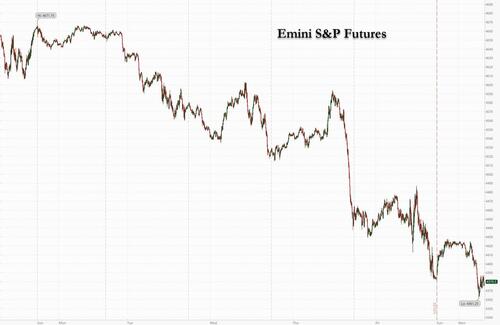

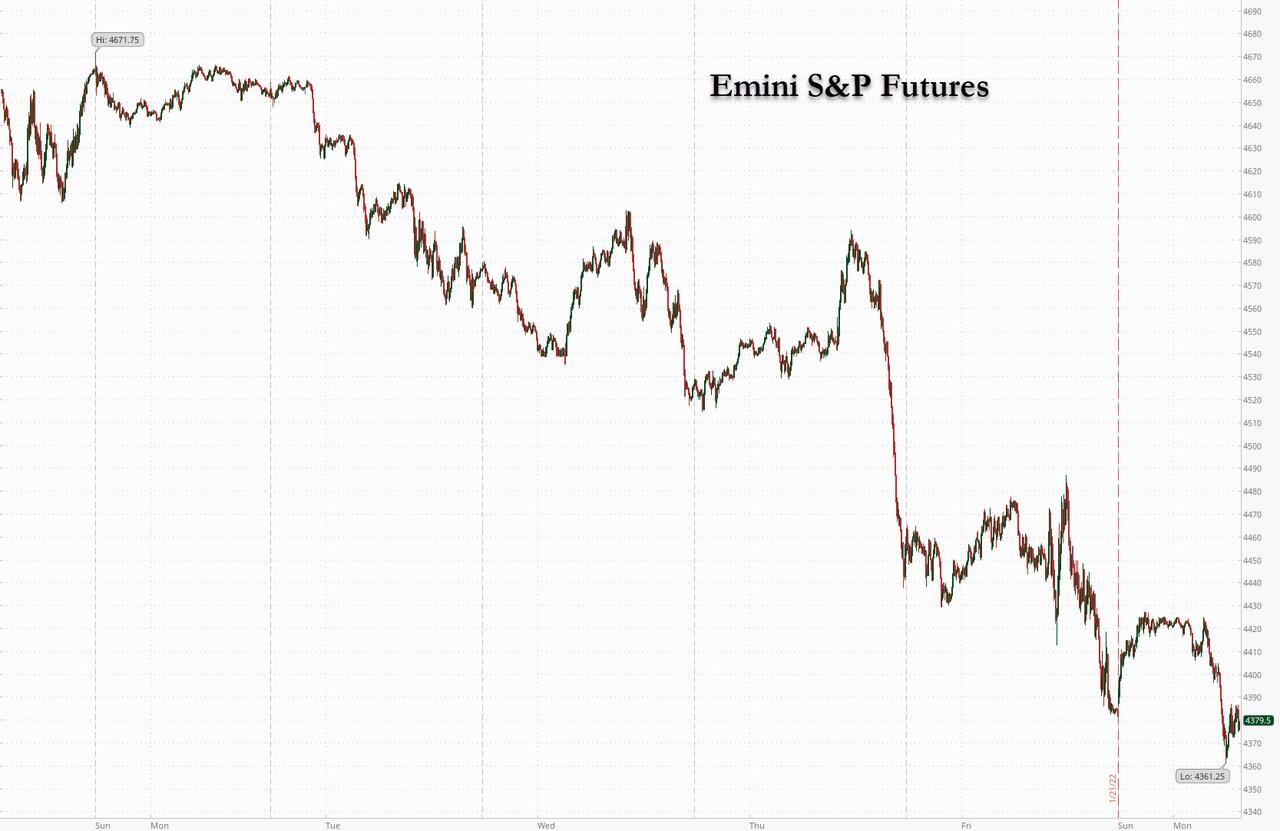

Futures Tumble On Rising Fed Fears, Geopolitical Tensions

Futures Tumble On Rising Fed Fears, Geopolitical Tensions

US stock index futures erased early overnight gains and turned negative, dimming hopes for a rebound after one of the worst stretches for global markets last week since the pandemic…

Futures Tumble On Rising Fed Fears, Geopolitical Tensions

US stock index futures erased early overnight gains and turned negative, dimming hopes for a rebound after one of the worst stretches for global markets last week since the pandemic began, as investors prepared for the upcoming Federal Reserve policy meeting and as the prospect of a war between Russia and Ukraine quashed demand for riskier assets such as bitcoin, and bolstered the dollar and oil. Nasdaq 100 futures declined 0.7% after rising as much as 1.1%. Those on the S&P 500 dropped 17 points or 0.4% while the Dow Jones dropped 0.3%. Elsewhere, the Stoxx Europe 600 fell 2% with travel and leisure as well as technology stocks leading declines. The dollar rose, bond yields dropped and oil was unchanged.

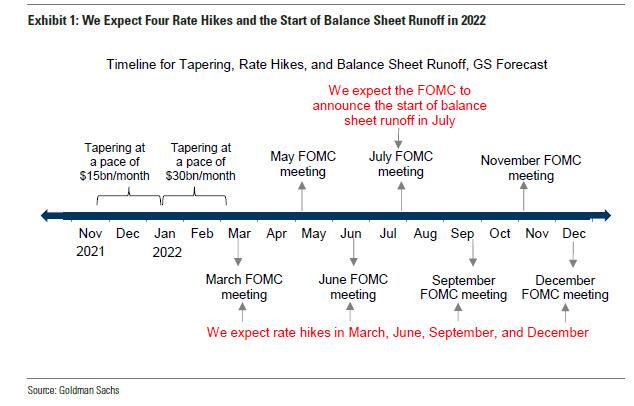

The Fed starts its two-day meeting on Tuesday and is expected to signal the first rate hike since 2018, paving the way for a March increase to fight raging inflation. Those bets have been adding pressure on stocks, which tumbled last week. Meanwhile, tensions are rising over Ukraine between Russia and the U.S. as well as its allies. The US ordered family members of the Kiev embassy to evacuate after a NYT report that Joe Biden may deploy thousands of troops to Eastern Europe. NATO said on Monday it was putting forces on standby and reinforcing eastern Europe with more ships and fighter jets in response to Russia's military build-up at Ukraine's borders. Russia’s benchmark stock index tumbled as much as 6.8%, while the Swiss franc rose to the highest level against the euro in more than six years as investors sought havens.

“Since we are coming off market highs and with higher rates on the horizon, investors are choosing to stand on the sidelines,” said Sharif Farha, a portfolio manager at Safehouse Capital. “I would imagine that in order to bring back some momentum we either need to see strong earnings this quarter or we need some sort of dovish rhetoric from the Fed.”

In U.S. premarket trading, Kohl’s rose as the department-store retailer fields interest from two suitors at the same time as it grapples with multiple activist investors pressuring it to sell. Peloton shares also gained 2.9% following a report that the fitness firm is set to face calls from an activist investor to fire its CEO and pursue a sale. Meanwhile, cryptocurrency-exposed stocks tumbled after massive declines across digital tokens last week. Riot Blockchain (RIOT US) -9.6%, Marathon Digital (MARA US) -9.6%, Bit Digital (BTBT US) -6%. Some other notable developments overnight:

Large tech stocks decline in premarket trading, with the Nasdaq 100 futures pointing to another negative open. Apple (AAPL US) is down -0.7%, Tesla (TSLA US -2.8%).

Arista Networks (ANET US) upgraded to buy from neutral at Citi following more than 17% YTD pullback in the shares through Friday, and with several positive catalysts in the near term. Stock up 1.6% in premarket trading.

Opko Health (OPK US) shares slump 12% in U.S. premarket trading, while Pfizer falls 3.2%, after the companies said the U.S. FDA issued a Complete Response Letter (CRL) for the Biologics License Application for somatrogon.

On Wednesday, the Fed is expected to signal a March hike in interest rates and balance-sheet reduction later this year to help fight inflation. Ebbing stimulus is forcing a rethink about the economic and market outlook. As reported yesterday, Goldman economists said they see a risk the Fed will tighten monetary policy more aggressively this year than the Wall Street bank now anticipates.

There is “likely a longer term rotation toward value stocks measured in quarters, not weeks” unfolding, Julian Emanuel, chief equity and quantitative strategist at Evercore ISI, wrote in a note. “Investors should retain a balanced view, staying patient in committing new capital to equities.”

In Europe, the Euro Stoxx 600 fell 2.1% to its lowest since Dec. 20 and was on track for the biggest two-day slump since June. Indexes in London, Paris and Frankfurt all were down between 1% and 2%. Travel is the weakest Stoxx 600 sector, dropping over 4.5%; only personal care and telecom in green. Tech is among the worst-hit sectors in Europe with the Stoxx Tech Index falling to its lowest level since July 2021 as investors continue a rotation out of pricey stocks ahead of this week’s Fed policy meeting. The subindex falls as much as 4.1%, among the biggest decliners in the Stoxx 600 index (-2.4%). Darktrace shares plunge as much as 10%, while ASML drops as much as 5.4%, OVH -6% and Wise -6.8%.

Earlier in the session, Asian stocks headed for their lowest close in about a month, amid expectations that the Federal Reserve will signal at a meeting Wednesday that it will kick off monetary tightening in March. The MSCI Asia Pacific Index lost as much as 1%, set for the seventh day of declines in eight sessions. Consumer discretionary and financials sectors contributed the most to the slide, with Alibaba Group and Tencent Holdings among the biggest drags. India and Vietnam were the day’s worst performers. “It’s because of the possibility of seeing a more hawkish-than-expected outcome,” said Shogo Maekawa, a strategist at JP Morgan Asset Management in Tokyo, referring to the Fed meeting. “It’s hard for investors to buy tech and growth stocks while the market remains wary over the FOMC meeting, earnings and the U.S. PMI data.” Major benchmarks in Asia are approaching new milestones following recent declines. Japan’s Topix Index is hovering near, while New Zealand has entered, technical correction territory on Monday. Measures for mainland China and South Korea are close to entering a bear market. “If there is any dovish surprise from the Fed, we expect stocks in general to see a relief rally as technical indicators do suggest already cautious positioning,” Nomura strategists including Chetan Seth wrote in a note. “The Fed normalization theme appears quite well entrenched now.”

Japanese equities rose, erasing a morning drop as investors looked toward the Federal Reserve’s monetary policy meeting this week. Banks were the biggest boost to the Topix, which gained 0.1%. Electronics makers dropped. The benchmark swung from a morning loss of as much as 1.2% -- flirting with a correction for a second day -- to an afternoon gain of as much as 0.3%. Tokyo Electron and Fast Retailing were the largest contributors to a 0.2% advance in the Nikkei 225, which also wiped out a 1.2% decline. The yen was slightly weaker after strengthening 0.4% against the dollar Friday. Futures on the Nasdaq 100 climbed as much as 1.1% in Asian trading hours. “Technicals show that Japanese stocks have been oversold, meaning even if there’s temporarily more selling in them, share prices are no longer likely to fall much,” said Masahiko Sato, an equity market analyst at Nomura Securities.

India’s benchmark index headed for its longest streak of losses since March, leading declines in Asia as investors braced for a looming U.S. interest rate hike. The S&P BSE Sensex fell 2.4% to 57,594.68 as of 1:37 p.m. in Mumbai, on course for its 5th day of decline, with all sub-sectors in the red. The NSE Nifty 50 Index slid by a similar magnitude. A gauge of small cap companies was on track for its biggest decline since mid-April. The weakness in Indian stocks is in line with a broader selloff in Asian equities amid concerns over the Federal Reserve’s upcoming tightening. The U.S. central bank is expected to signal a March rate liftoff and balance-sheet reduction later this year at this week’s meeting. “Rising crude oil prices, soaring inflation concerns and the growing possibility of Fed’s rate action being priced in the bond market have triggered selling by foreign institutional investors,” said Yesha Shah, head of research at Samco Securities Ltd. “Investors will remain on the sidelines for the outcome of the Fed’s meeting this week.”

In rates, Treasuries curve were flatter with long-end yields richer by at least 2bp while front-end of the curve continues to lag ahead of Wednesday’s Fed policy decision and auction cycle beginning with 2-year note sale at 1pm ET. Five-and 7-year auctions follow later this week. U.S. 10-year yields around 1.73%, down 2.5bp vs Friday’s close, lag gilts slightly while keeping pace with bunds; with front-end lagging, 2s10s spread approached 70bp, lowest since December 2020, while 5s30s breached 50bp. U.S. Treasury auctions cycle comprises $54b 2-year note, $55b 5-year note Tuesday and $53b 7-year notes Thursday. WI 2-year yield at ~1.050% is higher than auction stops since February 2020 and ~28bp cheaper than last month’s, which tailed by 0.6bp. IG dollar issuance slate expected to be moderate this week, with desks calling for around $20b as more companies emerge from earnings blackout periods.

In FX, the Bloomberg Dollar Spot Index advanced as the greenback traded higher against most of its Group-of-10 peers and the Treasury curve bull flattened, with the shorter tenors staying little changed.The yen reversed an earlier decline and the Swiss franc rose to the highest level against the euro in more than six years Monday, as concern over a possible military confrontation in Ukraine supported demand for haven currencies. The euro slipped against the dollar while European sovereign bonds advanced, outperforming Treasuries. Italian bonds lead peripheral outperformance over euro-area peers as Prime Minister Mario Draghi seals top spot among contenders in presidential elections that begin Monday. Bunds also advanced amid haven buying as stocks slide. Euro-area economic activity increased at its slowest pace in almost a year as infections of the coronavirus’s omicron strain ripped through the services industry, according to a survey of purchasing managers by IHS Markit. The Australian dollar declined ahead of data on Tuesday that’s forecast to show inflation quickened in the fourth quarter. Australian bond yields are primed to set new highs as bets that the central bank will scrap quantitative easing reach a crescendo ahead of a pivotal inflation report.

In commodities, crude futures drift of Asia’s best levels. WTI gives back Asia's gains, dipping into the red back, briefly back below $85. Brent finds support near $87.50. Spot gold adds $4 near $1,840/oz. Base metals trade poorly with risk assets broadly offered. LME nickel drops ~4% lagging peers

On the calendar today, we have the January flash manufacturing, services and composite PMIs from Japan, France, Germany, Euro Area, UK and US, US December Chicago Fed national activity index. IBM reports earnings.

Market Snapshot

S&P 500 futures up 0.3% to 4,402.00

MXAP down 0.7% to 190.48

MXAPJ down 1.1% to 622.96

Nikkei up 0.2% to 27,588.37

Topix up 0.1% to 1,929.87

Hang Seng Index down 1.2% to 24,656.46

Shanghai Composite little changed at 3,524.11

Sensex down 2.7% to 57,441.98

Australia S&P/ASX 200 down 0.5% to 7,139.55

Kospi down 1.5% to 2,792.00

STOXX Europe 600 down 1.4% to 467.84

German 10Y yield little changed at -0.10%

Euro little changed at $1.1334

Brent Futures up 0.3% to $88.11/bbl

Gold spot up 0.4% to $1,842.66

U.S. Dollar Index little changed at 95.70

Top Overnight News from Bloomberg

European Union foreign ministers will discuss Ukraine with U.S. Secretary of State Antony Blinken Monday after Washington ordered family members at its embassy in Kyiv to leave due to the “threat of Russian military action”

The European Union has a lot more to lose than the U.S. from conflict with Russia, explaining why the western allies are finding it hard to agree on a tough stance in the Ukraine standoff

The ECB will need to normalize policy gradually to avoid hurting growth while not acting too late, Bank of France Governor Francois Villeroy de Galhau tells Europe 1 radio in an interview Monday

Inflation hawks are about to get what they want from the Federal Reserve - - which means emerging markets are about to get what they’ve traditionally feared. The prospect of higher U.S. interest rates, which the Fed is promising to deliver this year and next, has typically been a recipe for trouble in developing economies, especially when it results in a stronger dollar

U.K. services firms increased their prices aggressively in January in an attempt to cover rising raw material costs, wages and energy bills, according to a survey of purchasing managers.

China posted strong foreign exchange inflows last year, thanks to record exports and high returns on domestic assets, helping to underpin the yuan’s rally

Turkish Finance Minister Nureddin Nebati told economists he expects the inflation rate to peak at about 40% in the months ahead and not to surpass 50% this year, according to people who attended

Central banks in some of Africa’s biggest economies will likely look past high inflation and U.S. policy tightening and hold interest rates over the coming weeks to shore up their recoveries from the Covid-19 stasis

A more detailed look at global markets courtesy of Newsquawk

In Asian trade, markets were mostly lower after the worst weekly performance on Wall St since the start of the pandemic. ASX 200 (-0.5%) was pressured by losses in mining names and following weaker production by South32. Nikkei 225 (+0.2%) initially fell as more areas sought virus measures but gradually recovered on JPY outflows. Hang Seng (-1.2%) and Shanghai Comp. (+0.1%) were somewhat varied with large tech selling in Hong Kong although the mainland was cushioned after a PBoC liquidity injection and 14-day reverse repo rate cut.

Top Asian News

Asia Stocks Drop to 1-Month Low as Investors Await Fed Meeting

Panasonic to Start Producing New Tesla Batteries in 2023: Nikkei

Beijing Tests Shoppers Buying Fever Drugs to Root Out Covid

Singapore and Indonesia Form Travel Bubble to Spur Economies

In Europe, the Stoxx 600 -2.3% on the session, as sentiment continues to deteriorate following a softer open/APAC handover. Pressure that has seen the NQ flip from the US outperformer to the underperformer, -0.5% In Europe, sectors are all in the red with Telecom the relative outperformer on stock specifics while Travel & Tech names post notable losses.

Top European News

European Power Prices Jump on Low Wind, Rising Russia Tension

U.K.’s Johnson Faces Week That Defines His Political Future

U.K. Services Firms Hike Prices as Material Costs, Wages Climb

Goldman Says Russia Conflict Could Curb Gas Flows Indefinitely

In FX, the dollar was firmer as longs pare back from over extended long base ahead of the Fed and GS flags risks of the FOMC hiking at each meeting this year kicking off in March. Yen and Franc outperform on safe haven grounds. Euro and Pound hampered by mixed to soft preliminary PMIs. Rouble is rattled by heightened concerns about Russia rift with the West over Ukraine. Aussie undermined by mostly contractionary flash PMIs. Yuan goes from strength to strength after PBoC cuts 14 day reverse repo rate, adds more liquidity and sets a firmer CNY midpoint rate.

In commodities, crude benchmarks are softer this morning, albeit, they remain a similar magnitude above overnight lows. Downside in the space comes amid the intensification of pressure seen in Equities this morning; eroding geopolitical driven upside that was in-play overnight. Spot gold and silver are diverging modestly with the yellow metal bid on the risk tone, while silver has continued to dip since it briefly surpassed the 200-DMA at USD 24.59/oz on the 20th. Iraq's Ministry of Electricity announces the suspension of the Iranian electricity and gas line, via Sky News Arabia. Russia's Norilsk Nickel reiterates FY 2022 production guidance; Oktyarbsky and Taimysky mines and the Norilsk concentrator have recovered and are operating at full capacity.

US Event Calendar

8:30am: Dec. Chicago Fed Nat Activity Index, prior 0.37

9:45am: Jan. Markit US Manufacturing PMI, est. 56.6, prior 57.7

9:45am: Jan. Markit US Composite PMI, prior 57.0

9:45am: Jan. Markit US Services PMI, est. 54.8, prior 57.6

DB's Jim Reid concludes the overnight wrap

Given the tough last week for the markets (which we review in the second half of this morning’s edition), this week brings a fascinating double header. Not only do we have the FOMC on Wednesday but we have some notable tech earnings in the form of Apple (Thursday), Tesla (Wednesday) and Microsoft (Tuesday). So plenty of scope for market moving info. Netflix was down -21.8% on Friday taking it to around -34% for the year. The slower than expected subscriber numbers were too blame. I would say to balance this that the new series of Ozark that was released over the weekend was very good!

Asian markets have started the week softer but this is a catch up to Friday's bad DM session with US equity futures now back up. The Kospi (-1.41%), Hang Seng (-0.92%) and Nikkei (-0.16%) are all down. Elsewhere, the Shanghai Composite (+0.20%) and CSI (+0.38%) are mildly higher after the PBOC delivered another rate cut, with the 14-day reverse repo lowered by 10bps to +2.25% ahead of the Lunar New Year holidays which begin on 31 Jan. Futures on the S&P 500 (+0.70%), Nasdaq (+0.75%) and Dow Jones (+0.66%) are all trading up.

Elsewhere this week, we’ll get a first look at how the global economy has fared into the new year (and with Omicron) with the release of the January flash PMIs today. Japan’s Jibun Bank manufacturing PMI edged up to +54.6 overnight, the highest in at least three years from +54.3 in December. However, the survey also showed that the nation’s service sector activity contracted in January for the first time in four months, from +46.6 versus +52.1 in December, as Omicron hit. Returning to the week ahead we'll also look back a bit with the Q4 GDP releases from the US (Thursday), France and Germany (both Friday) as well. Keep an eye out for the initial jobless claims from the US as well, since they’ve deteriorated in recent weeks and that’s one of the most timely indicators we get on the state of the labour market there. The weakness is likely Omicron related and given its on the retreat again this may be temporary. There’ll also be plenty of political developments to look out for as well, including the Italian Presidential election. Geopolitics doesn't always impact markets even if they feel very tense and fraught. However the current Russia/Ukraine situation does seem to be adding to the risk off at the moment and merits close attention. I won’t pretend I know how it’s going to pan out.

As discussed at the top, the main market highlight this week will be the Federal Reserve’s first monetary policy decision of the year on Wednesday, along with Fed Chair Powell’s subsequent press conference. According to our economists, this January meeting is set to be the last before they kick off that hiking cycle, with lift-off set to commence in March as part of the first of 4 hikes this year. However, they’ve also argued (link here) that there’s a tail risk of an even bigger hawkish surprise over the months ahead, with the possibility that the Fed raises rates in March and then goes onto raise rates 6 or 7 times this year. So maybe the calm before the storm. Also watch out to see if the committee want to outline more of their current QT plans. The Q&A could be a popcorn moment for the markets with plenty of questions likely on inflation, the Fed’s hiking path, financial conditions and QT amongst other things.

On the earnings side, the season really ramps up this week, with a number of US Tech companies reporting in particular. In total, we’ve got 106 companies in the S&P 500, along with a further 46 in the STOXX 600 so there’s plenty to look out for. Among the highlights are IBM today. Then tomorrow we’ll hear from Microsoft, Johnson & Johnson, Verizon Communications, NextEra Energy, Texas Instruments, American Express, General Electric and Moderna. On Wednesday, releases will include Tesla, Abbott Laboratories, Intel, AT&T and Boeing. Thursday then sees reports from Apple, Visa, LVMH, Mastercard, Comcast, Danaher, McDonald’s, SAP, UniCredit and Samsung Electronics. Finally on Friday, we’ll hear from Chevron and Caterpillar.

Turning to the political scene, there are a number of events expected this week. First, there’s the Italian Presidential election, with the Italian parliament and regional delegates set to start voting today. Our European economists have produced a guide to this election (link here), and if a president is not elected in the first round of voting, another vote will take place tomorrow, with a vote normally taking place each day until a President has been selected. As they note in the Q&A, since the approval of the Constitution in 1948, it’s taken 9 votes on average over 6 days to elect the President. In the first three rounds, a two-thirds majority is required, but from the fourth round only an absolute majority is needed.

Otherwise, there’ll be a lot of attention on the UK this week, where it’s expected that the long-awaited report by the civil servant Sue Gray will be released looking at allegations of parties having taken place in Downing Street during the pandemic. There isn’t a confirmed date for this yet, but it’s expected to arrive some time this week. Against this backdrop, there has been growing speculation that a vote of no confidence could be called in Prime Minister Johnson’s leadership of the Conservative Party, which will take place if 15% of Conservative MPs submit a letter of no confidence. Some Conservative MPs have already said publicly that they have submitted a letter, and if a vote then took place, it would be a secret ballot among Conservative MPs where a simple majority would then be required to remove Johnson as leader. Brexit will also remain in the headlines, as EU Commission Vice President Maroš Šefčovič will be meeting again with UK Foreign Secretary Liz Truss on Monday regarding the Northern Ireland Protocol. Finally in the UK, there’ll be a further easing of Covid-19 restrictions in England, as from Thursday there will be an end to the requirement for Covid passes at large events, and face coverings will no longer be legally required in any setting.

Elsewhere tomorrow, the IMF will be releasing their latest forecasts for economic growth around the world, with their World Economic Outlook update. These normally generate a few headlines.

Looking back, it was a tough last week for markets. After showing a semblance of stability on most days, the S&P 500 index wound up declining late on many days which helped push the index -5.68% lower on the week (-1.89% Friday). The index fell every day of the holiday-shortened week, and every major sector was lower. This marks the third consecutive weekly decline for the S&P, a feat last accomplished in September 2020. Tech shares were among the worst performing, which drove the NASDAQ down -7.55% this week (-2.72% Friday), bringing it -14.25% below its all-time high, firmly within correction territory. The Vix index of volatility increased +9.9pts (+3.5pts) over the week to 29.1, just below the highs reached on the initial Omicron outbreak.

Staying on the theme of high octane pandemic winners turning down, Bitcoin fell -15.19% on the week, a substantial -11.21% on Friday, and is now down -48.29% from the all time highs.

After faring better than US stocks most of the week, European stocks turned for the worst on Friday, with the STOXX 600 declining -1.84%, bringing its weekly return to -1.40%. The DAX and CAC met a similar fate, declining -1.94% and -1.75% Friday, respectively, and dropping -1.76% and -1.04% over the week.

Nominal sovereign yields were a bit more calm but did rally hard after 10yr treasury yields touched multi-year highs of 1.90% intraweek. They ending the week -2.4bps lower (-4.4bps Friday) at 1.76%. Though the real story in yields remains the continued march higher in real yields, with real 10yr yields increasing +9.6bps over the week (+1.9bps Friday) on the anticipated tightening of monetary policy and financial conditions. The climb in real yields has undoubtedly been a big driver of equity weakness.

In Europe, sovereign yields didn’t see the same ranges. 10yr bunds fell -1.9bps (-4.1bps Friday) to -0.065% after touching +0.02% midweek. 10yr gilts increased +2.1bps over the week even after falling -5.4bps Friday. The curve flattening in the UK proved more interesting, with 2yr gilts climbing +8.6bps (-1.7bps Friday), as tighter rate policy at the BoE was priced in following the highest UK CPI readings since 1992. The probability of a rate hike coming at the February MPC climbed to 92%.

Staying with fixed income, credit has proved to be a lot more resilient relative to equities, Friday did see spreads finally start to “catch up” though. HY spreads were +19bps wider in USD and +7bps wider in EUR. IG spreads were also +3bps wider in USD and +1bp wider in EUR. In terms of what that means YTD, USD HY is +19bps wider and IG +5bps with Friday accounting for all of the widening in HY and most of it in IG. In the EUR market, HY is +10bps wider and +3bps wider in IG.

Higher rates weren’t the only driver of poor equity prices last week. The first full week of fourth-quarter earnings in the US drew heavy representation from the financial sector. Financial results were mixed, but a common theme was a retreat in FICC trading profits while many companies reported rising cost pressures. As already discussed Netflix's results didn't help alongside Peleton's publicly discussed difficulties (-24.3% YTD).

Finally Oil ended the week off the highs last seen in 2014 on Wednesday, but Brent was still +2.13% on week.

Mathematicians use AI to identify emerging COVID-19 variants

Scientists at The Universities of Manchester and Oxford have developed an AI framework that can identify and track new and concerning COVID-19 variants…

Scientists at The Universities of Manchester and Oxford have developed an AI framework that can identify and track new and concerning COVID-19 variants and could help with other infections in the future.

Scientists at The Universities of Manchester and Oxford have developed an AI framework that can identify and track new and concerning COVID-19 variants and could help with other infections in the future.

The framework combines dimension reduction techniques and a new explainable clustering algorithm called CLASSIX, developed by mathematicians at The University of Manchester. This enables the quick identification of groups of viral genomes that might present a risk in the future from huge volumes of data.

The study, presented this week in the journal PNAS, could support traditional methods of tracking viral evolution, such as phylogenetic analysis, which currently require extensive manual curation.

Roberto Cahuantzi, a researcher at The University of Manchester and first and corresponding author of the paper, said: “Since the emergence of COVID-19, we have seen multiple waves of new variants, heightened transmissibility, evasion of immune responses, and increased severity of illness.

“Scientists are now intensifying efforts to pinpoint these worrying new variants, such as alpha, delta and omicron, at the earliest stages of their emergence. If we can find a way to do this quickly and efficiently, it will enable us to be more proactive in our response, such as tailored vaccine development and may even enable us to eliminate the variants before they become established.”

Like many other RNA viruses, COVID-19 has a high mutation rate and short time between generations meaning it evolves extremely rapidly. This means identifying new strains that are likely to be problematic in the future requires considerable effort.

Currently, there are almost 16 million sequences available on the GISAID database (the Global Initiative on Sharing All Influenza Data), which provides access to genomic data of influenza viruses.

Mapping the evolution and history of all COVID-19 genomes from this data is currently done using extremely large amounts of computer and human time.

The described method allows automation of such tasks. The researchers processed 5.7 million high-coverage sequences in only one to two days on a standard modern laptop; this would not be possible for existing methods, putting identification of concerning pathogen strains in the hands of more researchers due to reduced resource needs.

Thomas House, Professor of Mathematical Sciences at The University of Manchester, said: “The unprecedented amount of genetic data generated during the pandemic demands improvements to our methods to analyse it thoroughly. The data is continuing to grow rapidly but without showing a benefit to curating this data, there is a risk that it will be removed or deleted.

“We know that human expert time is limited, so our approach should not replace the work of humans all together but work alongside them to enable the job to be done much quicker and free our experts for other vital developments.”

The proposed method works by breaking down genetic sequences of the COVID-19 virus into smaller “words” (called 3-mers) represented as numbers by counting them. Then, it groups similar sequences together based on their word patterns using machine learning techniques.

Stefan Güttel, Professor of Applied Mathematics at the University of Manchester, said: “The clustering algorithm CLASSIX we developed is much less computationally demanding than traditional methods and is fully explainable, meaning that it provides textual and visual explanations of the computed clusters.”

Roberto Cahuantzi added: “Our analysis serves as a proof of concept, demonstrating the potential use of machine learning methods as an alert tool for the early discovery of emerging major variants without relying on the need to generate phylogenies.

“Whilst phylogenetics remains the ‘gold standard’ for understanding the viral ancestry, these machine learning methods can accommodate several orders of magnitude more sequences than the current phylogenetic methods and at a low computational cost.”

Journal

Proceedings of the National Academy of Sciences

DOI

10.1073/pnas.2317284121

Article Title

Unsupervised identification of significant lineages of SARS-CoV-2 through scalable machine learning methods

While the size of the United States makes it hard for it to compete with the inter-city train access available in places like Japan and many European countries, Amtrak trains are a very popular transportation option in certain pockets of the country — so much so that the country’s national railway company is expanding its Northeast Corridor by more than one million seats.

Running from Boston all the way south to Washington, D.C., the route is one of the most popular as it passes through the most densely populated part of the country and serves as a commuter train for those who need to go between East Coast cities such as New York and Philadelphia for business.

Veronika Bondarenko captured this photo of New York’s Moynihan Train Hall.

Veronika Bondarenko

Amtrak launches new routes, promises travelers ‘additional travel options’

Earlier this month, Amtrak announced that it was adding four additional Northeastern routes to its schedule — two more routes between New York’s Penn Station and Union Station in Washington, D.C. on the weekend, a new early-morning weekday route between New York and Philadelphia’s William H. Gray III 30th Street Station and a weekend route between Philadelphia and Boston’s South Station.

According to Amtrak, these additions will increase Northeast Corridor’s service by 20% on the weekdays and 10% on the weekends for a total of one million additional seats when counted by how many will ride the corridor over the year.

“More people are taking the train than ever before and we’re proud to offer our customers additional travel options when they ride with us on the Northeast Regional,” Amtrak Executive Vice President and Chief Commercial Officer Eliot Hamlisch said in a statement on the new routes. “The Northeast Regional gets you where you want to go comfortably, conveniently and sustainably as you breeze past traffic on I-95 for a more enjoyable travel experience.”

Here are some of the other Amtrak changes you can expect to see

Amtrak also said that, in the 2023 financial year, the Northeast Corridor had nearly 9.2 million riders — 8% more than it had pre-pandemic and a 29% increase from 2022. The higher demand, particularly during both off-peak hours and the time when many business travelers use to get to work, is pushing Amtrak to invest into this corridor in particular.

To reach more customers, Amtrak has also made several changes to both its routes and pricing system. In the fall of 2023, it introduced a type of new “Night Owl Fare” — if traveling during very late or very early hours, one can go between cities like New York and Philadelphia or Philadelphia and Washington. D.C. for $5 to $15.

As travel on the same routes during peak hours can reach as much as $300, this was a deliberate move to reach those who have the flexibility of time and might have otherwise preferred more affordable methods of transportation such as the bus. After seeing strong uptake, Amtrak added this type of fare to more Boston routes.

The largest distances, such as the ones between Boston and New York or New York and Washington, are available at the lowest rate for $20.

I am a conservation biologist who studies emerging infectious diseases. When people ask me what I think the next pandemic will be I often say that we are in the midst of one – it’s just afflicting a great many species more than ours.

I am referring to the highly pathogenic strain of avian influenza H5N1 (HPAI H5N1), otherwise known as bird flu, which has killed millions of birds and unknown numbers of mammals, particularly during the past three years.

This is the strain that emerged in domestic geese in China in 1997 and quickly jumped to humans in south-east Asia with a mortality rate of around 40-50%. My research group encountered the virus when it killed a mammal, an endangered Owston’s palm civet, in a captive breeding programme in Cuc Phuong National Park Vietnam in 2005.

How these animals caught bird flu was never confirmed. Their diet is mainly earthworms, so they had not been infected by eating diseased poultry like many captive tigers in the region.

This discovery prompted us to collate all confirmed reports of fatal infection with bird flu to assess just how broad a threat to wildlife this virus might pose.

This is how a newly discovered virus in Chinese poultry came to threaten so much of the world’s biodiversity.

Until December 2005, most confirmed infections had been found in a few zoos and rescue centres in Thailand and Cambodia. Our analysis in 2006 showed that nearly half (48%) of all the different groups of birds (known to taxonomists as “orders”) contained a species in which a fatal infection of bird flu had been reported. These 13 orders comprised 84% of all bird species.

We reasoned 20 years ago that the strains of H5N1 circulating were probably highly pathogenic to all bird orders. We also showed that the list of confirmed infected species included those that were globally threatened and that important habitats, such as Vietnam’s Mekong delta, lay close to reported poultry outbreaks.

Mammals known to be susceptible to bird flu during the early 2000s included primates, rodents, pigs and rabbits. Large carnivores such as Bengal tigers and clouded leopards were reported to have been killed, as well as domestic cats.

Our 2006 paper showed the ease with which this virus crossed species barriers and suggested it might one day produce a pandemic-scale threat to global biodiversity.

In the past couple of years, bird flu has spread rapidly across Europe and infiltrated North and South America, killing millions of poultry and a variety of bird and mammal species. A recent paper found that 26 countries have reported at least 48 mammal species that have died from the virus since 2020, when the latest increase in reported infections started.

Not even the ocean is safe. Since 2020, 13 species of aquatic mammal have succumbed, including American sea lions, porpoises and dolphins, often dying in their thousands in South America. A wide range of scavenging and predatory mammals that live on land are now also confirmed to be susceptible, including mountain lions, lynx, brown, black and polar bears.

The UK alone has lost over 75% of its great skuas and seen a 25% decline in northern gannets. Recent declines in sandwich terns (35%) and common terns (42%) were also largely driven by the virus.

Scientists haven’t managed to completely sequence the virus in all affected species. Research and continuous surveillance could tell us how adaptable it ultimately becomes, and whether it can jump to even more species. We know it can already infect humans – one or more genetic mutations may make it more infectious.

At the crossroads

Between January 1 2003 and December 21 2023, 882 cases of human infection with the H5N1 virus were reported from 23 countries, of which 461 (52%) were fatal.

Of these fatal cases, more than half were in Vietnam, China, Cambodia and Laos. Poultry-to-human infections were first recorded in Cambodia in December 2003. Intermittent cases were reported until 2014, followed by a gap until 2023, yielding 41 deaths from 64 cases. The subtype of H5N1 virus responsible has been detected in poultry in Cambodia since 2014. In the early 2000s, the H5N1 virus circulating had a high human mortality rate, so it is worrying that we are now starting to see people dying after contact with poultry again.

It’s not just H5 subtypes of bird flu that concern humans. The H10N1 virus was originally isolated from wild birds in South Korea, but has also been reported in samples from China and Mongolia.

Recent research found that these particular virus subtypes may be able to jump to humans after they were found to be pathogenic in laboratory mice and ferrets. The first person who was confirmed to be infected with H10N5 died in China on January 27 2024, but this patient was also suffering from seasonal flu (H3N2). They had been exposed to live poultry which also tested positive for H10N5.

Species already threatened with extinction are among those which have died due to bird flu in the past three years. The first deaths from the virus in mainland Antarctica have just been confirmed in skuas, highlighting a looming threat to penguin colonies whose eggs and chicks skuas prey on. Humboldt penguins have already been killed by the virus in Chile.

How can we stem this tsunami of H5N1 and other avian influenzas? Completely overhaul poultry production on a global scale. Make farms self-sufficient in rearing eggs and chicks instead of exporting them internationally. The trend towards megafarms containing over a million birds must be stopped in its tracks.

To prevent the worst outcomes for this virus, we must revisit its primary source: the incubator of intensive poultry farms.

Diana Bell does not work for, consult, own shares in or receive funding from any company or organisation that would benefit from this article, and has disclosed no relevant affiliations beyond their academic appointment.

We use cookies on our website to give you the most relevant experience by remembering your preferences and repeat visits. By clicking “Accept”, you consent to the use of ALL the cookies.

This website uses cookies to improve your experience while you navigate through the website. Out of these, the cookies that are categorized as necessary are stored on your browser as they are essential for the working of basic functionalities of the website. We also use third-party cookies that help us analyze and understand how you use this website. These cookies will be stored in your browser only with your consent. You also have the option to opt-out of these cookies. But opting out of some of these cookies may affect your browsing experience.

Necessary cookies are absolutely essential for the website to function properly. These cookies ensure basic functionalities and security features of the website, anonymously.

Cookie

Duration

Description

cookielawinfo-checbox-analytics

11 months

This cookie is set by GDPR Cookie Consent plugin. The cookie is used to store the user consent for the cookies in the category "Analytics".

cookielawinfo-checbox-functional

11 months

The cookie is set by GDPR cookie consent to record the user consent for the cookies in the category "Functional".

cookielawinfo-checbox-others

11 months

This cookie is set by GDPR Cookie Consent plugin. The cookie is used to store the user consent for the cookies in the category "Other.

cookielawinfo-checkbox-necessary

11 months

This cookie is set by GDPR Cookie Consent plugin. The cookies is used to store the user consent for the cookies in the category "Necessary".

cookielawinfo-checkbox-performance

11 months

This cookie is set by GDPR Cookie Consent plugin. The cookie is used to store the user consent for the cookies in the category "Performance".

viewed_cookie_policy

11 months

The cookie is set by the GDPR Cookie Consent plugin and is used to store whether or not user has consented to the use of cookies. It does not store any personal data.

Functional cookies help to perform certain functionalities like sharing the content of the website on social media platforms, collect feedbacks, and other third-party features.

Performance cookies are used to understand and analyze the key performance indexes of the website which helps in delivering a better user experience for the visitors.

Analytical cookies are used to understand how visitors interact with the website. These cookies help provide information on metrics the number of visitors, bounce rate, traffic source, etc.

Advertisement cookies are used to provide visitors with relevant ads and marketing campaigns. These cookies track visitors across websites and collect information to provide customized ads.

{kind=link}