Government

S&P Futures Fall, “Panic Selling” In China As US-China Spat Escalates

S&P Futures Fall, "Panic Selling" In China As US-China Spat Escalates

Share this:

U.S. stock index futures fell and Chinese stocks tumbled on Friday following another escalation in tensions between the United States and China, and as Intel’s shares slumped after reporting a delay in a developing new chip technology. The dollar continued its slide on the back of euro and yen strength, while interest rates and gold were mostly unchanged.

Global stocks took a hit after Beijing ordered the Washington to close its consulate in the city of Chengdu, responding to a U.S. demand this week that China close its Houston consulate. Intel fell 12% premarket after the company said it was six months behind schedule in developing 7-nanometer chip technology and it would consider farming out more work to outside semiconductor foundries. Competitor Advanced Micro Devices gained 6% on Intel's woes. American Express dropped in pre-market trading after missing revenue estimates. FAAMGs stocks — Facebook, Amazon.com, Apple, Microsoft and Google — which were pivotal in driving the stock market’s recovery in recent months, slipped between 1.0% and 1.4% on Friday.

On Thursday, the S&P 500 pulled back from a five-month high weighed down by losses in technology stocks, a surprise increase in U.S. jobless claims and Washington’s tug-of-war over stimulus measures. Senate Republicans will unveil their proposal next week for a fresh round of coronavirus aid, including more direct payments to Americans and a partial extension of enhanced unemployment benefits, Senate Majority Leader Mitch McConnell said on Thursday.

European equities also slumped, following a heavy session in Asia which saw Chinese stocks tumble 4%.

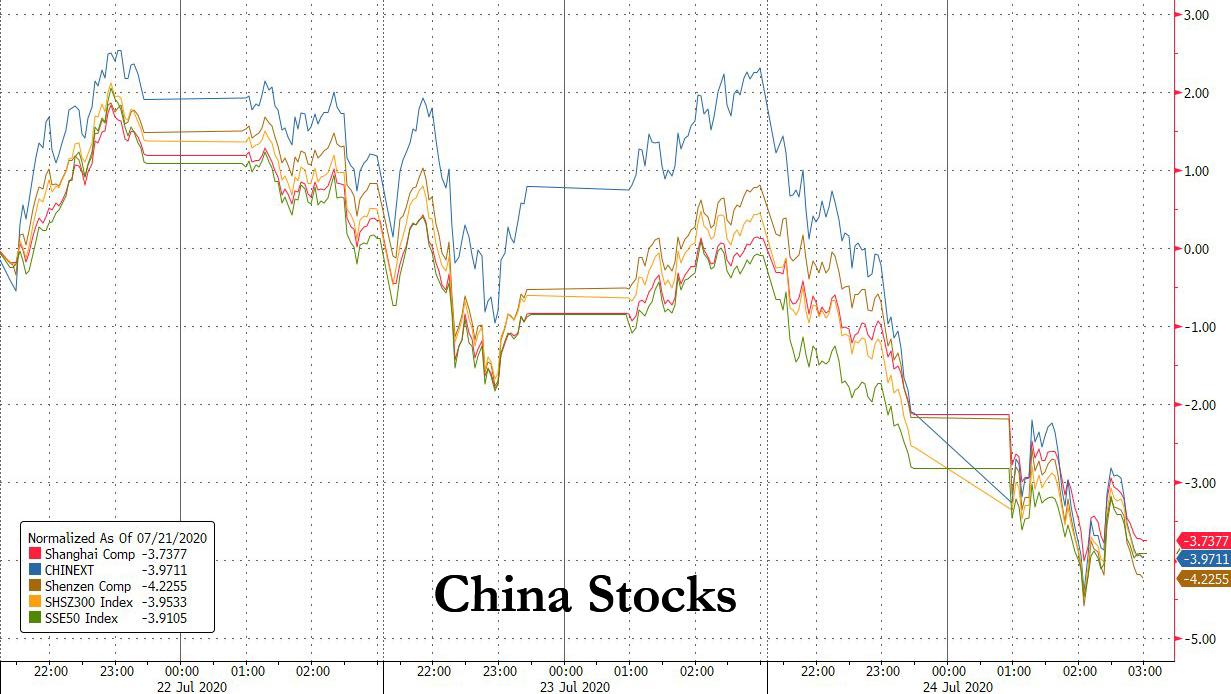

As Bloomberg reports, China’s traders, company insiders and overseas investors are all fleeing the country’s stock market. Sentiment is quickly souring amid the biggest threat to Beijing’s diplomatic ties with Washington in years. Traders based beyond mainland China sold more than $2.3 billion worth of Chinese stocks Friday, one of the largest ever outflows via Hong Kong’s exchange links. Some of China’s controlling tech shareholders are getting out as soon as they can. The CSI 300 Index fell 4.4% at the close, while the ChiNext Index dropped 6.1%, the most since Feb. 3. Losses accelerated in the afternoon after the Chinese foreign ministry said it ordered the U.S. to close its consulate in the southwestern city of Chengdu. The Trump administration earlier this week ordered the closure of a Chinese consulate in Houston. Overseas investors sold 16.4 billion yuan of China stocks Friday, the most since a record 17.4 billion yuan was dumped on July 14. Turnover rose to 1.3 trillion yuan, the 17th session over the 1 trillion yuan mark.

“Worries over China-U.S. relations will dominate the market,” said Raymond Chen, a portfolio manager with Keywise Capital Management (HK) Ltd. “People will be closely watching how the U.S. reacts to the closure of Chengdu consulate. I expect more panic selling in the near term.”

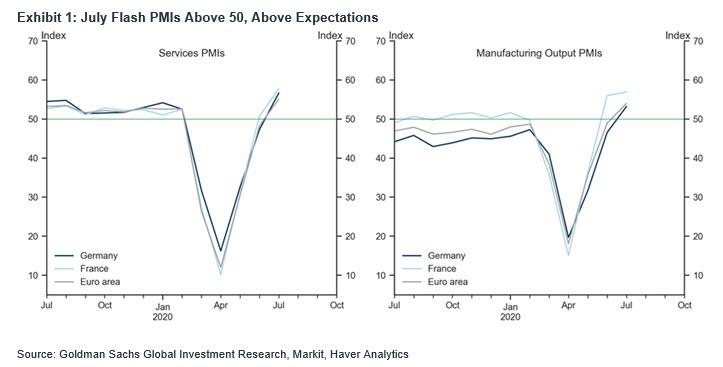

The Eurostoxx 600 dropped over 2% with tech, retailers and mining stocks posting sharp losses. Most equity indexes drop into the red for the week, brushing off broadly solid preliminary July PMI data, FTSE MIB underperforms at the margin. European market completely ignored the latest stronger than expected PMI data. As Globman notes, after a record, better-than-expected cumulative improvement of 34.8pt over May and June, the Euro area composite PMI improved further, by 6.3pt to 54.8 in July—notably above expectations—consistent with a continued positive impulse to economic activity from easier lockdown measures and the improvements in high-frequency data. Across sectors, the recovery was broad-based, and slightly stronger in services. The overall composition of the July PMIs was strong. New orders continued to improve amid firmer domestic and foreign demand. The German and French composite PMIs also registered larger-than-expected increases and rose comfortably above 50. Overall, the July PMIs indicate a continued, primarily demand-driven recovery in economic activity across the Euro area, with material positive growth in activity in July (but slower than in May and June).

Key numbers:

- Euro Area Composite PMI (July, Flash): 54.8, exp. 51.1, last 48.5.

- Euro Area Manufacturing PMI (July, Flash): exp. 50.1, last 47.4.

- Euro Area Services PMI (July, Flash): 55.1, exp. 51.0, last 48.3.

- Germany Composite PMI (July, Flash): 55.5, exp. 50.2, last 47.0.

- France Composite PMI (July, Flash): 57.6, exp. 53.5, last 51.7.

Australian stocks sunk along with regional peers on US-China escalation. The S&P/ASX 200 index fell 1.2% to close at 6,024.00.

In volatility, the VIX briefly snapped to a 28-handle while Europe's V2X sits at the week’s highs, just below a 27-handle.

In FX, the Japanese yen led G-10 currency gains amid a broad risk-off sentiment, and the Bloomberg Dollar Spot Index declined, while bunds fell on signs that German activity was expanding. The euro and the pound are on track for their biggest weekly rise against the dollar since early June following encouraging economic data from Germany, the euro area and the U.K. China’s yuan fell as much as 0.28% to 7.0238 versus the greenback, the weakest since July 8.

In rates, haven seekers pushed Treasury 5-year yields to a record low and U.S. equity futures slipped following escalating US-China tensions. Trade has been choppy: Bund futures rally to highs for the week near 177.00, before fading the move through Thursday’s worst levels. China’s government bonds extended gains, with futures contracts on 10-year notes climbing as much as 0.36% to the highest since July 3. The yield on debt due in a decade dropped 5 basis points to 2.86%, the lowest since July 1.

In commodities, oil was flat while gold closed in on $1,900 an ounce, nearing its all-time intraday high. The dollar extended this week’s slide, and the offshore yuan dipped. Core European bonds fell after U.S. Treasuries turned lower.

On the economic calendar, Markit manufacturing and services PMI surveys are due at 9:45 a.m. ET, while new home sales data is expected at 10 a.m.

Market Snapshot

- S&P 500 futures down 0.5% to 3,211.75

- STOXX Europe 600 down 1.9% to 366.44

- MXAP down 0.9% to 165.19

- MXAPJ down 1.8% to 542.36

- Nikkei down 0.6% to 22,751.61

- Topix down 0.6% to 1,572.96

- Hang Seng Index down 2.2% to 24,705.33

- Shanghai Composite down 3.9% to 3,196.77

- Sensex down 0.3% to 38,025.57

- Australia S&P/ASX 200 down 1.2% to 6,024.00

- Kospi down 0.7% to 2,200.44

- German 10Y yield unchanged at -0.48%

- Euro up 0.1% to $1.1612

- Brent Futures up 0.4% to $43.46/bbl

- Italian 10Y yield fell 5.3 bps to 0.858%

- Spanish 10Y yield rose 0.7 bps to 0.33%

- Brent Futures up 0.4% to $43.46/bbl

- Gold spot up 0.4% to $1,894.65

- U.S. Dollar Index down 0.03% to 94.66

Top Overnight News

- China retaliated to the U.S. decision to close its mission in Houston by ordering Washington to shut down its consulate in Chengdu, a key listening post for Tibet developments

- The euro- area economy saw activity grow for the first time in five months in July, but soft demand means companies continue to reduce headcount

- Banks haven’t sufficiently prepared for reforms to interest-rate benchmarks that underpin assets worth trillions of euros, the European Central Bank said

- European Union governments are poised to approve a “coordinated package” of measures to support Hong Kong in the face of China’s new national-security legislation for the financial hub

APAC stocks traded lower across the board as the region took its cue from the losses on Wall Street, where the S&P snapped a four-day winning streak and the Nasdaq underperformed on the back of the sell-off in major tech stocks. Furthermore, Intel shares slumped 10% after-hours despite broadly positive earnings as its advanced 7-nanometre chip product transition faces a further delay, albeit competitor AMD soared 7.5% on the news. Losses in Asia-Pac came ahead of the anticipated retaliatory announcement from China, where it confirmed it will be asking the US to close its consulate in Chengdu, as touted by sources. ASX 200 (-1.2%) was weighed on by the losses across its heavyweight miners and financials. KOSPI (-0.7%) took a breather from yesterday’s underperformance, and as new cases in South Korea continue to decline in pace. Hang Seng (-2.2%) was pressured by a number of large cap stocks in the red and with fears that the closure of the US consulate in Hong Kong is in China’s arsenal, although this would be akin to a nuclear option. Similarly. Shanghai Comp (-3.8%) underperformed as investors took chips off the table amid China’s retaliatory move, whilst experts cited by Global Times stated that Beijing could also consider a targeting strike such as expelling hundreds or more US diplomats in Mainland and Hong Kong,. As a reminder, Japanese markets were closed in observance of National Sports Day Holiday.

Top Asian News

- Panic Selling Grips Chinese Stocks After U.S. Tensions Worsen

- Glove Mania Boosts Malaysia Market Value to Challenge Singapore

European equities trade lower across the board (Eurostoxx 50 -1.5%) following a negative close on Wall Street yesterday, alongside heightening tensions between the US and China after China confirmed it will be asking the US to close the Chengdu consulate in response to the closure of the Chinese consulate in US. Furthermore, Europe is also being hampered by performance in tech names after Intel (-11.1% pre-market) reported after-hours yesterday. Despite financial metrics being broadly positive, disappointment was seen after reports that the Co.’s advanced 7-nanometre chip product transition faces a further delay. Given the above, a raft of broadly upbeat PMI prints from across the Eurozone have prompted only a modest pick-up in sentiment, with markets perhaps looking to the weeks/months ahead to determine if such readings are indicative of the recovery that is to come. Elsewhere in terms of sector-wide performance, telecom names are being weighed on by Vodafone (-5.2%) after the Co.’s Q1 sales fell short of expectations, whilst also announcing that it is targeting early 2021 for a Frankfurt listing of its mast business. Energy names are faring modestly better than peers, albeit still lower on the day with some reprieve being granted by slightly firmer energy prices and Equinor (+1.8%) after the Co. reported former than expected profits, supported by trading activities. Centrica (+20.0%) is the clear outperformer in the Stoxx 600 with the Co. announcing it is to propose the sale of Direct Energy to NRG Energy for USD 3.625bln in cash alongside H1 earnings.

Top European News

- U.K. July Flash Composite PMI 57.1 Vs 47.7; Est 51.7

- Vallourec Falls on Report That It Has Sought State Aid

- ECB Weighs the Publication of Compounded ESTR Term Rates

In FX, the lack of Japanese involvement and potential export/corporate supply may be exacerbating the move, but risk aversion on well documented and familiar factors have prompted a more pronounced and widespread increase in demand for the safe-haven Yen. Indeed, Usd/Jpy has made a decisive break through 107.00, 106.67-65 recent lows and is now edging towards the round number below where support resides at 106.07 (June 23 base) ahead of stronger downside technical levels in the form of a double or tweezer bottom at 105.99 (consecutive troughs from May 6 and 7). Similarly, Eur/Jpy has reversed sharply from post-EU fiscal stimulus highs to the low 123.00 zone, as the single currency loses momentum generally.

- EUR/GBP - Propped by better than expected and encouraging preliminary PMIs, including the German manufacturing sector returning from deep contraction to the threshold of expansion, but hampered on the other hand by broader risk-off sentiment and no progress on the Brexit trade front. Hence, the Euro is finding the altitude rare above 1.1600 against the Greenback and the Pound continues to struggle on the 1.2700 handle, albeit forming a firmer base above Cable’s 200 DMA (bang on the big figure today).

- AUD/CAD/NZD - Further erosion from lofty peaks vs their US counterpart, as the DXY pares some losses from a new 2020 nadir between 94.569-810 parameters, with the Aussie sub-0.7100, Loonie back under 1.3400 and Kiwi near the bottom of a 0.6653-19 range. Little independent reaction to decent improvements in CBA PMIs or a narrower NZ trade surplus overnight, with the former somewhat marred by more COVID-19 cases in Victoria and the Aud also monitoring another YUAN retreat below 7.0000 after confirmation of Chinese consulate retaliation against the US.

- EM - The aforementioned sour risk tone and rising virus infections are weighing on regional currencies, but the Rouble is deriving a degree of underlying support from Brent holding above Usd 43/brl awaiting the upcoming CBR rate call amidst expectations for a 50 bp reduction, but no guarantee after Governor Nabiullina intimated that a pause is possible following June’s ease to the current 4.5% ATH.

In commodities, WTI and Brent are firmer this morning in what appears to be a consolidation from some of the US hours downside given stimulus concerns and US-China tensions; albeit, the benchmarks still have some way to go to recapture yesterday’s decline. In terms of newsflow there is nothing fundamentally new for the complex, which has been the theme for the entirety of the week. On the docket for today we do have the weekly Baker Hughes rig count which may draw some attention but aside from that price action will likely follow, at least directionally, risk sentiment once again. This morning saw earnings from Equinor and in terms of their more qualitative commentary the CEO sees downward pressure on prices given OPEC easing their production cut quotas but ultimately continues to expect the market to achieve balance in 2022. For metals, the upside action for precious metals continues with gold and silver both firmer on the day aided by dollar downside. The yellow metal is yet to eclipse USD 1900/oz with the session high USD ~2/oz from this handle afterwhich just the all time high of USD 1921.75/oz lies as a possible sticking point.

US Event Calendar

- 9:45am: Markit US Manufacturing PMI, est. 52, prior 49.8

- Markit US Services PMI, est. 51, prior 47.9

- Markit US Composite PMI, prior 47.9

- 10am: New Home Sales, est. 700,000, prior 676,000

- 10am: New Home Sales MoM, est. 3.55%, prior 16.6%

DB's Jim Reid concludes the overnight wrap

I’m in the dog house today. As my golf club has now opened for outdoor dining I took Maisie on a lunch date yesterday and a rare hour away from the desk. She has missed their ice creams and was so excited about going back. I even bought her a pink putter to use on the practise green. We had a lovely lunch and by 1pm I was back at my desk. At 5pm my wife comes up to my study and says “how much ice cream did you give Maisie? She has been hyper all afternoon and I can’t control her. She’s being a nightmare”. I innocently replied that she ate 3 scoops. My wife said, “Jim, she’s only 4. She shouldn’t have more than one small scoop. Not 3 adult size ones. She’s still got so much sugar running through her veins. Thanks a lot”. I had no concept at the time although I did wonder why she kept on knocking the putts off the green.

It’s fair to say that US/Chinese relations continue to steer off the fairway and into the deep rough and US Secretary of State Pompeo speech last night didn’t help matters. In it the Secretary called on the Chinese people to change the direction of the ruling Communist Party. He also said that “a new alliance of democracies” should be made to push back against “the Chinese Communist Party’s designs on hegemony”. Overall the speech was fairly hawkish in nature. This came a few hours after it was reported that China is ‘set to shut US consulate’ in Chengdu (confirmed overnight). It is strategically important given American interest in Tibet and is seemingly in retaliation to the orders earlier this week to close the Chinese consulate in Houston.

Shortly after a draft of Pompeo speech was sent to major news networks, US risk assets started sliding, especially technology stocks. Remember that these were more sensitive to negative news flow during the trade war last year.

Today however, attention will turn to the flash PMIs for July, which will be one of the first indications of how different economies have performed in the month. Overnight we saw the numbers out from Australia, which showed a continued recovery with the services PMI printing at 58.5 (vs 53.1 last month) while manufacturing came in at 53.4 (vs. 51.2 last month) bringing the composite PMI to 57.9 (vs. 52.7 last month). In Europe and the US consensus expectations are that most of the PMIs will cross the crucial 50-mark that separates expansion from contraction, but of course this is following months of often severe contractions, so still a long way to go before we get back to where we were. A big focus will be on whether the US can hold up relative to Europe given the slowing down of reopenings in the former and the steady normalisation in the latter.

Asian markets are all trading lower this morning with Chinese bourses leading the declines amidst renewed tensions with the US. The Hang Seng (-1.83%), Shanghai Comp (-2.25%), CSI (-2.99%), Kospi (-0.66%) and Asx (-1.17%) are all down. Meanwhile, President Trump’s overnight statement that the trade deal with China “means less to me now than when I made it” is also appearing to weigh on sentiment. In a sign of risk off, the Japanese yen is up +0.43% this morning. Futures, on the S&P 500 are also down -0.46% after a tough close in the US. Elsewhere, Japan’s markets continue to remain closed for a holiday and Intel’s warning on a production delay also has seen an after-hours dip in the stock (-1.06%).

Ahead of Pompeo’s speech yesterday, risk assets ran out of steam on poor US data and then accelerated lower on weakness in Tech stocks. The S&P 500 dropped -1.23% from its post-pandemic high the previous day. It was the “Mega-cap” Tech stocks that led the declines, first on the US/China headlines and then took another leg lower later in the session, potentially on regulatory news. It was reported that Apple could be facing a multi-state consumer protection probe. Also the US House of Representatives panel is meeting next week (on July 27) to discuss Google (-3.07%), Facebook (-3.03%), Apple (-4.55%) and Amazon (-3.66%) on potential antitrust matters. The panel was prescheduled but the outcomes may have higher investor scrutiny now given recent outperformance of the complex. The underperformance of tech stocks saw the NASDAQ close down -2.29%, the largest retreat in nearly a month. A reminder that Apjit Walia, our Tech Strategist, published a report where he explores the upcoming tech cold war between the US and China (first touched upon in our latest Konzept magazine). This could cost the sector $3.5tn over the next five years in a full blown cold war. Link to new video here.

With the majority of the US loses coming later in the session, European equities survived with little change, with the STOXX 600 managing to eke out a +0.06% advance. Meanwhile, the DAX saw a miniscule -0.01% loss, but it still brought an end to a run of 10 successive sessions in which it had outpaced the STOXX 600.

Along with the ratcheting up of US-China tensions and the ensuing tech news, the mood among investors was further dampened by the initial weekly jobless claims from the US, which covered the week ending July 18. They showed an increase in claims to 1.416m (vs. 1.3m expected), marking the first time that weekly claims have risen since late March, bringing to an end a run of 15 successive declines. Certainly that’s a metric to watch out for given the resurgence of the virus in the US, and the increase will only add to concerns that the recent progress in reducing unemployment in the last couple of jobs reports is likely to slow in the months ahead. That said, we did get more positive news from the continuing claims for the previous week (ending July 11), which fell to 16.197m (vs. 17.1m expected), with the insured unemployment rate falling to 11.1%.

On the coronavirus, Florida reported a record 173 deaths yesterday as cases rose by 2.6%, which is under the 7-day 3.3% average but still represents over 10,000 new cases. Even in light of the pickup in fatalities and high absolute case rate, Governor DeSantis said there was no need to impose new restrictions, citing locally enacted mask and distancing measures. Meanwhile, California reported 5,975 new cases over the past 24 hours or a 2.9% increase, which is larger than the 2.5% 7-day average, indicating that the spread is still ongoing in the state even as they re-implemented some restrictions late last month. On the other hand, Arizona is likely seeing early returns on their restrictions as public-health experts in the state said the virus may have reached a peak. Cases rose by 1.3% vs. the 7-day average of 2.0% and the 7-day average of new cases has fallen from under 4000 per day to just over 2000 in the past week. Given the initial claims data worsening across the US, it will be important to watch which states can get the recent outbreak under control and how long it takes to do so. Elsewhere, Asian countries like Hong Kong, Japan, India and the Australian state of Victoria are also seeing worrying virus trends.

Sticking with the US, it looks like fiscal support may be a bit further away, as Senate majority leader Mitch McConnell said overnight that committee chairman and other Republicans would begin introducing components of their stimulus plan on Monday. This may mean the Fed decides it needs to do more of the lifting when it meets next week. In other details on the stimulus plan out overnight, instead of a payroll tax cut, the GOP will now back $1,200 checks for individuals who make as much as $75,000 a year, exactly as in the March stimulus bill.

Back to markets yesterday and in fixed income, the drop in risk sentiment saw 10yr Treasury yields fall a further -2.0bps to 0.577%, a 3-month low and just 3.7bps off its all-time record low back in March. In Europe there was yet another divergence between core and periphery following the agreement on the recovery fund. Notably, yields on 10yr Italian BTPs fell below 1% for the first time since the lockdown, and the spread of Italian (-6.2bps), Spanish (-2.0bps) and Portuguese (-2.9bps) 10yr yields over bunds all fell to 4-month lows.

Staying on Europe, the latest round of Brexit talks wrapped up yesterday on the UK and EU’s future relationship. However, it was clear from what both sides said afterwards that serious gaps remained between their respective positions. Judging by both statements, the two key sticking points continue to be the question of the level playing field, where the EU is seeking guarantees that the UK won’t undercut it with lower standards, along with fisheries. The UK’s chief negotiator David Frost said that “considerable gaps remain in the most difficult areas”, while the EU’s chief negotiator Michel Barnier notably said that the UK’s “refusal to commit to conditions of open and fair competition and to a balanced agreement on fisheries” meant that “the UK makes a trade agreement at this point unlikely.”

With all that said, there were some promising signs, with indications that there’d been movement by both sides on the question of how a future agreement would be governed, as well as progress on the question of UK participation in EU programmes. The two sides have until the end of the year to finalise a deal, when the Brexit transition period finishes. In practice an agreement will likely be needed earlier than that, because of the ratification process that needs to occur. Barnier himself has previously put this effective deadline at the end of October, so it should be an eventful few months ahead.

In terms of the latest in the precious metals rally, gold advanced a further +0.86% yesterday in its 5th consecutive move upwards, reaching a fresh 8-year high of $1887/oz. Note that we’re now less than 1% away from the all-time closing high in nominal terms for gold of $1900/oz back in September 2011, with the intraday high of $1921/oz also reached that month. The rally ran out of steam elsewhere however, with silver down by -1.77%, and platinum (-0.47%) and palladium (-0.07%) also moving lower.

Finally, there wasn’t much in the way of other data yesterday. However, the European Commission’s advance consumer confidence reading for the Euro Area in July unexpectedly fell back to -15.0 (vs. -14.7 in June), suggesting the rebound might not be as vigorous as expected. Over in the US meanwhile, the Kansas City Fed’s manufacturing index rose to 3 (vs. 5 expected).

Before the day ahead some advertising of some interesting recent DB research videos. Our APAC Economics team have received an unusually high number of questions about the future of the HKD peg in recent weeks. What's especially unusual is that market participants are concerned about devaluation of a currency that has been trading on the strong side of the convertibility band for most of the last four months. Video and report here from Michael Spencer, Head of APAC Research. Staying in APAC Yi Xiong, Chief China Economist, has published a report on how after a strong rebound in Q2, divergence across sectors will likely be the next main theme for China’s economy. Video and report here.

To the day ahead now, and the highlight is likely to be the aforementioned flash PMI readings. Otherwise, there’s UK retail sales out for June, Italy’s consumer confidence index for July, and US new home sales for June. Elsewhere, the Russian central bank will be making its latest monetary policy decision, while earnings highlights include Verizon, NextEra Energy, T-Mobile and American Express.

Government

Are Voters Recoiling Against Disorder?

Are Voters Recoiling Against Disorder?

Authored by Michael Barone via The Epoch Times (emphasis ours),

The headlines coming out of the Super…

Share this:

Authored by Michael Barone via The Epoch Times (emphasis ours),

The headlines coming out of the Super Tuesday primaries have got it right. Barring cataclysmic changes, Donald Trump and Joe Biden will be the Republican and Democratic nominees for president in 2024.

With Nikki Haley’s withdrawal, there will be no more significantly contested primaries or caucuses—the earliest both parties’ races have been over since something like the current primary-dominated system was put in place in 1972.

The primary results have spotlighted some of both nominees’ weaknesses.

Donald Trump lost high-income, high-educated constituencies, including the entire metro area—aka the Swamp. Many but by no means all Haley votes there were cast by Biden Democrats. Mr. Trump can’t afford to lose too many of the others in target states like Pennsylvania and Michigan.

Majorities and large minorities of voters in overwhelmingly Latino counties in Texas’s Rio Grande Valley and some in Houston voted against Joe Biden, and even more against Senate nominee Rep. Colin Allred (D-Texas).

Returns from Hispanic precincts in New Hampshire and Massachusetts show the same thing. Mr. Biden can’t afford to lose too many Latino votes in target states like Arizona and Georgia.

When Mr. Trump rode down that escalator in 2015, commentators assumed he’d repel Latinos. Instead, Latino voters nationally, and especially the closest eyewitnesses of Biden’s open-border policy, have been trending heavily Republican.

High-income liberal Democrats may sport lawn signs proclaiming, “In this house, we believe ... no human is illegal.” The logical consequence of that belief is an open border. But modest-income folks in border counties know that flows of illegal immigrants result in disorder, disease, and crime.

There is plenty of impatience with increased disorder in election returns below the presidential level. Consider Los Angeles County, America’s largest county, with nearly 10 million people, more people than 40 of the 50 states. It voted 71 percent for Mr. Biden in 2020.

Current returns show county District Attorney George Gascon winning only 21 percent of the vote in the nonpartisan primary. He’ll apparently face Republican Nathan Hochman, a critic of his liberal policies, in November.

Gascon, elected after the May 2020 death of counterfeit-passing suspect George Floyd in Minneapolis, is one of many county prosecutors supported by billionaire George Soros. His policies include not charging juveniles as adults, not seeking higher penalties for gang membership or use of firearms, and bringing fewer misdemeanor cases.

The predictable result has been increased car thefts, burglaries, and personal robberies. Some 120 assistant district attorneys have left the office, and there’s a backlog of 10,000 unprosecuted cases.

More than a dozen other Soros-backed and similarly liberal prosecutors have faced strong opposition or have left office.

St. Louis prosecutor Kim Gardner resigned last May amid lawsuits seeking her removal, Milwaukee’s John Chisholm retired in January, and Baltimore’s Marilyn Mosby was defeated in July 2022 and convicted of perjury in September 2023. Last November, Loudoun County, Virginia, voters (62 percent Biden) ousted liberal Buta Biberaj, who declined to prosecute a transgender student for assault, and in June 2022 voters in San Francisco (85 percent Biden) recalled famed radical Chesa Boudin.

Similarly, this Tuesday, voters in San Francisco passed ballot measures strengthening police powers and requiring treatment of drug-addicted welfare recipients.

In retrospect, it appears the Floyd video, appearing after three months of COVID-19 confinement, sparked a frenzied, even crazed reaction, especially among the highly educated and articulate. One fatal incident was seen as proof that America’s “systemic racism” was worse than ever and that police forces should be defunded and perhaps abolished.

2020 was “the year America went crazy,” I wrote in January 2021, a year in which police funding was actually cut by Democrats in New York, Los Angeles, San Francisco, Seattle, and Denver. A year in which young New York Times (NYT) staffers claimed they were endangered by the publication of Sen. Tom Cotton’s (R-Ark.) opinion article advocating calling in military forces if necessary to stop rioting, as had been done in Detroit in 1967 and Los Angeles in 1992. A craven NYT publisher even fired the editorial page editor for running the article.

Evidence of visible and tangible discontent with increasing violence and its consequences—barren and locked shelves in Manhattan chain drugstores, skyrocketing carjackings in Washington, D.C.—is as unmistakable in polls and election results as it is in daily life in large metropolitan areas. Maybe 2024 will turn out to be the year even liberal America stopped acting crazy.

Chaos and disorder work against incumbents, as they did in 1968 when Democrats saw their party’s popular vote fall from 61 percent to 43 percent.

Views expressed in this article are opinions of the author and do not necessarily reflect the views of The Epoch Times or ZeroHedge.

Government

Veterans Affairs Kept COVID-19 Vaccine Mandate In Place Without Evidence

Veterans Affairs Kept COVID-19 Vaccine Mandate In Place Without Evidence

Authored by Zachary Stieber via The Epoch Times (emphasis ours),

The…

Share this:

Authored by Zachary Stieber via The Epoch Times (emphasis ours),

The U.S. Department of Veterans Affairs (VA) reviewed no data when deciding in 2023 to keep its COVID-19 vaccine mandate in place.

VA Secretary Denis McDonough said on May 1, 2023, that the end of many other federal mandates “will not impact current policies at the Department of Veterans Affairs.”

He said the mandate was remaining for VA health care personnel “to ensure the safety of veterans and our colleagues.”

Mr. McDonough did not cite any studies or other data. A VA spokesperson declined to provide any data that was reviewed when deciding not to rescind the mandate. The Epoch Times submitted a Freedom of Information Act for “all documents outlining which data was relied upon when establishing the mandate when deciding to keep the mandate in place.”

The agency searched for such data and did not find any.

“The VA does not even attempt to justify its policies with science, because it can’t,” Leslie Manookian, president and founder of the Health Freedom Defense Fund, told The Epoch Times.

“The VA just trusts that the process and cost of challenging its unfounded policies is so onerous, most people are dissuaded from even trying,” she added.

The VA’s mandate remains in place to this day.

The VA’s website claims that vaccines “help protect you from getting severe illness” and “offer good protection against most COVID-19 variants,” pointing in part to observational data from the U.S. Centers for Disease Control and Prevention (CDC) that estimate the vaccines provide poor protection against symptomatic infection and transient shielding against hospitalization.

There have also been increasing concerns among outside scientists about confirmed side effects like heart inflammation—the VA hid a safety signal it detected for the inflammation—and possible side effects such as tinnitus, which shift the benefit-risk calculus.

President Joe Biden imposed a slate of COVID-19 vaccine mandates in 2021. The VA was the first federal agency to implement a mandate.

President Biden rescinded the mandates in May 2023, citing a drop in COVID-19 cases and hospitalizations. His administration maintains the choice to require vaccines was the right one and saved lives.

“Our administration’s vaccination requirements helped ensure the safety of workers in critical workforces including those in the healthcare and education sectors, protecting themselves and the populations they serve, and strengthening their ability to provide services without disruptions to operations,” the White House said.

Some experts said requiring vaccination meant many younger people were forced to get a vaccine despite the risks potentially outweighing the benefits, leaving fewer doses for older adults.

“By mandating the vaccines to younger people and those with natural immunity from having had COVID, older people in the U.S. and other countries did not have access to them, and many people might have died because of that,” Martin Kulldorff, a professor of medicine on leave from Harvard Medical School, told The Epoch Times previously.

The VA was one of just a handful of agencies to keep its mandate in place following the removal of many federal mandates.

“At this time, the vaccine requirement will remain in effect for VA health care personnel, including VA psychologists, pharmacists, social workers, nursing assistants, physical therapists, respiratory therapists, peer specialists, medical support assistants, engineers, housekeepers, and other clinical, administrative, and infrastructure support employees,” Mr. McDonough wrote to VA employees at the time.

“This also includes VA volunteers and contractors. Effectively, this means that any Veterans Health Administration (VHA) employee, volunteer, or contractor who works in VHA facilities, visits VHA facilities, or provides direct care to those we serve will still be subject to the vaccine requirement at this time,” he said. “We continue to monitor and discuss this requirement, and we will provide more information about the vaccination requirements for VA health care employees soon. As always, we will process requests for vaccination exceptions in accordance with applicable laws, regulations, and policies.”

The version of the shots cleared in the fall of 2022, and available through the fall of 2023, did not have any clinical trial data supporting them.

A new version was approved in the fall of 2023 because there were indications that the shots not only offered temporary protection but also that the level of protection was lower than what was observed during earlier stages of the pandemic.

Ms. Manookian, whose group has challenged several of the federal mandates, said that the mandate “illustrates the dangers of the administrative state and how these federal agencies have become a law unto themselves.”

Government

Low Iron Levels In Blood Could Trigger Long COVID: Study

Low Iron Levels In Blood Could Trigger Long COVID: Study

Authored by Amie Dahnke via The Epoch Times (emphasis ours),

People with inadequate…

Share this:

{kind=link}

{kind=link}

Authored by Amie Dahnke via The Epoch Times (emphasis ours),

People with inadequate iron levels in their blood due to a COVID-19 infection could be at greater risk of long COVID.

{kind=link}

A new study indicates that problems with iron levels in the bloodstream likely trigger chronic inflammation and other conditions associated with the post-COVID phenomenon. The findings, published on March 1 in Nature Immunology, could offer new ways to treat or prevent the condition.

Long COVID Patients Have Low Iron Levels

Researchers at the University of Cambridge pinpointed low iron as a potential link to long-COVID symptoms thanks to a study they initiated shortly after the start of the pandemic. They recruited people who tested positive for the virus to provide blood samples for analysis over a year, which allowed the researchers to look for post-infection changes in the blood. The researchers looked at 214 samples and found that 45 percent of patients reported symptoms of long COVID that lasted between three and 10 months.

In analyzing the blood samples, the research team noticed that people experiencing long COVID had low iron levels, contributing to anemia and low red blood cell production, just two weeks after they were diagnosed with COVID-19. This was true for patients regardless of age, sex, or the initial severity of their infection.

According to one of the study co-authors, the removal of iron from the bloodstream is a natural process and defense mechanism of the body.

But it can jeopardize a person’s recovery.

“When the body has an infection, it responds by removing iron from the bloodstream. This protects us from potentially lethal bacteria that capture the iron in the bloodstream and grow rapidly. It’s an evolutionary response that redistributes iron in the body, and the blood plasma becomes an iron desert,” University of Oxford professor Hal Drakesmith said in a press release. “However, if this goes on for a long time, there is less iron for red blood cells, so oxygen is transported less efficiently affecting metabolism and energy production, and for white blood cells, which need iron to work properly. The protective mechanism ends up becoming a problem.”

The research team believes that consistently low iron levels could explain why individuals with long COVID continue to experience fatigue and difficulty exercising. As such, the researchers suggested iron supplementation to help regulate and prevent the often debilitating symptoms associated with long COVID.

“It isn’t necessarily the case that individuals don’t have enough iron in their body, it’s just that it’s trapped in the wrong place,” Aimee Hanson, a postdoctoral researcher at the University of Cambridge who worked on the study, said in the press release. “What we need is a way to remobilize the iron and pull it back into the bloodstream, where it becomes more useful to the red blood cells.”

The research team pointed out that iron supplementation isn’t always straightforward. Achieving the right level of iron varies from person to person. Too much iron can cause stomach issues, ranging from constipation, nausea, and abdominal pain to gastritis and gastric lesions.

1 in 5 Still Affected by Long COVID

COVID-19 has affected nearly 40 percent of Americans, with one in five of those still suffering from symptoms of long COVID, according to the U.S. Centers for Disease Control and Prevention (CDC). Long COVID is marked by health issues that continue at least four weeks after an individual was initially diagnosed with COVID-19. Symptoms can last for days, weeks, months, or years and may include fatigue, cough or chest pain, headache, brain fog, depression or anxiety, digestive issues, and joint or muscle pain.

Veterans Affairs Kept COVID-19 Vaccine Mandate In Place Without Evidence

The Coming Of The Police State In America

When Military Rule Supplants Democracy

Low Iron Levels In Blood Could Trigger Long COVID: Study

Walmart has really good news for shoppers (and Joe Biden)

Another beloved brewery files Chapter 11 bankruptcy

Jack Smith Says Trump Retention Of Documents “Starkly Different” From Biden

Walmart joins Costco in sharing key pricing news

Angry Shouting Aside, Here’s What Biden Is Running On

Are Voters Recoiling Against Disorder?

-

Uncategorized2 weeks ago

Uncategorized2 weeks agoAll Of The Elements Are In Place For An Economic Crisis Of Staggering Proportions

-

Uncategorized1 month ago

Uncategorized1 month agoCathie Wood sells a major tech stock (again)

-

Uncategorized3 weeks ago

Uncategorized3 weeks agoCalifornia Counties Could Be Forced To Pay $300 Million To Cover COVID-Era Program

-

Uncategorized2 weeks ago

Uncategorized2 weeks agoApparel Retailer Express Moving Toward Bankruptcy

-

Uncategorized3 weeks ago

Uncategorized3 weeks agoIndustrial Production Decreased 0.1% in January

-

International2 days ago

International2 days agoWalmart launches clever answer to Target’s new membership program

-

International2 days ago

International2 days agoEyePoint poaches medical chief from Apellis; Sandoz CFO, longtime BioNTech exec to retire

-

Uncategorized3 weeks ago

Uncategorized3 weeks agoRFK Jr: The Wuhan Cover-Up & The Rise Of The Biowarfare-Industrial Complex