Government

Is The “Inflation Is Transitory” Narrative Dead?

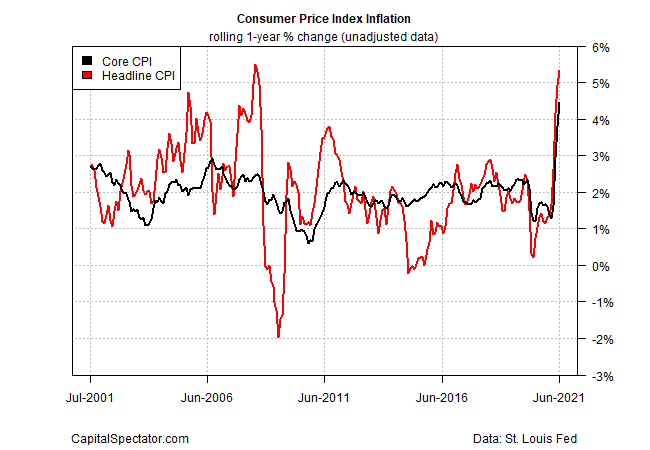

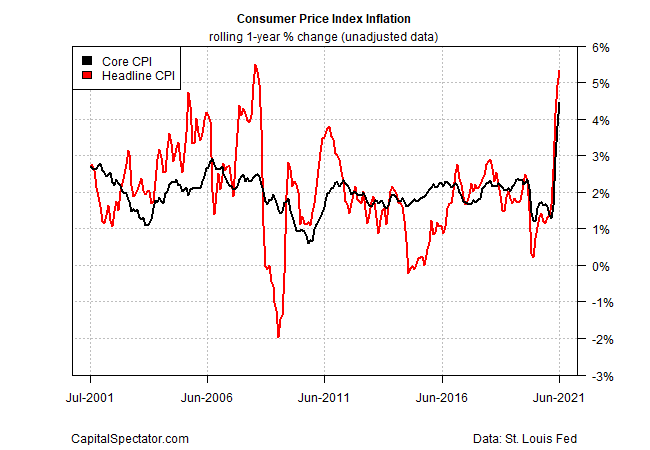

Consumer inflation in the US remained surprisingly hot in June, the Labor Department reported yesterday. Taken at face value, the numbers raise more doubts about the Federal Reserve’s assumption that the recent inflation surge is temporary. But a closer..

Share this:

Consumer inflation in the US remained surprisingly hot in June, the Labor Department reported yesterday. Taken at face value, the numbers raise more doubts about the Federal Reserve’s assumption that the recent inflation surge is temporary. But a closer look at the numbers paints a more complicated profile.

It’s still too early to dismiss inflation risk, but the same is true for putting a fork in transitory assumption. In other words, despite the ongoing acceleration in the consumer price index (CPI) in yesterday’s report, nothing much has changed. Pandemic-related blowback is still creating noise and so the search for signal on the inflation front remains challenging and ongoing. The truth will out eventually, perhaps by the fourth quarter. Meantime, the debate rages and genuine clarity remains elusive.

How is recession risk evolving? Monitor the outlook with a subscription to:

The US Business Cycle Risk Report

Let’s start with the main results in the June update. Headline CPI jumped to a 5.4% year-over-year increase, the highest since 2008. Core inflation (a more reliable measure of the trend) popped to a 4.5% annual pace last month – a 30-year high!

So-called base effects are still partly driving the annual changes. Unusually low prices during the depths of the pandemic a year ago continue to pair with this year’s rebounding prices to produce dramatic year-over-year increases. But the base effects are fading and with each passing month this factor explains less of the inflation trend.

On that note, looking at inflation in monthly terms highlights that last month’s acceleration in pricing pressure transcends base effects. For example, core CPI’s monthly change (seasonally adjusted) remained elevated, rising to a 0.8% gain – far above the increases seen in recent decades. The longer this monthly change stays elevated, the weaker the transitory-inflation narrative becomes.

Monthly CPI numbers are noisy, however, and we should view these results cautiously. Nonetheless, the sustained increase clearly points to strong inflationary pressure in recent months.

Digging deeper into the data reveals that a key driver of inflation’s acceleration last month is due to a handful of components that are expected to post softer gains, perhaps negative prices changes, in the months ahead. Notably, used vehicle prices continued to surge last month.

“Inflation surprised substantially to the upside in June but, once again, owing to outsized increases in prices in a few categories,” says Michelle Meyer, head of U.S. economics at Bank of America. “This reinforces the idea of transitory inflation.”

The White House Council of Economic Advisers tweeted a chart yesterday that highlights the outsized influence of vehicle-related prices in last month’s inflation report. Indeed, for the last three months, car prices have been unusually hot. The combination of recovering demand and reopening production bottlenecks has conspired to drive prices sharply higher. But this is likely a temporary change and a reversal of some degree is expected in the second half of the year as production capabilities rebound.

Meanwhile, “Bigger components (like shelter) are still well-behaved,” notes Carl Tannenbaum, chief economist for Northern Trust.

Steve Englander, a foreign exchange strategist at Standard Chartered, attempts to adjust inflation for the reopening shock and finds that monthly pricing pressure is significantly softer after this revision. Some may dismiss this as statistical fudging, but it’s another clue for at least considering the view that the runup inflation lately is less about regime shift vs. base effects.

The case for the transitory narrative may be weakening, but its not dead, at least not yet. But if there’s any validity to this forecast, the evidence will start to emerge soon… or not.

On that front, The Capital Spectator’s Inflation Trend Index (ITI) suggests that pricing pressure will peak this summer. ITI, an eight-factor modeling effort, attempts to provide a degree of forward guidance on the directional bias of pricing activity in real time, although it should not be used as a proxy for estimating the government’s inflation measures. Recent ITI updates suggested that reflation would peak in May or June. New data reveals those estimates were premature and the revised outlook points to July at the earliest. This could change, of course, as incoming numbers are published. Whatever comes, ITI will likely provide an early estimate for managing expectations, one way or the other.

Stepping back and considering the broad macro profile still leaves plenty of room for thinking that the disinflationary trend of recent decades remains intact, despite the pandemic-related interruption. Focusing on the last several months of inflation data suggests otherwise, but as Hoisington Investment Management reminds in its second quarter review, the “massive debt overhang” in the US continues to mount, creating an “obstacle” for the Federal Reserve’s efforts in reaching its goals for economic and inflation targets.

“The current economic growth and inflation rates of 2021 will be the highest for a very long time to come,” Hoisington predicts.

The main obstacle to a return to sustained growth in the standard of living, extreme over-indebtedness, was dramatically worsened by the multiple rounds of fiscal stimulus which has caused the temporary improvement in economic growth and inflation in the second quarter. No pathway out of this trap exists as long as the overreliance on debt remains the only tool of monetary and fiscal policy. The situation is no different in Japan and Europe. Thus, while long Treasury yields can increase over the short run, the fundamentals are too weak for yields to stay elevated. More debt does not cure a subpar economy mired in a debt trap. Given the above, our view is that the trend in long-term Treasury yields remains downward.

By this reasoning, the rise in inflation is noise and will soon give way to moderation. No one knows for sure if this will prove correct, but for now the Treasury market appears to be on board with this outlook. Although the 10-year yield rose yesterday to 1.42%, a six-day high, the trend for this benchmark rate still posting a downward bias after the recent bounce that started reversing in April .

If and when the 10-year yield starts to break to the upside, that may be an early clue that market sentiment is beginning to dismiss the transitory inflation narrative.

Perhaps an even bigger clue for embracing the higher inflation narrative would be if the Fed shifts its tone on the transitory narrative. For now, however, expect the central bank to maintain its current stance, advises Tim Duy at SGH Macro Advisors. “The Fed will continue to emphasize the ‘inflation is transitory’ story as it delays tapering until either the labor market recovers more fully or it is evident that labor supply is not bouncing back,” he writes in a note to clients. “That likely won’t happen until later this year.”

Learn To Use R For Portfolio Analysis

Quantitative Investment Portfolio Analytics In R:

An Introduction To R For Modeling Portfolio Risk and Return

By James Picerno

Government

Low Iron Levels In Blood Could Trigger Long COVID: Study

Low Iron Levels In Blood Could Trigger Long COVID: Study

Authored by Amie Dahnke via The Epoch Times (emphasis ours),

People with inadequate…

Share this:

Authored by Amie Dahnke via The Epoch Times (emphasis ours),

People with inadequate iron levels in their blood due to a COVID-19 infection could be at greater risk of long COVID.

A new study indicates that problems with iron levels in the bloodstream likely trigger chronic inflammation and other conditions associated with the post-COVID phenomenon. The findings, published on March 1 in Nature Immunology, could offer new ways to treat or prevent the condition.

Long COVID Patients Have Low Iron Levels

Researchers at the University of Cambridge pinpointed low iron as a potential link to long-COVID symptoms thanks to a study they initiated shortly after the start of the pandemic. They recruited people who tested positive for the virus to provide blood samples for analysis over a year, which allowed the researchers to look for post-infection changes in the blood. The researchers looked at 214 samples and found that 45 percent of patients reported symptoms of long COVID that lasted between three and 10 months.

In analyzing the blood samples, the research team noticed that people experiencing long COVID had low iron levels, contributing to anemia and low red blood cell production, just two weeks after they were diagnosed with COVID-19. This was true for patients regardless of age, sex, or the initial severity of their infection.

According to one of the study co-authors, the removal of iron from the bloodstream is a natural process and defense mechanism of the body.

But it can jeopardize a person’s recovery.

“When the body has an infection, it responds by removing iron from the bloodstream. This protects us from potentially lethal bacteria that capture the iron in the bloodstream and grow rapidly. It’s an evolutionary response that redistributes iron in the body, and the blood plasma becomes an iron desert,” University of Oxford professor Hal Drakesmith said in a press release. “However, if this goes on for a long time, there is less iron for red blood cells, so oxygen is transported less efficiently affecting metabolism and energy production, and for white blood cells, which need iron to work properly. The protective mechanism ends up becoming a problem.”

The research team believes that consistently low iron levels could explain why individuals with long COVID continue to experience fatigue and difficulty exercising. As such, the researchers suggested iron supplementation to help regulate and prevent the often debilitating symptoms associated with long COVID.

“It isn’t necessarily the case that individuals don’t have enough iron in their body, it’s just that it’s trapped in the wrong place,” Aimee Hanson, a postdoctoral researcher at the University of Cambridge who worked on the study, said in the press release. “What we need is a way to remobilize the iron and pull it back into the bloodstream, where it becomes more useful to the red blood cells.”

The research team pointed out that iron supplementation isn’t always straightforward. Achieving the right level of iron varies from person to person. Too much iron can cause stomach issues, ranging from constipation, nausea, and abdominal pain to gastritis and gastric lesions.

1 in 5 Still Affected by Long COVID

COVID-19 has affected nearly 40 percent of Americans, with one in five of those still suffering from symptoms of long COVID, according to the U.S. Centers for Disease Control and Prevention (CDC). Long COVID is marked by health issues that continue at least four weeks after an individual was initially diagnosed with COVID-19. Symptoms can last for days, weeks, months, or years and may include fatigue, cough or chest pain, headache, brain fog, depression or anxiety, digestive issues, and joint or muscle pain.

Government

Walmart joins Costco in sharing key pricing news

The massive retailers have both shared information that some retailers keep very close to the vest.

Share this:

As we head toward a presidential election, the presumed candidates for both parties will look for issues that rally undecided voters.

The economy will be a key issue, with Democrats pointing to job creation and lowering prices while Republicans will cite the layoffs at Big Tech companies, high housing prices, and of course, sticky inflation.

The covid pandemic created a perfect storm for inflation and higher prices. It became harder to get many items because people getting sick slowed down, or even stopped, production at some factories.

Related: Popular mall retailer shuts down abruptly after bankruptcy filing

It was also a period where demand increased while shipping, trucking and delivery systems were all strained or thrown out of whack. The combination led to product shortages and higher prices.

You might have gone to the grocery store and not been able to buy your favorite paper towel brand or find toilet paper at all. That happened partly because of the supply chain and partly due to increased demand, but at the end of the day, it led to higher prices, which some consumers blamed on President Joe Biden's administration.

Biden, of course, was blamed for the price increases, but as inflation has dropped and grocery prices have fallen, few companies have been up front about it. That's probably not a political choice in most cases. Instead, some companies have chosen to lower prices more slowly than they raised them.

However, two major retailers, Walmart (WMT) and Costco, have been very honest about inflation. Walmart Chief Executive Doug McMillon's most recent comments validate what Biden's administration has been saying about the state of the economy. And they contrast with the economic picture being painted by Republicans who support their presumptive nominee, Donald Trump.

Image source: Joe Raedle/Getty Images

Walmart sees lower prices

McMillon does not talk about lower prices to make a political statement. He's communicating with customers and potential customers through the analysts who cover the company's quarterly-earnings calls.

During Walmart's fiscal-fourth-quarter-earnings call, McMillon was clear that prices are going down.

"I'm excited about the omnichannel net promoter score trends the team is driving. Across countries, we continue to see a customer that's resilient but looking for value. As always, we're working hard to deliver that for them, including through our rollbacks on food pricing in Walmart U.S. Those were up significantly in Q4 versus last year, following a big increase in Q3," he said.

He was specific about where the chain has seen prices go down.

"Our general merchandise prices are lower than a year ago and even two years ago in some categories, which means our customers are finding value in areas like apparel and hard lines," he said. "In food, prices are lower than a year ago in places like eggs, apples, and deli snacks, but higher in other places like asparagus and blackberries."

McMillon said that in other areas prices were still up but have been falling.

"Dry grocery and consumables categories like paper goods and cleaning supplies are up mid-single digits versus last year and high teens versus two years ago. Private-brand penetration is up in many of the countries where we operate, including the United States," he said.

Costco sees almost no inflation impact

McMillon avoided the word inflation in his comments. Costco (COST) Chief Financial Officer Richard Galanti, who steps down on March 15, has been very transparent on the topic.

The CFO commented on inflation during his company's fiscal-first-quarter-earnings call.

"Most recently, in the last fourth-quarter discussion, we had estimated that year-over-year inflation was in the 1% to 2% range. Our estimate for the quarter just ended, that inflation was in the 0% to 1% range," he said.

Galanti made clear that inflation (and even deflation) varied by category.

"A bigger deflation in some big and bulky items like furniture sets due to lower freight costs year over year, as well as on things like domestics, bulky lower-priced items, again, where the freight cost is significant. Some deflationary items were as much as 20% to 30% and, again, mostly freight-related," he added.

bankruptcy pandemic trumpGovernment

Walmart has really good news for shoppers (and Joe Biden)

The giant retailer joins Costco in making a statement that has political overtones, even if that’s not the intent.

Share this:

{kind=link}

{kind=link}

As we head toward a presidential election, the presumed candidates for both parties will look for issues that rally undecided voters.

The economy will be a key issue, with Democrats pointing to job creation and lowering prices while Republicans will cite the layoffs at Big Tech companies, high housing prices, and of course, sticky inflation.

The covid pandemic created a perfect storm for inflation and higher prices. It became harder to get many items because people getting sick slowed down, or even stopped, production at some factories.

Related: Popular mall retailer shuts down abruptly after bankruptcy filing

It was also a period where demand increased while shipping, trucking and delivery systems were all strained or thrown out of whack. The combination led to product shortages and higher prices.

You might have gone to the grocery store and not been able to buy your favorite paper towel brand or find toilet paper at all. That happened partly because of the supply chain and partly due to increased demand, but at the end of the day, it led to higher prices, which some consumers blamed on President Joe Biden's administration.

Biden, of course, was blamed for the price increases, but as inflation has dropped and grocery prices have fallen, few companies have been up front about it. That's probably not a political choice in most cases. Instead, some companies have chosen to lower prices more slowly than they raised them.

However, two major retailers, Walmart (WMT) and Costco, have been very honest about inflation. Walmart Chief Executive Doug McMillon's most recent comments validate what Biden's administration has been saying about the state of the economy. And they contrast with the economic picture being painted by Republicans who support their presumptive nominee, Donald Trump.

Image source: Joe Raedle/Getty Images

Walmart sees lower prices

McMillon does not talk about lower prices to make a political statement. He's communicating with customers and potential customers through the analysts who cover the company's quarterly-earnings calls.

During Walmart's fiscal-fourth-quarter-earnings call, McMillon was clear that prices are going down.

"I'm excited about the omnichannel net promoter score trends the team is driving. Across countries, we continue to see a customer that's resilient but looking for value. As always, we're working hard to deliver that for them, including through our rollbacks on food pricing in Walmart U.S. Those were up significantly in Q4 versus last year, following a big increase in Q3," he said.

He was specific about where the chain has seen prices go down.

"Our general merchandise prices are lower than a year ago and even two years ago in some categories, which means our customers are finding value in areas like apparel and hard lines," he said. "In food, prices are lower than a year ago in places like eggs, apples, and deli snacks, but higher in other places like asparagus and blackberries."

McMillon said that in other areas prices were still up but have been falling.

"Dry grocery and consumables categories like paper goods and cleaning supplies are up mid-single digits versus last year and high teens versus two years ago. Private-brand penetration is up in many of the countries where we operate, including the United States," he said.

Costco sees almost no inflation impact

McMillon avoided the word inflation in his comments. Costco (COST) Chief Financial Officer Richard Galanti, who steps down on March 15, has been very transparent on the topic.

The CFO commented on inflation during his company's fiscal-first-quarter-earnings call.

"Most recently, in the last fourth-quarter discussion, we had estimated that year-over-year inflation was in the 1% to 2% range. Our estimate for the quarter just ended, that inflation was in the 0% to 1% range," he said.

Galanti made clear that inflation (and even deflation) varied by category.

"A bigger deflation in some big and bulky items like furniture sets due to lower freight costs year over year, as well as on things like domestics, bulky lower-priced items, again, where the freight cost is significant. Some deflationary items were as much as 20% to 30% and, again, mostly freight-related," he added.

bankruptcy pandemic trump

Walmart launches clever answer to Target’s new membership program

EyePoint poaches medical chief from Apellis; Sandoz CFO, longtime BioNTech exec to retire

Catastrophic Risk: Investing and Business Implications

When Military Rule Supplants Democracy

Redefining Poverty: Towards a Transpartisan Approach

The Digest #187

Gather ’round the crystal ball: A multi-commodity outlook from PDAC 2024

Deterra Royalties half-yearly result: stable performance and growth Initiatives

Deflationary pressures in China – be careful what you wish for

Measuring Treasury Market Depth

-

Uncategorized2 weeks ago

Uncategorized2 weeks agoAll Of The Elements Are In Place For An Economic Crisis Of Staggering Proportions

-

Uncategorized1 month ago

Uncategorized1 month agoCathie Wood sells a major tech stock (again)

-

Uncategorized3 weeks ago

Uncategorized3 weeks agoCalifornia Counties Could Be Forced To Pay $300 Million To Cover COVID-Era Program

-

Uncategorized2 weeks ago

Uncategorized2 weeks agoApparel Retailer Express Moving Toward Bankruptcy

-

Uncategorized3 weeks ago

Uncategorized3 weeks agoIndustrial Production Decreased 0.1% in January

-

International1 day ago

Walmart launches clever answer to Target’s new membership program

-

Uncategorized3 weeks ago

Uncategorized3 weeks agoRFK Jr: The Wuhan Cover-Up & The Rise Of The Biowarfare-Industrial Complex

-

Uncategorized3 weeks ago

Uncategorized3 weeks agoGOP Efforts To Shore Up Election Security In Swing States Face Challenges