Uncategorized

Is the Metaverse really turning out like ‘Snow Crash’?

Neal Stephenson’s science fiction novel Snow Crash predicted the Metaverse in 1992. This cult book has the amusingly-named Hiro Protagonist running around…

Share this:

Neal Stephenson’s science fiction novel Snow Crash predicted the Metaverse in 1992. This cult book has the amusingly-named Hiro Protagonist running around in an artificial cyber world, trying to stop a virus that wipes minds, aided by his hacker friend Y.T. Reality is a place to escape from, a neoliberal future wrecked by hyperinflation and […]

Neal Stephensons science fiction novel Snow Crash predicted the Metaverse in 1992. This cult book has the amusingly-named Hiro Protagonist running around in an artificial cyber world, trying to stop a virus that wipes minds, aided by his hacker friend Y.T. Reality is a place to escape from, a neoliberal future wrecked by hyperinflation and inequality and run by corporations and gangsters and insane bureaucracy.

In many ways, the book is horribly prescient. (Its also horribly written in places, more like an info dump than a novel.) The Metaverse was a place where people had digital avatars, where they hung out with friends, went shopping and attended concerts. It was full of ads, the infrastructure was owned by a billionaire, and a virus was wreaking havoc on society. It all sounds familiar.

It wasnt COVID-19 of course. The Snow Crash virus caused the infected to lose the ability to think for themselves, and they start speaking in tongues.

Obviously, at the time, we didnt have social media, Stephenson told The Washington Post, but added, I was writing about just a long-standing human trait, which is this tendency for the mind to get hijacked by ideas.

The metaverse cant enslave you, yet, but the addictive nature of social media suggests its possible you might get hooked on a better virtual world, where your hotter-looking avatar interacts with people from all over the planet and has adventures that are not possible in reality.

To give you one crazy example of the possibilities, there is an actual theater company in the zombie-infested online wasteland survival game Fallout 76 that puts on Shakespeare plays. So, you can be part of the audience, or even audition and act, if you desire. Almost normal, except you may have to blast a few zombies in the middle of Romeo and Juliet. The ushers patrol the perimeter with chainsaws and AK-47s to annihilate any undead critics seeking to make their analytical discourse upon the performance.

This is all very Snow Crash. There is a real tension between the use of virtual worlds for escape or leisure and the impetus for profiteering. Many corporations see the metaverse and metaverse platforms as new continents to be colonized and exploited. If the metaverse develops under a centralized model, then it will be Amazon, Facebook and Google all over again: whale time. A decentralized metaverse built around blockchain technology would be more egalitarian and put the power back in the hands of users.

Enter the metaverse, stage left

Dr. Christina Yan Zhang, nicknamed Dr. Metaverse, wrote her 2012 thesis about MMORPGs and the early metaverse platform Second Life, so shes been thinking about this longer than most. Shes now the CEO of the Metaverse Institute.

I think the beauty about the current development of the metaverse is basically the convergence of a whole range of different technologies coming together. Many of them are getting more advanced to really help to create the next generation of internet, which is more immersive, interactive and intuitive.

She sees the metaverse as an enabling technology to improve interaction in both real and digital worlds.

Gaming writer Wagner James Au has just finished a book that will be published in June titled Making a Metaverse That Matters. Back in the early 2000s, he was the virtual journalist named Hamlet in Second Life. His white-suited avatar (a nod to Tom Wolfe) went around submitting dispatches from that virtual world.

He envisions there being multiple metaverses: Its going to be based on the community; its going to be based on culture and aesthetics. For example, Roblox is huge, but its primarily with kids. And the aesthetics are very intentionally looking like Legos. You could jump from Roblox to Fortnite, then Fortnite to VR chat. So, it will not be a single, virtual world.

He continues, I define it very directly from what Snow Crash described: It was a vast virtual world with user creation tools and highly customizable avatars that is integrated with the real world economy.

In other words, you can make money from it and also integrate with external technology so you can actually hook it up to other technology beyond the immersive 3D experience.

Snow Crash and capitalist realism

Science fiction and fantasy are known for creating new worlds to experience through literature, art and cinema. These genres have roots in the pervasive zeitgeist of their time, so they can often end up being unimaginative about new political or social opportunities. Tragic, influential British culture theorist Mark Fisher (who committed suicide in 2017) defined this as capitalist realism, the notion that capitalism is the only political structure and even visionary literature can rarely rise above imagining variations on this.

Snow Crash posits a dystopian real world that makes escape into an alternative fantasy more attractive: Hiro is a pizza delivery boy in real life; in the Metaverse, he is the greatest swordsman alive.

The greatest tragedy would be if the specter of capitalist realism made the metaverse a mirror of the existing world. A virtual world where we peddle virtual crap to each other to keep our likes or crypto coming in. Roblox is a classic example: Its business model involves kids creating stuff with other kids that provides an income stream from their creativity. Web1 promised liberation but didnt fulfill it. Web3 needs decentralization so that corporations do not overwhelm it as they have with previous iterations of the internet.

The metaverse is not without its challenges. Magazines Jillian Godsil looks at some issues here. Author and futurist Bernard Marr also highlights some serious drawbacks.

Seven big problems

Author and futurist Bernard Marr says, Im super-excited about this technology, but that comes with a warning about the potential perils of the metaverse. He has identified seven major problems and disadvantages highlighting the downsides to the virtual worlds. Most are quite knotty challenges, which wont be easy to solve in a malleable, constantly evolving world open to deviant behavior.

Privacy issues

We already have privacy concerns when we browse the web, Marr says. The technology that is already tracking our behavior online will also exist in the metaverse, and the tracking is likely to become even more invasive and intense.

Wearable, haptic devices could measure all kinds of physical effects such as heart rate and sweating. Enormous amounts of data could be collected and used by companies for marketing or other purposes, Marr continues.

Safety of children

As parents, its already difficult to track what our kids are doing online, and that challenge will continue with the metaverse. Understanding what our kids are doing in the metaverse will be even more challenging because we cant see the world theyre looking at in their VR headset, and there is no process in place for monitoring their screens using tablets or phones, Marr opines.

Health concerns

The result of spending your entire life in the metaverse could result in everyone looking like the Axios Humans in Wall-E. VR hangovers are also a thing: The sadness and angst that come from leaving a very intense, absorbing experience and returning to reality can create a comedown similar to drugs or drinking. Gaming or internet addiction is already impacting mental and physical health, so it could potentially be even worse in the metaverse.

Access inequality

Bernard Marr says, In order to use augmented reality, we need the latest smartphone and handset technology, and VR experiences require high-tech, expensive headsets as well as strong and reliable connectivity, he says.

How can we make sure that everyone in the world has equal access to the metaverse, and not just the people who have the most money and live in developed countries? This issue concerns Zhang, too. She sees Starlink as a way forward: The reason I mentioned Starlink is because one-third of the global population are still suffering from the digital divide, so they do not have access to the internet. Those smaller Starlink satellites can cover the most remote areas in the world.

Laws and regulations

A significant problem with all new technology is how slowly legislators and regulators are to formulate appropriate legal responses to the challenges presented. With something thats immersive, global and anarchic, which includes cryptocurrencies as well as the metaverse, authorities have difficulties keeping up with these technological changes.

Desensitization

Marr also worries that even more realistic violence will desensitize people to real-life violence. Although the zombie-hunting amateur thespians of Fallout 76 seem pretty balanced when Magazine chats with them. The counterargument might be that therapeutically killing orcs and zombies or catapulting angry birds is a relief valve for real-world stresses. These are not exclusive issues for the metaverse of course and have been leveled at games for years.

Identity hacking

If your avatar is hacked, a malicious entity could spread damage or possibly steal from you. This is yet another use case for blockchain technology in the metaverse as NFTs or blockchain-based identity technology is a solution suggested by Marr. So, your avatar could be anyone, but to enter the world, you would have to produce a digital, verified identity. That is similar to KYC processes to sign up for most crypto exchanges.

Interoperability

Au believes that there will be many different metaverse platforms, catering to different audiences. Wang disagrees, believing that interoperability will be an important way to ensure that users can move between experiences in the metaverse, via agreed protocols of interoperability, standardization of the metaverse and all additional assets by organizations worldwide. Interoperability and one unified Metaverse were the vision in Snow Crash.

Theres also disagreement over the level of immersion. Wagner thinks that there is sufficient computing available for most people to have a reasonably immersive experience via their smartphones, without needing VR headsets. Zhang disagrees, feeling that a large increase in computing power and probably quantum computing will be needed to fully realize an immersive VR system with millions of users.

Where is the metaverse heading?

In this difficult time in the crypto universe, many metaverse projects seem to be reorientating themselves. People are exploring ventures with a longer timescale to reach fruition. Zhang thinks that it will take 10 years to reach mass adoption. She views the European Unions provisional agreement on the Markets in Crypto-Assets (MiCA) proposal which aims to safeguard investing while fostering innovation as an important step forward for regulating the sector.

Wagner sees the drivers of the metaverse as users at both ends of the age spectrum: kids because they will find value in the play space, and seniors, driven by disability or social isolation, but able to interact via their avatars in ways that wouldnt be so easy in the real world. Wagner quotes the example of an 86-year-old blues guitarist he met busking in the street in Second Life.

Interestingly, Snow Crashs Stephenson has now launched a metaverse startup called Lamina1.

Wagner says, Neal Stephenson launched it with a major player in the Bitcoin industry, Peter Vessenes. Theyre making what they call a metaverse-as-a-service so, a way for creators to monetize their content across various, multiple metaverse platforms.

Vessenes, a Bitcoin pioneer, called it the base layer for the open metaverse: a place to build something a bit closer to Neals vision one that privileges creators, technical and artistic, one that provides support, spatial computing tech, and a community to support those who are building out the metaverse.

Lamina1 is very much built around the interoperability vision: that there should be one internet-like platform where players big and small can mutually coexist and flourish. That said, Web1 and Web2 arguably didnt reach that goal, so it isnt certain that a future version wont get dominated by big players as the web is now.

The metaverse is another new technology that has enormous potential for both financial and social rewards. It also has significant negatives that could stifle its growth. But Zhang opts for the glass-half-full viewpoint:

Fundamentally, we want to use technology to really benefit more people to have a more diverse, equal and sustainable world. We dont want the technology to be for a few people who have privilege or they are lucky to be financially free. So, I think there needs to be a really coordinated movement by governments, investors, NGOs and individuals coming together to ensure the rest of one-third of the population, in countries where the basic infrastructure is not in place, can be given more opportunity to flourish so no one is left behind. That needs to be addressed on a much higher level internationally.

See, the world is full of things more powerful than us. But if you know how to catch a ride, you can go places.

Neal Stephenson, Snow Crash

Uncategorized

Key shipping company files for Chapter 11 bankruptcy

The Illinois-based general freight trucking company filed for Chapter 11 bankruptcy to reorganize.

Share this:

The U.S. trucking industry has had a difficult beginning of the year for 2024 with several logistics companies filing for bankruptcy to seek either a Chapter 7 liquidation or Chapter 11 reorganization.

The Covid-19 pandemic caused a lot of supply chain issues for logistics companies and also created a shortage of truck drivers as many left the business for other occupations. Shipping companies, in the meantime, have had extreme difficulty recruiting new drivers for thousands of unfilled jobs.

Related: Tesla rival’s filing reveals Chapter 11 bankruptcy is possible

Freight forwarder company Boateng Logistics joined a growing list of shipping companies that permanently shuttered their businesses as the firm on Feb. 22 filed for Chapter 7 bankruptcy with plans to liquidate.

The Carlsbad, Calif., logistics company filed its petition in the U.S. Bankruptcy Court for the Southern District of California listing assets up to $50,000 and and $1 million to $10 million in liabilities. Court papers said it owed millions of dollars in liabilities to trucking, logistics and factoring companies. The company filed bankruptcy before any creditors could take legal action.

Lawsuits force companies to liquidate in bankruptcy

Lawsuits, however, can force companies to file bankruptcy, which was the case for J.J. & Sons Logistics of Clint, Texas, which on Jan. 22 filed for Chapter 7 liquidation in the U.S. Bankruptcy Court for the Western District of Texas. The company filed bankruptcy four days before the scheduled start of a trial for a wrongful death lawsuit filed by the family of a former company truck driver who had died from drowning in 2016.

California-based logistics company Wise Choice Trans Corp. shut down operations and filed for Chapter 7 liquidation on Jan. 4 in the U.S. Bankruptcy Court for the Northern District of California, listing $1 million to $10 million in assets and liabilities.

The Hayward, Calif., third-party logistics company, founded in 2009, provided final mile, less-than-truckload and full truckload services, as well as warehouse and fulfillment services in the San Francisco Bay Area.

The Chapter 7 filing also implemented an automatic stay against all legal proceedings, as the company listed its involvement in four legal actions that were ongoing or concluded. Court papers reportedly did not list amounts for damages.

In some cases, debtors don't have to take a drastic action, such as a liquidation, and can instead file a Chapter 11 reorganization.

Shutterstock

Nationwide Cargo seeks to reorganize its business

Nationwide Cargo Inc., a general freight trucking company that also hauls fresh produce and meat, filed for Chapter 11 bankruptcy protection in the U.S. Bankruptcy Court for the Northern District of Illinois with plans to reorganize its business.

The East Dundee, Ill., shipping company listed $1 million to $10 million in assets and $10 million to $50 million in liabilities in its petition and said funds will not be available to pay unsecured creditors. The company operates with 183 trucks and 171 drivers, FreightWaves reported.

Nationwide Cargo's three largest secured creditors in the petition were Equify Financial LLC (owed about $3.5 million,) Commercial Credit Group (owed about $1.8 million) and Continental Bank NA (owed about $676,000.)

The shipping company reported gross revenue of about $34 million in 2022 and about $40 million in 2023. From Jan. 1 until its petition date, the company generated $9.3 million in gross revenue.

Related: Veteran fund manager picks favorite stocks for 2024

bankruptcy pandemic covid-19 stocksUncategorized

Key shipping company files Chapter 11 bankruptcy

The Illinois-based general freight trucking company filed for Chapter 11 bankruptcy to reorganize.

Share this:

The U.S. trucking industry has had a difficult beginning of the year for 2024 with several logistics companies filing for bankruptcy to seek either a Chapter 7 liquidation or Chapter 11 reorganization.

The Covid-19 pandemic caused a lot of supply chain issues for logistics companies and also created a shortage of truck drivers as many left the business for other occupations. Shipping companies, in the meantime, have had extreme difficulty recruiting new drivers for thousands of unfilled jobs.

Related: Tesla rival’s filing reveals Chapter 11 bankruptcy is possible

Freight forwarder company Boateng Logistics joined a growing list of shipping companies that permanently shuttered their businesses as the firm on Feb. 22 filed for Chapter 7 bankruptcy with plans to liquidate.

The Carlsbad, Calif., logistics company filed its petition in the U.S. Bankruptcy Court for the Southern District of California listing assets up to $50,000 and and $1 million to $10 million in liabilities. Court papers said it owed millions of dollars in liabilities to trucking, logistics and factoring companies. The company filed bankruptcy before any creditors could take legal action.

Lawsuits force companies to liquidate in bankruptcy

Lawsuits, however, can force companies to file bankruptcy, which was the case for J.J. & Sons Logistics of Clint, Texas, which on Jan. 22 filed for Chapter 7 liquidation in the U.S. Bankruptcy Court for the Western District of Texas. The company filed bankruptcy four days before the scheduled start of a trial for a wrongful death lawsuit filed by the family of a former company truck driver who had died from drowning in 2016.

California-based logistics company Wise Choice Trans Corp. shut down operations and filed for Chapter 7 liquidation on Jan. 4 in the U.S. Bankruptcy Court for the Northern District of California, listing $1 million to $10 million in assets and liabilities.

The Hayward, Calif., third-party logistics company, founded in 2009, provided final mile, less-than-truckload and full truckload services, as well as warehouse and fulfillment services in the San Francisco Bay Area.

The Chapter 7 filing also implemented an automatic stay against all legal proceedings, as the company listed its involvement in four legal actions that were ongoing or concluded. Court papers reportedly did not list amounts for damages.

In some cases, debtors don't have to take a drastic action, such as a liquidation, and can instead file a Chapter 11 reorganization.

Shutterstock

Nationwide Cargo seeks to reorganize its business

Nationwide Cargo Inc., a general freight trucking company that also hauls fresh produce and meat, filed for Chapter 11 bankruptcy protection in the U.S. Bankruptcy Court for the Northern District of Illinois with plans to reorganize its business.

The East Dundee, Ill., shipping company listed $1 million to $10 million in assets and $10 million to $50 million in liabilities in its petition and said funds will not be available to pay unsecured creditors. The company operates with 183 trucks and 171 drivers, FreightWaves reported.

Nationwide Cargo's three largest secured creditors in the petition were Equify Financial LLC (owed about $3.5 million,) Commercial Credit Group (owed about $1.8 million) and Continental Bank NA (owed about $676,000.)

The shipping company reported gross revenue of about $34 million in 2022 and about $40 million in 2023. From Jan. 1 until its petition date, the company generated $9.3 million in gross revenue.

Related: Veteran fund manager picks favorite stocks for 2024

bankruptcy pandemic covid-19 stocksUncategorized

Tight inventory and frustrated buyers challenge agents in Virginia

With inventory a little more than half of what it was pre-pandemic, agents are struggling to find homes for clients in Virginia.

Share this:

No matter where you are in the state, real estate agents in Virginia are facing low inventory conditions that are creating frustrating scenarios for their buyers.

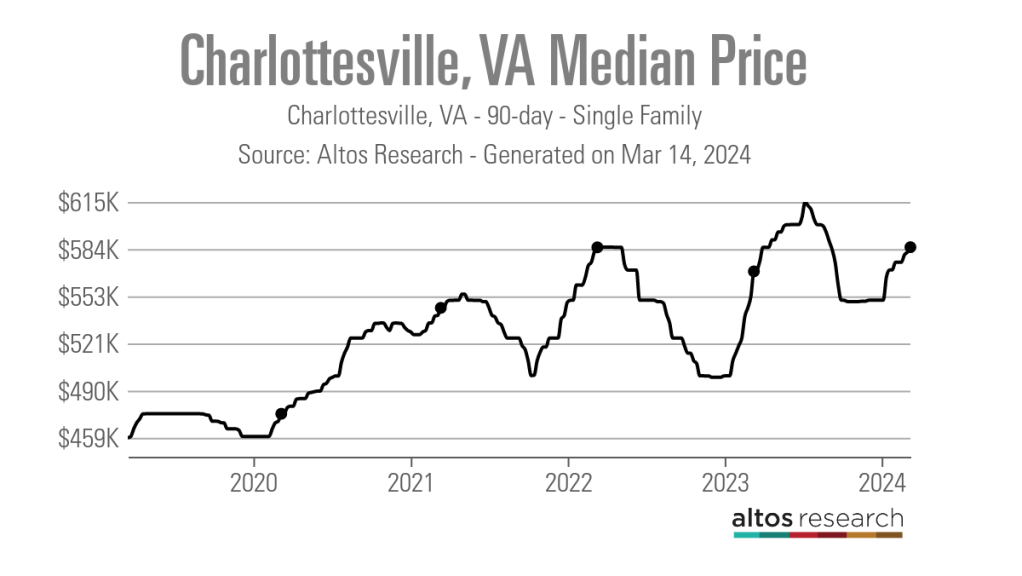

“I think people are getting used to the interest rates where they are now, but there is just a huge lack of inventory,” said Chelsea Newcomb, a RE/MAX Realty Specialists agent based in Charlottesville. “I have buyers that are looking, but to find a house that you love enough to pay a high price for — and to be at over a 6.5% interest rate — it’s just a little bit harder to find something.”

Newcomb said that interest rates and higher prices, which have risen by more than $100,000 since March 2020, according to data from Altos Research, have caused her clients to be pickier when selecting a home.

“When rates and prices were lower, people were more willing to compromise,” Newcomb said.

Out in Wise, Virginia, near the westernmost tip of the state, RE/MAX Cavaliers agent Brett Tiller and his clients are also struggling to find suitable properties.

“The thing that really stands out, especially compared to two years ago, is the lack of quality listings,” Tiller said. “The slightly more upscale single-family listings for move-up buyers with children looking for their forever home just aren’t coming on the market right now, and demand is still very high.”

Statewide, Virginia had a 90-day average of 8,068 active single-family listings as of March 8, 2024, down from 14,471 single-family listings in early March 2020 at the onset of the COVID-19 pandemic, according to Altos Research. That represents a decrease of 44%.

In Newcomb’s base metro area of Charlottesville, there were an average of only 277 active single-family listings during the same recent 90-day period, compared to 892 at the onset of the pandemic. In Wise County, there were only 56 listings.

Due to the demand from move-up buyers in Tiller’s area, the average days on market for homes with a median price of roughly $190,000 was just 17 days as of early March 2024.

“For the right home, which is rare to find right now, we are still seeing multiple offers,” Tiller said. “The demand is the same right now as it was during the heart of the pandemic.”

According to Tiller, the tight inventory has caused homebuyers to spend up to six months searching for their new property, roughly double the time it took prior to the pandemic.

For Matt Salway in the Virginia Beach metro area, the tight inventory conditions are creating a rather hot market.

“Depending on where you are in the area, your listing could have 15 offers in two days,” the agent for Iron Valley Real Estate Hampton Roads | Virginia Beach said. “It has been crazy competition for most of Virginia Beach, and Norfolk is pretty hot too, especially for anything under $400,000.”

According to Altos Research, the Virginia Beach-Norfolk-Newport News housing market had a seven-day average Market Action Index score of 52.44 as of March 14, making it the seventh hottest housing market in the country. Altos considers any Market Action Index score above 30 to be indicative of a seller’s market.

Further up the coastline on the vacation destination of Chincoteague Island, Long & Foster agent Meghan O. Clarkson is also seeing a decent amount of competition despite higher prices and interest rates.

“People are taking their time to actually come see things now instead of buying site unseen, and occasionally we see some seller concessions, but the traffic and the demand is still there; you might just work a little longer with people because we don’t have anything for sale,” Clarkson said.

“I’m busy and constantly have appointments, but the underlying frenzy from the height of the pandemic has gone away, but I think it is because we have just gotten used to it.”

While much of the demand that Clarkson’s market faces is for vacation homes and from retirees looking for a scenic spot to retire, a large portion of the demand in Salway’s market comes from military personnel and civilians working under government contracts.

“We have over a dozen military bases here, plus a bunch of shipyards, so the closer you get to all of those bases, the easier it is to sell a home and the faster the sale happens,” Salway said.

Due to this, Salway said that existing-home inventory typically does not come on the market unless an employment contract ends or the owner is reassigned to a different base, which is currently contributing to the tight inventory situation in his market.

Things are a bit different for Tiller and Newcomb, who are seeing a decent number of buyers from other, more expensive parts of the state.

“One of the crazy things about Louisa and Goochland, which are kind of like suburbs on the western side of Richmond, is that they are growing like crazy,” Newcomb said. “A lot of people are coming in from Northern Virginia because they can work remotely now.”

With a Market Action Index score of 50, it is easy to see why people are leaving the Washington-Arlington-Alexandria market for the Charlottesville market, which has an index score of 41.

In addition, the 90-day average median list price in Charlottesville is $585,000 compared to $729,900 in the D.C. area, which Newcomb said is also luring many Virginia homebuyers to move further south.

“They are very accustomed to higher prices, so they are super impressed with the prices we offer here in the central Virginia area,” Newcomb said.

For local buyers, Newcomb said this means they are frequently being outbid or outpriced.

“A couple who is local to the area and has been here their whole life, they are just now starting to get their mind wrapped around the fact that you can’t get a house for $200,000 anymore,” Newcomb said.

As the year heads closer to spring, triggering the start of the prime homebuying season, agents in Virginia feel optimistic about the market.

“We are seeing seasonal trends like we did up through 2019,” Clarkson said. “The market kind of soft launched around President’s Day and it is still building, but I expect it to pick right back up and be in full swing by Easter like it always used to.”

But while they are confident in demand, questions still remain about whether there will be enough inventory to support even more homebuyers entering the market.

“I have a lot of buyers starting to come off the sidelines, but in my office, I also have a lot of people who are going to list their house in the next two to three weeks now that the weather is starting to break,” Newcomb said. “I think we are going to have a good spring and summer.”

real estate housing market pandemic covid-19 interest rates

Q4 Update: Delinquencies, Foreclosures and REO

Pharma industry reputation remains steady at a ‘new normal’ after Covid, Harris Poll finds

These Cities Have The Highest (And Lowest) Share Of Unaffordable Neighborhoods In 2024

The Question You Should Ask Whenever You’re Wrong

Tight inventory and frustrated buyers challenge agents in Virginia

Part 1: Current State of the Housing Market; Overview for mid-March 2024

Walmart and Target make key self-checkout changes to fight theft

Your financial plan may be riskier without bitcoin

Key shipping company files Chapter 11 bankruptcy

The best real estate coaching programs for 2024

-

Uncategorized3 weeks ago

Uncategorized3 weeks agoAll Of The Elements Are In Place For An Economic Crisis Of Staggering Proportions

-

International7 days ago

International7 days agoEyePoint poaches medical chief from Apellis; Sandoz CFO, longtime BioNTech exec to retire

-

Uncategorized4 weeks ago

Uncategorized4 weeks agoCalifornia Counties Could Be Forced To Pay $300 Million To Cover COVID-Era Program

-

Uncategorized3 weeks ago

Uncategorized3 weeks agoApparel Retailer Express Moving Toward Bankruptcy

-

Uncategorized4 weeks ago

Uncategorized4 weeks agoIndustrial Production Decreased 0.1% in January

-

International6 days ago

International6 days agoWalmart launches clever answer to Target’s new membership program

-

Uncategorized4 weeks ago

Uncategorized4 weeks agoRFK Jr: The Wuhan Cover-Up & The Rise Of The Biowarfare-Industrial Complex

-

Uncategorized3 weeks ago

Uncategorized3 weeks agoGOP Efforts To Shore Up Election Security In Swing States Face Challenges