Government

Futures Tumble Amid Sudden Fears Over “Dramatically” New Covid Strain With “Extremely High Number” Of Mutations

Futures Tumble Amid Sudden Fears Over "Dramatically" New Covid Strain With "Extremely High Number" Of Mutations

Futures are sliding on Thursday night when, with most US traders snoring in a tryptophan coma, the world is suddenly freaking…

Share this:

Futures are sliding on Thursday night when, with most US traders snoring in a tryptophan coma, the world is suddenly freaking out, and algos are hitting bids, amid fears that a new coronavirus strain detected in South Africa, known as B.1.1529, reportedly carries an "extremely high number" of mutations and is “clearly very different” from previous incarnations, which may drive further waves of disease by evading the body’s defenses South African scientists said.

Translation: a new wave of restrictions, more lockdowns, and - eventually - trillions in new stimmies are coming... an outcome so "unexpected", we rhetorically asked if this was the endgame just one week ago.

Is this next lockdown going to result in more stimmies?

— zerohedge (@zerohedge) November 18, 2021

According to the Guardian, only 10 cases in three countries have been confirmed by genomic sequencing (and up to 100 suspected), but that is more than enough for the Pharma-Government complex to set the wheels of widespread social panic and future lockdowns in motion and, according to the liberal outlet, "the variant has sparked serious concern among some researchers because a number of the mutations may help the virus evade immunity." Which of course is a polite way for Bill Gates to suggest you panic.

According to reports, the new B.1.1.529 variant has 32 mutations in the spike protein, the part of the virus that most vaccines use to prime the immune system against Covid. Mutations in the spike protein make it harder for immune cells to attack the pathogen, just as so many vaccine skeptics have been warning for the past year when making the point that taking inefficient medications shoved down the population's throats (such as those from Pfizer and Moderna) that do not serve as real vaccines but merely paliatives, will only lead to more dangerous and weaponized versions of the virus.

That's precisely what is happening now.

The variant was first spotted in Botswana, where three cases have now been sequenced. Six more have been confirmed in South Africa, and one in Hong Kong in a traveller returning from South Africa.

Botswana’s health ministry confirmed in a statement that four cases of the new variant were detected in people who were all fully vaccinated. All four were tested before their planned travel. One sample was also detected in Hong Kong, carried by a traveler from South Africa, South African scientists said.

With over 1,200 new infections, South Africa’s daily infection rate is much lower than in Germany, where new cases are driving a wave. However, the density of mutations on this new variant raises fears that it could be highly contagious, leading scientists to sound the alarm early.

“This variant did surprise us, it has a big jump in evolution, many more mutations than we expected, especially after a very severe third wave of Delta,” said Tulio de Oliveira, director of the KwaZulu-Natal Research and Innovation Sequencing Platform.

The B1.1.529 variant has a “very unusual constellation of mutations,” with more than 30 mutations in the spike protein alone, said Mr. de Oliveira. On the ACE2 receptor — the protein that helps to create an entry point for the coronavirus to infect human cells — the new variant has 10 mutations. In comparison, the Beta variant has three, the Delta variant has two, said Mr. de Oliveira.

Dr Tom Peacock, a virologist at Imperial College London, agrees with Oliveira. Peacock posted details of the new variant on a genome-sharing website, noting that the “incredibly high amount of spike mutations suggest this could be of real concern”.

In a series of tweets, Peacock said it “very, very much should be monitored due to that horrific spike profile.”

For those interested this has an NTD insertion at the NTD insertion hotspot (at aa214) which shows high likelihood of being host-derived (from host TMEM245 mRNA) pic.twitter.com/huNZbgEEsv

— Tom Peacock (@PeacockFlu) November 23, 2021

But, as some cynics pointed out on twitter, "the Strangelove who provided that convenient media clickbait epithet 'horrifying' has also admitted it may be LESS not more of a danger" and indeed, the Guardian report notes that it may turn out to be an “odd cluster” that is not very transmissible. “I hope that’s the case,” he wrote.

That new, scary "#Variant of concern" about which the hype is again building? Well, the Strangelove who provided that convenient media clickabit epithet 'horrifying' has also admitted it may be LESS not more of a danger.

— Wild Goose #TNCM (@TrueSinews) November 25, 2021

They are SO transparent, aren't they?#COVID19(33) pic.twitter.com/xlPQwzYiaT

Perhaps even more importantly, it also appears that the Chinese were busy splicing away in the past few months (this time probably without Dr Fauci's money): according to Peacock, the this variant contains "not one, but two furin cleavage site mutations - P681H (seen in Alpha, Mu, some Gamma, B.1.1.318) combined with N679K (seen in C.1.2 amongst others)." As Peacock notes, "this is the first time I've seen two of these mutations in a single variant."

Why does this matter? Because as even the reputable Nature mag recently noted, researchers have asked Covid's "furin cleavage site — a feature that helps it to enter cells — is evidence of engineering, because SARS-CoV-2 has these sites but its closest relatives don’t. The furin cleavage site is important because it's in the virus's spike protein, and cleavage of the protein at that site is necessary for the virus to infect cells."

Translation: use of the furin cleavage sites is how covid would be genetically-engineered inside, say, a BSL-4 lab in China... of which the only one can be found in Wuhan.

In any case, while nobody knows yet what the spike protein mutation cluster actually does yet, the speculation that it will lead to another wave of global infections is already in the wild. Sure enough, Ravi Gupta, a professor of clinical microbiology at Cambridge University, said work in his lab found that two of the mutations on B.1.1.529 increased infectivity and reduced antibody recognition. “It does certainly look a significant concern based on the mutations present,” he said. “However, a key property of the virus that is unknown is its infectiousness, as that is what appears to have primarily driven the Delta variant. Immune escape is only part of the picture of what may happen.”

Prof Francois Balloux, the director of the UCL Genetics Institute, said the large number of mutations in the variant apparently accumulated in a “single burst”, suggesting it may have evolved during a chronic infection in a person with a weakened immune system, possibly an untreated HIV/Aids patient.

“I would definitely expect it to be poorly recognized by neutralizing antibodies relative to Alpha or Delta,” he added.

Translation: in terms of vaccines, B.1.1.529 could well represent an entirely new disease, as the existing neutralizing antibodies will have little to no impact on a virus with all these mutations. Which is music to the ears of politicians who have just the catalyst to order a whole new round of lockdowns and, critically, stimmies that keep them in power for another quarter or two.

Case in point, just as news of the new strain emerged, the U.K. announced it will temporarily ban flights from South Africa and five neighboring countries (Namibia, Lesotho, Eswatini, Zimbabwe and Botswana) over worries about the new covid variant. The travel restrictions go into effect at noon Friday and are a precautionary measure to keep the spread of the new variant in check, Health Secretary Sajid Javid said. The six African countries will be placed on the U.K.’s red list as of Sunday, requiring travelers to quarantine in hotels upon arrival.

“As part of our close surveillance of variants across the world, we have become aware of the spread of a new potentially concerning variant,” Javid said in a statement, adding that the new strain it’s now under investigation.

Israel also has banned travel from the six countries, along with Mozambique, another neighbor of South Africa, BNO News said in a tweet, without citing the source of the information.

The U.K.’s move is a further blow to the airline industry, which was starting to recover from earlier travel restrictions and lockdowns but now faces fresh curbs and a resurgent virus in parts of Europe. The measures announced Thursday mark the biggest change in the U.K.’s Covid travel rules since the so-called traffic light system was overhauled earlier in the autumn to ease border crossings. From 500 to 700 people daily arrive in the U.K. via South Africa on flights, a number that would normally be expected to increase in the next four to six weeks due to seasonal travel.

Of course, such bans never actually stop the virus from spreading, but they do ramp up the public frenzy about the new strain. And since B.1.1.529 is too long to pronounce, some time tomorrow we will have a new Greek letter to fear: according to the NYT, South African scientists will meet with the World Health Organization technical team on Friday, where authorities will assign a letter of the Greek alphabet to this one. It will take several weeks to see the impact of the new variant on hospitalizations and deaths and to study how it may interact with vaccines.

“Armed by our experience and understanding of the alpha and delta variants, we know that early action is far better than late action,” Ewan Birney, deputy director general of the European Molecular Biology Laboratory, said in a Science Media Centre briefing note. “It may turn out that this variant is not as large a threat as alpha and delta, but the potential consequences of not acting on the possibility it could be are serious.”

For those who wish to learn more about the new "horrifying" strain and superglue no less than 10 masks to their face, they can do so at this just released article from Nature "Heavily mutated coronavirus variant puts scientists on alert"

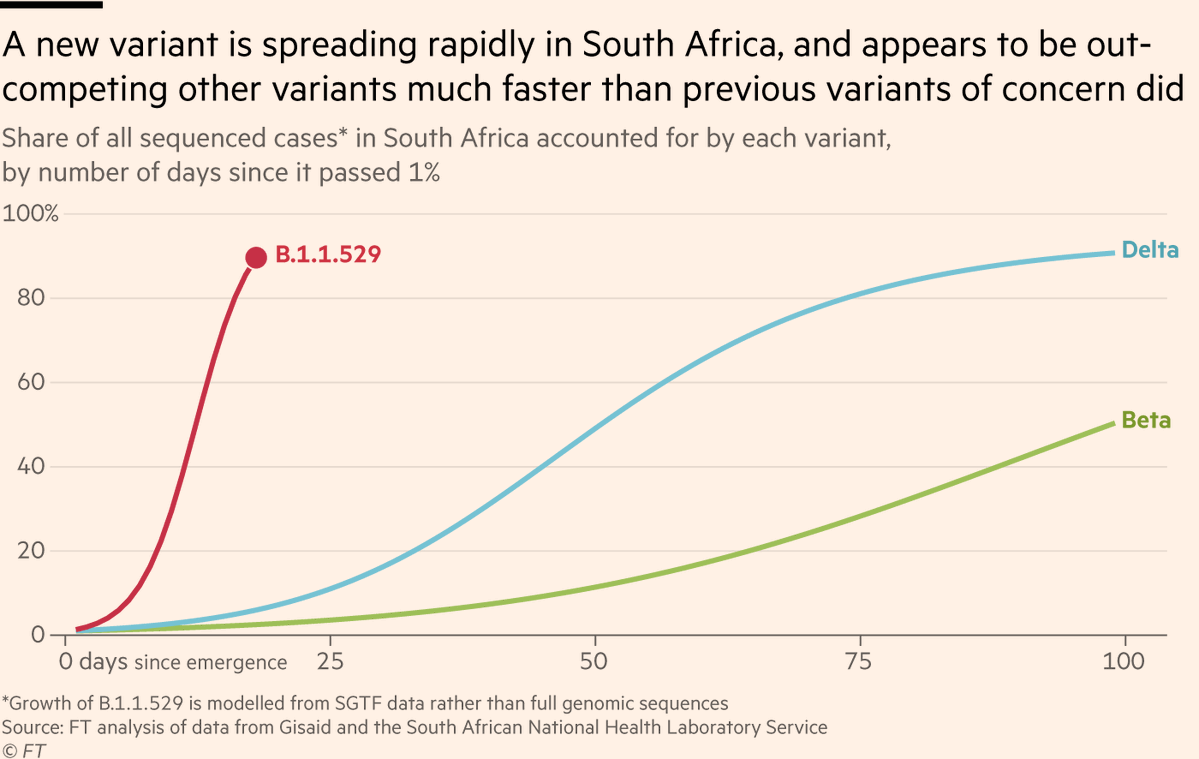

Everything we know so far on the new B.1.1.529 variant, for which there is an emergency @WHO meeting to reviewhttps://t.co/TmxGBi6IEv @nature by @ewencallaway @naturehttps://t.co/r9kHwg2zjWhttps://t.co/tBEct7F8M7 ????by @jburnmurdoch @FT pic.twitter.com/fe5pkIpqnW

— Eric Topol (@EricTopol) November 25, 2021

The sudden surge in fears that a new "delta" variant was coming was enough to spark a futures dump late on Thursday, and S&P 500 futures fell 0.6% as of 10:20 a.m. in Tokyo after news of a new coronavirus strain discovered in South Africa. Contracts on the Nasdaq 100 were down 0.3% (tech/growth stocks tend to do much better during lockdowns than value), and the broad MSCI Asia-Pac index was down 1.4% as worries about a new coronavirus variant discovered in South Africa were compounded by thinner liquidity in markets. .

Asia’s stock benchmark was on track for its worst day since Sept. 29, as selling on news about the latest Covid-19 variant detected in South Africa was exacerbated by thin liquidity. The MSCI Asia Pacific Index slumped as much as 1.4%, with financials and tech shares dragging the measure the most in a broad-based selloff. Japanese equities declined, leading losses in Asia, and the yen strengthened with some traders away for Thanksgiving celebrations.

"The fact we have North America off the desks means there’s a wall of buyers missing” at a time when there are “scary” headlines about the new Covid-19 variant, said Kyle Rodda, an analyst at IG Markets. According to Rodda, the virus-related headlines “may have caused a knee jerk reaction,” while “thinner markets make for more pronounced moves.” He added that some weakness through cyclicals, implying markets are also concerned about growth and an aggressive Fed that may slow the global economy.

Oil, an asset that is extremely sensitive to any future lockdowns, tumbled.

“Even before this news, virus cases were back on the rise in the U.S. and Europe, so investors are now wary of the possibility that with a new variant, infections could spread all at once,” said Sumitomo Mitsui DS Asset Management chief market strategist Masahiro Ichikawa.

There’s a risk the Nikkei 225 will break below the 29,000 mark; if it breaches that level, there’s a possibility the measure will finish the day in the 28,000-yen-range. “Today would have been a quiet day if not for the news of the variant.”

Ichikawa is right, only it's kinda the other way round, because this "heavily mutated variant" is just the deus ex both central bankers and politicians have been desperately hoping for: with Europe already locking down in several countries, expect a uniform global lockdown to follow in weeks, which will serve to reset the supply chain collapse and buy markets, pols and bankers about one or two quarters of time, during which expect several more trillion in stimmies, much more QE (to monetize the debt used to pay for the stimmies) and generally a rerun of the past 18 months only in a much more truncated timeline, which in turn will lead to a burst of inflation that will make the current soaring prices seems like Japan's deflationary debt trap.

International

Congress’ failure so far to deliver on promise of tens of billions in new research spending threatens America’s long-term economic competitiveness

A deal that avoided a shutdown also slashed spending for the National Science Foundation, putting it billions below a congressional target intended to…

Share this:

Federal spending on fundamental scientific research is pivotal to America’s long-term economic competitiveness and growth. But less than two years after agreeing the U.S. needed to invest tens of billions of dollars more in basic research than it had been, Congress is already seriously scaling back its plans.

A package of funding bills recently passed by Congress and signed by President Joe Biden on March 9, 2024, cuts the current fiscal year budget for the National Science Foundation, America’s premier basic science research agency, by over 8% relative to last year. That puts the NSF’s current allocation US$6.6 billion below targets Congress set in 2022.

And the president’s budget blueprint for the next fiscal year, released on March 11, doesn’t look much better. Even assuming his request for the NSF is fully funded, it would still, based on my calculations, leave the agency a total of $15 billion behind the plan Congress laid out to help the U.S. keep up with countries such as China that are rapidly increasing their science budgets.

I am a sociologist who studies how research universities contribute to the public good. I’m also the executive director of the Institute for Research on Innovation and Science, a national university consortium whose members share data that helps us understand, explain and work to amplify those benefits.

Our data shows how underfunding basic research, especially in high-priority areas, poses a real threat to the United States’ role as a leader in critical technology areas, forestalls innovation and makes it harder to recruit the skilled workers that high-tech companies need to succeed.

A promised investment

Less than two years ago, in August 2022, university researchers like me had reason to celebrate.

Congress had just passed the bipartisan CHIPS and Science Act. The science part of the law promised one of the biggest federal investments in the National Science Foundation in its 74-year history.

The CHIPS act authorized US$81 billion for the agency, promised to double its budget by 2027 and directed it to “address societal, national, and geostrategic challenges for the benefit of all Americans” by investing in research.

But there was one very big snag. The money still has to be appropriated by Congress every year. Lawmakers haven’t been good at doing that recently. As lawmakers struggle to keep the lights on, fundamental research is quickly becoming a casualty of political dysfunction.

Research’s critical impact

That’s bad because fundamental research matters in more ways than you might expect.

For instance, the basic discoveries that made the COVID-19 vaccine possible stretch back to the early 1960s. Such research investments contribute to the health, wealth and well-being of society, support jobs and regional economies and are vital to the U.S. economy and national security.

Lagging research investment will hurt U.S. leadership in critical technologies such as artificial intelligence, advanced communications, clean energy and biotechnology. Less support means less new research work gets done, fewer new researchers are trained and important new discoveries are made elsewhere.

But disrupting federal research funding also directly affects people’s jobs, lives and the economy.

Businesses nationwide thrive by selling the goods and services – everything from pipettes and biological specimens to notebooks and plane tickets – that are necessary for research. Those vendors include high-tech startups, manufacturers, contractors and even Main Street businesses like your local hardware store. They employ your neighbors and friends and contribute to the economic health of your hometown and the nation.

Nearly a third of the $10 billion in federal research funds that 26 of the universities in our consortium used in 2022 directly supported U.S. employers, including:

A Detroit welding shop that sells gases many labs use in experiments funded by the National Institutes of Health, National Science Foundation, Department of Defense and Department of Energy.

A Dallas-based construction company that is building an advanced vaccine and drug development facility paid for by the Department of Health and Human Services.

More than a dozen Utah businesses, including surveyors, engineers and construction and trucking companies, working on a Department of Energy project to develop breakthroughs in geothermal energy.

When Congress shortchanges basic research, it also damages businesses like these and people you might not usually associate with academic science and engineering. Construction and manufacturing companies earn more than $2 billion each year from federally funded research done by our consortium’s members.

Jobs and innovation

Disrupting or decreasing research funding also slows the flow of STEM – science, technology, engineering and math – talent from universities to American businesses. Highly trained people are essential to corporate innovation and to U.S. leadership in key fields, such as AI, where companies depend on hiring to secure research expertise.

In 2022, federal research grants paid wages for about 122,500 people at universities that shared data with my institute. More than half of them were students or trainees. Our data shows that they go on to many types of jobs but are particularly important for leading tech companies such as Google, Amazon, Apple, Facebook and Intel.

That same data lets me estimate that over 300,000 people who worked at U.S. universities in 2022 were paid by federal research funds. Threats to federal research investments put academic jobs at risk. They also hurt private sector innovation because even the most successful companies need to hire people with expert research skills. Most people learn those skills by working on university research projects, and most of those projects are federally funded.

High stakes

If Congress doesn’t move to fund fundamental science research to meet CHIPS and Science Act targets – and make up for the $11.6 billion it’s already behind schedule – the long-term consequences for American competitiveness could be serious.

Over time, companies would see fewer skilled job candidates, and academic and corporate researchers would produce fewer discoveries. Fewer high-tech startups would mean slower economic growth. America would become less competitive in the age of AI. This would turn one of the fears that led lawmakers to pass the CHIPS and Science Act into a reality.

Ultimately, it’s up to lawmakers to decide whether to fulfill their promise to invest more in the research that supports jobs across the economy and in American innovation, competitiveness and economic growth. So far, that promise is looking pretty fragile.

This is an updated version of an article originally published on Jan. 16, 2024.

Jason Owen-Smith receives research support from the National Science Foundation, the National Institutes of Health, the Alfred P. Sloan Foundation and Wellcome Leap.

economic growth covid-19 grants congress vaccine chinaInternational

What’s Driving Industrial Development in the Southwest U.S.

The post-COVID-19 pandemic pipeline, supply imbalances, investment and construction challenges: these are just a few of the topics address by a powerhouse…

Share this:

The post-COVID-19 pandemic pipeline, supply imbalances, investment and construction challenges: these are just a few of the topics address by a powerhouse panel of executives in industrial real estate this week at NAIOP’s I.CON West in Long Beach, California. Led by Dawn McCombs, principal and Denver lead industrial specialist for Avison Young, the panel tackled some of the biggest issues facing the sector in the Western U.S.

Starting with the pandemic in 2020 and continuing through 2022, McCombs said, the industrial sector experienced a huge surge in demand, resulting in historic vacancies, rent growth and record deliveries. Operating fundamentals began to normalize in 2023 and construction starts declined, certainly impacting vacancy and absorption moving forward.

“Development starts dropped by 65% year-over-year across the U.S. last year. In Q4, we were down 25% from pre-COVID norms,” began Megan Creecy-Herman, president, U.S. West Region, Prologis, noting that all of that is setting us up to see an improvement of fundamentals in the market. “U.S. vacancy ended 2023 at about 5%, which is very healthy.”

Vacancies are expected to grow in Q1 and Q2, peaking mid-year at around 7%. Creecy-Herman expects to see an increase in absorption as customers begin to have confidence in the economy, and everyone gets some certainty on what the Fed does with interest rates.

“It’s an interesting dynamic to see such a great increase in rents, which have almost doubled in some markets,” said Reon Roski, CEO, Majestic Realty Co. “It’s healthy to see a slowing down… before [rents] go back up.”

Pre-pandemic, a lot of markets were used to 4-5% vacancy, said Brooke Birtcher Gustafson, fifth-generation president of Birtcher Development. “Everyone was a little tepid about where things are headed with a mediocre outlook for 2024, but much of this is normalizing in the Southwest markets.”

McCombs asked the panel where their companies found themselves in the construction pipeline when the Fed raised rates in 2022.

In Salt Lake City, said Angela Eldredge, chief operations officer at Price Real Estate, there is a typical 12-18-month lead time on construction materials. “As rates started to rise in 2022, lots of permits had already been pulled and construction starts were beginning, so those project deliveries were in fall 2023. [The slowdown] was good for our market because it kept rates high, vacancies lower and helped normalize the market to a healthy pace.”

A supply imbalance can stress any market, and Gustafson joked that the current imbalance reminded her of a favorite quote from the movie Super Troopers: “Desperation is a stinky cologne.” “We’re all still a little crazed where this imbalance has put us, but for the patient investor and owner, there will be a rebalancing and opportunity for the good quality real estate to pass the sniff test,” she said.

At Bircher, Gustafson said that mid-pandemic, there were predictions that one billion square feet of new product would be required to meet tenant demand, e-commerce growth and safety stock. That transition opened a great opportunity for investors to run at the goal. “In California, the entitlement process is lengthy, around 24-36 months to get from the start of an acquisition to the completion of a building,” she said. Fast forward to 2023-2024, a lot of what is being delivered in 2024 is the result of that chase.

“Being an optimistic developer, there is good news. The supply imbalance helped normalize what was an unsustainable surge in rents and land values,” she said. “It allowed corporate heads of real estate to proactively evaluate growth opportunities, opened the door for contrarian investors to land bank as values drop, and provided tenants with options as there is more product. Investment goals and strategies have shifted, and that’s created opportunity for buyers.”

“Developers only know how to run and develop as much as we can,” said Roski. “There are certain times in cycles that we are forced to slow down, which is a good thing. In the last few years, Majestic has delivered 12-14 million square feet, and this year we are developing 6-8 million square feet. It’s all part of the cycle.”

Creecy-Herman noted that compared to the other asset classes and opportunities out there, including office and multifamily, industrial remains much more attractive for investment. “That was absolutely one of the things that underpinned the amount of investment we saw in a relatively short time period,” she said.

Market rent growth across Los Angeles, Inland Empire and Orange County moved up more than 100% in a 24-month period. That created opportunities for landlords to flexible as they’re filling up their buildings. “Normalizing can be uncomfortable especially after that kind of historic high, but at the same time it’s setting us up for strong years ahead,” she said.

Issues that owners and landlords are facing with not as much movement in the market is driving a change in strategy, noted Gustafson. “Comps are all over the place,” she said. “You have to dive deep into every single deal that is done to understand it and how investment strategies are changing.”

Tenants experienced a variety of challenges in the pandemic years, from supply chain to labor shortages on the negative side, to increased demand for products on the positive, McCombs noted.

“Prologis has about 6,700 customers around the world, from small to large, and the universal lesson [from the pandemic] is taking a more conservative posture on inventories,” Creecy-Herman said. “Customers are beefing up inventories, and that conservatism in the supply chain is a lesson learned that’s going to stick with us for a long time.” She noted that the company has plenty of clients who want to take more space but are waiting on more certainty from the broader economy.

“E-commerce grew by 8% last year, and we think that’s going to accelerate to 10% this year. This is still less than 25% of all retail sales, so the acceleration we’re going to see in e-commerce… is going to drive the business forward for a long time,” she said.

Roski noted that customers continually re-evaluate their warehouse locations, expanding during the pandemic and now consolidating but staying within one delivery day of vast consumer bases.

“This is a generational change,” said Creecy-Herman. “Millions of young consumers have one-day delivery as a baseline for their shopping experience. Think of what this means for our business long term to help our customers meet these expectations.”

McCombs asked the panelists what kind of leasing activity they are experiencing as a return to normalcy is expected in 2024.

“During the pandemic, shifts in the ports and supply chain created a build up along the Mexican border,” said Roski, noting border towns’ importance to increased manufacturing in Mexico. A shift of populations out of California and into Arizona, Nevada, Texas and Florida have resulted in an expansion of warehouses in those markets.

Eldridge said that Salt Lake City’s “sweet spot” is 100-200 million square feet, noting that the market is best described as a mid-box distribution hub that is close to California and Midwest markets. “Our location opens up the entire U.S. to our market, and it’s continuing to grow,” she said.

The recent supply chain and West Coast port clogs prompted significant investment in nearshoring and port improvements. “Ports are always changing,” said Roski, listing a looming strike at East Coast ports, challenges with pirates in the Suez Canal, and water issues in the Panama Canal. “Companies used to fix on one port and that’s where they’d bring in their imports, but now see they need to be [bring product] in a couple of places.”

“Laredo, [Texas,] is one of the largest ports in the U.S., and there’s no water. It’s trucks coming across the border. Companies have learned to be nimble and not focused on one area,” she said.

“All of the markets in the southwest are becoming more interconnected and interdependent than they were previously,” Creecy-Herman said. “In Southern California, there are 10 markets within 500 miles with over 25 million consumers who spend, on average, 10% more than typical U.S. consumers.” Combined with the port complex, those fundamentals aren’t changing. Creecy-Herman noted that it’s less of a California exodus than it is a complementary strategy where customers are taking space in other markets as they grow. In the last 10 years, she noted there has been significant maturation of markets such as Las Vegas and Phoenix. As they’ve become more diversified, customers want to have a presence there.

In the last decade, Gustafson said, the consumer base has shifted. Tenants continue to change strategies to adapt, such as hub-and-spoke approaches. From an investment perspective, she said that strategies change weekly in response to market dynamics that are unprecedented.

McCombs said that construction challenges and utility constraints have been compounded by increased demand for water and power.

“Those are big issues from the beginning when we’re deciding on whether to buy the dirt, and another decision during construction,” Roski said. “In some markets, we order transformers more than a year before they are needed. Otherwise, the time comes [to use them] and we can’t get them. It’s a new dynamic of how leases are structured because it’s something that’s out of our control.” She noted that it’s becoming a bigger issue with electrification of cars, trucks and real estate, and the U.S. power grid is not prepared to handle it.

Salt Lake City’s land constraints play a role in site selection, said Eldridge. “Land values of areas near water are skyrocketing.”

The panelists agreed that a favorable outlook is ahead for 2024, and today’s rebalancing will drive a healthy industry in the future as demand and rates return to normalized levels, creating opportunities for investors, developers and tenants.

This post is brought to you by JLL, the social media and conference blog sponsor of NAIOP’s I.CON West 2024. Learn more about JLL at www.us.jll.com or www.jll.ca.

fed pandemic covid-19 real estate interest rates mexicoGovernment

Buyouts can bring relief from medical debt, but they’re far from a cure

Local governments are increasingly buying – and forgiving – their residents’ medical debt.

Share this:

{kind=link}

One in 10 Americans carry medical debt, while 2 in 5 are underinsured and at risk of not being able to pay their medical bills.

This burden crushes millions of families under mounting bills and contributes to the widening gap between rich and poor.

Some relief has come with a wave of debt buyouts by county and city governments, charities and even fast-food restaurants that pay pennies on the dollar to clear enormous balances. But as a health policy and economics researcher who studies out-of-pocket medical expenses, I think these buyouts are only a partial solution.

A quick fix that works

Over the past 10 years, the nonprofit RIP Medical Debt has emerged as the leader in making buyouts happen, using crowdfunding campaigns, celebrity engagement, and partnerships in the private and public sectors. It connects charitable buyers with hospitals and debt collection companies to arrange the sale and erasure of large bundles of debt.

The buyouts focus on low-income households and those with extreme debt burdens. You can’t sign up to have debt wiped away; you just get notified if you’re one of the lucky ones included in a bundle that’s bought off. In 2020, the U.S. Department of Health and Human Services reviewed this strategy and determined it didn’t violate anti-kickback statutes, which reassured hospitals and collectors that they wouldn’t get in legal trouble partnering with RIP Medical Debt.

Buying a bundle of debt saddling low-income families can be a bargain. Hospitals and collection agencies are typically willing to sell the debt for steep discounts, even pennies on the dollar. That’s a great return on investment for philanthropists looking to make a big social impact.

And it’s not just charities pitching in. Local governments across the country, from Cook County, Illinois, to New Orleans, have been directing sizable public funds toward this cause. New York City recently announced plans to buy off the medical debt for half a million residents, at a cost of US$18 million. That would be the largest public buyout on record, although Los Angeles County may trump New York if it carries out its proposal to spend $24 million to help 810,000 residents erase their debt.

Nationally, RIP Medical Debt has helped clear more than $10 billion in debt over the past decade. That’s a huge number, but a small fraction of the estimated $220 billion in medical debt out there. Ultimately, prevention would be better than cure.

Preventing medical debt is trickier

Medical debt has been a persistent problem over the past decade even after the reforms of the 2010 Affordable Care Act increased insurance coverage and made a dent in debt, especially in states that expanded Medicaid. A recent national survey by the Commonwealth Fund found that 43% of Americans lacked adequate insurance in 2022, which puts them at risk of taking on medical debt.

Unfortunately, it’s incredibly difficult to close coverage gaps in the patchwork American insurance system, which ties eligibility to employment, income, age, family size and location – all things that can change over time. But even in the absence of a total overhaul, there are several policy proposals that could keep the medical debt problem from getting worse.

Medicaid expansion has been shown to reduce uninsurance, underinsurance and medical debt. Unfortunately, insurance gaps are likely to get worse in the coming year, as states unwind their pandemic-era Medicaid rules, leaving millions without coverage. Bolstering Medicaid access in the 10 states that haven’t yet expanded the program could go a long way.

Once patients have a medical bill in hand that they can’t afford, it can be tricky to navigate financial aid and payment options. Some states, like Maryland and California, are ahead of the curve with policies that make it easier for patients to access aid and that rein in the use of liens, lawsuits and other aggressive collections tactics. More states could follow suit.

Another major factor driving underinsurance is rising out-of-pocket costs – like high deductibles – for those with private insurance. This is especially a concern for low-wage workers who live paycheck to paycheck. More than half of large employers believe their employees have concerns about their ability to afford medical care.

Lowering deductibles and out-of-pocket maximums could protect patients from accumulating debt, since it would lower the total amount they could incur in a given time period. But if the current system otherwise stayed the same, then premiums would have to rise to offset the reduction in out-of-pocket payments. Higher premiums would transfer costs across everyone in the insurance pool and make enrolling in insurance unreachable for some – which doesn’t solve the underinsurance problem.

Reducing out-of-pocket liability without inflating premiums would only be possible if the overall cost of health care drops. Fortunately, there’s room to reduce waste. Americans spend more on health care than people in other wealthy countries do, and arguably get less for their money. More than a quarter of health spending is on administrative costs, and the high prices Americans pay don’t necessarily translate into high-value care. That’s why some states like Massachusetts and California are experimenting with cost growth limits.

Momentum toward policy change

The growing number of city and county governments buying off medical debt signals that local leaders view medical debt as a problem worth solving. Congress has passed substantial price transparency laws and prohibited surprise medical billing in recent years. The Consumer Financial Protection Bureau is exploring rule changes for medical debt collections and reporting, and national credit bureaus have voluntarily removed some medical debt from credit reports to limit its impact on people’s approval for loans, leases and jobs.

These recent actions show that leaders at all levels of government want to end medical debt. I think that’s a good sign. After all, recognizing a problem is the first step toward meaningful change.

Erin Duffy receives funding from Arnold Ventures.

congress trump pandemic

IFM’s Hat Trick and Reflections On Option-To-Buy M&A

Four Years Ago This Week, Freedom Was Torched

Red Candle In The Wind

CDC Warns Thousands Of Children Sent To ER After Taking Common Sleep Aid

Analyst reviews Apple stock price target amid challenges

Trump “Clearly Hasn’t Learned From His COVID-Era Mistakes”, RFK Jr. Says

Economic Trends, Risks and the Industrial Market

Chronic stress and inflammation linked to societal and environmental impacts in new study

SoCal Industrial Prioritizes Speed, Power and Sustainability

The next pandemic? It’s already here for Earth’s wildlife

-

Uncategorized3 weeks ago

Uncategorized3 weeks agoAll Of The Elements Are In Place For An Economic Crisis Of Staggering Proportions

-

International5 days ago

International5 days agoEyePoint poaches medical chief from Apellis; Sandoz CFO, longtime BioNTech exec to retire

-

Uncategorized4 weeks ago

Uncategorized4 weeks agoCalifornia Counties Could Be Forced To Pay $300 Million To Cover COVID-Era Program

-

Uncategorized3 weeks ago

Uncategorized3 weeks agoApparel Retailer Express Moving Toward Bankruptcy

-

Uncategorized4 weeks ago

Uncategorized4 weeks agoIndustrial Production Decreased 0.1% in January

-

International5 days ago

International5 days agoWalmart launches clever answer to Target’s new membership program

-

Uncategorized4 weeks ago

Uncategorized4 weeks agoRFK Jr: The Wuhan Cover-Up & The Rise Of The Biowarfare-Industrial Complex

-

Uncategorized3 weeks ago

Uncategorized3 weeks agoGOP Efforts To Shore Up Election Security In Swing States Face Challenges