Here Are The Two Things That Will Crush The Fed’s Hiking Plans

Here Are The Two Things That Will Crush The Fed’s Hiking Plans

During Powell confirmation hearing today, the Fed chair said something notable which explains the Fed’s aggressive tightening posture: "the economy no longer needs highly accommod

Share this:

During Powell confirmation hearing today, the Fed chair said something notable which explains the Fed's aggressive tightening posture: "the economy no longer needs highly accommodative policies" adding that "it is really time for us to move away from those emergency pandemic settings to a more normal level."

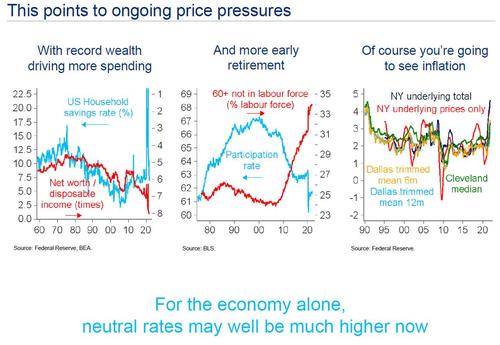

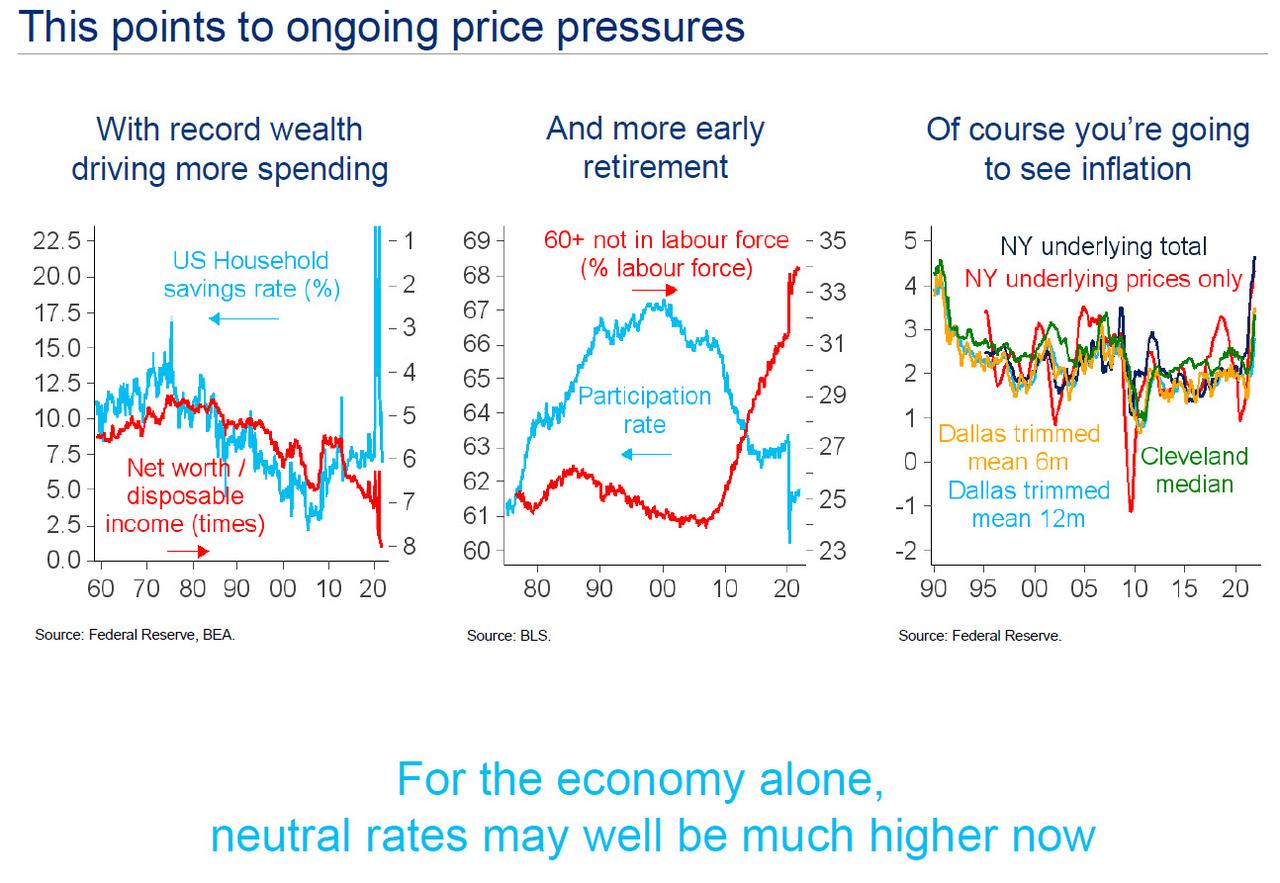

To be sure, this observation may actually be correct, and indeed in his latest presentation Citi's Matt King agreed, noting that "for the economy alone neutral rates may well be much higher now."

However, while the economy - with its rip-roaring inflation and ultra-tight labor market may indeed be able to absorb several rate hikes and even a material trim in the size of the Fed's balance sheet, the same can not be said about the market. Here we once again go to the latest Matt King slideshow, in which he warned that "neutral rates for markets likely well below neutral for the economy"...

... as "markets are much closer to late-cycle than the economy".

In other words, the Fed's tightening - whether in the form of rate hikes or balance sheet runoffs - while long overdue for the broader economy, will have dire effects on a market which is now used to the Fed's billions in monthly monetary injections; anything less, and certainly a drain of liquidity, and markets will unleash a major tantrum.

But while stocks may have no choice but to find what the strike price on the Fed's put is, which as Morgan Stanley's Michael Wilson recently said is about 20% below all time highs, some market elements are already signaling that not even the economy will be able to sustain just a handful of rate hikes.

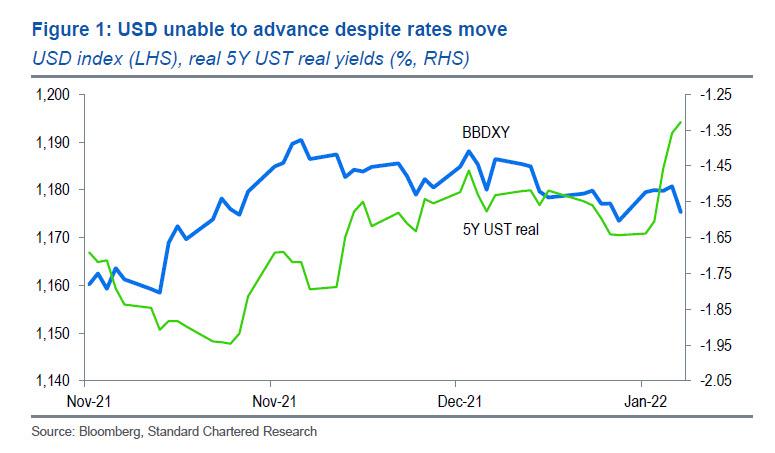

Take the dollar: as we noted earlier, a new conundrum has emerged in recent months, with the dollar now sliding despite "good" economic news such as rising real yields and falling equities.

And while we analyzed a recent note from Standard Chartered FX strategist Steven Englander looking at what may be causing this paradoxical USD response to an increasingly more hawkish Fed, the answer may be far simpler: FX traders are now pricing in the coming economic slowdown that will take place in the coming quarters as the Fed tightening further slows the stagflating economy, which if not contained in time, would lead to recession.

Or, even simpler, look at the December NFIB Small Business Optimism report which printed this morning, and which found that the share of small business expecting the economy to improve in the near future remains stuck at all time lows!

And when it comes to future of the economy, we will take the assessment of small businesses - those who actually transact every single day inside the US economy - over that of the Fed, which is a bunch of ideologically-driven economists who never exist their Marriner Eccles ivory tower, every day.

Which brings us to the gist of this article: what are the two things that will determine not only the end of the current market correction, but when the Fed will capitulate on its aggressive hawkish rhetoric, as it is forced to realize the US economy is slowing at an ever faster rate.In short, what are the two key things to watch to determine if economic growth is once again slowing.

For the answer we go to the latest Weekly Warm Up note from Morgan Stanley's Michael Wilson, whose persistent bearish bias appears to finally have been validated in recent days, and who writes that "with rates having adjusted, our focus now turns to growth".

As Wilson explains, "the Fire part of our narrative is in full gear with both nominal and real rates moving sharply higher so far this year. This is having a disproportionate impact on expensive growth stocks, as it should," but as the Morgan Stanley bear correctly stipulates, the real determinant of how long and deep this correction lasts will be growth.

And to assess where the US economy is in the all important business cycle, the Morgan Stanley chief strategist is laser focused on just two things: i) PMIs and ii) earnings revisions, both of which are heading lower in Wilson's view (who sees software as s a good case study and possible leading indicator in this regard for the broader market).

But let's step back for a second before we get to the meat of the argument, and instead let's take a look at some of the recent market context where, as noted above, just the threats of the Fed's liftoff and/or runoff have already wreaked havoc.

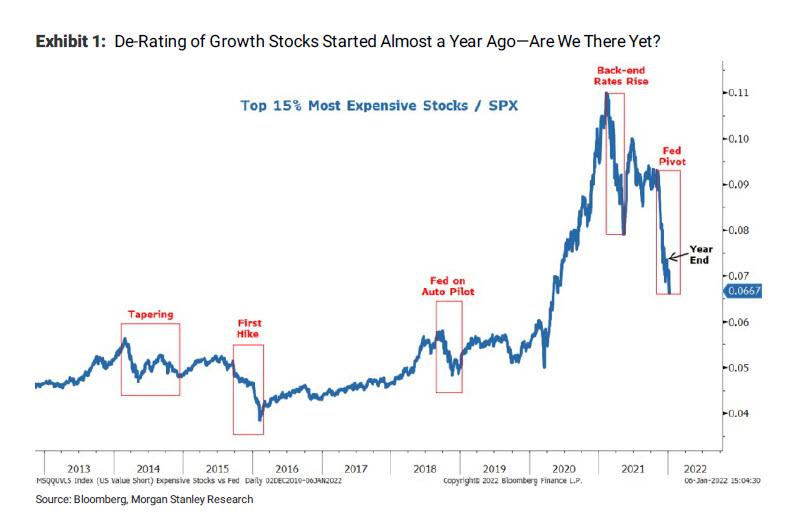

Summarizing the recent market situation, Wilson writes that 2022 is "off to a blazing start" with some of the biggest rotations ever witnessed at the beginning of the year, although in reality "much of this rotation in the equity markets began back in November with the Fed's more aggressive pivot on tapering and rate hikes. More specifically, and as shown below, the most expensive stocks were down almost 30 percent in the last 2 months of 2021. Year to date, this cohort is down another 10%, prompting the number one question Morgan Stanley's clients ask "is it over yet?"

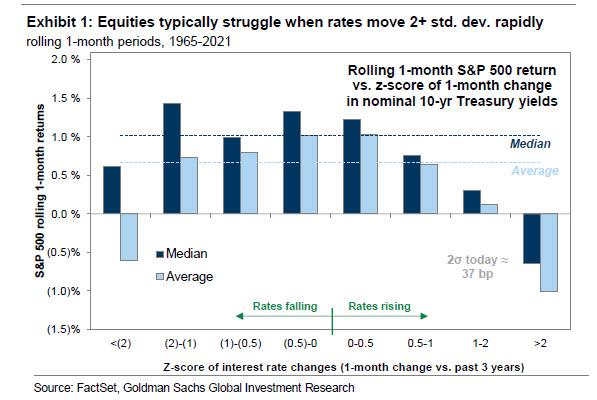

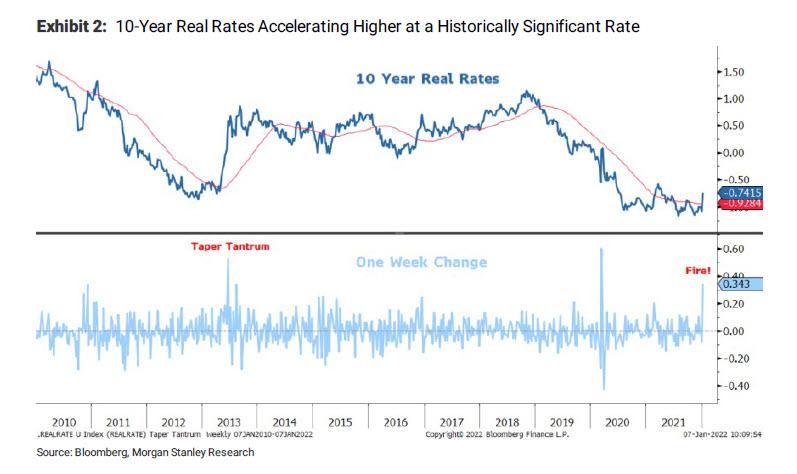

In response to this question, the equity strategist writes that what's changed since the turning of the calendar year "is the move in back end rates— both nominal and real. In fact, the move in 10-year real rates is one of the sharpest on record and harkens back to the original taper tantrum in 2013." Indeed, even Goldman over the weekend pointed out that while the absolute move in yields is hardly jarring, the speed with which yields have spiked is the kind of two-sigma event that sends stock lower in the ensuing weeks.

Wilson then notes that there is little doubt that such a move is garnering the attention of investors even though it's something equity markets have been thinking about for months. Indeed, if one looks again at the de-rating chart above, it's easy to see that the equity market has been discounting this inevitable rise in real rates for months. This fits Wilson's infamous "Fire" narrative, as well as his view that "the equity market is smart enough to know that the rates market has been influenced by QE, and therefore using the stated rate structure for one's discount rate would be a mistake for any longer term valuation assessment."

The obvious question to ask then is why is the rates market suddenly waking up to the reality of inflation and the Fed's response to it. After all, this has been telegraphed for months. Morgan Stanley thinks this has to do with several technical support mechanisms that are now being lifted:

- First, the Fed itself likely increased its liquidity provisions at year end to deal with the typical constraints in the banking system at this time of the year.

- Second, many macro speculators and trading desks likely shut down their books in December despite most views that long duration rates should be higher.

This combination has now reversed and ignited what seems like an inevitable move that many risky assets have been discounting ahead of time. So based on the move in 2013, Wilson predicts that "real rates still have further to run, potentially much further". Referencing Morgan Stanley's rates strategists, he believes that real rates are headed back toward 50bps which is another 25bps higher (Goldman's own forecast is for -0.70% real yields so a bit lower). Wilson notes that "real rates are unreasonably negative given very strong real GDP growth. Therefore, the Fed is absolutely correct to be trying to get them higher. It's also why tapering may not be tightening for the economy even though it is the epitome of tightening financial conditions for markets. Of course, the speed of this move is likely as important as the magnitude."

But while the market "Fire" is already raging, the good news (for the bulls) is that "winter is coming", or in other words the economic slowdown that inevitably accompanies all rate hikes by the Fed and which allows the Fed to resume its generous liquidity which in turn sends all risk assets soaring again.

This is the part which you should focus on even if you skip everything else in this post.

As Wilson explains, with the first part of his Fire and Ice narrative in full gear, it is time to turn our attention to the Ice. As already noted, growth is slowing and while most appreciate this dynamic, there is a lot of debate as to how much it will slow and whether it will matter for stocks. To be sure, growth is likely to remain positive (absent major shocks) but for some companies that remains to be seen given how difficult the comparisons are vs. last year especially in 1H 2022.

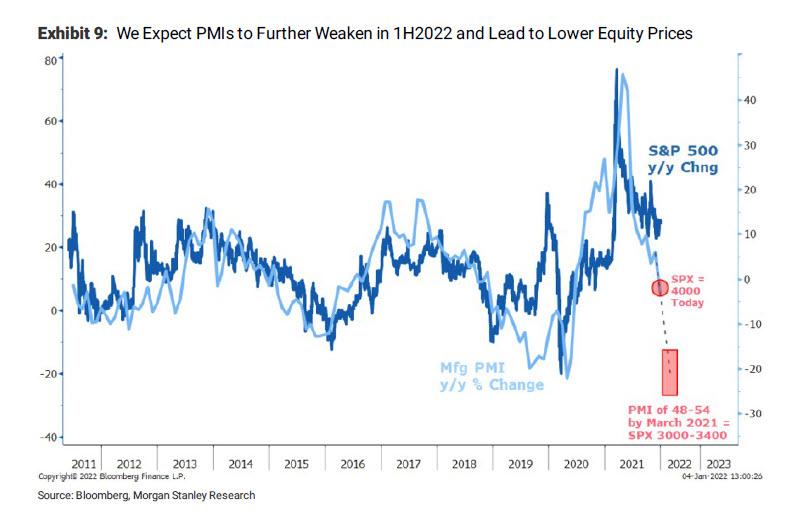

Here, as the title suggests, Morgan Stanley is focused on two metrics in particular as key drivers of stocks—PMIs and earnings revisions.

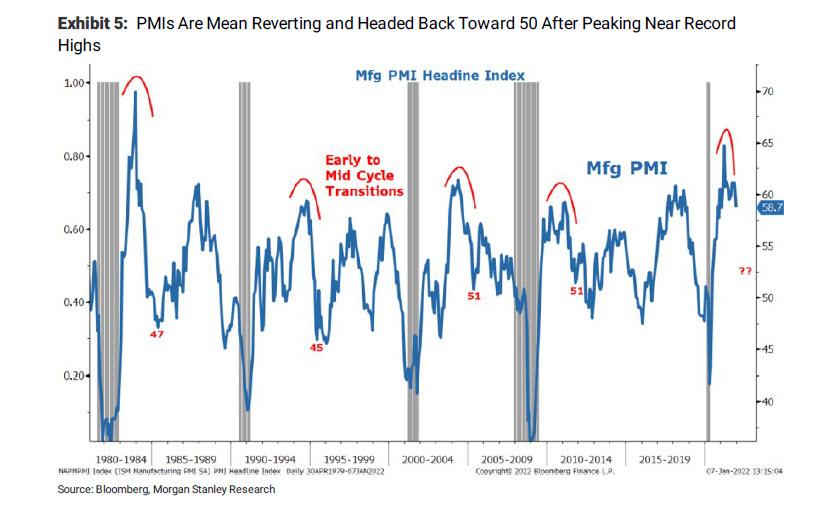

1. PMI

First on PMIs, both the manufacturing and services headline indices reached cycle highs and topped in 2021. Manufacturing PMIs peaked in the spring, while Services has more recently from an all time record high of 70. Given this survey is an oscillating/diffusion index, it typically returns toward 50 after the initial surge following a recession. This time will be no different, and it looks like we are headed there now. Wilson's guess is that by the spring of this year, we will see a Mfg PMI in the low 50s, if not slightly worse given how high it got this time—every action entails a comparable reaction.

In addition to the normal mean reversion we typically get in PMIs at this stage of the recovery, Wilson is also looking at other indicators that suggest "this reversion is imminent and could be sharper than normal."

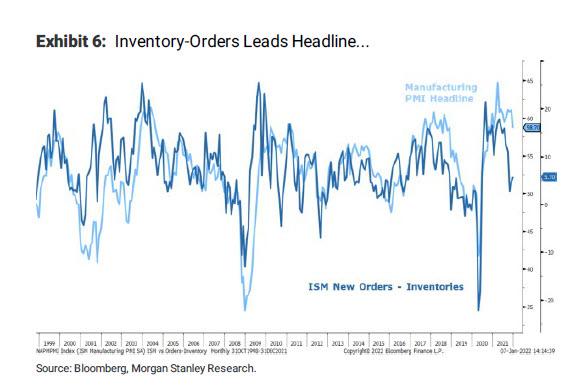

- First, limited supply has been one of the major constraints to growth for the past 6 months. Some of this is due to real supply chain issues and shortages but most of it is due to the excessive level of demand that was created by the extraordinary fiscal stimulus. As noted over the past few months, there have been more anecdotes about improving supply (although little actual results as even Powell noted during his testimony today). While this will help companies meet some of the extraordinary demand they haven't been able to fulfill, it may also lead to less tightness and therefore worse pricing and even cancellation of some of the double orders that make up a good part of the demand companies are seeing. On this score, the inventory and orders sub components suggest this is exactly the risk for the headline index. As inventories catch up to orders, the overall strength of the orders will likely fade.

- Second, the internal weakness in the market has been extraordinary. From weak breadth to extreme leadership in quality stocks, a deteriorating economic and earnings situation that is likely worse than most investors expect is being depicted within market internals—i.e., PMIs, economic and earnings growth will decelerate further than investors expect during the first half of 2022...the Ice part of Wilson's narrative. In fact, according to the MS strategist, some of the extraordinary price damage we are seeing beneath the surface of the index is foreshadowing this likely disappointment

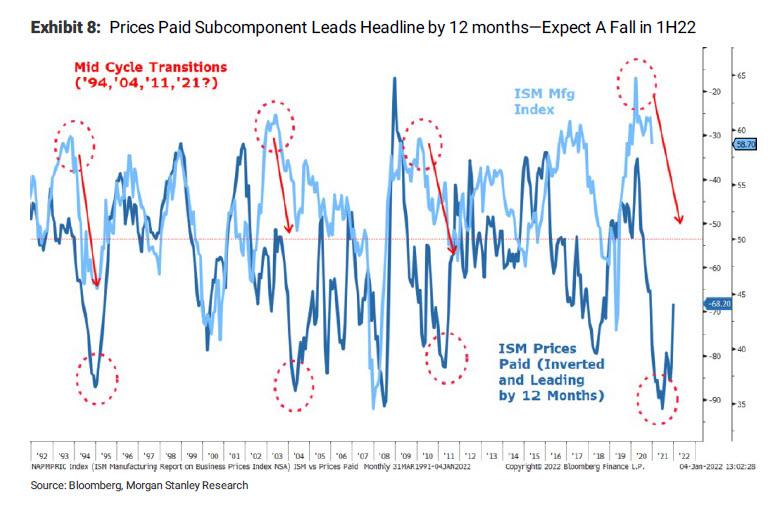

Another subcomponent of the PMI surveys that has significant signaling power is prices paid which tends to lead the headline index by approximately 12 months. It also fits Morgan Stanley's mid-cycle transition narrative nicely but has yet to fully play out. Similar to the charts above, the record increase in prices paid suggests the reversion to the mean for the headline PMI index should be imminent and sharper than normal.

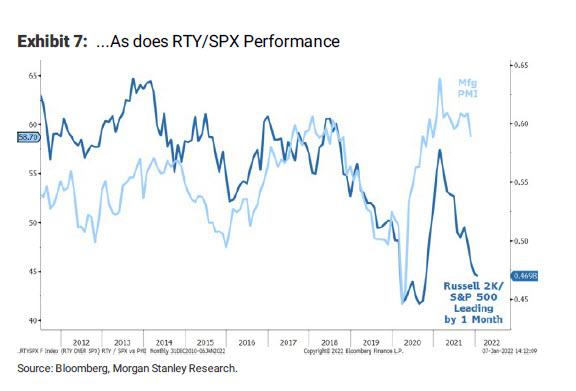

From a market standpoint, this is important because as Wilson notes, manufacturing PMIs tend to predict equity risk premiums (higher PMIs = lower ERPs), and is one of the reasons why the y/y change in PMIs lines up so well with the y/y change in the S&P 500

However - for now - the S&P 500 is still diverging from the deceleration we have already seen in the Mfg PMI to date. So if Wilson is right about PMIs falling further over the next few months, stocks still have material downside before this correction is over. This is very much in line with his outlook that tightening financial conditions with decelerating growth leads to falling valuations, particularly when the starting point is so high. Of course, it also leads to Fed panic and an even more aggressive stimulus down the line.

The good news, according to Michael Wilson, is that a good chunk of the de-rating has already happened at the individual stock level, even if the de-rating hasn't yet begun for the broader index. And while the equity strategist admits that he has been wrong (for now) at how well the index has held up in the face of so much damage to other asset prices and other mounting evidence (largely the results of an extremely narrow market leadership group in the face of the FAAMGs), this relationship with the PMI appears to be a smoking gun if it starts to fall more meaningfully.

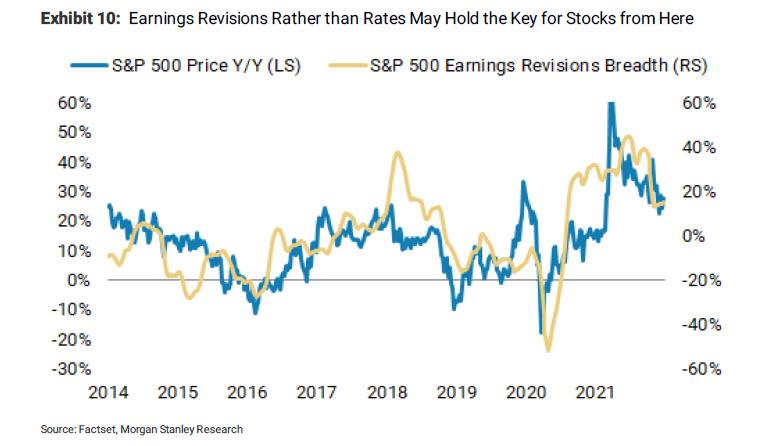

2. Earnings Revisions Breadth.

In addition to PMIs, the 2nd key signal Wilson also tracks is earnings revision breadth closely as a gauge of growth acceleration/ deceleration. It also has a high positive correlation vs. stock prices. In this case, the S&P 500 is trading in line with the current earnings revision breadth. While Morgan Stanley's work suggests the risk is to the downside for earnings revision breadth, it bears close watching as a possible offset to falling PMIs. In this regard, earnings revisions and PMIs will be more important than the direction of interest rates from here.

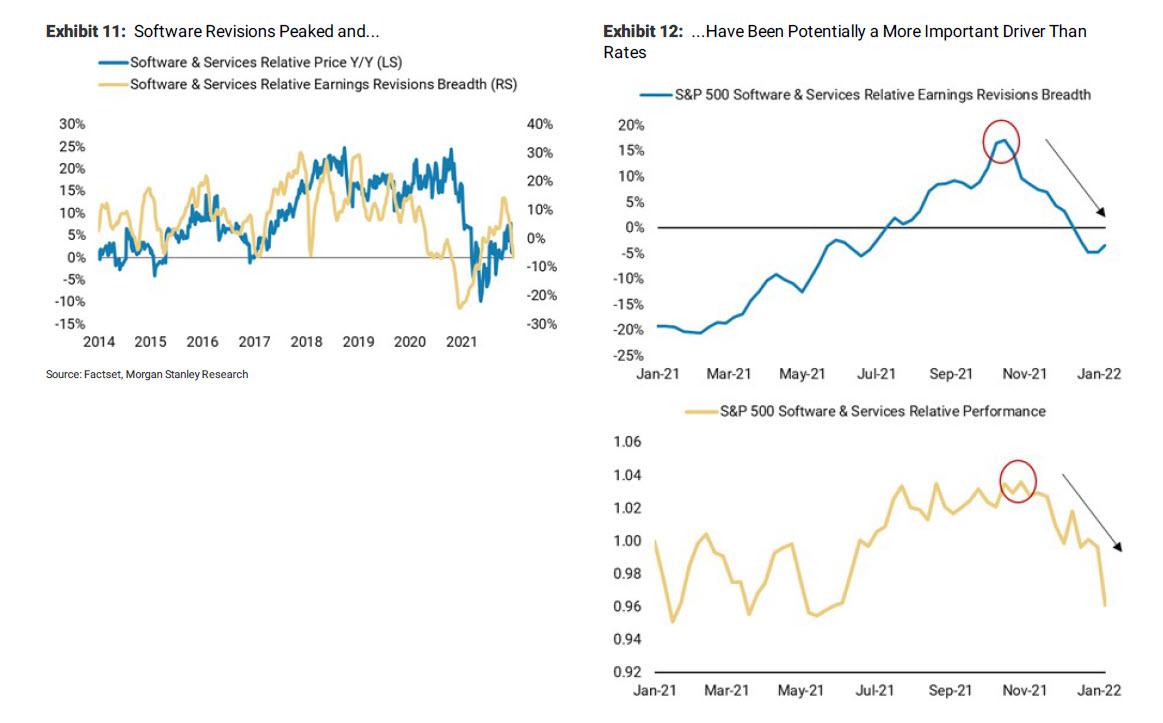

As an aside, Wilson brings readers' attention to what's been going on with Software and Services earnings revisions recently. Relative earnings revisions for the sector peaked in late October and have fallen decisively ever since. This coincided with the relative underperformance of the sector and may explain its underperformance even more so than the recent rise in rates. In other words, "Software stocks are simply reacting to what are deteriorating earnings revisions, at least relative to the S&P 500" and until this reverses, software as an overall cohort should continue to underperform, particularly if rates are still headed higher. Conversely, it does look like relative revisions are trying to bottom so if this can fully reverse during 4Q earnings season, so should the stocks, at least on a relative basis assuming rates stabilize, too. At this stage, Wilson says he would not recommend investors try to be too early here given how extreme valuations and positioning remain for the sector.

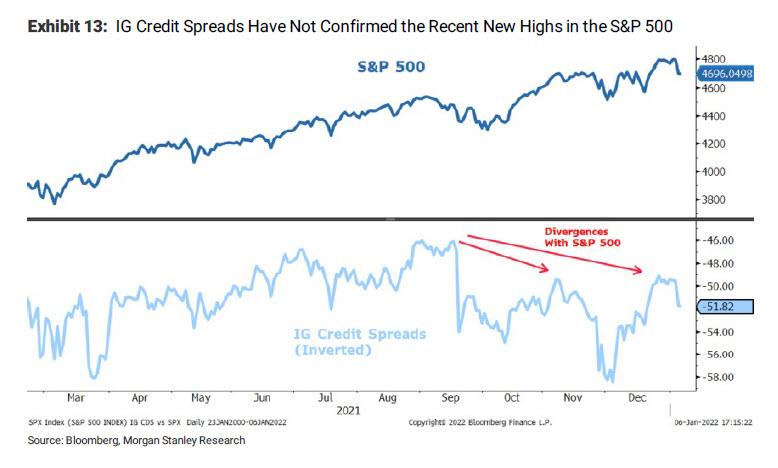

One final, and ominous, observation from Wilson which suggests the S&P 500 may finally be ready to catch up to the weak breadth under the surface is the recent divergence with IG credit spreads. For most of 2020-21, credit led the rally in stocks, as it typically does coming out of a recession. However, as shown below, "on the last two highs made by the S&P 500 in November and then December, IG credit spreads did not confirm them with new tights." Given the importance of credit spreads to equity valuations via the risk premium channel, Morgan Stanley's chief equity strategist would simply chalk this up as yet another thing to watch for the all clear sign that this correction is over, or that it is about to get much worse... and culminate with another Fed panic.

Uncategorized

Key shipping company files for Chapter 11 bankruptcy

The Illinois-based general freight trucking company filed for Chapter 11 bankruptcy to reorganize.

Share this:

The U.S. trucking industry has had a difficult beginning of the year for 2024 with several logistics companies filing for bankruptcy to seek either a Chapter 7 liquidation or Chapter 11 reorganization.

The Covid-19 pandemic caused a lot of supply chain issues for logistics companies and also created a shortage of truck drivers as many left the business for other occupations. Shipping companies, in the meantime, have had extreme difficulty recruiting new drivers for thousands of unfilled jobs.

Related: Tesla rival’s filing reveals Chapter 11 bankruptcy is possible

Freight forwarder company Boateng Logistics joined a growing list of shipping companies that permanently shuttered their businesses as the firm on Feb. 22 filed for Chapter 7 bankruptcy with plans to liquidate.

The Carlsbad, Calif., logistics company filed its petition in the U.S. Bankruptcy Court for the Southern District of California listing assets up to $50,000 and and $1 million to $10 million in liabilities. Court papers said it owed millions of dollars in liabilities to trucking, logistics and factoring companies. The company filed bankruptcy before any creditors could take legal action.

Lawsuits force companies to liquidate in bankruptcy

Lawsuits, however, can force companies to file bankruptcy, which was the case for J.J. & Sons Logistics of Clint, Texas, which on Jan. 22 filed for Chapter 7 liquidation in the U.S. Bankruptcy Court for the Western District of Texas. The company filed bankruptcy four days before the scheduled start of a trial for a wrongful death lawsuit filed by the family of a former company truck driver who had died from drowning in 2016.

California-based logistics company Wise Choice Trans Corp. shut down operations and filed for Chapter 7 liquidation on Jan. 4 in the U.S. Bankruptcy Court for the Northern District of California, listing $1 million to $10 million in assets and liabilities.

The Hayward, Calif., third-party logistics company, founded in 2009, provided final mile, less-than-truckload and full truckload services, as well as warehouse and fulfillment services in the San Francisco Bay Area.

The Chapter 7 filing also implemented an automatic stay against all legal proceedings, as the company listed its involvement in four legal actions that were ongoing or concluded. Court papers reportedly did not list amounts for damages.

In some cases, debtors don't have to take a drastic action, such as a liquidation, and can instead file a Chapter 11 reorganization.

Shutterstock

Nationwide Cargo seeks to reorganize its business

Nationwide Cargo Inc., a general freight trucking company that also hauls fresh produce and meat, filed for Chapter 11 bankruptcy protection in the U.S. Bankruptcy Court for the Northern District of Illinois with plans to reorganize its business.

The East Dundee, Ill., shipping company listed $1 million to $10 million in assets and $10 million to $50 million in liabilities in its petition and said funds will not be available to pay unsecured creditors. The company operates with 183 trucks and 171 drivers, FreightWaves reported.

Nationwide Cargo's three largest secured creditors in the petition were Equify Financial LLC (owed about $3.5 million,) Commercial Credit Group (owed about $1.8 million) and Continental Bank NA (owed about $676,000.)

The shipping company reported gross revenue of about $34 million in 2022 and about $40 million in 2023. From Jan. 1 until its petition date, the company generated $9.3 million in gross revenue.

Related: Veteran fund manager picks favorite stocks for 2024

bankruptcy pandemic covid-19 stocksUncategorized

Key shipping company files Chapter 11 bankruptcy

The Illinois-based general freight trucking company filed for Chapter 11 bankruptcy to reorganize.

Share this:

The U.S. trucking industry has had a difficult beginning of the year for 2024 with several logistics companies filing for bankruptcy to seek either a Chapter 7 liquidation or Chapter 11 reorganization.

The Covid-19 pandemic caused a lot of supply chain issues for logistics companies and also created a shortage of truck drivers as many left the business for other occupations. Shipping companies, in the meantime, have had extreme difficulty recruiting new drivers for thousands of unfilled jobs.

Related: Tesla rival’s filing reveals Chapter 11 bankruptcy is possible

Freight forwarder company Boateng Logistics joined a growing list of shipping companies that permanently shuttered their businesses as the firm on Feb. 22 filed for Chapter 7 bankruptcy with plans to liquidate.

The Carlsbad, Calif., logistics company filed its petition in the U.S. Bankruptcy Court for the Southern District of California listing assets up to $50,000 and and $1 million to $10 million in liabilities. Court papers said it owed millions of dollars in liabilities to trucking, logistics and factoring companies. The company filed bankruptcy before any creditors could take legal action.

Lawsuits force companies to liquidate in bankruptcy

Lawsuits, however, can force companies to file bankruptcy, which was the case for J.J. & Sons Logistics of Clint, Texas, which on Jan. 22 filed for Chapter 7 liquidation in the U.S. Bankruptcy Court for the Western District of Texas. The company filed bankruptcy four days before the scheduled start of a trial for a wrongful death lawsuit filed by the family of a former company truck driver who had died from drowning in 2016.

California-based logistics company Wise Choice Trans Corp. shut down operations and filed for Chapter 7 liquidation on Jan. 4 in the U.S. Bankruptcy Court for the Northern District of California, listing $1 million to $10 million in assets and liabilities.

The Hayward, Calif., third-party logistics company, founded in 2009, provided final mile, less-than-truckload and full truckload services, as well as warehouse and fulfillment services in the San Francisco Bay Area.

The Chapter 7 filing also implemented an automatic stay against all legal proceedings, as the company listed its involvement in four legal actions that were ongoing or concluded. Court papers reportedly did not list amounts for damages.

In some cases, debtors don't have to take a drastic action, such as a liquidation, and can instead file a Chapter 11 reorganization.

Shutterstock

Nationwide Cargo seeks to reorganize its business

Nationwide Cargo Inc., a general freight trucking company that also hauls fresh produce and meat, filed for Chapter 11 bankruptcy protection in the U.S. Bankruptcy Court for the Northern District of Illinois with plans to reorganize its business.

The East Dundee, Ill., shipping company listed $1 million to $10 million in assets and $10 million to $50 million in liabilities in its petition and said funds will not be available to pay unsecured creditors. The company operates with 183 trucks and 171 drivers, FreightWaves reported.

Nationwide Cargo's three largest secured creditors in the petition were Equify Financial LLC (owed about $3.5 million,) Commercial Credit Group (owed about $1.8 million) and Continental Bank NA (owed about $676,000.)

The shipping company reported gross revenue of about $34 million in 2022 and about $40 million in 2023. From Jan. 1 until its petition date, the company generated $9.3 million in gross revenue.

Related: Veteran fund manager picks favorite stocks for 2024

bankruptcy pandemic covid-19 stocksUncategorized

Tight inventory and frustrated buyers challenge agents in Virginia

With inventory a little more than half of what it was pre-pandemic, agents are struggling to find homes for clients in Virginia.

Share this:

{kind=link}

No matter where you are in the state, real estate agents in Virginia are facing low inventory conditions that are creating frustrating scenarios for their buyers.

“I think people are getting used to the interest rates where they are now, but there is just a huge lack of inventory,” said Chelsea Newcomb, a RE/MAX Realty Specialists agent based in Charlottesville. “I have buyers that are looking, but to find a house that you love enough to pay a high price for — and to be at over a 6.5% interest rate — it’s just a little bit harder to find something.”

Newcomb said that interest rates and higher prices, which have risen by more than $100,000 since March 2020, according to data from Altos Research, have caused her clients to be pickier when selecting a home.

“When rates and prices were lower, people were more willing to compromise,” Newcomb said.

Out in Wise, Virginia, near the westernmost tip of the state, RE/MAX Cavaliers agent Brett Tiller and his clients are also struggling to find suitable properties.

“The thing that really stands out, especially compared to two years ago, is the lack of quality listings,” Tiller said. “The slightly more upscale single-family listings for move-up buyers with children looking for their forever home just aren’t coming on the market right now, and demand is still very high.”

Statewide, Virginia had a 90-day average of 8,068 active single-family listings as of March 8, 2024, down from 14,471 single-family listings in early March 2020 at the onset of the COVID-19 pandemic, according to Altos Research. That represents a decrease of 44%.

In Newcomb’s base metro area of Charlottesville, there were an average of only 277 active single-family listings during the same recent 90-day period, compared to 892 at the onset of the pandemic. In Wise County, there were only 56 listings.

Due to the demand from move-up buyers in Tiller’s area, the average days on market for homes with a median price of roughly $190,000 was just 17 days as of early March 2024.

“For the right home, which is rare to find right now, we are still seeing multiple offers,” Tiller said. “The demand is the same right now as it was during the heart of the pandemic.”

According to Tiller, the tight inventory has caused homebuyers to spend up to six months searching for their new property, roughly double the time it took prior to the pandemic.

For Matt Salway in the Virginia Beach metro area, the tight inventory conditions are creating a rather hot market.

“Depending on where you are in the area, your listing could have 15 offers in two days,” the agent for Iron Valley Real Estate Hampton Roads | Virginia Beach said. “It has been crazy competition for most of Virginia Beach, and Norfolk is pretty hot too, especially for anything under $400,000.”

According to Altos Research, the Virginia Beach-Norfolk-Newport News housing market had a seven-day average Market Action Index score of 52.44 as of March 14, making it the seventh hottest housing market in the country. Altos considers any Market Action Index score above 30 to be indicative of a seller’s market.

Further up the coastline on the vacation destination of Chincoteague Island, Long & Foster agent Meghan O. Clarkson is also seeing a decent amount of competition despite higher prices and interest rates.

“People are taking their time to actually come see things now instead of buying site unseen, and occasionally we see some seller concessions, but the traffic and the demand is still there; you might just work a little longer with people because we don’t have anything for sale,” Clarkson said.

“I’m busy and constantly have appointments, but the underlying frenzy from the height of the pandemic has gone away, but I think it is because we have just gotten used to it.”

While much of the demand that Clarkson’s market faces is for vacation homes and from retirees looking for a scenic spot to retire, a large portion of the demand in Salway’s market comes from military personnel and civilians working under government contracts.

“We have over a dozen military bases here, plus a bunch of shipyards, so the closer you get to all of those bases, the easier it is to sell a home and the faster the sale happens,” Salway said.

Due to this, Salway said that existing-home inventory typically does not come on the market unless an employment contract ends or the owner is reassigned to a different base, which is currently contributing to the tight inventory situation in his market.

Things are a bit different for Tiller and Newcomb, who are seeing a decent number of buyers from other, more expensive parts of the state.

“One of the crazy things about Louisa and Goochland, which are kind of like suburbs on the western side of Richmond, is that they are growing like crazy,” Newcomb said. “A lot of people are coming in from Northern Virginia because they can work remotely now.”

With a Market Action Index score of 50, it is easy to see why people are leaving the Washington-Arlington-Alexandria market for the Charlottesville market, which has an index score of 41.

In addition, the 90-day average median list price in Charlottesville is $585,000 compared to $729,900 in the D.C. area, which Newcomb said is also luring many Virginia homebuyers to move further south.

“They are very accustomed to higher prices, so they are super impressed with the prices we offer here in the central Virginia area,” Newcomb said.

For local buyers, Newcomb said this means they are frequently being outbid or outpriced.

“A couple who is local to the area and has been here their whole life, they are just now starting to get their mind wrapped around the fact that you can’t get a house for $200,000 anymore,” Newcomb said.

As the year heads closer to spring, triggering the start of the prime homebuying season, agents in Virginia feel optimistic about the market.

“We are seeing seasonal trends like we did up through 2019,” Clarkson said. “The market kind of soft launched around President’s Day and it is still building, but I expect it to pick right back up and be in full swing by Easter like it always used to.”

But while they are confident in demand, questions still remain about whether there will be enough inventory to support even more homebuyers entering the market.

“I have a lot of buyers starting to come off the sidelines, but in my office, I also have a lot of people who are going to list their house in the next two to three weeks now that the weather is starting to break,” Newcomb said. “I think we are going to have a good spring and summer.”

real estate housing market pandemic covid-19 interest rates

IFM’s Hat Trick and Reflections On Option-To-Buy M&A

Q4 Update: Delinquencies, Foreclosures and REO

Net Zero, The Digital Panopticon, & The Future Of Food

Pharma industry reputation remains steady at a ‘new normal’ after Covid, Harris Poll finds

These Cities Have The Highest (And Lowest) Share Of Unaffordable Neighborhoods In 2024

For-profit nursing homes are cutting corners on safety and draining resources with financial shenanigans − especially at midsize chains that dodge public scrutiny

Trump nearly derailed democracy once − here’s what to watch out for in reelection campaign

Part 1: Current State of the Housing Market; Overview for mid-March 2024

Tight inventory and frustrated buyers challenge agents in Virginia

The Question You Should Ask Whenever You’re Wrong

-

Uncategorized3 weeks ago

Uncategorized3 weeks agoAll Of The Elements Are In Place For An Economic Crisis Of Staggering Proportions

-

International7 days ago

International7 days agoEyePoint poaches medical chief from Apellis; Sandoz CFO, longtime BioNTech exec to retire

-

Uncategorized4 weeks ago

Uncategorized4 weeks agoCalifornia Counties Could Be Forced To Pay $300 Million To Cover COVID-Era Program

-

Uncategorized3 weeks ago

Uncategorized3 weeks agoApparel Retailer Express Moving Toward Bankruptcy

-

Uncategorized4 weeks ago

Uncategorized4 weeks agoIndustrial Production Decreased 0.1% in January

-

International7 days ago

International7 days agoWalmart launches clever answer to Target’s new membership program

-

Uncategorized4 weeks ago

Uncategorized4 weeks agoRFK Jr: The Wuhan Cover-Up & The Rise Of The Biowarfare-Industrial Complex

-

Uncategorized3 weeks ago

Uncategorized3 weeks agoGOP Efforts To Shore Up Election Security In Swing States Face Challenges