Government

House Passes Biden’s Build Back Better Plan, Sending It To The Senate

House Passes Biden’s Build Back Better Plan, Sending It To The Senate

Update (940ET): As expected, the Democrat-controlled House has voted through Biden’s Build Back Better spending plan in a 220 to 213 vote with every Republican voting again

Share this:

Update (940ET): As expected, the Democrat-controlled House has voted through Biden's Build Back Better spending plan in a 220 to 213 vote with every Republican voting against the Bill, and one Democrat, Rep. Jared Golden, voted "no" over the SALT cap provision. It will now be sent to the Senate where its fate remains uncertain and will be determined by moderate Democrats Joe Manchin (WV) and Kyrsten Sinema (AZ).

House Democrats celebrate as the $1.75T Build Back Better Act passes the House 220-213. pic.twitter.com/56puVYdOFf

— The Recount (@therecount) November 19, 2021

Democrats are chanting “Build Back Better!” On the floor as bill passes.

— Erik Wasson (@elwasson) November 19, 2021

As Newsquawk notes, the Senate will take its turn to vote on the bill and all 50 Democratic senators are needed to vote for the bill in order for it to pass. The two senators in question are the moderate Senators Manchin and Sinema; a recent CNN report suggested that Democrats were far more reassured that Sinema would back the Build Back Better bill although they are still uncertain about Manchin.

Note, Senators also have the ability to change parts of the bill. Manchin has previously expressed concerns with the “Paid Leave” component of the bill and believes it should be passed in a bipartisan effort in a separate bill. The SALT cap may also face some concern as it is expected to be one of the most expensive parts in the bill. Manchin has also raised concerns that 10 years of funding should pay for 10 years of services, while Child Care aid only lasts for six years, and cheaper premiums on the Affordable Health Care Act only last for five years. If the Senate were to make adjustments, the bill would then have to be sent back to the House.

Here are some recent comments from Moderates:

- Manchin said Thursday 18th November he has not decided on whether to vote to proceed to the Build Back Better Bill, says the House passage of the bill would not influence his thinking.

- Sinema, in an interview with WaPo, noted Biden's spending plan differs from the blueprint that Biden had worked out with centrists weeks earlier, but she did not say what, if anything, she might change. She also reiterated she is worried about inflation and that new tax hikes could harm businesses still struggling in wake of the pandemic, adding she doesn’t think the solution is always more federal spending.

* * *

Update (0715ET): House Minority Leader Kevin McCarthy delayed the passage of President Joe Biden’s social spending package after embarking on an hours-long floor speech that lambasted the bill and Democrats for an array of issues.

The speech began as the House concluded debate on the sweeping budget Thursday night and proceeded to so-called “magic minutes,” which allow three members - the speaker, majority leader and minority leader - to speak for unlimited amounts of time.

McCarthy ended his speech at 5:11 a.m. Friday - eight hours and 33 minutes later.

“It’s okay. I’ll be here a long time,” McCarthy responded over two hours in, looking at Democrats.

“I think I’m upsetting other people on the other side of the aisle by telling them what’s in the bill. They just yelled at me that they’re leaving.”

Speaker Pelosi was indeed none too happy about McCarthy's record-breaking address, posting a statement in real-time during his speech, titled "McCarthy Needs a Reality Check" called the speech a "temper tantrum" full of "unhinged claims." It included a list of rebuttals to McCarthy.

"House Democrats are preparing to pass landmark legislation to lower costs, fight inflation and make big corporations and the wealthiest pay their fair share," the statement said.

"But McCarthy is welcome to keep getting facts wrong on the House Floor."

After McCarthy had gone on for a few hours, Pelosi's office released another statement asking: "Is Kevin McCarthy OK?"

"We're glad we're not the only one who can't follow Minority Leader McCarthy's meandering rant that has nothing to do with the Build Back Better Act," it said.

Pelosi is likely also upset since McCarthy's speech beat the Speaker's own previous record speech which she set in 2018 with an eight-hour speech aimed at urging Republicans to vote on immigration legislation for "dreamers."

* * *

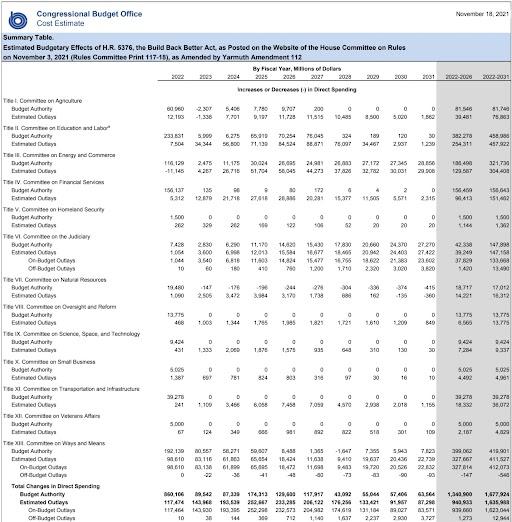

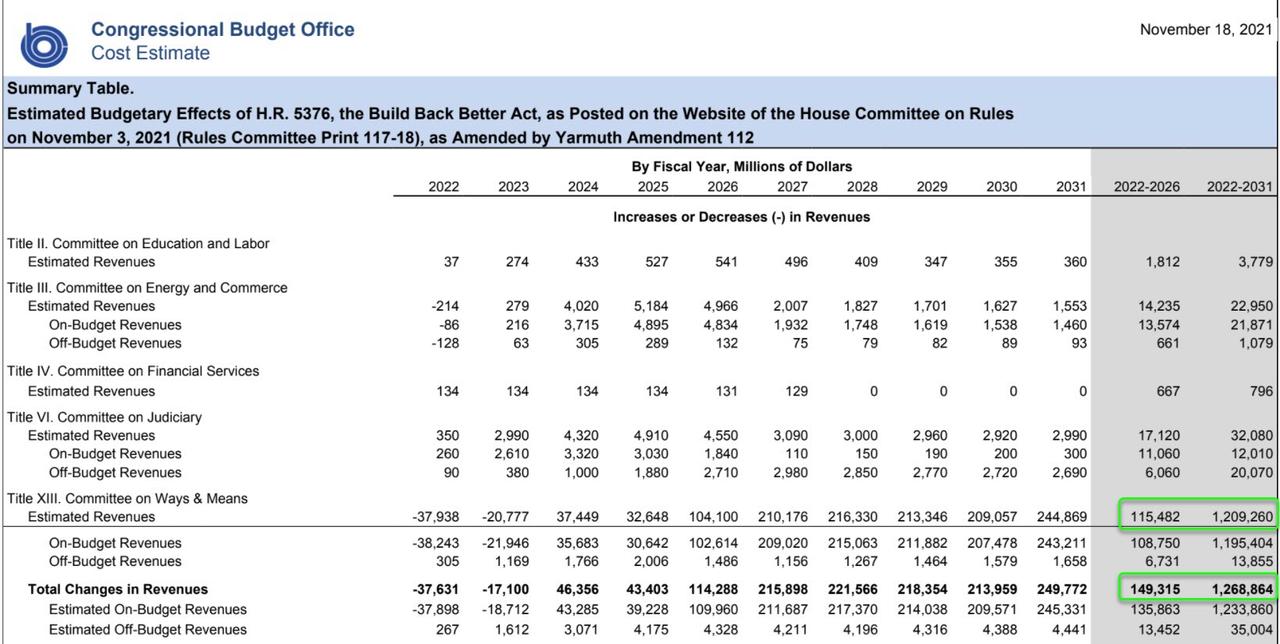

Update (2000ET): The House of Representatives is set to debate and then vote on President Biden's $1.75 trillion Build Back Better Act tonight, just hours after the Congressional Budget Office found that it will add more than $350 billion to the budget deficit - a determination which contradicts the White House's longstanding claim that the bill is 'paid for.'

The CBO found that the draft legislation contains $1.636 trillion in spending, and $1.269 trillion in revenue over 10 years, adding $367 billion to the US deficit over that period.

House speaker Nancy Pelosi sent a letter to fellow Democrats on Thursday advising them that they would be receiving an "updated chart from the White House, reflecting the revised numbers" from the CBO, adding that a vote would take place Thursday night "so that we can pass this legislation and achieve President Biden’s vision to Build Back Better!"

Of course, BBB passing the house was more or less a foregone conclusion given its broad support in the chamber. If House Republicans are united in opposition, Democrats can afford to lose three votes and still pass the bill.

What’s in Build Back Better for health care

— Dan Diamond (@ddiamond) November 18, 2021

- Capping insulin at $35/month

- Capping seniors’ out-of-pocket drug spending at $2,000/yr

- Medicare drug-price negotiations

- Expanding Medicare to cover hearing benefits

- Boosting ACA subsidies

- Closing Medicaid gap in 12 states https://t.co/QpWyrZA2oi

The big question now is whether moderate Senate Democrats Joe Manchin (WV) and Kyrsten Sinema (AZ) will support it. The (more) fiscally conservative Democrats will make their decision as Republicans hammer the bill for increasing the national debt, as well as its potential to intensify inflation, hinder job growth, and increase government dependency.

A key reason the CBO finds the bill does not pay for itself involves estimates of how much increased tax collection can result from expanding the Internal Revenue Service’s budget. While the White House has projected that increasing the number of enforcement agents at the Internal Revenue Service would yield $400 billion in higher revenue, the CBO does not agree. -Bloomberg

Critics also point to the fact that without sunset provisions, the bill would have actually exceeded $4 trillion, including tax credits for children and low-income workers which will be extended for one year.

And while it will likely pass the House tonight, the final bill is almost certain to be whittled down in the Senate, where Democrats are at the mercy of Manchin and Sinema, who have previously objected to how aspects of the legislation will be funded.

* * *

Just as the House Rules Committee cleared Biden's Build Back Better bill for debate by the full House with first votes on the bill set as early as 19:15EST (with Senator Manchin commenting earlier that he has not decided on whether to vote to proceed to the Build Back Better Bill), moments ago the CBO finally released its score of Biden's bill and, to nobody's surprise, it finds that contrary to what the Democrats asserted (and then un-asserted), that the bill would not fully pay for itself.

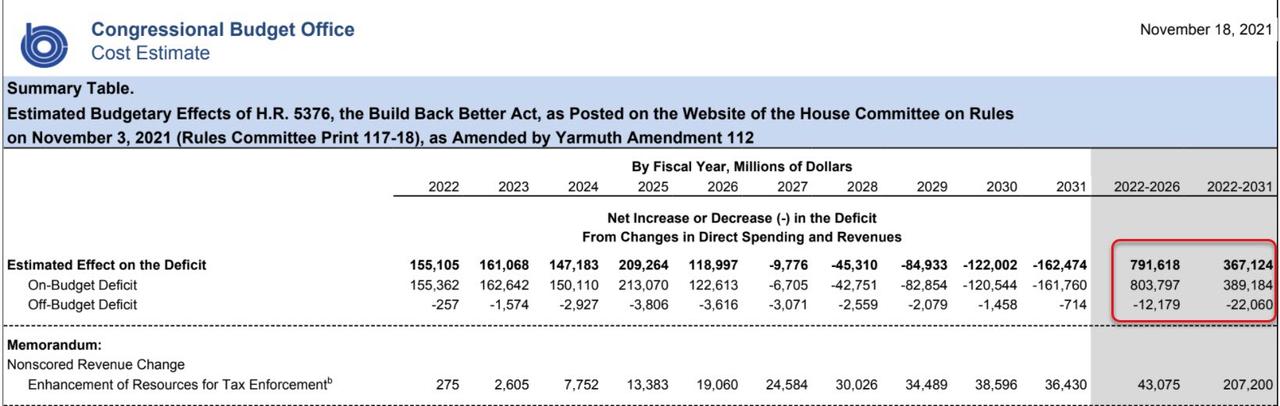

Instead, the CBO estimates that enacting this legislation would result in a net increase in the deficit totaling $367 billion over the 2022-2031 period, as a result of an additional $1.636 trillion in additional spending...

... offset by just $1.269 trillion in revenue (which however the CBO notes does not count any additional revenue that may be generated by additional funding for tax enforcement).

Worse, over just the next five years, the deficit grows by $792 billion, a number which somehow declines to $367 billion over the next decade, which comes as a result of a massive surge in revenues generated from Ways and Means, which magically surges from just $115BN over the next five years to a whopping $1.2 trillion over the next decade.

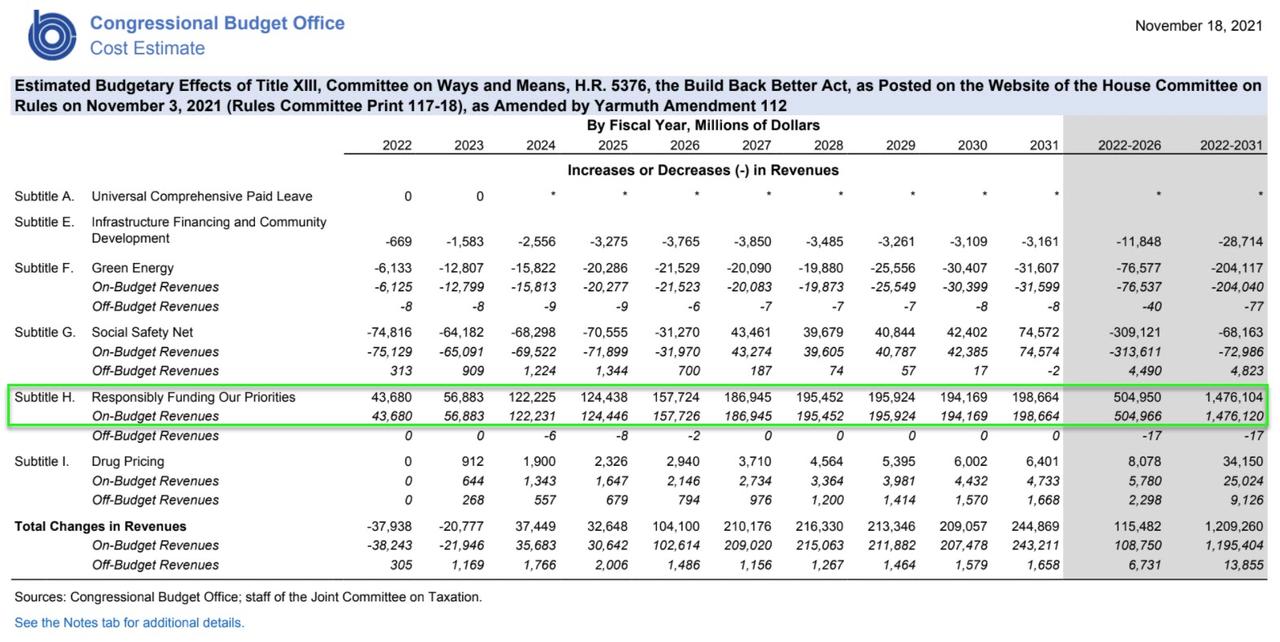

The massive surge in revenues from Ways and Means comes almost entirely from one section: "Responsibly Funding Our Priorities" (which conjures up an additional $1 trillion of revenues from 2026-2031, dramatically easing the 'cost' of the bill)...

That "Responsibly Funding Our Priorities" Section can be read in full here (Spoiler Alert - that's where all the Tax Reform gotchas are).

As Mike Shedlock notes, the 10-year lie is that Progressives say the front-loaded benefits will expire. Meanwhile they pledge to do everything in their power to ensure they don't.

History shows that government entitlement programs only get bigger, they don't expire.

Nor did the CBO look at ancillary costs such as inflation.

Earlier in the week, the Biden administration began preparing lawmakers for a 'disappointing estimate,' and told them to "disregard" the assessment according to the New York Times.

Hilariously, at just the same time as the CBO revised its long-awaited score, Janet Yellen - knowing how ugly it would look when the CBO scored that the Democrats lied - issued a statement saying that “the combination of CBO’s scores over the last week, the Joint Committee on Taxation estimates, and Treasury analysis, make it clear that Build Back Better is fully paid for, and in fact will reduce our nation’s debt over time by generating more than $2 trillion through reforms that ask the wealthiest Americans and large corporations to pay their fair share."

The wildcard? Yellen's estimate that the IRS will recoup "at least $400 billion in additional revenue" from high-earners to plug the hole.

A particularly salient aspect of the revenue raised by the legislation is a historic investment in the IRS to crack down on high-earners who avoid paying the taxes that they owe, which Treasury estimates would generate at least $400 billion in additional revenue.

The CBO somewhat agrees with this hypothetical wildcard which can not be modeled out and instead has to be taken as faith, which is why the CBO did not account for it, but it does say that its deficit estimates do not account for the $207 billion in IRS "savings", meaning CBO's effective estimate is $160 billion in new deficits.

Of course, in the end all of this is just optics and the CBO score won't have any impact, with the Bill sure to pass the House and then it will be up to the moderate Democrats in the Senate to determine if it becomes law.

Now let's see what moderate Senate Democrats Joe Manchin and Kyrsten Sinema have to say about it.

Government

Low Iron Levels In Blood Could Trigger Long COVID: Study

Low Iron Levels In Blood Could Trigger Long COVID: Study

Authored by Amie Dahnke via The Epoch Times (emphasis ours),

People with inadequate…

Share this:

Authored by Amie Dahnke via The Epoch Times (emphasis ours),

People with inadequate iron levels in their blood due to a COVID-19 infection could be at greater risk of long COVID.

A new study indicates that problems with iron levels in the bloodstream likely trigger chronic inflammation and other conditions associated with the post-COVID phenomenon. The findings, published on March 1 in Nature Immunology, could offer new ways to treat or prevent the condition.

Long COVID Patients Have Low Iron Levels

Researchers at the University of Cambridge pinpointed low iron as a potential link to long-COVID symptoms thanks to a study they initiated shortly after the start of the pandemic. They recruited people who tested positive for the virus to provide blood samples for analysis over a year, which allowed the researchers to look for post-infection changes in the blood. The researchers looked at 214 samples and found that 45 percent of patients reported symptoms of long COVID that lasted between three and 10 months.

In analyzing the blood samples, the research team noticed that people experiencing long COVID had low iron levels, contributing to anemia and low red blood cell production, just two weeks after they were diagnosed with COVID-19. This was true for patients regardless of age, sex, or the initial severity of their infection.

According to one of the study co-authors, the removal of iron from the bloodstream is a natural process and defense mechanism of the body.

But it can jeopardize a person’s recovery.

“When the body has an infection, it responds by removing iron from the bloodstream. This protects us from potentially lethal bacteria that capture the iron in the bloodstream and grow rapidly. It’s an evolutionary response that redistributes iron in the body, and the blood plasma becomes an iron desert,” University of Oxford professor Hal Drakesmith said in a press release. “However, if this goes on for a long time, there is less iron for red blood cells, so oxygen is transported less efficiently affecting metabolism and energy production, and for white blood cells, which need iron to work properly. The protective mechanism ends up becoming a problem.”

The research team believes that consistently low iron levels could explain why individuals with long COVID continue to experience fatigue and difficulty exercising. As such, the researchers suggested iron supplementation to help regulate and prevent the often debilitating symptoms associated with long COVID.

“It isn’t necessarily the case that individuals don’t have enough iron in their body, it’s just that it’s trapped in the wrong place,” Aimee Hanson, a postdoctoral researcher at the University of Cambridge who worked on the study, said in the press release. “What we need is a way to remobilize the iron and pull it back into the bloodstream, where it becomes more useful to the red blood cells.”

The research team pointed out that iron supplementation isn’t always straightforward. Achieving the right level of iron varies from person to person. Too much iron can cause stomach issues, ranging from constipation, nausea, and abdominal pain to gastritis and gastric lesions.

1 in 5 Still Affected by Long COVID

COVID-19 has affected nearly 40 percent of Americans, with one in five of those still suffering from symptoms of long COVID, according to the U.S. Centers for Disease Control and Prevention (CDC). Long COVID is marked by health issues that continue at least four weeks after an individual was initially diagnosed with COVID-19. Symptoms can last for days, weeks, months, or years and may include fatigue, cough or chest pain, headache, brain fog, depression or anxiety, digestive issues, and joint or muscle pain.

Government

Walmart joins Costco in sharing key pricing news

The massive retailers have both shared information that some retailers keep very close to the vest.

Share this:

As we head toward a presidential election, the presumed candidates for both parties will look for issues that rally undecided voters.

The economy will be a key issue, with Democrats pointing to job creation and lowering prices while Republicans will cite the layoffs at Big Tech companies, high housing prices, and of course, sticky inflation.

The covid pandemic created a perfect storm for inflation and higher prices. It became harder to get many items because people getting sick slowed down, or even stopped, production at some factories.

Related: Popular mall retailer shuts down abruptly after bankruptcy filing

It was also a period where demand increased while shipping, trucking and delivery systems were all strained or thrown out of whack. The combination led to product shortages and higher prices.

You might have gone to the grocery store and not been able to buy your favorite paper towel brand or find toilet paper at all. That happened partly because of the supply chain and partly due to increased demand, but at the end of the day, it led to higher prices, which some consumers blamed on President Joe Biden's administration.

Biden, of course, was blamed for the price increases, but as inflation has dropped and grocery prices have fallen, few companies have been up front about it. That's probably not a political choice in most cases. Instead, some companies have chosen to lower prices more slowly than they raised them.

However, two major retailers, Walmart (WMT) and Costco, have been very honest about inflation. Walmart Chief Executive Doug McMillon's most recent comments validate what Biden's administration has been saying about the state of the economy. And they contrast with the economic picture being painted by Republicans who support their presumptive nominee, Donald Trump.

Image source: Joe Raedle/Getty Images

Walmart sees lower prices

McMillon does not talk about lower prices to make a political statement. He's communicating with customers and potential customers through the analysts who cover the company's quarterly-earnings calls.

During Walmart's fiscal-fourth-quarter-earnings call, McMillon was clear that prices are going down.

"I'm excited about the omnichannel net promoter score trends the team is driving. Across countries, we continue to see a customer that's resilient but looking for value. As always, we're working hard to deliver that for them, including through our rollbacks on food pricing in Walmart U.S. Those were up significantly in Q4 versus last year, following a big increase in Q3," he said.

He was specific about where the chain has seen prices go down.

"Our general merchandise prices are lower than a year ago and even two years ago in some categories, which means our customers are finding value in areas like apparel and hard lines," he said. "In food, prices are lower than a year ago in places like eggs, apples, and deli snacks, but higher in other places like asparagus and blackberries."

McMillon said that in other areas prices were still up but have been falling.

"Dry grocery and consumables categories like paper goods and cleaning supplies are up mid-single digits versus last year and high teens versus two years ago. Private-brand penetration is up in many of the countries where we operate, including the United States," he said.

Costco sees almost no inflation impact

McMillon avoided the word inflation in his comments. Costco (COST) Chief Financial Officer Richard Galanti, who steps down on March 15, has been very transparent on the topic.

The CFO commented on inflation during his company's fiscal-first-quarter-earnings call.

"Most recently, in the last fourth-quarter discussion, we had estimated that year-over-year inflation was in the 1% to 2% range. Our estimate for the quarter just ended, that inflation was in the 0% to 1% range," he said.

Galanti made clear that inflation (and even deflation) varied by category.

"A bigger deflation in some big and bulky items like furniture sets due to lower freight costs year over year, as well as on things like domestics, bulky lower-priced items, again, where the freight cost is significant. Some deflationary items were as much as 20% to 30% and, again, mostly freight-related," he added.

bankruptcy pandemic trumpGovernment

Walmart has really good news for shoppers (and Joe Biden)

The giant retailer joins Costco in making a statement that has political overtones, even if that’s not the intent.

Share this:

{kind=link}

{kind=link}

As we head toward a presidential election, the presumed candidates for both parties will look for issues that rally undecided voters.

The economy will be a key issue, with Democrats pointing to job creation and lowering prices while Republicans will cite the layoffs at Big Tech companies, high housing prices, and of course, sticky inflation.

The covid pandemic created a perfect storm for inflation and higher prices. It became harder to get many items because people getting sick slowed down, or even stopped, production at some factories.

Related: Popular mall retailer shuts down abruptly after bankruptcy filing

It was also a period where demand increased while shipping, trucking and delivery systems were all strained or thrown out of whack. The combination led to product shortages and higher prices.

You might have gone to the grocery store and not been able to buy your favorite paper towel brand or find toilet paper at all. That happened partly because of the supply chain and partly due to increased demand, but at the end of the day, it led to higher prices, which some consumers blamed on President Joe Biden's administration.

Biden, of course, was blamed for the price increases, but as inflation has dropped and grocery prices have fallen, few companies have been up front about it. That's probably not a political choice in most cases. Instead, some companies have chosen to lower prices more slowly than they raised them.

However, two major retailers, Walmart (WMT) and Costco, have been very honest about inflation. Walmart Chief Executive Doug McMillon's most recent comments validate what Biden's administration has been saying about the state of the economy. And they contrast with the economic picture being painted by Republicans who support their presumptive nominee, Donald Trump.

Image source: Joe Raedle/Getty Images

Walmart sees lower prices

McMillon does not talk about lower prices to make a political statement. He's communicating with customers and potential customers through the analysts who cover the company's quarterly-earnings calls.

During Walmart's fiscal-fourth-quarter-earnings call, McMillon was clear that prices are going down.

"I'm excited about the omnichannel net promoter score trends the team is driving. Across countries, we continue to see a customer that's resilient but looking for value. As always, we're working hard to deliver that for them, including through our rollbacks on food pricing in Walmart U.S. Those were up significantly in Q4 versus last year, following a big increase in Q3," he said.

He was specific about where the chain has seen prices go down.

"Our general merchandise prices are lower than a year ago and even two years ago in some categories, which means our customers are finding value in areas like apparel and hard lines," he said. "In food, prices are lower than a year ago in places like eggs, apples, and deli snacks, but higher in other places like asparagus and blackberries."

McMillon said that in other areas prices were still up but have been falling.

"Dry grocery and consumables categories like paper goods and cleaning supplies are up mid-single digits versus last year and high teens versus two years ago. Private-brand penetration is up in many of the countries where we operate, including the United States," he said.

Costco sees almost no inflation impact

McMillon avoided the word inflation in his comments. Costco (COST) Chief Financial Officer Richard Galanti, who steps down on March 15, has been very transparent on the topic.

The CFO commented on inflation during his company's fiscal-first-quarter-earnings call.

"Most recently, in the last fourth-quarter discussion, we had estimated that year-over-year inflation was in the 1% to 2% range. Our estimate for the quarter just ended, that inflation was in the 0% to 1% range," he said.

Galanti made clear that inflation (and even deflation) varied by category.

"A bigger deflation in some big and bulky items like furniture sets due to lower freight costs year over year, as well as on things like domestics, bulky lower-priced items, again, where the freight cost is significant. Some deflationary items were as much as 20% to 30% and, again, mostly freight-related," he added.

bankruptcy pandemic trump

When Military Rule Supplants Democracy

The Digest #187

Redefining Poverty: Towards a Transpartisan Approach

Students lose out as cities and states give billions in property tax breaks to businesses − draining school budgets and especially hurting the poorest students

Is the United States overestimating China’s power?

Biden to call for first-time homebuyer tax credit, construction of 2 million homes

GBPINR: Analysis and Projections for 2024

Low Iron Levels In Blood Could Trigger Long COVID: Study

Walmart has really good news for shoppers (and Joe Biden)

Housing Is Unaffordable. Dems Want To Make It Worse.

-

Uncategorized2 weeks ago

Uncategorized2 weeks agoAll Of The Elements Are In Place For An Economic Crisis Of Staggering Proportions

-

Uncategorized1 month ago

Uncategorized1 month agoCathie Wood sells a major tech stock (again)

-

Uncategorized3 weeks ago

Uncategorized3 weeks agoCalifornia Counties Could Be Forced To Pay $300 Million To Cover COVID-Era Program

-

Uncategorized2 weeks ago

Uncategorized2 weeks agoApparel Retailer Express Moving Toward Bankruptcy

-

Uncategorized3 weeks ago

Uncategorized3 weeks agoIndustrial Production Decreased 0.1% in January

-

International1 day ago

International1 day agoWalmart launches clever answer to Target’s new membership program

-

Uncategorized3 weeks ago

Uncategorized3 weeks agoRFK Jr: The Wuhan Cover-Up & The Rise Of The Biowarfare-Industrial Complex

-

Uncategorized3 weeks ago

Uncategorized3 weeks agoGOP Efforts To Shore Up Election Security In Swing States Face Challenges