Government

Over 600 companies reporting earnings this week – primarily from tech, health care, industrials and energy

Over 600 companies reporting earnings this week – primarily from tech, health care, industrials and energy

Share this:

This week peak earnings season rolls on with over 600 companies set to report for Q1, we’re going to hear from a lot of names in the tech, pharma and industrials space in particular.

Today we’re also going to take a look at some energy companies out with earnings this week to see how they’ve been impacted by last week’s oil rout which is now extending into this week.

And lastly we end with some econ data to look out for this week, including Case-Shiller on Tuesday, Q1 GDP on Wednesday, and Jobless claims on Thursday.

First let’s start by recapping last week a bit.

Big Tech Reports

We had a couple of big tech and FAANG names kick off peak earnings season, starting with NFLX on Tuesday. Despite being a favored “stay at home” name, they missed bottom-line expectations by 8 cents a share, but slightly beat on revenues and the real clincher was global net subscriber additions which were almost double analysts expectations. Those came in at 15.8M vs. estimates of 8.2M. Neftlix said they expect subscriber numbers to peak this quarter and then slowly back off as lockdown mandates are lifted across the globe.

We also saw an impressive report from Intel which blew away analysts expectations for profits and revenues, partially on account of their client computing segment. Analysts had been predicting that INTC would benefit in the short term from people working from home, increasing the need for laptops and cloud computing power. However, this trend may not be as strong in Q2, with the company issuing guidance for Q2 that was lower than analysts’ estimates, and they gave no guidance for the second half of the year which has become a concerning trend this earnings season.

As you can see we’ve currently got a smart score of 9 for Intel, with every segment looking positive for now. The best performing analysts on TipRanks rate Intel as a moderate buy, with a price target of $62.81, 6% higher than where it stands now.

Despite the banks dragging down markets in the first half of the week, things were looking up Thursday and Friday as plans to reopen America emerged, and Gilead Sciences announced its antiviral medicine remdesivir was showing promise in combating COVID-19. It’s likely those are the headlines that will push investors this earnings season, instead of the earnings themselves, which might be a good thing for this rally.

US Housing Market

Housing numbers came in as badly as we thought they would last week, and even worse. Existing home sales reported their largest month-over-month (MoM) drop since November 2015, while New Home sales had their biggest MoM drop since July 2013. Sales were down in all regions, with the West being the hardest hit followed by the Northeast.

Gilead Sciences

We spoke about Gilead’s trials for their possible COVID-19 treatment, remdesiver, and since then we’ve gotten a lot of mixed news - first in the form of an FT article that reported trials for the drug in China showed it did not improve conditions for COVID-19 patients. The FT cited leaked World Health Organization documents as their source. Gilead followed up to say the results of that study are still “inconclusive” and the document contained “inappropriate characterizations.” We’ll wait to hear more from then when Gilead reports Thursday.

This week, now to transition to what we’ll be watching for, we get earnings results from a couple of other big names on the forefront of COVID-19 vaccines and treatments, Pfizer and Amgen.

Health Care

Pfizer is working on a vaccine in conjunction with BioNTech and was just cleared to start human testing this week in Germany and is expected to win US approval shortly. They’ve otherwise been mum on their vaccine, but when they report tomorrow we’ll be listening in for more details.

Pfizer currently earning a Smart Score of 10, overall analysts rating this a moderate buy, but the best performing analysts on our platform are actually call this a hold for now. The price target currently stands at $38.65.

Another health care name reporting this week that’s been picking up steam due to coronavirus related shutdowns is Teledoc. With most doctors only available for emergencies, most routine visits have been replaced by telemedicine, and Teledoc is a platform that facilitates these virtual visits.

The company said last month that it was "experiencing unprecedented daily visit volume.” Since coronavirus began to escalate in the US in March, Teledoc has seen demand shoot up to ~15k visits requested a day, up 50% from the weeks prior to that. Looks like telemedicine is here to stay.

Teledoc also with a Smart Score of 10, but with Return on Equity down over the last year. The most accurate analysts calling this a moderate buy, with a price target of $150.

Industrials

Also this week we hear from a handful of huge industrial names. Starting with Caterpillar out tomorrow, always seen as a bellwether of global growth. They are expected to report a YoY profit decline of 43%, and a revenue decline of 18% as it’s major end markets struggle. Roughly 45% of Caterpillar’s revenue comes from Energy & Transportation industries, followed closely by Construction industries at 38%.

CAT currently with a neutral score of 6.

But other industrials such as Honeywell and 3M have gotten a boost during this time. MMM out with earnings tomorrow, and Honeywell on Friday. Both of these companies, along with Owens & Minor have received Pentagon contracts to make 39M N95 masks for medical workers under the Defense Production Act, a contract that totals $133M. 3M has already done well, with their masks selling out everywhere and hard to find, but similar to CAT their end markets are in a rough place.

Because of this we see 3M has a Smart Score of 3 based on decreased hedge fund and insider activity, as well as concerning technicals. The best performing analysts calling this one a hold with a price target of $142.

And of course Industrials and Energy names go hand in hand. We start to get some results from energy companies this week, which will be interesting in the wake of last week’s oil volatility. On Monday we saw West Texas Intermediate (WTI) oil futures for May trade at negative prices for the first time ever, meaning traders holding oil futures were paying buyers to take it off their hands. US crude futures started to rise towards the end of the week however, as hopes began to mount that the US would adjust production to fit shrinking demand. But this morning oil is back down 25% on fears that storage will soon fill. Markets seem to be more optimistic tho on news of states planned reopenings.

The largest US Oil company, Exxon, reports Friday. As you can see they only have a Smart Score of 4, and the best analysts on our platform have them as a moderate sell right now.

Econ metrics out this week

Case-Shiller Home Price Index reports tomorrow and will give us an indication of how home prices were impacted for the month of February. This in many ways is more critical to consumer confidence than the stock market, as more Americans own homes than equities. Home prices are expected to be flat to slightly down for the next 12 - 18 months.

US Q1 GDP reports on Wednesday and estimates have been all over the map with the New York Fed’s Nowcast now clocking in at -0.4%. Many banks have been much harsher, Goldman Sachs for example anticipating the US economy has contracted 9% in Q1, with JP Morgan forecasting an even lower -10%.

Jobless Claims report on Thursday. Analysts expect that number to continue falling, but now that we’ve received another $484B injection in the Paycheck Protection Plan, we’ll want to focus on another reading… the continuing claims number which tracks how many people are currently receiving benefits. With more PPP funding that number should steadily drop as employees that were furloughed now can get back on the payroll.

Next week peak earnings season continues with over 700 companies expected to report for Q1.

The post Over 600 companies reporting earnings this week - primarily from tech, health care, industrials and energy appeared first on TipRanks Financial Blog.

Government

“I Can’t Even Save”: Americans Are Getting Absolutely Crushed Under Enormous Debt Load

"I Can’t Even Save": Americans Are Getting Absolutely Crushed Under Enormous Debt Load

While Joe Biden insists that Americans are doing great…

Share this:

While Joe Biden insists that Americans are doing great - suggesting in his State of the Union Address last week that "our economy is the envy of the world," Americans are being absolutely crushed by inflation (which the Biden admin blames on 'shrinkflation' and 'corporate greed'), and of course - crippling debt.

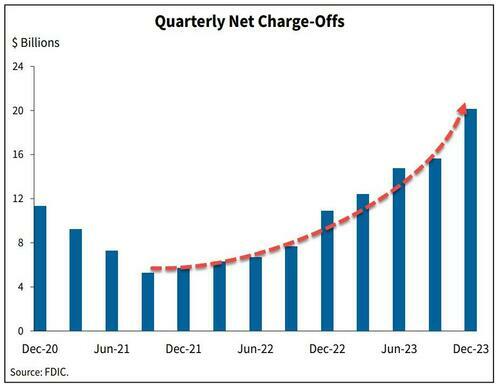

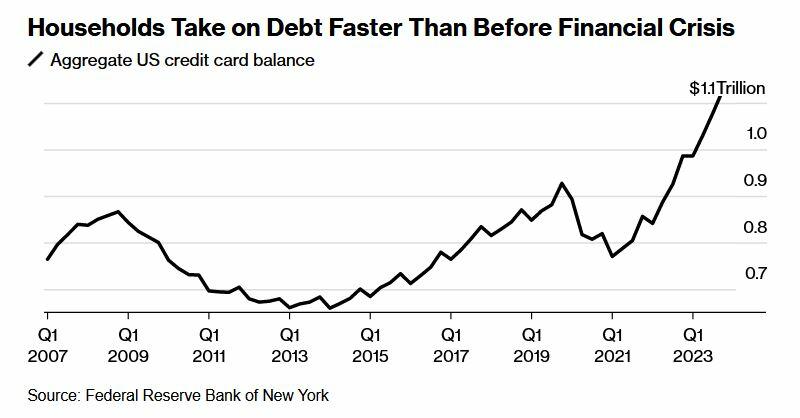

The signs are obvious. Last week we noted that banks' charge-offs are accelerating, and are now above pre-pandemic levels.

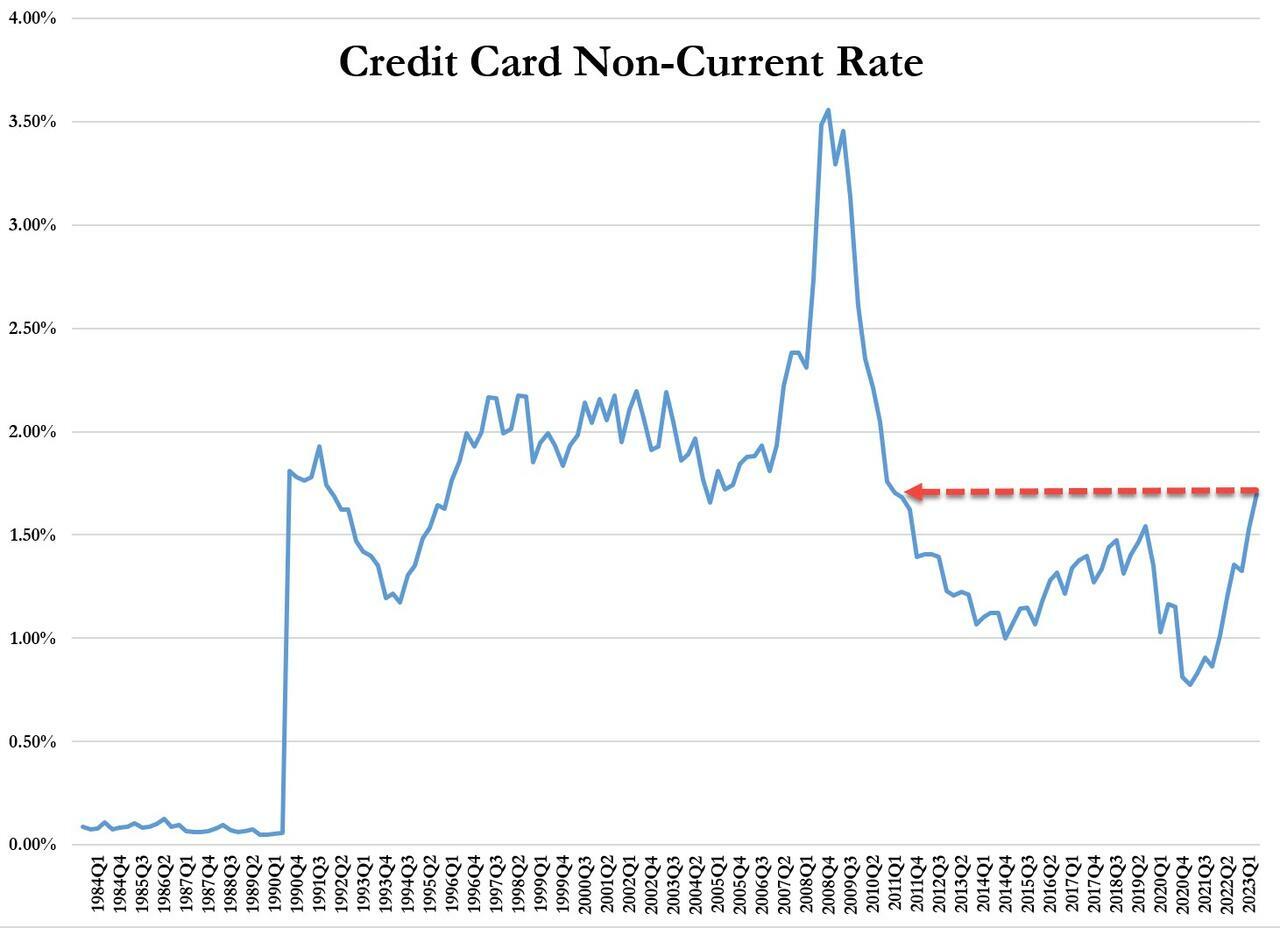

...and leading this increase are credit card loans - with delinquencies that haven't been this high since Q3 2011.

On top of that, while credit cards and nonfarm, nonresidential commercial real estate loans drove the quarterly increase in the noncurrent rate, residential mortgages drove the quarterly increase in the share of loans 30-89 days past due.

And while Biden and crew can spin all they want, an average of polls from RealClear Politics shows that just 40% of people approve of Biden's handling of the economy.

Crushed

On Friday, Bloomberg dug deeper into the effects of Biden's "envious" economy on Americans - specifically, how massive debt loads (credit cards and auto loans especially) are absolutely crushing people.

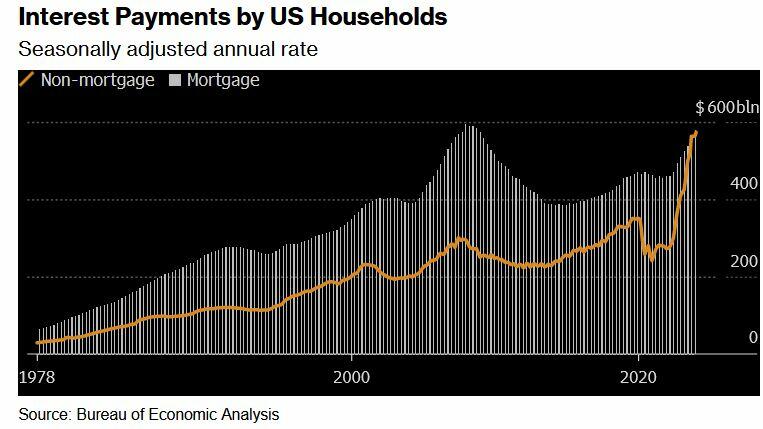

Two years after the Federal Reserve began hiking interest rates to tame prices, delinquency rates on credit cards and auto loans are the highest in more than a decade. For the first time on record, interest payments on those and other non-mortgage debts are as big a financial burden for US households as mortgage interest payments.

According to the report, this presents a difficult reality for millions of consumers who drive the US economy - "The era of high borrowing costs — however necessary to slow price increases — has a sting of its own that many families may feel for years to come, especially the ones that haven’t locked in cheap home loans."

The Fed, meanwhile, doesn't appear poised to cut rates until later this year.

According to a February paper from IMF and Harvard, the recent high cost of borrowing - something which isn't reflected in inflation figures, is at the heart of lackluster consumer sentiment despite inflation having moderated and a job market which has recovered (thanks to job gains almost entirely enjoyed by immigrants).

In short, the debt burden has made life under President Biden a constant struggle throughout America.

"I’m making the most money I've ever made, and I’m still living paycheck to paycheck," 40-year-old Denver resident Nikki Cimino told Bloomberg. Cimino is carrying a monthly mortgage of $1,650, and has $4,000 in credit card debt following a 2020 divorce.

"There's this wild disconnect between what people are experiencing and what economists are experiencing."

CBS: Do you attribute the inflation crisis to the pandemic or Biden?

— RNC Research (@RNCResearch) March 15, 2024

WISCONSIN VOTER: "It's been YEARS now since the pandemic — I'm not buying that anymore. At first I did; I'm not buying that anymore because yogurt is STILL going up in price!" pic.twitter.com/apahb65scB

What's more, according to Wells Fargo, families have taken on debt at a comparatively fast rate - no doubt to sustain the same lifestyle as low rates and pandemic-era stimmies provided. In fact, it only took four years for households to set a record new debt level after paying down borrowings in 2021 when interest rates were near zero.

Meanwhile, that increased debt load is exacerbated by credit card interest rates that have climbed to a record 22%, according to the Fed.

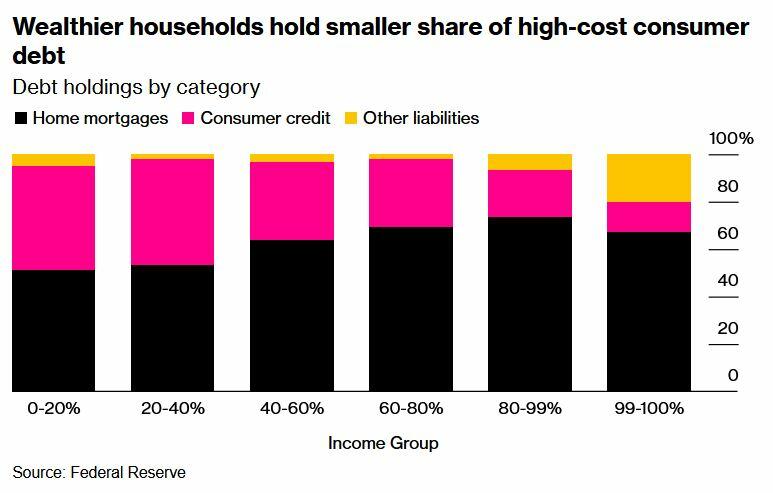

[P]art of the reason some Americans were able to take on a substantial load of non-mortgage debt is because they’d locked in home loans at ultra-low rates, leaving room on their balance sheets for other types of borrowing. The effective rate of interest on US mortgage debt was just 3.8% at the end of last year.

Yet the loans and interest payments can be a significant strain that shapes families’ spending choices. -Bloomberg

And of course, the highest-interest debt (credit cards) is hurting lower-income households the most, as tends to be the case.

The lowest earners also understandably had the biggest increase in credit card delinquencies.

"Many consumers are levered to the hilt — maxed out on debt and barely keeping their heads above water," Allan Schweitzer, a portfolio manager at credit-focused investment firm Beach Point Capital Management told Bloomberg. "They can dog paddle, if you will, but any uptick in unemployment or worsening of the economy could drive a pretty significant spike in defaults."

"We had more money when Trump was president," said Denise Nierzwicki, 69. She and her 72-year-old husband Paul have around $20,000 in debt spread across multiple cards - all of which have interest rates above 20%.

Photographer: Jon Cherry/Bloomberg

During the pandemic, Denise lost her job and a business deal for a bar they owned in their hometown of Lexington, Kentucky. While they applied for Social Security to ease the pain, Denise is now working 50 hours a week at a restaurant. Despite this, they're barely scraping enough money together to service their debt.

The couple blames Biden for what they see as a gloomy economy and plans to vote for the Republican candidate in November. Denise routinely voted for Democrats up until about 2010, when she grew dissatisfied with Barack Obama’s economic stances, she said. Now, she supports Donald Trump because he lowered taxes and because of his policies on immigration. -Bloomberg

Meanwhile there's student loans - which are not able to be discharged in bankruptcy.

"I can't even save, I don't have a savings account," said 29-year-old in Columbus, Ohio resident Brittany Walling - who has around $80,000 in federal student loans, $20,000 in private debt from her undergraduate and graduate degrees, and $6,000 in credit card debt she accumulated over a six-month stretch in 2022 while she was unemployed.

"I just know that a lot of people are struggling, and things need to change," she told the outlet.

The only silver lining of note, according to Bloomberg, is that broad wage gains resulting in large paychecks has made it easier for people to throw money at credit card bills.

Yet, according to Wells Fargo economist Shannon Grein, "As rates rose in 2023, we avoided a slowdown due to spending that was very much tied to easy access to credit ... Now, credit has become harder to come by and more expensive."

According to Grein, the change has posed "a significant headwind to consumption."

Then there's the election

"Maybe the Fed is done hiking, but as long as rates stay on hold, you still have a passive tightening effect flowing down to the consumer and being exerted on the economy," she continued. "Those household dynamics are going to be a factor in the election this year."

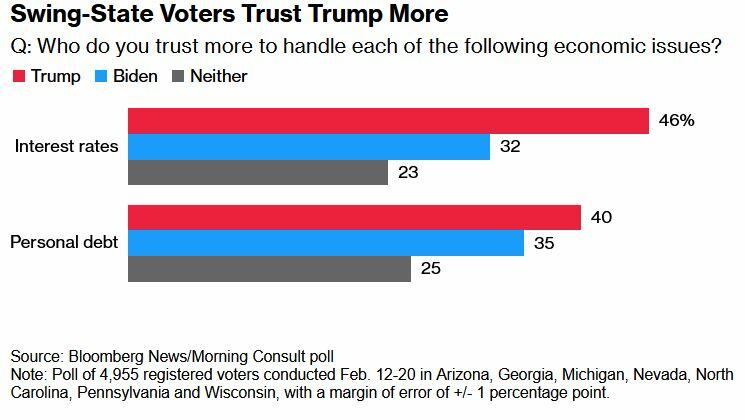

Meanwhile, swing-state voters in a February Bloomberg/Morning Consult poll said they trust Trump more than Biden on interest rates and personal debt.

Reverberations

These 'headwinds' have M3 Partners' Moshin Meghji concerned.

"Any tightening there immediately hits the top line of companies," he said, noting that for heavily indebted companies that took on debt during years of easy borrowing, "there's no easy fix."

International

Copper Soars, Iron Ore Tumbles As Goldman Says “Copper’s Time Is Now”

Copper Soars, Iron Ore Tumbles As Goldman Says "Copper’s Time Is Now"

After languishing for the past two years in a tight range despite recurring…

Share this:

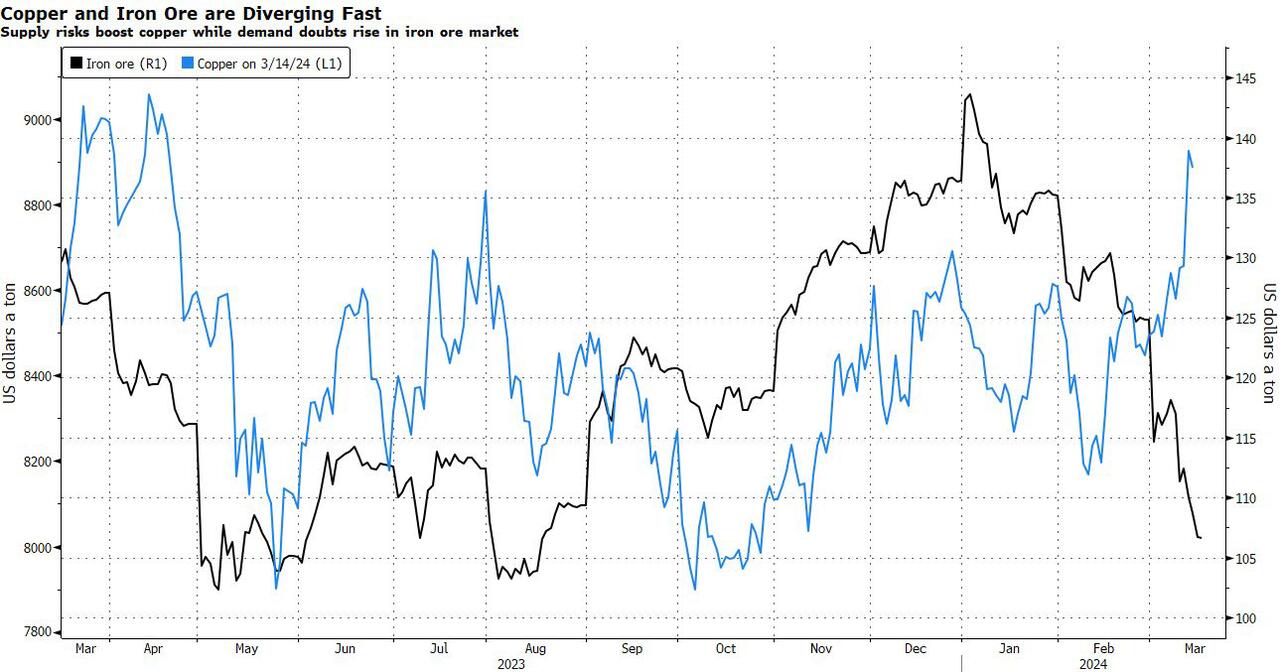

After languishing for the past two years in a tight range despite recurring speculation about declining global supply, copper has finally broken out, surging to the highest price in the past year, just shy of $9,000 a ton as supply cuts hit the market; At the same time the price of the world's "other" most important mined commodity has diverged, as iron ore has tumbled amid growing demand headwinds out of China's comatose housing sector where not even ghost cities are being built any more.

Copper surged almost 5% this week, ending a months-long spell of inertia, as investors focused on risks to supply at various global mines and smelters. As Bloomberg adds, traders also warmed to the idea that the worst of a global downturn is in the past, particularly for metals like copper that are increasingly used in electric vehicles and renewables.

Yet the commodity crash of recent years is hardly over, as signs of the headwinds in traditional industrial sectors are still all too obvious in the iron ore market, where futures fell below $100 a ton for the first time in seven months on Friday as investors bet that China’s years-long property crisis will run through 2024, keeping a lid on demand.

Indeed, while the mood surrounding copper has turned almost euphoric, sentiment on iron ore has soured since the conclusion of the latest National People’s Congress in Beijing, where the CCP set a 5% goal for economic growth, but offered few new measures that would boost infrastructure or other construction-intensive sectors.

As a result, the main steelmaking ingredient has shed more than 30% since early January as hopes of a meaningful revival in construction activity faded. Loss-making steel mills are buying less ore, and stockpiles are piling up at Chinese ports. The latest drop will embolden those who believe that the effects of President Xi Jinping’s property crackdown still have significant room to run, and that last year’s rally in iron ore may have been a false dawn.

Meanwhile, as Bloomberg notes, on Friday there were fresh signs that weakness in China’s industrial economy is hitting the copper market too, with stockpiles tracked by the Shanghai Futures Exchange surging to the highest level since the early days of the pandemic. The hope is that headwinds in traditional industrial areas will be offset by an ongoing surge in usage in electric vehicles and renewables.

And while industrial conditions in Europe and the US also look soft, there’s growing optimism about copper usage in India, where rising investment has helped fuel blowout growth rates of more than 8% — making it the fastest-growing major economy.

In any case, with the demand side of the equation still questionable, the main catalyst behind copper’s powerful rally is an unexpected tightening in global mine supplies, driven mainly by last year’s closure of a giant mine in Panama (discussed here), but there are also growing worries about output in Zambia, which is facing an El Niño-induced power crisis.

On Wednesday, copper prices jumped on huge volumes after smelters in China held a crisis meeting on how to cope with a sharp drop in processing fees following disruptions to supplies of mined ore. The group stopped short of coordinated production cuts, but pledged to re-arrange maintenance work, reduce runs and delay the startup of new projects. In the coming weeks investors will be watching Shanghai exchange inventories closely to gauge both the strength of demand and the extent of any capacity curtailments.

“The increase in SHFE stockpiles has been bigger than we’d anticipated, but we expect to see them coming down over the next few weeks,” Colin Hamilton, managing director for commodities research at BMO Capital Markets, said by phone. “If the pace of the inventory builds doesn’t start to slow, investors will start to question whether smelters are actually cutting and whether the impact of weak construction activity is starting to weigh more heavily on the market.”

* * *

Few have been as happy with the recent surge in copper prices as Goldman's commodity team, where copper has long been a preferred trade (even if it may have cost the former team head Jeff Currie his job due to his unbridled enthusiasm for copper in the past two years which saw many hedge fund clients suffer major losses).

As Goldman's Nicholas Snowdon writes in a note titled "Copper's time is now" (available to pro subscribers in the usual place)...

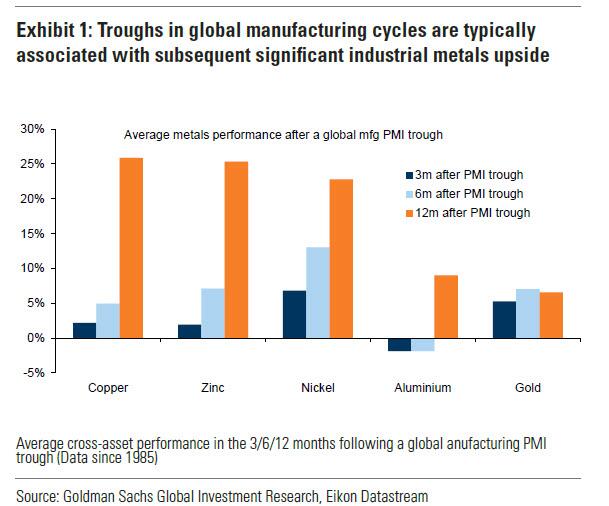

... there has been a "turn in the industrial cycle." Specifically according to the Goldman analyst, after a prolonged downturn, "incremental evidence now points to a bottoming out in the industrial cycle, with the global manufacturing PMI in expansion for the first time since September 2022." As a result, Goldman now expects copper to rise to $10,000/t by year-end and then $12,000/t by end of Q1-25.’

Here are the details:

Previous inflexions in global manufacturing cycles have been associated with subsequent sustained industrial metals upside, with copper and aluminium rising on average 25% and 9% over the next 12 months. Whilst seasonal surpluses have so far limited a tightening alignment at a micro level, we expect deficit inflexions to play out from quarter end, particularly for metals with severe supply binds. Supplemented by the influence of anticipated Fed easing ahead in a non-recessionary growth setting, another historically positive performance factor for metals, this should support further upside ahead with copper the headline act in this regard.

Goldman then turns to what it calls China's "green policy put":

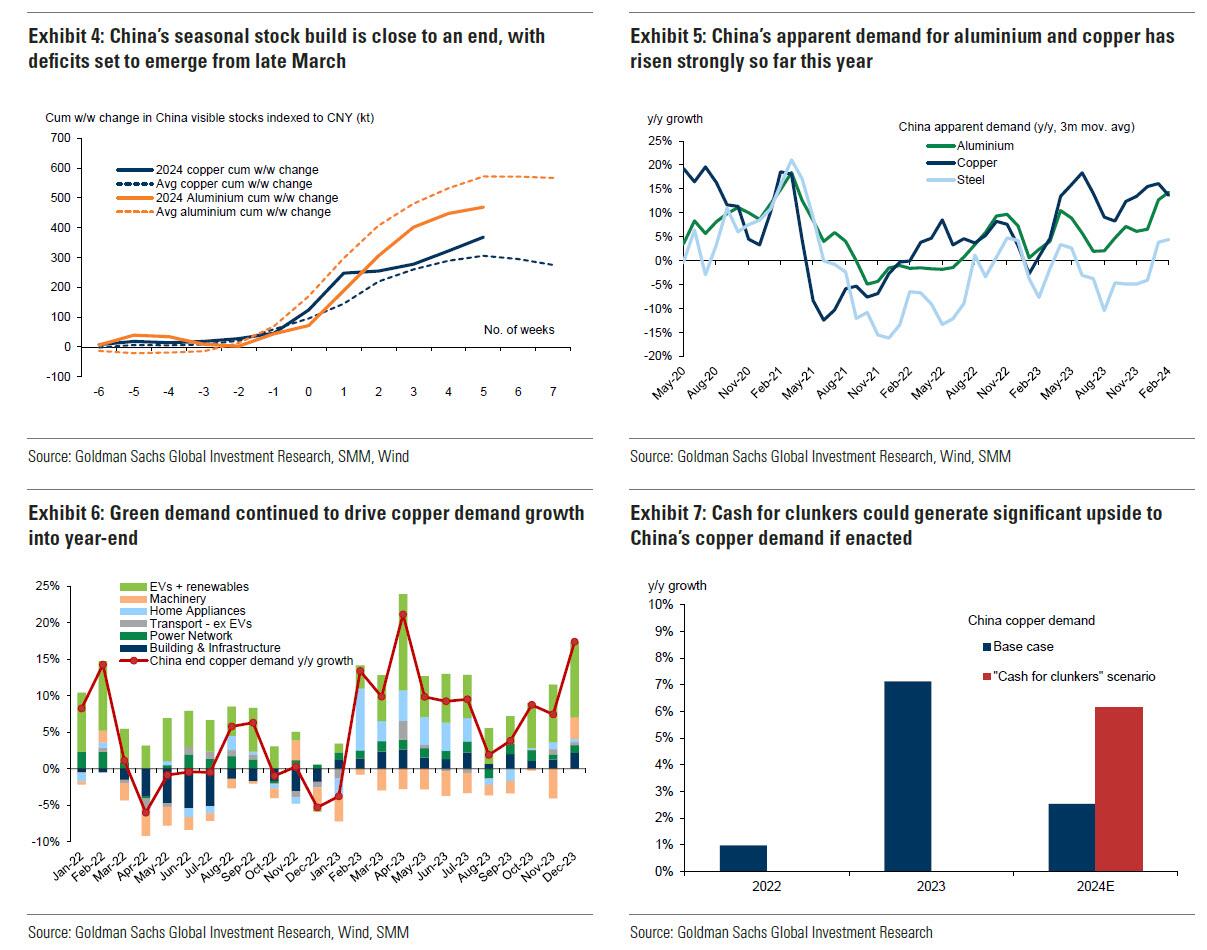

Much of the recent focus on the “Two Sessions” event centred on the lack of significant broad stimulus, and in particular the limited property support. In our view it would be wrong – just as in 2022 and 2023 – to assume that this will result in weak onshore metals demand. Beijing’s emphasis on rapid growth in the metals intensive green economy, as an offset to property declines, continues to act as a policy put for green metals demand. After last year’s strong trends, evidence year-to-date is again supportive with aluminium and copper apparent demand rising 17% and 12% y/y respectively. Moreover, the potential for a ‘cash for clunkers’ initiative could provide meaningful right tail risk to that healthy demand base case. Yet there are also clear metal losers in this divergent policy setting, with ongoing pressure on property related steel demand generating recent sharp iron ore downside.

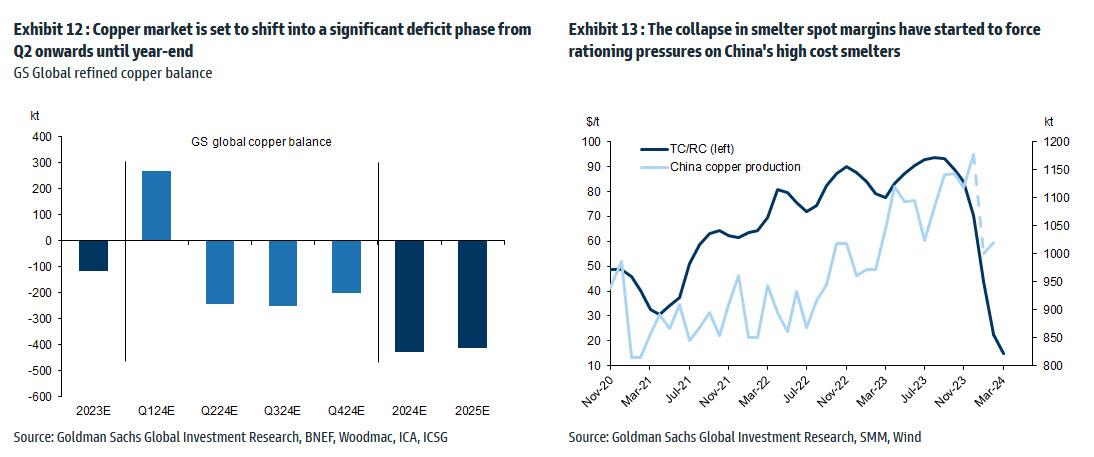

Meanwhile, Snowdon believes that the driver behind Goldman's long-running bullish view on copper - a global supply shock - continues:

Copper’s supply shock progresses. The metal with most significant upside potential is copper, in our view. The supply shock which began with aggressive concentrate destocking and then sharp mine supply downgrades last year, has now advanced to an increasing bind on metal production, as reflected in this week's China smelter supply rationing signal. With continued positive momentum in China's copper demand, a healthy refined import trend should generate a substantial ex-China refined deficit this year. With LME stocks having halved from Q4 peak, China’s imminent seasonal demand inflection should accelerate a path into extreme tightness by H2. Structural supply underinvestment, best reflected in peak mine supply we expect next year, implies that demand destruction will need to be the persistent solver on scarcity, an effect requiring substantially higher pricing than current, in our view. In this context, we maintain our view that the copper price will surge into next year (GSe 2025 $15,000/t average), expecting copper to rise to $10,000/t by year-end and then $12,000/t by end of Q1-25’

Another reason why Goldman is doubling down on its bullish copper outlook: gold.

The sharp rally in gold price since the beginning of March has ended the period of consolidation that had been present since late December. Whilst the initial catalyst for the break higher came from a (gold) supportive turn in US data and real rates, the move has been significantly amplified by short term systematic buying, which suggests less sticky upside. In this context, we expect gold to consolidate for now, with our economists near term view on rates and the dollar suggesting limited near-term catalysts for further upside momentum. Yet, a substantive retracement lower will also likely be limited by resilience in physical buying channels. Nonetheless, in the midterm we continue to hold a constructive view on gold underpinned by persistent strength in EM demand as well as eventual Fed easing, which should crucially reactivate the largely for now dormant ETF buying channel. In this context, we increase our average gold price forecast for 2024 from $2,090/toz to $2,180/toz, targeting a move to $2,300/toz by year-end.

Much more in the full Goldman note available to pro subs.

Government

Moderna turns the spotlight on long Covid with new initiatives

Moderna’s latest Covid effort addresses the often-overlooked chronic condition of long Covid — and encourages vaccination to reduce risks. A digital…

Share this:

{kind=link}

{kind=link}

Moderna’s latest Covid effort addresses the often-overlooked chronic condition of long Covid — and encourages vaccination to reduce risks. A digital campaign debuted Friday along with a co-sponsored event in Detroit offering free CT scans, which will also be used in ongoing long Covid research.

In a new video, a young woman describes her three-year battle with long Covid, which includes losing her job, coping with multiple debilitating symptoms and dealing with the negative effects on her family. She ends by saying, “The only way to prevent long Covid is to not get Covid” along with an on-screen message about where to find Covid-19 vaccines through the vaccines.gov website.

“Last season we saw people would get a flu shot, but they didn’t always get a Covid shot,” said Moderna’s Chief Brand Officer Kate Cronin. “People should get their flu shot, but they should also get their Covid shot. There’s no risk of long flu, but there is the risk of long-term effects of Covid.”

It’s Moderna’s “first effort to really sound the alarm,” she said, and the debut coincides with the second annual Long Covid Awareness Day.

An estimated 17.6 million Americans are living with long Covid, according to the latest CDC data. About four million of them are out of work because of the condition, resulting in an estimated $170 billion in lost wages.

While HHS anted up $45 million in grants last year to expand long Covid support initiatives along with public health campaigns, the condition is still often ignored and underfunded.

“It’s not just about the initial infection of Covid, but also if you get it multiple times, your risks goes up significantly,” Cronin said. “It’s important that people understand that.”

grants covid-19 cdc hhs

Sylvester researchers, collaborators call for greater investment in bereavement care

For-profit nursing homes are cutting corners on safety and draining resources with financial shenanigans − especially at midsize chains that dodge public scrutiny

“I Can’t Even Save”: Americans Are Getting Absolutely Crushed Under Enormous Debt Load

Problems After COVID-19 Vaccination More Prevalent Among Naturally Immune: Study

Trump nearly derailed democracy once − here’s what to watch out for in reelection campaign

‘Excess Mortality Skyrocketed’: Tucker Carlson and Dr. Pierre Kory Unpack ‘Criminal’ COVID Response

Looking Back At COVID’s Authoritarian Regimes

Moderna turns the spotlight on long Covid with new initiatives

Five Aerospace Investments to Buy as Wars Worsen Copy

Copper Soars, Iron Ore Tumbles As Goldman Says “Copper’s Time Is Now”

-

Uncategorized3 weeks ago

Uncategorized3 weeks agoAll Of The Elements Are In Place For An Economic Crisis Of Staggering Proportions

-

International1 week ago

International1 week agoEyePoint poaches medical chief from Apellis; Sandoz CFO, longtime BioNTech exec to retire

-

Uncategorized4 weeks ago

Uncategorized4 weeks agoCalifornia Counties Could Be Forced To Pay $300 Million To Cover COVID-Era Program

-

Uncategorized3 weeks ago

Uncategorized3 weeks agoApparel Retailer Express Moving Toward Bankruptcy

-

Uncategorized4 weeks ago

Uncategorized4 weeks agoIndustrial Production Decreased 0.1% in January

-

International1 week ago

International1 week agoWalmart launches clever answer to Target’s new membership program

-

Spread & Containment3 days ago

Spread & Containment3 days agoIFM’s Hat Trick and Reflections On Option-To-Buy M&A

-

Uncategorized4 weeks ago

Uncategorized4 weeks agoRFK Jr: The Wuhan Cover-Up & The Rise Of The Biowarfare-Industrial Complex