Government

Futures Under Water As Tech Selloff Spreads, Yields Spike, Lira Implodes

Futures Under Water As Tech Selloff Spreads, Yields Spike, Lira Implodes

US equity futures continued their selloff for the second day as Treasury yields spiked to 1.66%, up almost 4bps on the day, and as the selloff in tech shares spread…

Share this:

US equity futures continued their selloff for the second day as Treasury yields spiked to 1.66%, up almost 4bps on the day, and as the selloff in tech shares spread as traders trimmed bets for a dovish-for-longer Federal Reserve after the renomination of Jerome Powell as its chair. At 8:00am ET, S&P futures were down 2.75 points or -0.05%, with Dow futures flat and Nasdaq futures extended their selloff but were off worst levels, down 41.25 points or 0.25%, after Monday’s last-hour furious rout in technology stocks.

As repeatedly covered here in recent weeks, the Turkish currency crisis deepened with the lira weakening past 13 per USD, a drop of more than 10% in one day.

Oil rebounded - as expected - after a panicking Joe Biden, terrified about what soaring gas prices mean for Dems midterm changes, announced that the US, together with several other countries such as China, India and Japan, would tap up to 50 million barrels in strategic reserves, a move which was fully priced in and will now serve to bottom tick the price of oil.

In premarket trading, Zoom lost 9% in premarket trading on slowing growth.

For some unknown reason, investors have been reducing expectations for a deeper dovish stance by the Fed after Powell was selected for a second term (as if Powell - the man who started purchases of corporate bonds - is somehow hawkish). The chair himself sought to strike a balance in his policy approach saying the central bank would use tools at its disposal to support the economy as well as to prevent inflation from becoming entrenched.

“While investors no longer have to wonder about who will be leading the Federal Reserve for the next few years, the next big dilemma the central bank faces is how to normalize monetary policy without upsetting markets,” wrote Robert Schein, chief investment officer at Blanke Schein Wealth Management. Following Powell’s renomination, “the market has unwound hedges against a more ‘dovish’ personnel shift,” Chris Weston, head of research with Pepperstone Financial Pty Ltd., wrote in a note.

Not helping was Atlanta Fed President Raphael Bostic who said Monday that the Fed may need to speed up the removal of monetary stimulus and allow for an earlier-than-planned increase in interest rates

European stocks dropped with market focusing on potential Covid lockdowns and policy tightening over solid PMI data. Euro Stoxx 50 shed as much as 1.7% with tech, financial services and industrial names the hardest hit. Better-than-forecast PMI numbers out of Europe’s major economies prompted money markets to resume bets that the ECB will hike the deposit rate 10 basis points as soon as December 2022, versus 2023 on Monday.

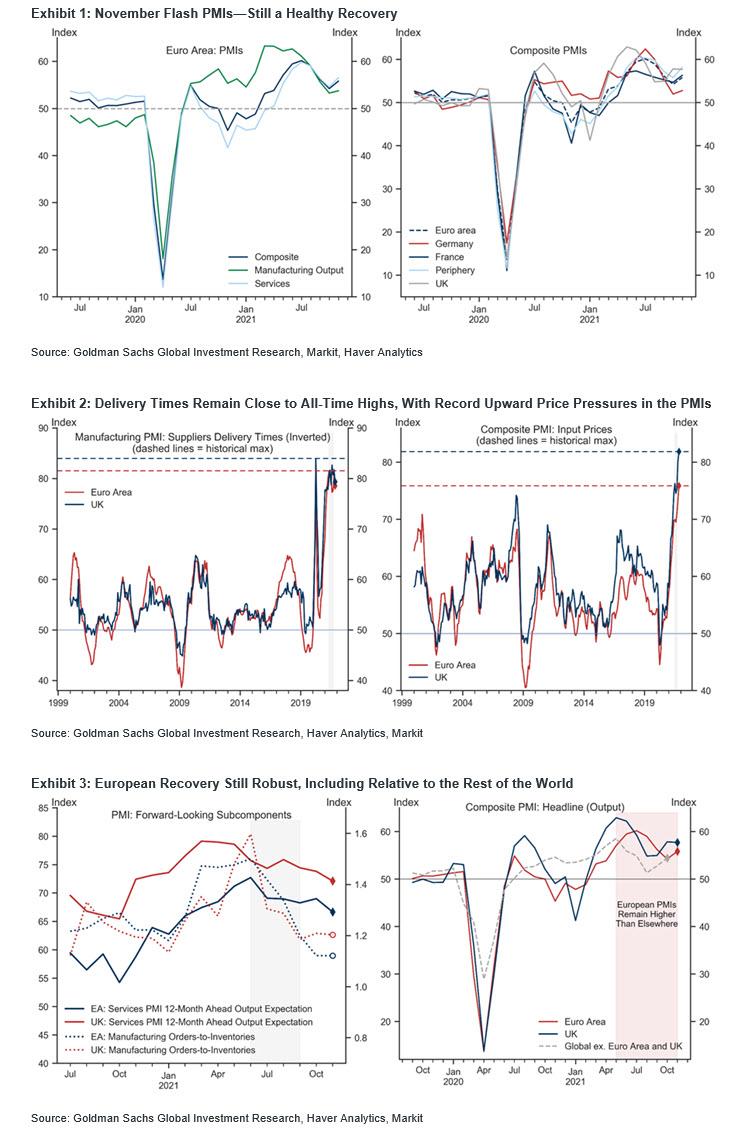

As Goldman notes, the Euro area composite flash PMI increased by 1.6pt to 55.8 in November — strongly ahead of consensus expectations — in a first gain since the post-July moderation. The area-wide gain was broad-based across countries, and sectors. Supply-side issues continued to be widely reported, with input and output price pressures climbing to all-time highs. In the UK, the November flash composite PMI came in broadly as expected, and while input costs rose to a new all-time high, pass-through into output prices appears lower than usual. Forward-looking expectations remain comfortably above historical averages across Europe, although today's data are unlikely to fully reflect the covid containment measures taken in a number of European countries over recent days.

Key numbers (the responses were collected between 10 and 19 November (except in the UK, where the survey response window spanned 12-19 November).

- Euro Area Composite PMI (Nov, Flash): 55.8, GS 53.6, consensus 53.0, last 54.2.

- Euro Area Manufacturing PMI (Nov, Flash): 58.6, GS 57.7, consensus 57.4, last 58.3.

- Euro Area Services PMI (Nov, Flash): 56.6, GS 53.9, consensus 53.5, last 54.6.

- Germany Composite PMI (Nov, Flash): 52.8, GS 52.1, consensus 51.0, last 52.0.

- France Composite PMI (Nov, Flash): 56.3, GS 54.4, consensus 53.9, last 54.7.

- UK Composite PMI (Nov, Flash): 57.7, GS 57.7, consensus 57.5, last 57.8.

And visually:

Earlier in the session, Asian stocks fell toward a three-week low as Jerome Powell’s renomination to head the Federal Reserve boosted U.S. yields, putting downward pressure on the region’s technology shares. The MSCI Asia Pacific Index declined as much as 0.5%, as the reappointment sent Treasury yields higher and buoyed the dollar amid concerns monetary stimulus will be withdrawn faster. Consumer discretionary and communication shares were the biggest drags on Asia’s benchmark, with Tencent and Alibaba slipping on worries over tighter regulations in China. “Powell’s renomination was generally expected by the market,” said Chetan Seth, an Asia-Pacific equity strategist at Nomura. The market’s reaction may be short-lived as traders turn their attention to the Fed’s meeting in December and Covid’s resurgence in Europe, he added. Asia shares have struggled to break higher as the jump in yields weighed on sentiment already damped by a lackluster earnings season and the risk of accelerating inflation. The region’s stock benchmark is down about 1% this year compared with a 16% advance in the MSCI AC World Index. Hong Kong and Taiwan were among the biggest decliners, while Australian and Indian shares bucked the downtrend, helped by miners and energy stocks.

India’s benchmark stock index rose, snapping four sessions of declines, boosted by gains in Reliance Industries Ltd. The S&P BSE Sensex climbed 0.3% to close at 58,664.33 in Mumbai, recovering after falling as much as 1.3% earlier in the session. The NSE Nifty 50 Index gained 0.5%. Of the 30 shares on the Sensex, 21 rose and 9 fell. All but one of the 19 sector sub-indexes compiled by BSE Ltd. advanced, led by a gauge of metal stocks. Reliance Industries Ltd. gained 0.9%, after dropping the most in nearly 10 months on Monday following its decision to scrap a plan to sell a 20% stake in its oil-to-chemicals unit to Saudi Arabian Oil Co. Shares of One 97 Communications Ltd., the parent company for digital payments firm Paytm, climbed 9.9% after two days of relentless selling since its trading debut.

In rates, Treasuries dropped, with the two-year rate jumping five basis points, helping to flatten the yield curve.

Bunds and Treasuries bear steepened with German 10y yields ~5bps cheaper. Gilts bear flatten, cheapening 1.5bps across the short end. 10Y TSY yields rose as high as 1.67% before reversing some of the move.

In FX, the Bloomberg Dollar Spot Index was little changed after earlier advancing to the highest level since September 2020 as markets moved to price in a full quarter-point rate hike by the June Fed meeting, with a good chance of two more by year-end; Treasury yields inched up across the curve apart from the front end. The Japanese yen briefly fell past 115 per dollar for the first time since 2017. The euro advanced after better-than-forecast PMI numbers out of Europe’s major economies prompted money markets to resume bets that the ECB will hike the deposit rate 10 basis points as soon as December 2022, versus 2023 on Monday. Sterling declined versus the dollar and the euro; traders are taking an increasingly negative view on the pound, betting that the decline that’s already left the currency near its lowest this year has further to run

New Zealand’s dollar under-performed all G-10 peers as leveraged longs backing a 50 basis-point hike from the central bank were flushed out of the market; sales were mainly seen against the greenback and Aussie. The yuan approached its strongest level against trade partners’ currencies in a sign that traders see a low likelihood of aggressive official intervention. The Turkish lira (see above) crashed to a record low on Tuesday, soaring more than 10% and just shy of 14 vs the USD, a day after President Recep Tayyip Erdogan defended his pursuit of lower interest rates to boost economic growth and job creation.

In commodities, crude futures rebounded sharply after Biden announced a coordinated, global SPR release which would see the US exchange up to 32mm barrels, or a negligible amount. Brent spiked back over $80 on the news after trading in the mid-$78s. Spot gold drops ~$8, pushing back below $1,800/oz. Base metals are well supported with LME nickel outperforming.

Looking at the day ahead, the main data highlight will be the flash PMIs for November from around the world, and there’s also the Richmond Fed manufacturing index for November. Finally from central banks, we’ll hear from BoE Governor Bailey, Deputy Governor Cunliffe and the BoE’s Haskel, as well as ECB Vice President de Guindos and the ECB’s Makhlouf.

Market Snapshot

S&P 500 futures down 0.3% to 4,667.75

Brent Futures down 0.9% to $78.95/bbl

Gold spot down 0.4% to $1,796.86

U.S. Dollar Index down 0.17% to 96.39

Top Overnight News from Bloomberg

- The volatility term structures in the major currencies show that next month’s meetings by monetary policy authorities are what matters most. Data galore out of the U.S. by Wednesday’s New York cut off means demand for one-day structures remains intact, yet it’s not enough to bring about term structure inversion as one-week implieds stay below recent cycle highs

- Lael Brainard, picked to be vice chair of the Federal Reserve, is expected to be a critical defender of its commitment to maximum employment across demographic groups at a time when other U.S. central bankers are more worried by inflation

- ECB Executive Board member Isabel Schnabel said there’s an increasing threat of inflation taking hold, as she played down the danger that resurgent coronavirus infections might impede the euro zone’s recovery

- Regarding latest pandemic restrictions, “when it comes to the impact, I would say that while it will surely have a moderating impact on economic activity, the impact on inflation will actually be more ambiguous because it might also reinforce some of the concerns we have around supply bottlenecks,” ECB Governing Council member Klaas Knot says in Bloomberg Television interview with Francine Lacqua

- European Union countries are pushing for an agreement on how long Covid-19 vaccinations protect people and how to manage booster shots as they try to counter the pandemic’s fourth wave and safeguard free travel

- Germany’s top health official reiterated a warning that the government can’t exclude any measures, including another lockdown, as it tries to check the latest wave of Covid-19 infections

- The State Council, China’s cabinet, released three documents in the past several days, outlining measures to help small and medium-sized enterprises weather the downturn: from encouraging local governments to roll out discounts for power usage to organizing internet companies to provide cloud and digital services to SMEs

A more detailed look at global markets courtesy of Newsquawk

Asia-Pac stocks traded mixed following a similar performance in the US where participants digested President Biden’s decision to nominate Fed Chair Powell for a second term and Fed’s Brainard for the Vice Chair role. This resulted in bear flattening for the US curve and underpinned the greenback, while the major indices were choppy but with late selling heading into the close in which the S&P 500 slipped beneath the 4,700 level and the Nasdaq underperformed as tech suffered the brunt of the higher yields. ASX 200 (+0.8%) was positive with sentiment encouraged after stronger PMI data and M&A developments including BHP’s signing of a binding agreement to merge its oil and gas portfolio with Woodside Petroleum to create a global top 10 independent energy company and the largest listed energy company in Australia, which spurred outperformance for the mining and energy related sectors. KOSPI (-0.5%) was lacklustre and retreated below the 3k level amid broad weakness in tech which was not helped by concerns that South Korea could take another aim at large tech through a platform bill and with the government said to be mulling strengthening social distancing measures. Hang Seng (-1.2%) and Shanghai Comp. (+0.2%) continued to diverge amid a neutral liquidity effort by the PBoC and with the Hong Kong benchmark conforming to the tech woes, while the mainland was kept afloat after the State Council pledged to strengthen assistance to smaller firms and with Global Times noting that China will likely adopt another RRR cut before year-end to cope with an economic slowdown. Finally, Japanese participants were absent from the market as they observed Labor Thanksgiving Day, while yields in Australia were higher as they tracked global counterparts and following a Treasury Indexed bond offering in the long-end.

Top Asian News

- Tiger Global Leads $210 Million Round by India Proptech Unicorn

- China’s Slowdown Tests Central Bank Amid Debate Over Easing

- Kuaishou Defies China Crackdown as Revenue Climbs 33%

- Evergrande Shares Jump in Afternoon Trading as Group Units Rally

Major bourses in Europe are lower across the board, but off worst levels (Euro Stoxx 50 -1.1%; Stoxx 600 -1.3%) following on from the mixed APAC performance, but with pandemic restrictions casting a shower over the region. US equity futures are mostly lower but to a lesser extent than European peers, with the YM (+0.1%) the relative outperformer vs the ES (-0.1%), NQ (-0.3%) and RTY (-0.8%). Back to Europe, the morning saw the release of Flash PMIs which failed to spur much action across market given the somewhat stale nature against the backdrop of a worsening COVID situation in Europe. Losses in the UK’s FTSE 100 (-0.1%) are more cushioned vs European counterparts, with heavyweight miners doing the heavy lifting, and as the basic resources sector outpaces and resides as the only sector in the green at the time of writing amid a surge in iron ore prices overnight. Sticking with sectors, there is no clear or overarching theme/bias. Tech resides at the foot of the pile, unaided by the intraday rise in yields. Travel and Leisure also reside towards the bottom of the bunch, but more a function of the “leisure” sub-sector as opposed to the “travel” component, with Evolution Gaming (-3.7%) and Flutter (-3.5%) on the back foot. In terms of individual movers, Thyssenkrupp (-7.0%) tumbles after the Co. announced a secondary offer by Cevian of 43mln shares. Meanwhile, Telecom Italia (-3%) is softer following yesterday’s run, whilst Vivendi (-0.5%) said the current KKR (KKR) offer does not reflect Telecom Italia's value and it has no intention of offloading its 24% stake.

Top European News

- U.K. PMIs Show Record Inflation and ‘Green Light’ for BOE Hike

- Kremlin Says New U.S. Sanctions on Nord Stream 2 Are ‘Illegal’

- ECB’s Knot Says New Lockdowns Won’t Delay Wind-Down of Stimulus

- Telefonica Drops, Berenberg Cuts on Spain Margin Problems

In FX, the Buck had already eased off best levels to relieve some pressure from its rivals, but the Euro also derived encouragement from the fact that a key long term Fib held (just) at 1.1225 before getting a rather unexpected fundamental fillip in the form of stronger than forecast flash Eurozone PMIs plus hawkish-sounding comments from ECB’s Schnabel. Eur/Usd duly rebounded to 1.1275 and the Dollar index retreated to 96.308 from a fresh y-t-d peak of 96.603, while the Yen and Franc also took advantage to varying degrees against the backdrop of deteriorating risk sentiment and in thinner trading volumes for the former due to Japan’s Labor Day Thanksgiving holiday. Usd/Jpy recoiled from 115.15 to 114.49 at one stage and Usd/Chf to 0.9301 from 0.9335 before both pairs bounced with the Greenback and a rebound in US Treasury yields ahead of Markit’s preliminary PMIs and Usd 59 bn 7 year note supply.

- TRY - Simply no respite for the Lira via another marked pull-back in oil prices on heightened prospects of SPR taps, the aforementioned Buck breather or even a decent correction as Usd/Try extended its meteoric rise beyond 11.5000 and 12.0000 towards 12.5000 irrespective of an ally of Turkish President Erdogan urging a debate on CBRT independence. Instead, the run and capital flight continues as talks with the IMF make no progress and an EU court condemns the country for detaining 400+ judges after the coup, while the President rules out a snap election after recent calls for an earlier vote than the scheduled one in 2023 by the main opposition party.

- NZD/CAD/GBP/AUD - It remains to be seen whether the RBNZ maintains a 25 bp pace of OCR normalisation overnight, but weak NZ retail activity in Q3 may be a telling factor and is applying more downside pressure on the Kiwi across the board, as Nzd/Usd hovers under 0.6950 and the Aud/Nzd cross tests 1.0425 on relative Aussie strength or resilience gleaned from another spike in iron ore that is helping to keep Aud/Usd above 0.7200. Conversely, the latest downturn in crude is undermining the Loonie and the Pound hardly derived any traction from better than anticipated UK PMIs even though they should provide the BoE more justification to hike rates next month. Usd/Cad has now breached 1.2700 and only stopped a few pips short of 1.2750 before fading ahead of comments from BoC’s Beaudry, while Cable topped out just over 1.3400 awaiting BoE Governor Bailey, whilst Haskel reaffirmed his stance in the transitory inflation camp, although suggested that if the labour market remains tight the Bank Rate will have to rise.

- SCANDI/EM - Hardly a shock that Brent’s reversal has hit the Nok alongside broader risk-aversion that is also keeping the Sek defensive in advance of the Riksbank, but the Zar is coping well considering Gold’s loss of Usd 1800+/oz status and test of chart support at the 100 DMA only a couple of Bucks off the 200. Similarly, the Cnh and Cny are still resisting general Usd strength and other negatives, with help from China’s State Council pledging to strengthen assistance to smaller firms perhaps.

In commodities, WTI and Brent Jan'22 futures remain under pressure with the former back under USD 76/bbl (vs USD 76.59/bbl high) and the latter around USD 79/bbl (vs USD 79.63/bbl high). The WTI contract is also narrowly lagging Brent by some USD 0.30/bbl at the time of writing. Participants are keeping their eyes peeled for reserve releases from the US, potentially in coordination with other nations including China, Japan, and India – with inflation concerns being the common denominator. The move also comes in reaction to OPEC+ flouting calls by large oil consumers, particularly the US, to further open the taps beyond the group’s planned 400k BPD/m hikes. A source cited by Politico caveated that a final decision is yet to be made, and US officials are hoping that the threat of an SPR release would persuade OPEC+ to double their quotas at the Dec 2nd meeting. As it stands, Energy Intel journalist Bakr noted that she has not heard anything from OPEC+ officials about changing production plans, but delegates yesterday suggested that plans may be tweaked. Click here for the full Newsquawk analysis piece. Aside from this, US President Biden is also poised to give a speech on the economy, whilst the weekly Private Inventories will also be released today. Elsewhere, spot gold and have been drifting lower in what is seemingly a function of technical, with the yellow metal dipping under USD 1,800/oz from a USD 1,812/oz current high, with a cluster of DMAs present to the downside including the 100 DMA (around USD 1,793/oz), 200 DMA (around USD 1,791/oz) and 50 DMA (around USD 1,789/oz). Turning to base metals, LME copper holds a positive bias with prices on either side of USD 9,750/t, whilst Dalian iron ore surged overnight - with reports suggesting that steel de-stockpiling accelerated last week, and analysts suggesting that the market is betting on steelmakers in December.

US Event Calendar

- 9:45am: Nov. Markit US Composite PMI, prior 57.6

- 9:45am: Nov. Markit US Services PMI, est. 59.0, prior 58.7

- 9:45am: Nov. Markit US Manufacturing PMI, est. 59.1, prior 58.4

- 10am: Nov. Richmond Fed Index, est. 11, prior 12

DB's Jim Reid concludes the overnight wrap

A reminder that yesterday we published our 2022 credit strategy outlook. See here for the full report. Craig has also put out a more detailed HY 2022 strategy document here and Karthik a more detail IG equivalent here. Basically we think spreads will widen as much as 30-40bps in IG and 120-160bps in HY due to a response to a more dramatic appreciation of the Fed being well behind the curve. This sort of move is consistent with typical mid-cycle ranges through history. We do expect this to mostly retrace in H2 as markets recover from the shock and growth remains decent and liquidity still high.

We also published the results of our ESG issuer and investor survey where around 530 responded. Please see the results here.

Today is the start of a new adventure as I’m doing my first overseas business trip in 20 months. It took me a stressful 2 hours last night to find and fill in various forms, download various apps and figure out how on earth I travel in this new world. Hopefully I’ve got it all correct or I’ll be turned back at the Eurostar gates! The interesting thing about not travelling is that I’ve filled the time doing other work stuff so productivity will suffer. So if I can do a CoTD today it’ll be done on an iPhone whilst racing through the French countryside. Actually finishing this off very early in a long taxi ride on the way to the train reminds me of how car sick I get working on my iPhone! The delights of travel are all coming flooding back.

After much anticipation over recent weeks, we finally heard yesterday that President Biden would be nominating Fed Chair Powell for another four-year term at the helm of the central bank. In some ways the decision had been widely expected, and Powell was the favourite in prediction markets all along over recent months. But the Fed’s staff trading issues and reports that Governor Brainard was also being considered had led many to downgrade Powell’s chances, so there was an element of uncertainty going into the decision, even if any policy differences between the two were fairly marginal. In the end however, Biden opted for continuity at the top, with Brainard tapped to become Vice Chair instead.

Powell’s nomination will require senate confirmation once again, but this isn’t expected to be an issue, not least with Powell having been confirmed in an 84-13 vote last time around. Further, Senate Banking Committee Chair Brown, viewed as a progressive himself, noted last week there should be no issue confirming Powell despite rumblings from progressive lawmakers. More important to watch out for will be who Biden selects for the remaining positions on the Fed Board of Governors, where there are still 3 vacant seats left to fill, including the position of Vice Chair for Supervision. In a statement released by the White House, it said that Biden intended to make those “beginning in early December”, so even with Powell staying on, there’s actually a reasonable amount of scope for Biden to re-shape the Fed’s leadership. A potential hint about who may be considered, President Biden noted his next appointments will “bring new diversity to the Fed.”

President Biden, flanked by Powell and Brainard, held a press conference following the announcement. He noted maintaining the Fed’s independence and leadership stability informed his decision, and that Chair Powell assured the President he would focus on fighting inflation. He was apparently also assured that the Chair would work to combat climate change, perhaps an olive branch to those in his party that wanted a more progressive nominee. Powell and Brainard both followed up with remarks of their own, but didn’t stray from the recent Fed party line.

In response to the decision, investors moved to bring forward their timing of the initial rate hike from the Fed, with one now just about priced by the time of their June 2022 meeting, whilst the dollar index (+0.54%) strengthened to a fresh one-year high. This reflects the perception among many investors that Brainard was someone who’d have taken the Fed on a more dovish trajectory. Inflation breakevens fell across the curve as well in response. Indeed the 4-year breakeven, which roughly coincides with the term of the next Fed chair, was down -3.8bps after yesterday’s session, with the bulk of that dive coming immediately after the confirmation of Powell’s nomination.

Nevertheless, that decline in breakevens was more than outweighed by a shift higher in real rates that sent nominal yields noticeably higher. By the close, yields on 2yr (+7.8bps) and 5yr (+9.5bps) Treasuries were at their highest levels since the pandemic began, and those on 10yr Treasuries were also up +7.7bps, ending the session at 1.62%. 2yr yields were a full 14.1bps higher than the intra-day lows on Friday after the Austria lockdown news.

We had similar bond moves in Europe too, with yields on 10yr bunds (+4.0bps) moving higher throughout the session thanks to a shift in real rates. Another noticeable feature in the US was the latest round of curve flattening, with the 5s30s (-4.4bps) reaching its flattest level (+64.1bps) since the initial market panic over Covid-19 back in March 2020.

The S&P 500 took a sharp turn heading into the New York close after trading in positive territory for most of the day, ultimately closing down -0.32%. Sector performance was mixed, energy (+1.81%) and financials (+1.43%) were notable outperformers on climbing oil prices and yields, while big tech companies across different sectors were hit by higher discount rates. The NASDAQ (-1.26%) ended the day lower, having pared back its initial gains that earlier put it on track to reach a record of its own.

The other main piece of news yesterday came on the energy front, where it’s been reported that we could have an announcement as soon as today about a release of oil from the US Strategic Petroleum Reserve, potentially as part of a joint announcement with other nations. Oil prices were fairly resilient to the news, with Brent crude (+1.03%) and WTI (+0.85%) still moving higher, although both are down from their recent peaks as speculation of such a move has mounted. This could help put some downward pressure on inflation, but as recent releases have shown, price gains have been broadening out over the last couple of months to a wider swathe of categories, so it remains to be seen how helpful this will prove, and will obviously depend on how much is released along with how the OPEC+ group react. For their part, OPEC+ members noted that the moves from the US and its allies would force them to reconsider their production plans at their meeting next week.

Looking ahead now, one of the main highlights today will come from the release of the flash PMIs for November, which will give us an initial indication of how the global economy has fared into the month. As mentioned yesterday, the Euro Area PMIs have been decelerating since the summer, so keep an eye out for how they’re being affected by the latest Covid wave. It’ll also be worth noting what’s happening to price pressures, particularly with inflation running at more than double the ECB’s target right now.

Overnight in Asia stocks are trading mixed with Shanghai Composite (+0.43%), CSI (+0.20%), KOSPI (-0.44%) and Hang Seng (-1.01%) diverging, while the Nikkei is closed for Labor Thanksgiving. The flash manufacturing PMI release from Australia (58.5 vs 58.2 previous) came in close to last month while both the composite (55 vs 52.1 previous) and services (55 vs 51.8 previous) accelerated. In Japan the Yen slid past an important level of 115 against the Dollar for the first time in four years after Powell was confirmed. This marks an overall slide of 10% this year making it the worst performer amongst advanced economy currencies. S&P 500 (-0.01%) and DAX futures (-0.31%) are flat to down with Europe seemingly catching up with the weak U.S. close.

Before this, in Europe yesterday, equities continued to be subdued, with the STOXX 600 down -0.13% after trading in a tight range, as the continent reacted to another surge in Covid-19 cases. The move by Austria back into lockdown has raised questions as to where might be next, and Bloomberg reported that Chancellor Merkel told CDU officials yesterday that the recent surge was worse than anything seen so far, and that additional restrictions would be required. So the direction of travel all appears to be one way for the time being in terms of European restrictions, and even a number of less-affected countries are still seeing cases move in an upward direction, including France, Italy and the UK. So a key one to watch that’ll have big implications for economies and markets too.

Staying on Germany, there was some interesting news on a potential coalition yesterday, with Bloomberg obtaining a preliminary list of cabinet positions that said that FDP leader Christian Lindner would become finance minister, and Green co-leader Robert Habeck would become a “super minister” with responsibility for the economy, climate protection and the energy transition. The report also said that both would become Vice Chancellors, whilst the Greens’ Annalena Baerbock would become foreign minister. It’s worth noting that’s still a preliminary list, and the coalition agreement is yet to be finalised, but it has been widely suggested that the parties are looking to reach a conclusion to the talks this week, so we could hear some more info on this relatively soon.

There wasn’t much in the way of data yesterday, though the European Commission’s advance November consumer confidence reading for the Euro Area fell back by more than expected to -6.8 (vs. -5.5 expected), which is the lowest it’s been since April. Over in the US, there was October data that was somewhat more positive however, with existing home sales rising to an annualised rate of 6.34m (vs. 6.20m expected), their highest level in 9 months. Furthermore, the Chicago Fed’s national activity index was up to 0.76 (vs. 0.10 expected).

To the day ahead now, and the main data highlight will be the aforementioned flash PMIs for November from around the world, and there’s also the Richmond Fed manufacturing index for November. Finally from central banks, we’ll hear from BoE Governor Bailey, Deputy Governor Cunliffe and the BoE’s Haskel, as well as ECB Vice President de Guindos and the ECB’s Makhlouf.

d

Spread & Containment

‘Excess Mortality Skyrocketed’: Tucker Carlson and Dr. Pierre Kory Unpack ‘Criminal’ COVID Response

‘Excess Mortality Skyrocketed’: Tucker Carlson and Dr. Pierre Kory Unpack ‘Criminal’ COVID Response

As the global pandemic unfolded, government-funded…

Share this:

As the global pandemic unfolded, government-funded experimental vaccines were hastily developed for a virus which primarily killed the old and fat (and those with other obvious comorbidities), and an aggressive, global campaign to coerce billions into injecting them ensued.

Then there were the lockdowns - with some countries (New Zealand, for example) building internment camps for those who tested positive for Covid-19, and others such as China welding entire apartment buildings shut to trap people inside.

It was an egregious and unnecessary response to a virus that, while highly virulent, was survivable by the vast majority of the general population.

Oh, and the vaccines, which governments are still pushing, didn't work as advertised to the point where health officials changed the definition of "vaccine" multiple times.

Tucker Carlson recently sat down with Dr. Pierre Kory, a critical care specialist and vocal critic of vaccines. The two had a wide-ranging discussion, which included vaccine safety and efficacy, excess mortality, demographic impacts of the virus, big pharma, and the professional price Kory has paid for speaking out.

Keep reading below, or if you have roughly 50 minutes, watch it in its entirety for free on X:

Ep. 81 They’re still claiming the Covid vax is safe and effective. Yet somehow Dr. Pierre Kory treats hundreds of patients who’ve been badly injured by it. Why is no one in the public health establishment paying attention? pic.twitter.com/IekW4Brhoy

— Tucker Carlson (@TuckerCarlson) March 13, 2024

"Do we have any real sense of what the cost, the physical cost to the country and world has been of those vaccines?" Carlson asked, kicking off the interview.

"I do think we have some understanding of the cost. I mean, I think, you know, you're aware of the work of of Ed Dowd, who's put together a team and looked, analytically at a lot of the epidemiologic data," Kory replied. "I mean, time with that vaccination rollout is when all of the numbers started going sideways, the excess mortality started to skyrocket."

When asked "what kind of death toll are we looking at?", Kory responded "...in 2023 alone, in the first nine months, we had what's called an excess mortality of 158,000 Americans," adding "But this is in 2023. I mean, we've had Omicron now for two years, which is a mild variant. Not that many go to the hospital."

'Safe and Effective'

Tucker also asked Kory why the people who claimed the vaccine were "safe and effective" aren't being held criminally liable for abetting the "killing of all these Americans," to which Kory replied: "It’s my kind of belief, looking back, that [safe and effective] was a predetermined conclusion. There was no data to support that, but it was agreed upon that it would be presented as safe and effective."

Tucker Carlson Asks the Forbidden Question

— The Vigilant Fox ???? (@VigilantFox) March 14, 2024

He wants to know why the people who made the claim “safe and effective” aren’t being held to criminal liability for abetting the “killing of all these Americans.”

DR. PIERRE KORY: “It’s my kind of belief, looking back, that [safe and… pic.twitter.com/Icnge18Rtz

Carlson and Kory then discussed the different segments of the population that experienced vaccine side effects, with Kory noting an "explosion in dying in the youngest and healthiest sectors of society," adding "And why did the employed fare far worse than those that weren't? And this particularly white collar, white collar, more than gray collar, more than blue collar."

Kory also said that Big Pharma is 'terrified' of Vitamin D because it "threatens the disease model." As journalist The Vigilant Fox notes on X, "Vitamin D showed about a 60% effectiveness against the incidence of COVID-19 in randomized control trials," and "showed about 40-50% effectiveness in reducing the incidence of COVID-19 in observational studies."

Dr. Pierre Kory: Big Pharma is ‘TERRIFIED’ of Vitamin D

— The Vigilant Fox ???? (@VigilantFox) March 14, 2024

Why?

Because “It threatens the DISEASE MODEL.”

A new meta-analysis out of Italy, published in the journal, Nutrients, has unearthed some shocking data about Vitamin D.

Looking at data from 16 different studies and 1.26… pic.twitter.com/q5CsMqgVju

Professional costs

Kory - while risking professional suicide by speaking out, has undoubtedly helped save countless lives by advocating for alternate treatments such as Ivermectin.

Kory shared his own experiences of job loss and censorship, highlighting the challenges of advocating for a more nuanced understanding of vaccine safety in an environment often resistant to dissenting voices.

"I wrote a book called The War on Ivermectin and the the genesis of that book," he said, adding "Not only is my expertise on Ivermectin and my vast clinical experience, but and I tell the story before, but I got an email, during this journey from a guy named William B Grant, who's a professor out in California, and he wrote to me this email just one day, my life was going totally sideways because our protocols focused on Ivermectin. I was using a lot in my practice, as were tens of thousands of doctors around the world, to really good benefits. And I was getting attacked, hit jobs in the media, and he wrote me this email on and he said, Dear Dr. Kory, what they're doing to Ivermectin, they've been doing to vitamin D for decades..."

"And it's got five tactics. And these are the five tactics that all industries employ when science emerges, that's inconvenient to their interests. And so I'm just going to give you an example. Ivermectin science was extremely inconvenient to the interests of the pharmaceutical industrial complex. I mean, it threatened the vaccine campaign. It threatened vaccine hesitancy, which was public enemy number one. We know that, that everything, all the propaganda censorship was literally going after something called vaccine hesitancy."

Money makes the world go 'round

Carlson then hit on perhaps the most devious aspect of the relationship between drug companies and the medical establishment, and how special interests completely taint science to the point where public distrust of institutions has spiked in recent years.

"I think all of it starts at the level the medical journals," said Kory. "Because once you have something established in the medical journals as a, let's say, a proven fact or a generally accepted consensus, consensus comes out of the journals."

"I have dozens of rejection letters from investigators around the world who did good trials on ivermectin, tried to publish it. No thank you, no thank you, no thank you. And then the ones that do get in all purportedly prove that ivermectin didn't work," Kory continued.

"So and then when you look at the ones that actually got in and this is where like probably my biggest estrangement and why I don't recognize science and don't trust it anymore, is the trials that flew to publication in the top journals in the world were so brazenly manipulated and corrupted in the design and conduct in, many of us wrote about it. But they flew to publication, and then every time they were published, you saw these huge PR campaigns in the media. New York Times, Boston Globe, L.A. times, ivermectin doesn't work. Latest high quality, rigorous study says. I'm sitting here in my office watching these lies just ripple throughout the media sphere based on fraudulent studies published in the top journals. And that's that's that has changed. Now that's why I say I'm estranged and I don't know what to trust anymore."

Vaccine Injuries

Carlson asked Kory about his clinical experience with vaccine injuries.

"So how this is how I divide, this is just kind of my perception of vaccine injury is that when I use the term vaccine injury, I'm usually referring to what I call a single organ problem, like pericarditis, myocarditis, stroke, something like that. An autoimmune disease," he replied.

"What I specialize in my practice, is I treat patients with what we call a long Covid long vaxx. It's the same disease, just different triggers, right? One is triggered by Covid, the other one is triggered by the spike protein from the vaccine. Much more common is long vax. The only real differences between the two conditions is that the vaccinated are, on average, sicker and more disabled than the long Covids, with some pretty prominent exceptions to that."

Watch the entire interview above, and you can support Tucker Carlson's endeavors by joining the Tucker Carlson Network here...

International

Shakira’s net worth

After 12 albums, a tax evasion case, and now a towering bronze idol sculpted in her image, how much is Shakira worth more than 4 decades into her care…

Share this:

Shakira’s considerable net worth is no surprise, given her massive popularity in Latin America, the U.S., and elsewhere.

In fact, the belly-dancing contralto queen is the second-wealthiest Latin-America-born pop singer of all time after Gloria Estefan. (Interestingly, Estefan actually helped a young Shakira translate her breakout album “Laundry Service” into English, hugely propelling her stateside success.)

Since releasing her first record at age 13, Shakira has spent decades recording albums in both Spanish and English and performing all over the world. Over the course of her 40+ year career, she helped thrust Latin pop music into the American mainstream, paving the way for the subsequent success of massively popular modern acts like Karol G and Bad Bunny.

In December 2023, a 21-foot-tall beachside bronze statue of the “Hips Don’t Lie” singer was unveiled in her Colombian hometown of Barranquilla, making her a permanent fixture in the city’s skyline and cementing her legacy as one of Latin America’s most influential entertainers.

After 12 albums, a plethora of film and television appearances, a highly publicized tax evasion case, and now a towering bronze idol sculpted in her image, how much is Shakira worth? What does her income look like? And how does she spend her money?

How much is Shakira worth?

In late 2023, Spanish sports and lifestyle publication Marca reported Shakira’s net worth at $400 million, citing Forbes as the figure’s source (although Forbes’ profile page for Shakira does not list a net worth — and didn’t when that article was published).

Most other sources list the singer’s wealth at an estimated $300 million, and almost all of these point to Celebrity Net Worth — a popular but dubious celebrity wealth estimation site — as the source for the figure.

A $300 million net worth would make Shakira the third-richest Latina pop star after Gloria Estefan ($500 million) and Jennifer Lopez ($400 million), and the second-richest Latin-America-born pop singer after Estefan (JLo is Puerto Rican but was born in New York).

Shakira’s income: How much does she make annually?

Entertainers like Shakira don’t have predictable paychecks like ordinary salaried professionals. Instead, annual take-home earnings vary quite a bit depending on each year’s album sales, royalties, film and television appearances, streaming revenue, and other sources of income. As one might expect, Shakira’s earnings have fluctuated quite a bit over the years.

From June 2018 to June 2019, for instance, Shakira was the 10th highest-earning female musician, grossing $35 million, according to Forbes. This wasn’t her first time gracing the top 10, though — back in 2012, she also landed the #10 spot, bringing in $20 million, according to Billboard.

In 2023, Billboard listed Shakira as the 16th-highest-grossing Latin artist of all time.

How much does Shakira make from her concerts and tours?

A large part of Shakira’s wealth comes from her world tours, during which she sometimes sells out massive stadiums and arenas full of passionate fans eager to see her dance and sing live.

According to a 2020 report by Pollstar, she sold over 2.7 million tickets across 190 shows that grossed over $189 million between 2000 and 2020. This landed her the 19th spot on a list of female musicians ranked by touring revenue during that period. In 2023, Billboard reported a more modest touring revenue figure of $108.1 million across 120 shows.

In 2003, Shakira reportedly generated over $4 million from a single show on Valentine’s Day at Foro Sol in Mexico City. 15 years later, in 2018, Shakira grossed around $76.5 million from her El Dorado World Tour, according to Touring Data.

Related: RuPaul's net worth: Everything to know about the cultural icon and force behind 'Drag Race'

How much has Shakira made from her album sales?

According to a 2023 profile in Variety, Shakira has sold over 100 million records throughout her career. “Laundry Service,” the pop icon’s fifth studio album, was her most successful, selling over 13 million copies worldwide, according to TheRichest.

Exactly how much money Shakira has taken home from her album sales is unclear, but in 2008, it was widely reported that she signed a 10-year contract with LiveNation to the tune of between $70 and $100 million to release her subsequent albums and manage her tours.

How much did Shakira make from her Super Bowl and World Cup performances?

Shakira co-wrote one of her biggest hits, “Waka Waka (This Time for Africa),” after FIFA selected her to create the official anthem for the 2010 World Cup in South Africa. She performed the song, along with several of her existing fan-favorite tracks, during the event’s opening ceremonies. TheThings reported in 2023 that the song generated $1.4 million in revenue, citing Popnable for the figure.

A decade later, 2020’s Superbowl halftime show featured Shakira and Jennifer Lopez as co-headliners with guest performances by Bad Bunny and J Balvin. The 14-minute performance was widely praised as a high-energy celebration of Latin music and dance, but as is typical for Super Bowl shows, neither Shakira nor JLo was compensated beyond expenses and production costs.

The exposure value that comes with performing in the Super Bowl Halftime Show, though, is significant. It is typically the most-watched television event in the U.S. each year, and in 2020, a 30-second Super Bowl ad spot cost between $5 and $6 million.

How much did Shakira make as a coach on “The Voice?”

Shakira served as a team coach on the popular singing competition program “The Voice” during the show’s fourth and sixth seasons. On the show, celebrity musicians coach up-and-coming amateurs in a team-based competition that eventually results in a single winner. In 2012, The Hollywood Reporter wrote that Shakira’s salary as a coach on “The Voice” was $12 million.

Related: John Cena's net worth: The wrestler-turned-actor's investments, businesses, and more

How does Shakira spend her money?

Shakira doesn’t just make a lot of money — she spends it, too. Like many wealthy entertainers, she’s purchased her share of luxuries, but Barranquilla’s barefoot belly dancer is also a prolific philanthropist, having donated tens of millions to charitable causes throughout her career.

Private island

Back in 2006, she teamed up with Roger Waters of Pink Floyd fame and Spanish singer Alejandro Sanz to purchase Bonds Cay, a 550-acre island in the Bahamas, which was listed for $16 million at the time.

Along with her two partners in the purchase, Shakira planned to develop the island to feature housing, hotels, and an artists’ retreat designed to host a revolving cast of artists-in-residence. This plan didn’t come to fruition, though, and as of this article’s last update, the island was once again for sale on Vladi Private Islands.

Real estate and vehicles

Like most wealthy celebs, Shakira’s portfolio of high-end playthings also features an array of luxury properties and vehicles, including a home in Barcelona, a villa in Cyprus, a Miami mansion, and a rotating cast of Mercedes-Benz vehicles.

Philanthropy and charity

Shakira doesn’t just spend her massive wealth on herself; the “Queen of Latin Music” is also a dedicated philanthropist and regularly donates portions of her earnings to the Fundación Pies Descalzos, or “Barefoot Foundation,” a charity she founded in 1997 to “improve the education and social development of children in Colombia, which has suffered decades of conflict.” The foundation focuses on providing meals for children and building and improving educational infrastructure in Shakira’s hometown of Barranquilla as well as four other Colombian communities.

In addition to her efforts with the Fundación Pies Descalzos, Shakira has made a number of other notable donations over the years. In 2007, she diverted a whopping $40 million of her wealth to help rebuild community infrastructure in Peru and Nicaragua in the wake of a devastating 8.0 magnitude earthquake. Later, during the COVID-19 pandemic in 2020, Shakira donated a large supply of N95 masks for healthcare workers and ventilators for hospital patients to her hometown of Barranquilla.

Back in 2010, the UN honored Shakira with a medal to recognize her dedication to social justice, at which time the Director General of the International Labour Organization described her as a “true ambassador for children and young people.”

Shakira’s tax fraud scandal: How much did she pay?

In 2018, prosecutors in Spain initiated a tax evasion case against Shakira, alleging she lived primarily in Spain from 2012 to 2014 and therefore failed to pay around $14.4 million in taxes to the Spanish government. Spanish law requires anyone who is “domiciled” (i.e., living primarily) in Spain for more than half of the year to pay income taxes.

During the period in question, Shakira listed the Bahamas as her primary residence but did spend some time in Spain, as she was dating Gerard Piqué, a professional footballer and Spanish citizen. The couple’s first son, Milan, was also born in Barcelona during this period.

Shakira maintained that she spent far fewer than 183 days per year in Spain during each of the years in question. In an interview with Elle Magazine, the pop star opined that “Spanish tax authorities saw that I was dating a Spanish citizen and started to salivate. It's clear they wanted to go after that money no matter what."

Prosecutors in the case sought a fine of almost $26 million and a possible eight-year prison stint, but in November of 2023, Shakira took a deal to close the case, accepting a fine of around $8 million and a three-year suspended sentence to avoid going to trial. In reference to her decision to take the deal, Shakira stated, "While I was determined to defend my innocence in a trial that my lawyers were confident would have ruled in my favour [had the trial proceeded], I have made the decision to finally resolve this matter with the best interest of my kids at heart who do not want to see their mom sacrifice her personal well-being in this fight."

How much did the Shakira statue in Barranquilla cost?

In late 2023, a 21-foot-tall bronze likeness of Shakira was unveiled on a waterfront promenade in Barranquilla. The city’s then-mayor, Jaime Pumarejo, commissioned Colombian sculptor Yino Márquez to create the statue of the city’s treasured pop icon, along with a sculpture of the city’s coat of arms.

According to the New York Times, the two sculptures cost the city the equivalent of around $180,000. A plaque at the statue’s base reads, “A heart that composes, hips that don’t lie, an unmatched talent, a voice that moves the masses and bare feet that march for the good of children and humanity.”

Related: Taylor Swift net worth: The most successful entertainer joins the billionaire's club

bonds pandemic covid-19 real estate africa mexico spainInternational

Delta Air Lines adds a new route travelers have been asking for

The new Delta seasonal flight to the popular destination will run daily on a Boeing 767-300.

Share this:

{kind=link}

{kind=link}

Those who have tried to book a flight from North America to Europe in the summer of 2023 know just how high travel demand to the continent has spiked.

At 2.93 billion, visitors to the countries making up the European Union had finally reached pre-pandemic levels last year while North Americans in particular were booking trips to both large metropolises such as Paris and Milan as well as smaller cities growing increasingly popular among tourists.

Related: A popular European city is introducing the highest 'tourist tax' yet

As a result, U.S.-based airlines have been re-evaluating their networks to add more direct routes to smaller European destinations that most travelers would have previously needed to reach by train or transfer flight with a local airline.

Shutterstock

Delta Air Lines: ‘Glad to offer customers increased choice…’

By the end of March, Delta Air Lines (DAL) will be restarting its route between New York’s JFK and Marco Polo International Airport in Venice as well as launching two new flights to Venice from Atlanta. One will start running this month while the other will be added during peak demand in the summer.

More Travel:

- A new travel term is taking over the internet (and reaching airlines and hotels)

- The 10 best airline stocks to buy now

- Airlines see a new kind of traveler at the front of the plane

“As one of the most beautiful cities in the world, Venice is hugely popular with U.S. travelers, and our flights bring valuable tourism and trade opportunities to the city and the region as well as unrivalled opportunities for Venetians looking to explore destinations across the Americas,” Delta’s SVP for Europe Matteo Curcio said in a statement. “We’re glad to offer customers increased choice this summer with flights from New York and additional service from Atlanta.”

The JFK-Venice flight will run on a Boeing 767-300 (BA) and have 216 seats including higher classes such as Delta One, Delta Premium Select and Delta Comfort Plus.

Delta offers these features on the new flight

Both the New York and Atlanta flights are seasonal routes that will be pulled out of service in October. Both will run daily while the first route will depart New York at 8:55 p.m. and arrive in Venice at 10:15 a.m. local time on the way there, while leaving Venice at 12:15 p.m. to arrive at JFK at 5:05 p.m. on the way back.

According to Delta, this will bring its service to 17 flights from different U.S. cities to Venice during the peak summer period. As with most Delta flights at this point, passengers in all fare classes will have access to free Wi-Fi during the flight.

Those flying in Delta’s highest class or with access through airline status or a credit card will also be able to use the new Delta lounge that is part of the airline’s $12 billion terminal renovation and is slated to open to travelers in the coming months. The space will take up more than 40,000 square feet and have an outdoor terrace.

“Delta One customers can stretch out in a lie-flat seat and enjoy premium amenities like plush bedding made from recycled plastic bottles, more beverage options, and a seasonal chef-curated four-course meal,” Delta said of the new route. “[…] All customers can enjoy a wide selection of in-flight entertainment options and stay connected with Wi-Fi and enjoy free mobile messaging.”

stocks pandemic european europe

IFM’s Hat Trick and Reflections On Option-To-Buy M&A

Net Zero, The Digital Panopticon, & The Future Of Food

For-profit nursing homes are cutting corners on safety and draining resources with financial shenanigans − especially at midsize chains that dodge public scrutiny

Trump nearly derailed democracy once − here’s what to watch out for in reelection campaign

Riley Gaines Explains How Women’s Sports Are Rigged To Promote The Trans Agenda

‘Excess Mortality Skyrocketed’: Tucker Carlson and Dr. Pierre Kory Unpack ‘Criminal’ COVID Response

Health Officials: Man Dies From Bubonic Plague In New Mexico

MIPIM 2024 Reflects Mixed Feelings on CRE Recovery

The SNF Institute for Global Infectious Disease Research announces new advisory board

Delta Air Lines adds a new route travelers have been asking for

-

Uncategorized3 weeks ago

Uncategorized3 weeks agoAll Of The Elements Are In Place For An Economic Crisis Of Staggering Proportions

-

International7 days ago

International7 days agoEyePoint poaches medical chief from Apellis; Sandoz CFO, longtime BioNTech exec to retire

-

Uncategorized4 weeks ago

Uncategorized4 weeks agoCalifornia Counties Could Be Forced To Pay $300 Million To Cover COVID-Era Program

-

Uncategorized3 weeks ago

Uncategorized3 weeks agoApparel Retailer Express Moving Toward Bankruptcy

-

Uncategorized4 weeks ago

Uncategorized4 weeks agoIndustrial Production Decreased 0.1% in January

-

International7 days ago

International7 days agoWalmart launches clever answer to Target’s new membership program

-

Uncategorized4 weeks ago

Uncategorized4 weeks agoRFK Jr: The Wuhan Cover-Up & The Rise Of The Biowarfare-Industrial Complex

-

Spread & Containment2 days ago

IFM’s Hat Trick and Reflections On Option-To-Buy M&A