International

Reasons For Scepticism About Nominal GDP Targeting

There has been an ongoing push for a switch to nominal GDP targeting by Market Monetarists and some mainstream allies. Although I agree that being able to hit a nominal GDP target would be attractive, it would also be attractive to have a yacht. There …

Share this:

One of the more approachable discussions of nominal GDP targeting is this discussion from Bullard from a few years ago: https://www.stlouisfed.org/publications/regional-economist/second-quarter-2019/bullard-nominal-gdp-targeting. I must confess that I read some of the nominal GDP targeting literature years ago, but have not kept abreast of the latest developments.

Yay For Abolishing the Business Cycle

The usual means of justifying a switch to nominal GDP targeting is to point to advantageous properties within in mainstream models. This requires one to take these models seriously, which I do not. However, it is easy to see that there would be theoretical advantages over inflation targeting — under a key assumption.

Let us assume that we can use monetary policy to achieve the following.

We can control the rate of nominal GDP growth.

We can control the rate of inflation.

Controlling nominal GDP growth implies that we are controlling gross domestic income. This means that we have stabilised gross incomes. This means that we have effectively abolished the business cycle.

Given a choice between stabilising inflation and abolishing the business cycle, I can see the attractions of the latter possibility. However, the last time mainstream economists promised that they could use the science of macroeconomics to abolish the business cycle — the 1960s — it did not work out well.

When we look at neoclassical models, they are built around the assumption that all markets clear in equilibrium — which includes forward markets. If the central bank is not happy with with a possible future path for the price of goods, it allegedly can change interest rates so that prices go where they are supposed to. (How exactly a central bank can set the policy rate based on expected prices without those prices being already determined in markets is one of those questions that neoclassicals prefer to avoid discussing.) This means that the central bank can enforce its objectives on the economy.

Neoclassicals switch between arguing that economic mathematical models are tentative but empirically sound to then demanding that policy be examined using models which imply implausible central bank powers. As such, we need to look at the empirical record and ask whether a different policy framework might have fared better.

Nominal GDP and Inflation Correlated

When we look at past cycles, we discover that both nominal GDP and inflation tend to be pro-cyclical. (If we define “inflation” as the change in the GDP deflator, nominal GDP growth and “inflation” are mechanically linked by real GDP growth. This means that the two time series are at least somewhat correlated — both rise and fall in a linked fashion.

The correlation is not perfect, the usual observation is that inflation lags the cycle, while nominal GDP is coincident with the business cycle (almost by definition). Although economists love discussing various theoretical “shocks,” it is very hard to find situations where inflation and nominal GDP go in opposite directions for anything other than short periods of time.

This means that there is not going to be a major difference in policy decisions in terms of dealing with large changes to the business cycle (e.g., recessions). Where one might see a difference is in cases where growth and inflation are steady — and only one variable differs from its target. We had such stability in the middle of the business cycles from 1990-2020, but that has not been the situation recently.

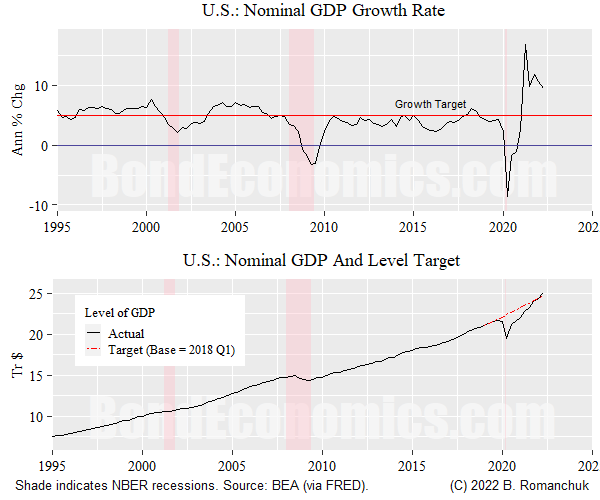

Level Targeting

One of bright ideas that Market Monetarists have been pushing is a level target — rather than trying to get the target variable to grow near a target level, instead there is a level target that grows at desired rate. That is, instead of hoping that nominal GDP growth is around 5%, we instead pick a reference level of nominal GDP, and grow that target by 5% per year.

This means that if we overshoot the desired growth rate, the level of the targeted time series will deviate from the target level. This implies the need for a corresponding overshoot of growth to erase the deficit. For example, imagine that the nominal GDP growth target grows by 5% per year, and we start out at the target level. If growth undershoots by 1% (4% growth), we would need 6% nominal GDP growth in the second year to erase the deviation — just returning to 5% growth is not enough.

The alleged advantage of this involves (surprise, surprise) expectations. If the policymakers commit to erasing deviations from target, this is supposed to affect behaviour so that the deviations will not be allowed to happen. (It works great in the models, trust me.)

Given my control engineering background and decent knowledge of modern economic history, such a policy framework is horrifying to me. Unless the expected return to target is drawn out extremely slowly, policymakers are committing to a policy of destabilising growth dynamics. For every deviation that happens, a corresponding “counter-deviation” has to happen. Any sort of inertia in the response to policy pretty much guarantees oscillatory deviations (assuming that central bankers were not impeached for raw incompetence, which is what one would expect to happen in the real world).

Meanwhile, if the time to erase deviations is stretched out to a long period, policymakers are effectively saying that they want a cycle that deviates from desired growth rates for an extended period. If there is a growth overshoot, they then want a long period of sluggishness to follow.

In any event, this resembles the rather disastrous policy stances of the inter-war Gold Standard. Policymakers forced through austerity policies in order to regain pre-World War gold parities, which did not help the brittle political economy of the period.

What Would Have Happened This Cycle?

It is very hard to see how using a nominal GDP target would have made a difference in this cycle. Both inflation and nominal GDP had a similar pattern — an undershoot of desired levels during the pandemic itself (oil futures prices going negative), coupled with an overshoot afterwards.

If the target were expressed as a target growth rate and not a level target (like most inflation targets now), then we would have had an unavoidable undershoot due to the pandemic restrictions, then the overshoot as restrictions reversed and stimulus hit. Although it might have been easier to believe that inflation would be “stickier” than nominal GDP growth and thus be more transitory, the extent of the nominal GDP overshoot we saw was obviously incompatible with either a nominal GDP or inflation target on a forward-looking basis.

If the target were expressed as a level, it is hard to see the attractions. In the figure above, I set a target nominal GDP level for the United States that grows at 5% per year, with a base year of 2018. The entire pandemic/post-pandemic trajectory just brings us back to target. The burst of inflation that was politically unpopular was literally what a level target objective implies is an “optimal” outcome.

Paging Goldilocks

In this current cycle, if policymakers were to hit either an inflation or nominal GDP target, they needed to steer the economy to the Goldilocks outcome: growth continued without causing inflationary bottlenecks. In places like Canada and the United States, there was considerable fiscal support to compensate for the enforced shutdowns. This meant that demand was supported while supply constrained, which implies bottlenecks. Although one could imagine that alternative policy frameworks could have resulted in better outcomes, those frameworks were not put in place in advance, and there was no way of organising them amid the administrative chaos.

Monetary policy — by conventional standards — was loose, and thus allegedly accentuated the fiscal stimulus. (Many MMTers will debate the effects of monetary policy.) The only way that the recent inflation spike would have been avoided if central bankers managed to fine tune monetary policy settings so that growth remained more moderate. (In my view, supply chain disruptions implied at least a transitory inflation spike, so I am not holding forth the possibility that inflation rates be perfectly on target — which some of the more extreme Market Monetarists insist that central banks can achieve.)

However, central banks were stuffed to the gills with neoclassical doctorates who gave us a consensus view that the inflation spike would be transitory. Even putting aside the effects of the Russian war of aggression, this was a serious forecast miss. If your massive teams of neoclassical economists blow their forecasts, it does not matter what objective you set for them: they are going to miss it.

Political Issues

Even if we grant there are some technical advantages for nominal GDP targeting, the main reason I do not take the policy seriously is that it has serious political disadvantages versus an inflation constraint of some form. (This could either be an inflation target, or a fuzzier objective that mixes an inflation goal with goals for employment or growth.) I will sketch out the argument here, since it is a subtext of my previous article discussing the political attractions of an inflation target.

The most important issue is that a nominal GDP growth target does not answer the question: why does a fiat currency have value in exchange? A currency peg offers a somewhat self-evident answer to that question — although if the peg is to another fiat currency, it raises some philosophical questions. An inflation target is a vague commitment to “peg” to the price of a basket of domestic consumer goods, which is understandable to everyone except the CPI conspiracy nutters. What does a nominal GDP target allow someone to buy?

James Bullard in his earlier linked article alluded to “communications issues,” which is what I am referring to. I write advanced popularisations of concepts in this area of economics, and I do not see any particularly exciting way to sell the policy.

The first barrier is that I would guess that a very small number of people understand what nominal GDP is. Although it is clear that many people do not understand the CPI either, they at least have a somewhat instinctive idea of what “inflation” is supposed to be. (The popularity of a certain website that adds 6% to US CPI inflation rates tells us that a lot of those people are innumerate.) We see a lot of references to GDP in financial/economic media, but it is typically real GDP, not nominal. Telling people that the central bank should drop worrying about inflation to target some economic concept that they have never heard of is a hard sell.

Shifting gears and saying that stabilising nominal GDP will have attractive properties runs into the question of why not target what you are actually interested in? If having stable nominal GDP means that inflation would be stable, why not target inflation and drop the indirection? Saying that you want to abolish the business cycle raises the question as to why not target a key business cycle indicator like unemployment? Why not be crazy and give the central bank a dual mandate like “maximum employment, stable prices” (and maybe even throw in “ moderate long-term interest rates”)?

Saying that CPI inflation rates are supposed to average 2% is meaningful for both households and firms. For households, it gives a guideline for financial planning. For firms, they generally cannot expect their output prices to deviate too far from 2% over extended periods. A nominal GDP target gives us very little information to most economic agents. Is the growth inflation or real? What will population growth be?

Although a 2% inflation target was somewhat arbitrary, a 5% (or whatever) nominal GDP target is even more arbitrary. The 1990-2020 period saw inflation run around 2% in most of the developed countries (Japan being a notable exception), and one can argue that it is low enough that it was not a political issue other than for the hard money nutters. There is no law of economic nature that determines the breakdown in nominal GDP growth — is 5% nominal growth the result of 1% real growth, 4% inflation, or 4% real growth, 1% inflation? Those two outcomes are going to be viewed in very different ways by politicians, while central bankers are supposed to be indifferent to them under a nominal GDP target.

Concluding Remarks

This treatment is brief because I do not view nominal GDP targeting to be politically viable. Mainstream economists are going to use the concept to publish papers, but it is going to be hard to convince people outside their in group. In the real world, people who have been paying attention have seen highly credentialled first claim to have abolished the business cycle (“the Great Moderation”) only to have them take desperate actions to save the financial system. (That financial fragility was courtesy of light touch regulation championed by prominent mainstream economists.) More recently, central bankers dropped the ball on their “transitory inflation” call. This is not a great environment to try to convince people that pretty much the exact same people are now going to micro-manage nominal GDP.

International

Angry Shouting Aside, Here’s What Biden Is Running On

Angry Shouting Aside, Here’s What Biden Is Running On

Last night, Joe Biden gave an extremely dark, threatening, angry State of the Union…

Share this:

Last night, Joe Biden gave an extremely dark, threatening, angry State of the Union address - in which he insisted that the American economy is doing better than ever, blamed inflation on 'corporate greed,' and warned that Donald Trump poses an existential threat to the republic.

But in between the angry rhetoric, he also laid out his 2024 election platform - for which additional details will be released on March 11, when the White House sends its proposed budget to Congress.

To that end, Goldman Sachs' Alec Phillips and Tim Krupa have summarized the key points:

Taxes

While railing against billionaires (nothing new there), Biden repeated the claim that anyone making under $400,000 per year won't see an increase in their taxes. He also proposed a 21% corporate minimum tax, up from 15% on book income outlined in the Inflation Reduction Act (IRA), as well as raising the corporate tax rate from 21% to 28% (which would promptly be passed along to consumers in the form of more inflation). Goldman notes that "Congress is unlikely to consider any of these proposals this year, they would only come into play in a second Biden term, if Democrats also won House and Senate majorities."

Biden once again tells the complete lie that "nobody earning less than $400,000/year will pay additional penny in federal taxes."

— RNC Research (@RNCResearch) March 8, 2024

FACT: Biden has *already* raised the tax burden on Americans making as little as $20,000 per year. pic.twitter.com/VrZ1m0rzG3

Biden also called on Congress to restore the pandemic-era child tax credit.

Immigration

Instead of simply passing a slew of border security Executive Orders like the Trump ones he shredded on day one, Biden repeated the lie that Congress 'needs to act' before he can (translation: send money to Ukraine or the US border will continue to be a sieve).

As immigration comes into even greater focus heading into the election, we continue to expect the Administration to tighten policy (e.g., immigration has surged 20pp the last 7 months to first place with 28% in Gallup’s “most important problem” survey). As such, we estimate the foreign-born contribution to monthly labor force growth will moderate from 110k/month in 2023 to around 70-90k/month in 2024. -GS

SEE IT: Biden gets boo-ed while talking about his immigration bill. WATCH pic.twitter.com/O5FmkYx3xM

— Simon Ateba (@simonateba) March 8, 2024

Ukraine

Biden, with House Speaker Mike Johnson doing his best impression of a bobble-head, urged Congress to pass additional assistance for Ukraine based entirely on the premise that Russia 'won't stop' there (and would what, trigger article 5 and WW3 no matter what?), despite the fact that Putin explicitly told Tucker Carlson he has no further ambitions, and in fact seeks a settlement.

‼️ Breaking: Putin wants a negotiated settlement to what’s happening in Ukraine.

— Ed (@EdMagari) February 9, 2024

In a surprising turn of events, Tucker Carlson could be the key to peace, potentially playing a crucial role in ending the current conflict????️ pic.twitter.com/IKN8ajlEUX

As Goldman estimates, "While there is still a clear chance that such a deal could come together, for now there is no clear path forward for Ukraine aid in Congress."

China

Biden, forgetting about all the aggressive tariffs, suggested that Trump had been soft on China, and that he will stand up "against China's unfair economic practices" and "for peace and stability across the Taiwan Strait."

SOTU FACT CHECK:

— Wesley Hunt (@WesleyHuntTX) March 8, 2024

Biden claims we’re in a strong position to take on China.

No president in our lifetime has been WEAKER on China than Biden. pic.twitter.com/Y73JsIzmM3

Healthcare

Lastly, Biden proposed to expand drug price negotiations to 50 additional drugs each year (an increase from 20 outlined in the IRA), which Goldman said would likely require bipartisan support "even if Democrats controlled Congress and the White House," as such policies would likely be ineligible for the budget "reconciliation" process which has been used in previous years to pass the IRA and other major fiscal party when Congressional margins are just too thin.

So there you have it. With no actual accomplishments to speak of, Biden can only attack Trump, lie, and make empty promises.

International

United Airlines adds new flights to faraway destinations

The airline said that it has been working hard to "find hidden gem destinations."

Share this:

Since countries started opening up after the pandemic in 2021 and 2022, airlines have been seeing demand soar not just for major global cities and popular routes but also for farther-away destinations.

Numerous reports, including a recent TripAdvisor survey of trending destinations, showed that there has been a rise in U.S. traveler interest in Asian countries such as Japan, South Korea and Vietnam as well as growing tourism traction in off-the-beaten-path European countries such as Slovenia, Estonia and Montenegro.

Related: 'No more flying for you': Travel agency sounds alarm over risk of 'carbon passports'

As a result, airlines have been looking at their networks to include more faraway destinations as well as smaller cities that are growing increasingly popular with tourists and may not be served by their competitors.

Shutterstock

United brings back more routes, says it is committed to 'finding hidden gems'

This week, United Airlines (UAL) announced that it will be launching a new route from Newark Liberty International Airport (EWR) to Morocco's Marrakesh. While it is only the country's fourth-largest city, Marrakesh is a particularly popular place for tourists to seek out the sights and experiences that many associate with the country — colorful souks, gardens with ornate architecture and mosques from the Moorish period.

More Travel:

- A new travel term is taking over the internet (and reaching airlines and hotels)

- The 10 best airline stocks to buy now

- Airlines see a new kind of traveler at the front of the plane

"We have consistently been ahead of the curve in finding hidden gem destinations for our customers to explore and remain committed to providing the most unique slate of travel options for their adventures abroad," United's SVP of Global Network Planning Patrick Quayle, said in a press statement.

The new route will launch on Oct. 24 and take place three times a week on a Boeing 767-300ER (BA) plane that is equipped with 46 Polaris business class and 22 Premium Plus seats. The plane choice was a way to reach a luxury customer customer looking to start their holiday in Marrakesh in the plane.

Along with the new Morocco route, United is also launching a flight between Houston (IAH) and Colombia's Medellín on Oct. 27 as well as a route between Tokyo and Cebu in the Philippines on July 31 — the latter is known as a "fifth freedom" flight in which the airline flies to the larger hub from the mainland U.S. and then goes on to smaller Asian city popular with tourists after some travelers get off (and others get on) in Tokyo.

United's network expansion includes new 'fifth freedom' flight

In the fall of 2023, United became the first U.S. airline to fly to the Philippines with a new Manila-San Francisco flight. It has expanded its service to Asia from different U.S. cities earlier last year. Cebu has been on its radar amid growing tourist interest in the region known for marine parks, rainforests and Spanish-style architecture.

With the summer coming up, United also announced that it plans to run its current flights to Hong Kong, Seoul, and Portugal's Porto more frequently at different points of the week and reach four weekly flights between Los Angeles and Shanghai by August 29.

"This is your normal, exciting network planning team back in action," Quayle told travel website The Points Guy of the airline's plans for the new routes.

stocks pandemic south korea japan hong kong europeanInternational

Walmart launches clever answer to Target’s new membership program

The retail superstore is adding a new feature to its Walmart+ plan — and customers will be happy.

Share this:

{kind=link}

{kind=link}

{kind=link}

It's just been a few days since Target (TGT) launched its new Target Circle 360 paid membership plan.

The plan offers free and fast shipping on many products to customers, initially for $49 a year and then $99 after the initial promotional signup period. It promises to be a success, since many Target customers are loyal to the brand and will go out of their way to shop at one instead of at its two larger peers, Walmart and Amazon.

Related: Walmart makes a major price cut that will delight customers

And stop us if this sounds familiar: Target will rely on its more than 2,000 stores to act as fulfillment hubs.

This model is a proven winner; Walmart also uses its more than 4,600 stores as fulfillment and shipping locations to get orders to customers as soon as possible.

Sometimes, this means shipping goods from the nearest warehouse. But if a desired product is in-store and closer to a customer, it reduces miles on the road and delivery time. It's a kind of logistical magic that makes any efficiency lover's (or retail nerd's) heart go pitter patter.

Walmart rolls out answer to Target's new membership tier

Walmart has certainly had more time than Target to develop and work out the kinks in Walmart+. It first launched the paid membership in 2020 during the height of the pandemic, when many shoppers sheltered at home but still required many staples they might ordinarily pick up at a Walmart, like cleaning supplies, personal-care products, pantry goods and, of course, toilet paper.

It also undercut Amazon (AMZN) Prime, which costs customers $139 a year for free and fast shipping (plus several other benefits including access to its streaming service, Amazon Prime Video).

Walmart+ costs $98 a year, which also gets you free and speedy delivery, plus access to a Paramount+ streaming subscription, fuel savings, and more.

If that's not enough to tempt you, however, Walmart+ just added a new benefit to its membership program, ostensibly to compete directly with something Target now has: ultrafast delivery.

Target Circle 360 particularly attracts customers with free same-day delivery for select orders over $35 and as little as one-hour delivery on select items. Target executes this through its Shipt subsidiary.

We've seen this lightning-fast delivery speed only in snippets from Amazon, the king of delivery efficiency. Who better to take on Target, though, than Walmart, which is using a similar store-as-fulfillment-center model?

"Walmart is stepping up to save our customers even more time with our latest delivery offering: Express On-Demand Early Morning Delivery," Walmart said in a statement, just a day after Target Circle 360 launched. "Starting at 6 a.m., earlier than ever before, customers can enjoy the convenience of On-Demand delivery."

Walmart (WMT) clearly sees consumers' desire for near-instant delivery, which obviously saves time and trips to the store. Rather than waiting a day for your order to show up, it might be on your doorstep when you wake up.

Consumers also tend to spend more money when they shop online, and they remain stickier as paying annual members. So, to a growing number of retail giants, almost instant gratification like this seems like something worth striving for.

Related: Veteran fund manager picks favorite stocks for 2024

stocks pandemic mexico

Walmart launches clever answer to Target’s new membership program

EyePoint poaches medical chief from Apellis; Sandoz CFO, longtime BioNTech exec to retire

Catastrophic Risk: Investing and Business Implications

The Digest #187

Gather ’round the crystal ball: A multi-commodity outlook from PDAC 2024

Deterra Royalties half-yearly result: stable performance and growth Initiatives

Deflationary pressures in China – be careful what you wish for

Measuring Treasury Market Depth

GBPINR: Analysis and Projections for 2024

We Are Not On The 1970s Inflation Rollercoaster – Part Four

-

Uncategorized2 weeks ago

Uncategorized2 weeks agoAll Of The Elements Are In Place For An Economic Crisis Of Staggering Proportions

-

Uncategorized1 month ago

Uncategorized1 month agoCathie Wood sells a major tech stock (again)

-

Uncategorized3 weeks ago

Uncategorized3 weeks agoCalifornia Counties Could Be Forced To Pay $300 Million To Cover COVID-Era Program

-

Uncategorized2 weeks ago

Uncategorized2 weeks agoApparel Retailer Express Moving Toward Bankruptcy

-

Uncategorized3 weeks ago

Uncategorized3 weeks agoIndustrial Production Decreased 0.1% in January

-

International12 hours ago

Walmart launches clever answer to Target’s new membership program

-

Uncategorized3 weeks ago

Uncategorized3 weeks agoRFK Jr: The Wuhan Cover-Up & The Rise Of The Biowarfare-Industrial Complex

-

Uncategorized3 weeks ago

Uncategorized3 weeks agoGOP Efforts To Shore Up Election Security In Swing States Face Challenges