"It’s A Civil War": Decade Of Covenant-Lite Deals Leads To Leveraged Loan "Panic"Tyler DurdenWed, 10/07/2020 - 20:06

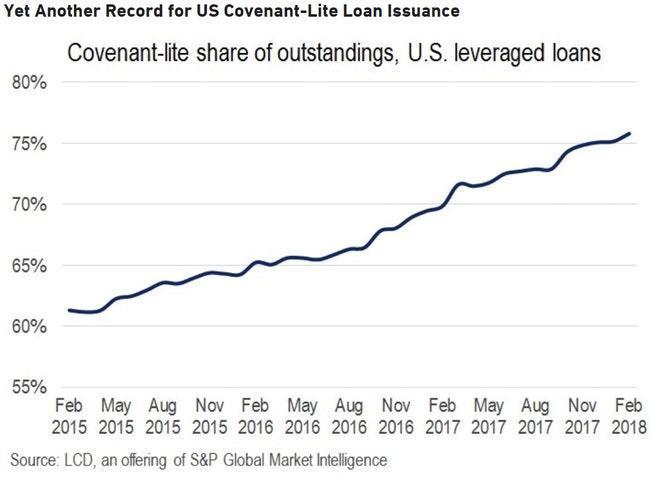

It was a little over two years ago that we last looked at the "covenant lite" insanity sweeping the loan market for the past decade, where as a result of a buying frenzy among yield-starved investors, corporations had managed to get away with selling "secured" debt that was anything but secured, and offered only the slimmest - if any - protections to investors. In fact, by early 2018, the amount of covenant-lite loans hit an unprecedented 75%...

... which meant that Moody's Loan Covenant Quality Indicator (LCQI) dropped to its record-worst level in the first quarter of 2018.

"While the rate of deterioration in covenant quality has slowed, protections remain distressingly weak on average," said Derek Gluckman, Moody's VP-Senior Covenant Officer. "Investors should remain wary given the risks presented by most loan documents and the likelihood that any steadying of covenant protections is temporary."

But it wasn't just the sheer volume of cov-lite outstandings that mattered: an analysis by LCD looked at the debt cushion of outstanding loans – the amount of debt in a borrower’s capital structure that is subordinated to the senior loan – and found that most cov-lite deals have little or no debt cushion beneath them. Consider that by mid-2018, an all time high 23% of all cov-lite loans did not have any debt, such as a mezzanine tranche, high yield bond, or other, below the cov-lite facility. That number was up from 18% in 2013 and from just 10% at the end of 2007, shortly before the financial crisis.

This is also why we explicitly warned that "the lack of a debt cushion significantly lessens what an investor will recover on a loan, if that credit defaults" and left readers with the following:

In other words, during the next default cycle, whenever the business cycle finally turns, loan investors not only will have virtually no "secured" protection, but are now the de facto equity tranche in numerous deals, or said otherwise, for the first time in history, loan investors are looking at 0 recoveries in default.

Well, fast forward to today when the chickens from the covenant-lite euphoria of the past decade have come home... for the slaughter.

In a transaction which has terminally tilted the "landscape in favor of distressed borrowers and pitted creditors against each other" a $120 million loan to cash-strapped restaurant supplier TriMark USA has "not only unilaterally placed the new lenders above everyone else in the repayment pecking order, but it also stripped some of the older creditors of safeguards they had written into the contracts to protect their investments" according to Bloomberg, which notes that when word of the deal spearheaded by Howard Marks and his distressed debt giant, Oaktree, first hit the market in mid-September, "it sparked a panic", prompting investors to puke the old loan so fast it cratered 20 cents in days, an unheard of move in the world of secured finance where underlying assets never reprice so fast, even in bankruptcy.

Of course, for those who had been following the degradation of creditor protections and the ascent of cov-lite deals over the past decade, what just took place is hardly a surprise: as investors bargained away most of their legal rights in hopes of getting a modest allocation in the latest "high yielding" note, they now find themselves with virtually no protection for their investments just as the pandemic is causing a wave of corporate bankruptcies across the country.

And just to underscore that "anything goes" in the brave new world of leveraged (and unsecured) loans, the presence of Marks - who had long been seen as one of the more staid voices in a distressed-debt world full of pugnacious vultures - served to upend the market only further and spark fears about what is coming next as tens of billions of other "secured" loans are about to see their investors crammed down or otherwise wiped out, just as we warned in 2018.

"It’s a civil war between lenders, and we’re going to see more of this," said Thomas Majewski, managing partner and founder at Eagle Point Credit Management. “Nearly every company restructuring debt is looking at these possibilities.”

So what exactly happened?

The TriMark transaction, which according to Bloomberg was similar to another loan that surf-clothing maker Boardriders entered recently, followed in the "priming" footsteps of a divisive financing by Serta Simmons Bedding earlier this year. The mattress maker got $200 million of fresh capital from existing lenders including Eaton Vance Corp. and Invesco Ltd. Those lenders jumped to the top of the capital stack meaning they would be repaid first if the company defaulted, pushing Serta Simmons’ other lenders further back, in a process known as priming.

There’s nothing new about priming - in fact it happens all the time in bankruptcy when a company issues what is known as a "priming DIP" - but the way lenders did it in the Serta Simmons deal resulted in litigation. The new investor group led by Eaton Vance and Invesco didn’t give all other lenders the right to participate in the new loan, a move that is allowed by many deals’ documents, but hadn’t really been done before. Lenders who were left out, including Apollo Global Management, sued the company but a state court let the deal go ahead, ushering in a new precedent in the market where existing "secured" creditors hiding behind the thin defense of non-existent covenants, realize they are in fact, unsecured.

“Serta did open the floodgates in that regard,” said Tim Sullivan, an analyst at Xtract Research, "because it showed how provisions which are very common in agreements today can be used to incur priming debt."

Of course, creditors have only themselves to fault: nobody put a gun to their heads in 2010-2018 when they signed the dotted line on yet another high-yielding loan that offered no covenant protection. Yet they just had to do it. Well, now that the catastrophic event that nobody thought could possibly happen happened, and as investors pore through their covenant term sheets, they finally realize why all those warnings over the past decade hit home.

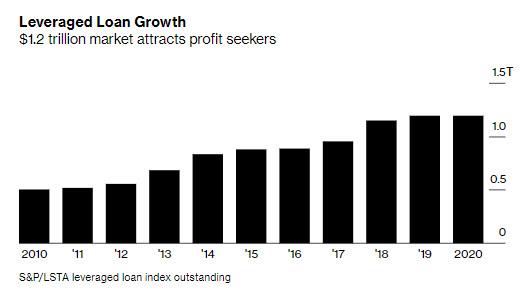

The catalyst for this realization, of course, is the covid crisis, as a result of which countless companies in the U.S. are going broke as the pandemic saps their revenues. Fitch Ratings projects 7% to 8% of leveraged loans will default by the end of 2021, compared with 1.8% in 2019, a cataclysmic event for the $1.2 trillion loan market. Making matters worse, after years of the loan market growing rapidly, failing corporations that issued debt and pledged assets now have less in the way of income or assets to fork over to creditors, which is making fights among all parties more acrimonious.

It also means that those investors with fresh capital can trample over the gullible ones who received a couple of years of interest payments and are now facing near complete losses on principal.

In the case of Boardriders, Oaktree was one of the equity owners: as Bloomberg details, the company negotiated a $135 million financing including a $45 million loan that has priority over all others. The debt came from Boardriders’ bigger lenders, a group that included Brigade Capital Management, Canyon Capital and MidOcean Credit Partners, according to people with knowledge of the situation.

The $45 million loan, which is effectively a pre-petition DIP, ranks ahead of all investors that didn’t participate in the new financing. Just as a secured bankruptcy loan does. The minority lenders that were primed argue that was unfair because they weren’t given a chance to participate in the deal, the people said. Good luck to them: meanwhile, the new loan which is secured by all the assets, is trading around 100 cents on the dollar; the old loan that was primed? About a third of that, or around 35 cents.

The situation was similar for TriMark. The company saw its revenue falling and hired advisers to help it consider its options. It ultimately picked a transaction to raise $120 million from lenders including Oaktree and Ares Management Corp. The group of existing lenders also included Blackstone’s credit arm GSO Capital Partners, Sculptor Capital Management, and BlackRock. Their new loan is trading around face value, about 40 cents on the dollar higher than the loan that was primed. TriMark is owned by Centerbridge, which is about to get a big fat doughnut on its investment.

So how did the new investors prime existing lenders? In both Boardriders and TriMark, minority lenders had covenants including limits on future company borrowings removed, while the debt amortization schedule was slowed down.

According to Etract’s Sullivan, the additional step of removing covenants is highly unusual in the loan world and is a big loss for investors. On the other hand, such covenant stripping would never had been possible if the loans were not covenant-lite to begin with.

“It’s gone beyond Serta -- now it’s worse. By stripping it down to the ultra bare bones, all that leaves you with is just a promise to pay,” he said.

It also means that the entire $1.2 trillion universe of secured loans - because by definition first and second-lien bank debt is secured by company assets and has first dibs on them in case of default - is effectively no longer secured.

* * *

To be sure the primed lenders are fighting back, and some companies are deciding not to embrace these transactions (they can of course do that, but one way or another a priming loan will come, the only difference is that if it is in bankruptcy, it is called a DIP Loan). Meanwhile, covenant lite deals have resulted in even more ingenious instances of asset stripping. In May debtholders rebelled against Elliott Management and Siris Capital Group, the owners of global travel reservation company Travelport, after those two firms tried to move assets out of the reach of creditors. And when Oaktree proposed a priming transaction for PSAV, the borrower elected to raise new capital through a loan that was in the same class as the existing facility.

"Priming transactions such as those executed by Serta and Boardriders are still the exception and the priming play is not the ‘new normal,’” said Judah Gross, a director at Fitch Ratings. "That being said, the higher degree of frequency with which such deals get done may indicate that priming transactions are not as taboo as once assumed."

He is right, and the real kicker will take place some time in 2021 if there is no new fiscal stimulus, and a default wave washes over the leveraged loan market: only then will our warning from 2018 become clear - years of issuance of loans that were "secured" only in name, has ensured that recoveries for these unsecured creditors will be the lowest in history; in fact depending on the severity of the coming double dip, it is likely that "secured" lenders are looking at the unthinkable - a total wipeout on principal.

It was Jan. 11, 2024 when software giant Microsoft (MSFT) briefly passed Apple (AAPL) as the most valuable company in the world.

Microsoft's stock closed 0.5% higher, giving it a market valuation of $2.859 trillion.

It rose as much as 2% during the session and the company was briefly worth $2.903 trillion. Apple closed 0.3% lower, giving the company a market capitalization of $2.886 trillion.

"It was inevitable that Microsoft would overtake Apple since Microsoft is growing faster and has more to benefit from the generative AI revolution," D.A. Davidson analyst Gil Luria said at the time, according to Reuters.

The two tech titans have jostled for top spot over the years and Microsoft was ahead at last check, with a market cap of $3.085 trillion, compared with Apple's value of $2.684 trillion.

Analysts noted that Apple had been dealing with weakening demand, including for the iPhone, the company’s main source of revenue.

Demand in China, a major market, has slumped as the country's economy makes a slow recovery from the pandemic and competition from Huawei.

Sales in China of Apple's iPhone fell by 24% in the first six weeks of 2024 compared with a year earlier, according to research firm Counterpoint, as the company contended with stiff competition from a resurgent Huawei "while getting squeezed in the middle on aggressive pricing from the likes of OPPO, vivo and Xiaomi," said senior Analyst Mengmeng Zhang.

“Although the iPhone 15 is a great device, it has no significant upgrades from the previous version, so consumers feel fine holding on to the older-generation iPhones for now," he said.

A man scrolling through Netflix on an Apple iPad Pro. Photo by Phil Barker/Future Publishing via Getty Images.

Counterpoint said that the first six weeks of 2023 saw abnormally high numbers with significant unit sales being deferred from December 2022 due to production issues.

Apple is planning to open its eighth store in Shanghai – and its 47th across China – on March 21.

The company also plans to expand its research centre in Shanghai to support all of its product lines and open a new lab in southern tech hub Shenzhen later this year, according to the South China Morning Post.

Meanwhile, over in Europe, Apple announced changes to comply with the European Union's Digital Markets Act (DMA), which went into effect last week, Reuters reported on March 12.

Beginning this spring, software developers operating in Europe will be able to distribute apps to EU customers directly from their own websites instead of through the App Store.

"To reflect the DMA’s changes, users in the EU can install apps from alternative app marketplaces in iOS 17.4 and later," Apple said on its website, referring to the software platform that runs iPhones and iPads.

"Users will be able to download an alternative marketplace app from the marketplace developer’s website," the company said.

Apple has also said it will appeal a $2 billion EU antitrust fine for thwarting competition from Spotify (SPOT) and other music streaming rivals via restrictions on the App Store.

The company's shares have suffered amid all this upheaval, but some analysts still see good things in Apple's future.

Bank of America Securities confirmed its positive stance on Apple, maintaining a buy rating with a steady price target of $225, according to Investing.com.

The firm's analysis highlighted Apple's pricing strategy evolution since the introduction of the first iPhone in 2007, with initial prices set at $499 for the 4GB model and $599 for the 8GB model.

BofA said that Apple has consistently launched new iPhone models, including the Pro/Pro Max versions, to target the premium market.

Analyst says Apple selloff 'overdone'

Concurrently, prices for previous models are typically reduced by about $100 with each new release.

This strategy, coupled with installment plans from Apple and carriers, has contributed to the iPhone's installed base reaching a record 1.2 billion in 2023, the firm said.

Apple has effectively shifted its sales mix toward higher-value units despite experiencing slower unit sales, BofA said.

This trend is expected to persist and could help mitigate potential unit sales weaknesses, particularly in China.

BofA also noted Apple's dominance in the high-end market, maintaining a market share of over 90% in the $1,000 and above price band for the past three years.

The firm also cited the anticipation of a multi-year iPhone cycle propelled by next-generation AI technology, robust services growth, and the potential for margin expansion.

On Monday, Evercore ISI analysts said they believed that the sell-off in the iPhone maker’s shares may be “overdone.”

The firm said that investors' growing preference for AI-focused stocks like Nvidia (NVDA) has led to a reallocation of funds away from Apple.

In addition, Evercore said concerns over weakening demand in China, where Apple may be losing market share in the smartphone segment, have affected investor sentiment.

And then ongoing regulatory issues continue to have an impact on investor confidence in the world's second-biggest company.

“We think the sell-off is rather overdone, while we suspect there is strong valuation support at current levels to down 10%, there are three distinct drivers that could unlock upside on the stock from here – a) Cap allocation, b) AI inferencing, and c) Risk-off/defensive shift," the firm said in a research note.

Major typhoid fever surveillance study in sub-Saharan Africa indicates need for the introduction of typhoid conjugate vaccines in endemic countries

There is a high burden of typhoid fever in sub-Saharan African countries, according to a new study published today in The Lancet Global Health. This high…

There is a high burden of typhoid fever in sub-Saharan African countries, according to a new study published today in The Lancet Global Health. This high burden combined with the threat of typhoid strains resistant to antibiotic treatment calls for stronger prevention strategies, including the use and implementation of typhoid conjugate vaccines (TCVs) in endemic settings along with improvements in access to safe water, sanitation, and hygiene.

Credit: IVI

There is a high burden of typhoid fever in sub-Saharan African countries, according to a new study published today in The Lancet Global Health. This high burden combined with the threat of typhoid strains resistant to antibiotic treatment calls for stronger prevention strategies, including the use and implementation of typhoid conjugate vaccines (TCVs) in endemic settings along with improvements in access to safe water, sanitation, and hygiene.

The findings from this 4-year study, the Severe Typhoid in Africa (SETA) program, offers new typhoid fever burden estimates from six countries: Burkina Faso, Democratic Republic of the Congo (DRC), Ethiopia, Ghana, Madagascar, and Nigeria, with four countries recording more than 100 cases for every 100,000 person-years of observation, which is considered a high burden. The highest incidence of typhoid was found in DRC with 315 cases per 100,000 people while children between 2-14 years of age were shown to be at highest risk across all 25 study sites.

There are an estimated 12.5 to 16.3 million cases of typhoid every year with 140,000 deaths. However, with generic symptoms such as fever, fatigue, and abdominal pain, and the need for blood culture sampling to make a definitive diagnosis, it is difficult for governments to capture the true burden of typhoid in their countries.

“Our goal through SETA was to address these gaps in typhoid disease burden data,” said lead author Dr. Florian Marks, Deputy Director General of the International Vaccine Institute (IVI). “Our estimates indicate that introduction of TCV in endemic settings would go to lengths in protecting communities, especially school-aged children, against this potentially deadly—but preventable—disease.”

In addition to disease incidence, this study also showed that the emergence of antimicrobial resistance (AMR) in Salmonella Typhi, the bacteria that causes typhoid fever, has led to more reliance beyond the traditional first line of antibiotic treatment. If left untreated, severe cases of the disease can lead to intestinal perforation and even death. This suggests that prevention through vaccination may play a critical role in not only protecting against typhoid fever but reducing the spread of drug-resistant strains of the bacteria.

There are two TCVs prequalified by the World Health Organization (WHO) and available through Gavi, the Vaccine Alliance. In February 2024, IVI and SK bioscience announced that a third TCV, SKYTyphoid™, also achieved WHO PQ, paving the way for public procurement and increasing the global supply.

Alongside the SETA disease burden study, IVI has been working with colleagues in three African countries to show the real-world impact of TCV vaccination. These studies include a cluster-randomized trial in Agogo, Ghana and two effectiveness studies following mass vaccination in Kisantu, DRC and Imerintsiatosika, Madagascar.

Dr. Birkneh Tilahun Tadesse, Associate Director General at IVI and Head of the Real-World Evidence Department, explains, “Through these vaccine effectiveness studies, we aim to show the full public health value of TCV in settings that are directly impacted by a high burden of typhoid fever.” He adds, “Our final objective of course is to eliminate typhoid or to at least reduce the burden to low incidence levels, and that’s what we are attempting in Fiji with an island-wide vaccination campaign.”

As more countries in typhoid endemic countries, namely in sub-Saharan Africa and South Asia, consider TCV in national immunization programs, these data will help inform evidence-based policy decisions around typhoid prevention and control.

###

About the International Vaccine Institute (IVI)

The International Vaccine Institute (IVI) is a non-profit international organization established in 1997 at the initiative of the United Nations Development Programme with a mission to discover, develop, and deliver safe, effective, and affordable vaccines for global health.

IVI’s current portfolio includes vaccines at all stages of pre-clinical and clinical development for infectious diseases that disproportionately affect low- and middle-income countries, such as cholera, typhoid, chikungunya, shigella, salmonella, schistosomiasis, hepatitis E, HPV, COVID-19, and more. IVI developed the world’s first low-cost oral cholera vaccine, pre-qualified by the World Health Organization (WHO) and developed a new-generation typhoid conjugate vaccine that is recently pre-qualified by WHO.

IVI is headquartered in Seoul, Republic of Korea with a Europe Regional Office in Sweden, a Country Office in Austria, and Collaborating Centers in Ghana, Ethiopia, and Madagascar. 39 countries and the WHO are members of IVI, and the governments of the Republic of Korea, Sweden, India, Finland, and Thailand provide state funding. For more information, please visit https://www.ivi.int.

Incidence of typhoid fever in Burkina Faso, Democratic Republic of the Congo, Ethiopia, Ghana, Madagascar, and Nigeria (the Severe Typhoid in Africa programme): a population-based study

We’ve added 60% to national debt since 2018. Germany - a country with major economic woes - added ‘just’ 32%.

Maybe it will never matter. Maybe MMT is real. Maybe we just cancel or inflate it out. Maybe career real estate borrowers or career politicians aren’t the answer.

I have no idea. Only time will tell. But it’s going to be fascinating to watch it play out.

He is right: it will be fascinating, and the latest budget deficit data simply confirmed that the day of reckoning will come very soon, certainly sooner than the two years that One River's Eric Peters predicted this weekend for the coming "US debt sustainability crisis."

According to the US Treasury, in February, the US collected $271 billion in various tax receipts, and spent $567 billion, more than double what it collected.

The two charts below show the divergence in US tax receipts which have flatlined (on a trailing 6M basis) since the covid pandemic in 2020 (with occasional stimmy-driven surges)...

... and spending which is about 50% higher compared to where it was in 2020.

The end result is that in February, the budget deficit rose to $296.3 billion, up 12.9% from a year prior, and the second highest February deficit on record.

And the punchline: on a cumulative basis, the budget deficit in fiscal 2024 which began on October 1, 2023 is now $828 billion, the second largest cumulative deficit through February on record, surpassed only by the peak covid year of 2021.

But wait there's more: because in a world where the US is spending more than twice what it is collecting, the endgame is clear: debt collapse, and while it won't be tomorrow, or the week after, it is coming... and it's also why the US is now selling $1 trillion in debt every 100 days just to keep operating (and absorbing all those millions of illegal immigrants who will keep voting democrat to preserve the socialist system of the US, so beloved by the Soros clan).

... having already surpassed total US defense spending and soon to surpass total health spending and, finally all social security spending, the largest spending category of all, which means that US debt will now rise exponentially higher until the inevitable moment when the US dollar loses its reserve status and it all comes crashing down.

We conclude with another observation by CNBC's Brian Sullivan, who quotes an email by a DC strategist...

.. which lays out the proposed Biden budget as follows:

The budget deficit will growth another $16 TRILLION over next 10 years. Thats *with* the proposed massive tax hikes.

Without them the deficit will grow $19 trillion.

That's why you will hear the "deficit is being reduced by $3 trillion" over the decade.

No family budget or business could exist with this kind of math.

Of course, in the long run, neither can the US... and since neither party will ever cut the spending which everyone by now is so addicted to, the best anyone can do is start planning for the endgame.

We use cookies on our website to give you the most relevant experience by remembering your preferences and repeat visits. By clicking “Accept”, you consent to the use of ALL the cookies.

This website uses cookies to improve your experience while you navigate through the website. Out of these, the cookies that are categorized as necessary are stored on your browser as they are essential for the working of basic functionalities of the website. We also use third-party cookies that help us analyze and understand how you use this website. These cookies will be stored in your browser only with your consent. You also have the option to opt-out of these cookies. But opting out of some of these cookies may affect your browsing experience.

Necessary cookies are absolutely essential for the website to function properly. These cookies ensure basic functionalities and security features of the website, anonymously.

Cookie

Duration

Description

cookielawinfo-checbox-analytics

11 months

This cookie is set by GDPR Cookie Consent plugin. The cookie is used to store the user consent for the cookies in the category "Analytics".

cookielawinfo-checbox-functional

11 months

The cookie is set by GDPR cookie consent to record the user consent for the cookies in the category "Functional".

cookielawinfo-checbox-others

11 months

This cookie is set by GDPR Cookie Consent plugin. The cookie is used to store the user consent for the cookies in the category "Other.

cookielawinfo-checkbox-necessary

11 months

This cookie is set by GDPR Cookie Consent plugin. The cookies is used to store the user consent for the cookies in the category "Necessary".

cookielawinfo-checkbox-performance

11 months

This cookie is set by GDPR Cookie Consent plugin. The cookie is used to store the user consent for the cookies in the category "Performance".

viewed_cookie_policy

11 months

The cookie is set by the GDPR Cookie Consent plugin and is used to store whether or not user has consented to the use of cookies. It does not store any personal data.

Functional cookies help to perform certain functionalities like sharing the content of the website on social media platforms, collect feedbacks, and other third-party features.

Performance cookies are used to understand and analyze the key performance indexes of the website which helps in delivering a better user experience for the visitors.

Analytical cookies are used to understand how visitors interact with the website. These cookies help provide information on metrics the number of visitors, bounce rate, traffic source, etc.

Advertisement cookies are used to provide visitors with relevant ads and marketing campaigns. These cookies track visitors across websites and collect information to provide customized ads.

{kind=link}