Futures, Yields, Oil And Gold Slide As German Confidence Plummets To 2011 Lows, Euro Hits Parity

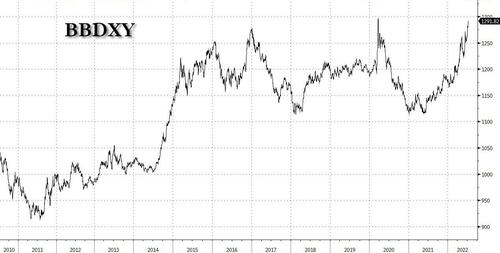

US index futures, global markets, Treasury yields, bitcoin and oil all fell on Tuesday as the dollar continued its relentless ascent to levels just shy of the March 2020 global crash record high...

... highlighting pervasive trader unease about the economic outlook as high inflation and a looming recession are set to unleash a catastrophic global recession coupled with a worldwide dollar shortage, now with the added boost of China’s renewed struggles with Covid. S&P and Nasdaq 100 emini futures dropped about 0.5% each having slumped as much as 0.9% earlier, as traders brace for an ugly Q2 earnings season which may provide clues on how companies are weathering inflation and recession concerns.

The US 10-year Treasury yield falls to about 2.91% amid a broad-based flight to safety; bonds also rallied in Europe. German bonds surged, sending the benchmark 10-year yield to the lowest since May, after data showed investor confidence plunged to a 2011 low.

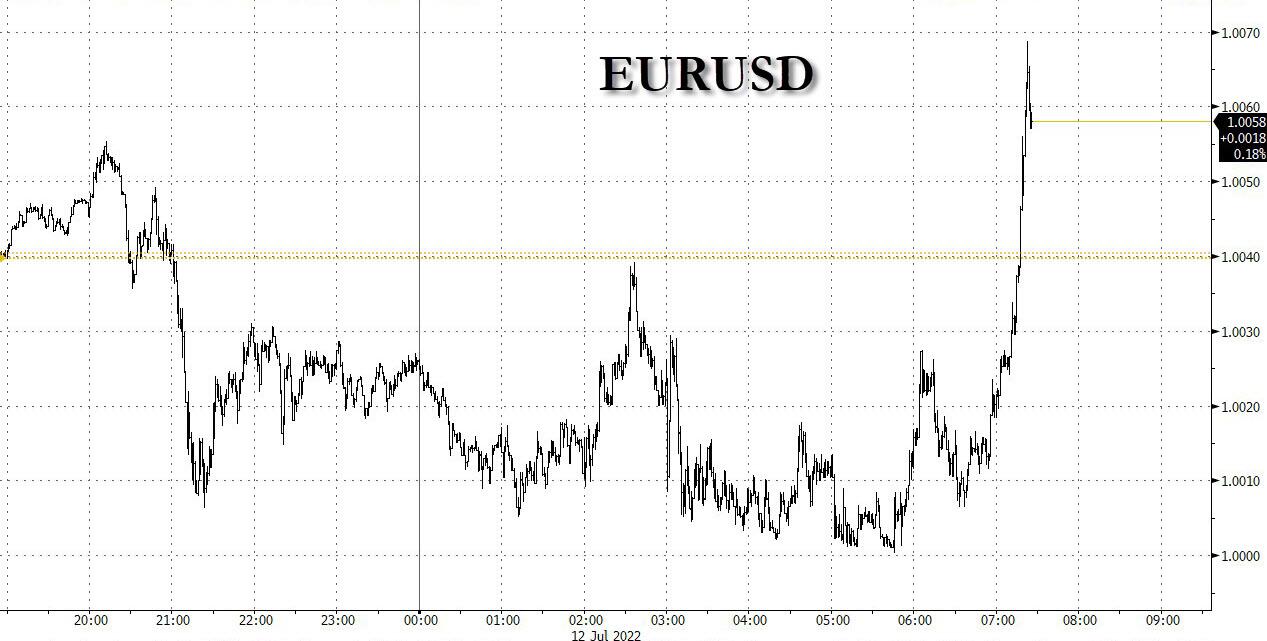

As shown above, the dollar rose just shy of record highs last seen at the height of the 2020 market panic over Covid and the yen strengthened, underlining investor caution. The euro meanwhile briefly touched parity (technically, it was 1.00003 but that's semantics for purists who have nothing better to do) hammered by the region’s energy crisis and acute recession fears.

Dollar strength will not only “affect this quarter’s earnings, but more likely it’s going to affect the revenue generation outlook for the next couple of quarters and that, I think, is a big problem,” Kimberly Forrest, founder and chief investment officer of Bokeh Capital Partners, said on Bloomberg Radio.

PepsiCo, one of the first major corporations to report, rose in premarket trading after lifting its revenue forecast. The soft-drinks maker said demand remained robust despite inflation, though it expected headwinds from the strong dollar. Bank stocks, meanwhile, were lower in premarket trading amid a broader slump in risk assets. Cryptocurrency stocks drop in premarket trading as Bitcoin drops below $20,000 in its fourth straight day of declines amid a stronger dollar. In corporate news, LoanDepot said it will cut about 2,000 additional staff by the end of the year. Here are the other notable premarket movers:

Gap (GPS US) shares fall 6.4% in premarket trading after the apparel retailer fired CEO Sonia Syngal and said it expects rising costs and deepening discounts to erase this quarter’s operating profit.

American Express (AXP US) shares are down 2.2% in premarket trading after Morgan Stanley cut the recommendation on the stock, as well as on Capital One (COF US), to equal- weight from overweight as inflation takes a larger share of household disposable incomes.

STORE Capital (STOR US) shares fall 3.3% in premarket trading after Morgan Stanley downgrades it to underweight from equal-weight and cuts National Retail Properties (NNN US) to equal-weight from overweight, saying that US triple net REITs could see a headwind from the rising cost of capital.

Ginkgo Bioworks (DNA US) shares are up 9% in premarket trading after exchange-traded funds managed by Cathie Wood’s Ark Investment Management bought 860,480 shares in the company.

Meanwhile, the latest Fed commentary highlighted both the central bank’s hawkishness and the risks that come with aggressive interest-rate hikes. Fed Bank of Atlanta President Raphael Bostic said the US economy can copewith higher interest rates and repeated his support for another jumbo move this month. Fed Bank of Kansas City President Esther George, who dissented last month against the central bank’s 75 basis-point rate increase, cautioned that rushing to tighten policy could backfire.

European bourses are also deep in the red. Euro Stoxx 50 falls 0.7% with the Stoxx Europe 600 sliding for a second day, though it pared the decline with utilities outperforming as EDF jumped after a report that the French government will pay a premium to take control of the electricity company. The DAX lags, dropping 0.8%. Banks, travel and autos are the worst performing sectors. German bonds surged, sending the benchmark 10-year yield to the lowest since May, after data showed investor confidence plunged to a level not seen since the sovereign debt crisis in 2011.

Asian stocks fell to a new two-year low as China’s technology shares continued to face selling pressure amid regulatory jitters and a resurgence of Covid cases in the nation. The MSCI Asia Pacific Index slipped as much as 1.5%, dragged by tech and consumer discretionary shares. The Hang Seng Tech Index fell 11% from a June high to enter a technical correction as regulatory fines for the country’s tech giants continued to damp sentiment.

In China, investors are concerned more Covid lockdowns may lie ahead as Beijing continues with a strategy of mass testing and mobility curbs. Chinese benchmarks took a hit from renewed lockdown fears from a fresh virus outbreak in Shanghai. Japan and Taiwan were among the region’s worst performing markets on lingering concerns of a global economic slowdown. Market participants are hoping that key US inflation data due Wednesday and China’s GDP figures on Friday will provide clues on the global economy’s direction. Asia’s stock benchmark has slumped 20% this year amid worries about higher interest rates and the prospect of an economic downturn. Investor sentiment continued to weaken in Asia despite remaining positive in China, said Olivier d’Assier, the head of APAC applied research at Qontigo. “Within an inflationary background, hopes of continued high profit margins in developed markets can only be balanced with fears of a margin squeeze among the developing world’s supply chain.”

In FX, the Bloomberg Dollar Spot Index rose a second day as the greenback was steady or higher against all of its Group-of-10 peers apart from the yen amid rising recession concerns. The euro fell to a low of 1.00003 per dollar but struggled to go below parity. Options traders are still preparing for life below this psychological support level. The pound lagged all of its Group-of-10 peers. UK retailers reported another drop in sales, while economists see the risk of a UK recession in the next 12 months at almost 50-50. Australian and New Zealand fell gradually. Iron ore prices sank to a seven- month low, with the demand outlook dimming on fears China may again impose strict Covid-19 curbs that hurt construction activity.

In rates, Treasuries were underpinned following gains for bunds and gilts after German ZEW expectations gauge dropped to -53.8 vs -40.5 estimate. Treasury yields richer by up to 7.5bp across intermediates, flattening 2s10s spread by 1.4bp on the day to -10.3bp, deepest inversion since 2007; German 10s outperform Treasuries by ~5bp, gilts by ~7bp. German 10-year yields dropped to lowest since May, dragging Treasury yields lower. German curve bull-flattens, richening 12-14bps across the back end. Gilts bull-steepen, with short-dated yields dropping over 15bps. Peripheral spreads widen to Germany with 10y BTP/Bund widening ~3bps to 199bps. In bond auctions we get a $33BN reopening of 10-year notes at 1pm ET follows good demand for Monday’s 3-year new issue, which stopped 0.5bp through. WI 10-year yield around 2.92% is ~11bp richer than June result, which tailed by 1.2bp.

Crude futures decline. WTI falls ~2.5% to trade near $101.60. Base metals are mixed; LME tin falls 3.1% while LME aluminum gains 0.3%. Spot gold is little changed at $1,735/oz. Spot silver loses 1.1% near $19. Bitcoin drops over 3.5% to trade back below $20,000.

Looking at the day ahead now, and data releases include the US NFIB small business optimism index for June. Central bank speakers include BoE Governor Bailey, the Fed’s Barkin and the ECB’s Villeroy. Finally, earnings releases today include PepsiCo.

Market Snapshot

S&P 500 futures down 0.6% to 3,835.50

STOXX Europe 600 down 0.4% to 413.46

MXAP down 1.3% to 154.65

MXAPJ down 1.3% to 508.44

Nikkei down 1.8% to 26,336.66

Topix down 1.6% to 1,883.30

Hang Seng Index down 1.3% to 20,844.74

Shanghai Composite down 1.0% to 3,281.47

Sensex down 0.6% to 54,067.35

Australia S&P/ASX 200 little changed at 6,606.28

Kospi down 1.0% to 2,317.76

German 10Y yield little changed at 1.16%

Euro down 0.3% to $1.0008

Brent Futures down 2.1% to $104.83/bbl

Gold spot up 0.2% to $1,736.88

U.S. Dollar Index up 0.43% to 108.48

Top Overnight News from Bloomnerg

Investor confidence in Germany’s economy slumped to the lowest since 2011 as the country faces the growing prospect of a recession and risks mount that it’s shut off from Russian energy supplies

US Treasury Secretary Janet Yellen agreed with her Japanese counterpart Tuesday that volatile exchange rates pose a risk, and pledged to consult and cooperate as appropriate

A global squeeze on energy supply that’s triggered crippling shortages and sent power and fuel prices surging may get worse, according to the head of the International Energy Agency

A more detailed look at global markets courtesy of Newsquawk

Asia-Pac stocks were mostly negative after the weak performance across global counterparts as China's COVID flare-up and Europe's energy concerns added to the headwinds for the growth outlook. ASX 200 bucked the trend with the index kept afloat by defensives although the upside was capped by weak consumer and business confidence data. Nikkei 225 underperformed as the Japanese currency attempted to compose itself from recent rapid depreciation and with automakers pressured after Toyota flagged a potential cut to its output plan citing a chip shortage and COVID impact. Hang Seng and Shanghai Comp. were lower amid the ongoing COVD concerns which overshadowed reports that China’s authorities will increase financial support for manufacturers, as well as the recent stronger than expected aggregate financing and loans data.

Top Asian News

China is to lockdown Wugang city in Henan for 3 days due to 1 COVID case, according to Bloomberg.

Japanese Finance Minister Suzuki said they will conduct necessary economic steps taking prices and economy into account, while he added that they are watching the FX market even more closely while working with the BoJ and will take necessary steps against the FX market with FX authorities from other nations, according to Reuters.

Japanese Finance Minister told US Treasury Secretary Yellen that Japan is concerned about the rapid JPY weakening recently; watching currency markets with a sense of urgency; agreed to continue consulting in foreign exchange.

European bourses are pressured in a broad China-COVID driven risk move, Euro Stoxx 50 -0.5%; alongside known concerns and a dismal ZEW. Stateside, futures are lower across the board with the NQ somewhat more choppy than peers amid pronounced rate activity this morning and on PEP earnings. Back to Europe, sectors are mixed and feature IT as the laggard while Energy is green despite benchmark pricing amid outperformance in EDF.

PepsiCo Inc (PEP) Q2 2022 (USD): EPS 1.86 (exp. 1.74), Revenue 20.2bln (exp. 19.51bln). FY Revenue view 82.7bln (exp. 82.72bln)

Top European News

UK's Heathrow airport is imposing a capacity cap of 100k departing passengers a day, until September 11th. Beleive further action is needed now; cap means some summer journeys will be rescheduled, relocated or cancelled. Asks airline partners to stop the sale of summer tickets in order to limit the passenger impact.

Former UK Chancellor Sunak confirmed his commitment to fiscal discipline and will stand firm on taxes until he has 'gripped inflation', according to FT.

German ZEW Economic Sentiment (Jul) -53.8 vs. Exp. -38.3 (Prev. -28.0); ZEW Survey Expectations (Jul) -51.1 (Prev. -28.0)

ZEW: current major concerns about energy supply, ECB's announced rate hikes, restrictions in China, led to a deterioration in the outlook; economic situation significantly more negative than in previous month, experts further lower their already unfavourable forecast for the next six months.

Fixed Income

Bonds breach recent resistance levels, with Bunds up to new July highs at 153.48 after a bleak German ZEW survey

Gilts back on the 116.00 handle from a 115.04 Liffe low awaiting more comments from BoE Governor Bailey and 10 year T-note towards top of 119-03/118-09+ range pre-USD 33bn refunding leg

DMO's 2032 tap well received and German Schatz covered, but results mixed overall

FX

Pound underperforms awaiting UK political developments as Labour Party prepares no-confidence motion against Tories; Cable on the cusp of 1.1800, while EUR/GBP rebounds over 0.8450.

Euro prods parity vs Dollar before and after dire German ZEW survey, while DXY breaches 108.500 amidst broad Buck gains.

Yen regroups as risk sentiment remains sour and yields retreat further, with Japan’s Finance Minister also raising concern about rapid decline, USD/JPY closer to 137.00 than 137.50+ top and Monday's 137.75 peak.

Loonie and Nokkie recoil alongside crude prices, but Kiwi holds up better than Aussie ahead of anticipated 50bp RBNZ rate hike on Wednesday, USD/CAD back up near 1.3050, EUR/NOK propped around 10.2600, NZD/USD holding just above 0.6100 and AUD/USD sub-0.6750.

Yuan breaks below recent range as China’s Covid situation continues to deteriorate - USD/CNH and USD/CNY probe 6.7500 and 6.7350 respectively.

Commodities

WTI and Brent have extended on APAC pressure as the demand-side of the equation remains sensitive to lockdowns with the OPEC MOMR and EIA STEO due.

Currently, benchmarks are in relative proximity to their respective USD 101.06/bbl and USD 104.35/bbl lows.

IEA's Birol said the world is in the midst of the first energy crisis and it has not seen the worst of the energy crisis, according to Bloomberg.

US senior official warned that a failure to implement a proposed price cap on Russian oil with the exemption of purchases below the cap, could see oil prices increase to around USD 140/bbl, while the official added that Treasury Secretary Yellen will speak to Japanese Finance Minister Suzuki on the proposed Russian oil price cap, according to Reuters.

US Department of Energy announced a contract for 14 companies to purchase crude oil from the SPR with deliveries to take place between August 16th to September 30th, according to Reuters.

China's NDRC says retail prices of gasoline and diesel will be cut by CNY 360/tonne and CNY 345/tonne respectively from July 13th.

US National Security Adviser Sullivan responded that there is a capacity for further steps that can be taken when questioned about oil output, according to Reuters.

Spot gold is relatively resilient despite broader price action, and the yellow metal is torn between COVID-driven haven allure and the USD’s ongoing advances.

US Event Calendar

06:00: June SMALL BUSINESS OPTIMISM, 89.5, est. 92.5, prior 93.1

Central Banks

12:30: Fed’s Barkin Discusses the ‘Recession Question’

Government:

President Biden will meet with Mexico President Andrés Manuel López Obrador at 11:15am ET

House Jan. 6 select committee will hold a hearing on the extremists involved in the assault at 1pm ET

DB's Jim Reid concludes the overnight wrap

It's so hot, even at 5am, that I have two fans pointing at me as I type this. Electric ones not two people that have kindly voted for me in the II survey. Never has a commute to the office and the lure of aircon been so alluring. When we renovated 3-4 years ago we considered having some aircon fitted but decided that given the cost we would forgo that for the couple of days a year where Britain sweltered. Given that this spell looks set to last a couple of weeks I may sleep in the office, especially as the kids have now broken up and are running riot at home.

The heat may have also tired markets out after a mini rally so far in July. The last 24 hours has seen sentiment become more gloomy once again as investors looked forward to multiple data releases and earnings reports this week that’ll set the stage for some important central bank meetings over the next couple of weeks. The US CPI report will be the main highlight tomorrow, but we shouldn’t forget the start of the Q2 earnings season either, which will shed some light on how corporates are faring as the market narrative has flirted with the view that the US economy might already be in a recession. One bit of “good” news yesterday was the NY Fed’s long-run consumer inflation expectations series which showed a decent dip and helped encourage a big rally in bonds as the tug of war in the asset class continues.

More on that later but equities didn’t get that memo as they lost ground on both sides of the Atlantic yesterday with the S&P 500 shedding -1.15% by the close of trade, in what looked like a classic risk off rotation, with only Utilities and Real Estate higher, and the latter only barely up (+0.01%). Tech stocks led the declines, with the NASDAQ down by -2.26% whilst the FANG+ index of megacap tech stocks saw an even larger -4.52% decline as all 10 companies in the index lost ground. Along with a sour risk day, mega-cap shares were probably sluggish following the news over the weekend that Elon Musk would be pulling out of his Twitter deal. Small-caps were another underperformer, with the Russell 2000 down -2.11%, whereas the Dow Jones experienced a more modest -0.52% loss. Meanwhile in Europe it was much the same story, with the STOXX 600 (-0.50%) and Germany’s DAX (-1.40%) seeing decent losses of their own.

Speaking of Europe, all eyes are on what’s going to happen with the gas situation now that the Nord Stream pipeline is undergoing scheduled 10-day maintenance. European natural gas futures (-6.10%) did come down yesterday after rising for 4 consecutive weeks, thanks to the news at the very end of last week that Canada would return a turbine for the Nord Stream pipeline after their government issued a “time-limited and revocable” permit that removed it from sanctions. That said there are still significant jitters as to whether the pipeline will be turned back on again after the maintenance concludes, which meant that the Euro itself fell even closer to parity against the US Dollar. In fact, the euro closed near its weakest levels of the day at $1.0040, and has hit a fresh low of $1.0010 as we go to press as markets face up to the prospect of what a full cut-off of Russian gas would mean for the European economy. Speaking to DB's Peter Sidorov yesterday, he tells me that the ambiguity over gas may linger as even if Russia did need this turbine part to restore stronger gas flows, the technical logistics may mean it would take an extra week or two to integrate into the pipeline. So the uncertainty may linger until early August.

Another factor behind the Euro’s decline recently has been the growing divergence in interest rates between the Fed (who’ve already hiked by 150bps this year) and the ECB (who haven’t even begun yet and with worries as to how far they will get). If the upcoming moves this month are in line with our economists’ (and market) expectations, then that divergence will only grow as the Fed hikes by 75bps for a second consecutive meeting, while the ECB commences the hiking cycle with a much smaller 25bps move. However, yesterday brought some more dovish news from the Fed, with Kansas City President George warning against moving too fast on rate hikes, saying that moving “too fast raises the prospect of oversteering”. That may not be too surprising given that George was the only FOMC voters to dissent from the 75bps majority last month in favour of a smaller 50bps hike. George also warned that the extra volatility the Fed injects into the market when its policy path is so uncertain may hurt Treasury market functioning, which seems like she was not a fan changing policy guidance with such short notice before the June FOMC, perhaps another reason for her dissent. Elsewhere, as discussed at the top, we also received the New York Fed’s latest Survey of Consumer Expectations for June. And whilst 1-year ahead inflation expectations hit a record high since the series began at 6.8%, 3-year ahead expectations came down from 3.9% in May to 3.6% in June, and 5-year ahead expectations fell from 2.9% to 2.8%.

That newsflow along with the more general risk-off tone helped support a major rally in Treasuries, with 10yr yields falling -8.8bps to 2.99%, as both inflation breakevens and real rates fell on the day. There was also a fresh flattening in the yield curve, with the 2s10s closing in inversion territory for a 5th day running, finishing at -8.5bps, which isn’t such a good sign as a recessionary indicator, and the length of the inversion now puts it ahead of the 3-day inversion back in late-March/early April, so this is getting harder to dismiss as just a blip. Furthermore, even the Fed’s preferred yield curve indicator of the near-term forward spread flattened to just 114bps, which is something we haven’t seen since early January after peaking at 270bps on April 1. This morning yields on 10yr USTs are another -3.34 bps lower at 2.954% as I type.

In Europe there was much the same pattern, with yields on 10yr bunds (-9.9bps), OATs (-10.3bps) and BTPs (-7.3bps) all moving lower. But the risk-off move meant there was a widening in peripheral spreads, and the iTraxx Crossover was another to widen (+8.6bps to 585bps), thus reversing three consecutive moves lower.

The losses in US and European equities are echoing in Asian this morning. The nervousness is not being helped by news of another Covid-19 surge in China as the renewed outbreak is raising fears of more lockdowns (see below). As I type, the Nikkei (-1.68%) is leading losses across the region followed by the Hang Seng (-1.57%) and the Kospi (-1.37%). In mainland China, the Shanghai Composite and (-0.83%) and CSI (-0.74%) are also lower. Outside of Asia, equity futures in DMs point to further losses with contracts on the S&P 500 (-0.54%), NASDAQ 100 (-0.68%) and DAX (-0.71%) all weaker. Oil prices are also lower overnight as recession fears and China’s Covid curbs weigh on demand prospects. As we go to press, Brent futures are -1.46% at $105.54/bbl and WTI futures -1.68% at $102.34/bbl.

Over in China, Shanghai city reported 59 new infections for Monday, above 50 for the fourth day in a row thus prompting the city authorities to another mass testing effort after finding a highly transmissible Omicron subvariant.

Early morning data showed that producer prices in Japan rose +0.7% m/m in June (v/s +0.6% expected) and against a +0.1% rise in May.

In the UK, the ruling Conservative party are opening nominations for the next leadership today, with voting starting tomorrow. MPs will then, through a series of voting rounds over the next week choose their favourite two candidates, from which point the party membership will make their decision and with the new PM expected to be announced on September 5.

There wasn’t much data to speak of yesterday, but Italian retail sales for May grew by +1.9% (vs. +0.4% expected), and the prior month was also revised positively.

To the day ahead now, and data releases include the German ZEW survey for July, as well as the US NFIB small business optimism index for June. Central bank speakers include BoE Governor Bailey, the Fed’s Barkin and the ECB’s Villeroy. Finally, earnings releases today include PepsiCo.

Simple blood test could predict risk of long-term COVID-19 lung problems

UVA Health researchers have discovered a potential way to predict which patients with severe COVID-19 are likely to recover well and which are likely to…

UVA Health researchers have discovered a potential way to predict which patients with severe COVID-19 are likely to recover well and which are likely to suffer “long-haul” lung problems. That finding could help doctors better personalize treatments for individual patients.

Credit: UVA Health

UVA Health researchers have discovered a potential way to predict which patients with severe COVID-19 are likely to recover well and which are likely to suffer “long-haul” lung problems. That finding could help doctors better personalize treatments for individual patients.

UVA’s new research also alleviates concerns that severe COVID-19 could trigger relentless, ongoing lung scarring akin to the chronic lung disease known as idiopathic pulmonary fibrosis, the researchers report. That type of continuing lung damage would mean that patients’ ability to breathe would continue to worsen over time.

“We are excited to find that people with long-haul COVID have an immune system that is totally different from people who have lung scarring that doesn’t stop,” said researcher Catherine A. Bonham, MD, a pulmonary and critical care expert who serves as scientific director of UVA Health’s Interstitial Lung Disease Program. “This offers hope that even patients with the worst COVID do not have progressive scarring of the lung that leads to death.”

Long-Haul COVID-19

Up to 30% of patients hospitalized with severe COVID-19 continue to suffer persistent symptoms months after recovering from the virus. Many of these patients develop lung scarring – some early on in their hospitalization, and others within six months of their initial illness, prior research has found. Bonham and her collaborators wanted to better understand why this scarring occurs, to determine if it is similar to progressive pulmonary fibrosis and to see if there is a way to identify patients at risk.

To do this, the researchers followed 16 UVA Health patients who had survived severe COVID-19. Fourteen had been hospitalized and placed on a ventilator. All continued to have trouble breathing and suffered fatigue and abnormal lung function at their first outpatient checkup.

After six months, the researchers found that the patients could be divided into two groups: One group’s lung health improved, prompting the researchers to label them “early resolvers,” while the other group, dubbed “late resolvers,” continued to suffer lung problems and pulmonary fibrosis.

Looking at blood samples taken before the patients’ recovery began to diverge, the UVA team found that the late resolvers had significantly fewer immune cells known as monocytes circulating in their blood. These white blood cells play a critical role in our ability to fend off disease, and the cells were abnormally depleted in patients who continued to suffer lung problems compared both to those who recovered and healthy control subjects.

Further, the decrease in monocytes correlated with the severity of the patients’ ongoing symptoms. That suggests that doctors may be able to use a simple blood test to identify patients likely to become long-haulers — and to improve their care.

“About half of the patients we examined still had lingering, bothersome symptoms and abnormal tests after six months,” Bonham said. “We were able to detect differences in their blood from the first visit, with fewer blood monocytes mapping to lower lung function.”

The researchers also wanted to determine if severe COVID-19 could cause progressive lung scarring as in idiopathic pulmonary fibrosis. They found that the two conditions had very different effects on immune cells, suggesting that even when the symptoms were similar, the underlying causes were very different. This held true even in patients with the most persistent long-haul COVID-19 symptoms. “Idiopathic pulmonary fibrosis is progressive and kills patients within three to five years,” Bonham said. “It was a relief to see that all our COVID patients, even those with long-haul symptoms, were not similar.”

Because of the small numbers of participants in UVA’s study, and because they were mostly male (for easier comparison with IPF, a disease that strikes mostly men), the researchers say larger, multi-center studies are needed to bear out the findings. But they are hopeful that their new discovery will provide doctors a useful tool to identify COVID-19 patients at risk for long-haul lung problems and help guide them to recovery.

“We are only beginning to understand the biology of how the immune system impacts pulmonary fibrosis,” Bonham said. “My team and I were humbled and grateful to work with the outstanding patients who made this study possible.”

Findings Published

The researchers have published their findings in the scientific journal Frontiers in Immunology. The research team consisted of Grace C. Bingham, Lyndsey M. Muehling, Chaofan Li, Yong Huang, Shwu-Fan Ma, Daniel Abebayehu, Imre Noth, Jie Sun, Judith A. Woodfolk, Thomas H. Barker and Bonham. Noth disclosed that he has received personal fees from Boehringer Ingelheim, Genentech and Confo unrelated to the research project. In addition, he has a patent pending related to idiopathic pulmonary fibrosis. Bonham and all other members of the research team had no financial conflicts to disclose.

The UVA research was supported by the National Institutes of Health, grants R21 AI160334 and U01 AI125056; NIH’s National Heart, Lung and Blood Institute, grants 5K23HL143135-04 and UG3HL145266; UVA’s Engineering in Medicine Seed Fund; the UVA Global Infectious Diseases Institute’s COVID-19 Rapid Response; a UVA Robert R. Wagner Fellowship; and a Sture G. Olsson Fellowship in Engineering.

To keep up with the latest medical research news from UVA, subscribe to the Making of Medicine blog at http://makingofmedicine.virginia.edu.

After having moved from Canada to the United States, partly to be wealthier and partly to be freer (those two are connected, by the way), I was shocked,…

After having moved from Canada to the United States, partly to be wealthier and partly to be freer (those two are connected, by the way), I was shocked, in March 2020, when President Trump and most US governors imposed heavy restrictions on people’s freedom. The purpose, said Trump and his COVID-19 advisers, was to “flatten the curve”: shut down people’s mobility for two weeks so that hospitals could catch up with the expected demand from COVID patients. In her book Silent Invasion, Dr. Deborah Birx, the coordinator of the White House Coronavirus Task Force, admitted that she was scrambling during those two weeks to come up with a reason to extend the lockdowns for much longer. As she put it, “I didn’t have the numbers in front of me yet to make the case for extending it longer, but I had two weeks to get them.” In short, she chose the goal and then tried to find the data to justify the goal. This, by the way, was from someone who, along with her task force colleague Dr. Anthony Fauci, kept talking about the importance of the scientific method. By the end of April 2020, the term “flatten the curve” had all but disappeared from public discussion.

Now that we are four years past that awful time, it makes sense to look back and see whether those heavy restrictions on the lives of people of all ages made sense. I’ll save you the suspense. They didn’t. The damage to the economy was huge. Remember that “the economy” is not a term used to describe a big machine; it’s a shorthand for the trillions of interactions among hundreds of millions of people. The lockdowns and the subsequent federal spending ballooned the budget deficit and consequent federal debt. The effect on children’s learning, not just in school but outside of school, was huge. These effects will be with us for a long time. It’s not as if there wasn’t another way to go. The people who came up with the idea of lockdowns did so on the basis of abstract models that had not been tested. They ignored a model of human behavior, which I’ll call Hayekian, that is tested every day.

That wasn’t the only uncertainty. My daughter Karen lived in San Francisco and made her living teaching Pilates. San Francisco mayor London Breed shut down all the gyms, and so there went my daughter’s business. (The good news was that she quickly got online and shifted many of her clients to virtual Pilates. But that’s another story.) We tried to see her every six weeks or so, whether that meant our driving up to San Fran or her driving down to Monterey. But were we allowed to drive to see her? In that first month and a half, we simply didn’t know.

These are the themes that emerged when I invited nine Black women to chronicle their professional experiences and relationships with colleagues as they earned their Ph.D.s at a public university in the Midwest. I featured their writings in the dissertation I wrote to get my Ph.D. in curriculum and instruction.

“It’s not just the beating me down that is hard,” one participant told me about constantly having her intelligence questioned. “It is the fact that it feels like I’m villainized and made out to be the problem for trying to advocate for myself.”

The women told me they did not feel like they belonged. They spoke of routinely being isolated by peers and potential mentors.

One participant told me she felt that peer community, faculty mentorship and cultural affinity spaces were lacking.

Participants also discussed the ways they felt they were duped into taking on more than their fair share of work.

“I realized I had been tricked into handling a two- to four-person job entirely by myself,” one participant said of her paid graduate position. “This happened just about a month before the pandemic occurred so it very quickly got swept under the rug.”

Why it matters

The hostility that Black women face in higher education can be hazardous to their health. The women in my study told me they were struggling with depression, had thought about suicide and felt physically ill when they had to go to campus.

Other studies have found similar outcomes. For instance, a 2020 study of 220 U.S. Black college women ages 18-48 found that even though being seen as a strong Black woman came with its benefits – such as being thought of as resilient, hardworking, independent and nurturing – it also came at a cost to their mental and physical health.

Several anthologies examine the negative experiences that Black women experience in academia. They include education scholars Venus Evans-Winters and Bettina Love’s edited volume, “Black Feminism in Education,” which examines how Black women navigate what it means to be a scholar in a “white supremacist patriarchal society.” Gender and sexuality studies scholar Stephanie Evans analyzes the barriers that Black women faced in accessing higher education from 1850 to 1954. In “Black Women, Ivory Tower,” African American studies professor Jasmine Harris recounts her own traumatic experiences in the world of higher education.

What’s next

In addition to publishing the findings of my research study, I plan to continue exploring the depths of Black women’s experiences in academia, expanding my research to include undergraduate students, as well as faculty and staff.

I believe this research will strengthen this field of study and enable people who work in higher education to develop and implement more comprehensive solutions.

The Research Brief is a short take on interesting academic work.

Ebony Aya received funding from the Black Collective Foundation in 2022 to support the work of the Aya Collective.

We use cookies on our website to give you the most relevant experience by remembering your preferences and repeat visits. By clicking “Accept”, you consent to the use of ALL the cookies.

This website uses cookies to improve your experience while you navigate through the website. Out of these, the cookies that are categorized as necessary are stored on your browser as they are essential for the working of basic functionalities of the website. We also use third-party cookies that help us analyze and understand how you use this website. These cookies will be stored in your browser only with your consent. You also have the option to opt-out of these cookies. But opting out of some of these cookies may affect your browsing experience.

Necessary cookies are absolutely essential for the website to function properly. These cookies ensure basic functionalities and security features of the website, anonymously.

Cookie

Duration

Description

cookielawinfo-checbox-analytics

11 months

This cookie is set by GDPR Cookie Consent plugin. The cookie is used to store the user consent for the cookies in the category "Analytics".

cookielawinfo-checbox-functional

11 months

The cookie is set by GDPR cookie consent to record the user consent for the cookies in the category "Functional".

cookielawinfo-checbox-others

11 months

This cookie is set by GDPR Cookie Consent plugin. The cookie is used to store the user consent for the cookies in the category "Other.

cookielawinfo-checkbox-necessary

11 months

This cookie is set by GDPR Cookie Consent plugin. The cookies is used to store the user consent for the cookies in the category "Necessary".

cookielawinfo-checkbox-performance

11 months

This cookie is set by GDPR Cookie Consent plugin. The cookie is used to store the user consent for the cookies in the category "Performance".

viewed_cookie_policy

11 months

The cookie is set by the GDPR Cookie Consent plugin and is used to store whether or not user has consented to the use of cookies. It does not store any personal data.

Functional cookies help to perform certain functionalities like sharing the content of the website on social media platforms, collect feedbacks, and other third-party features.

Performance cookies are used to understand and analyze the key performance indexes of the website which helps in delivering a better user experience for the visitors.

Analytical cookies are used to understand how visitors interact with the website. These cookies help provide information on metrics the number of visitors, bounce rate, traffic source, etc.

Advertisement cookies are used to provide visitors with relevant ads and marketing campaigns. These cookies track visitors across websites and collect information to provide customized ads.

{kind=link}