Goldman Sachs: There’s an Opportunity Brewing in These 3 Stocks

Goldman Sachs: There’s an Opportunity Brewing in These 3 Stocks

Share this:

The COVID-19 pandemic has decimated the U.S. economy, yet the stock market is alive and well. Against the backdrop of a recession, the market actually had its strongest quarter in over 20 years, with the S&P 500 notching its largest quarterly gain since the last quarter of 1998, surging 20%. As for the NASDAQ, it climbed 31% higher during the quarter, marking its best quarterly performance since Q4 1999.

While certainly volatile, the quarter saw investors take an optimistic approach due to reopening efforts and unprecedented stimulus packages. That being said, going forward into Q3, plenty of uncertainty is lingering over Wall Street. So, how are investors supposed to lock in on compelling plays? The Street’s pros can provide some much-needed inspiration, namely those from investment firm Goldman Sachs.

Taking all of this into consideration, we used TipRanks’ database to learn more about three stocks backed by Goldman Sachs. As it turns out, the firm’s analysts projecting more than 30% upside potential for each. The rest of the Street is on the same page, with each ticker earning a “Strong Buy” consensus rating.

Myovant Sciences (MYOV)

Combining purpose-driven science, empowering medicines and transformative advocacy, Myovant Sciences wants to change the treatment landscape for both women and men. On the heels of its recent data readout, Goldman Sachs is even more optimistic about this healthcare name.

Covering this stock for the firm, five-star analyst Paul Choi tells clients that a key component of his bullish thesis is its relugolix asset. MYOV recently published positive Phase 3 data from its SPIRIT 1 study evaluating a once-daily relugolix combination therapy in women with endometriosis. This data supported the data from the previously reported SPIRIT 2 study.

Looking more closely at the results, 74.5% of patients saw a clinically meaningful reduction in dysmenorrhea compared to 26.9% of women in the placebo group, with the placebo-adjusted difference landing at 47.6%. Choi notes that Orilissa, the currently approved therapy for moderate to severe pain caused by endometriosis, demonstrated a 27%/21% (two trials) placebo-adjusted difference for its 150 mg once-daily therapy and a difference of 56%/50% for its 200 mg twice daily dose.

However, Orilissa can cause hypoestrogenic symptoms including hot flashes and loss of bone mineral density. Choi pointed out, “To avoid this, physicians can co-prescribe progestin and/or estradiol (add-back therapy). However, physicians emphasized that the once-daily, fixed-dose pill containing relugolix and add-back therapy would more readily convince a physician to prescribe it instead as the dosing schedule of Orilissa can be confusing, even for the prescriber.” MYOV’s candidate produced significantly fewer hot flashes, making Choi even more confident.

“In addition to the side effect profile and simple dosing schedule, physicians called out that many OBGYN offices were not equipped to handle the prior authorizations required for use. MYOV has focused efforts here to ensure that the proper tools are delivered to support prior auth requirements,” Choi added.

As updated data from the Phase 3 open-label extension study (LIBERTY) evaluating relugolix combination therapy in women with uterine fibroids (UF) was also promising, the deal is sealed for Choi.

To this end, the analyst maintained a Buy rating along with a $28 price target, suggesting 40% upside potential. (To watch Choi’s track record, click here)

Most other analysts also take a bullish approach. MYOV’s Strong Buy consensus rating breaks down into 3 Buys and only 1 Hold. Additionally, the $27.33 average price target puts the upside potential at 36%. (See MYOV stock analysis on TipRanks)

Southwest Airlines (LUV)

It’s no secret that COVID-19 has dealt the travel industry a swift blow. That being said, as passenger volumes have started to recover from the low point hit in April and market trends improve, Goldman Sachs is turning more bullish on Southwest Airlines.

Representing the firm, analyst Catherine O’Brien doesn’t dispute the fact that since LUV was added to the Americas Sell List on February 19, shares have plummeted 40% compared to the S&P 500’s 8% loss.

Singing a different tune now, O’Brien argues that given the airline industry’s focus on driving a rebound from the pandemic-induced lows, “Southwest’s primarily domestic network and industry leading balance sheet will drive a faster-than-industry recovery in profitability.”

Specifically looking at the latter, the analyst commented, “Additionally, given that liquidity remains a concern for the industry, balance sheet strength is currently of even more importance than it typically is, in our view.”

It should also be noted that LUV shares have historically experienced less turbulence than other players in the space. Therefore, while it boasts less upside potential than some of the firm’s other Buy-rated stocks, the level of upside here is enough to convince O’Brien to stand squarely in the bull camp.

As a result, O’Brien just gave LUV a thumbs up, upgrading her rating from Sell to Buy. If that wasn’t enough, the price target also gets a lift, from $35 to $47. Should the target be met, a twelve-month gain of 37% could be in store. (To watch O’Brien’s track record, click here)

In general, other analysts also like what they’re seeing. 11 Buys and 3 Holds add up to a Strong Buy consensus rating. Based on the $42.25 average price target, the upside potential comes in at 23%. (See LUV stock analysis on TipRanks)

ServiceNow (NOW)

As for Goldman Sachs’ third pick, ServiceNow offers software that delivers digital workflows designed to improve productivity. Given the strength of its technology, the firm sees big things in store for the tech company.

After looking at the space as a whole, four-star analyst Christopher Merwin goes so far as to deem NOW a best idea. Expounding on this, he wrote, “We believe the resiliency of the sector throughout COVID underscores the criticality of many software categories as businesses adjust for more distributed workforces and therefore require modernized cloud systems. With sector multiples at all-time highs, we favor stocks where we see compelling relative value.”

According to Merwin, NOW is set to be a “key beneficiary of digital transformations as enterprise customers increasingly focus on leveraging a select few strategic platforms that can deliver could-based solutions with ease, agility, and integrations.” Citing its product development, the analyst believes its approach is “best-in-class", with the company continuing to expand into new areas like financial operations management and DevOps.

“We believe this rich product roadmap, and ongoing momentum for ITSM, ITOM, HR, and CSM, will all help to sustain 28%-plus subscription revenue growth through FY22E,” Merwin commented. Going forward, its efforts to re-invest in new products in order to increase the addressable market and runway for growth should help NOW reach its long-term revenue target of $10 billion, in the analyst’s opinion.

Merwin added, “As software valuations continue to move higher across the space, we believe NOW stands out as an attractively valued stock - particularly on a growth-adjusted FCF, trading at 45.5x our CY21E FCF, relative to FCF growth expectations of 35%.”

It should come as no surprise, then, that Merwin stayed with the bulls. In addition to keeping a Buy rating on the stock, the analyst gave the price target a boost, from $403 to $538, which brings the upside potential to 33%. (To watch Merwin’s track record, click here)

Do other analysts agree with Merwin? As it turns out, most do. With 19 Buys and 4 Holds assigned in the last three months, the word on the Street is that NOW is a Strong Buy. However, at $396.32, the average price target does indicate 3% downside potential. (See ServiceNow stock-price forecast on TipRanks)

To find good ideas for stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a newly launched tool that unites all of TipRanks’ equity insights.

The post Goldman Sachs: There's an Opportunity Brewing in These 3 Stocks appeared first on TipRanks Financial Blog.

International

It’s Not Coercion If We Do It…

It’s Not Coercion If We Do It…

Authored by James Howard Kunstler via Kunstler.com,

Gags and Jibes

“My law firm is currently in court…

Share this:

Authored by James Howard Kunstler via Kunstler.com,

Gags and Jibes

“My law firm is currently in court fighting for free and fair elections in 52 cases across 19 states.”

- Marc Elias, DNC Lawfare Ninja, punking voters

Have you noticed how quickly our Ukraine problem went away, vanished, phhhhttttt? At least from the top of US news media websites.

The original idea, as cooked-up by departed State Department strategist Victoria Nuland, was to make Ukraine a problem for Russia, but instead we made it a problem for everybody else, especially ourselves in the USA, since it looked like an attempt to kick-start World War Three.

Now she is gone, but the plans she laid apparently live on.

Our Congress so far has resisted coughing up another $60-billion for the Ukraine project — most of it to be laundered through Raytheon (RTX), General Dynamics, and Lockheed Martin — so instead “Joe Biden” sent Ukraine’s President Zelensky a few reels of Laurel and Hardy movies. The result was last week’s prank: four groups of mixed Ukraine troops and mercenaries drawn from sundry NATO members snuck across the border into Russia’s Belgorod region to capture a nuclear weapon storage facility while Russia held its presidential election.

I suppose it looked good on the war-gaming screen.

Alas, the raid was a fiasco. Russian intel was on it like white-on-rice. The raiders met ferocious resistance and retreated into a Russian mine-field - this was the frontier, you understand, between Kharkov (Ukr) and Belgorod (Rus) - where they were annihilated. The Russian election concluded Sunday without further incident. V.V. Putin, running against three other candidates from fractional parties, won with 87 percent of the vote. He’s apparently quite popular.

“Joe Biden,” not so much here, where he is pretending to run for reelection with a party pretending to go along with the gag. Ukraine is lined up to become Afghanistan Two, another gross embarrassment for the US foreign policy establishment and “JB” personally. So, how long do you think V. Zelensky will be bopping around Kiev like Al Pacino in Scarface?

This time, poor beleaguered Ukraine won’t need America’s help plotting a coup. When that happens, as it must, since Mr. Z has nearly destroyed his country, and money from the USA for government salaries and pensions did not arrive on-time, there will be peace talks between his successors and Mr. Putin’s envoys. The optimum result for all concerned — including NATO, whether the alliance knows it or not — will be a demilitarized Ukraine, allowed to try being a nation again, though in a much-reduced condition than prior to its becoming a US bear-poking stick. It will be on a short leash within Russia’s sphere-of-influence, where it has, in fact, resided for centuries, and life will go on. Thus, has Russia at considerable cost, had to reestablish the status quo.

Meanwhile, Saturday night, “Joe Biden” turned up at the annual Gridiron dinner thrown by the White House [News] Correspondents’ Association, where he told the ballroom of Intel Community quislings:

“You make it possible for ordinary citizens to question authority without fear or intimidation.”

The dinner, you see, is traditionally a venue for jokes and jibes. So, this must have been a gag, right? Try to imagine The New York Times questioning authority. For instance, the authority of the DOJ, the FBI, the DHS, and the DC Federal District court. Instant hilarity, right?

As it happens, though, today, Monday, March 18, 2024, attorneys for the State of Missouri (and other parties) in a lawsuit against “Joe Biden” (and other parties) will argue in the Supreme Court that those government agencies above, plus the US State Department, with assistance from the White House (and most of the White House press corps, too), were busy for years trying to prevent ordinary citizens from questioning authority.

For instance, questioning the DOD’s Covid-19 prank, the CDC’s vaccination op, the DNC’s 2020 election fraud caper, the CIA’s Frankenstein experiments in Ukraine, the J6 “insurrection,” and sundry other trips laid on the ordinary citizens of the USA.

Specifically, Missouri v. Biden is about the government’s efforts to coerce social media into censoring any and all voices that question official dogma.

The case is about birthing the new concept - new to America, anyway - known as “misinformation” - that is, truth about what our government is doing that cannot be allowed to enter the public arena, making it very difficult for ordinary citizens to question authority.

The government will apparently argue that they were not coercing, they were just trying to persuade the social media execs to do this or that.

As The Epoch Times' Jacob Burg reported, the court appeared wary of arguments by the respondents that the White House is wholesale prevented under the Constitution from recommending to social media companies to remove posts it considered harmful, in cases where the suggestions themselves didn't cross the line into "coercion."

Deputy Solicitor General for the U.S. Brian Fletcher argued that the White House's communications with news media and social media companies regarding the content promoted on their platforms do not rise to the level of governmental “coercion,” which would have been prohibited under the Constitution.

Instead, the government was merely using its "bully pulpit" to "persuade" private parties, in this case social media companies, to do what they are "lawfully allowed to do,” he said.

Louisiana Solicitor General Benjamin Aguiñaga, representing the respondents, argued that the case demonstrates “unrelenting pressure by the government to coerce social media platforms to suppress the speech of millions of Americans.”

Mr. Aguiñaga argued that the government had no right to tell social media companies what content to carry. Its only remedy in the event of genuinely false or misleading content, he said, was to counter it by putting forward "true speech."

The attorney general took pointed questions from Liberal Justice Ketanji Brown Jackson about the extent to which the government can step in to take down certain potentially harmful content. Justice Jackson raised the hypothetical of a "teen challenge that involves teens jumping out of windows at increasing elevations," asking if it would be a problem if the government tried to suppress the publication of said challenge on social media. Mr. Aguiñaga replied that those facts were different from the present case.

Justice Ketanji Brown Jackson raised the opinion that some say “the government actually has a duty to take steps to protect the citizens of this country” when it comes to monitoring the speech that is promoted on online platforms.

“So can you help me because I'm really worried about that, because you've got the First Amendment operating in an environment of threatening circumstances from the government's perspective.

“The line is, does the government pursuant to the First Amendment have a compelling interest in doing things that result in restricting speech in this way?”

KBJ doubles down: “My biggest concern is that your view has the First Amendment hamstringing the government in significant ways.”

— System Update (@SystemUpdate_) March 18, 2024

That is, quite literally, the entire point of the First Amendment—of the entire Bill of Rights. pic.twitter.com/gWMCaHDG1WAttorneys General Liz Merrill of Louisiana and Andrew Bailey of Missouri both told The Epoch Times they felt positive about the case and how the justices reacted.

"I am cautiously optimistic that we will have a majority of the court that lands where I wholeheartedly believe they should land, and that is in favor of protecting speech," Ms. Merrill said.

Journalist Jim Hoft, a party listed in the case, said, "This has to be where they put a stop to this. The government shouldn't be doing this, especially when they're wrong, and pushing their own opinion, silencing dissenting voices. Of course, it's against the Constitution. It's a no-brainer."

In response to a question from Brett Kavanaugh, an associate justice of the Supreme Court, Louisiana Solicitor General Benjamin Aguiñaga said the "government is not helpless" when it comes to countering factually inaccurate speech.

Precedent before the court suggests the government can and should counter false speech with true speech, Mr. Aguiñaga said.

"Censorship has never been the default remedy for perceived First Amendment violation," Mr. Aguiñaga said.

Maybe one of the justices might ask how it came to be that a Chief Counsel of the FBI, James Baker, after a brief rest-stop at a DC think tank, happened to take the job as Chief Counsel at Twitter in 2020.

That was a mighty strange switcheroo, don’t you think?

And ordinary citizens were not generally informed of it until the fall of 2022, when Elon Musk bought Twitter and delved into its workings.

* * *

Support his blog by visiting Jim’s Patreon Page or Substack

Uncategorized

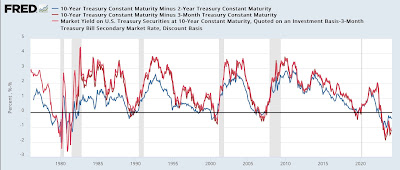

Manufacturing and construction vs. the still-inverted yield curve

– by New Deal democratProf. Menzie Chinn at Econbrowser makes the point that the yield curve is still inverted, and has not yet eclipsed the longest…

Share this:

- by New Deal democrat

Prof. Menzie Chinn at Econbrowser makes the point that the yield curve is still inverted, and has not yet eclipsed the longest previous time between onset of such an inversion and a recession. So he believes the threat of recession is still on the table.

Uncategorized

Half Of Downtown Pittsburgh Office Space Could Be Empty In 4 Years

Half Of Downtown Pittsburgh Office Space Could Be Empty In 4 Years

Authored by Mike Shedlock via MishTalk.com,

The CRE implosion is picking…

Share this:

{kind=link}

{kind=link}

Authored by Mike Shedlock via MishTalk.com,

The CRE implosion is picking up steam.

Check out the grim stats on Pittsburgh.

Unions are also a problem in Pittsburgh as they are in Illinois and California.

{kind=link}

Downtown Pittsburgh Implosion

The Post Gazette reports nearly half of Downtown Pittsburgh office space could be empty in 4 years.

Confidential real estate information obtained by the Pittsburgh Post-Gazette estimates that 17 buildings are in “significant distress” and another nine are in “pending distress,” meaning they are either approaching foreclosure or at risk of foreclosure. Those properties represent 63% of the Downtown office stock and account for $30.5 million in real estate taxes, according to the data.

It also calculates the current office vacancy rate at 27% when subleases are factored in — one of the highest in the country.

And with an additional three million square feet of unoccupied leased space becoming available over the next five years, the vacancy rate could soar to 46% by 2028, based on the data.

Property assessments on 10 buildings, including U.S. Steel Tower, PPG Place, and the Tower at PNC Plaza, have been slashed by $364.4 million for the 2023 tax year, as high vacancies drive down their income.

Another factor has been the steep drop — to 63.5% from 87.5% — in the common level ratio, the number used to compute taxable value in county assessment appeal hearings.

The assessment cuts have the potential to cost the city, the county, and the Pittsburgh schools nearly $8.4 million in tax refunds for that year alone. Downtown represents nearly 25% of the city’s overall tax base.

In response Pittsburgh City Councilman Bobby Wilson wants to remove a $250,000 limit on the amount of tax relief available to a building owner or developer as long as a project creates at least 50 full-time equivalent jobs.

It’s unclear if the proposal will be enough. Annual interest costs to borrow $1 million have soared from $32,500 at the start of the pandemic in 2020 to $85,000 on March 1. Local construction costs have increased by about 30% since 2019.

But the city is doomed if it does nothing. Aaron Stauber, president of Rugby Realty said it will probably empty out Gulf Tower and mothball it once all existing leases expire.

“It’s cheaper to just shut the lights off,” he said. “At some point, we would move on to greener pastures.”

Where’s There’s Smoke There’s Unions

In addition to the commercial real estate woes, the city is also wrestling with union contracts.

Please consider Sounding the alarm: Pittsburgh Controller’s letter should kick off fiscal soul-searching

It’s only March, and Pittsburgh’s 2024 house-of-cards operating budget is already falling down. That’s the clear implication of a letter sent by new City Controller Rachael Heisler to Mayor Ed Gainey and members of City Council on Wednesday afternoon.

The letter is a rare and welcome expression of urgency in a city government that has fallen in complacency — and is close to falling into fiscal disaster.

The approaching crisis was thrown into sharp relief this week, when City Council approved amendments to the operating budget accounting for a pricey new contract with the firefighters union. The Post-Gazette Editorial Board had predicted that this contract — plus two others yet to be announced and approved — would demonstrate the dishonesty of Mayor Ed Gainey’s budget, and that’s exactly what’s happening: The new contract is adding $11 million to the administration’s artificially low 5-year spending projections, bringing expected 2028 reserves to just barely the legal limit.

But there’s still two big contracts to go, with the EMS union and the Pittsburgh Joint Collective Bargaining Committee, which covers Public Works workers. Worse, there are tens — possibly hundreds — of millions in unrealistic revenues still on the books. On this, Ms. Heisler’s letter only scratched the surface.

Similarly, as we have observed, the budget’s real estate tax revenue projections are radically inconsistent with reality. Due to high vacancies and a sharp reduction in the common level ratio, a significant drop in revenues was predictable — but not reflected in the budget. Ms. Heisler’s estimate of a 20% drop in revenues from Downtown property, or $5.3 million a year, may even be optimistic: Other estimates peg the loss at twice that, or more.

Left unmentioned in the letter are massive property tax refunds the city will owe, as well as fanciful projections of interest income that are inconsistent with the dwindling reserves, and drawing-down of federal COVID relief funds, predicted in the budget itself. That’s another unrealistic $80 million over five years.

Pittsburgh exited Act 47 state oversight after nearly 15 years on Feb. 12, 2018, with a clean bill of fiscal health.

It has already ruined that bill of health.

Act 47 in Pittsburgh

Flashback February 21, 2018: Act 47 in Pittsburgh: What Was Accomplished?

Pittsburgh’s tax structure was a much-complained-about topic leading up to the Act 47 declaration. The year following Pittsburgh’s designation as financially distressed under Act 47 it levied taxes on real estate, real estate transfers, parking, earned income, business gross receipts (business privilege and mercantile), occupational privilege and amusements. The General Assembly enacted tax reforms in 2004 giving the city authority to levy a payroll preparation tax in exchange for the immediate elimination of the mercantile tax and the phase out of the business privilege tax. The tax reforms increased the amount of the occupational privilege tax from $10 to $52 (this is today known as the local services tax and all municipalities outside of Philadelphia levy it and could raise it thanks to the change for Pittsburgh).

The coordinators recommended an increase in the deed transfer tax, which occurred in late 2004 (it was just increased again by City Council) and in the real estate tax, which increased in 2015.

Legacy costs, principally debt and underfunded pensions, were the primary focus of the 2009 amended recovery plan. The city’s pension funded ratio has increased significantly from where it stood a decade ago, rising from the mid-30 percent range to over 60 percent at last measurement.

The obvious question? Will the city stick to the steps taken to improve financially and avoid slipping back into distressed status? If Pittsburgh once stood “on the precipice of full-blown crisis,” as described in the first recovery plan, hopefully it won’t return to that position.

The Obvious Question

I could have answered the 2018 obvious question with the obvious answer. Hell no.

No matter how much you raise taxes, it will never be enough because public unions will suck every penny and want more.

On top of union graft, and insanely woke policies in California, we have an additional huge problem.

Hybrid Work Leaves Offices Empty and Building Owners Reeling

Hybrid work has put office building owners in a bind and could pose a risk to banks. Landlords are now confronting the fact that some of their office buildings have become obsolete, if not worthless.

Meanwhile, in Illinois …

Chicago Teachers’ Union Seeks $50 Billion Despite $700 Million City Deficit

Please note the Chicago Teachers’ Union Seeks $50 Billion Despite $700 Million City Deficit

The CTU wants to raise taxes across the board, especially targeting real estate.

My suggestion, get the hell out...

Mistakes Were Made

Home buyers must now navigate higher mortgage rates and prices

Supreme Court Rules Public Officials May Block Their Constituents On Social Media

Manufacturing and construction vs. the still-inverted yield curve

Harvard Medical School Professor Was Fired Over Not Getting COVID Vaccine

You can strike gold and silver investment opportunities at Costco

Germany Is Running Out Of Money And Debt Levels Are Exploding, Finance Minister Warns

TikTok Ban Obscures Chinese Stock Gold Rush

Default: San Francisco Four Seasons Hotel Investors $3 Million Late On Loan As Foreclosure Looms

Correcting the Washington Post’s 11 Charts That Are Supposed to Tell Us How the Economy Changed Since Covid

-

Uncategorized4 weeks ago

Uncategorized4 weeks agoAll Of The Elements Are In Place For An Economic Crisis Of Staggering Proportions

-

Spread & Containment5 days ago

Spread & Containment5 days agoIFM’s Hat Trick and Reflections On Option-To-Buy M&A

-

International1 week ago

International1 week agoEyePoint poaches medical chief from Apellis; Sandoz CFO, longtime BioNTech exec to retire

-

Uncategorized1 month ago

Uncategorized1 month agoCalifornia Counties Could Be Forced To Pay $300 Million To Cover COVID-Era Program

-

Uncategorized3 weeks ago

Uncategorized3 weeks agoApparel Retailer Express Moving Toward Bankruptcy

-

Uncategorized1 month ago

Uncategorized1 month agoIndustrial Production Decreased 0.1% in January

-

International1 week ago

International1 week agoWalmart launches clever answer to Target’s new membership program

-

Uncategorized1 month ago

Uncategorized1 month agoRFK Jr: The Wuhan Cover-Up & The Rise Of The Biowarfare-Industrial Complex