Futures Tumble As Nat Gas Prices Explode, Stagflation Fears Surge

Futures Tumble As Nat Gas Prices Explode, Stagflation Fears Surge

In our market comments on Tuesday we were stunned by the resilient surge in tech names and the broader market, even as yields soared on the biggest jump in breakevens since…

Share this:

In our market comments on Tuesday we were stunned by the resilient surge in tech names and the broader market, even as yields soared on the biggest jump in breakevens since the presidential election, noting that something is very broken with this picture. Well, one day later normalcy is back: US stock index futures tumbled as much as 1.3% on Wednesday before paring some losses, after soaring oil and gas prices (rising as much as 40% in Europe today alone) fed into fears of higher inflation and fueled concerns of sooner-than-expected tapering, which in turn pushed 10Y yields just shy of 1.57%. At 730 a.m. ET, Dow e-minis were down 309 points, or 0.9%, S&P 500 e-minis were down 49 points, or 1.12%, and Nasdaq 100 e-minis were down 181 points, or 1.23%, to the lowest level since June 25 on a closing basis, signaling more downside for tech shares after Tuesday’s short reprieve

Up to Tuesday’s close, the S&P 500 index logged its fourth straight day of 1% moves in either direction. According to Reuters, the last time the index saw that much volatility was in November 2020, when it rose or fell 1% or more for seven straight sessions.

The selloff was much more severe in Europe, with the Stoxx 600 falling as much as 2% to a 2 month low, with every industry sector firmly in the red as the region’s natural gas prices soared to catastrophic levels...

... even as the European Union pledged swift action to ensure the spiking costs don’t stifle the economy (it just didn't explain precisely what it would do). Asian stocks also dropped amid continued China property contagion fears. The 10-year TSY yield touched their highest since June, slamming shares of mega-cap FAAMGs; tech shares led the stocks selloff Apple (AAPL US -1.5%), Facebook (FB US -1.6%), Microsoft (MSFT US -1.6%), Tesla (TSLA US -1.4%) down in U.S. premarket trading.

Economy-sensitive parts of the market also came under pressure, with lenders such as Bank of America Corp , JPMorgan Chase & Co and Morgan Stanley shedding more than 1% each. Boeing and industrial conglomerates Caterpillar Inc and 3M Co dropped between 0.8% and 2.0%. Ironically, even though Brent remained well above $82, energy names also slumped with Exxon sliding 1% on what appears to be profit taking to plug margin holes elsewhere. American Airlines’ shares fell 3.7% in U.S. premarket session after Goldman cut its recommendation for the stock to sell. Meanwhile, Palantir Technologies extended its gains to rise 9.3% as the company said it won a U.S. Army contract to supply data and analytics services. Here are some of the other notable market movers:

- Gogo (GOGO US) drops 5.3% in U.S. premarket trading after Morgan Stanley downgrades to underweight, with competitive landscape expected to pressure valuation and free cash flow over coming year

- American Airlines (AAL US) slides 3.6% in U.S. premarket trading on Goldman Sachs downgrade, according to Bloomberg data

- U.S. Steel (X US) down more than 5% in U.S. premarket trading on Goldman Sachs downgrade, according to Bloomberg data

- Calyxt (CLXT US) shares jump 5.4% premarket after the company said it will focus on engineering synthetic biology solutions for customers across the nutraceutical, cosmeceutical, pharmaceutical, advanced materials, and chemical industries

- Indus Realty Trust (INDT US) fell postmarket Tuesday after launching a 2 million stock offering

- Noodles & Co. (NDLS US) shares rose 2% in Tuesday postmarket trading after Stephens started coverage with an overweight rating, saying the restaurant chain is poised for strong growth that should lead to higher multiples

- Allison Transmission (ALSN US) is accelerating the development of electrification technology for integration into the U.S. Army’s ground combat vehicle fleet

- Palantir (PLTR US) shares rise 14% in U.S. premarket trading after the the software company said Tuesday it was selected by the U.S. Army to provide data and analytics for the Capability Drop 2 program

"Right now you’re seeing inflation risk really start to percolate and I do think that you’re going to see that really eat into margins as we go through the fourth quarter into 2022,” Erin Browne, multi-asset portfolio manager at Pimco, said on Bloomberg Television. “The energy crisis that’s starting to loom in Europe is a real risk that is being underestimated by the market right now."

“The spike in energy prices continue fueling expectations of higher inflation for longer. Therefore, central banks will be forced to cool down the overheating in inflation rather than trying to boost recovery,” said Ipek Ozkardeskaya, senior analyst at Swissquote Bank. “Any weakness in the jobs figure could send the U.S. equities back below their 100-dma levels, as soft economic data could no longer revive the central bank doves."

As such, all eyes will be on the U.S. private payrolls data, due at 8:15 a.m. ET. The numbers come ahead of the more comprehensive non-farm payrolls data on Friday, which is expected to cement the case for the Federal Reserve’s slowing of asset purchases. Meanwhile, a stalemate over Republicans and Democrats about the debt limit showed no sign of abating, with President Joe Biden saying that his Democrats might make an exception to a U.S. Senate rule to allow them to extend the government’s borrowing authority without Republican help.

European stocks fell even more, with the Stoxx Europe 600 index plunging 2% to lowest since July 20; Travel, autos and retail names are the weakest sectors although all Stoxx 600 sub-indexes are off at least 1%, tech was also underperforming. As noted above, gas prices remain a focal pressure point with several measures hitting record levels. Here are some of the biggest European movers today:

- Adler shares extend decline to 21% in Frankfurt after Viceroy Research publishes a report saying it is short Adler Group SA and its listed subsidiaries.

- Deutsche Telekom shares fall 4%, close to the level at which Goldman Sachs offered about EU1.5b worth of shares, as part of a deal to swap some of Softbank’s T- Mobile stake for one in Deutsche Telekom.

- Ambu shares fall as much as 8.1%, most since Aug. 17, after company cut its FY financial outlook.

- IP Group shares drop as much as 8.1%, their worst day in nine months, after CEO Alan Aubrey and CIO Mike Townend retire.

- GN Store Nord shares rise as much as 7.5% as it agrees to buy SteelSeries, a maker of software-enabled gaming gear, from Nordic private equity company Axcel for an enterprise value of DKK8b on a cash and debt-free basis.

- Tesco shares rise as much as 4.6% to an eight-month high after Britain’s biggest supermarket operator said it will buy back GBP500m of stock and raised its FY profit forecast.

- HSBC rises as much 2.5% as UBS upgrades the Asia-focused lender to buy from neutral, saying the market is taking a risk by being underweight.

- PageGroup shares jump as much as 6.9%, most since April, as the staffing firm boosts its profit forecast. Peer Hays also gains.

- Dustin shares jump as much as 11%, most since April 13, after the IT solutions provider’s Ebit for the fourth quarter beat the average analyst estimate.

- Atlantic Sapphire gains as much as 15% as Pareto sees improvements ahead.

Asian stocks headed for their longest losing streak since August as a selloff in the heavyweight tech sector deepened amid rising Treasury yields. The MSCI Asia Pacific Index declined as much as 0.8%, in its fourth day of decline, with Samsung and Tencent among the biggest drags. A benchmark tracking Chinese technology stocks in Hong Kong closed at a record low. Japan’s Nikkei 225 and South Korea’s Kospi were the biggest losers, sliding more than 1% each. China Tech Stock Gauge Falls to Test Record Low as Yields Rise Investors have yet to digest issues such as the inflation outlook, among other concerns including gridlock over the U.S. debt ceiling and higher global energy prices. The MSCI Asia Pacific Index is approaching year-to-date lows seen in August. “At the moment, given all the uncertainties regarding the growth, inflation and policy outlooks, we are still in the middle of the tempest, so to speak,” Kyle Rodda, an analyst at IG Markets, said by email. Indonesian, Malaysian and Philippine stock benchmarks were among the region’s best performers.

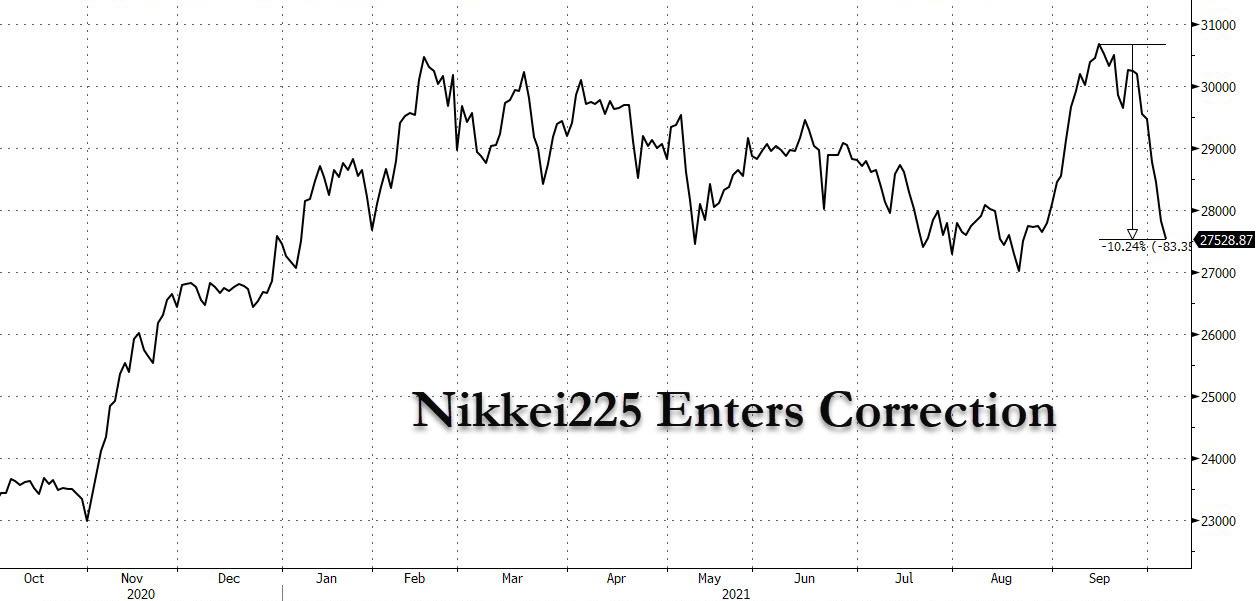

In Japan, the Topix closed 0.3% lower while the Nikkei225 capped its worst daily losing streak since July 2009 and entered a technical correction, as Japanese equities tumbled while Treasury yields climbed.

Fast Retailing Co. and Tokyo Electron Ltd. were the largest contributors to a 1.1% loss in the Nikkei 225, which fell for an eighth-straight day. The gauge, which had risen as much as 1.4% earlier in the day, closed more than 10% down from its September high. The broader Topix dipped 0.3%, erasing an early 1.6% advance, driven by losses in automakers. Banks climbed on the spike in Treasury yields. Japanese stocks had opened the day higher, following a rebound in U.S. shares. Both major gauges fell for a seventh day Tuesday amid market disappointment with the new government and a host of threats to global economic growth. ‘Kishida Shock’ Hits Japan Markets Wary of Redistribution Plan “Technicals such as RSI and Bollinger are showing that these moves may have been overdone in the short term, but Japan is hostage to the continued global concerns regarding inflation, supply chains and Chinese credit along with PM Kishida’s ‘new capitalism’ concept,” said Takeo Kamai, head of execution services at CLSA Securities Japan Co

Australia's S&P/ASX 200 index fell 0.6% to close at 7,206.50, reversing an earlier advance of as much as 0.4%. Banks contributed the most to the benchmark’s decline after Australia’s banking regulator raised loan buffers in a bid to cool the nation’s booming housing market. a2 Milk was the worst performer after a class action lawsuit was filed against the company. Whitehaven was the top performer, rising for a fourth straight day. In New Zealand, the S&P/NZX 50 index fell 0.3% to 13,166.44. The nation’s central bank raised interest rates for the first time in seven years and signaled further increases will likely be needed to tame inflation. The RBNZ lifted the official cash rate by a quarter percentage point to 0.5%.

In rates, Treasuries were off their worst levels of the day after the 10Y yield rose briefly topped 1.57%, and remained cheaper by more than 2bps across long-end. The 10-year yield was around 1.55%, cheapest since June 17; U.K. 10-year cheapens by further 1.8bp vs U.S., German 10-year by 0.5bp.

In the U.K., the 10-year breakeven rate climbed above 4%, twice the Bank of England’s target, spurred by soaring energy costs. Money markets have almost fully priced a rate hike as soon as December, in what would be the central bank’s first increase in over three years. Peripheral spreads widen to core with long-dated BTPs widening ~3bps to Germany.

In FX, USD is well bid with risk assets trading poorly. Bloomberg dollar index rises 0.5%, pushing through last Friday’s highs. NZD, NOK and AUD are the weakest in G-10. Crude futures trade a narrow range near Asia’s opening levels. WTI is down 0.4% near $78.60, Brent briefly trades above $83 before dipping into the red. Spot gold extends Asia’s weakness to print fresh lows for the week near $1,745/oz. Base metals are in the red. LME copper the worst performer, dropping 1.9% to trade near the $9k mark.

In commodities, crude futures trade a narrow range near Asia’s opening levels. WTI is down 0.4% near $78.60, Brent briefly trades above $83 before dipping into the red. Spot gold extends Asia’s weakness to print fresh lows for the week near $1,745/oz. Base metals are in the red. LME copper the worst performer, dropping 1.9% to trade near the $9k mark

Elsewhere, Bitcoin traded around the $51,000 mark.

Looking at the day ahead, data releases include German factory orders for August, the German and UK construction PMIs for September, Euro Area retail sales for August, and the ADP’s September report on private payrolls from the US. From central banks, we’ll also hear from the ECB’s Centeno.

Market Wrap

- S&P 500 futures down 0.9% to 4,294.75

- STOXX Europe 600 down 1.5% to 449.34

- MXAP down 0.7% to 191.25

- MXAPJ down 0.8% to 622.40

- Nikkei down 1.1% to 27,528.87

- Topix down 0.3% to 1,941.91

- Hang Seng Index down 0.6% to 23,966.49

- Shanghai Composite up 0.9% to 3,568.17

- Sensex down 0.2% to 59,596.78

- Australia S&P/ASX 200 down 0.6% to 7,206.55

- Kospi down 1.8% to 2,908.31

- Brent Futures up 0.1% to $82.67/bbl

- Gold spot down 0.7% to $1,747.69

- U.S. Dollar Index up 0.32% to 94.28

- German 10Y yield up 2 bps to -0.168%

- Euro down 0.3% to $1.1560

Top Overnight News from Bloomberg

- Boris Johnson’s insistence that higher pay for U.K. workers is worth the pain of supply chain turmoil is generating buzz among Conservative Party members that he’s planning to raise the minimum wage in a keynote speech on Wednesday

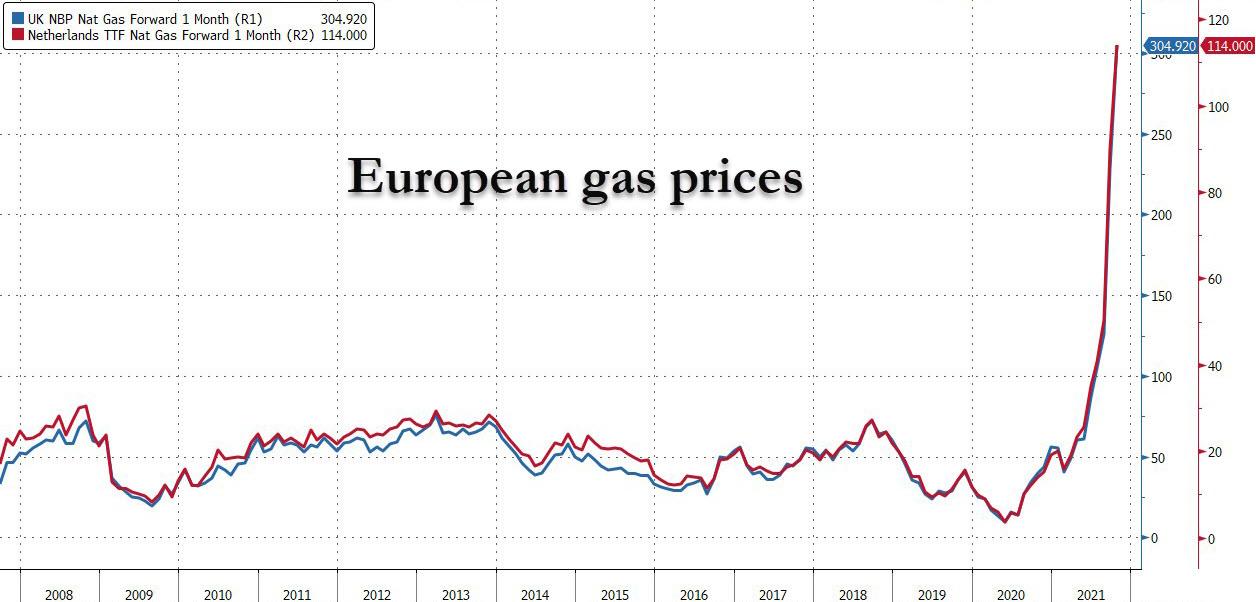

- European energy prices extend their blistering rally as the supply crunch shows no sign of easing and the European Union pledged a quick response to keep the crisis from damaging the economy

- Chinese Fantasia Holdings Group Co., which develops high-end apartments and urban renewal projects, failed to repay a $205.7 million bond that came due Monday. That prompted a flurry of rating downgrades late Tuesday to levels signifying default. The stumble stirred broader angst in volatile markets amid public holidays in China and uncertainty about Evergrande

- President Emmanuel Macron nominated Bank of France Governor Francois Villeroy de Galhau for a second term, opting for stability in one of the most important appointment decisions on European Central Bank policy making for years to come

- The German Green Party is seeking to start exploratory talks with the SPD and liberal FDP party on forming a governing coalition, Green Party co-leader Annalena Baerbock said

- Saudi Arabia reduced oil prices for its main buyers, a day after OPEC+ sent crude futures surging by sticking to a plan for slow and steady supply increases

A more detailed look at global markets courtesy of Newsquawk:

Asia-Pac bourses traded mostly lower after failing to sustain the initial momentum from Wall St, where all major indices gained as investors bought back into tech and with sentiment helped by better-than-expected ISM services PMI, while continued upside in oil prices and a higher yield environment also underpinned energy and financials. This initially lifted the overnight benchmark indices although gains in the ASX 200 (-0.6%) were later reversed as the strength in energy and tech was overshadowed by weakness in the broader market including underperformance in the top-weighted financials sector after the regulator announced a loan curb measure targeting mortgage lending. Nikkei 225 (-1.1%) faded its opening gains and brief foray into 28k territory with auto names among the laggards amid ongoing production disruptions and with PM Kishida’s new cabinet beginning on shaky ground as polls showed his approval rating was at just 55% heading into the upcoming election, which was also the lowest for a new leader in 13 years, while KOSPI (-1.8%) gave up initial spoils with firmer than expected CPI data supporting the case for another hike by the BoK this year. Hang Seng (-0.6%) conformed to the soured mood amid weakness in property and biotech with participants also focusing on Chief Executive Lam’s final policy address of her current term where she proposed measures to address the housing issue, although this failed to lift the property sector as Evergrande concerns lingered after Hong Kong property agencies sued the Co. to recover overdue commissions and with shares in its New Energy Vehicle unit suffering double-digit percentage losses. Finally, 10yr JGBs were lower on spillover selling from T-notes and despite the downturn in stocks, while the absence of BoJ purchases in the market today added to the lacklustre demand with the central bank instead offering to buy JPY 125bln in corporate bonds from October 11th with 1yr-3yr maturities.

Top Asian News

- China Tech Stock Gauge Falls to Record Low as Yields Rise

- Top Glove Says Cooperating in Investigation Over Worker’s Death

- China Resources Unit Said to Be in Talks for JLL China Business

- Asian Stocks Drop as Tech Selloff Deepens Amid Rising Yields

Stocks in Europe have extended on the losses seen at the cash open (Euro Stoxx 50 -2.4%; Stoxx 600 -1.8%) with risk aversion intensifying from a downbeat APAC session as markets grapple with the prospect of stagflation, the energy crunch, Evergrande woes, and geopolitics. US equity futures have conformed to the losses across stocks with the ES (-1.3%) RTY (-1.5%), NQ (-1.5%) and YM (-1.0%) all softer, whilst the former two dipped under 4,300 and 2,200 respectively. From a news-flow standpoint, fresh catalysts have been light. Euro-bouses see broad-based losses whilst the FTSE 100 (-1.6%) is somewhat cushioned (albeit under 7k) by a softer sterling alongside some heavyweight individual stocks including HSBC (+3.3%) following a broker move, and Tesco (+4.5%) after topping H1 forecasts, raised guidance and a GBP 500mln share buyback scheme. Sectors in Europe are all in the red. Banks are the best of the bunch amid the favourable yield environment. On this note, SocGen suggested that the banking sector should benefit from the rise in yields and limited exposure to China, higher energy and supply-chain bottlenecks, while that market consolidation offers some opportunities in the European tech and industrial sectors. Back to sectors, the downside sees some of the more cyclical sectors including Travel & Leisure and Auto names. In terms of some individual movers, Deutsche Telekom (-5.6%) is hit after a bookrunner noted a share offering of some 90mln shares priced at a discount to yesterday’s close.

Top European News

- German Greens Seek Talks With SPD, FDP on Post-Merkel Government

- European Industry Buckles Under a Worsening Energy Squeeze

- Polish Central Bank Unbowed Despite Price Spike: Decision Guide

- Bayer Shares Turn Lower After Initial Gains on Roundup Win

In FX, the Dollar is firmly back in the driving seat and the index is eyeing YTD highs having reclaimed 94.000+ status amidst another sharp downturn in risk appetite just a day after what some pundits were dubbing as a ‘turnaround Tuesday’. Instead, Asia-Pacific bourses were reluctant to pick up the baton from Wall Street and the failure to keep the ball rolling against the backdrop of ongoing strength in gas and oil prices has rattled EU equities to the extent that the Dax has lost grip of the 15k handle and FTSE is down below 7k regardless of the fact that the UK benchmark has some positive impulses beyond the obvious revenue implications for the energy sector. Back to the DXY 94.448 is the best so far ahead of 94.500 for sentimental reasons and the current y-t-d peak just a fraction above at 94.504. In terms of fundamentals, next up for the Greenback is ADP as one of the usual pointers for NFP, while Fed speak comes from Bostic who is down to talk twice today.

- NZD/AUD - Ironically perhaps, the Kiwi is underperforming even though the RBNZ matched market expectations with a 25 bp OCR hike overnight, and this could well be described as a classic ‘buy rumour, sell fact’ reaction given that the move was all priced in. Moreover, the accompanying statement has not altered expectations for further measured tightening and this could compound the inclination to re-position/take profit/cut longs to the detriment of the Nzd. Indeed, the Kiwi has retreated from around 0.6980 vs its US rival to circa 0.6878 and is struggling to tread water on the 1.0500 mark against the Aussie that is also losing out to its US rival on the aforementioned risk dynamic, as Aud/Usd hovers towards the bottom end of 0.7295-0.7227 parameters ahead of AIG’s services sector index.

- CAD/GBP - Also somewhat perverse, though a measure of the degree that the market mood has changed since yesterday, the Loonie and Sterling are both struggling to derive much from the latest advances in WTI or Brent. In fact, Usd/Cad approached 1.2650 having breached the 50 DMA (1.2626) and pulling away from a cluster of decent option expiries that start at 1.2520-25 (1 bn) and continue through 1.2550-60 (2.1 bn) to 1.2600 (1 bn) and end between 1.2720-30 (1.5 bn, while Cable has reversed through 1.3600 and the 10 DMA (1.3592) with little assistance from a sub-consensus UK construction PMI.

- EUR/CHF/JPY - All unable to escape the Buck’s clutches, with the Euro down to a minor new 2021 low and probing barriers at 1.1550, while the Franc is treading water around 0.9300 and the Yen is thriving to keep tabs on 111.50 due to its renowned safe-haven properties, and with the prop of JGB yields reaching multi-month peaks, albeit in catch-up trade with US Treasuries and other global bonds.

- SCANDI/EM - Little solace for the Nok via Brent almost touching Usd 83.50/brl at one stage, though it is holding a firm line following its ascent beyond 10.0000 vs the Eur, while the Sek has largely taken mixed Swedish data and Riksbank rhetoric from Skingsley in stride (caution warranted and now is not the time to change monetary policy), but EM currencies are all floundering with the Try sliding to yet another record trough and on course to hit 9.0000. Ahead, the Zar will be looking for something supportive from SARB Governor Kganyago via a webinar on the economy, jobs and growth.

- RBNZ hiked the OCR by 25bps to 0.50% as expected and the committee noted further removal of monetary policy stimulus is expected over time. RBNZ added that it is appropriate to continue reducing the level of stimulus and that future moves are contingent on the medium term outlook for inflation and employment, while policy stimulus will need to be reduced to maintain price stability and maximum sustainable employment over the medium term. Furthermore, it noted that cost pressures are becoming more persistent and capacity pressures are still evident, but added that demand shortfalls are less of an issue than the economy hitting capacity constraints and that economic activity will rebound quickly as alert level restrictions ease. (Newswires)

In commodities, WTI and Brent front month futures are choppy in early European trade with a downside bias amid the risk tone, but ultimately, prices remain near recent highs with the WTI Nov contract north of USD 78.50/bbl (78.25-79.78/bbl) and Brent Dec around 82/bbl (vs USD 81.92-83.47/bbl range) at the time of writing. Nat gas has once again been the focus in the energy complex, with the UK Nat Gas future surging some 40% intraday at one point, although its US counterpart has lost some steam. A lot of attention has been the Nord Stream 2 pipeline to alleviate some of the supply/demand imbalances in the gas market heading into the winter period. Yesterday, an EU lawmaker suggested that the pipeline does not comply with EU rules, although an EU court adviser noted that Nord Stream 2 could challenge the energy rule and the decision is not final. European natural gas futures climbed to a fresh all-time high. Back to crude, it’s worth being cognizant of the underlying demand that could be fed via the higher gas prices as other energy sources are more sought after, including diesel generators for electricity usually produced by Nat Gas. Over to metals, spot gold and silver are pressured by the firmer Buck with the former back under USD 1,750/oz and at session lows at the time of writing. The downbeat tone has also taken a toll on the base metals complex, with LME copper again dipping below the USD 9,000/t from a USD 9,135/t intraday peak.

US Event Calendar

- 7am: Oct. MBA Mortgage Applications, prior -1.1%

- 8:15am: Sept. ADP Employment Change, est. 430,000, prior 374,000

DB's Jim Reid concludes the overnight wrap

Risk appetite returned to markets yesterday, but not without some astonishing moves in commodities and inflation markets alongside a selloff in bonds. On top of that, we also had a fresh round of signals that supply-chain issues and inflation were beginning to have real economic impacts, thanks to the global September PMI readings.

The most eye catching stat of the last 24 hours is probably that the UK’s index linked bonds are now implying that the April 2022 YoY UK RPI print will be c.7%. Thanks to DB’s Sanjay Raja for pointing this out to me. That’s the point in time where Ofgem next updates its price cap for utility bills.

This comes after further astonishing moves in natural gas. In the UK, gas prices were up +19.54%, marking the biggest daily percentage increase in over a year and a +183.3% move since the start of August. 10 year UK breakevens closed at an incredible 3.979% (+9.6bps on the day). To be fair this is based on RPI not the CPI that other index linked markets are. As of early next year the UK is moving to a CPI-H benchmark so these numbers will come down but it’s still an astonishing reflection on expectations for 10-year average inflation numbers.

Benchmark European natural gas futures weren’t much different and were up by +20.04% to a record €116.02 per megawatt hour. That’s also the biggest daily percentage increase in over a year, and the absolute increase of €19.37 is actually more than the level at which natural gas was trading as recently as Q1 this year! That leaves natural gas prices up more than six-fold since the start of the year, and up more than three-fold since the start of July. In comparison the US gas future was “only” up +9.20%, but still reached its highest closing level since December 2008. And oil itself saw another round of gains, with Brent Crude (+1.60%) rising to its highest in almost 3 years, at $82.56/bbl, whilst WTI was up +1.69% to $78.93/bbl, its highest since 2014.

This fresh round of price surges has led to another spike in inflation expectations across multiple countries even in 10 year markets, so way beyond the transitory stage. We’ve already highlighted the UK number but the 10yr German breakeven (+7.6bps) saw its biggest daily increase in nearly a year, hitting a fresh 8-year high of 1.796%. Its Italian counterpart (+8.3bps) hit a new high for the decade at 1.715%. Even in the US, where breakevens have been trading in a fairly tight band recently, we saw a +6.8bps rise to 2.460%, which is its highest closing level in 4 months.

With breakevens moving sharply higher, this was clearly bad news for sovereign bonds, which sold off on both sides of the Atlantic across different maturities. Yields on 10yr Treasuries were up +4.7bps to 1.53%, with the entirety of that move resulting from higher inflation expectations rather than real rates, which actually fell on the day (-2.0bps). Over in Europe, gilts saw the biggest declines as investors continue to anticipate a potential BoE rate hike in the coming months, with 10yr yields rising by a further +7.3bps, whilst the spread of UK 10yr yields over bunds actually widened to its biggest level since the day of the Brexit referendum in 2016. That said, yields were also moving higher on the continent, with those on 10yr bunds (+2.6bps), OATs (+2.5bps) and BTPs (+3.0bps) all moving to their highest level in 3 months.

The case for inflation was given further support by the September PMI releases, which pointed to supply-chain issues across multiple countries. In the Euro Area, the composite PMI was revised up a tenth to 56.2, but the release said that input prices were rising at the joint-fastest on record. Over in the US, the composite PMI was also revised up half a point from the flash reading to 55.0, but the release similarly mentioned labour shortages and capacity constraints holding back growth. The US composite PMI of 55.0 was its lowest level in a year, albeit still above the 50-mark that separates expansion from contraction. The September US ISM services reading rose 0.2 to 61.9 (59.9 expected) with the report suggesting that delta variant concerns are easing as 17 of the 18 industries reported growth over the last month. However, there were still comments in the report highlighting supply chain issues and some inability to retain or hire labour.

In spite of the renewed inflation concerns clouding the Q4 outlook, the major equity indices managed to post a decent rebound from Monday’s losses, although it’s worth noting that many were only recouping those declines rather than advancing to new heights. The S&P 500 was up +1.05%, so still just beneath where it started the week after Monday’s -1.30% decline, whilst the NASDAQ was up +1.25% and the FANG+ recovered +2.23%. It was the 4th straight day that the S&P 500 moved more than 1% in either direction, the longest such streak since November 2020. While yesterday saw a broad-based rally with 21 of the 24 S&P 500 industries gaining, financials were the big outperformer thanks to higher yields. The US Financials sectors added +1.78%, whilst in Europe the STOXX Banks index (+3.99%) hit a post-pandemic high, well outpacing the broader STOXX 600 (+1.17%).

Overnight in Asia, most markets continued to slide with the Nikkei (-1.00%), Kospi (-1.00%), Hang Seng (-0.71%) and Australia’s ASX (-0.68%) all moving lower on the back of higher energy prices and inflation concerns. In Japan the Nikkei extended losses for an eighth consecutive session on concerns that new PM Fumio Kishida could be outlining a redistribution plan that includes higher taxes, including on capital gains, although he’s yet to outline the specifics of the policy. Separately the Reserve Bank of New Zealand joined the club of central banks raising rates, hiking by 25bps in a move that was the first rate rise in seven years, as they also indicated more hikes might be warranted. In terms of the latest on Evergrande, the firm is still yet to release details of the “major transaction” we mentioned on Monday, with the company’s shares still suspended, whilst Fantasia saw its long-term rating cut to selective default by S&P yesterday, down from CCC. US futures are pointing to further declines later with those on the S&P 500 down -0.39%.

Turning to the ongoing debt ceiling saga, the US Senate has a cloture vote scheduled for today to suspend the ceiling, but Republican leadership are confident they can block the measure and force the Democrats to raise the debt ceiling unilaterally using the budget reconciliation process (which only requires a simple majority of votes in the Senate). So this would tie a move on the debt ceiling into the reconciliation bill that includes President Biden’s “Build Back Better” economic plan. However, the Democrats are maintaining that the reconciliation process takes too long, with the Treasury estimating it will run out of funding around October 18, and have made the case that both parties have a duty to raise the ceiling, since it reflects debts racked up under administrations of both parties rather than just the Democrats. Irrespective of the debt ceiling though, it does continue to sound like there’s movement toward a deal amongst Congressional Democrats on the size of the plan, withSenator Manchin (a key Democratic moderate) reportedly not ruling out a $1.9-2.2 trillion spending plan price tag, which is also the level that President Biden had been floating to House Democrats last week.

Speaking of the Senate, yesterday Senator Elizabeth Warren had yet more strong words for Fed Chair Powell. Warren has already said she opposes giving Powell a second term as the Fed Chair, and yesterday’s speech criticised him for his lack of oversight of the trading activity of Federal Reserve officials. She said Powell has “failed as a leader” and that there are “legitimate questions about conflicts of interest and insider trading” around the actions of certain Fed Officials. This follows her actions on Monday, when she called the SEC to investigate Federal Reserve officials for insider trading. At the same time, Chair Powell asked its inspector general to conduct a review of trades made by Federal Reserve members to ensure they complied with the law and Fed rules. While a White House spokesperson said yesterday that President Biden continues to have confidence in Chair Powell, Senator Warren may be setting up to float an alternative candidate for Chair in the coming weeks ahead of Powell’s term ending early next year.

To the day ahead now, and data releases include German factory orders for August, the German and UK construction PMIs for September, Euro Area retail sales for August, and the ADP’s September report on private payrolls from the US. From central banks, we’ll also hear from the ECB’s Centeno.

Government

Are Voters Recoiling Against Disorder?

Are Voters Recoiling Against Disorder?

Authored by Michael Barone via The Epoch Times (emphasis ours),

The headlines coming out of the Super…

Share this:

Authored by Michael Barone via The Epoch Times (emphasis ours),

The headlines coming out of the Super Tuesday primaries have got it right. Barring cataclysmic changes, Donald Trump and Joe Biden will be the Republican and Democratic nominees for president in 2024.

With Nikki Haley’s withdrawal, there will be no more significantly contested primaries or caucuses—the earliest both parties’ races have been over since something like the current primary-dominated system was put in place in 1972.

The primary results have spotlighted some of both nominees’ weaknesses.

Donald Trump lost high-income, high-educated constituencies, including the entire metro area—aka the Swamp. Many but by no means all Haley votes there were cast by Biden Democrats. Mr. Trump can’t afford to lose too many of the others in target states like Pennsylvania and Michigan.

Majorities and large minorities of voters in overwhelmingly Latino counties in Texas’s Rio Grande Valley and some in Houston voted against Joe Biden, and even more against Senate nominee Rep. Colin Allred (D-Texas).

Returns from Hispanic precincts in New Hampshire and Massachusetts show the same thing. Mr. Biden can’t afford to lose too many Latino votes in target states like Arizona and Georgia.

When Mr. Trump rode down that escalator in 2015, commentators assumed he’d repel Latinos. Instead, Latino voters nationally, and especially the closest eyewitnesses of Biden’s open-border policy, have been trending heavily Republican.

High-income liberal Democrats may sport lawn signs proclaiming, “In this house, we believe ... no human is illegal.” The logical consequence of that belief is an open border. But modest-income folks in border counties know that flows of illegal immigrants result in disorder, disease, and crime.

There is plenty of impatience with increased disorder in election returns below the presidential level. Consider Los Angeles County, America’s largest county, with nearly 10 million people, more people than 40 of the 50 states. It voted 71 percent for Mr. Biden in 2020.

Current returns show county District Attorney George Gascon winning only 21 percent of the vote in the nonpartisan primary. He’ll apparently face Republican Nathan Hochman, a critic of his liberal policies, in November.

Gascon, elected after the May 2020 death of counterfeit-passing suspect George Floyd in Minneapolis, is one of many county prosecutors supported by billionaire George Soros. His policies include not charging juveniles as adults, not seeking higher penalties for gang membership or use of firearms, and bringing fewer misdemeanor cases.

The predictable result has been increased car thefts, burglaries, and personal robberies. Some 120 assistant district attorneys have left the office, and there’s a backlog of 10,000 unprosecuted cases.

More than a dozen other Soros-backed and similarly liberal prosecutors have faced strong opposition or have left office.

St. Louis prosecutor Kim Gardner resigned last May amid lawsuits seeking her removal, Milwaukee’s John Chisholm retired in January, and Baltimore’s Marilyn Mosby was defeated in July 2022 and convicted of perjury in September 2023. Last November, Loudoun County, Virginia, voters (62 percent Biden) ousted liberal Buta Biberaj, who declined to prosecute a transgender student for assault, and in June 2022 voters in San Francisco (85 percent Biden) recalled famed radical Chesa Boudin.

Similarly, this Tuesday, voters in San Francisco passed ballot measures strengthening police powers and requiring treatment of drug-addicted welfare recipients.

In retrospect, it appears the Floyd video, appearing after three months of COVID-19 confinement, sparked a frenzied, even crazed reaction, especially among the highly educated and articulate. One fatal incident was seen as proof that America’s “systemic racism” was worse than ever and that police forces should be defunded and perhaps abolished.

2020 was “the year America went crazy,” I wrote in January 2021, a year in which police funding was actually cut by Democrats in New York, Los Angeles, San Francisco, Seattle, and Denver. A year in which young New York Times (NYT) staffers claimed they were endangered by the publication of Sen. Tom Cotton’s (R-Ark.) opinion article advocating calling in military forces if necessary to stop rioting, as had been done in Detroit in 1967 and Los Angeles in 1992. A craven NYT publisher even fired the editorial page editor for running the article.

Evidence of visible and tangible discontent with increasing violence and its consequences—barren and locked shelves in Manhattan chain drugstores, skyrocketing carjackings in Washington, D.C.—is as unmistakable in polls and election results as it is in daily life in large metropolitan areas. Maybe 2024 will turn out to be the year even liberal America stopped acting crazy.

Chaos and disorder work against incumbents, as they did in 1968 when Democrats saw their party’s popular vote fall from 61 percent to 43 percent.

Views expressed in this article are opinions of the author and do not necessarily reflect the views of The Epoch Times or ZeroHedge.

Government

Veterans Affairs Kept COVID-19 Vaccine Mandate In Place Without Evidence

Veterans Affairs Kept COVID-19 Vaccine Mandate In Place Without Evidence

Authored by Zachary Stieber via The Epoch Times (emphasis ours),

The…

Share this:

Authored by Zachary Stieber via The Epoch Times (emphasis ours),

The U.S. Department of Veterans Affairs (VA) reviewed no data when deciding in 2023 to keep its COVID-19 vaccine mandate in place.

VA Secretary Denis McDonough said on May 1, 2023, that the end of many other federal mandates “will not impact current policies at the Department of Veterans Affairs.”

He said the mandate was remaining for VA health care personnel “to ensure the safety of veterans and our colleagues.”

Mr. McDonough did not cite any studies or other data. A VA spokesperson declined to provide any data that was reviewed when deciding not to rescind the mandate. The Epoch Times submitted a Freedom of Information Act for “all documents outlining which data was relied upon when establishing the mandate when deciding to keep the mandate in place.”

The agency searched for such data and did not find any.

“The VA does not even attempt to justify its policies with science, because it can’t,” Leslie Manookian, president and founder of the Health Freedom Defense Fund, told The Epoch Times.

“The VA just trusts that the process and cost of challenging its unfounded policies is so onerous, most people are dissuaded from even trying,” she added.

The VA’s mandate remains in place to this day.

The VA’s website claims that vaccines “help protect you from getting severe illness” and “offer good protection against most COVID-19 variants,” pointing in part to observational data from the U.S. Centers for Disease Control and Prevention (CDC) that estimate the vaccines provide poor protection against symptomatic infection and transient shielding against hospitalization.

There have also been increasing concerns among outside scientists about confirmed side effects like heart inflammation—the VA hid a safety signal it detected for the inflammation—and possible side effects such as tinnitus, which shift the benefit-risk calculus.

President Joe Biden imposed a slate of COVID-19 vaccine mandates in 2021. The VA was the first federal agency to implement a mandate.

President Biden rescinded the mandates in May 2023, citing a drop in COVID-19 cases and hospitalizations. His administration maintains the choice to require vaccines was the right one and saved lives.

“Our administration’s vaccination requirements helped ensure the safety of workers in critical workforces including those in the healthcare and education sectors, protecting themselves and the populations they serve, and strengthening their ability to provide services without disruptions to operations,” the White House said.

Some experts said requiring vaccination meant many younger people were forced to get a vaccine despite the risks potentially outweighing the benefits, leaving fewer doses for older adults.

“By mandating the vaccines to younger people and those with natural immunity from having had COVID, older people in the U.S. and other countries did not have access to them, and many people might have died because of that,” Martin Kulldorff, a professor of medicine on leave from Harvard Medical School, told The Epoch Times previously.

The VA was one of just a handful of agencies to keep its mandate in place following the removal of many federal mandates.

“At this time, the vaccine requirement will remain in effect for VA health care personnel, including VA psychologists, pharmacists, social workers, nursing assistants, physical therapists, respiratory therapists, peer specialists, medical support assistants, engineers, housekeepers, and other clinical, administrative, and infrastructure support employees,” Mr. McDonough wrote to VA employees at the time.

“This also includes VA volunteers and contractors. Effectively, this means that any Veterans Health Administration (VHA) employee, volunteer, or contractor who works in VHA facilities, visits VHA facilities, or provides direct care to those we serve will still be subject to the vaccine requirement at this time,” he said. “We continue to monitor and discuss this requirement, and we will provide more information about the vaccination requirements for VA health care employees soon. As always, we will process requests for vaccination exceptions in accordance with applicable laws, regulations, and policies.”

The version of the shots cleared in the fall of 2022, and available through the fall of 2023, did not have any clinical trial data supporting them.

A new version was approved in the fall of 2023 because there were indications that the shots not only offered temporary protection but also that the level of protection was lower than what was observed during earlier stages of the pandemic.

Ms. Manookian, whose group has challenged several of the federal mandates, said that the mandate “illustrates the dangers of the administrative state and how these federal agencies have become a law unto themselves.”

Spread & Containment

The Coming Of The Police State In America

The Coming Of The Police State In America

Authored by Jeffrey Tucker via The Epoch Times,

The National Guard and the State Police are now…

Share this:

{kind=link}

{kind=link}

{kind=link}

Authored by Jeffrey Tucker via The Epoch Times,

The National Guard and the State Police are now patrolling the New York City subway system in an attempt to do something about the explosion of crime. As part of this, there are bag checks and new surveillance of all passengers. No legislation, no debate, just an edict from the mayor.

{kind=link}

Many citizens who rely on this system for transportation might welcome this. It’s a city of strict gun control, and no one knows for sure if they have the right to defend themselves. Merchants have been harassed and even arrested for trying to stop looting and pillaging in their own shops.

The message has been sent: Only the police can do this job. Whether they do it or not is another matter.

Things on the subway system have gotten crazy. If you know it well, you can manage to travel safely, but visitors to the city who take the wrong train at the wrong time are taking grave risks.

In actual fact, it’s guaranteed that this will only end in confiscating knives and other things that people carry in order to protect themselves while leaving the actual criminals even more free to prey on citizens.

The law-abiding will suffer and the criminals will grow more numerous. It will not end well.

When you step back from the details, what we have is the dawning of a genuine police state in the United States. It only starts in New York City. Where is the Guard going to be deployed next? Anywhere is possible.

If the crime is bad enough, citizens will welcome it. It must have been this way in most times and places that when the police state arrives, the people cheer.

We will all have our own stories of how this came to be. Some might begin with the passage of the Patriot Act and the establishment of the Department of Homeland Security in 2001. Some will focus on gun control and the taking away of citizens’ rights to defend themselves.

My own version of events is closer in time. It began four years ago this month with lockdowns. That’s what shattered the capacity of civil society to function in the United States. Everything that has happened since follows like one domino tumbling after another.

It goes like this:

1) lockdown,

2) loss of moral compass and spreading of loneliness and nihilism,

3) rioting resulting from citizen frustration, 4) police absent because of ideological hectoring,

5) a rise in uncontrolled immigration/refugees,

6) an epidemic of ill health from substance abuse and otherwise,

7) businesses flee the city

8) cities fall into decay, and that results in

9) more surveillance and police state.

The 10th stage is the sacking of liberty and civilization itself.

It doesn’t fall out this way at every point in history, but this seems like a solid outline of what happened in this case. Four years is a very short period of time to see all of this unfold. But it is a fact that New York City was more-or-less civilized only four years ago. No one could have predicted that it would come to this so quickly.

But once the lockdowns happened, all bets were off. Here we had a policy that most directly trampled on all freedoms that we had taken for granted. Schools, businesses, and churches were slammed shut, with various levels of enforcement. The entire workforce was divided between essential and nonessential, and there was widespread confusion about who precisely was in charge of designating and enforcing this.

It felt like martial law at the time, as if all normal civilian law had been displaced by something else. That something had to do with public health, but there was clearly more going on, because suddenly our social media posts were censored and we were being asked to do things that made no sense, such as mask up for a virus that evaded mask protection and walk in only one direction in grocery aisles.

Vast amounts of the white-collar workforce stayed home—and their kids, too—until it became too much to bear. The city became a ghost town. Most U.S. cities were the same.

As the months of disaster rolled on, the captives were let out of their houses for the summer in order to protest racism but no other reason. As a way of excusing this, the same public health authorities said that racism was a virus as bad as COVID-19, so therefore it was permitted.

The protests had turned to riots in many cities, and the police were being defunded and discouraged to do anything about the problem. Citizens watched in horror as downtowns burned and drug-crazed freaks took over whole sections of cities. It was like every standard of decency had been zapped out of an entire swath of the population.

Meanwhile, large checks were arriving in people’s bank accounts, defying every normal economic expectation. How could people not be working and get their bank accounts more flush with cash than ever? There was a new law that didn’t even require that people pay rent. How weird was that? Even student loans didn’t need to be paid.

By the fall, recess from lockdown was over and everyone was told to go home again. But this time they had a job to do: They were supposed to vote. Not at the polling places, because going there would only spread germs, or so the media said. When the voting results finally came in, it was the absentee ballots that swung the election in favor of the opposition party that actually wanted more lockdowns and eventually pushed vaccine mandates on the whole population.

The new party in control took note of the large population movements out of cities and states that they controlled. This would have a large effect on voting patterns in the future. But they had a plan. They would open the borders to millions of people in the guise of caring for refugees. These new warm bodies would become voters in time and certainly count on the census when it came time to reapportion political power.

Meanwhile, the native population had begun to swim in ill health from substance abuse, widespread depression, and demoralization, plus vaccine injury. This increased dependency on the very institutions that had caused the problem in the first place: the medical/scientific establishment.

The rise of crime drove the small businesses out of the city. They had barely survived the lockdowns, but they certainly could not survive the crime epidemic. This undermined the tax base of the city and allowed the criminals to take further control.

The same cities became sanctuaries for the waves of migrants sacking the country, and partisan mayors actually used tax dollars to house these invaders in high-end hotels in the name of having compassion for the stranger. Citizens were pushed out to make way for rampaging migrant hordes, as incredible as this seems.

But with that, of course, crime rose ever further, inciting citizen anger and providing a pretext to bring in the police state in the form of the National Guard, now tasked with cracking down on crime in the transportation system.

What’s the next step? It’s probably already here: mass surveillance and censorship, plus ever-expanding police power. This will be accompanied by further population movements, as those with the means to do so flee the city and even the country and leave it for everyone else to suffer.

As I tell the story, all of this seems inevitable. It is not. It could have been stopped at any point. A wise and prudent political leadership could have admitted the error from the beginning and called on the country to rediscover freedom, decency, and the difference between right and wrong. But ego and pride stopped that from happening, and we are left with the consequences.

The government grows ever bigger and civil society ever less capable of managing itself in large urban centers. Disaster is unfolding in real time, mitigated only by a rising stock market and a financial system that has yet to fall apart completely.

Are we at the middle stages of total collapse, or at the point where the population and people in leadership positions wise up and decide to put an end to the downward slide? It’s hard to know. But this much we do know: There is a growing pocket of resistance out there that is fed up and refuses to sit by and watch this great country be sacked and taken over by everything it was set up to prevent.

Walmart launches clever answer to Target’s new membership program

EyePoint poaches medical chief from Apellis; Sandoz CFO, longtime BioNTech exec to retire

Wendy’s has a new deal for daylight savings time haters

Veterans Affairs Kept COVID-19 Vaccine Mandate In Place Without Evidence

The Coming Of The Police State In America

When Military Rule Supplants Democracy

Catastrophic Risk: Investing and Business Implications

Where Is R‑Star and the End of the Refi Boom: The Top 5 Posts of 2023

Mortgage rates fall as labor market normalizes

The Digest #187

-

Uncategorized2 weeks ago

Uncategorized2 weeks agoAll Of The Elements Are In Place For An Economic Crisis Of Staggering Proportions

-

Uncategorized1 month ago

Uncategorized1 month agoCathie Wood sells a major tech stock (again)

-

Uncategorized3 weeks ago

Uncategorized3 weeks agoCalifornia Counties Could Be Forced To Pay $300 Million To Cover COVID-Era Program

-

Uncategorized2 weeks ago

Uncategorized2 weeks agoApparel Retailer Express Moving Toward Bankruptcy

-

Uncategorized3 weeks ago

Uncategorized3 weeks agoIndustrial Production Decreased 0.1% in January

-

International2 days ago

Walmart launches clever answer to Target’s new membership program

-

Uncategorized3 weeks ago

Uncategorized3 weeks agoRFK Jr: The Wuhan Cover-Up & The Rise Of The Biowarfare-Industrial Complex

-

International2 days ago

EyePoint poaches medical chief from Apellis; Sandoz CFO, longtime BioNTech exec to retire