Government

More Market Volatility? Treasury Yields Surge Ahead Of Today’s FOMC Meeting

Nasdaq Futures Tumbled, European and Asian markets were mostly lower and Treasury yields climbed sharply ahead of a key Federal Reserve meeting today…

Share this:

This article was originally published by ZeroHedge.

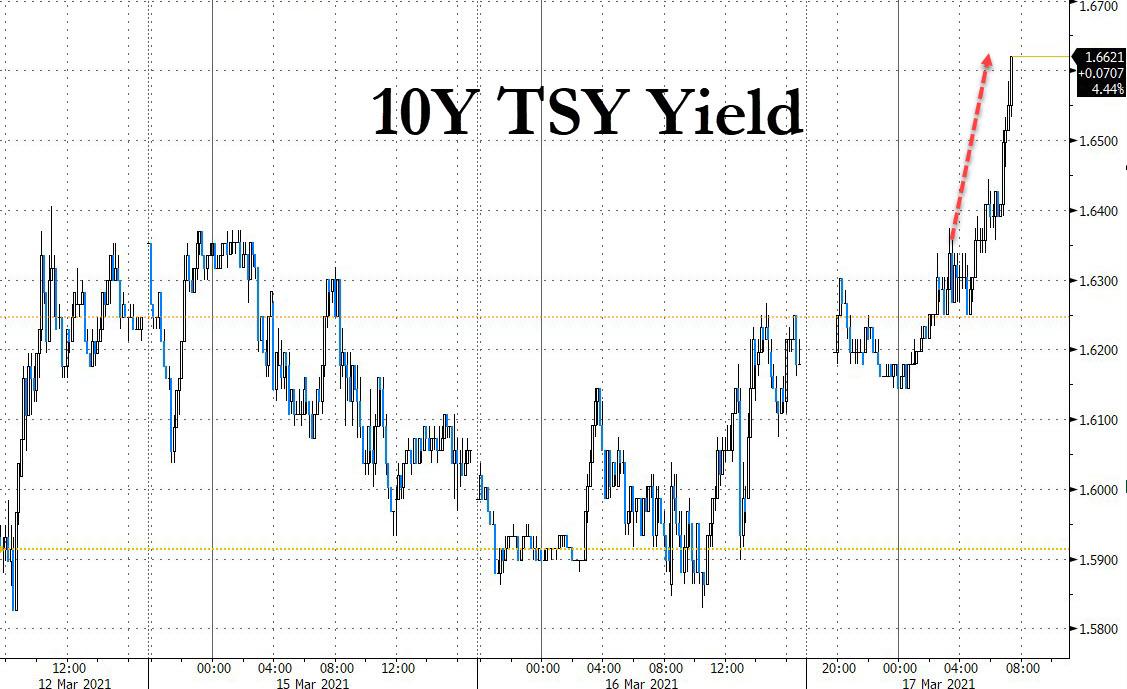

Nasdaq Futures Tumble As Treasury Yields Suddenly Surge Ahead Of FOMCS&P futures edged lower, European and Asian markets were mostly lower and Treasury yields climbed sharply ahead of a key Federal Reserve meeting at which officials will deliver their outlook for the economy amid an overheating recovery that risks stoking inflation, and where all eyes will be the median 2023 dot for a potential hawkish signal that sends yields soaring.

At 0715 a.m. ET, S&P 500 E-minis were down 14 points, or 0.34% and Nasdaq 100 E-minis were down 148 points, or 1.13. The FAAMG stocks all slumped while Fuel-cell firm Plug Power Inc. plunged more than 20% in pre-market trading after it disclosed accounting errors.

The 10-year TSY yield ticked up to a new 13-month high of 1.6656% ahead of the policy decision, with market-implied inflation expectations are at 12-year highs even after yesterday's 20-year bond auction drew stellar demand...

.... hammering demand for high-growth technology stocks, and sending Nasdaq 100 futs tumbling.

Powell and company are expected to issue a blowout GDP forecast for 2021 at the end of a two-day meeting on Wednesday, at 2 p.m. ET (1800 GMT) which will be followed by Fed Chair Jerome Powell’s news conference shortly after.

Echoing what we said yesterday, Nordea macro strategist Sebastien Galy said that “there is a decent chance that the rates forecasts from the 18 members committee could start focusing on a 2023 hike which would be quite a surprise, that Chairman Powell would then try to walk back in his speech.”

Rates markets are positioned for the Fed to raise borrowing costs sooner than current guidance suggests. Higher inflation expectations have boosted bond yields and sparked a rotation from growth to value stocks. Bond investor Bill Gross predicted in a Bloomberg TV interview that inflation will rise to 3% to 4% in the coming months.

“The concern is the assets that have worked best over the last decade -- rates, credit of all kinds and long-duration equities -- may not be the only games in town any more,” said David Wong, investment strategist at AllianceBernstein.

In Europe, the Stoxx Europe 600 Index is down 0.4% with the UK's FTSE 100 underperforming slightly. Autos, media and banks broadly offsetting softness in oil & gas, retail and mining stocks. The Stoxx Europe 600 Energy Index slides as much as 1.3% after European renewable-energy stocks fell, with the high-flying sub-sector’s sensitivity to higher bond yields dragging on the shares. Wind- turbine makers Vestas and Siemens Gamesa, solar firm Scatec and electrolyzer company Nel were the worst performers in the subgroup. Here are some of the biggest European movers today:

- BMW shares gain as much as 5.5% after results and setting electric vehicles targets. Morgan Stanley said the focus will be on a “sharp acceleration” in battery electric vehicle targets, which may be “enough to offset uneventful earnings.”

- MorphoSys shares advanced as much as 5% as the biopharmaceutical firm rebounded from yesterday’s 11% slump following FY results and 2021 guidance. Berenberg said that FY20 results were “upbeat” and set a foundation for future growth.

- Rolls-Royce shares rise as much as 4.6% after the engineer was upgraded to neutral from underweight at JPMorgan and had its price target raised at Berenberg. JPMorgan cited investors turning more optimistic because of vaccine progress, as well as the stock lagging behind peers since 2018.

- Allegro shares drop as much as 8.7% after major shareholders decided to sell 7% stake via an accelerated book- building before the end of its lock-up period. MBank said the large stake sale prior to 180 days pledged by major shareholders as lock-up period is “definitely a disappointment.”

- Verbund shares fall as much as 6.9%, with Barclays saying the market focus will be on the utility’s outlook, which is significantly weaker than expected. The company’s 2021 outlook miss was predominantly due to step-down in Grid unit earnings and lower flexibility products revenue, Barclays said in a note.

Earlier in the session, Asia’s equity benchmark headed for its third drop in four days, pulled down by weakness in the semiconductor sector. Regional chip giants TSMC and Samsung were among the heaviest drags on the MSCI Asia Pacific Index, after Samsung warned of a “serious” imbalance in the semiconductor industry and said it may have to delay the introduction of one of its key smartphones. Communication services and materials sectors were the other big losers. Equity gauges in India and South Korea were the worst performers in Asia. However, benchmarks in China and Vietnam rose, with the CSI 300 Index capping a second day of gains as telecom and consumer discretionary shares climbed.

As shown above, treasury futures volumes spiked as 10-year yields rose above 1.65%, topping at 1.6673% in early U.S. session. The move appeared to be technically driven, with 10-year yields back up to cheapest levels of the year. Gilts lead developed bond markets lower following 2035 bond sale while bunds outperform. Trading may be subdued into FOMC decision at 2pm ET. As 10-year yield exceeded its February 2020 high for the first time, 20k 10-year note futures changed hands on the move down to 131-21+ lows; 5s10s30s fly cheapened, approaching its March 8 multiyear high. Fixed income had a quiet start in Europe with price action stalling ahead of today’s FOMC meeting. Gilts and bund curves bear steepen slightly. Long end of the U.K. curve underperformed, trading ~1.5bps cheaper to bunds. Peripheral spreads are mostly tighter to core, Greece underperforms with focus on its 30y syndication. Treasuries bear flatten a touch, 10y yields ~2bps higher near 1.64%.

In FX, the Bloomberg dollar index was initially flat but then spiked, trading higher versus most major peers. The euro edged up after dipping below $1.18; one-day volatility in euro-dollar has risen to levels unseen since the U.S. election in November, while swap markets are outpricing the Fed ‘dots’ in a rare occurrence before the decision. The pound bucked a three-day losing streak amid speculation the Bank of England could take a relatively hawkish stance at its policy meeting Thursday. Australian 10-year yields extended gains and Aussie eased on greenback positioning ahead of the Federal Reserve’s policy decision.

Crude futures reverse Asia’s gains. WTI drops 0.6% near $64.40, Brent drops as much as 0.9% after the IEA said markets aren’t on the verge of a new price supercycle. Bitcoin held at about $55,000, below the weekend record above $61,000. Spot gold trades a tight range. Base metals trade well with LME aluminum and tin outperforming.

As DB's Jim Reid writes, today is all about the conclusion of the 2-day FOMC and Powell’s subsequent press conference with this meeting also including the latest economic projections and dot plot from the FOMC’s members. Back in December when the last dot plot was released, it showed that most of the committee favored keeping rates on hold at least through to the end of 2023. But since then we’ve seen a sharp move higher in Treasury yields thanks to the passage of the $1.9tn stimulus package, and markets are now pricing in an initial hike from the Fed within the next 2 years and three hikes in total by the end of 2023. With a more robust outlook ahead, DB US economists expect that one hike should be reflected in the committee’s updated projections out to end 2023 (via the median dot) but it’s a close call. However higher growth and lower unemployment will be in the forecasts, as well as a modestly higher inflation trajectory. The press conference may bring most of the focus though with every word scrutinised and cross examined given the recent run up in yields. Powell has now presided over 24 FOMCs and on average the S&P 500 has been -0.15% (15 out of the 24 were down days) lower on decision day – though this is heavily weighted by his first 7 meetings, which saw equities slip back when the Fed started its small hiking cycle in 2018. In terms of 10 year yields they have been -3.0bps lower on average with a median of -1.6bps (16 out 24 down in yield) on Powell FOMC days. To put this in perspective the S&P 500 is up +49.5% since his tenure begun in February 2018 and 10yr yields are down -108.8bps.

To the day ahead now, and the highlight is likely to be the aforementioned FOMC meeting and Fed Chair Powell’s subsequent press conference. In addition, the ECB’s Elderson will be speaking. Separately, data releases include US housing starts and building permits for February, as well as EU new car registrations for the same month.

Market Snapshot

- S&P 500 futures down less than 0.1% to 3,950.25

- STOXX Europe 600 falls 0.3%

- MXAP down 0.3% to 208.31

- MXAPJ down 0.4% to 692.22

- Nikkei little changed at 29,914.33

- Topix up 0.1% to 1,984.03

- Hang Seng Index little changed at 29,034.12

- Shanghai Composite little changed at 3,445.55

- Sensex down 0.7% to 50,015.22

- Australia S&P/ASX 200 down 0.5% to 6,795.23

- Kospi down 0.6% to 3,047.50

- Brent Futures little changed at $68.43/bbl

- Gold spot up 0.2% to $1,734.91

- U.S. Dollar Index little changed at 91.96

- German 10Y yield rose 0.008 bps to -0.328%

- Euro little changed at $1.1892

Top Overnight News from Bloomberg

- The rebounding greenback and weakness in global tech shares are curbing demand for Taiwan’s currency, reducing pressure on the central bank to act to slow appreciation

- Market expectations for a sustained rise in inflation and withdrawal of policy support are misplaced, creating buying opportunities in corporate bonds, according to BlackRock Inc. and Lombard Odier

- Greece is issuing its longest-maturity bonds since 2008, completing the country’s full return to debt markets. The nation is selling 30-year bonds via banks, which could be an opportunity for investors to pick up yields that are likely to be the highest in the euro area

- Senior U.S. officials sought to set a low bar on expectations for the Biden administration’s first face-to-face meeting with Chinese officials later this week, saying it will be more about discussing priorities -- and differences -- than trying to craft agreements

- The U.K. government revealed plans to slash the amount of carbon dioxide spewed out by factories and other industrial processes by two-thirds within the next 15 years

- Support for German Chancellor Angela Merkel’s conservative bloc slumped to its lowest in a year as discontent over the government’s handling of the vaccination rollout mounts and some opposition leaders called for her to fire the health minister

Quick look at global markets courtesy of Newsquawk

Asia-Pac stocks traded in a subdued manner after the similar handover from the US with participants also cautious ahead of a busy schedule of central bank announcements including the FOMC later today. ASX 200 (-0.5%) was pressured amid underperformance in commodity-related stocks and as nearly all sectors suffered losses aside from tech and telecoms. Nikkei 225 (-0.1%) initially bucked the trend after a rebound in USD/JPY and with Japan planning to lift the state of emergency for the Tokyo area on March 21st but then succumbed to the broad cautious mood which was not helped by weaker than expected trade data. Hang Seng (unch.) and Shanghai Comp. (unch.) opened with losses amid tough rhetoric from the US heading into Thursday’s high-level meeting in Alaska with an official stating they will lay out specific areas where the US believes Beijing needs to take steps to change course and will make clear the concerns regarding China's malicious cyber activity. The official also noted that the US doesn't expect specific negotiated deliverables from the meeting, nor does it anticipate issuing a joint statement, while there were separate comments from Secretary of State Blinken that China is acting more aggressively and more repressively. Nonetheless, Chinese markets briefly reversed their losses spearheaded by a recovery in tech and growth which saw the ChiNext rebound from losses of 1.5% to trade higher on the session by a similar extent. Finally, 10yr JGBs were steady with prices kept afloat by the subdued risk tone and with the BoJ also present in the market for more than JPY 1.3tln of JGBs with 1yr-25yr maturities.

Top Asian News

- Apple Is Said to Cut Off China’s Ofilm Over Xinjiang Labor

- Naver Plans Debut Dollar Bond as Korea Web Firms Expand Abroad

- Asia Chip Stocks Slip as Samsung Warns of Severe Global Shortage

- Hong Kong Vaccine Bookings Jump in First Day of Expanded Access

European equities saw somewhat of a uninspiring cash open and have since retained a downside bias (Euro Stoxx -0.1%) after the region took a similar cue from the APAC session, albeit the depth of the price action is shallow in the run up to the blockbuster FOMC policy announcement at 18:00GMT and presser at 18:30GMT (full preview available in the Newsquawk Research Suite). Ahead of that, reports note that billions of Dollars in stimulus payments are expected to drop into Americans' bank accounts later today, with expectations for some to be funnelled into the stock market. Nonetheless, US equity futures remain subdued with the cyclically-led RTY (-0.5%) the laggard vs the NQ (-0.2%), ES (-0.1%) and YM (Unch). Back to Europe, Italy's FTSE MIB (+0.1%) and Germany's DAX (+0.1%) fare modestly better vs peers, with the former led by Italian banks, whilst the latter is kept afloat by auto names VW (+5.8%) and BMW (+5.0%) amid their ambitious plans to expand in the EV space, with BMW targeting some 2mln EV deliveries by end-2025 whilst guiding its group pretax this year "significantly" above 2020 levels. Sectors in Europe are mostly in the red with the exception of Autos, Media and Banks, with the latter due to the high-yield environment. Laggards mostly incorporate some of the more cyclical "reopening" or "recovery" sectors including, Retail, Basic Resources, Travel & Leisure and Oil & Gas - with the IBEX (-0.4%) narrowly underperforming the region amid its exposure to these sectors. In terms of individual movers, BT (+4.6%) extends on gains following a well-received OFCOM spectrum auctions. Rolls-Royce (+3.6%) is bolstered by an upgrade at JPM. AstraZeneca (-0.7%) is softer in the run-up to the EMA verdict on the blood clot reports (due tomorrow), with France, Germany, Spain and Italy have said they are awaiting an investigation by the EU's regulator into reports of clots, set to be published tomorrow.

Top European News

- Dutch Go to Polls With Rutte Set for Fourth Straight Term

- Hargreaves Lansdown Sees Profit Boost on U.S. Share Trading

- Backing for Merkel’s Bloc Sinks After Drubbing in Regional Votes

- European Food & HPC Margin Prospects This Year Are ‘Weak:’ Citi

In FX, not the weakest G10 link by any means, but under pressure again and top heavy vs the Dollar above 1.1900 where 1.7 bn option expiries reside ahead of the Fed. However, the single currency has lurched some distance away from 1.2 bn at the 0.8600 strike against Sterling after stops at 0.8550 were finally tripped to push the cross down to test 2021 lows circa 0.8540 and underlying bids arrested a deeper retreat to expose the round number below. Hence, the Pound is being propped indirectly and gleaning sufficient support to stay within sight of the 1.3900 handle vs the Buck even though the DXY bounced towards 92.000 before fading again in the run up to the FOMC.

- AUD/NZD - Yet more dovish remarks and guidance for the Aussie to digest overnight, and this time from Deputy Governor Kent ramming home the 2-3% inflation goal before lifting rates from the effective lower bound. Nevertheless, Aud/Usd is holding 0.7700+ status and Aud/Nzd is still hovering above 1.0750, as the Kiwi treads cautiously into Q4 NZ GDP following minor beats in current account metrics and an unchanged deficit as a proportion of GDP. Nzd/Usd is currently near the bottom of a 0.7195-73 range and Aud/Usd is closer to 0.7722 than 0.7747 awaiting the RBA bulletin and jobs data more importantly.

- CAD/CHF/JPY - The Loonie, Franc and Yen remain locked within narrow bands against the Greenback, as Usd/Cad straddles 1.2450, Usd/Chf meanders between 0.9282-43 and Usd/Jpy continues to rotate around 109.00 in wake of worrying Japanese trade data revealing a much smaller than expected surplus due to a significantly larger than forecast fall in exports. Next up, Fed aside, Canadian CPI, Swiss producer/import prices and trade then Japanese inflation on the eve of the BoJ.

- SCANDI/EM - Another swing in the pendulum between the Swedish Krona and its Norwegian peer, with the former unwinding some of Tuesday’s recovery gains towards 10.1400 vs the Euro, but latter rebounding through 10.1000 in anticipation of a hawkish twist from the Norges Bank tomorrow. Similarly, the Turkish Lira is looking for a boost from the CBRT on Thursday, albeit in actual tightening terms even though the Government has taken steps to cap fuel prices in an effort to combat above target inflation. Usd/Try is around 7.5000, while Usd/Cnh is circa 6.5000 eyeing China’s high level summit with the US over the next 2 days. Elsewhere, softer crude is undermining the Mexican Peso and Russian Rouble, though the Rub is also embroiled in ongoing diplomatic spats, awaiting new US sanctions and ready to retaliate.

WTI and Brent front month were firmer heading into the European open but have since given up APAC gains and then some, with the initial leg lower seen in the run-up to the IEA monthly oil report. The gains overnight were spurred by the surprise draw of 1mln bbls in US private inventories (vs exp. +3mln bbls), but this upside lost steam as Europe entered the fray, with the temporary suspension of the AstraZeneca vaccine rollout, due to health concerns, potentially hampering recovery momentum against the backdrop of the slower inoculation seen in major EZ economies vs overseas. The IEA's report was a damp squib as the agency left its oil demand forecast unchanged from the prior report, deviating from the EIA and OPEC. IEA noted that oil demand is seen returning to 2019 levels by 2023 and noted that stronger demand and OPEC + output reductions point to sharp stocks draws in H2 2021. That being said, much of the OECD's vaccination momentum lies with tomorrow's EMA verdict on the reported AstraZeneca vaccine-related blood clots, with France, Germany, Spain and Italy poised to make their decision based on the EMA. In terms of today’s trade, oil has been choppy in the run-up to the weekly EIA stocks figures - which will be released at the early time of 14:30GMT to those across the pond - whilst markets await the FOMC rate decision & press conference. WTI trades around the mid-USD 64.00/bbl (vs high USD 65.34/bbl) and Brent trades sub-USD 68.00/bbl (vs high USD 68.89/bbl). Onto precious metals, spot gold and silver are seeing marginal upside but are within a contained range as they await the aforementioned FOMC. Spot gold trades around USD 1,735/oz and spot silver on either side of USD 26/oz as they track Dollar action. Regarding base metals LME copper is firmer and back above USD 9,000/t as the EV-led firm demand outlook coincides with supply disruptions in some South American mines. Elsewhere, Dalian coking coal rose over 5%, propped up by supply concerns and the robust demand outlook, with reports of plants also ramping up production to chase profit. Lastly, Rusal expects global demand for aluminium to grow by 6.1% in 2021.

US Event Calendar

- 8:30am: Feb. Building Permits est. 1.75m, prior 1.88m, revised 1.89m; MoM, est. -7.2%, prior 10.4%, revised 10.7%

- 8:30am: Feb. Housing Starts est. 1.56m, prior 1.58m; MoM, est. -1.3%, prior -6.0%

- 2pm: March Interest Rate on Excess Reserv, est. 0.10%, prior 0.10%

DB's Jim Reid concludes the overnight wrap

Today is all about the conclusion of the 2-day FOMC and Powell’s subsequent press conference with this meeting also including the latest economic projections and dot plot from the FOMC’s members. Back in December when the last dot plot was released, it showed that most of the committee favoured keeping rates on hold at least through to the end of 2023. But since then we’ve seen a sharp move higher in Treasury yields thanks to the passage of the $1.9tn stimulus package, and markets are now pricing in an initial hike from the Fed within the next 2 years and three hikes in total by the end of 2023. With a more robust outlook ahead, our US economists (link here) expect that one hike should be reflected in the committee’s updated projections out to end 2023 (via the median dot) but it’s a close call. However higher growth and lower unemployment will be in the forecasts, as well as a modestly higher inflation trajectory. The press conference may bring most of the focus though with every word scrutinised and cross examined given the recent run up in yields. Powell has now presided over 24 FOMCs and on average the S&P 500 has been -0.15% (15 out of the 24 were down days) lower on decision day – though this is heavily weighted by his first 7 meetings, which saw equities slip back when the Fed started its small hiking cycle in 2018. In terms of 10 year yields they have been -3.0bps lower on average with a median of -1.6bps (16 out 24 down in yield) on Powell FOMC days. To put this in perspective the S&P 500 is up +49.5% since his tenure begun in February 2018 and 10yr yields are down -108.8bps.

Yesterday saw risk assets a little mixed ahead of today’s meeting, as investors brushed off recent vaccine concerns in Europe to send European equity markets higher, while US equity markets were more two paced. The S&P 500 finished down -0.16%, just off its record high from Monday, though in more positive news the VIX volatility index fell -0.3pts to its lowest level since the pandemic began, at 19.8pts. Looking at the US equity moves in more depth, only 30% of the S&P 500 constituents saw their stocks rise yesterday, with a large majority of the gains concentrated in semiconductors (+1.31%), media (+1.04%) and tech hardware (+0.95%). This helped the NASDAQ eke out the slimmest of gains (+0.09%), while the NYSE FANG+ index was just on the other side of unchanged, falling -0.02%. In contrast, the small-cap Russell 2000 experienced a sharp -1.72% decline.

Furthermore, it’s worth noting that the recent recovery among big tech stocks has come in spite of the fact that bond yields have remained at elevated levels by recent standards, with the NASDAQ now up +6.75% since its recent low on the Monday of last week. Is stimulus money already going into retail favourites? One such favourite Tesla (-4.39%) was down on the day though and it must be significant that VW’s preferred shares (those in the DAX index) rose +6.71% (+9.3% at the intra-day peak) on the company’s plans of how they can beat Tesla to be the world’s leader in electric vehicles. The preferred shares are up +38.4% in 2021 and the company does seem to have attracted the retail bid as well, especially VW’s common shares which have a far lower float. That class of shares rose +25.7% at its highs yesterday before settling +13.32% higher. For the record Tesla and VW’s market caps are $649.7bn and $149.7bn respectively.

Over in bonds, those on 10yr US Treasuries closed up +1.4bps yesterday as the focus moved to today’s Federal Reserve meeting. But the bigger story was yet another rise in inflation expectations, which continued to move to fresh multi-year highs. The moves were evident across the curve, with both 2yr and 5yr US breakevens at their highest levels since 2008 yesterday, at 2.744% and 2.652% respectively, while 10yr breakevens were up +2.93bps to 2.304%, which hasn’t been seen since 2013. Interestingly, this shift wasn’t confined to the US either, with Euro Area 5y5y forward inflation swaps closing above 1.51% for the first time since March 2019, while 1yr German and Italian breakevens both rose to their highest levels since 2018 as well. So a sign that markets are increasingly pricing in a potential shift to a higher-inflation regime beyond just the next year or two.

Asian markets are trading weaker overnight with the Nikkei (-0.21%), Hang Seng (-0.34%), Shanghai Comp (-0.48%) and Kospi (-0.99% ) all down. Futures on the S&P 500 (-0.09%) are also trading slightly lower and the European ones are pointing to a weaker open. Yields on 10y USTs are trading broadly flat.

In other news, Samsung warned overnight that it’s grappling with the fallout from a “serious imbalance” in semiconductors globally with its co-CEO Koh Dong-jin saying that he expects the crunch to pose a problem to its business next quarter. This also indicated that chip shortages are now spreading beyond the auto making industry. Elsewhere, Huawei has said that it will begin charging mobile giants like Apple and Samsung, a “reasonable” fee for access to its portfolio of wireless 5G patents. Huawei has the largest such portfolio.

Turning to the pandemic, yesterday saw the head of the European Medicines Agency reaffirm the organisation’s message that the benefits of the AstraZeneca vaccine outweigh the potential for side effects, even with the moves from major European countries to suspend its usage while the EMA comes to its conclusions. Furthermore, she said that there wasn’t any indication that it was the vaccine that had caused the blood clot incidents, which were no higher than in the general population. We should get the full conclusions of the EMA’s review tomorrow following an extraordinary meeting, but given the different statements since the start of the week, it would be a big surprise if they didn’t indicate their approval. Furthermore, the UK has already vaccinated over 11m people with the AZ vaccine without reports of any issues, and is continuing its programme unaffected. Italian Prime Minister Draghi and French President Macron announced that they are both ready to allow use of the AZ vaccine immediately following advisement from the EMA.

European assets proved unfazed by the vaccine developments, and the STOXX 600 was up +0.88% yesterday to a fresh post-pandemic high, as the STOXX 600 travel and leisure index rose +0.80% to another record high. Core sovereign bonds saw little movement, with yields on 10yr bunds falling just -0.2bps and 10yr gilts down -1.2bps. However southern European debt underperformed, with yields on 10yr Italian (+2.7bps) and Greek (+4.2bps) debt both rising.

Looking at yesterday’s data, US retail sales in February fell by a stronger-than-expected -3.0% (vs. -0.5% expected), but given that the January reading was revised up to +7.6% (vs. +5.3% previously), the overall picture from the release was better than the headline number suggested. The industrial production numbers for February also saw a surprise fall of -2.2% (vs. +0.3% expected), but most of that decline could be explained by the severe winter weather last month.

To the day ahead now, and the highlight is likely to be the aforementioned FOMC meeting and Fed Chair Powell’s subsequent press conference. In addition, the ECB’s Elderson will be speaking. Separately, data releases include US housing starts and building permits for February, as well as EU new car registrations for the same month.

Government

Are Voters Recoiling Against Disorder?

Are Voters Recoiling Against Disorder?

Authored by Michael Barone via The Epoch Times (emphasis ours),

The headlines coming out of the Super…

Share this:

Authored by Michael Barone via The Epoch Times (emphasis ours),

The headlines coming out of the Super Tuesday primaries have got it right. Barring cataclysmic changes, Donald Trump and Joe Biden will be the Republican and Democratic nominees for president in 2024.

With Nikki Haley’s withdrawal, there will be no more significantly contested primaries or caucuses—the earliest both parties’ races have been over since something like the current primary-dominated system was put in place in 1972.

The primary results have spotlighted some of both nominees’ weaknesses.

Donald Trump lost high-income, high-educated constituencies, including the entire metro area—aka the Swamp. Many but by no means all Haley votes there were cast by Biden Democrats. Mr. Trump can’t afford to lose too many of the others in target states like Pennsylvania and Michigan.

Majorities and large minorities of voters in overwhelmingly Latino counties in Texas’s Rio Grande Valley and some in Houston voted against Joe Biden, and even more against Senate nominee Rep. Colin Allred (D-Texas).

Returns from Hispanic precincts in New Hampshire and Massachusetts show the same thing. Mr. Biden can’t afford to lose too many Latino votes in target states like Arizona and Georgia.

When Mr. Trump rode down that escalator in 2015, commentators assumed he’d repel Latinos. Instead, Latino voters nationally, and especially the closest eyewitnesses of Biden’s open-border policy, have been trending heavily Republican.

High-income liberal Democrats may sport lawn signs proclaiming, “In this house, we believe ... no human is illegal.” The logical consequence of that belief is an open border. But modest-income folks in border counties know that flows of illegal immigrants result in disorder, disease, and crime.

There is plenty of impatience with increased disorder in election returns below the presidential level. Consider Los Angeles County, America’s largest county, with nearly 10 million people, more people than 40 of the 50 states. It voted 71 percent for Mr. Biden in 2020.

Current returns show county District Attorney George Gascon winning only 21 percent of the vote in the nonpartisan primary. He’ll apparently face Republican Nathan Hochman, a critic of his liberal policies, in November.

Gascon, elected after the May 2020 death of counterfeit-passing suspect George Floyd in Minneapolis, is one of many county prosecutors supported by billionaire George Soros. His policies include not charging juveniles as adults, not seeking higher penalties for gang membership or use of firearms, and bringing fewer misdemeanor cases.

The predictable result has been increased car thefts, burglaries, and personal robberies. Some 120 assistant district attorneys have left the office, and there’s a backlog of 10,000 unprosecuted cases.

More than a dozen other Soros-backed and similarly liberal prosecutors have faced strong opposition or have left office.

St. Louis prosecutor Kim Gardner resigned last May amid lawsuits seeking her removal, Milwaukee’s John Chisholm retired in January, and Baltimore’s Marilyn Mosby was defeated in July 2022 and convicted of perjury in September 2023. Last November, Loudoun County, Virginia, voters (62 percent Biden) ousted liberal Buta Biberaj, who declined to prosecute a transgender student for assault, and in June 2022 voters in San Francisco (85 percent Biden) recalled famed radical Chesa Boudin.

Similarly, this Tuesday, voters in San Francisco passed ballot measures strengthening police powers and requiring treatment of drug-addicted welfare recipients.

In retrospect, it appears the Floyd video, appearing after three months of COVID-19 confinement, sparked a frenzied, even crazed reaction, especially among the highly educated and articulate. One fatal incident was seen as proof that America’s “systemic racism” was worse than ever and that police forces should be defunded and perhaps abolished.

2020 was “the year America went crazy,” I wrote in January 2021, a year in which police funding was actually cut by Democrats in New York, Los Angeles, San Francisco, Seattle, and Denver. A year in which young New York Times (NYT) staffers claimed they were endangered by the publication of Sen. Tom Cotton’s (R-Ark.) opinion article advocating calling in military forces if necessary to stop rioting, as had been done in Detroit in 1967 and Los Angeles in 1992. A craven NYT publisher even fired the editorial page editor for running the article.

Evidence of visible and tangible discontent with increasing violence and its consequences—barren and locked shelves in Manhattan chain drugstores, skyrocketing carjackings in Washington, D.C.—is as unmistakable in polls and election results as it is in daily life in large metropolitan areas. Maybe 2024 will turn out to be the year even liberal America stopped acting crazy.

Chaos and disorder work against incumbents, as they did in 1968 when Democrats saw their party’s popular vote fall from 61 percent to 43 percent.

Views expressed in this article are opinions of the author and do not necessarily reflect the views of The Epoch Times or ZeroHedge.

Government

Veterans Affairs Kept COVID-19 Vaccine Mandate In Place Without Evidence

Veterans Affairs Kept COVID-19 Vaccine Mandate In Place Without Evidence

Authored by Zachary Stieber via The Epoch Times (emphasis ours),

The…

Share this:

Authored by Zachary Stieber via The Epoch Times (emphasis ours),

The U.S. Department of Veterans Affairs (VA) reviewed no data when deciding in 2023 to keep its COVID-19 vaccine mandate in place.

VA Secretary Denis McDonough said on May 1, 2023, that the end of many other federal mandates “will not impact current policies at the Department of Veterans Affairs.”

He said the mandate was remaining for VA health care personnel “to ensure the safety of veterans and our colleagues.”

Mr. McDonough did not cite any studies or other data. A VA spokesperson declined to provide any data that was reviewed when deciding not to rescind the mandate. The Epoch Times submitted a Freedom of Information Act for “all documents outlining which data was relied upon when establishing the mandate when deciding to keep the mandate in place.”

The agency searched for such data and did not find any.

“The VA does not even attempt to justify its policies with science, because it can’t,” Leslie Manookian, president and founder of the Health Freedom Defense Fund, told The Epoch Times.

“The VA just trusts that the process and cost of challenging its unfounded policies is so onerous, most people are dissuaded from even trying,” she added.

The VA’s mandate remains in place to this day.

The VA’s website claims that vaccines “help protect you from getting severe illness” and “offer good protection against most COVID-19 variants,” pointing in part to observational data from the U.S. Centers for Disease Control and Prevention (CDC) that estimate the vaccines provide poor protection against symptomatic infection and transient shielding against hospitalization.

There have also been increasing concerns among outside scientists about confirmed side effects like heart inflammation—the VA hid a safety signal it detected for the inflammation—and possible side effects such as tinnitus, which shift the benefit-risk calculus.

President Joe Biden imposed a slate of COVID-19 vaccine mandates in 2021. The VA was the first federal agency to implement a mandate.

President Biden rescinded the mandates in May 2023, citing a drop in COVID-19 cases and hospitalizations. His administration maintains the choice to require vaccines was the right one and saved lives.

“Our administration’s vaccination requirements helped ensure the safety of workers in critical workforces including those in the healthcare and education sectors, protecting themselves and the populations they serve, and strengthening their ability to provide services without disruptions to operations,” the White House said.

Some experts said requiring vaccination meant many younger people were forced to get a vaccine despite the risks potentially outweighing the benefits, leaving fewer doses for older adults.

“By mandating the vaccines to younger people and those with natural immunity from having had COVID, older people in the U.S. and other countries did not have access to them, and many people might have died because of that,” Martin Kulldorff, a professor of medicine on leave from Harvard Medical School, told The Epoch Times previously.

The VA was one of just a handful of agencies to keep its mandate in place following the removal of many federal mandates.

“At this time, the vaccine requirement will remain in effect for VA health care personnel, including VA psychologists, pharmacists, social workers, nursing assistants, physical therapists, respiratory therapists, peer specialists, medical support assistants, engineers, housekeepers, and other clinical, administrative, and infrastructure support employees,” Mr. McDonough wrote to VA employees at the time.

“This also includes VA volunteers and contractors. Effectively, this means that any Veterans Health Administration (VHA) employee, volunteer, or contractor who works in VHA facilities, visits VHA facilities, or provides direct care to those we serve will still be subject to the vaccine requirement at this time,” he said. “We continue to monitor and discuss this requirement, and we will provide more information about the vaccination requirements for VA health care employees soon. As always, we will process requests for vaccination exceptions in accordance with applicable laws, regulations, and policies.”

The version of the shots cleared in the fall of 2022, and available through the fall of 2023, did not have any clinical trial data supporting them.

A new version was approved in the fall of 2023 because there were indications that the shots not only offered temporary protection but also that the level of protection was lower than what was observed during earlier stages of the pandemic.

Ms. Manookian, whose group has challenged several of the federal mandates, said that the mandate “illustrates the dangers of the administrative state and how these federal agencies have become a law unto themselves.”

Government

Low Iron Levels In Blood Could Trigger Long COVID: Study

Low Iron Levels In Blood Could Trigger Long COVID: Study

Authored by Amie Dahnke via The Epoch Times (emphasis ours),

People with inadequate…

Share this:

{kind=link}

{kind=link}

Authored by Amie Dahnke via The Epoch Times (emphasis ours),

People with inadequate iron levels in their blood due to a COVID-19 infection could be at greater risk of long COVID.

{kind=link}

A new study indicates that problems with iron levels in the bloodstream likely trigger chronic inflammation and other conditions associated with the post-COVID phenomenon. The findings, published on March 1 in Nature Immunology, could offer new ways to treat or prevent the condition.

Long COVID Patients Have Low Iron Levels

Researchers at the University of Cambridge pinpointed low iron as a potential link to long-COVID symptoms thanks to a study they initiated shortly after the start of the pandemic. They recruited people who tested positive for the virus to provide blood samples for analysis over a year, which allowed the researchers to look for post-infection changes in the blood. The researchers looked at 214 samples and found that 45 percent of patients reported symptoms of long COVID that lasted between three and 10 months.

In analyzing the blood samples, the research team noticed that people experiencing long COVID had low iron levels, contributing to anemia and low red blood cell production, just two weeks after they were diagnosed with COVID-19. This was true for patients regardless of age, sex, or the initial severity of their infection.

According to one of the study co-authors, the removal of iron from the bloodstream is a natural process and defense mechanism of the body.

But it can jeopardize a person’s recovery.

“When the body has an infection, it responds by removing iron from the bloodstream. This protects us from potentially lethal bacteria that capture the iron in the bloodstream and grow rapidly. It’s an evolutionary response that redistributes iron in the body, and the blood plasma becomes an iron desert,” University of Oxford professor Hal Drakesmith said in a press release. “However, if this goes on for a long time, there is less iron for red blood cells, so oxygen is transported less efficiently affecting metabolism and energy production, and for white blood cells, which need iron to work properly. The protective mechanism ends up becoming a problem.”

The research team believes that consistently low iron levels could explain why individuals with long COVID continue to experience fatigue and difficulty exercising. As such, the researchers suggested iron supplementation to help regulate and prevent the often debilitating symptoms associated with long COVID.

“It isn’t necessarily the case that individuals don’t have enough iron in their body, it’s just that it’s trapped in the wrong place,” Aimee Hanson, a postdoctoral researcher at the University of Cambridge who worked on the study, said in the press release. “What we need is a way to remobilize the iron and pull it back into the bloodstream, where it becomes more useful to the red blood cells.”

The research team pointed out that iron supplementation isn’t always straightforward. Achieving the right level of iron varies from person to person. Too much iron can cause stomach issues, ranging from constipation, nausea, and abdominal pain to gastritis and gastric lesions.

1 in 5 Still Affected by Long COVID

COVID-19 has affected nearly 40 percent of Americans, with one in five of those still suffering from symptoms of long COVID, according to the U.S. Centers for Disease Control and Prevention (CDC). Long COVID is marked by health issues that continue at least four weeks after an individual was initially diagnosed with COVID-19. Symptoms can last for days, weeks, months, or years and may include fatigue, cough or chest pain, headache, brain fog, depression or anxiety, digestive issues, and joint or muscle pain.

Veterans Affairs Kept COVID-19 Vaccine Mandate In Place Without Evidence

When Military Rule Supplants Democracy

The Digest #187

Redefining Poverty: Towards a Transpartisan Approach

Students lose out as cities and states give billions in property tax breaks to businesses − draining school budgets and especially hurting the poorest students

Is the United States overestimating China’s power?

Biden to call for first-time homebuyer tax credit, construction of 2 million homes

GBPINR: Analysis and Projections for 2024

Low Iron Levels In Blood Could Trigger Long COVID: Study

Walmart has really good news for shoppers (and Joe Biden)

-

Uncategorized2 weeks ago

Uncategorized2 weeks agoAll Of The Elements Are In Place For An Economic Crisis Of Staggering Proportions

-

Uncategorized1 month ago

Uncategorized1 month agoCathie Wood sells a major tech stock (again)

-

Uncategorized3 weeks ago

Uncategorized3 weeks agoCalifornia Counties Could Be Forced To Pay $300 Million To Cover COVID-Era Program

-

Uncategorized2 weeks ago

Uncategorized2 weeks agoApparel Retailer Express Moving Toward Bankruptcy

-

Uncategorized3 weeks ago

Uncategorized3 weeks agoIndustrial Production Decreased 0.1% in January

-

International2 days ago

International2 days agoWalmart launches clever answer to Target’s new membership program

-

International2 days ago

International2 days agoEyePoint poaches medical chief from Apellis; Sandoz CFO, longtime BioNTech exec to retire

-

Uncategorized3 weeks ago

Uncategorized3 weeks agoRFK Jr: The Wuhan Cover-Up & The Rise Of The Biowarfare-Industrial Complex