Uncategorized

Housing completion data is positive news for housing market

During a typical recession, builders typically show lower starts, permits, and completion data. But builders now they have a massive backlog of homes they…

Share this:

The best way to deal with inflation is always adding more supply: if you’re trying to defeat inflation by destroying demand, you’ve already lost the battle and will hurt future production. That’s why today’s housing completion data was excellent news.

During a traditional recession, builders typically show lower starts, permits, and completion data. However, in an odd twist, builders now they have a massive backlog of homes they need to finish, which is historically abnormal. This is the reason construction workers still have jobs, and that backlog needs to be finished; this is a positive outcome.

The bigger story here is that if we want to see mortgage rates fall, we need more rental units, and right now we have a massive backlog of 2-unit homes under construction — over 900,000. If we didn’t have this backlog of rental units that need to be built, the inflationary story wouldn’t look so bright next year, meaning that we would have higher inflationary data for longer.

So in the latest Census report, housing completion data grew. Still, outside of that, it’s a story of a sector in a traditional recession, something I wrote about in June and talked about on CNBC several months ago. With that said, let’s look at today’s housing starts data.

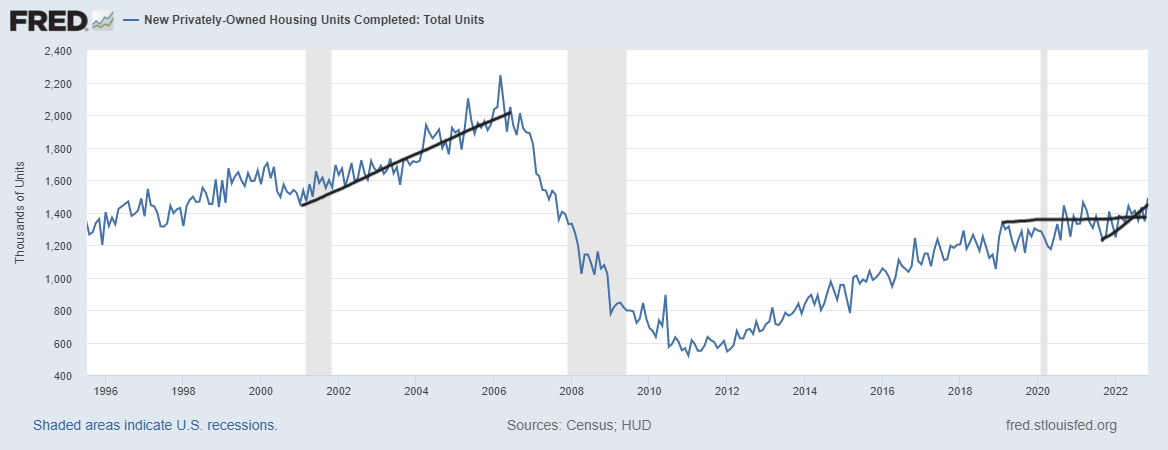

From Census: Housing Completions Privately owned housing completions in November were at a seasonally adjusted annual rate of 1,490,000. This is 10.8 percent (±15.8 percent)* above the revised October estimate of 1,345,000 and is 6.0 percent (±17.6 percent)* above the November 2021 rate of 1,406,000. Single-family housing completions in November were at a rate of 1,047,000; this is 9.5 percent (±12.9 percent)* above the revised October rate of 956,000. The November rate for units in buildings with five units or more was 430,000.

Traditionally, housing starts, permits, and completions would move together, like what we saw in 2002-2005. However, due to the supply chain lag, it took too long to build homes over the last several years. The upside to that is that the builders have this backlog keeping construction workers employed and creating more supply to fight inflation next year.

The housing recession story is separate from the housing completion story and inventory backlog. Housing permits are falling, since builders need to be more confident in building something. Cheaper housing is a terrible business model because the builders need to get paid. So, the housing permits story is done. The builders will finish what they are legally obligated to do. After that process, it’s all about rates, rates and more rates.

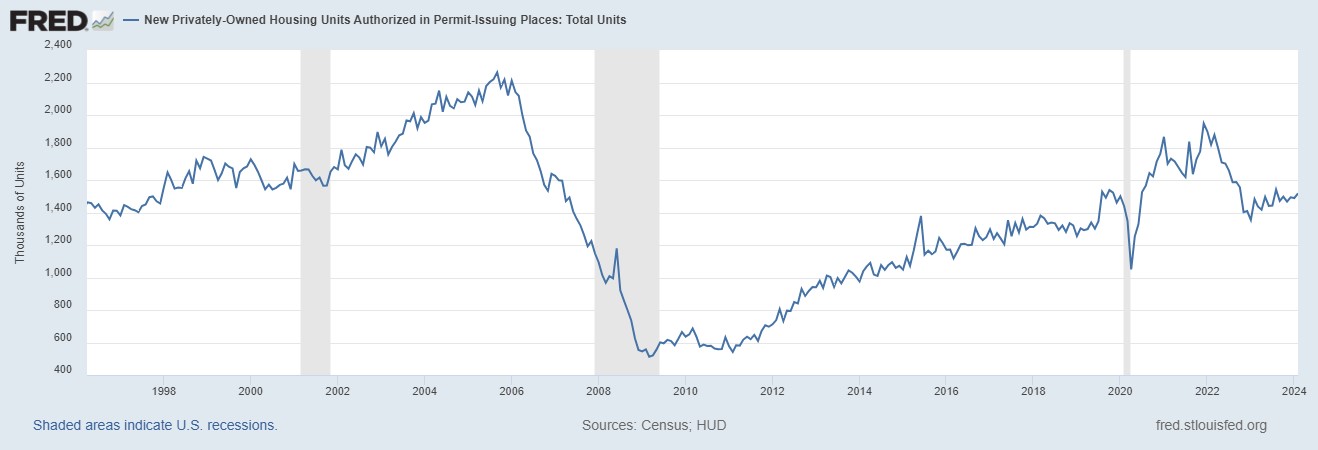

From Census: Building Permits Privately owned housing units authorized by building permits in November were at a seasonally adjusted annual rate of 1,342,000. This is 11.2 percent below the revised October rate of 1,512,000 and 22.4 percent below the November 2021 rate of 1,729,000. Single-family authorizations in November were at a rate of 781,000; this is 7.1 percent below the revised October figure of 841,000. Authorizations of units in buildings with five units or more were at a rate of 509,000 in November.

In the chart below you can see more evidence of the housing recession; permits are falling as expected with demand getting weaker. From 2002-2005 it was a steady rise to the top of the housing bubble, and then it burst. We see how wild the COVID-19 data has been, but if you smooth out the heated parts, we never got production close to what we saw during the housing bubble years.

Housing starts are also done. The builders have a backlog here, but they are lower than they do with the multifamily sector. We should be grateful that the backlog exists because otherwise construction labor would have already been hit.

From Census: Housing Starts Privately owned housing starts in November were at a seasonally adjusted annual rate of 1,427,000. This is 0.5 percent (±12.3 percent)* below the revised October estimate of 1,434,000 and is 16.4 percent (±13.4 percent) below the November 2021 rate of 1,706,000. ingle-family housing starts in November were at a rate of 828,000; this is 4.1 percent (±11.3 percent)* below the revised October figure of 863,000. The November rate for units in buildings with five units or more was 584,000.

The most extensive housing recessionary data line is in the single-family starts. As we can see in the chart below, single-family starts are heading toward the lows we had in COVID-19. The homebuilders will not issue any new permits to build single-family homes until they can get their monthly supply levels down.

My rule of thumb for anticipating builder behavior is based on the three-month supply average. This has nothing to do with the existing home sales market; this monthly supply data only applies the new home sales market.

- When supply is 4.3 months, and below, this is an excellent market for builders.

- When supply is 4.4 to 6.4 months, this is an OK market for the builders. They will build as long as new home sales are growing.

- The builders will pull back on construction when the supply is 6.5 months and above.

We currently have 8.9 months of supply, and we will get an update on this data line next week.

The builder’s confidence data came out yesterday, and the decline in this index continues. As long as this is the case, the housing recession regarding the future production of homes outside the backlog will continue.

Except, we had one bit of good news. The forward-looking data regarding sales looking out six months was positive.

From the NAHB/Wells Fargo Housing Market Index (HMI): “The silver lining in this HMI report is that it is the smallest drop in the index in the past six months, indicating that we are possibly nearing the bottom of the cycle for builder sentiment. Mortgage rates are down from above 7% in recent weeks to about 6.3% today, and for the first time since April, builders registered an increase in future sales expectations”.

Over the last six weeks, we have seen that buyers came back in the data line when mortgage rates fell from 7.373% to 6.12%. The forward-looking purchase application data found a bottom in the data line and has been rising ever since. Mortgage rates have increased from the lows recently. However, this is a good sign that we don’t even need to get rates back down to 5% to find some stabilization. We need rates to get to the low 6% range with duration for the market to find some stabilization.

The housing starts report was good only because housing completions rose, and that’s the most positive story we can have for having mortgage rates to go lower next year. The housing recession, which started in June, is still going on, as we can see with the builders confidence index collapsing. The longer this housing recession goes, the less productive we will see.

I do expect a significant slowdown in multifamily construction next year, but the backlog of over 900,000 units under construction is something we all should be rooting for to get done. To have a sustained move lower in mortgage rates, the growth rate of inflation needs to fall, and shelter inflation is the big driver of core inflation.

Uncategorized

Apartment permits are back to recession lows. Will mortgage rates follow?

If housing leads us into a recession in the near future, that means mortgage rates have stayed too high for too long.

Share this:

In Tuesday’s report, the 5-unit housing permits data hit the same levels we saw in the COVID-19 recession. Once the backlog of apartments is finished, those jobs will be at risk, which traditionally means mortgage rates would fall soon after, as they have in previous economic cycles.

However, this is happening while single-family permits are still rising as the rate of builder buy-downs and the backlog of single-family homes push single-family permits and starts higher. It is a tale of two markets — something I brought up on CNBC earlier this year to explain why this trend matters with housing starts data because the two marketplaces are heading in opposite directions.

The question is: Will the uptick in single-family permits keep mortgage rates higher than usual? As long as jobless claims stay low, the falling 5-unit apartment permit data might not lead to lower mortgage rates as it has in previous cycles.

From Census: Building Permits: Privately‐owned housing units authorized by building permits in February were at a seasonally adjusted annual rate of 1,518,000. This is 1.9 percent above the revised January rate of 1,489,000 and 2.4 percent above the February 2023 rate of 1,482,000.

When people say housing leads us in and out of a recession, it is a valid premise and that is why people carefully track housing permits. However, this housing cycle has been unique. Unfortunately, many people who have tracked this housing cycle are still stuck on 2008, believing that what happened during COVID-19 was rampant demand speculation that would lead to a massive supply of homes once home sales crashed. This would mean the builders couldn’t sell more new homes or have housing permits rise.

Housing permits, starts and new home sales were falling for a while, and in 2022, the data looked recessionary. However, new home sales were never near the 2005 peak, and the builders found a workable bottom in sales by paying down mortgage rates to boost demand. The first level of job loss recessionary data has been averted for now. Below is the chart of the building permits.

On the other hand, the apartment boom and bust has already happened. Permits are already back to the levels of the COVID-19 recession and have legs to move lower. Traditionally, when this data line gets this negative, a recession isn’t far off. But, as you can see in the chart below, there’s a big gap between the housing permit data for single-family and five units. Looking at this chart, the recession would only happen after single-family and 5-unit permits fall together, not when we have a gap like we see today.

From Census: Housing completions: Privately‐owned housing completions in February were at a seasonally adjusted annual rate of 1,729,000.

As we can see in the chart below, we had a solid month of housing completions. This was driven by 5-unit completions, which have been in the works for a while now. Also, this month’s report show a weather impact as progress in building was held up due to bad weather. However, the good news is that more supply of rental units will mean the fight against rent inflation will be positive as more supply is the best way to deal with inflation. In time, that is also good news for mortgage rates.

Housing Starts: Privately‐owned housing starts in February were at a seasonally adjusted annual rate of 1,521,000. This is 10.7 percent (±14.2 percent)* above the revised January estimate of 1,374,000 and is 5.9 percent (±10.0 percent)* above the February 2023 rate of 1,436,000.

Housing starts data beat to the upside, but the real story is that the marketplace has diverged into two different directions. The apartment boom is over and permits are heading below the COVID-19 recession, but as long as the builders can keep rates low enough to sell more new homes, single-family permits and starts can slowly move forward.

If we lose the single-family marketplace, expect the chart below to look like it always does before a recession — meaning residential construction workers lose their jobs. For now, the apartment construction workers are at the most risk once they finish the backlog of apartments under construction.

Overall, the housing starts beat to the upside. Still, the report’s internals show a marketplace with early recessionary data lines, which traditionally mean mortgage rates should go lower soon. If housing leads us into a recession in the near future, that means mortgage rates have stayed too high for too long and restrictive policy by the Fed created a recession as we have seen in previous economic cycles.

The builders have been paying down rates to keep construction workers employed, but if rates go higher, it will get more and more challenging to do this because not all builders have the capacity to buy down rates. Last year, we saw what 8% mortgage rates did to new home sales; they dropped before rates fell. So, this is something to keep track of, especially with a critical Federal Reserve meeting this week.

recession covid-19 fed federal reserve home sales mortgage rates recessionUncategorized

One more airline cracks down on lounge crowding in a way you won’t like

Qantas Airways is increasing the price of accessing its network of lounges by as much as 17%.

Share this:

Over the last two years, multiple airlines have dealt with crowding in their lounges. While they are designed as a luxury experience for a small subset of travelers, high numbers of people taking a trip post-pandemic as well as the different ways they are able to gain access through status or certain credit cards made it difficult for some airlines to keep up with keeping foods stocked, common areas clean and having enough staff to serve bar drinks at the rate that customers expect them.

In the fall of 2023, Delta Air Lines (DAL) caught serious traveler outcry after announcing that it was cracking down on crowding by raising how much one needs to spend for lounge access and limiting the number of times one can enter those lounges.

Related: Competitors pushed Delta to backtrack on its lounge and loyalty program changes

Some airlines saw the outcry with Delta as their chance to reassure customers that they would not raise their fees while others waited for the storm to pass to quietly implement their own increases.

Shutterstock

This is how much more you'll have to pay for Qantas lounge access

Australia's flagship carrier Qantas Airways (QUBSF) is the latest airline to announce that it would raise the cost accessing the 24 lounges across the country as well as the 600 international lounges available at airports across the world through partner airlines.

More Travel:

- A new travel term is taking over the internet (and reaching airlines and hotels)

- The 10 best airline stocks to buy now

- Airlines see a new kind of traveler at the front of the plane

Unlike other airlines which grant access primarily after reaching frequent flyer status, Qantas also sells it through a membership — starting from April 18, 2024, prices will rise from $600 Australian dollars ($392 USD) to $699 AUD ($456 USD) for one year, $1,100 ($718 USD) to $1,299 ($848 USD) for two years and $2,000 AUD ($1,304) to lock in the rate for four years.

Those signing up for lounge access for the first time also currently pay a joining fee of $99 AUD ($65 USD) that will rise to $129 AUD ($85 USD).

The airline also allows customers to purchase their membership with Qantas Points they collect through frequent travel; the membership fees are also being raised by the equivalent amount in points in what adds up to as much as 17% — from 308,000 to 399,900 to lock in access for four years.

Airline says hikes will 'cover cost increases passed on from suppliers'

"This is the first time the Qantas Club membership fees have increased in seven years and will help cover cost increases passed on from a range of suppliers over that time," a Qantas spokesperson confirmed to Simple Flying. "This follows a reduction in the membership fees for several years during the pandemic."

The spokesperson said the gains from the increases will go both towards making up for inflation-related costs and keeping existing lounges looking modern by updating features like furniture and décor.

While the price increases also do not apply for those who earned lounge access through frequent flyer status or change what it takes to earn that status, Qantas is also introducing even steeper increases for those renewing a membership or adding additional features such as spouse and partner memberships.

In some cases, the cost of these features will nearly double from what members are paying now.

stocks pandemicUncategorized

Star Wars icon gives his support to Disney, Bob Iger

Disney shareholders have a huge decision to make on April 3.

Share this:

Disney's (DIS) been facing some headwinds up top, but its leadership just got backing from one of the company's more prominent investors.

Star Wars creator George Lucas put out of statement in support of the company's current leadership team, led by CEO Bob Iger, ahead of the April 3 shareholders meeting which will see investors vote on the company's 12-member board.

"Creating magic is not for amateurs," Lucas said in a statement. "When I sold Lucasfilm just over a decade ago, I was delighted to become a Disney shareholder because of my long-time admiration for its iconic brand and Bob Iger’s leadership. When Bob recently returned to the company during a difficult time, I was relieved. No one knows Disney better. I remain a significant shareholder because I have full faith and confidence in the power of Disney and Bob’s track record of driving long-term value. I have voted all of my shares for Disney’s 12 directors and urge other shareholders to do the same."

Related: Disney stands against Nelson Peltz as leadership succession plan heats up

Lucasfilm was acquired by Disney for $4 billion in 2012 — notably under the first term of Iger. He received over 37 million in shares of Disney during the acquisition.

Lucas' statement seems to be an attempt to push investors away from the criticism coming from The Trian Partners investment group, led by Nelson Peltz. The group, owns about $3 million in shares of the media giant, is pushing two candidates for positions on the board, which are Peltz and former Disney CFO Jay Rasulo.

Peltz and Co. have called out a pair of Disney directors — Michael Froman and Maria Elena Lagomasino — for their lack of experience in the media space.

Related: Women's basketball is gaining ground, but is March Madness ready to rival the men's game?

Blackwells Capital is also pushing three of its candidates to take seats during the early April shareholder meeting, though Reuters has reported that the firm has been supportive of the company's current direction.

Disney has struggled in recent years amid the changes in media and the effects of the pandemic — which triggered the return of Iger at the helm in late 2022. After going through mass layoffs in the spring of 2023 and focusing on key growth brands, the company has seen a steady recovery with its stock up over 25% year-to-date and around 40% for the last six months.

Related: Veteran fund manager picks favorite stocks for 2024

stocks pandemic recovery

Apartment permits are back to recession lows. Will mortgage rates follow?

Manufacturing and construction vs. the still-inverted yield curve

When words make you sick

How much stress is too much? A psychiatrist explains the links between toxic stress and poor health − and how to get help

Caitlin Clark, Coach Prime, and Linsanity: The Anatomy of a Viewership ‘Craze’

PR55α-controlled PP2A Inhibits p16 Expression and Blocks Cellular Senescence Induction

US Economic Conditions Scream “Buy Gold”

Wall Street Bonuses Fall For Second Year To 2019 Lows Amid Capital Markets Freeze

Half Of Downtown Pittsburgh Office Space Could Be Empty In 4 Years

Airline, travel companies face Chapter 11 bankruptcy, default risk

-

Spread & Containment7 days ago

Spread & Containment7 days agoIFM’s Hat Trick and Reflections On Option-To-Buy M&A

-

Uncategorized4 weeks ago

Uncategorized4 weeks agoAll Of The Elements Are In Place For An Economic Crisis Of Staggering Proportions

-

International2 weeks ago

International2 weeks agoEyePoint poaches medical chief from Apellis; Sandoz CFO, longtime BioNTech exec to retire

-

Uncategorized1 month ago

Uncategorized1 month agoCalifornia Counties Could Be Forced To Pay $300 Million To Cover COVID-Era Program

-

Uncategorized4 weeks ago

Uncategorized4 weeks agoApparel Retailer Express Moving Toward Bankruptcy

-

Uncategorized1 month ago

Uncategorized1 month agoIndustrial Production Decreased 0.1% in January

-

International2 weeks ago

International2 weeks agoWalmart launches clever answer to Target’s new membership program

-

Uncategorized1 month ago

Uncategorized1 month agoRFK Jr: The Wuhan Cover-Up & The Rise Of The Biowarfare-Industrial Complex