more toward the end of the quarter next week as well as the Nov. 3 presidential election.

Incidentally, overnight Goldman said investors are overestimating the risk of the U.S. election upending markets, while Republican lawmakers vowed that the presidential transition after November’s election will occur without disruption, in a rebuke to President Donald Trump’s refusal to commit to a peaceful transfer of power.

Investors remain glued to all the latest news from DC where Democrats proposed a new $2.4 trillion stimulus bill to try to break the deadlock with Republicans, but chances of getting it passed before the November election appear slim. The risk of a slowdown in the economic recovery has risen with the lack of another package, prompting Goldman and JPMorgan to cut their forecast for U.S. growth in the fourth quarter.

"The odds of Phase 4 stimulus are a close call,” wrote Aneta Markowska, chief economist at Jefferies LLC in New York. “While still possible, there is a high risk that it does not happen this year. Without it, we would expect the economy to hit a major speed bump in Q4."

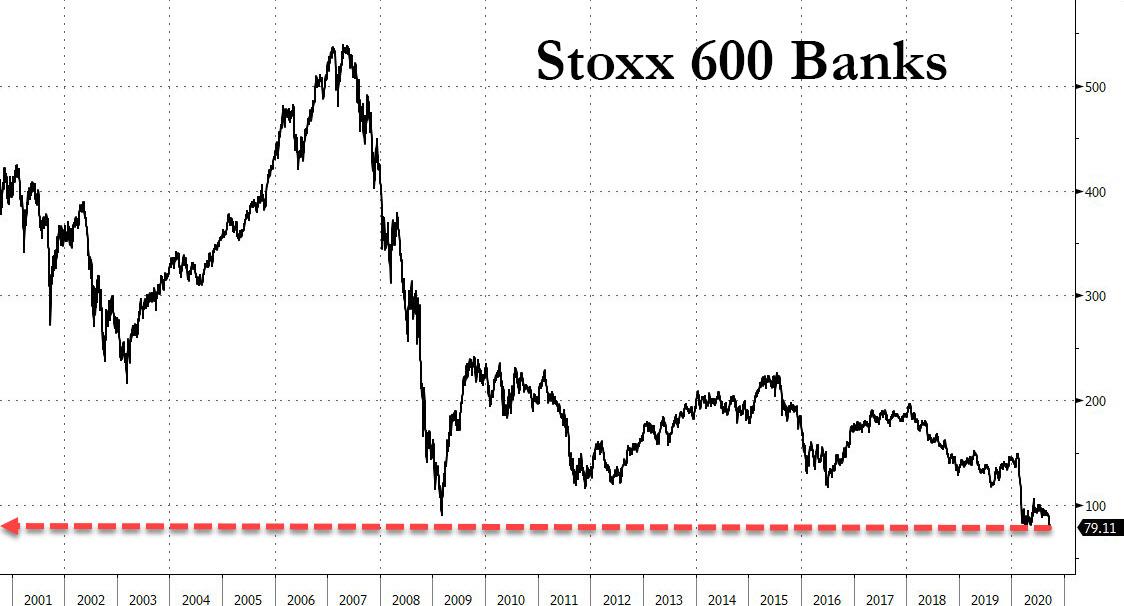

In Europe, the Stoxx 600 index tumbled 1% after fluctuating between gains and losses earlier, and was poised for its biggest weekly drop since June. Automotive and travel & leisure companies led the decline with losses of 2.1% and 1.6%, respectively. Airliners including Lufthansa AG, Ryanair Holdings Plc and IAG were among the biggest decliners as European leaders grappled with bringing infections back under control as hospitalizations climb again.

Also of note, the Stoxx Europe 600 Banks index dropped to an all time low as banks on the content continued to get punished.

Asian stocks were mixed, with materials and finance posting gains, after falling in the last session. The Jakarta Composite and India's S&P BSE Sensex Index rose, while Hong Kong's Hang Seng Index and Taiwan's Taiex Index fell. The Topix gained 0.5%, with Moresco and Niitaka rising the most. The Shanghai Composite Index retreated 0.1%, with New East New Materials and Tianjin Benefo Tejing Electric posting the biggest slides.

In rates, Treasuries gained as stocks slumped. Yields were down by up to 2bp across long-end of the curve, flattening 5s30s by almost 1bp; 10-year yields around 0.655% and richer by 1bp on the day, although underperforming bunds, gilts by 1bp and 1.5bp. German bonds edged higher along with most of the euro area, outperforming Treasuries.

In FX, the dollar recovered from early losses, and was set to conclude its best week since April. The Bloomberg Dollar Spot Index climbed 0.2%, after earlier falling as much as 0.2%, as the euro slipped in early London trading. Risk sensitive Group-of-10 currencies traded mixed against the dollar; the New Zealand dollar held an advance, trimming heavy losses over the week, while the Norwegian krone was the worst performer among peers, extending its slide versus the greenback to a seventh day, the longest since February 2019. The Swiss franc and the yen hovered. The Turkish Lira performed the best in EMFX, rallying sharply after the Turkish banking regulator eased trading restrictions for foreign investors.

In commodities, crude futures return to flat on the day near $40.25, failing twice to breach Wednesday’s highs. Spot gold holds a tight range, trading near $1,862/oz near its Asian lows. Base metals are mixed: LME nickel outperform, lead drops ~1%.

Market Snapshot

- S&P 500 futures up 0.5% to 3,225.25

- STOXX Europe 600 down 0.1% to 355.40

- MXAP up 0.5% to 168.48

- MXAPJ up 0.5% to 547.38

- Nikkei up 0.5% to 23,204.62

- Topix up 0.5% to 1,634.23

- Hang Seng Index down 0.3% to 23,235.42

- Shanghai Composite down 0.1% to 3,219.42

- Sensex up 1.8% to 37,193.57

- Australia S&P/ASX 200 up 1.5% to 5,964.92

- Kospi up 0.3% to 2,278.79

- Brent futures up 0.6% to $42.18/bbl

- Gold spot up 0.2% to $1,871.20

- U.S. Dollar Index little changed at 94.41

- German 10Y yield fell 1.6 bps to -0.517%

- Euro down 0.2% to $1.1655

- Italian 10Y yield rose 4.3 bps to 0.69%

- Spanish 10Y yield fell 1.4 bps to 0.237%

Top Overnight News from Bloomberg

- ECB policy maker Francois Villeroy Galhau signaled that he’s open to letting inflation rise above the institution’s goal and changing the language it has used for nearly two decades to set its objective

- EU negotiators have agreed not to allow their opposition to Boris Johnson’s plan to break international law distract them from trying to secure a deal over the bloc’s relationship with the U.K. after Brexit

- Germany’s federal government plans to sell a record of almost 419 billion euros ($489 billion) in bonds and bills in 2021, as it maintains a spending splurge designed to put the economy back on track

- European leaders are grappling with how to bring the coronavirus back under control as hospitalizations climb following a surge in cases to record levels in some countries

- Chinese sovereign bonds have won inclusion into FTSE Russell’s benchmark bond index a year after they were rejected

- Increasingly alarmed at the prospect of a White House without Donald Trump, Russia is trying to determine what that’ll mean for sensitive issues from nuclear arms to relations with China, energy exports, sanctions and far-flung global conflicts, according to people familiar with the efforts

A quick look at global markets courtesy of NewsSquawk

Asian equity markets were mostly higher amid tailwinds from Wall St where stocks finished a choppy session in the green as the tech sector rebounded, but with the gains in the US major indices only marginal amid mixed data which showed higher than expected jobless claimants. Nonetheless, the regional bourses were positive with ASX 200 (+1.5%) outperformance spurred by the largest weighted financials sector as the government seeks to repeal the responsible lending obligations legislation in an effort to spur more lending, while Nikkei 225 (+0.5%) was helped by a softer currency and after reports that Japan is mulling a corporate tax cut for SME’s to encourage M&A. Hang Seng (-0.3%) and Shanghai Comp. (-0.1%) swung between gains and losses despite the recent announcement by FTSE Russell to include China in the World Government Bond Index effective October 2021 and pending confirmation in March, which Morgan Stanley sees to likely spur inflows of as much as USD 90bln from September next year. However, the initial advances in Chinese markets were reversed amid ongoing uncertainty regarding the TikTok deal ahead of looming deadlines with the Trump administration given until 14:30EDT/19:30BST later today to notify the court whether it will postpone the ban set for midnight on Sunday, or file a motion of opposition to the preliminary injunction, which the court would then have to consider on Sunday. There were also jitters caused by China’s second largest developer Evergrande after it warned of a cash crunch that could result to systemic risks if its restructuring/listing plan doesn’t get government approval by January 31st, which saw its shares whipsaw and pressured bond prices to trigger a trading halt of its 5-year bonds in Shanghai due to abnormal fluctuations. Finally, 10yr JGBs were lower amid similar uninspired trade in T-notes with demand sapped by the gains in equities and the lack of BoJ’s presence in the market today.

Top Asian News

- Evergrande Faces Crisis of Confidence Over $120 Billion Debt

- Turkey Approaches France to Procure European Missile Defense

- Thai Parliament Stalls Charter Decision, Angering Protesters

- HNA Unit CWT Jumps as Trading Resumes After 17-Month Suspension

A tentative session thus far in Europe, major Euro-bourses drift lower in early hours (Euro Stoxx 50 -1.2%) with the overall picture in Europe now lower and bourses remain at session lows, following on from a mixed APAC handover. News-flow in early hours has been light with no real catalysts to spur or influence price action. Nonetheless, the FTSE 100 (-0.2%), AEX (-0.3%) and IBEX (-0.5%) are somewhat cushioned on the back of Consumer Staples, Utilities, and Telecoms– the only sectors in the green. Meanwhile, the DAX (-1.2%) and CAC (-1.1%) are pressured by losses in some large-cap cyclical names such as SAP (-1.8%) and Airbus (-2.3%) as the IT and Industrial sectors post losses. That being said, no real risk profile can be derived from either the broader sectors nor the breakdown, with the latter also seeing Travel & Leisure at the bottom of the pile on COVID-19 fears for the sector as UK and France reported a fresh record number of new cases and further Madrid lockdowns are announced. The sector also sees additional downside from the likes of easyJet (-2.5%) and Ryanair (-5.2%) after the Italian Antitrust regulators opened up a probe into the Cos, among other names, regarding the provision of vouchers and no refunds for consumers with flights cancelled owed to the pandemic. In terms of other movers and shakers, Bayer (-0.5%) shares were initially supported by reports that the Co. is continuing to resolve thousands of cases regarding its Roundup weedkiller, and therefore the prospects for the USD 11bln deal to end litigation is seen to be improving. Meanwhile, Suez (+4.6%) is among the top gainers in the Stoxx 600 after Veolia (+0.7%) CEO said the Co. will present a better offer to Engie (+0.3%) for its Suez stake. Finally, Lagardere (+31%) tops the charts as investor Bernard Arnault revealed he has built up a direct stake in the group.

Top European News

- Villeroy Says ECB Should Consider Tweaking Its Inflation Goal

- Veolia CEO Says He Will Raise Offer Price for Suez Stake

- Russia Weighs Euro Debt Sale by Year-End Despite Volatility

- Germany Plans Record Gross Borrowing in 2021 to Help Stem Crisis

In FX, it makes some sense that the Kiwi and Aussie are front-running major currency recovery gains vs the Greenback having been amongst the biggest losers when their US counterpart was in the ascendency and DXY reached its 94.601 peak. Nzd/Usd has bounced firmly from yesterday’s low not far from 0.6500 towards the round number above and Aud/Usd is back in the high 0.7000s after shaving the level by a similar margin on Thursday, with some impetus from CBA’s counter view on the RBA holding fire at October’s policy meeting after 2 forecasts for a 15 bp cut. Meanwhile, the US Dollar has regrouped from initial consolidation and resides at the top-end of a current 94.186-94.558 band. Such movement comes ahead of the notoriously erratic durable goods data and 2 scheduled speeches from Fed’s Williams, but still monitoring the broad risk tone for direction, particularly as US participants arrive, after further progress on the stopgap spending bill as the Senate approved the proposal overwhelmingly.

- GBP - The Pound continues to hold off worst levels with some hope that latest fiscal support will cushion the UK economy against further COVID-19 collateral damage. Cable is hovering just above 1.2700 after failing to sustain a 1.2800+ push, while Eur/Gbp has rebounded from a breach of 0.9150 amidst conflicting Brexit reports, as Britain’s chief negotiator Frost and EU peer Barnier are said to have laid foundations for formal negotiations next week. but some in the UK press suggest that Brussels is still not optimistic and indeed gloomy after latest informal talks.

- CHF/CAD/JPY/EUR - All narrowly mixed vs the Greenback in fairly subdued, aimless trade compared to the whippy sessions to date this week, as the Franc pivots 0.9260 (and 1.0800 against the Euro) following little fresh inspiration from the SNB, the Loonie straddles 1.3350 and Yen flirts with a key Fib retracement at 105.53 that looks more inclined to keep it compressed than more decent option expiry interest at the 105.00 strike (1.3 bn rolling off at Friday’s NY cut). Elsewhere, the Euro has regained some poise around the 1.1650 mark, but remains technically weak under 1.1700, a Fib and the 50 HMA at 1.1691 and 1.1670 respectively.

- SCANDI/EM - Some calm for the underperforming Swedish Krona, but the Norwegian Crown is struggling to stop the rot after the Norges Bank pushed back rate hike intentions in stark contrast to the CBRT that has backed up its monetary policy aggression with a 50 bp hike in swap rates, while increasing limits between local and foreign banks. Hence, Usd/Try has tested support into 7.5000 from record highs circa 7.7160 pre-2 full percent blanket tightening. Conversely, Usd/Mxn is hovering above 22.1500 after Banxico eased 25 bp and noted ample slack in the economy.

- Turkish Banking Watchdog says they have increased TRY swap limits of local banks with foreign entities. Additionally, CBRT increase TRY swap market rates to 10.25% vs. Prev. 9.75%. (Newswires)

In commodities, WTI and Brent front month futures are essentially unchanged at present, in what looks to be a continuation of APAC price action, but with complex-specific newsflow rather scarce; most recently, price action has deteriorated in-line with the broader market sentiment. In terms of where we stand, the demand side of the equation continues to be clouded by the COVID-19 resurgence in Europe and elsewhere, with eyes remaining on fuel demand as air travel falters. Meanwhile on the supply-side, eyes remain on any OPEC+ commentary in relation to the COVID-19 case rises alongside the situation in Libya and production ramp ups and exports are underway, with the country expected to output some 260k BPD by next week. OPEC earlier this week noted that the situation will be monitored for continuity, in which the OPEC member will then likely be issued am output quota as it is currently exempt. WTI resides around the 40.30/bbl mark (vs. low 40.13/bbl), while its Brent counterpart resides north of USD 42/bbl (vs. low 47.75/bbl). Precious metals meanwhile are uneventful and largely trade in tandem with a caged USD, with spot gold around the 1865/oz mark and spot silver just above USD 22/oz. In terms of base metals, LME copper gave up earlier gains in sympathy of downside seen in European stocks, whilst Dalian iron ore futures ended the day lower amid a lacklustre performance in China.

US Event Calendar

- 8:30am: Durable Goods Orders, est. 1.4%, prior 11.4%; Durables Ex Transportation, est. 1.0%, prior 2.6%

- 8:30am: Cap Goods Orders Nondef Ex Air, est. 0.95%, prior 1.9%; Cap Goods Ship Nondef Ex Air, est. 0.8%, prior 2.4%

Central Bank Speakers

- 9am: Fed’s Williams Talks With Community Development Leaders

- 12:15pm: Fed’s George to Speak about Community Banks

- 3:10pm: Fed’s Williams Discusses the Covid-19 Job Market

DB's Jim Reid concludes the overnight wrap

The NASDAQ rose +0.37% as tech (+0.62%) took a back seat to Utilities (+1.17%), Consumer Staples (+0.76%) and Materials (+0.70%) stocks. Europe lagged behind however as it caught up with the US slide the previous evening, with the FTSE 100 (-1.30%), the CAC 40 (-0.83%) and the DAX (-0.29%) all moving lower. The STOXX 600 was also down -1.02% and at a 3-month low, and there was a further widening in both sovereign bond and corporate credit spreads. For reference European Crossover widened +21bps and is now +63bps above its intra-day post pandemic tights seen on September 16th. The same numbers for US CDX HY were +3bp yesterday and +54 wider from the absolute tights. In sovereign bond markets, there was a selloff later in the European session, and by the close yields on 10yr bunds (+0.4bps), OATs (+1.8bps) and BTPs (+4.3bps) had all moved higher. US Treasuries made a modest advance, and 10yr yields fell -0.8bps, though there was another decline in inflation expectations, as 10yr breakevens fell -2.0bps to 1.584%, their lowest since early August. The dollar fell in the New York afternoon for the first time all week, after the dollar index had reached a 2-month high. It finished -0.04%.

As discussed above, the coronavirus pandemic dominated the agenda, and with it concerns that a spike in cases would hamper the economic recovery. Yesterday’s news didn’t give much cause for hope on that front, with Europe being a source of concern once again. Indeed, the ECDC released their latest risk assessment, which found that non-pharmaceutical interventions such as social distancing had not been sufficient when it came to reducing or controlling exposure to the virus, and the Commissioner for Health and Food Safety warned that “This might be our last chance to prevent a repeat of last spring.” The numbers didn’t offer much cause for optimism either. Italy, which has been protected from the second wave so far, reported 1,786 new cases (vs. 1,640 the previous day) and is slowly edging higher. Meanwhile Poland (1,136), France (16,096) and the UK (6,648) all recorded record one day rises in new cases albeit with a much higher level of testing than during the first wave. In the US weekly cases have risen to over 300,000 again after falling under that level back at the end of August. The country may be seeing the start of another round of infections. On the vaccine front, New York Governor Andrew Cuomo said he didn’t trust the Trump administration and that the state would review any vaccine authorised by the federal government. Meanwhile, President Trump said overnight that Americans in the Medicare program for the elderly and disabled will be sent $200 discount cards for prescription drugs within weeks. Trump didn’t explain in his speech what program or authority would allow the government to provide the cards which are likely to cost c. $6.6bn, according to Bloomberg.

When it came to policy support, there were some promising noises on a stimulus in the US yesterday, with Treasury Secretary Mnuchin saying that “If the Democrats are willing to sit down, I’m willing to sit down anytime for bipartisan legislation, let’s pass something quickly”. On the Democratic side, Speaker Pelosi also said that “We’ll be, hopefully soon, going to the table with them”. So the question will be whether the public willingness of both sides to talk to each other will translate into actual talks. It could be both sides are preparing to blame the other when talks don’t go anywhere.

It was also reported that the House Democrats were drafting a stimulus proposal of $2.4 trillion late yesterday, which is far more than Senate Republicans have said they are comfortable with, but is closer to the $1.5 trillion plan the President has shown support for. We will know far more on Monday, after the President names a Supreme Court nominee, about how serious the sides are on stimulus and if something can get done or whether the confirmation process becomes too distracting.

Here in the UK we did get some concrete fresh measures, as Chancellor Sunak announced a package to boost employment heading through the winter. The main policy was a new Job Support Scheme that will come into place at the start of November for 6 months once the furlough scheme finishes. This will see the government subsidise workers’ wages, so long as they’re working at least a third of their usual hours. For the hours not worked, both the government and the employer will each pay a third of the employee’s normal salary, subject to a cap on government contributions. This new scheme will run for 6 months, and is available to small and medium-sized businesses, as well as large ones that can demonstrate they’ve been adversely affected by the pandemic. In addition, the temporary VAT reduction for the hospitality sector has been extended to the end of March, and has also extended four temporary loan schemes for businesses.

Overnight in Asia, markets are mostly trading higher outside of the Hang Seng (-0.21%) and Shanghai Comp (-0.24%) which are both down. The Nikkei (+0.38%), Kospi (+0.64%), Asx (+1.18%) and Indian’s Nifty (+1.0%) are all up along with S&P 500 futures which are trading +0.44%. Futures in Europe are also pointing to a positive open with those on the Stoxx 50 +0.41%. In Fx, the onshore yuan is up +0.16% on expected inflows post the FTSE Russell saying overnight that it would include Chinese sovereign bonds in its flagship World Government Bond Index. The inclusion will start in October 2021.

Back to yesterday now, and investor sentiment wasn’t helped by the weak economic data that came through from the US. The weekly initial jobless claims for the week through September 19 were at an above-expected 870k (vs. 840k expected) and the previous week’s number was also revised up +6k. For context, it’s worth remembering that although the 870k reading is well below the peak of 6.867m back in late March, that’s still higher than the pre-Covid record of 695k back in 1982, and exceeds even the worst week of the financial crisis, raising concerns that labour market progress is stalling in the US.

The poor data was the backdrop for a third straight day of Fed Chair Powell testifying before Congress, this time in front of the Senate Banking Committee. The Main Street lending vehicle again came up with Chair Powell indicating that by the end of the year the facility could grow from less than $2 billion now to as much as $10-30 billion in outstanding loans to mid-size companies. When pressed by Republican Senators on the unused funds in some Fed facilities, the Chair indicated the government’s Paycheck Protection Program and additional unemployment benefits would have greater impact. In fact the Chair indicated, like many of his colleagues in the previous 24 hours, that the lack of additional fiscal aid was a ”downside risk” to the economy. But as we indicated above, discussions have yet to restart and there are ample distractions.

Wrapping up with yesterday’s other data now, and the US reported better-than-expected new home sales in August, which rose to an annualised rate of 1.011m (vs. 890k expected). Meanwhile in Germany, the Ifo’s business climate index rose to 93.4 (vs. 93.8 expected). Though this was the 5th consecutive monthly increase, it was also the smallest monthly gain in the reading seen since the trough in April. That said, the expectations reading was at a stronger 97.7, which was the highest since November 2018.

To the day ahead now, and the data highlights include the UK public finances for August, Euro Area M3 money supply for August, and Italy’s consumer confidence index for September. Meanwhile in the US, we’ll get the preliminary readings for August’s durable goods orders and nondefence capital goods orders ex air. From central banks, we’ll hear from the Fed’s Williams, and the ECB’s Villeroy and Hernandez de Cos.

Government

Are Voters Recoiling Against Disorder?

Are Voters Recoiling Against Disorder?

Authored by Michael Barone via The Epoch Times (emphasis ours),

The headlines coming out of the Super…

Share this:

Authored by Michael Barone via The Epoch Times (emphasis ours),

The headlines coming out of the Super Tuesday primaries have got it right. Barring cataclysmic changes, Donald Trump and Joe Biden will be the Republican and Democratic nominees for president in 2024.

With Nikki Haley’s withdrawal, there will be no more significantly contested primaries or caucuses—the earliest both parties’ races have been over since something like the current primary-dominated system was put in place in 1972.

The primary results have spotlighted some of both nominees’ weaknesses.

Donald Trump lost high-income, high-educated constituencies, including the entire metro area—aka the Swamp. Many but by no means all Haley votes there were cast by Biden Democrats. Mr. Trump can’t afford to lose too many of the others in target states like Pennsylvania and Michigan.

Majorities and large minorities of voters in overwhelmingly Latino counties in Texas’s Rio Grande Valley and some in Houston voted against Joe Biden, and even more against Senate nominee Rep. Colin Allred (D-Texas).

Returns from Hispanic precincts in New Hampshire and Massachusetts show the same thing. Mr. Biden can’t afford to lose too many Latino votes in target states like Arizona and Georgia.

When Mr. Trump rode down that escalator in 2015, commentators assumed he’d repel Latinos. Instead, Latino voters nationally, and especially the closest eyewitnesses of Biden’s open-border policy, have been trending heavily Republican.

High-income liberal Democrats may sport lawn signs proclaiming, “In this house, we believe ... no human is illegal.” The logical consequence of that belief is an open border. But modest-income folks in border counties know that flows of illegal immigrants result in disorder, disease, and crime.

There is plenty of impatience with increased disorder in election returns below the presidential level. Consider Los Angeles County, America’s largest county, with nearly 10 million people, more people than 40 of the 50 states. It voted 71 percent for Mr. Biden in 2020.

Current returns show county District Attorney George Gascon winning only 21 percent of the vote in the nonpartisan primary. He’ll apparently face Republican Nathan Hochman, a critic of his liberal policies, in November.

Gascon, elected after the May 2020 death of counterfeit-passing suspect George Floyd in Minneapolis, is one of many county prosecutors supported by billionaire George Soros. His policies include not charging juveniles as adults, not seeking higher penalties for gang membership or use of firearms, and bringing fewer misdemeanor cases.

The predictable result has been increased car thefts, burglaries, and personal robberies. Some 120 assistant district attorneys have left the office, and there’s a backlog of 10,000 unprosecuted cases.

More than a dozen other Soros-backed and similarly liberal prosecutors have faced strong opposition or have left office.

St. Louis prosecutor Kim Gardner resigned last May amid lawsuits seeking her removal, Milwaukee’s John Chisholm retired in January, and Baltimore’s Marilyn Mosby was defeated in July 2022 and convicted of perjury in September 2023. Last November, Loudoun County, Virginia, voters (62 percent Biden) ousted liberal Buta Biberaj, who declined to prosecute a transgender student for assault, and in June 2022 voters in San Francisco (85 percent Biden) recalled famed radical Chesa Boudin.

Similarly, this Tuesday, voters in San Francisco passed ballot measures strengthening police powers and requiring treatment of drug-addicted welfare recipients.

In retrospect, it appears the Floyd video, appearing after three months of COVID-19 confinement, sparked a frenzied, even crazed reaction, especially among the highly educated and articulate. One fatal incident was seen as proof that America’s “systemic racism” was worse than ever and that police forces should be defunded and perhaps abolished.

2020 was “the year America went crazy,” I wrote in January 2021, a year in which police funding was actually cut by Democrats in New York, Los Angeles, San Francisco, Seattle, and Denver. A year in which young New York Times (NYT) staffers claimed they were endangered by the publication of Sen. Tom Cotton’s (R-Ark.) opinion article advocating calling in military forces if necessary to stop rioting, as had been done in Detroit in 1967 and Los Angeles in 1992. A craven NYT publisher even fired the editorial page editor for running the article.

Evidence of visible and tangible discontent with increasing violence and its consequences—barren and locked shelves in Manhattan chain drugstores, skyrocketing carjackings in Washington, D.C.—is as unmistakable in polls and election results as it is in daily life in large metropolitan areas. Maybe 2024 will turn out to be the year even liberal America stopped acting crazy.

Chaos and disorder work against incumbents, as they did in 1968 when Democrats saw their party’s popular vote fall from 61 percent to 43 percent.

Views expressed in this article are opinions of the author and do not necessarily reflect the views of The Epoch Times or ZeroHedge.

Government

Veterans Affairs Kept COVID-19 Vaccine Mandate In Place Without Evidence

Veterans Affairs Kept COVID-19 Vaccine Mandate In Place Without Evidence

Authored by Zachary Stieber via The Epoch Times (emphasis ours),

The…

Share this:

Authored by Zachary Stieber via The Epoch Times (emphasis ours),

The U.S. Department of Veterans Affairs (VA) reviewed no data when deciding in 2023 to keep its COVID-19 vaccine mandate in place.

VA Secretary Denis McDonough said on May 1, 2023, that the end of many other federal mandates “will not impact current policies at the Department of Veterans Affairs.”

He said the mandate was remaining for VA health care personnel “to ensure the safety of veterans and our colleagues.”

Mr. McDonough did not cite any studies or other data. A VA spokesperson declined to provide any data that was reviewed when deciding not to rescind the mandate. The Epoch Times submitted a Freedom of Information Act for “all documents outlining which data was relied upon when establishing the mandate when deciding to keep the mandate in place.”

The agency searched for such data and did not find any.

“The VA does not even attempt to justify its policies with science, because it can’t,” Leslie Manookian, president and founder of the Health Freedom Defense Fund, told The Epoch Times.

“The VA just trusts that the process and cost of challenging its unfounded policies is so onerous, most people are dissuaded from even trying,” she added.

The VA’s mandate remains in place to this day.

The VA’s website claims that vaccines “help protect you from getting severe illness” and “offer good protection against most COVID-19 variants,” pointing in part to observational data from the U.S. Centers for Disease Control and Prevention (CDC) that estimate the vaccines provide poor protection against symptomatic infection and transient shielding against hospitalization.

There have also been increasing concerns among outside scientists about confirmed side effects like heart inflammation—the VA hid a safety signal it detected for the inflammation—and possible side effects such as tinnitus, which shift the benefit-risk calculus.

President Joe Biden imposed a slate of COVID-19 vaccine mandates in 2021. The VA was the first federal agency to implement a mandate.

President Biden rescinded the mandates in May 2023, citing a drop in COVID-19 cases and hospitalizations. His administration maintains the choice to require vaccines was the right one and saved lives.

“Our administration’s vaccination requirements helped ensure the safety of workers in critical workforces including those in the healthcare and education sectors, protecting themselves and the populations they serve, and strengthening their ability to provide services without disruptions to operations,” the White House said.

Some experts said requiring vaccination meant many younger people were forced to get a vaccine despite the risks potentially outweighing the benefits, leaving fewer doses for older adults.

“By mandating the vaccines to younger people and those with natural immunity from having had COVID, older people in the U.S. and other countries did not have access to them, and many people might have died because of that,” Martin Kulldorff, a professor of medicine on leave from Harvard Medical School, told The Epoch Times previously.

The VA was one of just a handful of agencies to keep its mandate in place following the removal of many federal mandates.

“At this time, the vaccine requirement will remain in effect for VA health care personnel, including VA psychologists, pharmacists, social workers, nursing assistants, physical therapists, respiratory therapists, peer specialists, medical support assistants, engineers, housekeepers, and other clinical, administrative, and infrastructure support employees,” Mr. McDonough wrote to VA employees at the time.

“This also includes VA volunteers and contractors. Effectively, this means that any Veterans Health Administration (VHA) employee, volunteer, or contractor who works in VHA facilities, visits VHA facilities, or provides direct care to those we serve will still be subject to the vaccine requirement at this time,” he said. “We continue to monitor and discuss this requirement, and we will provide more information about the vaccination requirements for VA health care employees soon. As always, we will process requests for vaccination exceptions in accordance with applicable laws, regulations, and policies.”

The version of the shots cleared in the fall of 2022, and available through the fall of 2023, did not have any clinical trial data supporting them.

A new version was approved in the fall of 2023 because there were indications that the shots not only offered temporary protection but also that the level of protection was lower than what was observed during earlier stages of the pandemic.

Ms. Manookian, whose group has challenged several of the federal mandates, said that the mandate “illustrates the dangers of the administrative state and how these federal agencies have become a law unto themselves.”

Government

Low Iron Levels In Blood Could Trigger Long COVID: Study

Low Iron Levels In Blood Could Trigger Long COVID: Study

Authored by Amie Dahnke via The Epoch Times (emphasis ours),

People with inadequate…

Share this:

{kind=link}

{kind=link}

Authored by Amie Dahnke via The Epoch Times (emphasis ours),

People with inadequate iron levels in their blood due to a COVID-19 infection could be at greater risk of long COVID.

{kind=link}

A new study indicates that problems with iron levels in the bloodstream likely trigger chronic inflammation and other conditions associated with the post-COVID phenomenon. The findings, published on March 1 in Nature Immunology, could offer new ways to treat or prevent the condition.

Long COVID Patients Have Low Iron Levels

Researchers at the University of Cambridge pinpointed low iron as a potential link to long-COVID symptoms thanks to a study they initiated shortly after the start of the pandemic. They recruited people who tested positive for the virus to provide blood samples for analysis over a year, which allowed the researchers to look for post-infection changes in the blood. The researchers looked at 214 samples and found that 45 percent of patients reported symptoms of long COVID that lasted between three and 10 months.

In analyzing the blood samples, the research team noticed that people experiencing long COVID had low iron levels, contributing to anemia and low red blood cell production, just two weeks after they were diagnosed with COVID-19. This was true for patients regardless of age, sex, or the initial severity of their infection.

According to one of the study co-authors, the removal of iron from the bloodstream is a natural process and defense mechanism of the body.

But it can jeopardize a person’s recovery.

“When the body has an infection, it responds by removing iron from the bloodstream. This protects us from potentially lethal bacteria that capture the iron in the bloodstream and grow rapidly. It’s an evolutionary response that redistributes iron in the body, and the blood plasma becomes an iron desert,” University of Oxford professor Hal Drakesmith said in a press release. “However, if this goes on for a long time, there is less iron for red blood cells, so oxygen is transported less efficiently affecting metabolism and energy production, and for white blood cells, which need iron to work properly. The protective mechanism ends up becoming a problem.”

The research team believes that consistently low iron levels could explain why individuals with long COVID continue to experience fatigue and difficulty exercising. As such, the researchers suggested iron supplementation to help regulate and prevent the often debilitating symptoms associated with long COVID.

“It isn’t necessarily the case that individuals don’t have enough iron in their body, it’s just that it’s trapped in the wrong place,” Aimee Hanson, a postdoctoral researcher at the University of Cambridge who worked on the study, said in the press release. “What we need is a way to remobilize the iron and pull it back into the bloodstream, where it becomes more useful to the red blood cells.”

The research team pointed out that iron supplementation isn’t always straightforward. Achieving the right level of iron varies from person to person. Too much iron can cause stomach issues, ranging from constipation, nausea, and abdominal pain to gastritis and gastric lesions.

1 in 5 Still Affected by Long COVID

COVID-19 has affected nearly 40 percent of Americans, with one in five of those still suffering from symptoms of long COVID, according to the U.S. Centers for Disease Control and Prevention (CDC). Long COVID is marked by health issues that continue at least four weeks after an individual was initially diagnosed with COVID-19. Symptoms can last for days, weeks, months, or years and may include fatigue, cough or chest pain, headache, brain fog, depression or anxiety, digestive issues, and joint or muscle pain.

Walmart launches clever answer to Target’s new membership program

Veterans Affairs Kept COVID-19 Vaccine Mandate In Place Without Evidence

The Coming Of The Police State In America

When Military Rule Supplants Democracy

United Airlines adds new flights to faraway destinations

Low Iron Levels In Blood Could Trigger Long COVID: Study

Walmart has really good news for shoppers (and Joe Biden)

Another beloved brewery files Chapter 11 bankruptcy

Angry Shouting Aside, Here’s What Biden Is Running On

Jack Smith Says Trump Retention Of Documents “Starkly Different” From Biden

-

Uncategorized2 weeks ago

Uncategorized2 weeks agoAll Of The Elements Are In Place For An Economic Crisis Of Staggering Proportions

-

Uncategorized1 month ago

Uncategorized1 month agoCathie Wood sells a major tech stock (again)

-

Uncategorized3 weeks ago

Uncategorized3 weeks agoCalifornia Counties Could Be Forced To Pay $300 Million To Cover COVID-Era Program

-

Uncategorized2 weeks ago

Uncategorized2 weeks agoApparel Retailer Express Moving Toward Bankruptcy

-

Uncategorized3 weeks ago

Uncategorized3 weeks agoIndustrial Production Decreased 0.1% in January

-

International2 days ago

Walmart launches clever answer to Target’s new membership program

-

International2 days ago

International2 days agoEyePoint poaches medical chief from Apellis; Sandoz CFO, longtime BioNTech exec to retire

-

Uncategorized3 weeks ago

Uncategorized3 weeks agoRFK Jr: The Wuhan Cover-Up & The Rise Of The Biowarfare-Industrial Complex