International

Inflation Is A Monetary Curse

Inflation Is A Monetary Curse

Authored by Alasdair Macleod via GoldMoney.com,

Remarkably, in a speech on monetary policy given at the Jackson Hole conference last Friday, Jay Powell never mentioned money, money supply, M1 or M2. With money..

Share this:

Authored by Alasdair Macleod via GoldMoney.com,

Remarkably, in a speech on monetary policy given at the Jackson Hole conference last Friday, Jay Powell never mentioned money, money supply, M1 or M2. With money supply expanding at a record pace to fund both QE and intractable budget deficits the omission is extraordinary.

The FOMC (the rate setting committee) appears to no longer take the consequences of monetary expansion into account. But the fact is that rising consumer prices caused by monetary expansion have driven real rates sharply negative and are leading to pressure for higher interest rates.

This article looks at the consequences of policies which combine the maintenance of a wealth effect by juicing markets with QE, and funding enormous government deficits, which are now beyond control. A flight out of foreign-owned dollars and dollar-denominated financial assets, which currently total over $32 trillion, is becoming inevitable.

Will the Fed respond by increasing its QE support for financial markets, while resisting the pressure of rising interest rates? If so, there is no surer way to destroy the dollar.

The lessons from history combined with sound economic analysis tell us that markets will reassert themselves over the Fed, and for that matter, over all other central banks which have embarked on similar monetary policies.

Gold is the ultimate hedge against these events and their consequences.

Introduction

Last week, in his Jackson Hole speech Jay Powell grudgingly admitted that prices might rise a bit more than the FOMC previously thought. But it was too early to conclude that policies should be adjusted immediately. He said:

“Over the 12 months through July, measures of headline and core personal consumption expenditures inflation have run at 4.2% and 3.6% respectively— well above our 2 per cent longer-run objective. Businesses and consumers widely report upward pressure on prices and wages. Inflation at these levels is, of course, a cause for concern. But that concern is tempered by a number of factors that suggest that these elevated readings are likely to be temporary. This assessment is a critical and ongoing one, and we are carefully monitoring incoming data.”

In other words, with prices rising at over double the 2% target, there’s nothing to worry about. But be reassured, the Fed is on the case.

This was followed by

“Policymakers and analysts generally believe that, as long as longer-term inflation expectations remain anchored, policy can and should look through temporary swings in inflation. Our monetary policy framework emphasises that anchoring longer-term expectations at 2 per cent is important for both maximum employment and price stability.”

In other words, because inflation is always 2 per cent and Humpty-Dumpty insists it is so, markets will return to the 2 per cent target. Incidentally, when someone invokes belief, it is either the product of faith or lack of knowledge. This is why politicians cite faith a lot, and we should be wary when it is a justification for monetary policy.

There is, of course, one glaring problem with all this as Powell admits before dismissing it: “businesses and consumers widely report upward pressure on prices and wages”. There is an associated problem, an enormous elephant in the room that no official seems to be aware of, which independent analysts such as John Williams at Shadowstats.com points out, and that is if you strip out all the changes in statistical method that have deliberately reduced headline price rises since 1980, you find that according to an unadjusted CPI(U), prices are now rising at over 13% annualised.

Perhaps we should give Powell one out of ten for courage for participating at Jackson Hole, while zero points must be awarded to Christine Lagarde and Andrew Bailey, both having refused to take part in the symposium when at other times they would surely have welcomed the chance to be in the limelight on the global monetary stage. We are left wondering why they preferred not to justify their monetary policies in such a forum.

But if Powell gets one point for at least appearing, he gets at least nine out of ten for evasion. A word-search of his speech reveals why. It is headlined about monetary policy. But money was only mentioned once, and that was in the title of one of the references at the end. Not even when discussing longer-term inflation expectations was money mentioned. And word searches for M1 and M2 show nothing. The Fed’s monetary policy does not appear to involve money.

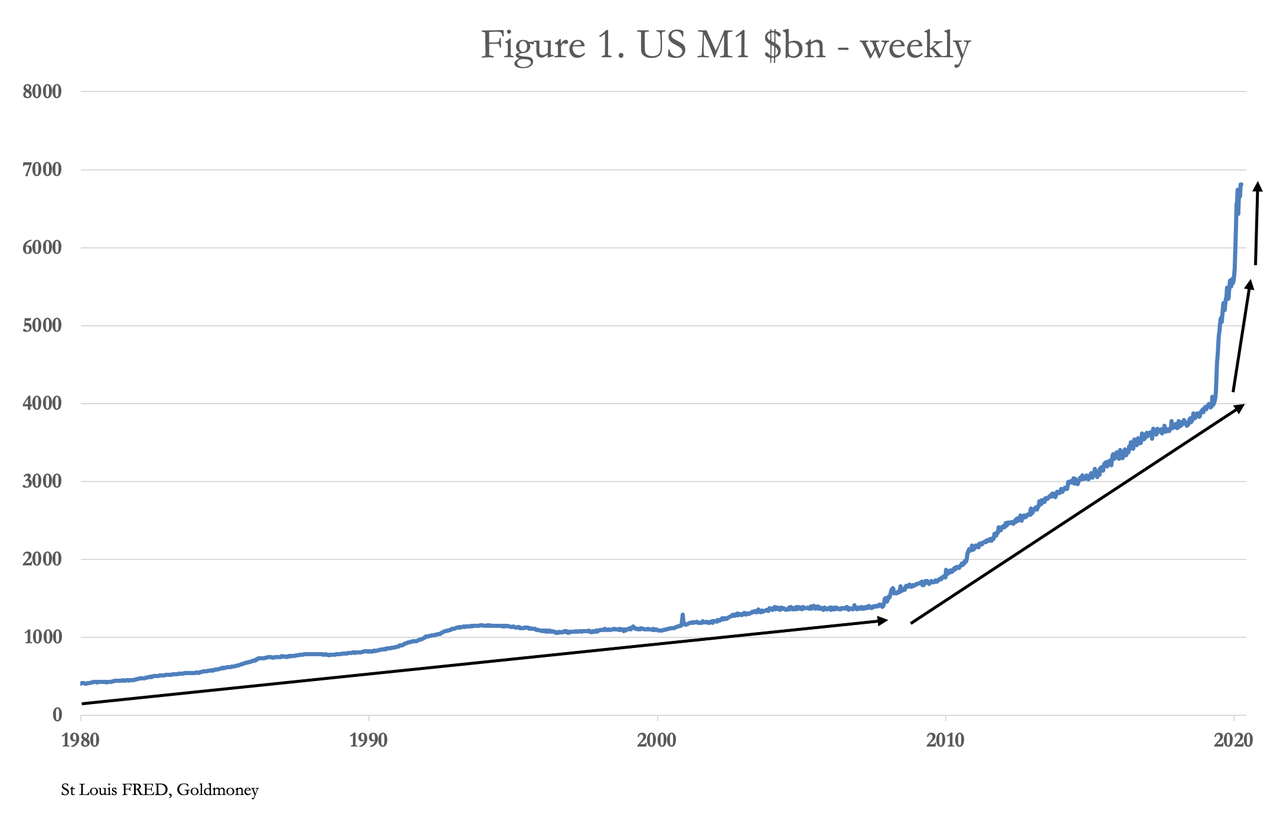

To be clear, the chart in Figure 1 has nothing to do with rising prices, according to Jay Powell.

Figure 1 shows narrow money supply before it was amended to include former categories of broader M2 money last February, rendering it useless for comparative analysis. Narrow money supply is going off the scales. Yet at Jackson Hole it was never mentioned, except in a footnote. Equally incredible is the gullibility of the investment establishment knowing that money does matter yet was drawn into the Fed’s non-monetary narrative.

The relationship between prices and money

Like the child in the fable who observed the emperor had been conned into wearing no clothes, a child today with an elementary grasp of arithmetic will understand that if you increase the quantity of something, each unit will be worth less. Today’s masters of the monetary universe seem unaware of the fact. They have written many erudite books and articles, made speeches as we saw last week, in ignorance of or wishing away monetary facts.

The consequences of debasement are therefore ducked. Interventionists dismiss the Cantillon effect, whereby prices increase in the wake of the new money being spent into circulation. Have they even heard of it? As an unarguable fact, it should be indisputable. And clearly, rising prices are a consequence of the massive increase in circulating currency evidenced in Figure 1 above, and not due solely to an imbalance between production and consumer demand which will correct in time, as Powell claimed at Jackson Hole.

Economic dislocation is part of and at the same time an additional factor to monetary expansion behind price increases. It arises from monetary inflation distorting markets, which continue to be disrupted by the covid pandemic. Covid-related disruption will continue into the foreseeable future, most noticeably due to logistical foul-ups, trading nations going in and out of lockdowns and other related restrictions on commerce. But at base, increases in the general level of prices occur as newly issued currency enters circulation.

The Fed overseas two separate mechanisms for currency expansion. Quantitative easing is targeted at providing investing institutions with cash in return for low-risk assets, specifically US Treasury and agency bonds to the tune of $120bn every month. This QE has the effect of keeping bond yields suppressed and equity markets inflated because of the targeted institutions’ reinvestments. In addition — and it is separate from QE — there is the government’s budget deficit, theoretically financed out of private sector savings, but in the absence of an increase in the savings ratio, financed through the expansion of currency and credit.

Fund raising for the government is about to become chaotic

We can see that the Fed’s non-monetary approach to monetary policy begs important questions, but there are usually reasons behind it which we must consider. They give us a steer to the Fed’s real mission; its twin objectives of 2% price inflation and full employment having become secondary. It is to keep the Federal government financed by suppressing the interest cost and encouraging the expansion of bank credit to subscribe for government debt. The latter task was made easier during covid lockdowns, since unspent income temporarily accumulated in the financial system, which together with currency and credit expansion led to the government being awash with funds. But that has now changed, as the balance on the government’s general account at the Fed in Figure 2 shows.

Since March 2020, when the balance was $380bn, the government accumulated a further $1.437 trillion to a balance of $1.817 trillion in a little over four months, funded by a mixture of currency and credit inflation to fund extra government debt. Since August last year, all that accumulation and a little more has been spent into general circulation, leading to liquidity flooding the economy. This liquidity has been absorbed by the Fed’s reverse repo (RRP) balances expanding to over a trillion dollars. The increase in RRPs had been necessary to prevent bank deposit and money market rates from going negative due to excessive liquidity.

The effect on the dollar of the RRP level increasing has been to stabilise it on the foreign exchanges and to pause the headlong increase in commodity and raw material prices for the last few months. But this will almost certainly turn out to be a temporary effect. Assuming the debt ceiling will be raised in the coming weeks (it is inconceivable that either it will not or it will be suspended) the US Government will resume selling US Treasuries and T-bills into the market to top up its general account and fund its ongoing deficit. No doubt, the plan initially is for the Fed to accommodate this demand by reducing its outstanding RRP balances, thereby keeping its funds rate at the zero bound, and therefore yields on US Treasury stock suppressed.

The best laid plans need numbers to add up, and immediately we can see a problem. The Fed may have a trillion up its sleeve in the form of RRPs which can be wound down. But the Biden administration is planning $6 trillion spending in fiscal 2022, rising to $8.2 trillion by 2031. Combined with a structural deficit, the government deficit next year will almost certainly be substantially higher than the Congressional Budget Office’s current forecasts. Furthermore, the CBO assumes the annual average growth of “real” GDP will average 2.8% during fiscal 2021—2025, an assumption that is looking optimistic, given the unexpected increase in the price deflator.

In recent years the CBO’s forecasts have turned out to be overly optimistic. Furthermore, disruption of global logistics is an ongoing problem, so the supply of products to satisfy the increase in consumer spending assumed in the forecasts will continue to be restricted well into 2022. Covid disruptions have not ended and increases in infections are likely in the coming months. It all adds up to a recovery in tax revenues being postponed again, and government spending being increased more than budgeted, even before taking Biden’s proposed extra spending into account.

The CBO’s optimistic assessment of the government deficit for next year is $1.153 trillion, reducing from over $3 trillion in the current year. Allowing for all the factors listed above, more realistically, another $3 trillion deficit is likely to be the minimum for fiscal 2022, which commences at the end of this month.

Therefore, the simple problem is one of the Fed only being able to release one trillion of RRP liquidity into a market that will face demands for three trillion or more, being the likely fiscal deficit for 2022. We are back to where we were in March 2020, when the CBO forecast the deficit at $1.073 trillion, but the outturn was $3.13 trillion.

The problem for the US Treasury is it cannot close the fiscal gap, even if it wanted to — which it doesn’t. Putting record budget deficits to one side, the neo-Keynesian script demands yet more stimulus. But consumer prices are rising and are continuing to do so as the economy falters. Raising the general level of taxation would obviously be counterproductive and cutting government spending is politically impossible — not least because spending $6 trillion is Biden’s committed plan. No wonder he is looking for ways to tax the rich to fund his planned spending, but even his economic advisers must realise the numbers simply don’t stack up.

With the Biden administration unable to reduce its budget deficit, a rising interest rate environment, reflecting price inflation, is bound to result in a funding crisis. These are the debt trap circumstances which not only deters foreign ownership of the currency but persuades foreigners to dump existing currency holdings in increasing amounts. It is the downside of the Triffin dilemma, when decades of irresponsible fiscal policy are encouraged to supply foreigners with a reserve currency. Inevitably, it ends with a currency crisis. It is what led to the gold pool failure in the late 1960s and ended the Bretton Woods agreement in 1971. And according to the Treasury’s own TIC figures, foreign investment in dollar-denominated financial assets and cash now exceeds $32 trillion, roughly 150% of US GDP. The dollar has never been so over-owned by flaky foreign interests.

The impact on the dollar

While Powell hinted in his speech that tapering QE at some point is on the cards, it will simply not be possible if a similar budget deficit to this year is to be funded in 2022. Furthermore, in real terms interest rates are now deeply negative.

The impact on the dollar of another expansion of monetary policy on top of deeply negative real rates is likely to follow the pattern established in March last year. The Fed cut interest rates by 1.75% in two steps to the zero bound and announced monthly QE of $120bn. Foreigners at that time turned out to be particularly sensitive to these developments, driving the trade-weighted index down 13% between the Fed’s reflation announcements in March 2020 and January this year. More importantly, commodity and raw material prices moved significantly higher, or put more accurately the dollar lost substantial purchasing power in commodity markets. The gold price moved from a low of $1450 to a high last August of $2075.

But price inflation today is far higher than in March 2020, equivalent to a cut in interest rates into deeply negative territory in real terms — considerably greater than the 1.75% cut eighteen months ago. And the increasing certainty of rising interest rates and the effect on financial asset values rules out tapering — if anything, it is likely to be increased at the first sign of markets stumbling.

In March 2020, official price inflation measured by the CPI (U) was 1.5%. In July 2021, it was 5.4%, the equivalent of a cut in real interest rates of 4%. When they become more sensitive to the deficit arithmetic, the question now arises as to how foreigners will value the dollar against other currencies, and more importantly, against commodities. The dollar’s dead-cat bounce and the recent sideways consolidation in commodities and raw materials will not only be over, but the higher starting point for price inflation is likely to make their reactions more severe. The effect on US domestic prices are bound to reflect these factors, with price inflation increasing substantially from current levels.

We can see that in theory the first trillion of the government’s budget deficit should not be too much of a funding problem, because the Fed has a trillion of RRPs to release, which in roundabout ways can be deployed into US Treasuries. But funding the likely higher deficit at current coupons will almost certainly turn into an impossibility. Not only are implied rates highly negative in real terms, but with price inflation rising even more, coupons will have to rise significantly. The possibility that Shadowstats might record true price inflation at over 20% becomes a live prospect.

Unless the American public increase their savings materially — which is highly unlikely and therefore can be ruled out — the budget deficit will be broadly mirrored in a continuing trade deficit. So not only will foreigners be dumping over-owned dollars, but they will have further dollars to sell as well.

Rising bond yields drives bear markets

With an increasing inevitability, yields on US Treasuries are bound to rise considerably from deeply negative real rates. And since equity markets take their cue from bond yields, the damage to values in those and all other financial assets will be substantial. The more so, because the Fed has pursued a policy of inflating values of all financial assets through unprecedented levels of QE. The mystery is why markets view talk of reducing QE with equanimity.

Experience informs us that market participants can be complacent for long periods, and that during such times, the monetary authorities can suppress interest rates and distort markets with impunity. We have been in such a period for decades. The American investing public is now fully predisposed to be unquestionably bullish of financial assets having not known a period when markets, and not the Fed, decided values. Like the Fed, investors only accept the inevitable consequences of currency inflation reluctantly.

When triggered by events, the discovery of true economic and financial conditions leads to market moves that can be violent, taking nearly everyone by surprise. The consequences are likely to become self-feeding, with rising bond yields imposed by markets on the Fed, rather than the other way round, making debt funding problems even worse.

The Fed doesn’t have a mandate to just stand back and let markets decide outcomes, which is what it should do and is going to happen eventually anyway. But rising interest rates create enormous problems not just for relative values in financial assets generally, but threatens to wipe out overly indebted borrowers, including over-leveraged businesses, corporate zombies and others burdened with unproductive debt. They will also undermine commercial and residential property markets. Even the solvency of the government becomes questioned. The days when a Paul Volcker can simply raise the Fed’s fund rate to whatever it takes to kickstart falling interest rates are clearly over.

The combination of Biden’s spending proposals and a stagnating economy is making it impossible for the Fed to continue to suppress interest rates and therefore bond yields. And it is equally impossible to see how the Fed can stop them from rising without sacrificing the dollar. Not only are we going to see a new trend of rising yields established, but very quickly it will be evident there is no visible end to it. These were the dynamics faced by Rudolf von Havenstein when he was President of the Reichsbank during Germany’s hyperinflation of 1921—1923. And we know what happened at that time. And as Jay Powell demonstrated at Jackson Hole, the importance he attributes to the consequences of monetary expansion mirrors that of von Havenstein.

The truth of an emerging situation is that America has changed from a low inflation economy with a gentle erosion of the dollar’s value artificially cheapening US Treasury debt, to a commitment to hyperinflation, the start of which was the rapid expansion of M1 money supply as shown in Figure 1 above.

Meanwhile, equity markets have become wildly overvalued on the back of the Fed’s guarantee that they will never fall; that is the primary purpose of QE. A falling dollar and rising bond yields along the curve will almost certainly be the signal for the start of a bear market. And with foreign investors holding $13.3 trillion in US equities as of end-June (up $4.1 trillion in a year) foreign selling of both equities and the dollar proceeds could well be an early feature of a new bear market.

If the Fed loses control over rates, the bear market will be considerable. But the Fed is expected to keep economic confidence high. If it is to save markets, it will have to increase QE at the start of any significant fall in the S&P 500 Index — standing back and watching investors being hammered is not an option. This is why QE was reinstated in March 2020 and continues to this day at $120bn every month, amounting to $2 trillion so far.

The John Law precedent

If the inflation problem was simply one of runaway government spending, then the falling purchasing power of the currency would lead to ever greater demands on the printing presses. And the process would accelerate exponentially until the public realised there was no hope for the currency and hasten to rid themselves of it in a final collapse. This is the classic hyperinflation model, for which Germany’s well-documented monetary policies after the First World War are frequently cited.

But today’s circumstances include a commitment to ensure public confidence in financial assets is maintained by the state intervening to ensure their values remain buoyant. That is the primary purpose of quantitative easing, which we now see deployed in all major jurisdictions in the West and Japan. The consequence is that ever greater quantities of QE are required to maintain financial asset values. The policy is additional to interest rate suppression, which as I have pointed out above, is invaluable for the affordable funding of government deficits.

There is an historical precedent in the Mississippi bubble in France between 1718—1720. John Law created a similar wealth effect through a combination of monetary inflation and the encouragement of asset speculation. His objectives were firstly to reduce the royal debts, and secondly, having acquired a monopoly on France’s foreign trade, he needed to equip his Mississippi venture with ships and other infrastructure.

His method was to issue partly paid shares 10% down and the balance to be paid later. But when further issues were needed, earlier subscribers sold shares to take up their new rights to subscribe, and they also sold shares when calls were due. Law, who had also been appointed controller of the currency, printed livres to buy these shares back and support the price. But selling eventually overwhelmed the project in March 1720, and the shares fell from a peak of 10,000 livres to 4,000 livres by the following September. But the more significant casualty was the livre itself, which became worthless on the foreign exchanges in London and Amsterdam by the end of that month.

What concerns us is the similarity with today’s QE and Law acting as a director of the Banque Royale, a prototype central bank, and controller of the currency. Today, his actions would be described as quantitative easing. So far as I’m aware, while the connection is not made in the histories of the bubble, the expansion of the quantity of livres in circulation had begun to drive up prices, not just in Paris, but outwards into the countryside as well. The reason prices rose was the livre was losing purchasing power due to its inflation. The natural rate of interest on Law’s unexchangeable paper currency was therefore increasing, which became the final nail in the coffin of the Mississippi bubble.

The similarity with today’s intervention by central banks expanding the money quantity through QE to support markets is striking. It is a monetary policy, which initially suppresses the natural level of interest rates as the quantity of money increases, before it begins to lose purchasing power. It then fuels higher interest rates as its purchasing power begins to decline.

As noted above, from the peak of the Mississippi bubble the currency collapsed with the bear market in the shares over little more than six months. The use of currency printing to support the market failed for the reasons we can expect to be repeated today. By ending in a market related crisis, the normal process of currency destruction reflected in the Weimar model becomes foreshortened. Additionally, modern communications and the sheer scale of the global financial bubble today leads us to expect the end of fiat currencies to be swifter than that experienced in France just over 300 years ago.

Gold

The last time the consequences of Triffin’s dilemma hit the dollar was the failure of the gold pool in the late 1960s, which ended up driving the dollar off the last vestiges of a gold standard in 1971. The lesson was not learned. If anything, the imperative to produce dollars for export accelerated as US monetary policy was to replace gold with the dollar as the international monetary standard.

But one thing the US authorities could not wish away is the difference between a national currency and true money, the latter not being the product of credit creation. The benefit of a currency, to the issuer at least, is that it is the vehicle for transferring wealth to the government, its cronies, its licenced banks, and their favoured customers. Without currency, a government is severely limited financially.

Gold is the money naturally preferred by the people. A state-issued currency alternative inevitably suffers debasement, which is generally tolerated so long as it is not acute. The compounding debasement of the dollar since the Nixon shock in 1971 has removed about 98% of the dollar’s value, measured against gold. While the economic effect has not been beneficial —contrary to claims by neo-Keynesian economists — it has not been sufficiently marked to stop foreigners using the dollar for transactions and accumulating fixed interest bonds, bills and cash.

The evidence strongly points to foreigners’ tolerance already undermined by the fall in the dollar’s purchasing power since March 2020. At the margin, commercial entities will again alter the balance between owning useful materials and holding dollar cash in favour of the former, leading to a renewed bout of price increases for commodities. But measured against commodity and energy prices, over the very long-term gold tends to retain its purchasing power, which is why when currency debasement accelerates, measured in fiat currencies the price of gold rises.

Gold is and will remain the ultimate hedge against failing currencies and their economic consequences, and its importance has never been greater in modern times.

International

Rand Paul Teases Senate GOP Leader Run – Musk Says “I Would Support”

Rand Paul Teases Senate GOP Leader Run – Musk Says "I Would Support"

Republican Kentucky Senator Rand Paul on Friday hinted that he may jump…

Share this:

Republican Kentucky Senator Rand Paul on Friday hinted that he may jump into the race to become the next Senate GOP leader, and Elon Musk was quick to support the idea. Republicans must find a successor for periodically malfunctioning Mitch McConnell, who recently announced he'll step down in November, though intending to keep his Senate seat until his term ends in January 2027, when he'd be within weeks of turning 86.

So far, the announced field consists of two quintessential establishment types: John Cornyn of Texas and John Thune of South Dakota. While John Barrasso's name had been thrown around as one of "The Three Johns" considered top contenders, the Wyoming senator on Tuesday said he'll instead seek the number two slot as party whip.

Paul used X to tease his potential bid for the position which -- if the GOP takes back the upper chamber in November -- could graduate from Minority Leader to Majority Leader. He started by telling his 5.1 million followers he'd had lots of people asking him about his interest in running...

Thousands of people have been asking if I'd run for Senate leadership...

— Rand Paul (@RandPaul) March 8, 2024

...then followed up with a poll in which he predictably annihilated Cornyn and Thune, taking a 96% share as of Friday night, with the other two below 2% each.

????????️VOTE NOW ????️ ???? Who would you like to be the next Senate leader?

— Rand Paul (@RandPaul) March 8, 2024

Elon Musk was quick to back the idea of Paul as GOP leader, while daring Cornyn and Thune to follow Paul's lead by throwing their names out for consideration by the Twitter-verse X-verse.

I would support Rand Paul and suspect that other candidates will not actually run polls out of concern for the results, but let’s see if they will!

— Elon Musk (@elonmusk) March 8, 2024

Paul has been a stalwart opponent of security-state mass surveillance, foreign interventionism -- to include shoveling billions of dollars into the proxy war in Ukraine -- and out-of-control spending in general. He demonstrated the latter passion on the Senate floor this week as he ridiculed the latest kick-the-can spending package:

This bill is an insult to the American people. The earmarks are all the wasteful spending that you could ever hope to see, and it should be defeated. Read more: https://t.co/Jt8K5iucA4 pic.twitter.com/I5okd4QgDg

— Senator Rand Paul (@SenRandPaul) March 8, 2024

In February, Paul used Senate rules to force his colleagues into a grueling Super Bowl weekend of votes, as he worked to derail a $95 billion foreign aid bill. "I think we should stay here as long as it takes,” said Paul. “If it takes a week or a month, I’ll force them to stay here to discuss why they think the border of Ukraine is more important than the US border.”

Don't expect a Majority Leader Paul to ditch the filibuster -- he's been a hardy user of the legislative delay tactic. In 2013, he spoke for 13 hours to fight the nomination of John Brennan as CIA director. In 2015, he orated for 10-and-a-half-hours to oppose extension of the Patriot Act.

Among the general public, Paul is probably best known as Capitol Hill's chief tormentor of Dr. Anthony Fauci, who was director of the National Institute of Allergy and Infectious Disease during the Covid-19 pandemic. Paul says the evidence indicates the virus emerged from China's Wuhan Institute of Virology. He's accused Fauci and other members of the US government public health apparatus of evading questions about their funding of the Chinese lab's "gain of function" research, which takes natural viruses and morphs them into something more dangerous. Paul has pointedly said that Fauci committed perjury in congressional hearings and that he belongs in jail "without question."

Musk is neither the only nor the first noteworthy figure to back Paul for party leader. Just hours after McConnell announced his upcoming step-down from leadership, independent 2024 presidential candidate Robert F. Kennedy, Jr voiced his support:

Mitch McConnell, who has served in the Senate for almost 40 years, announced he'll step down this November.

— Robert F. Kennedy Jr (@RobertKennedyJr) February 28, 2024

Part of public service is about knowing when to usher in a new generation. It’s time to promote leaders in Washington, DC who won’t kowtow to the military contractors or…

In a testament to the extent to which the establishment recoils at the libertarian-minded Paul, mainstream media outlets -- which have been quick to report on other developments in the majority leader race -- pretended not to notice that Paul had signaled his interest in the job. More than 24 hours after Paul's test-the-waters tweet-fest began, not a single major outlet had brought it to the attention of their audience.

That may be his strongest endorsement yet.

Spread & Containment

‘I couldn’t stand the pain’: the Turkish holiday resort that’s become an emergency dental centre for Britons who can’t get treated at home

The crisis in NHS dentistry is driving increasing numbers abroad for treatment. Here are some of their stories.

Share this:

It’s a hot summer day in the Turkish city of Antalya, a Mediterranean resort with golden beaches, deep blue sea and vibrant nightlife. The pool area of the all-inclusive resort is crammed with British people on sun loungers – but they aren’t here for a holiday. This hotel is linked to a dental clinic that organises treatment packages, and most of these guests are here to see a dentist.

From Norwich, two women talk about gums and injections. A man from Wales holds a tissue close to his mouth and spits blood – he has just had two molars extracted.

The dental clinic organises everything for these dental “tourists” throughout their treatment, which typically lasts from three to 15 days. The stories I hear of what has caused them to travel to Turkey are strikingly similar: all have struggled to secure dental treatment at home on the NHS.

“The hotel is nice and some days I go to the beach,” says Susan*, a hairdresser in her mid-30s from Norwich. “But really, we aren’t tourists like in a proper holiday. We come here because we have no choice. I couldn’t stand the pain.”

This is Susan’s second visit to Antalya. She explains that her ordeal started two years earlier:

I went to an NHS dentist who told me I had gum disease … She did some cleaning to my teeth and gums but it got worse. When I ate, my teeth were moving … the gums were bleeding and it was very painful. I called to say I was in pain but the clinic was not accepting NHS patients any more.

The only option the dentist offered Susan was to register as a private patient:

I asked how much. They said £50 for x-rays and then if the gum disease got worse, £300 or so for extraction. Four of them were moving – imagine: £1,200 for losing your teeth! Without teeth I’d lose my clients, but I didn’t have the money. I’m a single mum. I called my mum and cried.

Susan’s mother told her about a friend of hers who had been to Turkey for treatment, then together they found a suitable clinic:

The prices are so much cheaper! Tooth extraction, x-rays, consultations – it all comes included. The flight and hotel for seven days cost the same as losing four teeth in Norwich … I had my lower teeth removed here six months ago, now I’ve got implants … £2,800 for everything – hotel, transfer, treatments. I only paid the flights separately.

In the UK, roughly half the adult population suffers from periodontitis – inflammation of the gums caused by plaque bacteria that can lead to irreversible loss of gums, teeth, and bone. Regular reviews by a dentist or hygienist are required to manage this condition. But nine out of ten dental practices cannot offer NHS appointments to new adult patients, while eight in ten are not accepting new child patients.

Some UK dentists argue that Britons who travel abroad for treatment do so mainly for cosmetic procedures. They warn that dental tourism is dangerous, and that if their treatment goes wrong, dentists in the UK will be unable to help because they don’t want to be responsible for further damage. Susan shrugs this off:

Dentists in England say: ‘If you go to Turkey, we won’t touch you [afterwards].’ But I don’t worry because there are no appointments at home anyway. They couldn’t help in the first place, and this is why we are in Turkey.

‘How can we pay all this money?’

As a social anthropologist, I travelled to Turkey a number of times in 2023 to investigate the crisis of NHS dentistry, and the journeys abroad that UK patients are increasingly making as a result. I have relatives in Istanbul and have been researching migration and trading patterns in Turkey’s largest city since 2016.

In August 2023, I visited the resort in Antalya, nearly 400 miles south of Istanbul. As well as Susan, I met a group from a village in Wales who said there was no provision of NHS dentistry back home. They had organised a two-week trip to Turkey: the 12-strong group included a middle-aged couple with two sons in their early 20s, and two couples who were pensioners. By going together, Anya tells me, they could support each other through their different treatments:

I’ve had many cavities since I was little … Before, you could see a dentist regularly – you didn’t even think about it. If you had pain or wanted a regular visit, you phoned and you went … That was in the 1990s, when I went to the dentist maybe every year.

Anya says that once she had children, her family and work commitments meant she had no time to go to the dentist. Then, years later, she started having serious toothache:

Every time I chewed something, it hurt. I ate soups and soft food, and I also lost weight … Even drinking was painful – tea: pain, cold water: pain. I was taking paracetamol all the time! I went to the dentist to fix all this, but there were no appointments.

Anya was told she would have to wait months, or find a dentist elsewhere:

A private clinic gave me a list of things I needed done. Oh my God, almost £6,000. My husband went too – same story. How can we pay all this money? So we decided to come to Turkey. Some people we know had been here, and others in the village wanted to come too. We’ve brought our sons too – they also need to be checked and fixed. Our whole family could be fixed for less than £6,000.

By the time they travelled, Anya’s dental problems had turned into a dental emergency. She says she could not live with the pain anymore, and was relying on paracetamol.

In 2023, about 6 million adults in the UK experienced protracted pain (lasting more than two weeks) caused by toothache. Unintentional paracetamol overdose due to dental pain is a significant cause of admissions to acute medical units. If left untreated, tooth infections can spread to other parts of the body and cause life-threatening complications – and on rare occasions, death.

In February 2024, police were called to manage hundreds of people queuing outside a newly opened dental clinic in Bristol, all hoping to be registered or seen by an NHS dentist. One in ten Britons have admitted to performing “DIY dentistry”, of which 20% did so because they could not find a timely appointment. This includes people pulling out their teeth with pliers and using superglue to repair their teeth.

In the 1990s, dentistry was almost entirely provided through NHS services, with only around 500 solely private dentists registered. Today, NHS dentist numbers in England are at their lowest level in a decade, with 23,577 dentists registered to perform NHS work in 2022-23, down 695 on the previous year. Furthermore, the precise division of NHS and private work that each dentist provides is not measured.

The COVID pandemic created longer waiting lists for NHS treatment in an already stretched public service. In Bridlington, Yorkshire, people are now reportedly having to wait eight-to-nine years to get an NHS dental appointment with the only remaining NHS dentist in the town.

In his book Patients of the State (2012), Argentine sociologist Javier Auyero describes the “indignities of waiting”. It is the poor who are mostly forced to wait, he writes. Queues for state benefits and public services constitute a tangible form of power over the marginalised. There is an ethnic dimension to this story, too. Data suggests that in the UK, patients less likely to be effective in booking an NHS dental appointment are non-white ethnic groups and Gypsy or Irish travellers, and that it is particularly challenging for refugees and asylum-seekers to access dental care.

This article is part of Conversation Insights

The Insights team generates long-form journalism derived from interdisciplinary research. The team is working with academics from different backgrounds who have been engaged in projects aimed at tackling societal and scientific challenges.

In 2022, I experienced my own dental emergency. An infected tooth was causing me debilitating pain, and needed root canal treatment. I was advised this would cost £71 on the NHS, plus £307 for a follow-up crown – but that I would have to wait months for an appointment. The pain became excruciating – I could not sleep, let alone wait for months. In the same clinic, privately, I was quoted £1,300 for the treatment (more than half my monthly income at the time), or £295 for a tooth extraction.

I did not want to lose my tooth because of lack of money. So I bought a flight to Istanbul immediately for the price of the extraction in the UK, and my tooth was treated with root canal therapy by a private dentist there for £80. Including the costs of travelling, the total was a third of what I was quoted to be treated privately in the UK. Two years on, my treated tooth hasn’t given me any more problems.

A better quality of life

Not everyone is in Antalya for emergency procedures. The pensioners from Wales had contacted numerous clinics they found on the internet, comparing prices, treatments and hotel packages at least a year in advance, in a carefully planned trip to get dental implants – artificial replacements for tooth roots that help support dentures, crowns and bridges.

In Turkey, all the dentists I speak to (most of whom cater mainly for foreigners, including UK nationals) consider implants not a cosmetic or luxurious treatment, but a development in dentistry that gives patients who are able to have the procedure a much better quality of life. This procedure is not available on the NHS for most of the UK population, and the patients I meet in Turkey could not afford implants in private clinics back home.

Paul is in Antalya to replace his dentures, which have become uncomfortable and irritating to his gums, with implants. He says he couldn’t find an appointment to see an NHS dentist. His wife Sonia went through a similar procedure the year before and is very satisfied with the results, telling me: “Why have dentures that you need to put in a glass overnight, in the old style? If you can have implants, I say, you’re better off having them.”

Most of the dental tourists I meet in Antalya are white British: this city, known as the Turkish Riviera, has developed an entire economy catering to English-speaking tourists. In 2023, more than 1.3 million people visited the city from the UK, up almost 15% on the previous year.

Read more: NHS dentistry is in crisis – are overseas dentists the answer?

In contrast, the Britons I meet in Istanbul are predominantly from a non-white ethnic background. Omar, a pensioner of Pakistani origin in his early 70s, has come here after waiting “half a year” for an NHS appointment to fix the dental bridge that is causing him pain. Omar’s son had been previously for a hair transplant, and was offered a free dental checkup by the same clinic, so he suggested it to his father. Having worked as a driver for a manufacturing company for two decades in Birmingham, Omar says he feels disappointed to have contributed to the British economy for so long, only to be “let down” by the NHS:

At home, I must wait and wait and wait to get a bridge – and then I had many problems with it. I couldn’t eat because the bridge was uncomfortable and I was in pain, but there were no appointments on the NHS. I asked a private dentist and they recommended implants, but they are far too expensive [in the UK]. I started losing weight, which is not a bad thing at the beginning, but then I was worrying because I couldn’t chew and eat well and was losing more weight … Here in Istanbul, I got dental implants – US$500 each, problem solved! In England, each implant is maybe £2,000 or £3,000.

In the waiting area of another clinic in Istanbul, I meet Mariam, a British woman of Iraqi background in her late 40s, who is making her second visit to the dentist here. Initially, she needed root canal therapy after experiencing severe pain for weeks. Having been quoted £1,200 in a private clinic in outer London, Mariam decided to fly to Istanbul instead, where she was quoted £150 by a dentist she knew through her large family. Even considering the cost of the flight, Mariam says the decision was obvious:

Dentists in England are so expensive and NHS appointments so difficult to find. It’s awful there, isn’t it? Dentists there blamed me for my rotten teeth. They say it’s my fault: I don’t clean or I ate sugar, or this or that. I grew up in a village in Iraq and didn’t go to the dentist – we were very poor. Then we left because of war, so we didn’t go to a dentist … When I arrived in London more than 20 years ago, I didn’t speak English, so I still didn’t go to the dentist … I think when you move from one place to another, you don’t go to the dentist unless you are in real, real pain.

In Istanbul, Mariam has opted not only for the urgent root canal treatment but also a longer and more complex treatment suggested by her consultant, who she says is a renowned doctor from Syria. This will include several extractions and implants of back and front teeth, and when I ask what she thinks of achieving a “Hollywood smile”, Mariam says:

Who doesn’t want a nice smile? I didn’t come here to be a model. I came because I was in pain, but I know this doctor is the best for implants, and my front teeth were rotten anyway.

Dentists in the UK warn about the risks of “overtreatment” abroad, but Mariam appears confident that this is her opportunity to solve all her oral health problems. Two of her sisters have already been through a similar treatment, so they all trust this doctor.

The UK’s ‘dental deserts’

To get a fuller understanding of the NHS dental crisis, I’ve also conducted 20 interviews in the UK with people who have travelled or were considering travelling abroad for dental treatment.

Joan, a 50-year-old woman from Exeter, tells me she considered going to Turkey and could have afforded it, but that her back and knee problems meant she could not brave the trip. She has lost all her lower front teeth due to gum disease and, when I meet her, has been waiting 13 months for an NHS dental appointment. Joan tells me she is living in “shame”, unable to smile.

In the UK, areas with extremely limited provision of NHS dental services – known as as “dental deserts” – include densely populated urban areas such as Portsmouth and Greater Manchester, as well as many rural and coastal areas.

In Felixstowe, the last dentist taking NHS patients went private in 2023, despite the efforts of the activist group Toothless in Suffolk to secure better access to NHS dentists in the area. It’s a similar story in Ripon, Yorkshire, and in Dumfries & Galloway, Scotland, where nearly 25,000 patients have been de-registered from NHS dentists since 2021.

Data shows that 2 million adults must travel at least 40 miles within the UK to access dental care. Branding travel for dental care as “tourism” carries the risk of disguising the elements of duress under which patients move to restore their oral health – nationally and internationally. It also hides the immobility of those who cannot undertake such journeys.

The 90-year-old woman in Dumfries & Galloway who now faces travelling for hours by bus to see an NHS dentist can hardly be considered “tourism” – nor the Ukrainian war refugees who travelled back from West Sussex and Norwich to Ukraine, rather than face the long wait to see an NHS dentist.

Many people I have spoken to cannot afford the cost of transport to attend dental appointments two hours away – or they have care responsibilities that make it impossible. Instead, they are forced to wait in pain, in the hope of one day securing an appointment closer to home.

‘Your crisis is our business’

The indignities of waiting in the UK are having a big impact on the lives of some local and foreign dentists in Turkey. Some neighbourhoods are rapidly changing as dental and other health clinics, usually in luxurious multi-storey glass buildings, mushroom. In the office of one large Istanbul medical complex with sections for hair transplants and dentistry (plus one linked to a hospital for more extensive cosmetic surgery), its Turkish owner and main investor tells me:

Your crisis is our business, but this is a bazaar. There are good clinics and bad clinics, and unfortunately sometimes foreign patients do not know which one to choose. But for us, the business is very good.

This clinic only caters to foreign patients. The owner, an architect by profession who also developed medical clinics in Brazil, describes how COVID had a major impact on his business:

When in Europe you had COVID lockdowns, Turkey allowed foreigners to come. Many people came for ‘medical tourism’ – we had many patients for cosmetic surgery and hair transplants. And that was when the dental business started, because our patients couldn’t see a dentist in Germany or England. Then more and more patients started to come for dental treatments, especially from the UK and Ireland. For them, it’s very, very cheap here.

The reasons include the value of the Turkish lira relative to the British pound, the low cost of labour, the increasing competition among Turkish clinics, and the sheer motivation of dentists here. While most dentists catering to foreign patients are from Turkey, others have arrived seeking refuge from war and violence in Syria, Iraq, Afghanistan, Iran and beyond. They work diligently to rebuild their lives, careers and lost wealth.

Regardless of their origin, all dentists in Turkey must be registered and certified. Hamed, a Syrian dentist and co-owner of a new clinic in Istanbul catering to European and North American patients, tells me:

I know that you say ‘Syrian’ and people think ‘migrant’, ‘refugee’, and maybe think ‘how can this dentist be good?’ – but Syria, before the war, had very good doctors and dentists. Many of us came to Turkey and now I have a Turkish passport. I had to pass the exams to practise dentistry here – I study hard. The exams are in Turkish and they are difficult, so you cannot say that Syrian doctors are stupid.

Hamed talks excitedly about the latest technology that is coming to his profession: “There are always new materials and techniques, and we cannot stop learning.” He is about to travel to Paris to an international conference:

I can say my techniques are very advanced … I bet I put more implants and do more bone grafting and surgeries every week than any dentist you know in England. A good dentist is about practice and hand skills and experience. I work hard, very hard, because more and more patients are arriving to my clinic, because in England they don’t find dentists.

While there is no official data about the number of people travelling from the UK to Turkey for dental treatment, investors and dentists I speak to consider that numbers are rocketing. From all over the world, Turkey received 1.2 million visitors for “medical tourism” in 2022, an increase of 308% on the previous year. Of these, about 250,000 patients went for dentistry. One of the most renowned dental clinics in Istanbul had only 15 British patients in 2019, but that number increased to 2,200 in 2023 and is expected to reach 5,500 in 2024.

Like all forms of medical care, dental treatments carry risks. Most clinics in Turkey offer a ten-year guarantee for treatments and a printed clinical history of procedures carried out, so patients can show this to their local dentists and continue their regular annual care in the UK. Dental treatments, checkups and maintaining a good oral health is a life-time process, not a one-off event.

Many UK patients, however, are caught between a rock and a hard place – criticised for going abroad, yet unable to get affordable dental care in the UK before and after their return. The British Dental Association has called for more action to inform these patients about the risks of getting treated overseas – and has warned UK dentists about the legal implications of treating these patients on their return. But this does not address the difficulties faced by British patients who are being forced to go abroad in search of affordable, often urgent dental care.

A global emergency

The World Health Organization states that the explosion of oral disease around the world is a result of the “negligent attitude” that governments, policymakers and insurance companies have towards including oral healthcare under the umbrella of universal healthcare. It as if the health of our teeth and mouth is optional; somehow less important than treatment to the rest of our body. Yet complications from untreated tooth decay can lead to hospitalisation.

The main causes of oral health diseases are untreated tooth decay, severe gum disease, toothlessness, and cancers of the lip and oral cavity. Cases grew during the pandemic, when little or no attention was paid to oral health. Meanwhile, the global cosmetic dentistry market is predicted to continue growing at an annual rate of 13% for the rest of this decade, confirming the strong relationship between socioeconomic status and access to oral healthcare.

In the UK since 2018, there have been more than 218,000 admissions to hospital for rotting teeth, of which more than 100,000 were children. Some 40% of children in the UK have not seen a dentist in the past 12 months. The role of dentists in prevention of tooth decay and its complications, and in the early detection of mouth cancer, is vital. While there is a 90% survival rate for mouth cancer if spotted early, the lack of access to dental appointments is causing cases to go undetected.

The reasons for the crisis in NHS dentistry are complex, but include: the real-term cuts in funding to NHS dentistry; the challenges of recruitment and retention of dentists in rural and coastal areas; pay inequalities facing dental nurses, most of them women, who are being badly hit by the cost of living crisis; and, in England, the 2006 Dental Contract that does not remunerate dentists in a way that encourages them to continue seeing NHS patients.

The UK is suffering a mass exodus of the public dentistry workforce, with workers leaving the profession entirely or shifting to the private sector, where payments and life-work balance are better, bureaucracy is reduced, and prospects for career development look much better. A survey of general dental practitioners found that around half have reduced their NHS work since the pandemic – with 43% saying they were likely to go fully private, and 42% considering a career change or taking early retirement.

Reversing the UK’s dental crisis requires more commitment to substantial reform and funding than the “recovery plan” announced by Victoria Atkins, the secretary of state for health and social care, on February 7.

The stories I have gathered show that people travelling abroad for dental treatment don’t see themselves as “tourists” or vanity-driven consumers of the “Hollywood smile”. Rather, they have been forced by the crisis in NHS dentistry to seek out a service 1,500 miles away in Turkey that should be a basic, affordable right for all, on their own doorstep.

*Names in this article have been changed to protect the anonymity of the interviewees.

For you: more from our Insights series:

GP crisis: how did things go so wrong, and what needs to change?

Insomnia: how chronic sleep problems can lead to a spiralling decline in mental health

To hear about new Insights articles, join the hundreds of thousands of people who value The Conversation’s evidence-based news. Subscribe to our newsletter.

Diana Ibanez Tirado receives funding from the School of Global Studies, University of Sussex.

pound pandemic treatment therapy spread recovery iran brazil european europe uk germany ukraine world health organizationInternational

Beloved mall retailer files Chapter 7 bankruptcy, will liquidate

The struggling chain has given up the fight and will close hundreds of stores around the world.

Share this:

{kind=link}

{kind=link}

It has been a brutal period for several popular retailers. The fallout from the covid pandemic and a challenging economic environment have pushed numerous chains into bankruptcy with Tuesday Morning, Christmas Tree Shops, and Bed Bath & Beyond all moving from Chapter 11 to Chapter 7 bankruptcy liquidation.

In all three of those cases, the companies faced clear financial pressures that led to inventory problems and vendors demanding faster, or even upfront payment. That creates a sort of inevitability.

Related: Beloved retailer finds life after bankruptcy, new famous owner

When a retailer faces financial pressure it sets off a cycle where vendors become wary of selling them items. That leads to barren shelves and no ability for the chain to sell its way out of its financial problems.

Once that happens bankruptcy generally becomes the only option. Sometimes that means a Chapter 11 filing which gives the company a chance to negotiate with its creditors. In some cases, deals can be worked out where vendors extend longer terms or even forgive some debts, and banks offer an extension of loan terms.

In other cases, new funding can be secured which assuages vendor concerns or the company might be taken over by its vendors. Sometimes, as was the case with David's Bridal, a new owner steps in, adds new money, and makes deals with creditors in order to give the company a new lease on life.

It's rare that a retailer moves directly into Chapter 7 bankruptcy and decides to liquidate without trying to find a new source of funding.

Image source: Getty Images

The Body Shop has bad news for customers

The Body Shop has been in a very public fight for survival. Fears began when the company closed half of its locations in the United Kingdom. That was followed by a bankruptcy-style filing in Canada and an abrupt closure of its U.S. stores on March 4.

"The Canadian subsidiary of the global beauty and cosmetics brand announced it has started restructuring proceedings by filing a Notice of Intention (NOI) to Make a Proposal pursuant to the Bankruptcy and Insolvency Act (Canada). In the same release, the company said that, as of March 1, 2024, The Body Shop US Limited has ceased operations," Chain Store Age reported.

A message on the company's U.S. website shared a simple message that does not appear to be the entire story.

"We're currently undergoing planned maintenance, but don't worry we're due to be back online soon."

That same message is still on the company's website, but a new filing makes it clear that the site is not down for maintenance, it's down for good.

The Body Shop files for Chapter 7 bankruptcy

While the future appeared bleak for The Body Shop, fans of the brand held out hope that a savior would step in. That's not going to be the case.

The Body Shop filed for Chapter 7 bankruptcy in the United States.

"The US arm of the ethical cosmetics group has ceased trading at its 50 outlets. On Saturday (March 9), it filed for Chapter 7 insolvency, under which assets are sold off to clear debts, putting about 400 jobs at risk including those in a distribution center that still holds millions of dollars worth of stock," The Guardian reported.

After its closure in the United States, the survival of the brand remains very much in doubt. About half of the chain's stores in the United Kingdom remain open along with its Australian stores.

The future of those stores remains very much in doubt and the chain has shared that it needs new funding in order for them to continue operating.

The Body Shop did not respond to a request for comment from TheStreet.

bankruptcy pandemic canada

Veterans Affairs Kept COVID-19 Vaccine Mandate In Place Without Evidence

The Coming Of The Police State In America

Beloved mall retailer files Chapter 7 bankruptcy, will liquidate

‘I couldn’t stand the pain’: the Turkish holiday resort that’s become an emergency dental centre for Britons who can’t get treated at home

Low Iron Levels In Blood Could Trigger Long COVID: Study

Rand Paul Teases Senate GOP Leader Run – Musk Says “I Would Support”

Another beloved brewery files Chapter 11 bankruptcy

Walmart has really good news for shoppers (and Joe Biden)

Walmart joins Costco in sharing key pricing news

Are Voters Recoiling Against Disorder?

-

Uncategorized3 weeks ago

Uncategorized3 weeks agoAll Of The Elements Are In Place For An Economic Crisis Of Staggering Proportions

-

Uncategorized1 month ago

Uncategorized1 month agoCathie Wood sells a major tech stock (again)

-

Uncategorized3 weeks ago

Uncategorized3 weeks agoCalifornia Counties Could Be Forced To Pay $300 Million To Cover COVID-Era Program

-

Uncategorized2 weeks ago

Uncategorized2 weeks agoApparel Retailer Express Moving Toward Bankruptcy

-

Uncategorized4 weeks ago

Uncategorized4 weeks agoIndustrial Production Decreased 0.1% in January

-

International3 days ago

International3 days agoWalmart launches clever answer to Target’s new membership program

-

International3 days ago

International3 days agoEyePoint poaches medical chief from Apellis; Sandoz CFO, longtime BioNTech exec to retire

-

Uncategorized3 weeks ago

Uncategorized3 weeks agoRFK Jr: The Wuhan Cover-Up & The Rise Of The Biowarfare-Industrial Complex