Government

Nasdaq Futures Surge Despite Vaccine Setback As Gamma Squeeze Continues

Nasdaq Futures Surge Despite Vaccine Setback As Gamma Squeeze Continues

Share this:

Global stocks and S&P futures struggled on Tuesday amid concerns over a Johnson & Johnson vaccine setback, which overshadowed Chinese trade data that pointed to a buoyant recovery, while yields dropped and the U.S. dollar edged away from a three-week low.

S&P 500 contracts were modestly in the red after falling as much as 0.6% after a late Monday report that Johnson & Johnson’s Covid-19 vaccine study has been paused due to an unexplained illness in a participant. BlackRock rose in pre-market trading after earnings beat estimates and assets under management surged to a record, while JPMorgan climbed after revenue and EPS topped expectations as a result of a massive reserve release.

However while the S&P was trading with fractional losses, Nasdaq futures were sharply higher again as the European open appears to have triggered a continuation of yesterday's gamma squeeze which sent the Nasdaq up as much as 4% in what many believe is another attempt by a Nasdaq whale such as SoftBank to squeeze shorts in either options or NQ futures, as we explained yesterday.

The MSCI world equity index, which tracks shares in nearly 50 countries, fell 0.1%. The Euro STOXX 600 fell 0.4% before trimming losses, with markets in Frankfurt, London and Paris mirroring its moves. It was last down 0.2%, on course to end three straight days of gains. The travel and leisure and autos sectors suffered, losing 1% and 0.3% respectively after heavier falls in early trading, after the J&J news spooked traders. Investors had seen the quick introduction of a vaccine as key to helping economies recover. J&J's move comes after AstraZeneca paused late-stage trials of its experimental vaccine in September, also due to a participant's unexplained illness.

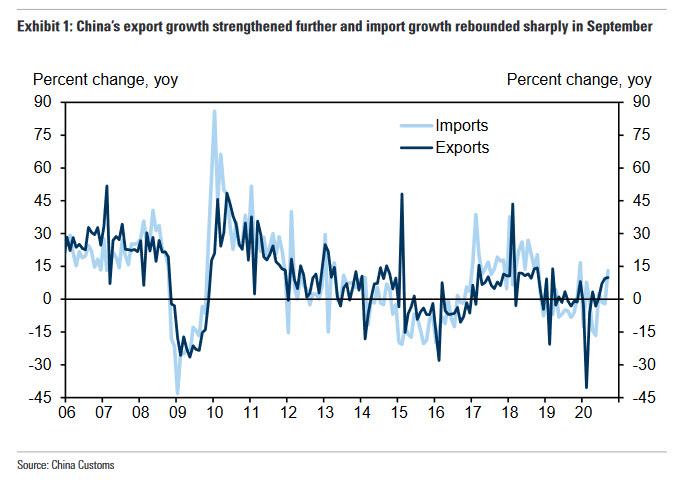

The risk-off mood contrasted with earlier resilience for Asian markets. They recovered losses after Chinese data showed exports rising 9.9% in September, in line with the 10% expected, while imports swung to a 13.2% gain, far higher than expected, versus a 2.1% drop in August.

The data, which suggests Chinese exporters are recovering from the pandemic’s damage to overseas orders, helped MSCI’s broadest index of Asia-Pacific shares outside Japan gain 0.2%. Chinese blue-chip shares added 0.3% after dipping early in the day. Some investors, though, raised questions about how strong consumer demand would prove to be.

"The question is not necessarily how China’s trade is doing per se, but how well will consumers spend on Christmas to give some sense of normalcy amid a period of great stress," said Nordea Investments’ Sebastien Galy, according to Reuters.

Currency traders were also watching Chinese trade-related issues. Reports that Beijing has stopped taking shipments of Australian coal caused the Australian dollar to drop as much as 0.6% to $0.7165.

In rates, treasuries flattened as cash trading resumes following Monday’s Fed-observed holiday; long-end yields were richer by ~2bps vs Friday’s close. These long-end-led gains flattened the 2s10s, 5s30s by ~1bp; 10-year yields down 1.7bp at 0.757% vs little-changed bunds and gilts. Government bond yields in the euro zone held near recent troughs, with hefty supply failing to dent a market bolstered by expectations for further central bank easing. Germany's 10-year Bund yield touched -0.538%, its lowest in just over a week. Italian and Greek benchmark 10-year debt both hit record lows.

Meanwhile, despite a total gridlock on fiscal stimulus, markets are now increasingly bulled up that Joe Biden will win the presidential election next month, which the narrative expects to lead to a big stimulus package to help the coronavirus-battered U.S. economy. “Biden effectively leading in the polls is removing some element of uncertainty,” said Jeremy Gatto, an investment manager at Unigestion in Geneva. “In investors’ minds, it’s not a question of if we get a stimulus, but when.”

“The hurdles at the moment come from the uncertainty around the U.S. election and the uncertainty about the timing and effectiveness of a vaccine,” Chris Iggo, chief investment officer at AXA IM Core Investments.

At the same time, many banks such as Goldman Sachs, expect a Biden win to undermine the U.S. dollar, since he's pledged to raise corporate tax rates. But the dollar rose 0.2% against a basket of other currencies to 93.214, trying to extend a rebound from Friday's near-three-week low of 92.997. The Chinese yuan fell 0.1% to 6.7466 per dollar after the central bank set a weaker-than-forecast midpoint, offsetting any boost from the trade data, and followed Monday's drop when the PBOC made it easier to short the currency.

In commodities, WTI & Brent prices have been choppy but at present are supported as attention moves from the trio of supply-side factors that were impacting benchmarks yesterday and turns towards the sessions events with the OPEC MOMR due for release today (timing TBC); ahead of the IEA equivalent due tomorrow. Spot gold is essentially unchanged on the session and has been relatively steady ~USD 1920/oz for the morning given the USD’s rangebound performance and lack of fundamental catalysts thus far. Silver is up notably after the recent upgrade of the precious metal by Goldman Sachs.

Today, the hearings for the Supreme Court nomination of Judge Amy Coney Barrett continue in the Senate Judiciary Committee as Republicans try to cement a conservative majority on the court before the Nov. 3 election. Expected data include inflation. BlackRock, Citigroup, Delta Air, Fastenal, J&J and JPMorgan are among companies reporting earnings

Market Snapshot

- S&P 500 futures little changed at 3,529.75

- STOXX Europe 600 down 0.1% to 372.56

- MXAP up 0.2% to 177.24

- MXAPJ up 0.2% to 588.52

- Nikkei up 0.2% to 23,601.78

- Topix up 0.4% to 1,649.10

- Hang Seng Index up 2.2% to 24,649.68

- Shanghai Composite up 0.04% to 3,359.75

- Sensex down 0.01% to 40,588.00

- Australia S&P/ASX 200 up 1% to 6,195.75

- Kospi down 0.02% to 2,403.15

- Brent futures up 1.6% to $42.39/bbl

- Gold spot little changed at $1,923.07

- U.S. Dollar Index up 0.1% to 93.15

- German 10Y yield fell 0.5 bps to -0.55%

- Euro down 0.1% to $1.1797

- Italian 10Y yield fell 4.6 bps to 0.475%

- Spanish 10Y yield rose 0.3 bps to 0.148%

Top Overnight News from Bloomberg

- European Union leaders will discuss preparations for the potential collapse of trade talks with the U.K. when they hold a summit later this week after France dug in, questioning whether it could hold Boris Johnson’s government to any agreement

- Boris Johnson clashed with his own government’s scientific advisers who wanted tougher action against the resurgent coronavirus outbreak in the U.K. in September

- China’s exports rose for the fourth straight month in September while imports surged, pointing to further recovery in the month for global trade and a robust domestic rebound

- U.K. job cuts jumped the most on record in the three months through August even as lockdown eased, raising concern that the worst is yet to come. The number of redundancies climbed 114,000 in the June-August period, the most since 1995, the Office for National Statistics said Tuesday

A quick look at global markets courtesy of Newsquawk

Asia-Pac equities traded mixed following the upbeat performance on Wall Street where the Nasdaq posted its best session in around month as the tech-sector led the gains and Apple shares closed higher by over 6% ahead of the Apple Event and the much-anticipated unveiling of the iPhone 12. Sentiment softened following a firm re-opening of cash Treasuries, which could’ve encouraged defensive flows in other assets, whilst the risk-mood further waned following reports that Johnson & Johnson paused its COVID-19 study (ahead of earnings) amid an unexplained illness in a participant – with the company later confirming and caveating that adverse events are an expected part of any clinical study, especially large ones. Nonetheless, ASX 200 (+1.2%) was supported by advances in its heavyweight financials as the broader sector eyes US bank earnings set to kick off with JP Morgan and Citi, meanwhile mining names in the index retrace some of yesterday’s upside. Nikkei 225 (unch) was choppy and gave up opening gains at one point as shares in heavyweight Softbank reversed course following the announcement of its Vision Fund mulling a special purpose acquisition company (SPAC) and is seeking outside investments, albeit it may reportedly put its own capital in the vehicle. Elsewhere, KOSPI (-0.5%) continued grinding lower as South Korea’s new COVID-19 cases rebounded to over 100 a day after the country eased restrictions. Meanwhile, Shanghai Comp (-0.4%) was lacklustre after the PBoC skipped open market operations for a net daily drain of CNY 100bln – with little reaction to September exports and imports hitting record highs in Yuan terms, whilst the Hang Seng session was cancelled due to tropical storm Nangka. Finally, broader defensive flows have kept JGBs supported, with the 5yr outperforming in cash and futures.

Top Asian News

- China’s Exports Gain, Imports Surge in September Amid Reopenings

- Singapore Marks Milestone in Virus Fight with No New Local Cases

- China Evergrande Seeks Up to $1.09 Billion in Share Placement

- HSBC Is Left Off First China Dollar Bond Deal Since 2017

European equities (Eurostoxx 50 -0.2%) have seen a mild scaling back of yesterday’s gains with a decline in US equity index futures alongside the EU cash open dictating the sate-of-play early doors; although, the NQ is the mornings outperform with gains of 0.7%. In terms of the current key themes for the market, little in the way has changed in the Presidential election or stimulus front since yesterday’s close, whilst on the vaccine front, Johnson & Johnson announced that it has paused all dosing in its Janssen COVID-19 vaccine trial due to an unexplained illness. Johnson & Johnson caveated the announcement by noting that such incidents are an expected part of any clinical study, especially of this size. On the vaccine front, even in the event of a more material disruption to the trial process, desks will likely be cognizant of the volume of vaccine candidates in the pipeline and therefore would likely remain confident that a vaccine of some description will materialise at some stage. Across Europe, losses are relatively broad-based across major indices with sectoral performance mixed. To the downside, banking names are notably softer this morning as the sector remains out of favour with investors; Pantheon Macro highlights that the Eurostoxx bank index is down 40% YTD compared to losses of 12% for the broader index. Travel & leisure stocks are also softer with the tenor of updates on the COVID front continuing to come in on the negative side for the sector. To the upside, telecom and utilities names are faring better than peers with the later supported by SSE (+4.0%) after the Co. disposed of its 50% stake in Multifuel Energy Limited for GBP 995mln. Elsewhere, Maersk (+1.9%) have seen mild support after the Co. upgraded its 2020 adj. EBITDA outlook, Airbus (-3.1%) trade softer after signing a labour deal with French unions and being downgraded at JP Morgan, whilst stock-specific newsflow is otherwise relatively light this morning. Looking ahead, increasing focus will likely be placed on US earnings with Johnson & Johnson, BlackRock, JP Morgan, Delta Airlines and Citi all due to report before the opening bell today.

Top European News

- Top U.K. Scientists Clash With Johnson Over Virus Lockdown

- U.K. Job Cuts Jump Most on Record With More Pain on the Way

- Investor Hopes For German Recovery Plunge After Virus Resurgence

- Macron Turns to Former Taxi Driver to Save French Shopkeepers

In FX, ironically, a significantly narrower trade surplus due to imports exceeding consensus by a huge margin in China has not helped the Aussie at all given the fact that the latter is now tightening levels of custom checks for coal and related products from the former after banning other goods. Indeed, Aud/Usd has now lost grip of the 0.7200 handle and the Aud/Nzd cross is testing support/bids at the psychological 1.0800 mark to provide the Kiwi with some relative support above 0.6600 vs its US peer. Ahead, Aussie consumer sentiment before a speech by RBA Governor Lowe on Wednesday and jobs data the day after.

- USD – The Dollar seems to be benefiting at the expense of others rather than in its own right, though a downturn in risk sentiment after Monday’s excesses on Wall Street may also be impacting alongside some consolidation after the DXY held above 93.000 yesterday and subsequently eclipsed the 50 DMA, albeit unconvincingly so far within 93.273-034 parameters as attention turns to US CPI data and the start of Q3 earnings.

- CAD/JPY/CHF/EUR/GBP - All softer against the Greenback, though to varying degrees as the Loonie gleans some encouragement from stabilising oil prices to stay within reach of 1.3100 and the Yen holds above 105.50 amidst reports that new Japanese PM Suga is mulling further economic support measures to be rolled out in November. Meanwhile, the Franc remains anchored around 0.9100, the Euro is striving to keep sight of 1.1800 where even bigger option expiries (2.5 bn) align with the 50 DMA and Sterling has survived another test of 1.3000 in wake of mixed UK labour and retail survey data in the run up to another speech from BoE Governor Bailey and a report on Brexit trade negotiations from EU Ministers. Note, Eur/Usd has slipped a few pips on the back of a pretty downbeat October German ZEW survey.

- SCANDI/EM - Softer than forecast Swedish CPI readings have not hampered the Swedish Crown given the Riskbank’s insistence that inflation undershoots are transitory blips and likelihood that Governor Ingves will stick to that script if he mentions the data later. Elsewhere, the Norwegian Krona is also deriving a degree of traction from the aforementioned recovery in crude awaiting a trio of Norges Bank commentators including chief Olsen, while the SA Rand could receive some independent impetus from Gold and overall mining production as Usd/Zar hovers under 16.5000, Eur/Sek eyes 10.3500 and Eur/Nok probes 10.7800.

In commodities, WTI & Brent prices have been choppy throughout the morning but at present are supported as attention moves from the trio of supply-side factors that were impacting benchmarks yesterday and turns towards the sessions events with the OPEC MOMR due for release today (timing TBC); ahead of the IEA equivalent due tomorrow. Currently, WTI and Brent futures are at the top end of session ranges, USD 40.22/bbl and USD 42.43/bbl respectively, seemingly moving in tandem to the grinding upside seen in US futures; but, as mentioned, have been choppy thus far printing both fresh session highs and lows in the European morning. Elsewhere and ahead of today’s OPEC MOMR, thus far this month the EIA STEO cut both 2020 and 2021 world oil demand growth by 300k and 280k BPD respectively; note, attention from an OPEC perspective is perhaps more on the upcoming JMMC meeting on October 19th for any potential alterations to the output cut schedule given returning Libyan demand among other factors. Separately, updates from the IEA overnight saw them forecast oil demand -8% this year alongside a -5% drop in global energy demand; such commentary comes ahead of the IEA monthly report tomorrow and as a reminder in September the agency cut their demand forecast for both this year and next. Moving to metals, where spot gold is essentially unchanged on the session and has been relatively steady ~USD 1920/oz for the morning given the USD’s rangebound performance and lack of fundamental catalysts thus far.

US Event Calendar

- 8:30am: US CPI MoM, est. 0.2%, prior 0.4%; YoY, est. 1.4%, prior 1.3%

- 8:30am: US CPI Ex Food and Energy MoM, est. 0.2%, prior 0.4%; YoY, est. 1.7%, prior 1.7%

- 8:30am: Real Avg Weekly Earnings YoY, prior 3.9%; Avg Hourly Earning YoY, prior 3.3%

DB's Jim Reid concludes the overnight wrap

Today is the annual day where resistance is futile. Every year I go into it with good intentions after a conversation with my wife the night before as to how I don’t need to join the crowd. Then by the end of the day I’ve always committed to becoming a stampeding lemming. Yes today I shall agree to buy the new iPhone regardless of what features the product launch tells me it has. I’d imagine they could go all retro and go back to a phone that just allows you to speak to someone and l’d simply ask them to name their price. Oh and as I’ve been typing this I’ve just had an alert telling me it’s Amazon Prime Day. I could be much poorer by the time you read this and then bankrupt by the time the Apple event ends tonight.

Ahead of this big product launch and the start of US earnings season today, global equity markets followed up the last two weeks of gains with yet another strong performance yesterday. Even with the US slow due to the Columbus Day holiday, by the close the S&P 500 was up another +1.64%, as the index closed at its 2nd highest level ever, just over 1% down from its record close. The index’s biggest component, Apple (+6.35%), was the best performing S&P stock in anticipation of today’s news. Overall, megacap tech stocks outperformed the broader index leading the NASDAQ to finish an even stronger +2.56% higher, the best day for the index since early September. The rally was still fairly broad-based with 22 of the 24 S&P industry groups higher with only defensives like consumer durables (-0.44%) giving way. Over in Europe, the STOXX 600 climbed +0.72% to reach its own 3-week high. Energy stocks were among the laggards on both sides of the Atlantic as Brent crude (-2.64%) and WTI (-2.88%) oil prices fell back. The drop was the most in just over a week and comes as news that supply disruptions are easing. Specifically, Royal Dutch Shell, BHP Group and Chevron all said they have resumed operations in the Gulf of Mexico and separately Libya’s National Oil Corp has ramped up production of its largest oil field. The STOXX 600 travel and leisure index was down -0.64% in spite of the broader market rally as the move to tighter restrictions gathered pace.

Attention will now turn to the start of the Q3 earnings season with today’s releases including Johnson & Johnson, JPMorgan Chase, Citigroup and BlackRock, ahead of a number of other financials releasing later in the week. As our asset allocation team wrote in their preview (link here), the bottom-up consensus for Q3 is for a sharp rebound in headline earnings, but the bulk is being driven by reductions in loan loss provisions and energy sector losses. If you exclude these, underlying earnings growth is forecast to barely move up, in spite of rising Q3 GDP growth estimates pointing to a strong macro rebound. According to them, this suggests the consensus is likely again underestimating the bounce in earnings. This is the same as we highlighted in Q2 but the big difference is that US equity positioning is more neutral now and that election uncertainty has increasingly been priced out over the last couple of weeks. So while the Q2 season was set up for a big market rally, it’s going to be much harder in Q3 even if the positive earnings story is similar.

You can bet companies will continue to be asked about ESG on their earnings calls. The ESG themes this year may have been dominated by health and sustainability, but Luke and Karthik from my team have just published a piece that shows the hottest growth topics in the third quarter were new ones as companies looked to start rebuilding from the pandemic. Their piece also reviews Q3 performance and flows for ESG funds. See here for more.

Back to the virus and in terms of the new measures, UK Prime Minister Johnson announced there’d be a new tiered alert system for England, which would see different areas grouped into medium, high and very high. The new measures come as data showed hospitalisations in England rose to 3,665 yesterday, which its highest level since June 12. Areas under a Very High alert will see pubs and bars close, though shops and schools are remaining open. Later today Dutch Prime Minister Rutte is expected to announce stricter measures and Italy’s Prime Minister Conte was also reportedly looking into new restrictions on private parties, amateur sports activities and social gatherings.

Elsewhere in the US, Covid cases are now averaging over 48,000 per day over the last week and to the highest levels since mid-August. The highest impacted states per 10K people are those that missed the initial wave (Northeast and West Coast) and the second wave (Sun Belt). The states most affected now are in the upper Midwest – North and South Dakota as well as Wisconsin. The latter continues to be a big focus of next month’s election and the impact of the virus may make counting votes there take longer than normal with many voters mailing in ballots for the first time.

On the vaccine front, Johnson & Johnson said overnight that its Covid-19 Phase 3 trial has been paused due to an unexplained illness in a participant. Elsewhere, China’s local daily Jiemian reported that Sinopharm has started to administer its two vaccines to residents in Wuhan and Beijing. Residents can now make appointments to get the shot and students who need to go abroad from November to January are being given priority. As a reminder, Sinopharm already has limited approval in China to administer its vaccine.

The above news on J&J is weighing on risk overnight even if most markets have recovered from their respective intraday lows. The Shanghai Comp (-0.28%) and Kospi (-0.36%) are down while the Nikkei (+0.12%) is up. S&P 500 futures also retreated following the news and is now -0.41% as we type. The Hang Seng suspended morning trading on the likelihood of a tropical storm hitting Hong Kong’s shore. In FX, the US dollar index is trading up +0.13%. Elsewhere, spot gold prices are down -0.62%. In terms of overnight data, China’s September exports came in at +9.9% yoy (vs. +10.0% yoy expected) while imports jumped to +13.2% yoy (vs. +0.4% yoy expected). As a result the trade balance for the month stood at $37bn (vs. $60bn expected). In other news, the hearings for the Supreme Court nomination of Judge Amy Coney Barrett have begun in the Senate Judiciary Committee.

Back to the election and investor sentiment was further supported yesterday by the continued poll lead for Joe Biden amidst hopes that a blue wave for the Democrats will set markets up for substantial fiscal stimulus next year. The FiveThirtyEight and the RealClearPolitics polling averages now put Biden +10.4pts and +10.2pts ahead respectively. The FiveTirthyEight Senate model now gives Democrats a 69% chance of winning control of the Senate (given the Vice President is the tiebreaker), the highest probability of this election cycle. The November VIX future, which expires two weeks following the election, fell to its lowest level since August 20 as polls continue to widen. On this today DB are hosting a live video call on “Who is going to win the 2020 US Presidential election?” at 3pm BST/4pm CET/10am ET with US polling experts Amy Walter, National Editor, The Cook Political Report and G. Elliott Morris, Data journalist for The Economist. Register here if you want to get the details.

New records were set over in the fixed income sphere, as yields on 10yr Italian debt hit another record low of 0.67%. In our chart of the day yesterday (link here ), we looked at 700 years of data on this, and show how Italian yields have continued to fall even as the country’s public debt burden looks set to climb to even higher records. The spread of 10yr yields over bunds has also continued to narrow, and yesterday hit a fresh 2-year low of 1.22%. Bunds themselves saw a -1.8bps fall in yields to -0.55%, while US Treasury markets were closed for a bond holiday in the US. Yields on 10y USTs are trading down -1.3bps this morning at 0.763%.

To the day ahead now, and earnings season kicks off with releases from Johnson & Johnson, JPMorgan Chase, Citigroup and BlackRock. From central banks, we’ll hear from Bank of England Governor Bailey, the ECB’s Hernandez de Cos and the Fed’s Barkin. Data releases include the US CPI reading for September, while the IMF will be releasing their latest World Economic Outlook.

International

Illegal Immigrants Leave US Hospitals With Billions In Unpaid Bills

Illegal Immigrants Leave US Hospitals With Billions In Unpaid Bills

By Autumn Spredemann of The Epoch Times

Tens of thousands of illegal…

Share this:

By Autumn Spredemann of The Epoch Times

Tens of thousands of illegal immigrants are flooding into U.S. hospitals for treatment and leaving billions in uncompensated health care costs in their wake.

The House Committee on Homeland Security recently released a report illustrating that from the estimated $451 billion in annual costs stemming from the U.S. border crisis, a significant portion is going to health care for illegal immigrants.

With the majority of the illegal immigrant population lacking any kind of medical insurance, hospitals and government welfare programs such as Medicaid are feeling the weight of these unanticipated costs.

Apprehensions of illegal immigrants at the U.S. border have jumped 48 percent since the record in fiscal year 2021 and nearly tripled since fiscal year 2019, according to Customs and Border Protection data.

Last year broke a new record high for illegal border crossings, surpassing more than 3.2 million apprehensions.

And with that sea of humanity comes the need for health care and, in most cases, the inability to pay for it.

In January, CEO of Denver Health Donna Lynne told reporters that 8,000 illegal immigrants made roughly 20,000 visits to the city’s health system in 2023.

The total bill for uncompensated care costs last year to the system totaled $140 million, said Dane Roper, public information officer for Denver Health. More than $10 million of it was attributed to “care for new immigrants,” he told The Epoch Times.

Though the amount of debt assigned to illegal immigrants is a fraction of the total, uncompensated care costs in the Denver Health system have risen dramatically over the past few years.

The total uncompensated costs in 2020 came to $60 million, Mr. Roper said. In 2022, the number doubled, hitting $120 million.

He also said their city hospitals are treating issues such as “respiratory illnesses, GI [gastro-intenstinal] illnesses, dental disease, and some common chronic illnesses such as asthma and diabetes.”

“The perspective we’ve been trying to emphasize all along is that providing healthcare services for an influx of new immigrants who are unable to pay for their care is adding additional strain to an already significant uncompensated care burden,” Mr. Roper said.

He added this is why a local, state, and federal response to the needs of the new illegal immigrant population is “so important.”

Colorado is far from the only state struggling with a trail of unpaid hospital bills.

Dr. Robert Trenschel, CEO of the Yuma Regional Medical Center situated on the Arizona–Mexico border, said on average, illegal immigrants cost up to three times more in human resources to resolve their cases and provide a safe discharge.

“Some [illegal] migrants come with minor ailments, but many of them come in with significant disease,” Dr. Trenschel said during a congressional hearing last year.

“We’ve had migrant patients on dialysis, cardiac catheterization, and in need of heart surgery. Many are very sick.”

He said many illegal immigrants who enter the country and need medical assistance end up staying in the ICU ward for 60 days or more.

A large portion of the patients are pregnant women who’ve had little to no prenatal treatment. This has resulted in an increase in babies being born that require neonatal care for 30 days or longer.

Dr. Trenschel told The Epoch Times last year that illegal immigrants were overrunning healthcare services in his town, leaving the hospital with $26 million in unpaid medical bills in just 12 months.

ER Duty to Care

The Emergency Medical Treatment and Labor Act of 1986 requires that public hospitals participating in Medicare “must medically screen all persons seeking emergency care … regardless of payment method or insurance status.”

The numbers are difficult to gauge as the policy position of the Centers for Medicare & Medicaid Services (CMS) is that it “will not require hospital staff to ask patients directly about their citizenship or immigration status.”

In southern California, again close to the border with Mexico, some hospitals are struggling with an influx of illegal immigrants.

American patients are enduring longer wait times for doctor appointments due to a nursing shortage in the state, two health care professionals told The Epoch Times in January.

A health care worker at a hospital in Southern California, who asked not to be named for fear of losing her job, told The Epoch Times that “the entire health care system is just being bombarded” by a steady stream of illegal immigrants.

“Our healthcare system is so overwhelmed, and then add on top of that tuberculosis, COVID-19, and other diseases from all over the world,” she said.

A newly-enacted law in California provides free healthcare for all illegal immigrants residing in the state. The law could cost taxpayers between $3 billion and $6 billion per year, according to recent estimates by state and federal lawmakers.

In New York, where the illegal immigration crisis has manifested most notably beyond the southern border, city and state officials have long been accommodating of illegal immigrants’ healthcare costs.

Since June 2014, when then-mayor Bill de Blasio set up The Task Force on Immigrant Health Care Access, New York City has worked to expand avenues for illegal immigrants to get free health care.

“New York City has a moral duty to ensure that all its residents have meaningful access to needed health care, regardless of their immigration status or ability to pay,” Mr. de Blasio stated in a 2015 report.

The report notes that in 2013, nearly 64 percent of illegal immigrants were uninsured. Since then, tens of thousands of illegal immigrants have settled in the city.

“The uninsured rate for undocumented immigrants is more than three times that of other noncitizens in New York City (20 percent) and more than six times greater than the uninsured rate for the rest of the city (10 percent),” the report states.

The report states that because healthcare providers don’t ask patients about documentation status, the task force lacks “data specific to undocumented patients.”

Some health care providers say a big part of the issue is that without a clear path to insurance or payment for non-emergency services, illegal immigrants are going to the hospital due to a lack of options.

“It’s insane, and it has been for years at this point,” Dana, a Texas emergency room nurse who asked to have her full name omitted, told The Epoch Times.

Working for a major hospital system in the greater Houston area, Dana has seen “a zillion” migrants pass through under her watch with “no end in sight.” She said many who are illegal immigrants arrive with treatable illnesses that require simple antibiotics. “Not a lot of GPs [general practitioners] will see you if you can’t pay and don’t have insurance.”

She said the “undocumented crowd” tends to arrive with a lot of the same conditions. Many find their way to Houston not long after crossing the southern border. Some of the common health issues Dana encounters include dehydration, unhealed fractures, respiratory illnesses, stomach ailments, and pregnancy-related concerns.

“This isn’t a new problem, it’s just worse now,” Dana said.

Medicaid Factor

One of the main government healthcare resources illegal immigrants use is Medicaid.

All those who don’t qualify for regular Medicaid are eligible for Emergency Medicaid, regardless of immigration status. By doing this, the program helps pay for the cost of uncompensated care bills at qualifying hospitals.

However, some loopholes allow access to the regular Medicaid benefits. “Qualified noncitizens” who haven’t been granted legal status within five years still qualify if they’re listed as a refugee, an asylum seeker, or a Cuban or Haitian national.

Yet the lion’s share of Medicaid usage by illegal immigrants still comes through state-level benefits and emergency medical treatment.

A Congressional report highlighted data from the CMS, which showed total Medicaid costs for “emergency services for undocumented aliens” in fiscal year 2021 surpassed $7 billion, and totaled more than $5 billion in fiscal 2022.

Both years represent a significant spike from the $3 billion in fiscal 2020.

An employee working with Medicaid who asked to be referred to only as Jennifer out of concern for her job, told The Epoch Times that at a state level, it’s easy for an illegal immigrant to access the program benefits.

Jennifer said that when exceptions are sent from states to CMS for approval, “denial is actually super rare. It’s usually always approved.”

She also said it comes as no surprise that many of the states with the highest amount of Medicaid spending are sanctuary states, which tend to have policies and laws that shield illegal immigrants from federal immigration authorities.

Moreover, Jennifer said there are ways for states to get around CMS guidelines. “It’s not easy, but it can and has been done.”

The first generation of illegal immigrants who arrive to the United States tend to be healthy enough to pass any pre-screenings, but Jennifer has observed that the subsequent generations tend to be sicker and require more access to care. If a family is illegally present, they tend to use Emergency Medicaid or nothing at all.

The Epoch Times asked Medicaid Services to provide the most recent data for the total uncompensated care that hospitals have reported. The agency didn’t respond.

Continue reading over at The Epoch Times

International

Fuel poverty in England is probably 2.5 times higher than government statistics show

The top 40% most energy efficient homes aren’t counted as being in fuel poverty, no matter what their bills or income are.

Share this:

The cap set on how much UK energy suppliers can charge for domestic gas and electricity is set to fall by 15% from April 1 2024. Despite this, prices remain shockingly high. The average household energy bill in 2023 was £2,592 a year, dwarfing the pre-pandemic average of £1,308 in 2019.

The term “fuel poverty” refers to a household’s ability to afford the energy required to maintain adequate warmth and the use of other essential appliances. Quite how it is measured varies from country to country. In England, the government uses what is known as the low income low energy efficiency (Lilee) indicator.

Since energy costs started rising sharply in 2021, UK households’ spending powers have plummeted. It would be reasonable to assume that these increasingly hostile economic conditions have caused fuel poverty rates to rise.

However, according to the Lilee fuel poverty metric, in England there have only been modest changes in fuel poverty incidence year on year. In fact, government statistics show a slight decrease in the nationwide rate, from 13.2% in 2020 to 13.0% in 2023.

Our recent study suggests that these figures are incorrect. We estimate the rate of fuel poverty in England to be around 2.5 times higher than what the government’s statistics show, because the criteria underpinning the Lilee estimation process leaves out a large number of financially vulnerable households which, in reality, are unable to afford and maintain adequate warmth.

Energy security

In 2022, we undertook an in-depth analysis of Lilee fuel poverty in Greater London. First, we combined fuel poverty, housing and employment data to provide an estimate of vulnerable homes which are omitted from Lilee statistics.

We also surveyed 2,886 residents of Greater London about their experiences of fuel poverty during the winter of 2022. We wanted to gauge energy security, which refers to a type of self-reported fuel poverty. Both parts of the study aimed to demonstrate the potential flaws of the Lilee definition.

Introduced in 2019, the Lilee metric considers a household to be “fuel poor” if it meets two criteria. First, after accounting for energy expenses, its income must fall below the poverty line (which is 60% of median income).

Second, the property must have an energy performance certificate (EPC) rating of D–G (the lowest four ratings). The government’s apparent logic for the Lilee metric is to quicken the net-zero transition of the housing sector.

In Sustainable Warmth, the policy paper that defined the Lilee approach, the government says that EPC A–C-rated homes “will not significantly benefit from energy-efficiency measures”. Hence, the focus on fuel poverty in D–G-rated properties.

Generally speaking, EPC A–C-rated homes (those with the highest three ratings) are considered energy efficient, while D–G-rated homes are deemed inefficient. The problem with how Lilee fuel poverty is measured is that the process assumes that EPC A–C-rated homes are too “energy efficient” to be considered fuel poor: the main focus of the fuel poverty assessment is a characteristic of the property, not the occupant’s financial situation.

In other words, by this metric, anyone living in an energy-efficient home cannot be considered to be in fuel poverty, no matter their financial situation. There is an obvious flaw here.

Around 40% of homes in England have an EPC rating of A–C. According to the Lilee definition, none of these homes can or ever will be classed as fuel poor. Even though energy prices are going through the roof, a single-parent household with dependent children whose only income is universal credit (or some other form of benefits) will still not be considered to be living in fuel poverty if their home is rated A-C.

The lack of protection afforded to these households against an extremely volatile energy market is highly concerning.

In our study, we estimate that 4.4% of London’s homes are rated A-C and also financially vulnerable. That is around 171,091 households, which are currently omitted by the Lilee metric but remain highly likely to be unable to afford adequate energy.

In most other European nations, what is known as the 10% indicator is used to gauge fuel poverty. This metric, which was also used in England from the 1990s until the mid 2010s, considers a home to be fuel poor if more than 10% of income is spent on energy. Here, the main focus of the fuel poverty assessment is the occupant’s financial situation, not the property.

Were such alternative fuel poverty metrics to be employed, a significant portion of those 171,091 households in London would almost certainly qualify as fuel poor.

This is confirmed by the findings of our survey. Our data shows that 28.2% of the 2,886 people who responded were “energy insecure”. This includes being unable to afford energy, making involuntary spending trade-offs between food and energy, and falling behind on energy payments.

Worryingly, we found that the rate of energy insecurity in the survey sample is around 2.5 times higher than the official rate of fuel poverty in London (11.5%), as assessed according to the Lilee metric.

It is likely that this figure can be extrapolated for the rest of England. If anything, energy insecurity may be even higher in other regions, given that Londoners tend to have higher-than-average household income.

The UK government is wrongly omitting hundreds of thousands of English households from fuel poverty statistics. Without a more accurate measure, vulnerable households will continue to be overlooked and not get the assistance they desperately need to stay warm.

Torran Semple receives funding from Engineering and Physical Sciences Research Council (EPSRC) grant EP/S023305/1.

John Harvey does not work for, consult, own shares in or receive funding from any company or organisation that would benefit from this article, and has disclosed no relevant affiliations beyond their academic appointment.

european uk pandemicGovernment

Looking Back At COVID’s Authoritarian Regimes

After having moved from Canada to the United States, partly to be wealthier and partly to be freer (those two are connected, by the way), I was shocked,…

Share this:

{kind=link}

After having moved from Canada to the United States, partly to be wealthier and partly to be freer (those two are connected, by the way), I was shocked, in March 2020, when President Trump and most US governors imposed heavy restrictions on people’s freedom. The purpose, said Trump and his COVID-19 advisers, was to “flatten the curve”: shut down people’s mobility for two weeks so that hospitals could catch up with the expected demand from COVID patients. In her book Silent Invasion, Dr. Deborah Birx, the coordinator of the White House Coronavirus Task Force, admitted that she was scrambling during those two weeks to come up with a reason to extend the lockdowns for much longer. As she put it, “I didn’t have the numbers in front of me yet to make the case for extending it longer, but I had two weeks to get them.” In short, she chose the goal and then tried to find the data to justify the goal. This, by the way, was from someone who, along with her task force colleague Dr. Anthony Fauci, kept talking about the importance of the scientific method. By the end of April 2020, the term “flatten the curve” had all but disappeared from public discussion.

Now that we are four years past that awful time, it makes sense to look back and see whether those heavy restrictions on the lives of people of all ages made sense. I’ll save you the suspense. They didn’t. The damage to the economy was huge. Remember that “the economy” is not a term used to describe a big machine; it’s a shorthand for the trillions of interactions among hundreds of millions of people. The lockdowns and the subsequent federal spending ballooned the budget deficit and consequent federal debt. The effect on children’s learning, not just in school but outside of school, was huge. These effects will be with us for a long time. It’s not as if there wasn’t another way to go. The people who came up with the idea of lockdowns did so on the basis of abstract models that had not been tested. They ignored a model of human behavior, which I’ll call Hayekian, that is tested every day.

These are the opening two paragraphs of my latest Defining Ideas article, “Looking Back at COVID’s Authoritarian Regimes,” Defining Ideas, March 14, 2024.

Another excerpt:

That wasn’t the only uncertainty. My daughter Karen lived in San Francisco and made her living teaching Pilates. San Francisco mayor London Breed shut down all the gyms, and so there went my daughter’s business. (The good news was that she quickly got online and shifted many of her clients to virtual Pilates. But that’s another story.) We tried to see her every six weeks or so, whether that meant our driving up to San Fran or her driving down to Monterey. But were we allowed to drive to see her? In that first month and a half, we simply didn’t know.

Read the whole thing, which is longer than usual.

(0 COMMENTS) budget deficit coronavirus covid-19 white house fauci trump canada

Net Zero, The Digital Panopticon, & The Future Of Food

Problems After COVID-19 Vaccination More Prevalent Among Naturally Immune: Study

For-profit nursing homes are cutting corners on safety and draining resources with financial shenanigans − especially at midsize chains that dodge public scrutiny

‘Excess Mortality Skyrocketed’: Tucker Carlson and Dr. Pierre Kory Unpack ‘Criminal’ COVID Response

Looking Back At COVID’s Authoritarian Regimes

Trump nearly derailed democracy once − here’s what to watch out for in reelection campaign

Riley Gaines Explains How Women’s Sports Are Rigged To Promote The Trans Agenda

Health Officials: Man Dies From Bubonic Plague In New Mexico

MIPIM 2024 Reflects Mixed Feelings on CRE Recovery

Delta Air Lines adds a new route travelers have been asking for

-

Uncategorized3 weeks ago

Uncategorized3 weeks agoAll Of The Elements Are In Place For An Economic Crisis Of Staggering Proportions

-

International1 week ago

International1 week agoEyePoint poaches medical chief from Apellis; Sandoz CFO, longtime BioNTech exec to retire

-

Uncategorized4 weeks ago

Uncategorized4 weeks agoCalifornia Counties Could Be Forced To Pay $300 Million To Cover COVID-Era Program

-

Uncategorized3 weeks ago

Uncategorized3 weeks agoApparel Retailer Express Moving Toward Bankruptcy

-

Uncategorized4 weeks ago

Uncategorized4 weeks agoIndustrial Production Decreased 0.1% in January

-

International1 week ago

International1 week agoWalmart launches clever answer to Target’s new membership program

-

Spread & Containment2 days ago

Spread & Containment2 days agoIFM’s Hat Trick and Reflections On Option-To-Buy M&A

-

Uncategorized4 weeks ago

Uncategorized4 weeks agoRFK Jr: The Wuhan Cover-Up & The Rise Of The Biowarfare-Industrial Complex