“Record Market Fragility”: Something Snapped In Q1… And What Goldman Expects For Q2

"Record Market Fragility": Something Snapped In Q1… And What Goldman Expects For Q2

As Goldman trader and head of HF sales Tony Pasquariello writes in his first quarter post-mortem, "Q1 is done. boring, it was not."

And, boy, can say that.

Share this:

As Goldman trader and head of HF sales Tony Pasquariello writes in his first quarter post-mortem, "Q1 is done. boring, it was not."

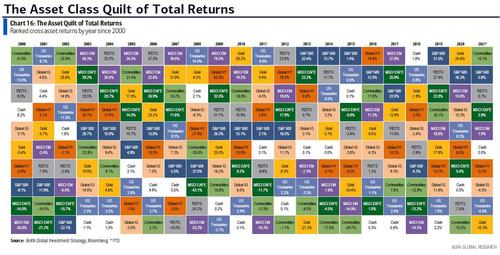

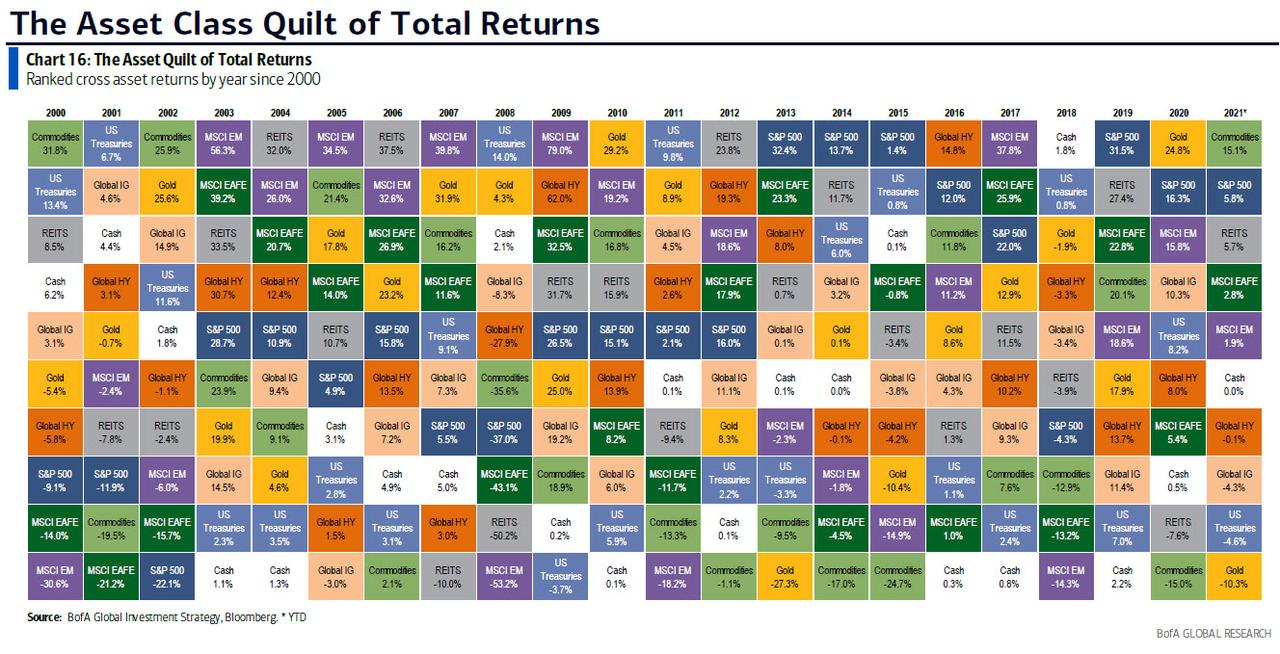

And, boy, can say that again... but before we get into the weeds of what happened (and what may happen) let's first take a look at the obvious - the best and worst performing assets of the past quarter.

Luckily, Deutsche Bank has done the analysis, and in a note from the bank's strategist Henry Allen, he writes that markets had a pretty mixed performance in Q1, with 20 of the 38 non-currency assets in the German bank's sample having a positive return over the first three months of the year. The gains concentrated among risk assets including equities, oil and HY credit, as progress on the vaccine rollout and the prospect of further stimulus in the US proved supportive. In a reversal of 2020 however, safe havens have struggled against this backdrop, with gold the worst-performing asset in the main sample (bitcoin was on the other end) and sovereign bonds also losing ground over the quarter.

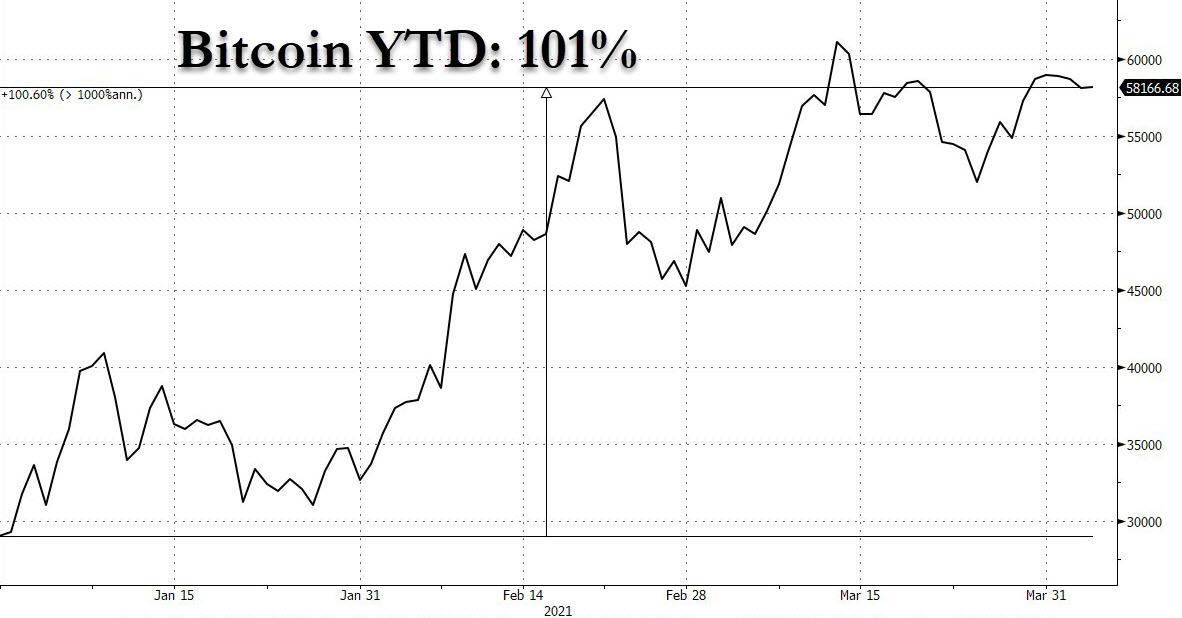

A quick detour here from BofA CIO Michael Hartnett, gives us the highlights in the form of the following performance: Bitcoin 103.3%, oil 21.9%, global stocks 4.7%, US$ 3.7%, cash 0.0%, HY bonds -0.1%, IG bonds -4.3%, government bonds -5.8%, gold -9.6% YTD.

Going back to DB, we are reminder that one of the biggest stories over Q1 has been the massive rise in US Treasury yields. This began at the very start of the year as the results of the Georgia Senate runoffs meant that the Democrats would have control of both houses of Congress under the new Biden administration. In turn, this has given them the leeway to pursue substantial stimulus, with the $1.9tn American Rescue Plan already signed into law, and Biden announcing his American Jobs Plan yesterday. In response, yields on 10yr Treasuries have risen by +82.7bps over the quarter, which is the largest rise in absolute terms since Q4 2016 when Donald Trump unexpectedly won the presidency.

However, the selloff in sovereign bonds hasn’t been confined to the US, with their European counterparts also losing ground as investors increasingly bet on a stronger economic recovery once the vaccine is rolled out. Gilts (-7.3%), bunds (- 2.4%) and BTPs (-0.9%) all fell over the quarter, though their monthly performance for March hasn’t been quite as bad, with only bunds losing ground slightly.

On the other end, for equities, both March and Q1 marked a very strong performance, and in a major reversal from 2020, it was European indices which saw the largest advances. Over Q1, the DAX (+9.4%), the FTSE MIB (+11.3%) and the STOXX 600 (+8.4%) all saw solid gains in total return terms, while banks led the way thanks to higher yields, with the STOXX 600 Banks up +20.3% over the quarter. The US lagged behind however, with the S&P 500 up +6.2%, albeit rising to fresh highs in March, while EM indices were even further back, with the MSCI EM Equities up just +2.2% over the last three months.

Of course, nothing compares to bitcoin, which has exactly doubled since the start of the year...

... but away from crypto, the top performing asset continues to be oil on a YTD basis, with a Q1 performance of +22.7% for Brent Crude and +21.9% for WTI. Oil is still in the lead in spite of the fact that both prices fell over the last month, as concerns over a rise in Covid cases at the global level led to renewed fears about further restrictions and reductions in mobility. Nevertheless, while oil is at the top of the DB YTD sample, other commodities haven’t performed so well, with precious metals the worst, in a mirror image of returns last year.

Bottom line, going back to Pasquariello, he puts it best saying that "on the surface, it was a fine quarter: S&P printed a 6.2% total return on 7.8% realized volatility, and sits within close reach of both the highs and the 4000 level." However, as the Goldman trader expands, "those headlines, belie the degree of difficulty involved in managing professional money along the path -- particularly within the fundamental long/short space."

To illustrate the turbulence below the surface, consider the following Q1 returns:

- the hedge fund VIP basket (GSTHHVIP) underperformed a basket of widely held shorts (GSCBMSAL) by ... 30%

- growth stocks (GSXUMFGL) underperformed value stocks (GSXUMFVL) by ... 28%.

- 52-week momentum winners (GSCBHMOM) underperformed 52-week momentum losers (GSCBLMOM) by ... 18%.

In working through the presumed drivers of these factor breaks, the Goldman trader points out the following key items:

- be it the 82bps backup in US 10-year note yields -- or the worst start to a year in the history of the aggregate index -- the bond market sold off hard, with that came an element of climate change for stock operators.

- on one hand, Q1 saw the largest inflows to equity funds on record; on the other hand, as the quarter progressed, some steam came out of the higher velocity vehicles (witness a clear decline in single stock call option volumes, recent outflows from ARKK, and some indigestion in certain corners of the new issue market). ZH discussed this one month ago in "Another Market Paradox: Wall Street Struggles To Explain Record Equity Inflows Amid Stock Turmoil"

- on the fundamental side, the fiscal story in Q1 was eye-popping; a $900bn rush in December was followed by a $1.84bn boomer in March. All of that was deficit financed. Meanwhile, as we learned last week, the next round - perhaps the final round - will be much more complicated with respect to funding and taxes.

If all that is a little abstract for some, here is BofA's CIO Michael Hartnett breaking down Q1 i) by the numbers; ii) by winners and losers and iii) by flows:

Q1 by the Numbers:

- 608MM global Covid-19 vaccinations,

- More than $4tn US fiscal stimulus,

- 200bps jump in US ’21 nominal GDP forecast to >8%,

- global stocks +$5tn in market cap,

- Value of negative-yielding global bonds drops $6tn,

- Worst Q1 return for 30-year Treasury since 1919,

- Worst Q1 for IG bonds since 1980,

- Worst Q1 for gold since 1982.

Q1 Winners & Losers:

- winners = cyclical stocks…energy stocks 29%, oil 22%, banks 23%, copper 13%;

- losers = bonds & duration…30yr UST -16%, gold -10%, EM LC bonds -8%, US IG bonds -6%, US biotech -4%;

- tighter financial conditions led to “events”, e.g. GME, Archegos…, but stocks (XHB +22%, XBD +16%) signal “good” rise in rates thus far.

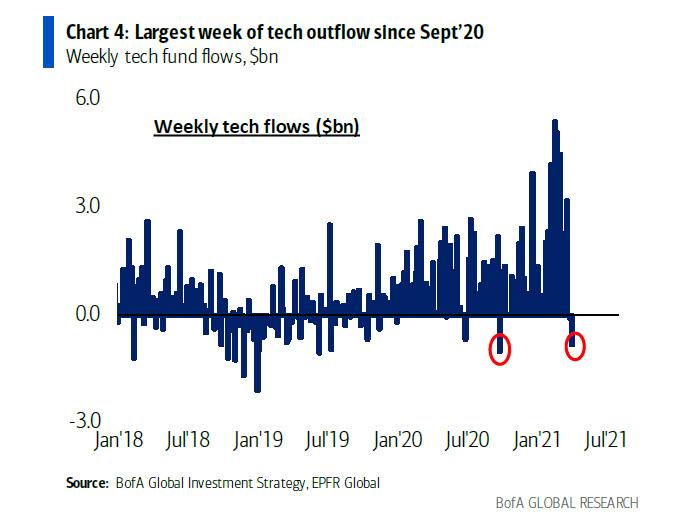

Q1 flows: record inflow to global equity ($372bn), EM ($65bn), value ($35bn), tech ($30bn), financials ($24bn); largest equity inflow % AUM (2.4% - Chart 3) in 15 years...

... although this appears to be reversing with the biggest tech outflows since Sept 2020:

Indeed, while superficially the broader markets rose, there was a tangible bifurcation within risk assets with catastrophic results for some traders.

Which brings us to the latest note from BofA derivatives strategist Benjamin Bowler, who in a note published last week, reverts to his favorite theme, namely that growing market fragility has made risk-taking extremely risky, despite the overall rise in markets.

As Bowler puts it, in words that could threaten to "cancel" him for being overly honest, "markets are fragile owing to extreme liquidity driving asset bubbles and trading liquidity drying up at record speed during times of stress." He then adds that "while an increasing number of people intuitively accept this fact, modelling this risk can be difficult, and underappreciating the nature of fragility can make risk-managing levered positions challenging. In part, this is because traditional volatility metrics woefully understate today’s still high PNL volatility among US stocks."

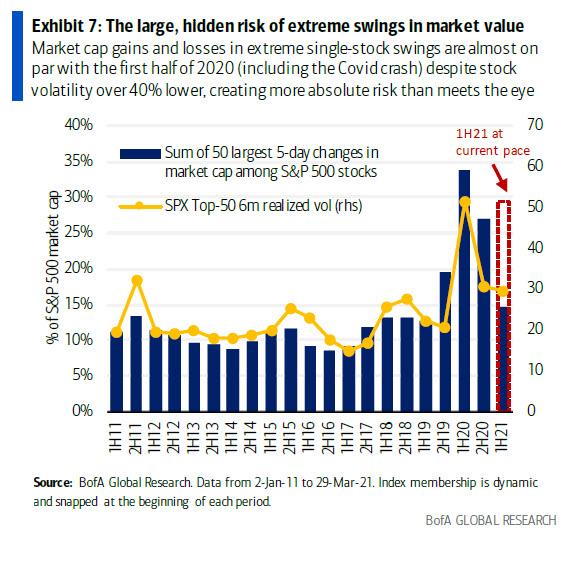

What does Bowler mean by this? Well, consider that as shown in the chart below, so far in 2021, the total market cap being gained or lost in extreme swings among S&P 500 stocks is nearly on par with that of the first half of 2020 (during the Covid crash), despite stock volatility being over 40% lower now.

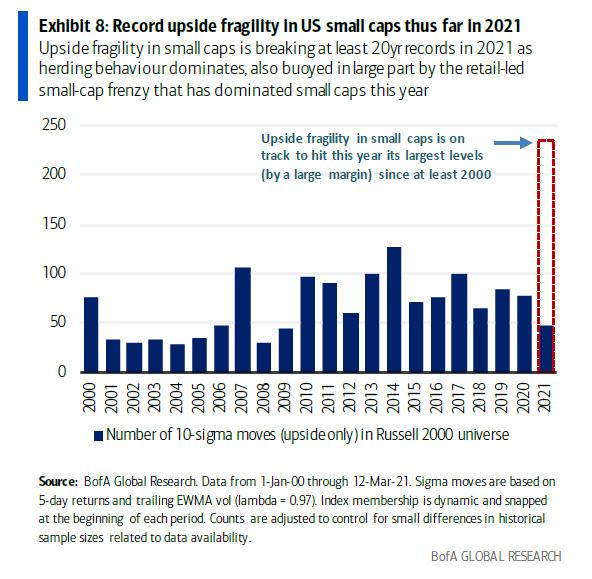

Notably, there were unprecedented, extreme swings among small cap stocks, which in Q1 set records with 80% more 10-sigma upside shocks this year than ever before according to BofA, which to Bowler illustrates that "there is more risk to managing risk than meets the eye."

In other words, something clearly snapped in the market's "reaction function" to a quarter that saw a gargantuan fiscal stimulus injected into the economy to make the already massive monetary stimulus.

This, in turn, takes us back to the conclusion from Goldman's Pasquariello, who summarizes his market sentiment as follows:

certain impulses changed as the quarter wore on, which presents a different setup for Q2. to be clear, if April and May are THE peak growth months for US economic activity -- perhaps as robust as anything we'll see in the remainder of our careers, -- there's still a lot to play for.

It perhaps not surprising then that looking ahead, one of Goldman's top traders believes that "a reflationary framework is the right place to anchor your risk-taking" although there are a few key caveats:

I'm trying to balance that anchor point against an instinct that liquidity dynamics - and the trading environment - are changing. If that's all mostly correct, the path higher from here is apt to be choppier and risk/reward is not what it was four or five months ago. in practical terms, this argues for a more tactical trading stance where illiquid positions - and recency bias - are the enemy.

That said, in his final point, Pasquariello writes that if he is wrong on the view that risk/reward is a bit more balanced now, he thinks it will be on the right tail. as the US quickly moves towards herd immunity. In other words, he expects a blow off top in risk assets, due to the following three data points:

- i. $4.44tr currently sits in US money market funds ($1.5tr is held by retail, $2.94tr is held by institutions). since February of 2020, that $4.44tr pile has grown by … $830bn.

- ii. US households have accumulated about $1.5tn in 'excess' or 'forced' savings, and Goldman expects that to rise to about $2.4tn, or 11% of GDP, by the time that normal economic life is restored around mid-year

- iii. attendant to the largest jump in US consumer confidence in 18 years: a record share of respondents said they plan to purchase a home in the coming months. a measure of consumers' plans to buy cars and major appliances also rose. a separate report Tuesday showed U.S. home prices surged to the highest since February 2006.

Pasquariello then shares several "must see" charts (profiled earlier), which also includes the long-term chart of the 30Y TSY, which to the Goldman trader is "the most interesting chart on planet earth right now."

Read the full post here.

Spread & Containment

Another beloved brewery files Chapter 11 bankruptcy

The beer industry has been devastated by covid, changing tastes, and maybe fallout from the Bud Light scandal.

Share this:

Before the covid pandemic, craft beer was having a moment. Most cities had multiple breweries and taprooms with some having so many that people put together the brewery version of a pub crawl.

It was a period where beer snobbery ruled the day and it was not uncommon to hear bar patrons discuss the makeup of the beer the beer they were drinking. This boom period always seemed destined for failure, or at least a retraction as many markets seemed to have more craft breweries than they could support.

Related: Fast-food chain closes more stores after Chapter 11 bankruptcy

The pandemic, however, hastened that downfall. Many of these local and regional craft breweries counted on in-person sales to drive their business.

And while many had local and regional distribution, selling through a third party comes with much lower margins. Direct sales drove their business and the pandemic forced many breweries to shut down their taprooms during the period where social distancing rules were in effect.

During those months the breweries still had rent and employees to pay while little money was coming in. That led to a number of popular beermakers including San Francisco's nationally-known Anchor Brewing as well as many regional favorites including Chicago’s Metropolitan Brewing, New Jersey’s Flying Fish, Denver’s Joyride Brewing, Tampa’s Zydeco Brew Werks, and Cleveland’s Terrestrial Brewing filing bankruptcy.

Some of these brands hope to survive, but others, including Anchor Brewing, fell into Chapter 7 liquidation. Now, another domino has fallen as a popular regional brewery has filed for Chapter 11 bankruptcy protection.

Image source: Shutterstock

Covid is not the only reason for brewery bankruptcies

While covid deserves some of the blame for brewery failures, it's not the only reason why so many have filed for bankruptcy protection. Overall beer sales have fallen driven by younger people embracing non-alcoholic cocktails, and the rise in popularity of non-beer alcoholic offerings,

Beer sales have fallen to their lowest levels since 1999 and some industry analysts

"Sales declined by more than 5% in the first nine months of the year, dragged down not only by the backlash and boycotts against Anheuser-Busch-owned Bud Light but the changing habits of younger drinkers," according to data from Beer Marketer’s Insights published by the New York Post.

Bud Light parent Anheuser Busch InBev (BUD) faced massive boycotts after it partnered with transgender social media influencer Dylan Mulvaney. It was a very small partnership but it led to a right-wing backlash spurred on by Kid Rock, who posted a video on social media where he chastised the company before shooting up cases of Bud Light with an automatic weapon.

Another brewery files Chapter 11 bankruptcy

Gizmo Brew Works, which does business under the name Roth Brewing Company LLC, filed for Chapter 11 bankruptcy protection on March 8. In its filing, the company checked the box that indicates that its debts are less than $7.5 million and it chooses to proceed under Subchapter V of Chapter 11.

"Both small business and subchapter V cases are treated differently than a traditional chapter 11 case primarily due to accelerated deadlines and the speed with which the plan is confirmed," USCourts.gov explained.

Roth Brewing/Gizmo Brew Works shared that it has 50-99 creditors and assets $100,000 and $500,000. The filing noted that the company does expect to have funds available for unsecured creditors.

The popular brewery operates three taprooms and sells its beer to go at those locations.

"Join us at Gizmo Brew Works Craft Brewery and Taprooms located in Raleigh, Durham, and Chapel Hill, North Carolina. Find us for entertainment, live music, food trucks, beer specials, and most importantly, great-tasting craft beer by Gizmo Brew Works," the company shared on its website.

The company estimates that it has between $1 and $10 million in liabilities (a broad range as the bankruptcy form does not provide a space to be more specific).

Gizmo Brew Works/Roth Brewing did not share a reorganization or funding plan in its bankruptcy filing. An email request for comment sent through the company's contact page was not immediately returned.

bankruptcy pandemic social distancing

Government

Walmart joins Costco in sharing key pricing news

The massive retailers have both shared information that some retailers keep very close to the vest.

Share this:

As we head toward a presidential election, the presumed candidates for both parties will look for issues that rally undecided voters.

The economy will be a key issue, with Democrats pointing to job creation and lowering prices while Republicans will cite the layoffs at Big Tech companies, high housing prices, and of course, sticky inflation.

The covid pandemic created a perfect storm for inflation and higher prices. It became harder to get many items because people getting sick slowed down, or even stopped, production at some factories.

Related: Popular mall retailer shuts down abruptly after bankruptcy filing

It was also a period where demand increased while shipping, trucking and delivery systems were all strained or thrown out of whack. The combination led to product shortages and higher prices.

You might have gone to the grocery store and not been able to buy your favorite paper towel brand or find toilet paper at all. That happened partly because of the supply chain and partly due to increased demand, but at the end of the day, it led to higher prices, which some consumers blamed on President Joe Biden's administration.

Biden, of course, was blamed for the price increases, but as inflation has dropped and grocery prices have fallen, few companies have been up front about it. That's probably not a political choice in most cases. Instead, some companies have chosen to lower prices more slowly than they raised them.

However, two major retailers, Walmart (WMT) and Costco, have been very honest about inflation. Walmart Chief Executive Doug McMillon's most recent comments validate what Biden's administration has been saying about the state of the economy. And they contrast with the economic picture being painted by Republicans who support their presumptive nominee, Donald Trump.

Image source: Joe Raedle/Getty Images

Walmart sees lower prices

McMillon does not talk about lower prices to make a political statement. He's communicating with customers and potential customers through the analysts who cover the company's quarterly-earnings calls.

During Walmart's fiscal-fourth-quarter-earnings call, McMillon was clear that prices are going down.

"I'm excited about the omnichannel net promoter score trends the team is driving. Across countries, we continue to see a customer that's resilient but looking for value. As always, we're working hard to deliver that for them, including through our rollbacks on food pricing in Walmart U.S. Those were up significantly in Q4 versus last year, following a big increase in Q3," he said.

He was specific about where the chain has seen prices go down.

"Our general merchandise prices are lower than a year ago and even two years ago in some categories, which means our customers are finding value in areas like apparel and hard lines," he said. "In food, prices are lower than a year ago in places like eggs, apples, and deli snacks, but higher in other places like asparagus and blackberries."

McMillon said that in other areas prices were still up but have been falling.

"Dry grocery and consumables categories like paper goods and cleaning supplies are up mid-single digits versus last year and high teens versus two years ago. Private-brand penetration is up in many of the countries where we operate, including the United States," he said.

Costco sees almost no inflation impact

McMillon avoided the word inflation in his comments. Costco (COST) Chief Financial Officer Richard Galanti, who steps down on March 15, has been very transparent on the topic.

The CFO commented on inflation during his company's fiscal-first-quarter-earnings call.

"Most recently, in the last fourth-quarter discussion, we had estimated that year-over-year inflation was in the 1% to 2% range. Our estimate for the quarter just ended, that inflation was in the 0% to 1% range," he said.

Galanti made clear that inflation (and even deflation) varied by category.

"A bigger deflation in some big and bulky items like furniture sets due to lower freight costs year over year, as well as on things like domestics, bulky lower-priced items, again, where the freight cost is significant. Some deflationary items were as much as 20% to 30% and, again, mostly freight-related," he added.

bankruptcy pandemic trumpGovernment

Walmart has really good news for shoppers (and Joe Biden)

The giant retailer joins Costco in making a statement that has political overtones, even if that’s not the intent.

Share this:

As we head toward a presidential election, the presumed candidates for both parties will look for issues that rally undecided voters.

The economy will be a key issue, with Democrats pointing to job creation and lowering prices while Republicans will cite the layoffs at Big Tech companies, high housing prices, and of course, sticky inflation.

The covid pandemic created a perfect storm for inflation and higher prices. It became harder to get many items because people getting sick slowed down, or even stopped, production at some factories.

Related: Popular mall retailer shuts down abruptly after bankruptcy filing

It was also a period where demand increased while shipping, trucking and delivery systems were all strained or thrown out of whack. The combination led to product shortages and higher prices.

You might have gone to the grocery store and not been able to buy your favorite paper towel brand or find toilet paper at all. That happened partly because of the supply chain and partly due to increased demand, but at the end of the day, it led to higher prices, which some consumers blamed on President Joe Biden's administration.

Biden, of course, was blamed for the price increases, but as inflation has dropped and grocery prices have fallen, few companies have been up front about it. That's probably not a political choice in most cases. Instead, some companies have chosen to lower prices more slowly than they raised them.

However, two major retailers, Walmart (WMT) and Costco, have been very honest about inflation. Walmart Chief Executive Doug McMillon's most recent comments validate what Biden's administration has been saying about the state of the economy. And they contrast with the economic picture being painted by Republicans who support their presumptive nominee, Donald Trump.

Image source: Joe Raedle/Getty Images

Walmart sees lower prices

McMillon does not talk about lower prices to make a political statement. He's communicating with customers and potential customers through the analysts who cover the company's quarterly-earnings calls.

During Walmart's fiscal-fourth-quarter-earnings call, McMillon was clear that prices are going down.

"I'm excited about the omnichannel net promoter score trends the team is driving. Across countries, we continue to see a customer that's resilient but looking for value. As always, we're working hard to deliver that for them, including through our rollbacks on food pricing in Walmart U.S. Those were up significantly in Q4 versus last year, following a big increase in Q3," he said.

He was specific about where the chain has seen prices go down.

"Our general merchandise prices are lower than a year ago and even two years ago in some categories, which means our customers are finding value in areas like apparel and hard lines," he said. "In food, prices are lower than a year ago in places like eggs, apples, and deli snacks, but higher in other places like asparagus and blackberries."

McMillon said that in other areas prices were still up but have been falling.

"Dry grocery and consumables categories like paper goods and cleaning supplies are up mid-single digits versus last year and high teens versus two years ago. Private-brand penetration is up in many of the countries where we operate, including the United States," he said.

Costco sees almost no inflation impact

McMillon avoided the word inflation in his comments. Costco (COST) Chief Financial Officer Richard Galanti, who steps down on March 15, has been very transparent on the topic.

The CFO commented on inflation during his company's fiscal-first-quarter-earnings call.

"Most recently, in the last fourth-quarter discussion, we had estimated that year-over-year inflation was in the 1% to 2% range. Our estimate for the quarter just ended, that inflation was in the 0% to 1% range," he said.

Galanti made clear that inflation (and even deflation) varied by category.

"A bigger deflation in some big and bulky items like furniture sets due to lower freight costs year over year, as well as on things like domestics, bulky lower-priced items, again, where the freight cost is significant. Some deflationary items were as much as 20% to 30% and, again, mostly freight-related," he added.

bankruptcy pandemic trump

Walmart launches clever answer to Target’s new membership program

EyePoint poaches medical chief from Apellis; Sandoz CFO, longtime BioNTech exec to retire

Wendy’s has a new deal for daylight savings time haters

Watch Live: President Biden Reminds Americans Just How Good They’ve Got It Thanks To Him

Catastrophic Risk: Investing and Business Implications

Racial and Ethnic Wealth Inequality in the Post‑Pandemic Era

Redefining Poverty: Towards a Transpartisan Approach

The Digest #187

When Military Rule Supplants Democracy

Dropping Like a Stone: ON RRP Take‑up in the Second Half of 2023

-

Uncategorized2 weeks ago

Uncategorized2 weeks agoAll Of The Elements Are In Place For An Economic Crisis Of Staggering Proportions

-

Uncategorized1 month ago

Uncategorized1 month agoCathie Wood sells a major tech stock (again)

-

Uncategorized3 weeks ago

Uncategorized3 weeks agoCalifornia Counties Could Be Forced To Pay $300 Million To Cover COVID-Era Program

-

Uncategorized2 weeks ago

Uncategorized2 weeks agoApparel Retailer Express Moving Toward Bankruptcy

-

Uncategorized3 weeks ago

Uncategorized3 weeks agoIndustrial Production Decreased 0.1% in January

-

International1 day ago

Walmart launches clever answer to Target’s new membership program

-

Uncategorized3 weeks ago

Uncategorized3 weeks agoRFK Jr: The Wuhan Cover-Up & The Rise Of The Biowarfare-Industrial Complex

-

Uncategorized3 weeks ago

Uncategorized3 weeks agoGOP Efforts To Shore Up Election Security In Swing States Face Challenges