Uncategorized

Social Credit Brazilian Style: All UBI Recipients Must Be Vaxxed

Social Credit Brazilian Style: All UBI Recipients Must Be Vaxxed

Authored by Mark Jeftovic via BombThrower.com,

This is what CBDCs are being…

Share this:

Authored by Mark Jeftovic via BombThrower.com,

This is what CBDCs are being built for

Anybody who seriously thinks that Universal Basic Income (UBI) programs of the future won’t be full blown social credit systems need look no further than Brazil, where newly selected socialist / globalist Lula da Silva just decreed that the Bolsa Familia program will require family members to be vaccinated in order to continue receiving benefits.

“We can’t play, it’s a question of science. If I have 10 covid vaccines to take, I will take all that is necessary ”.

The news comes via The Rio Times, which describes the Bolsa program as “a social welfare program for the poorest families in Brazil” and “a kind of Universal Basic Income”.

Lula says Brazilians can receive financial aid only if they have taken the vax. Bolsa Família will require vax certificates from participants & their children: We can't play, it's a question of science. If I have 10 covid vaccines to take, I will take all that is necessary. ???? ???? pic.twitter.com/hqrYq4jO6r

— Geopolitics & Empire (@Geopolitics_Emp) February 7, 2023

UBI is considered by many to be beneficent and inevitable. I personally believe the latter but not the former.

However it shouldn’t surprise anyone that if you’re dependent on The Saviour State for your sustenance (as Charles Hugh Smith calls it), you are, in effect, their chattel.

CBDCs will be the rails for UBI programs

The emergence of Central Bank Digital Currency (CBDC) initiatives in nearly every nation on earth clearly signals the direction this is going. Nearly every CBDC white paper or proposal I’ve come across have the following three characteristics spelled out in plain text, and I expect every CBDC to have these five capabilities baked-in, whether or not they are initially enabled (or documented).

#1) Expiry dates / use-by dates

CBDCs will have expiry dates after which their value will evaporate or erode. What I’ve noticed is white papers coming out of central banks started framing it as a feature, not a bug, to facilitate “recovery of lost funds”.

Abstract

An important feature of physical cash payments is resilience, which is due to their indifference to power outages or network coverage. Many central banks are exploring issuing digital cash substitutes with similar online payment functionality. Such substitutes could incorporate novel features, making them more desirable than physical cash. This paper considers introducing an expiry date for online digital currency balances to automate personal loss recovery. We show that this functionality could substantially increase consumer demand for digital cash, with the time to expiration playing an important role. Having more information available to the central bank improves accuracy of loss recovery but may decrease welfare.

— Best Before Expiry? Expiring Digital Currency and Loss Recovery, Bank of Canada Staff Paper, December 24, 2021

However the real reason CBDCs will have expiry dates is to stimulate money velocity and keep recipients dependent.

#2) “Anti-hoarding” features

Saving for the future is being rebranded as “hoarding” and it is becoming officially unfashionable because personal savings reduces dependancy on the state. The easiest mechanism for achieving this will be through negative interest rates on savings accounts, as per this IMF white paper,

“A world with lower inflation (and even zero inflation) and no persistent recessions may sound like a pipe dream, but we argue that it is possible by transitioning to an “electronic money standard.” Such a transition requires eliminating the zero lower bound, which central banks can achieve using readily available tools. Breaking the zero lower bound implies that the optimal rate of inflation will be lower than in the presence of the lower bound. This will empower central banks to quickly restore full employment and, over the medium term, possibly move toward targeting full price stability with zero inflation.”

…which goes on to outline the challenges there would be in eliminating the “arbitrage” between digital and physical cash:

A zero lower bound can be broken through a combination of (1) adopting or strengthening an electronic money standard in which electronic money is the unit of account and (2) implementing a time-varying interest rate (or more generally, rate of return) on paper currency (cash). Then, as the interest rate on cash moves in line with the official policy rates, there is no arbitrage between cash and money in the bank. Operationally this can be done while remaining quite close to the current monetary system, but there are several legal, communication, and political challenges to a transition to such an electronic money standard (Agarwal, and Kimball 2019).

(Despite the current rise in rates, once the money printers fire back up, this is where we’re headed).

#3) Total Information Awareness

Once it’s digitized in a centralized database (central banks) as opposed to being cryptographically secured on a decentralized blockchain (Bitcoin) – everything becomes known to central authorities instantly. Taxation can be applied per-transaction, but more interestingly – prices can also be modified on the fly.

If you’re behind on your property or income taxes – or have an unpaid fine (maybe because you’re fighting it), for example, they could simply enable a rolling garnishee on your wallet until it’s paid off.

While all transaction signatures are public on Bitcoin – they are pseudonymous and more importantly, unalterable. It’s true it may be known or discoverable that A sent sats to B, but there’s nothing any third-party can do about it. With Lightning on the ascent, combined with various privacy enhancements there – Bitcoin development is moving in the direction of more freedom and more privacy – which is the opposite direction of most CBDC initiatives.

Finally, whether CBDCs are launched with the noblest of intentions, there will at some point arise “an emergency” which will make it necessary for The People in Charge to “flip the switch” and turn them into:

#4) Social Credit Systems

Imagine if “LoonCoin” was a thing last year when the #FreedomConvoy hit Ottawa (and signalled the beginning of a worldwide revolt against Covid tyranny). Instead of emailing a list of bank accounts to be frozen that were cribbed from a (hacked) spreadsheet, they could simply direct the Bank of Canada to turn off everybody’s digital wallets who were in the vicinity of the protest, or who contributed to their crowdfund, or who retweeted the #HonkHonk hashtag.

Do you think they wouldn’t have done it?

Covid vaxports have already been weaponized in China, Brazil is doing it with their UBI program and when this is all formaized into a CBDC, they will probably not launch it without the framework for widespread social credit and control systems being part of the plumbing.

We all know from our experience with the pandemic, emergencies tend to drag on in perpetuity. The “War on Terror” is still in effect, and there are still legions of collectivist automatons tweeting #CovidIsntOver.

So when “The Long Emergency” (to use James Kunstler’s term) becomes a never ending, rolling climate crisis, the social credit systems built into CBDCs will be used to enforce:

#5) Carbon footprint tracking

Back in Carbon Rationing, CBDCs and Sound Money I wrote how this trajectory is more or less baked-in now, and that the state-run financial system is undergoing a shift from a debt-backed monetary system to one based on carbon quotas.

Dashboard of Svalna’s app. Image credit Svalna.

This is the ultimate end-game of CBDCs. There is no hidden agenda or conspiracy around this (there’s already a Mastercard that cuts off your spending when you exceed your carbon quota), and globalist elites are quite up front about it….

Notice how he pitched it as “track your own footprint” then described it as “track their”, “what they’re eating”, “where they’re travelling” https://t.co/omHLzwqJAZ

— Mark Jeftovic, The ₿itcoin Capitalist (@StuntPope) February 9, 2023

Why CBDCs will ultimately fail

The developments of CBDCs is something we monitor in The Bitcoin Capitalist (formerly The Crypto Capitalist). Every month we put out our coverage of CBDCs in the “Eye On Evilcoin” section and it’s not always bad news:

There is still some time to stop CBDCs

Despite all the jawboning about CBDCs, nobody has really deployed anything viable. It’s all still design and planning – with some test beds going on. The few projects that have launched formal, actual CBDC’s have largely stiffed: Nigeria’s Enaira, Venezuela (lol). Even China’s much vaunted Digital Yuan had an underwhelming reception at last year’s Olympics (my suspicion is that the global financial system is unraveling faster than CBDCs can be developed, so they may have to go with something already out there, like Ethereum).

Worth noting, is that Brazil plans to deploy its CBDC next year.

I should note one exception to all the proposals out there in former CFTC Commissioner Chris Giancarlo (a.k.a “CryptoDad”) and the Digital Dollar Project. So far it’s the one proposal I’ve seen bucking the trend among all CBDC specifications in that there is no talk of expiry dates, and an actual emphasis on tokenization, custody and privacy.

CBDCs will not be permanent

It amuses me that when I read these plans around social credit flavoured CBDC’s, policy makers still continue to believe that by hobbling “cash”, making it impossible to save, eliminating privacy and layering on Orwellian levels of social control, they still get something that the public will prefer to cash, crypto or Bitcoin.

Only a central banker would be worried that people are going to want to hoard a statist shitcoin. (Especially after they put expiry dates on it).

— Mark Jeftovic, The ₿itcoin Capitalist (@StuntPope) February 8, 2023

It’s delusional.

Incentives matter, and that’s why nobody in their right might isn’t going to hold any wealth in CBDCs and keep their transactions within it to the lowest practical level.

The overall global system of governance is in a Fourth Turning style restructuring. With institutional legitimacy in tatters and public trust plummeting, CBDCs are typical and symbolic of the last gasp of industrial era, centrally planned economies.

The transition period between where we are now (Late Stage Globalism) and where we are headed – decentralized Network States, is going to be rough, so I advise battening down the hatches and reducing one’s reliance on government entitlements as much as possible…

Pro Tip: Don’t be poor

This is where we’re headed folks, so at the risk of sounding flippant, the solution is not to need financial aid.

Anybody depending on state entitlements or financial support will be CBDCerfs, their affairs fully regulated by the state, their carbon footprints metered, and rationed, while their lives are gamified through their smartphones.

Among the affluent G20 nations where woke-ism reigns supreme and neo-Marxism is still fashionable, a lot of them may even like it.

But for the rest of us, who would prefer not to “own nothing and be happy”, it’s imperative that you have zero reliance on government subsidies, entitlements or support payments.

If you haven’t already:

- Start a business. (Even a kitchen table business or an online venture)

- Start stacking sats (Bitcoin) – get off zero, today.

- Start taking sats at your business.

If you already own or run a business, buy, start or invest in another one.

It’s going to get a lot more expensive to be free. It’s not right or fair, but that doesn’t matter.

The good news is there’s never been a better time in history to learn, create, innovate and grow and these are the dynamics and incentives that will ultimately prevail. We’re in a period of Peak Collectivism and Peak Centralization now (for the next few years). This dominating ideology is ultimately an anti-human philosophy and this too shall pass.

Be ready for it, either way.

* * *

Follow me on Nostr , Gettr, or Twitter. For new pieces sent straight to your inbox subscribe to the Bombthrower mailing list – and receive a free copy of our long term thesis on Monetary Regime Change. Our premium newsletter, The Bitcoin Capitalist, covers CBDCs, digital assets and publicly traded crypto stocks using a distinctly value oriented approach. Try it for $2.

Uncategorized

Fast-food chain closes restaurants after Chapter 11 bankruptcy

Several major fast-food chains recently have struggled to keep restaurants open.

Share this:

Competition in the fast-food space has been brutal as operators deal with inflation, consumers who are worried about the economy and their jobs and, in recent months, the falling cost of eating at home.

Add in that many fast-food chains took on more debt during the covid pandemic and that labor costs are rising, and you have a perfect storm of problems.

It's a situation where Restaurant Brands International (QSR) has suffered as much as any company.

Related: Wendy's menu drops a fan favorite item, adds something new

Three major Burger King franchise operators filed for bankruptcy in 2023, and the chain saw hundreds of stores close. It also saw multiple Popeyes franchisees move into bankruptcy, with dozens of locations closing.

RBI also stepped in and purchased one of its key franchisees.

"Carrols is the largest Burger King franchisee in the United States today, operating 1,022 Burger King restaurants in 23 states that generated approximately $1.8 billion of system sales during the 12 months ended Sept. 30, 2023," RBI said in a news release. Carrols also owns and operates 60 Popeyes restaurants in six states."

The multichain company made the move after two of its large franchisees, Premier Kings and Meridian, saw multiple locations not purchased when they reached auction after Chapter 11 bankruptcy filings. In that case, RBI bought select locations but allowed others to close.

Image source: Chen Jianli/Xinhua via Getty

Another fast-food chain faces bankruptcy problems

Bojangles may not be as big a name as Burger King or Popeye's, but it's a popular chain with more than 800 restaurants in eight states.

"Bojangles is a Carolina-born restaurant chain specializing in craveable Southern chicken, biscuits and tea made fresh daily from real recipes, and with a friendly smile," the chain says on its website. "Founded in 1977 as a single location in Charlotte, our beloved brand continues to grow nationwide."

Like RBI, Bojangles uses a franchise model, which makes it dependent on the financial health of its operators. The company ultimately saw all its Maryland locations close due to the financial situation of one of its franchisees.

Unlike. RBI, Bojangles is not public — it was taken private by Durational Capital Management LP and Jordan Co. in 2018 — which means the company does not disclose its financial information to the public.

That makes it hard to know whether overall softness for the brand contributed to the chain seeing its five Maryland locations after a Chapter 11 bankruptcy filing.

Bojangles has a messy bankruptcy situation

Even though the locations still appear on the Bojangles website, they have been shuttered since late 2023. The locations were operated by Salim Kakakhail and Yavir Akbar Durranni. The partners operated under a variety of LLCs, including ABS Network, according to local news channel WUSA9.

The station reported that the owners face a state investigation over complaints of wage theft and fraudulent W2s. In November Durranni and ABS Network filed for bankruptcy in New Jersey, WUSA9 reported.

"Not only do former employees say these men owe them money, WUSA9 learned the former owners owe the state, too, and have over $69,000 in back property taxes."

Former employees also say that the restaurant would regularly purchase fried chicken from Popeyes and Safeway when it ran out in their stores, the station reported.

Bojangles sent the station a comment on the situation.

"The franchisee is no longer in the Bojangles system," the company said. "However, it is important to note in your coverage that franchisees are independent business owners who are licensed to operate a brand but have autonomy over many aspects of their business, including hiring employees and payroll responsibilities."

Kakakhail and Durranni did not respond to multiple requests for comment from WUSA9.

bankruptcy pandemicUncategorized

Industrial Production Increased 0.1% in February

From the Fed: Industrial Production and Capacity Utilization

Industrial production edged up 0.1 percent in February after declining 0.5 percent in January. In February, the output of manufacturing rose 0.8 percent and the index for mining climbed 2.2 p…

Share this:

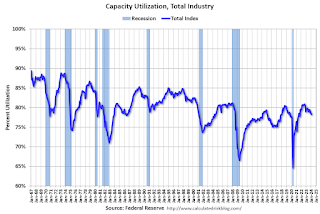

Industrial production edged up 0.1 percent in February after declining 0.5 percent in January. In February, the output of manufacturing rose 0.8 percent and the index for mining climbed 2.2 percent. Both gains partly reflected recoveries from weather-related declines in January. The index for utilities fell 7.5 percent in February because of warmer-than-typical temperatures. At 102.3 percent of its 2017 average, total industrial production in February was 0.2 percent below its year-earlier level. Capacity utilization for the industrial sector remained at 78.3 percent in February, a rate that is 1.3 percentage points below its long-run (1972–2023) average.Click on graph for larger image.

emphasis added

This graph shows Capacity Utilization. This series is up from the record low set in April 2020, and above the level in February 2020 (pre-pandemic).

Capacity utilization at 78.3% is 1.3% below the average from 1972 to 2022. This was below consensus expectations.

Note: y-axis doesn't start at zero to better show the change.

The second graph shows industrial production since 1967.

The second graph shows industrial production since 1967.Industrial production increased to 102.3. This is above the pre-pandemic level.

Industrial production was above consensus expectations.

Uncategorized

Southwest and United Airlines have bad news for passengers

Both airlines are facing the same problem, one that could lead to higher airfares and fewer flight options.

Share this:

{kind=link}

{kind=link}

Airlines operate in a market that's dictated by supply and demand: If more people want to fly a specific route than there are available seats, then tickets on those flights cost more.

That makes scheduling and predicting demand a huge part of maximizing revenue for airlines. There are, however, numerous factors that go into how airlines decide which flights to put on the schedule.

Related: Major airline faces Chapter 11 bankruptcy concerns

Every airport has only a certain number of gates, flight slots and runway capacity, limiting carriers' flexibility. That's why during times of high demand — like flights to Las Vegas during Super Bowl week — do not usually translate to airlines sending more planes to and from that destination.

Airlines generally do try to add capacity every year. That's become challenging as Boeing has struggled to keep up with demand for new airplanes. If you can't add airplanes, you can't grow your business. That's caused problems for the entire industry.

Every airline retires planes each year. In general, those get replaced by newer, better models that offer more efficiency and, in most cases, better passenger amenities.

If an airline can't get the planes it had hoped to add to its fleet in a given year, it can face capacity problems. And it's a problem that both Southwest Airlines (LUV) and United Airlines have addressed in a way that's inevitable but bad for passengers.

Image source: Kevin Dietsch/Getty Images

Southwest slows down its pilot hiring

In 2023, Southwest made a huge push to hire pilots. The airline lost thousands of pilots to retirement during the covid pandemic and it needed to replace them in order to build back to its 2019 capacity.

The airline successfully did that but will not continue that trend in 2024.

"Southwest plans to hire approximately 350 pilots this year, and no new-hire classes are scheduled after this month," Travel Weekly reported. "Last year, Southwest hired 1,916 pilots, according to pilot recruitment advisory firm Future & Active Pilot Advisors. The airline hired 1,140 pilots in 2022."

The slowdown in hiring directly relates to the airline expecting to grow capacity only in the low-single-digits percent in 2024.

"Moving into 2024, there is continued uncertainty around the timing of expected Boeing deliveries and the certification of the Max 7 aircraft. Our fleet plans remain nimble and currently differs from our contractual order book with Boeing," Southwest Airlines Chief Financial Officer Tammy Romo said during the airline's fourth-quarter-earnings call.

"We are planning for 79 aircraft deliveries this year and expect to retire roughly 45 700 and 4 800, resulting in a net expected increase of 30 aircraft this year."

That's very modest growth, which should not be enough of an increase in capacity to lower prices in any significant way.

United Airlines pauses pilot hiring

Boeing's (BA) struggles have had wide impact across the industry. United Airlines has also said it was going to pause hiring new pilots through the end of May.

United (UAL) Fight Operations Vice President Marc Champion explained the situation in a memo to the airline's staff.

"As you know, United has hundreds of new planes on order, and while we remain on path to be the fastest-growing airline in the industry, we just won't grow as fast as we thought we would in 2024 due to continued delays at Boeing," he said.

"For example, we had contractual deliveries for 80 Max 10s this year alone, but those aircraft aren't even certified yet, and it's impossible to know when they will arrive."

That's another blow to consumers hoping that multiple major carriers would grow capacity, putting pressure on fares. Until Boeing can get back on track, it's unlikely that competition between the large airlines will lead to lower fares.

In fact, it's possible that consumer demand will grow more than airline capacity which could push prices higher.

Related: Veteran fund manager picks favorite stocks for 2024

bankruptcy pandemic stocks

Key shipping company files for Chapter 11 bankruptcy

Pharma industry reputation remains steady at a ‘new normal’ after Covid, Harris Poll finds

These Cities Have The Highest (And Lowest) Share Of Unaffordable Neighborhoods In 2024

Tight inventory and frustrated buyers challenge agents in Virginia

Part 1: Current State of the Housing Market; Overview for mid-March 2024

The Question You Should Ask Whenever You’re Wrong

Walmart and Target make key self-checkout changes to fight theft

Industrial Production Increased 0.1% in February

Key shipping company files Chapter 11 bankruptcy

The best real estate coaching programs for 2024

-

Uncategorized3 weeks ago

Uncategorized3 weeks agoAll Of The Elements Are In Place For An Economic Crisis Of Staggering Proportions

-

International1 week ago

International1 week agoEyePoint poaches medical chief from Apellis; Sandoz CFO, longtime BioNTech exec to retire

-

Uncategorized4 weeks ago

Uncategorized4 weeks agoCalifornia Counties Could Be Forced To Pay $300 Million To Cover COVID-Era Program

-

Uncategorized3 weeks ago

Uncategorized3 weeks agoApparel Retailer Express Moving Toward Bankruptcy

-

Uncategorized4 weeks ago

Uncategorized4 weeks agoIndustrial Production Decreased 0.1% in January

-

International1 week ago

International1 week agoWalmart launches clever answer to Target’s new membership program

-

Spread & Containment2 days ago

Spread & Containment2 days agoIFM’s Hat Trick and Reflections On Option-To-Buy M&A

-

Uncategorized4 weeks ago

Uncategorized4 weeks agoRFK Jr: The Wuhan Cover-Up & The Rise Of The Biowarfare-Industrial Complex