Futures Tumble, Europe In Bear Market As Oil, Gold Soar

Futures Tumble, Europe In Bear Market As Oil, Gold Soar

Not much has changed since our market update last night which saw all risk assets…

Share this:

Not much has changed since our market update last night which saw all risk assets collapse and in many cases set to open in bear markets, amid a soaring panic that the US will impose a unilateral oil embargo on Russia leading to an energy supply shock and global stagflation, while safe havens such as gold, treasuries, and the dollar are exploding higher not to mention crude which was last trading at $125 after briefly rising above $139 at the start of the session. Commodities from grains, metals have also surged on concerns of chaos in raw-material flows due to the invasion and sanctions on Russia that are turning the resources powerhouse into a global pariah. Commodity-linked currencies strengthened.

S&P 500 e-mini futures were down as much as 2.1% earlier before trading 1% lower 7am in New York after a faint glimmer of hope of de-escalation when the following headlines hit Reuters:

- KREMLIN SPOKESMAN SAYS UKRAINE MUST AMEND CONSTITUTION AND REJECT CLAIMS TO ENTER ANY BLOC

- UKRAINE MUST RECOGNISE CRIMEA AS RUSSIAN, AND DONETSK AND LUGANSK AS INDEPENDENT STATES

- IF THESE CONDITIONS ARE MET, THEN RUSSIAN MILITARY ACTION WILL ‘STOP IN A MOMENT’ - SPOKESMAN

And now we wait for the latest Ukranian refusal of these conditions. Meanwhile Nasdaq futures retreated 1.7%. Brent oil was up as much as 18% today, trading around $125 a barrel as the Biden administration is considering whether to prohibit Russian oil imports into the U.S. without participation of allies in Europe, at least initially, according to a Bloomberg report.

“For the U.S. economy, we now see stagflation, with persistently higher inflation and less economic growth than expected before the war,” Ed Yardeni, president of Yardeni Research, wrote in a note. “For stock investors, we think 2022 will continue to be one of this bull market’s toughest years.”

Travel stocks were down in premarket trading, with airlines dropping as a surge in oil prices stokes worries over higher jet fuel costs. American Airlines Group (AAL US) -3.2%, Delta Air Lines (DAL US) -3%. On the other end, U.S. energy shares soared as crude oil prices soar after the U.S. said it was considering curbs on imports of Russian oil. Exxon (XOM US), Chevron (CVX US), Marathon Oil (MRO US) are all up about 3% as WTI crude futures gain 6.4% to $123.02 a barrel. Cryptocurrency-exposed stocks could be active on Monday as digital currencies including Bitcoin slide alongside risk assets such as stocks. Watch Coinbase (COIN US), Riot Blockchain (RIOT US), Marathon Digital (MARA US). Banks stocks slumped in premarket trading, pushing their recent rout to a third day. In corporate news, banking and credit card technology unicorn Zeta Services has raised $30 million from investors including Mastercard. Meanwhile, American Express says it is suspending its operations in Russia and Belarus. Bed Bath & Beyond (BBBY US) shares exploded as much as 75% after RC Ventures, an investment firm started by GameStop Chairman Ryan Cohen, disclosed a large stake in the retailer, while pushing it to explore a sale of the company.

“While the Russian aggression in Ukraine continues the risk of a further escalation keeps investors unsettled. Soaring energy prices are at the heart of economic vulnerabilities,” said Thomas Hempell, head of macro and market research at Generali Investments. “Price pressures are compounded by mounting risk of supply chain disruptions as Russian firms are cut off financially and cargo traffic is curtailed.”

Late on Sunday Bloomberg reported that the Biden administration is considering whether to ban the import of Russian oil and energy products unilaterally, a move that could add to economic pressure as more companies pull out of the country in response to Moscow’s invasion of Ukraine. High energy prices threaten to stall global growth, a risk that is sending tremors across markets.

The commodity supply shock comes as the global economy was already struggling with high inflation due to the pandemic. The Federal Reserve and other key central banks now face the tricky task of tightening monetary policy to contain the cost of living without upending economic expansion or roiling risky assets.

Meanwhile, traders piled into options that oil could surge even further after rising to the highest since 2008, with many adding to calls that Brent futures will rise above $200 before the end of March. For those who missed the key developments over the weekend and overnight, here is a recap of the latest Russian energy/economic updates, courtesy of Newsquawk

- US Secretary of State Blinken said the US and allies are in active discussions regarding a Russian oil import ban and reports later stated the US is weighing acting without allies on a ban of Russian oil imports, although the timing and scope of any ban is still fluid, according to Bloomberg.

- US House Speaker Pelosi said the House is exploring legislation to ban the import of Russian oil.

- Japan is in talks with the US and Europe regarding a Russian oil embargo, according to Kyodo.

- Russian Kremlin spokesman Peskov said there will be a reaction to the economic banditry they are seeing and that a ban on Russian oil risks the most serious market impact, while Peskov added that NATO is aware it cannot get directly involved in Ukraine. Kremlin also stated that companies will return to Russia and invest one day.

- Russia said it is to service and pay Russian bonds fully on time but stated that payments on debts to foreign residents will depend on limits imposed by foreign states.

- American Express (AXP) suspends operations in Russia and Belarus which is due to the Russian attack on the people of Ukraine. Visa (V) and Mastercard (MA) are also to suspend operations in Russia in which Visa noted that all transactions initiated with Visa cards issued in Russia will no longer work outside the country and Mastercard said cards issued by Russian banks will no longer be supported by its network. However, Russia’ s largest lender Sberbank noted that the Visa and Mastercards it issued will continue to work in Russia, according to Tass.

- Banks in Russia are rapidly trying to move to the Chinese UnionPay's system and its own Mir network after Visa and Mastercard suspended operations in Russia

- VTB Bank is preparing to pull out of Europe, according to FT.

- PwC is to separate its Russian firm from the rest of its global network which affects 3,700 partners and staff in the country.

- TikTok limited services in Russia due to the 'Fake News' law and Netflix (NFLX) also decided to suspend its service in Russia.

- Moody’s downgraded Russia’s sovereign ratings from B3 to CA; Outlook Negative, while it cut Ukraine’s sovereign rating two notches from B3 to Caa2.

- Ukraine introduced export licences for key agricultural commodities including wheat, corn and sunflower oil.

And here is the latest in the ongoing discussions and negotiations:

- Russia-Ukraine discussions to commence at 12:00GMT/07:00EST on Monday, according to Russian State TV citing Belta; Russian delegation has arrived for the discussions; subsequently, Ukraine Presidential Adviser says new talks with Russia will start at 14:00GMT/09:00EST.

- Russian & Ukraine Foreign Ministers are to meet in Antalya, Turkey, according to the Turkish Foreign Minister; meeting will occur on Thursday.

- Ukrainian Foreign Minister Kuleba said he doesn’t see progress in peace talks with Russia but have to continue talking, while he talked to US Secretary of State Blinken about providing more weapons to Ukrainian fighters and implementing more sanctions against Russia. Furthermore, US Secretary of State Blinken said unprecedented pressure on Russia will increase until the war with Ukraine is brought to an end, according to Reuters.

- Russian President Putin warned that they would consider any third-party declaration of a no-fly zone over Ukraine as participation in the armed conflict and said western sanctions are akin to a declaration of war, while he added there is no reason to declare martial law in Russia.

- Russian President Putin held a call with Turkish President Erdogan in which Putin said Russia is ready for dialogue with Ukraine and foreign partners, while he added that the military operation in Ukraine is going according to plan and any attempt to draw out the negotiation process will fail.

- Russian President Putin and French President Macron held a call on Sunday in which Putin told Macron that he agreed to talks between the IAEA, Ukraine and Russia to ensure security at nuclear sites.

- Russian Defence Ministry said the use of airfields of other countries by Ukraine airforce may be considered as participation of those countries in the conflict, according to Interfax.

- Russian Foreign Ministry said Britain has chosen to move towards open confrontation with Russia and that Russia will respond which will undoubtedly undermine British interests in Russia.

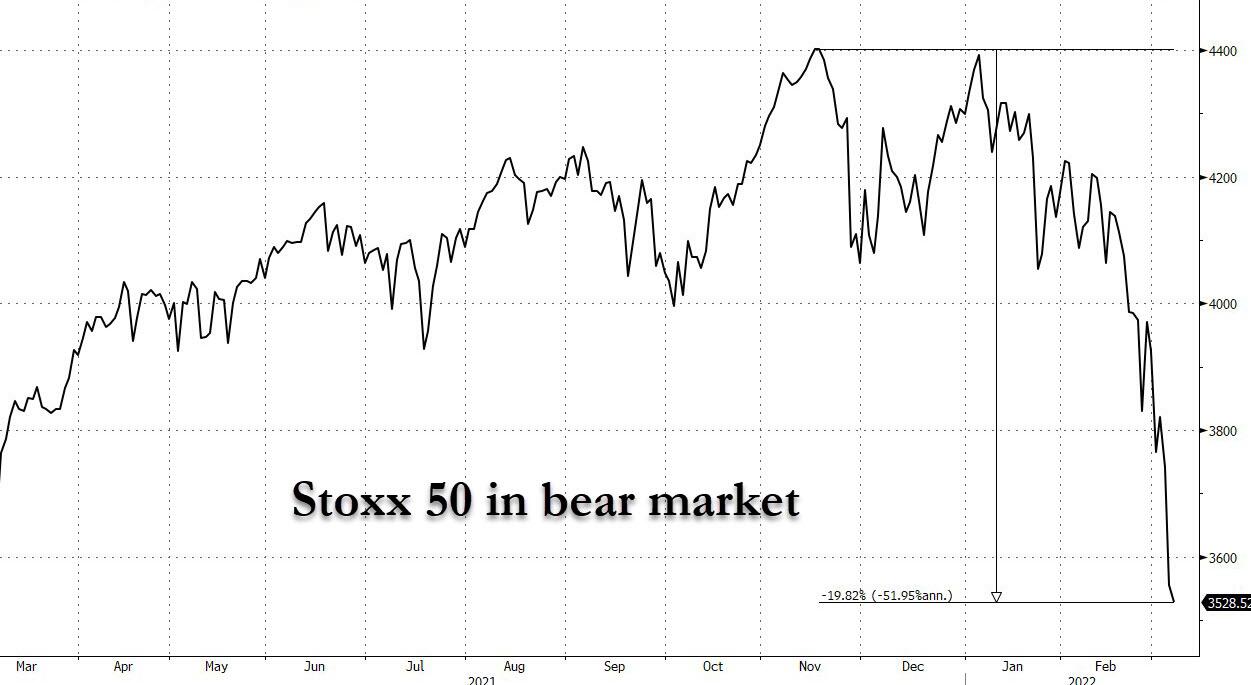

European equities were hit hard at the open with focus turning to the inflationary impact of elevated energy and the subsequent dent to global trade. Cash indexes are deep in the red, Euro Stoxx 50 down as much as 4.75%, DAX and CAC drop 5%; FTSE MIB lags, cratering as much as 6.25%. As BBG's Heather Burke notes, the Euro Stoxx 50 has slid more than 20% from its November high, poised for a technical bear market at the close, with similar moves seen in major European regional benchmarks. Banks, retail, autos and travel are the biggest decliners as investors worry about Russia exposure and the prospects of higher inflation and slower growth. Energy and miners are in the green as commodities soar. Over 90% of Stoxx 600 members are down. U.S. futures’ declines are also picking up. Energy and banks had benefited from gains in value stocks; through mid-February they were the two best Stoxx 600 performers.

Banks, autos and retail names are the hardest hit; energy and mining stocks hold in positive territory with the commodities well bid. European banks declined 8% to lowest level since February 2021 amid a global sell-off spurred by concerns that surging oil prices will slow global growth. The Stoxx 600 Banks Index was the worst-performing sector in Europe, with all 39 members declining. Russia exposed banks were all down double digits: UniCredit -12%, Commerzbank -12%, Societe Generale -11%, Deutsche Bank -10%, while Raiffeisen fell as much as 13% down, to lowest level since June 2016. Energy and miners are now the only two sectors in the green ytd as oil trades near $130 and metals spike. Banks, on the other hand, have been pressured by Russia exposure, falling bond yields and economic uncertainty and how that will affect monetary policy. The ratio between European energy and banks has risen to the highest since April 2020 and can easily surpass the March 2020 pandemic peak.

Here are some of the biggest European movers today:

- European energy and basic resources stocks surged in the face of a broader equity-market rout as commodity prices extended gains amid concerns that the war in Ukraine may spur a supply shock, with Lundin Energy, Shell, Equinor and Galp Energia all up 6% or more.

- European defense companies, including BAE Systems and Thales, are also among Monday’s gainers, as Russian President Vladimir Putin reiterated over the weekend that the war will continue.

- Clarkson shares jump as much as 8.8% after Liberum said the shipping services provider made the most of strong markets in its broking and financial segments.

- Pearson is the only member of the Stoxx 600 media index, as UBS upgrades to neutral from sell, saying the stock could advance by more than 50% if the company can deliver 2025 targets.

- The Automobiles & Parts subindex is the worst-performing subindex on the Stoxx 600, dropping 5%. Finland’s Nokian Renkaat, which is heavily exposed to Russia, leads losses.

- European bank stocks declined to their lowest level since February 2021, led by losses for banks with exposure to eastern Europe, such as Erste Group Bank and PKO Bank, both dropping more than 11%.

- Luxury stocks slumped as store closures in Russia dented earnings prospects for the group while the oil price surge also added to pessimism over the economic outlook.

- Airline stocks also took a beating from Brent oil’s climb, signaling a further increase in costs for the aviation sector, with Wizz Air -11% and International Consolidated Air -7.9% leading losses.

- Inditex shares dropped as Credit Suisse said the clothes retailer may struggle to deliver medium-term growth, cutting its PT for the Spanish retailer to a new street low.

- Jupiter Fund Management shares hit their lowest since April 2020. Stock is cut to hold from add at Peel Hunt, which now expects net outflows to continue into FY22 for the asset manager.

- Oxford Instruments shares drop as much as 24

Earlier in the session, APAC stocks declined as geopolitical concerns lingered ahead of the third round of Ukraine-Russia talks and after evacuation attempts over the weekend in Mariupol were halted amid a ceasefire breach, while the US and allies are engaged in a “very active discussion” regarding a Russian oil embargo. ASX 200 weakened as tech led the declines across most industries aside from the commodity-related sectors which were boosted by a spike in oil and supply squeeze concerns across the metals complex. Nikkei 225 suffered a near-1000 point intraday loss with notable weakness in autos and airlines stocks. Hang Seng and Shanghai Comp. conformed to the risk aversion after China set its lowest growth target in 30 years at 'around 5.5%' and with mixed Chinese trade data also failing to inspire a turnaround.

In rates, treasuries have erased their opening gains, when futures gapped higher when Asia session began. Short-dated yields lead the move, higher by nearly ~5bp. Yields were higher across the curve, 10-year by 4.3bp at 1.77%; during Asia session it declined as much as 6.5bp to 1.666%, lowest since Jan. 5 and just above its 100-DMA, which has held since end of last year. TIPS yields little changed, outperforming after oil’s surge to 2008 levels above $130. In Europe, curves were mixed as Germany bull flattens with the short end ~3bps richer. Peripheral spreads widened, short end Spain and Italy snap ~8bps wider. Core European bonds advanced in the front end while peripherals slumped; Germany’s 10-year breakeven rate jumped to a record high. Euro 5y5y inflation swaps ramp up ~14bps near 2.24%, German 10y breakevens print a record high near 2.4%.

In FX, the Bloomberg Dollar Spot Index rallied 0.6% back above 1,200 as a selloff of European currencies continued; Treasuries were a tad lower. Australian, New Zealand and Canadian dollars rose as they benefited from rallying commodity prices, while Poland’s zloty and Hungary’s forint tumbled to all-time lows against the euro and Sweden’s krona fell below 10 per dollar for the first time since April 2020. The euro slid to 1.0822, its weakest level in almost two years against the greenback and three-month 25 delta risk reversals on EUR/USD showed the biggest bias to puts since the European debt crisis. The common currency slipped below parity with the Swiss franc for the first time since January 2015. It erased the losses on speculation that the SNB was intervening.

The pound slumped to the lowest since December and Gilt yields rose by up to 7bps, led by the front end. Australian and New Zealand dollars gained as much as 1% each, before paring, amid the spike in oil and as iron ore jumped on Chinese stimulus hopes. The yen dropped for the first time in three days on concern higher energy prices will weigh on Japan’s trade balance.

In commodities, Brent and WTI hold roughly half of their gains; Brent trades near $125 having surged on to a $139-handle in early Asia triggered by reports that the U.S. was discussing a ban on Russian crude imports. Base metals skyrocket: LME nickel surges ~30%, palladium hits an all-time high. Spot gold trades near $2,000/oz.

The Indian rupee fell to a record low as crude oil prices surged to the highest since 2008, stoking fears about inflation and finances for the net-energy importer. Bonds also declined. USD/INR rose 1% on Monday to 76.9662 after climbing to 76.9812 earlier.

Bitcoin remains subdued and sub-USD 40k after losing the handle towards the tail-end of last week.

Market Snapshot

- S&P 500 futures down 1.6% to 4,259.25

- STOXX Europe 600 down 3.0% to 409.12

- MXAP down 2.8% to 173.52

- MXAPJ down 2.7% to 567.72

- Nikkei down 2.9% to 25,221.41

- Topix down 2.8% to 1,794.03

- Hang Seng Index down 3.9% to 21,057.63

- Shanghai Composite down 2.2% to 3,372.86

- Sensex down 2.9% to 52,756.70

- Australia S&P/ASX 200 down 1.0% to 7,038.59

- Kospi down 2.3% to 2,651.31

- German 10Y yield little changed at -0.06%

- Euro down 0.6% to $1.0865

- Brent Futures up 6.4% to $125.64/bbl

- Gold spot up 1.3% to $1,995.63

- U.S. Dollar Index up 0.39% to 99.03

Top Overnight News from Bloomberg

- President Vladimir Putin said again on Sunday the war will continue until Ukraine accepts his demands and halts resistance, dimming hopes for a negotiated settlement. Putin says Ukraine must “demilitarize” and he has made clear his goal is to remove the current government

- Major stock markets from Europe to Asia are heading for bear markets -- falling more than 20% from highs -- amid fears of an inflation shock as crude oil soared on the prospect of a ban on Russian supplies

- The SNB’s foreign-exchange holdings slipped as a surging franc weighed on its stockpile. Foreign-currency reserves declined by 8.4 billion francs ($8.7 billion) to 938.3 billion francs in February, according to data published Monday. The central bank said “the franc continues to be highly valued. The SNB takes the overall currency situation into consideration, individual currency pairs don’t play a special role. The central bank is still ready to intervene in the foreign exchange market if necessary.”

- German factory orders increased for a third month, driven by foreign demand, even as the pandemic probably tipped Europe’s largest economy into another recession. Orders rose 1.8% from the previous month in January after advancing 2.8% in December -- more than the median estimate in a Bloomberg survey

- With soaring consumer prices showing little signs so far of feeding a pay spiral in the euro zone, the region’s labor market faces an even bigger cost-of- living increase as energy prices soar after Russia’s invasion of Ukraine

- China declared ties with Russia to be “rock solid” despite President Vladimir Putin’s invasion of Ukraine, while repeating earlier an accusation that the U.S. is trying to build a Pacific version of NATO

- China’s export growth moderated in the first two months of the year, pointing to more stable global demand as multiple risks cloud the outlook

A more detailed look at global markets from Newsquawk

Asia-Pac stocks declined as geopolitical concerns lingered ahead of the third round of Ukraine-Russia talks and after evacuation attempts over the weekend in Mariupol were halted amid a ceasefire breach, while the US and allies are engaged in a “very active discussion” regarding a Russian oil embargo. ASX 200 weakened as tech led the declines across most industries aside from the commodity-related sectors which were boosted by a spike in oil and supply squeeze concerns across the metals complex. Nikkei 225 suffered a near-1000 point intraday loss with notable weakness in autos and airlines stocks. Hang Seng and Shanghai Comp. conformed to the risk aversion after China set its lowest growth target in 30 years at 'around 5.5%' and with mixed Chinese trade data also failing to inspire a turnaround

Top Asian News

- Xi Warns Missteps on Ethnic Issues Would ‘Destabilize’ China

- LSE Reviewing Trades Executed in Polymetal After Brief Spike

- SMBC Nikko Strips 2 Arrested Employees of Executive Titles

- China Builder Logan Downgraded Deeper into Junk by Moody’s

European bourses are hampered across the board, Euro Stoxx 50 -2.3%, as geopolitics continue to dominate. US futures are also pressured, ES -1.7%, but faring marginally better than European peers as participants remain cognisant of US CPI this week and the Fed next week. In Europe, the likes of the FTSE 100 are the relative outperformers given exposure to crude names as the associated Oil & Gas sector cheers benchmark pricing while Basis Resources are firmer.

Top European News

- JPM Strategists Stay Positive for Europe Stocks on Fundamentals

- Danske Bank Senior ESG Analyst Leaves for Risk Management at DNB

- Vopak Plummets; Jefferies Cuts on ‘Looming’ Overcapacity

- Jupiter Sinks as Peel Hunt Cuts Rating on Difficult Outlook

In FX, the dollar remains king, but not quite all conquering as commodity currencies outperform and Gold scales in around the 2k per ounce mark; DXY approaching 99.500 after clearer round number breach. Aussie hovers on 0.7400 handle as iron ore and copper soar. Euro slammed but off worst levels vs Franc after verbal SNB intervention; EUR/CHF back over parity, but EUR /USD dangling above 1.0800. Rouble slides to new record lows ahead of third attempt to strike ceasefire agreement between Russia and Ukraine - Usd/Rub over 135.00 at one stage. Norwegian Crown elevated as Brent remains bid alongside WTI on possible Russian export embargo; EUR /NOK sub-9.8000 vs EUR/SEK around 10.8800 for comparison. SNB says the CHF continues to be "Highly Valued", remains prepared to intervene in FX markets if needed. CHF appreciation reflects the inflation differentials between Switzerland and other nations, inflation abroad is significantly higher than in Switzerland. BoJ could lower its economic assessment at its policy meeting next week, according to Reuters sources.

In commodities, WTI and Brent surge amid multiple bullish-factors re. US possibly banning Russian oil, Iran-nuclear delays and China growth ambitions; thus, benchmarks reached highs of USD 130.50/bbl and USD 139.13/bbl respectively. US officials held meetings in Venezuela amid a search for alternative oil supplies, according to FT. It was later reported that US and Venezuela discussed possible easing of oil sanctions although made little progress towards an agreement, according to sources cited by Reuters. US President Biden's advisers are mulling a Saudi Arabia trip to convince the kingdom to pump more oil, according to Axios. Canada's Alberta Province has some spare pipeline and rail capacity to export additional oil to the US, according to Alberta's Energy Minister. Libya NOC announced an armed group closed pump valves at the Sharara and el-Feel oil fields which reduced its daily production by 330k bbls. Goldman Sachs says a sustained USD 20/bbl increase in oil prices would reduce US GDP by 0.3% and Euroarea by 0.6%. Spot gold/silver are bid though the yellow metal is yet to embark on a substantial move above the USD 2000/oz mark. Copper strengthened to above USD 5/lb for the first time in history amid the broad upside across the commodities complex that saw LME nickel futures gain around 19%.

US Event Calendar

- 3pm: Jan. Consumer Credit, est. $24.5b, prior $18.9b

DB's Jim Reid concludes the overnight wrap

In normal times this Thursday's US CPI and ECB meeting would be the blockbuster couple of hours of the week. It will still be important but clearly won't be the main event given the Ukrainian situation.

Indeed the week is set to start in somewhat of a fraught manner after a remarkable surge in oil overnight with Brent futures up +9.7% to $129.59/bbl and WTI futures +8.1% to $125.07/bbl, as I type - the highest since 2008. Indeed Brent actually opened nearer $139 in a stunning early move.

This comes following US Secretary of State, Antony Blinken stating that Washington and its allies were in talks about banning Russian oil and natural gas imports to tighten economic sanctions on Russia. Blinken added that the US administration will make sure that there is sufficient oil in the global market, if such measures were imposed. Additionally, Speaker Nancy Pelosi said in a letter to Democratic colleagues that the chamber is exploring strong legislation to ban the imports of Russian oil – a move which would “further isolate Russia from the global economy”.

Equity markets are set to open sharply lower as a result with contracts on the S&P 500 (-1.27%), Nasdaq (-1.72%), Dow Jones (-1.0%) and DAX (-3.11%) all weak. Meanwhile, 10-year US Treasury yields moved -2.9bps lower at 1.70%. Elsewhere, the Nikkei (-3.48%), Hang Seng (-3.41%), Shanghai Composite (-1.48%), CSI (-2.38%) and Kospi (-2.02%) are also weak.

There hasn't been much new news over the weekend that progresses the narrative on the conflict and it's looking more likely that this will be an attritional battle absent a major development. For economies and markets, especially in Europe it then depends on whether the gas (and to a lesser extent oil) continues to flow from Russia to the continent. At the moment it seems the European governments are keen for the gas flow to continue (assuming Russia does) but I suppose a risk to this scenario is that public opinion becomes increasingly against that scenario and politicians have to respond. The news out of the US over the weekend shows the momentum is building for fiercer sanctions on Russia.

The oil move this morning comes after there was some hope on Saturday that Iran have moved closer to a position where sanctions could be reduced and thus allowing their oil to flow onto the global market place as early as the third quarter. However yesterday it seemed that Tehran's links to Russia were increasingly seen as a big stumbling block. So we'll see how this story develops.

Another interesting story over the weekend was the Chinese government’s 5.5% 2022 growth target announced at the National People's Congress. Most analysts believed it would be around 5% or just above and our economists wrote last week that if the target was 5.5% it would imply direct additional government support for the economy. They added that this could come at the expense of long-term growth and financial stability. Our economists' update yesterday on how the target might be achieved here.

Previewing the main scheduled events of the week now. For US CPI our economists expect year-on-year inflation to rise to +7.8% in February, the fastest in 40 years. This is the last reading before next Wednesday's FOMC conclusion with the committee now in a blackout period. Perhaps the drama of both these events has been reduced by a quite explicit reference last week by Powell that he favours a 25bps hike next week. Having said that a strong CPI will certainly keep a 50bps move in subsequent meetings firmly on the radar so it's still clearly important to try to assess where we are in the inflation cycle.

As for the ECB on Thursday, their meeting comes after the Euro Area flash CPI print for February last week came in at +5.8% (vs. +5.6% expected), which is the highest level in the single currency's history. A preview of the meeting from our European economists can be found here. They expect the Ukraine crisis to prevent the central bank from announcing APP tapering at this point. Also, in their view, the ECB's message will reinforce its commitment to price stability and addressing fragmentation. Our FX strategists have made a strong case for how the ECB need to intervene soon to ensure that a falling Euro doesn't magnify the soaring energy costs. See here for more

Elsewhere Wednesday is an interesting day as we have US JOLTS which is a good gauge of labour market tightness, and PPI in both China and Japan. The rest of the day by day week ahead is at the end as usual.

Looking back now, it was a difficult and volatile week for markets with commodities the highlight. Brent crude oil futures increased +20.55% over the week (+6.93% Friday) reaching $118/bbl, the highest level since 2013, and the largest weekly increase in absolute dollar terms in Bloomberg’s data dating back to 1988. European natural gas, however, stole the show, increasing +116.20% (+19.73% Friday) to an all-time high of €204.14. Unsurprisingly it marked the largest weekly increase in percentage and euro terms on record. Clearly a very worrying situation on this side of the continent.

The price pressures extend beyond energy, as agricultural prices also saw marked increases. Russia and Ukraine collectively export just under a third of the world’s wheat, leading wheat futures to increase +40.62% (+6.61% Friday). Metals were not spared, with aluminium, copper, and palladium increasing +14.39% (+3.57% Friday), +9.65% (+3.30% Friday), and +27.14% (+8.19% Friday), respectively. The Bloomberg commodity spot index therefore increased +13.02% (+3.34%) over the week, the highest level and largest weekly gain on record.

Central banks were obviously in focus given the inflationary pressures and change to the growth outlook. STIR markets are pricing +24.1bps of ECB tightening through this year, down from +34.3bps of tightening at the end of the week before. Meanwhile, Chair Powell signalled his preference to lift rates by 25 basis points at the March FOMC meeting. He sounded a hawkish tone on the risks from inflation. He paid heed to the uncertain impacts stemming from the war but downplayed the direct economic impacts to the US. Markets are pricing +141.3bps of tightening from the Fed this year, down slightly from +155.6bps at the end of the week before. Not a big destruction in pricing given the war and sanctions escalation.

Longer term interest rates fell on the flight to quality flows, with 10yr treasury, bund, OAT, and gilt yields tumbling -23.1bps (-11.0bps Friday), -30.0bps (-8.9bps Friday), -27.2bps (-6.1bps Friday), and -24.9bps (-9.1bs Friday), respectively. Notably, 10yr bund yields ended the week back in negative territory at -0.07%. The move was driven by real yields, as breakevens widened in line with increases in commodity prices, with 10yr US, German, French, and UK breakevens increasing +14.1bps (+0.8bps Friday), +34.5bps (+9.6bps Friday), +27.4bps (+5.0bps Friday), and +12.8bps (-1.3bps Friday), respectively.

The continued pricing of central bank tightening combined with global risk off drove the 2s10s treasury yield curve -13.9bps (-5.8bps Friday) flatter, finishing the week at +24.9bps, another low that is only matched by March 2020 levels.

The final piece is global equity indices, which were red across the board but with US stocks holding up impressively well. The S&P 500, STOXX 600, DAX, and CAC fell -1.27% (-0.79% Friday), -7.00% (-3.56% Friday), -10.11% (-4.41% Friday), -10.23% (-4.97% Friday), respectively. European stocks underperformed given the proximity to the conflict and sanctions, with the DAX and CAC entering a -10% correction on the week alone, while the STOXX 600 is now down -13.53% YTD. Financials on both sides of the Atlantic were notable underperformers, with the S&P 500 banks and STOXX banks indices down -8.51% (-3.35% Friday) and -18.69% (-7.92% Friday), respectively.

Finally, the US jobs numbers were one bit of optimistic news in an otherwise dismal week. The economy added +678k jobs in February, sending the unemployment rate down to +3.8%, both better than consensus estimates. Labor force participation ticked up to +62.3% while average hourly earnings were actually flat MoM and below expectations easing some inflationary fears. However there looked like there may have been some compositional issues. So we will have to wait for next month's report to see.

International

Copper Soars, Iron Ore Tumbles As Goldman Says “Copper’s Time Is Now”

Copper Soars, Iron Ore Tumbles As Goldman Says "Copper’s Time Is Now"

After languishing for the past two years in a tight range despite recurring…

Share this:

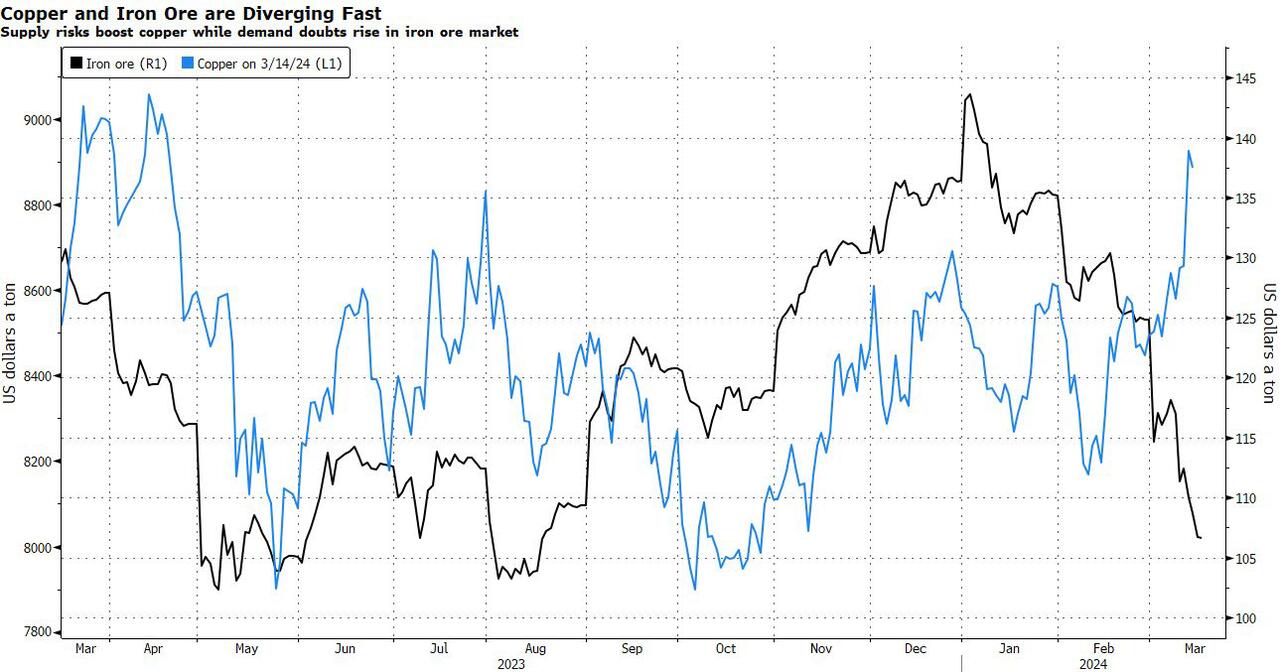

After languishing for the past two years in a tight range despite recurring speculation about declining global supply, copper has finally broken out, surging to the highest price in the past year, just shy of $9,000 a ton as supply cuts hit the market; At the same time the price of the world's "other" most important mined commodity has diverged, as iron ore has tumbled amid growing demand headwinds out of China's comatose housing sector where not even ghost cities are being built any more.

Copper surged almost 5% this week, ending a months-long spell of inertia, as investors focused on risks to supply at various global mines and smelters. As Bloomberg adds, traders also warmed to the idea that the worst of a global downturn is in the past, particularly for metals like copper that are increasingly used in electric vehicles and renewables.

Yet the commodity crash of recent years is hardly over, as signs of the headwinds in traditional industrial sectors are still all too obvious in the iron ore market, where futures fell below $100 a ton for the first time in seven months on Friday as investors bet that China’s years-long property crisis will run through 2024, keeping a lid on demand.

Indeed, while the mood surrounding copper has turned almost euphoric, sentiment on iron ore has soured since the conclusion of the latest National People’s Congress in Beijing, where the CCP set a 5% goal for economic growth, but offered few new measures that would boost infrastructure or other construction-intensive sectors.

As a result, the main steelmaking ingredient has shed more than 30% since early January as hopes of a meaningful revival in construction activity faded. Loss-making steel mills are buying less ore, and stockpiles are piling up at Chinese ports. The latest drop will embolden those who believe that the effects of President Xi Jinping’s property crackdown still have significant room to run, and that last year’s rally in iron ore may have been a false dawn.

Meanwhile, as Bloomberg notes, on Friday there were fresh signs that weakness in China’s industrial economy is hitting the copper market too, with stockpiles tracked by the Shanghai Futures Exchange surging to the highest level since the early days of the pandemic. The hope is that headwinds in traditional industrial areas will be offset by an ongoing surge in usage in electric vehicles and renewables.

And while industrial conditions in Europe and the US also look soft, there’s growing optimism about copper usage in India, where rising investment has helped fuel blowout growth rates of more than 8% — making it the fastest-growing major economy.

In any case, with the demand side of the equation still questionable, the main catalyst behind copper’s powerful rally is an unexpected tightening in global mine supplies, driven mainly by last year’s closure of a giant mine in Panama (discussed here), but there are also growing worries about output in Zambia, which is facing an El Niño-induced power crisis.

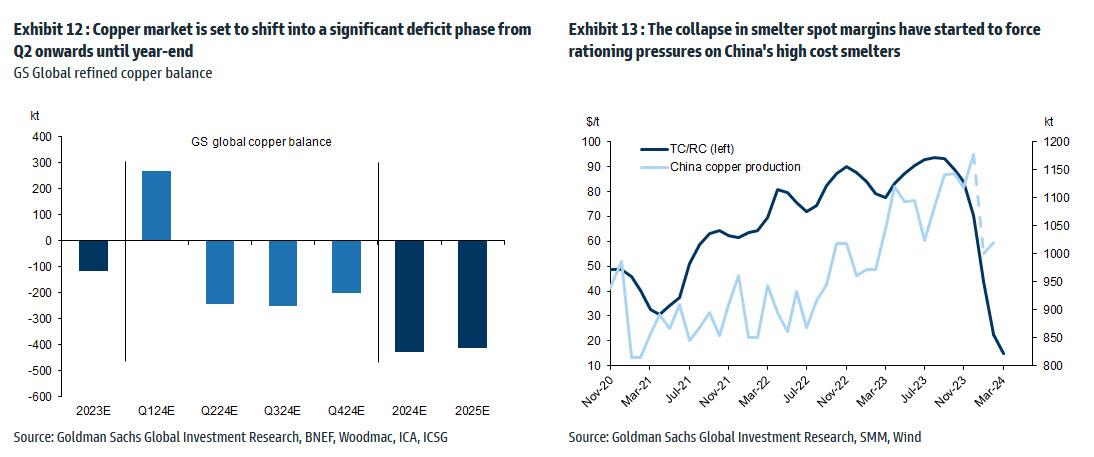

On Wednesday, copper prices jumped on huge volumes after smelters in China held a crisis meeting on how to cope with a sharp drop in processing fees following disruptions to supplies of mined ore. The group stopped short of coordinated production cuts, but pledged to re-arrange maintenance work, reduce runs and delay the startup of new projects. In the coming weeks investors will be watching Shanghai exchange inventories closely to gauge both the strength of demand and the extent of any capacity curtailments.

“The increase in SHFE stockpiles has been bigger than we’d anticipated, but we expect to see them coming down over the next few weeks,” Colin Hamilton, managing director for commodities research at BMO Capital Markets, said by phone. “If the pace of the inventory builds doesn’t start to slow, investors will start to question whether smelters are actually cutting and whether the impact of weak construction activity is starting to weigh more heavily on the market.”

* * *

Few have been as happy with the recent surge in copper prices as Goldman's commodity team, where copper has long been a preferred trade (even if it may have cost the former team head Jeff Currie his job due to his unbridled enthusiasm for copper in the past two years which saw many hedge fund clients suffer major losses).

As Goldman's Nicholas Snowdon writes in a note titled "Copper's time is now" (available to pro subscribers in the usual place)...

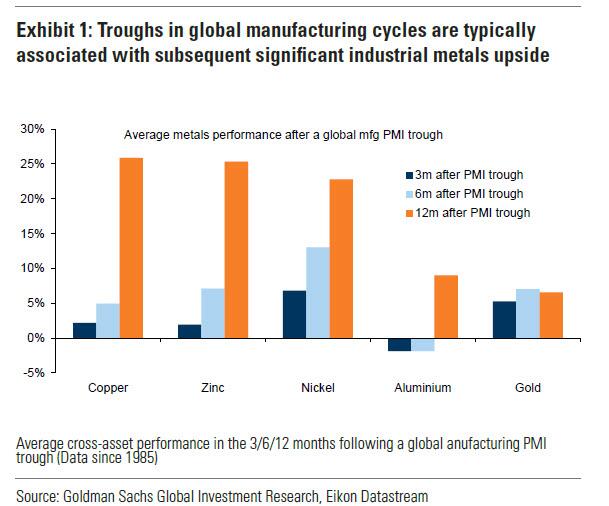

... there has been a "turn in the industrial cycle." Specifically according to the Goldman analyst, after a prolonged downturn, "incremental evidence now points to a bottoming out in the industrial cycle, with the global manufacturing PMI in expansion for the first time since September 2022." As a result, Goldman now expects copper to rise to $10,000/t by year-end and then $12,000/t by end of Q1-25.’

Here are the details:

Previous inflexions in global manufacturing cycles have been associated with subsequent sustained industrial metals upside, with copper and aluminium rising on average 25% and 9% over the next 12 months. Whilst seasonal surpluses have so far limited a tightening alignment at a micro level, we expect deficit inflexions to play out from quarter end, particularly for metals with severe supply binds. Supplemented by the influence of anticipated Fed easing ahead in a non-recessionary growth setting, another historically positive performance factor for metals, this should support further upside ahead with copper the headline act in this regard.

Goldman then turns to what it calls China's "green policy put":

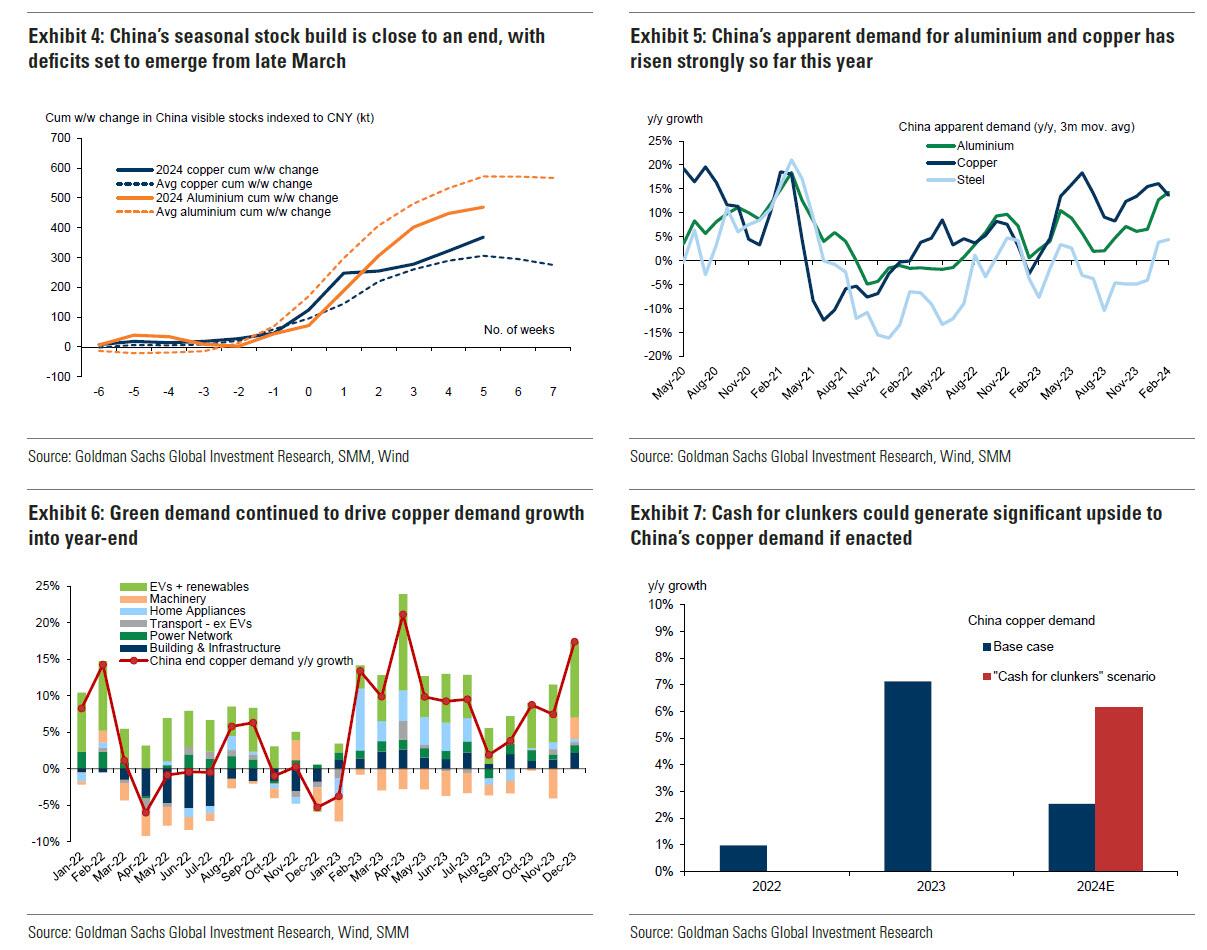

Much of the recent focus on the “Two Sessions” event centred on the lack of significant broad stimulus, and in particular the limited property support. In our view it would be wrong – just as in 2022 and 2023 – to assume that this will result in weak onshore metals demand. Beijing’s emphasis on rapid growth in the metals intensive green economy, as an offset to property declines, continues to act as a policy put for green metals demand. After last year’s strong trends, evidence year-to-date is again supportive with aluminium and copper apparent demand rising 17% and 12% y/y respectively. Moreover, the potential for a ‘cash for clunkers’ initiative could provide meaningful right tail risk to that healthy demand base case. Yet there are also clear metal losers in this divergent policy setting, with ongoing pressure on property related steel demand generating recent sharp iron ore downside.

Meanwhile, Snowdon believes that the driver behind Goldman's long-running bullish view on copper - a global supply shock - continues:

Copper’s supply shock progresses. The metal with most significant upside potential is copper, in our view. The supply shock which began with aggressive concentrate destocking and then sharp mine supply downgrades last year, has now advanced to an increasing bind on metal production, as reflected in this week's China smelter supply rationing signal. With continued positive momentum in China's copper demand, a healthy refined import trend should generate a substantial ex-China refined deficit this year. With LME stocks having halved from Q4 peak, China’s imminent seasonal demand inflection should accelerate a path into extreme tightness by H2. Structural supply underinvestment, best reflected in peak mine supply we expect next year, implies that demand destruction will need to be the persistent solver on scarcity, an effect requiring substantially higher pricing than current, in our view. In this context, we maintain our view that the copper price will surge into next year (GSe 2025 $15,000/t average), expecting copper to rise to $10,000/t by year-end and then $12,000/t by end of Q1-25’

Another reason why Goldman is doubling down on its bullish copper outlook: gold.

The sharp rally in gold price since the beginning of March has ended the period of consolidation that had been present since late December. Whilst the initial catalyst for the break higher came from a (gold) supportive turn in US data and real rates, the move has been significantly amplified by short term systematic buying, which suggests less sticky upside. In this context, we expect gold to consolidate for now, with our economists near term view on rates and the dollar suggesting limited near-term catalysts for further upside momentum. Yet, a substantive retracement lower will also likely be limited by resilience in physical buying channels. Nonetheless, in the midterm we continue to hold a constructive view on gold underpinned by persistent strength in EM demand as well as eventual Fed easing, which should crucially reactivate the largely for now dormant ETF buying channel. In this context, we increase our average gold price forecast for 2024 from $2,090/toz to $2,180/toz, targeting a move to $2,300/toz by year-end.

Much more in the full Goldman note available to pro subs.

Government

Moderna turns the spotlight on long Covid with new initiatives

Moderna’s latest Covid effort addresses the often-overlooked chronic condition of long Covid — and encourages vaccination to reduce risks. A digital…

Share this:

Moderna’s latest Covid effort addresses the often-overlooked chronic condition of long Covid — and encourages vaccination to reduce risks. A digital campaign debuted Friday along with a co-sponsored event in Detroit offering free CT scans, which will also be used in ongoing long Covid research.

In a new video, a young woman describes her three-year battle with long Covid, which includes losing her job, coping with multiple debilitating symptoms and dealing with the negative effects on her family. She ends by saying, “The only way to prevent long Covid is to not get Covid” along with an on-screen message about where to find Covid-19 vaccines through the vaccines.gov website.

“Last season we saw people would get a flu shot, but they didn’t always get a Covid shot,” said Moderna’s Chief Brand Officer Kate Cronin. “People should get their flu shot, but they should also get their Covid shot. There’s no risk of long flu, but there is the risk of long-term effects of Covid.”

It’s Moderna’s “first effort to really sound the alarm,” she said, and the debut coincides with the second annual Long Covid Awareness Day.

An estimated 17.6 million Americans are living with long Covid, according to the latest CDC data. About four million of them are out of work because of the condition, resulting in an estimated $170 billion in lost wages.

While HHS anted up $45 million in grants last year to expand long Covid support initiatives along with public health campaigns, the condition is still often ignored and underfunded.

“It’s not just about the initial infection of Covid, but also if you get it multiple times, your risks goes up significantly,” Cronin said. “It’s important that people understand that.”

grants covid-19 cdc hhsGovernment

Consequences Minus Truth

Consequences Minus Truth

Authored by James Howard Kunstler via Kunstler.com,

“People crave trust in others, because God is found there.”

-…

Share this:

{kind=link}

{kind=link}

Authored by James Howard Kunstler via Kunstler.com,

“People crave trust in others, because God is found there.”

- Dom de Bailleul

The rewards of civilization have come to seem rather trashy in these bleak days of late empire; so, why even bother pretending to be civilized? This appears to be the ethos driving our politics and culture now. But driving us where? Why, to a spectacular sort of crack-up, and at warp speed, compared to the more leisurely breakdown of past societies that arrived at a similar inflection point where Murphy’s Law replaced the rule of law.

{kind=link}

The US Military Academy at West point decided to “upgrade” its mission statement this week by deleting the phrase Duty, Honor, Country that summarized its essential moral orientation. They replaced it with an oblique reference to “Army Values,” without spelling out what these values are, exactly, which could range from “embrace the suck” to “charlie foxtrot” to “FUBAR” — all neatly applicable to our country’s current state of perplexity and dread.

Are you feeling more confident that the US military can competently defend our country? Probably more like the opposite, because the manipulation of language is being used deliberately to turn our country inside-out and upside-down. At this point we probably could not successfully pacify a Caribbean island if we had to, and you’ve got to wonder what might happen if we have to contend with countless hostile subversive cadres who have slipped across the border with the estimated nine-million others ushered in by the government’s welcome wagon.

Momentous events await. This Monday, the Supreme Court will entertain oral arguments on the case Missouri, et al. v. Joseph R. Biden, Jr., et al. The integrity of the First Amendment hinges on the decision. Do we have freedom of speech as set forth in the Constitution? Or is it conditional on how government officials feel about some set of circumstances? At issue specifically is the government’s conduct in coercing social media companies to censor opinion in order to suppress so-called “vaccine hesitancy” and to manipulate public debate in the 2020 election. Government lawyers have argued that they were merely “communicating” with Twitter, Facebook, Google, and others about “public health disinformation and election conspiracies.”

You can reasonably suppose that this was our government’s effort to disable the truth, especially as it conflicted with its own policy and activities — from supporting BLM riots to enabling election fraud to mandating dubious vaccines. Former employees of the FBI and the CIA were directly implanted in social media companies to oversee the carrying-out of censorship orders from their old headquarters. The former general counsel (top lawyer) for the FBI, James Baker, slid unnoticed into the general counsel seat at Twitter until Elon Musk bought the company late in 2022 and flushed him out. The so-called Twitter Files uncovered by indy reporters Matt Taibbi, Michael Shellenberger, and others, produced reams of emails from FBI officials nagging Twitter execs to de-platform people and bury their dissent. You can be sure these were threats, not mere suggestions.

One of the plaintiffs joined to Missouri v. Biden is Dr. Martin Kulldorff, a biostatistician and professor at the Harvard Medical School, who opposed Covid-19 lockdowns and vaccine mandates. He was one of the authors of the open letter called The Great Barrington Declaration (October, 2020) that articulated informed medical dissent for a bamboozled public. He was fired from his job at Harvard just this past week for continuing his refusal to take the vaccine. Harvard remains among a handful of institutions that still require it, despite massive evidence that it is ineffective and hazardous. Like West Point, maybe Harvard should ditch its motto, Veritas, Latin for “truth.”

A society hostile to truth can’t possibly remain civilized, because it will also be hostile to reality. That appears to be the disposition of the people running things in the USA these days. The problem, of course, is that this is not a reality-optional world, despite the wishes of many Americans (and other peoples of Western Civ) who wish it would be.

Next up for us will be “Joe Biden’s” attempt to complete the bankruptcy of our country with $7.3-trillion proposed budget, 20 percent over the previous years spending, based on a $5-billion tax increase. Good luck making that work. New York City alone is faced with paying $387 a day for food and shelter for each of an estimated 64,800 illegal immigrants, which amounts to $9.15-billion a year. The money doesn’t exist, of course. New York can thank “Joe Biden’s” executive agencies for sticking them with this unbearable burden. It will be the end of New York City. There will be no money left for public services or cultural institutions. That’s the reality and that’s the truth.

A financial crack-up is probably the only thing short of all-out war that will get the public’s attention at this point. I wouldn’t be at all surprised if it happened next week. Historians of the future, stir-frying crickets and fiddleheads over their campfires will marvel at America’s terminal act of gluttony: managing to eat itself alive.

* * *

Support his blog by visiting Jim’s Patreon Page or Substack

Key shipping company files for Chapter 11 bankruptcy

Net Zero, The Digital Panopticon, & The Future Of Food

Illegal Immigrants Leave US Hospitals With Billions In Unpaid Bills

These Cities Have The Highest (And Lowest) Share Of Unaffordable Neighborhoods In 2024

Problems After COVID-19 Vaccination More Prevalent Among Naturally Immune: Study

For-profit nursing homes are cutting corners on safety and draining resources with financial shenanigans − especially at midsize chains that dodge public scrutiny

The Question You Should Ask Whenever You’re Wrong

Trump nearly derailed democracy once − here’s what to watch out for in reelection campaign

Looking Back At COVID’s Authoritarian Regimes

‘Excess Mortality Skyrocketed’: Tucker Carlson and Dr. Pierre Kory Unpack ‘Criminal’ COVID Response

-

Uncategorized3 weeks ago

Uncategorized3 weeks agoAll Of The Elements Are In Place For An Economic Crisis Of Staggering Proportions

-

International1 week ago

International1 week agoEyePoint poaches medical chief from Apellis; Sandoz CFO, longtime BioNTech exec to retire

-

Uncategorized4 weeks ago

Uncategorized4 weeks agoCalifornia Counties Could Be Forced To Pay $300 Million To Cover COVID-Era Program

-

Uncategorized3 weeks ago

Uncategorized3 weeks agoApparel Retailer Express Moving Toward Bankruptcy

-

Uncategorized4 weeks ago

Uncategorized4 weeks agoIndustrial Production Decreased 0.1% in January

-

International1 week ago

International1 week agoWalmart launches clever answer to Target’s new membership program

-

Spread & Containment2 days ago

Spread & Containment2 days agoIFM’s Hat Trick and Reflections On Option-To-Buy M&A

-

Uncategorized4 weeks ago

Uncategorized4 weeks agoRFK Jr: The Wuhan Cover-Up & The Rise Of The Biowarfare-Industrial Complex