Spread & Containment

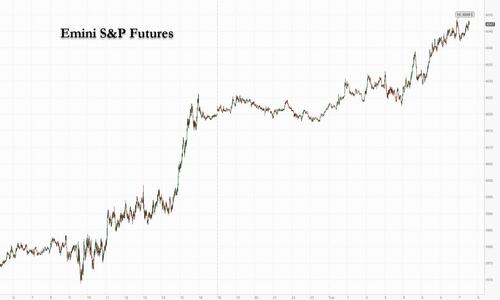

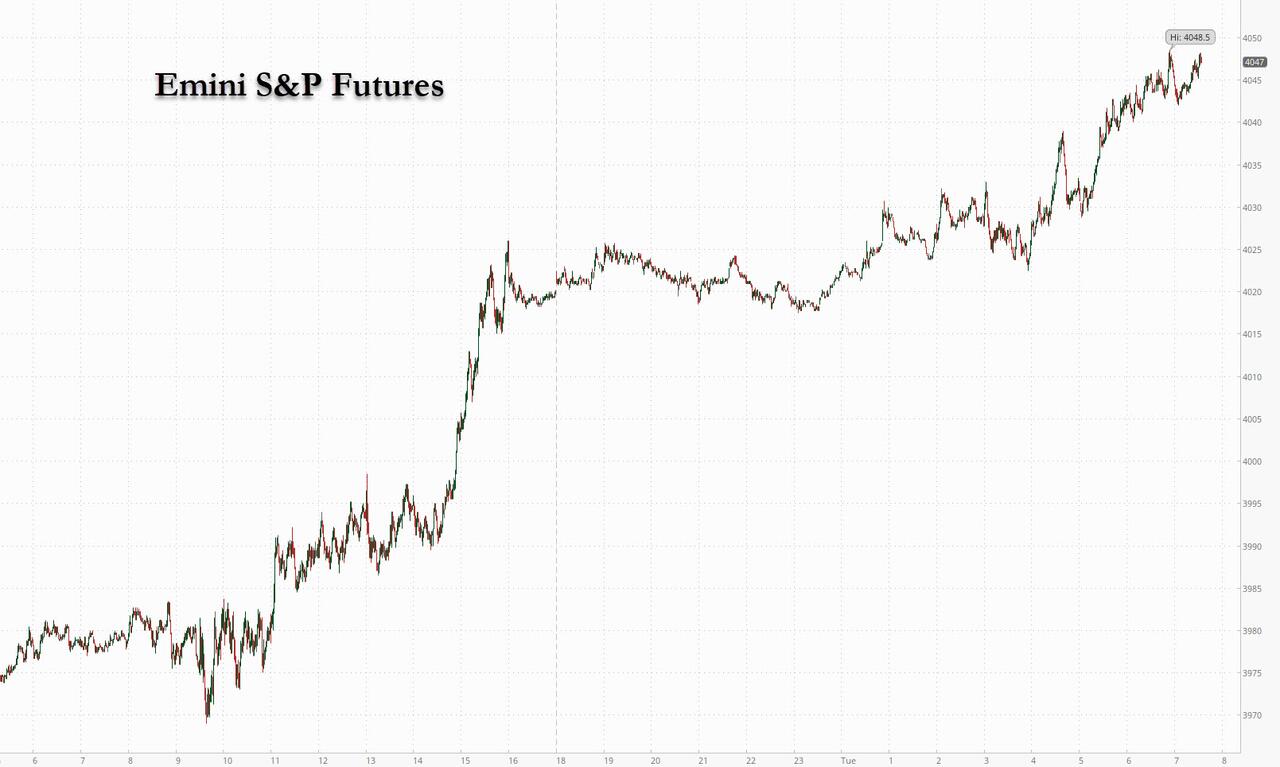

Futures Storm Higher Ahead Of Last Most Important Datapoint Of 2022

Futures Storm Higher Ahead Of Last Most Important Datapoint Of 2022

After a dismal start to December, US futures extended their gains to a…

Share this:

After a dismal start to December, US futures extended their gains to a second day ahead of today's critical economic data: the final consumer prices print due of 2022 which in turn precedes tomorrow's final for 2022 FOMC meeting where Powell is expected to slow the pace of hiking to 50bps. Contracts on the S&P 500 rose 0.6% higher by 7:45 a.m. ET while Nasdaq 100 futures gained 0.7%. The underlying benchmarks advanced on Monday in anticipation Tuesday’s inflation data and Wednesday’s Federal Reserve decision will establish a slower pace of interest-rate increases. The greenback halted a two-day rally, while Treasuries gained. Oil futures extended gains by another 0.5% after almost sliding below $70 on Monday on signs of further easing in China’s Covid rules. Oil traded higher by 0.5% on signs of further easing in China’s Covid rules.

Overnight news centered around further re-opening headlines in Greater China (especially Hong Kong) and a decline in German inflation MoM (although in-line with expectations). On the CPI front, Goldman expects a 0.2% rise MoM (vs cons .3%) as a decline in used cars, hotels and apparel prices should help the headline number (on the flip side expect rebound in airfares and another gain in car insurance). Full preview here. There are no major earnings.

In premarket trading, Oracle shares rose 2.5% after the software company reported second-quarter results that beat expectations. Analysts were positive about the company’s execution and revenue growth in the quarter amid tough macro conditions. Pinterest Inc. also gained, rising 3.75%, after Pinterest (PINS US) shares rise 3.7% after Piper Sandler lifted the social networking site to overweight from neutral, noting multiple tailwinds heading into 2023 that are separate from the health of the ad market. here are the other notable premarket movers:

- NetApp stock declines 2.2% on thin volumes as Morgan Stanley cut it to underweight. The broker cut PT to $58 from $66 as a name where the backlog is smaller and estimates are more at risk; raises Coherent (COHR US) to overweight.

- Magenta Therapeutics jumps 48% after the biotechnology company released a positive update on clinical trial data for a drug called MGTA-117 treating acute myeloid leukemia patients.

- Mirati Therapeutics shares rally 18% after the biotech company’s cancer drug Krazati (adagrasib) won approval from the FDA. The drug’s label was as expected, which analysts said was also a positive development.

- Keep an eye on US internet stocks as Citi sees a “significant reset” for the sector in 2023 and says the long-term secular attractions still outweigh the near-term challenges.

- It initiates coverage on 16 stocks, though Amazon remains its top internet sector pick, followed by Meta (META US) within online advertising.

- Watch Carrier Global and nVent Electric as both stocks are downgraded to sector weight from overweight at KeyBanc, which is cautious that sentiment on late-cycle industrial names has peaked.

- Keep an eye on Fiverr, Xometry and Zillow as all three stocks were initiated with buy ratings at Citi, which expanded its coverage of online marketplaces, with a preference for stocks leading their respective categories across autos and real estate.

- Equinix stock may be in focus as it was upgraded to outperform from market perform and named among ‘best ideas for 2023’ at Cowen, with the company seen as strongly positioned to weather a tough economic outlook.

- Credit Suisse says it is positive on the long-term outlook for US industrial tech stocks but more cautious on the near-term, in a note initiating coverage on eight stocks in the sector.

Stocks retreated last week over concerns that strong US economic data will force the Fed to remain aggressive in tightening policy. This inflation print will be closely monitored as traders assess the impact of higher rates on prices. If economists’ projection for a 7.3% expansion in the US consumer price index for November is on target, it would be the lowest reading in 11 months and the fifth consecutive drop. While that would still leave inflation much higher than the Fed’s target of 2%, it could justify a slowdown in the pace of monetary tightening, with a projected half-point move on Wednesday. However, it also leaves the bar low for disappointment and a selloff. A 7.3% print would also spark a 2%-3% gain in stocks according to JPMorgan, which provided the following market reaction matrix:

- Prints 7.8% or higher. Inflation moving higher after the November print would likely have investors questioning whether the Nov was an aberration and if inflation is reaccelerating from here. Further, the near-term inflation outlook is muddled as the Chinese reopening could prove to be inflation. SPX down 4% - 5%; Probability 5%

- 7.5% - 7.7%. If the CPI is to miss hawkishly, the misses this year have ranged from 10bps – 30bps. The 20bps+ misses have triggered an average -2.3% move in the SPX. Should this outcome occur, given the recent bear rally, we could see a more dramatic move here. SPX down 2.5% - 3.5; Probability 25%

- 7.2% - 7.4%. This inline print is a market positive event but given positioning being less light than in November but is historically low. This could initiate short-covering as well as shifting the near-term trading range higher, potentially from 3700 – 3900 to 3850 – 4150. SPX +2% - +3%; Probability 50%

- 7.0% - 7.2%. A bullish outcome that could pull terminal rate lower despite expectations for higher DOTS being released the next day. While 2 data points is not a trend, this may embolden bulls especially if commodity prices continue their decline. SPX +4% - 5%; Probability 15%

- 6.9% or lower. A print here could be the technical end of the bear market, putting this latest rally at a more than 20% move from its lows in October. The logic here is that not only is inflation dissipating but its pace is accelerating. This would give increasing confidence in projections of headline inflation falling ~3% in 2023. Further, if inflation is at 3%, irrespective of the labor market conditions, it seems unlikely that the Fed would hold the terminal rate at 5%. Any Fed pivot will rip Equities. SPX +8% - 10%; Probability 5%

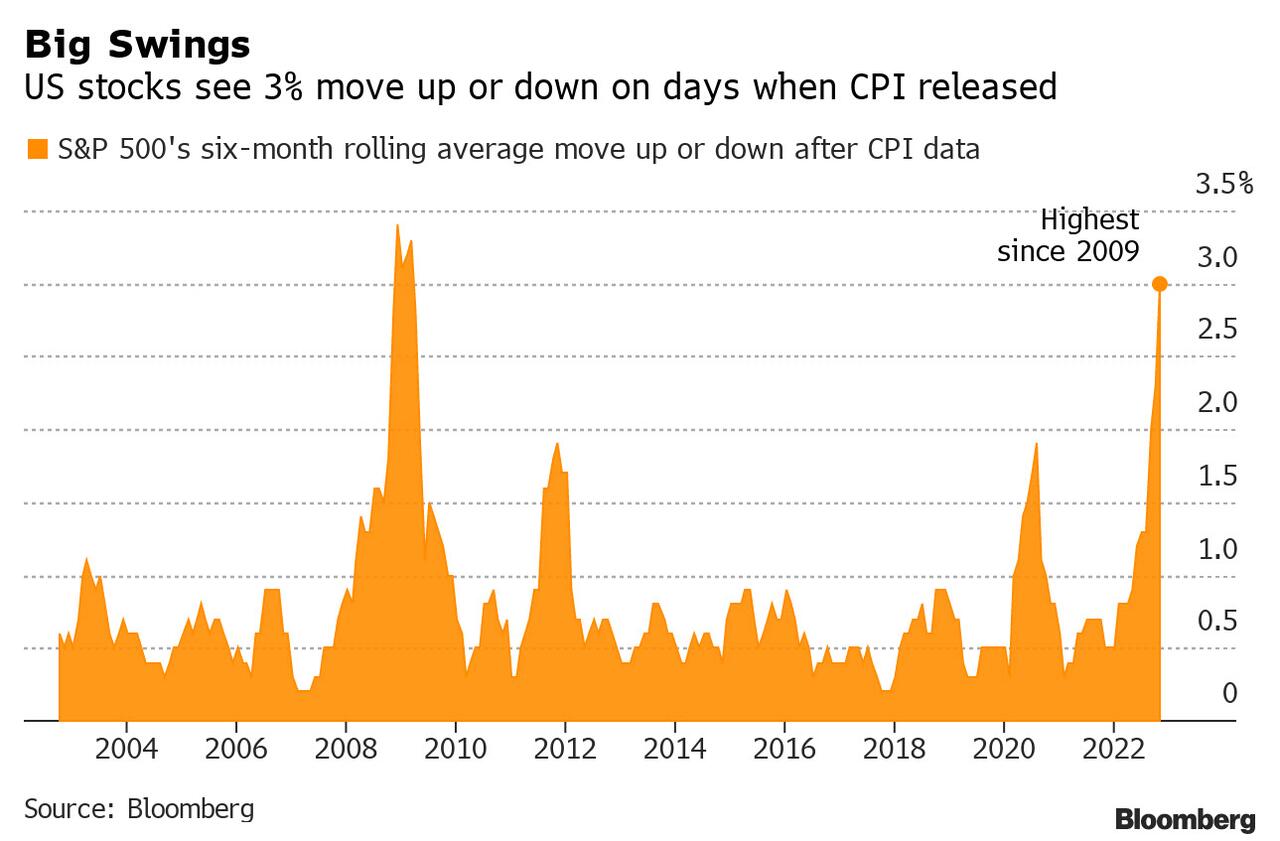

One thing is certain: expect a big move - options are implying a 2.3% move in the S&P today, in line with recent swings which are among the highest in history.

“Today’s US CPI data will give us an idea on how the market pricing for the Fed’s terminal rate will clash with the dot plot projections that will come out tomorrow, and that will, in all cases, hammer any potentially optimistic market sentiment,” Ipek Ozkardeskaya, a senior analyst at Swissquote Bank, wrote in a note. “Therefore, even if we see a great CPI print and a nice market rally today, it may not extend past the Fed decision on Wednesday.”

November CPI is expected at +0.3% m/m and +7.3% y/y; easing supply constraints, discounts to clear excess inventory, a downturn in interest-rate sensitive sectors, and lower energy prices are all factors effecting this month’s print. Our full preview can be found here, and this is the CPI forecast by bank:

- 7.2% - Barclays

- 7.2% - Credit Suisse

- 7.2% - Goldman Sachs

- 7.2% - Bloomberg Econ

- 7.2% - Citigroup

- 7.2% - Morgan Stanley

- 7.2% - Wells Fargo

- 7.3% - HSBC

- 7.3% - JP Morgan Chase

- 7.3% - UBS

- 7.3% - Bank of America

- 7.4% - SocGen

Meanwhile, the US central bank is expected to hike interest rates by 50 basis points on Wednesday.

“I wouldn’t be so bullish on the upside to a softer print. I’m afraid I’d be a bit more bearish on the downside if we get a stronger than expected number,” said Altaf Kassam, State Street Global Advisors’ EMEA head of investment strategy and research in an interview with Bloomberg Television. “I don’t think the market is quite positioned that strongly for the upside. but at the same time, we do expect the numbers to keep trending downwards.”

In Europe, the Stoxx 50 rose 0.5% with tech, banks and energy the strongest-performing sectors in Europe. On the data front, German CPI was -.5% MoM vs cons -.5% (still 10% YoY), while German ZEW economic sentiment improved for the third straight month (highest reading since Feb). Regional focus will turn to central bank decisions later in the week (BOE, ECB and SNB on Thursday. European equity benchmark recovered from Monday’s losses as traders awaited the US release but were also mindful of the European Central Bank’s rate decision due Thursday. The continent’s policymakers are expected to follow the Fed with their own half-point hike. Meanwhile, data showed that UK wages are rising at close to a record pace, maintaining pressure on the Bank of England to keep hiking interest rates despite a worsening economic outlook. Here are some of the most notable European movers:

- Elior climbed as much as 11% after Citi upgraded the stock to buy, saying it sees a pathway toward deleveraging in coming weeks on conclusion of chairman’s strategic review.

- Synthomer shares rise as much as 6% after the company said it would sell its laminates, films and coated fabrics businesses to Surteco North America Inc. for a total enterprise value of approximately $255 million.

- Temenos shares rise as much as 5.2% after the software firm said a US financial institution is extending its relationship with the Swiss company.

- Lufthansa shares jump as much as 4.8% after the German airline raised its earnings forecast for 2022, boosting shares of regional peers Air France- KLM and British Airways-owner IAG.

- Banco BPM gains as much as 4.5% in Milan, the most intraday since Nov. 9, to lead gains on the FTSE MIB index after Fondazione Enasarco completed the purchase of a ~1.97% stake in the lender at a price higher than yesterday’s close.

- Rolls-Royce Holdings slides as much as 4.1% after JPMorgan placed stock on negative catalyst watch as the broker believes that when new CEO Tufan Erginbilgic addresses investors in February, he’s likely to flag weaker-than-expected free cash flow and a strained balance sheet.

- Erste shares fall as much as 3.7% after it was cut to underperform from market perform at KBW on a difficult setup for the Austrian lender into 2023 and an unattractive valuation.

- EMS-Chemie falls as much as 3.4% after it was cut to hold at Stifel with the broker saying it expects a weak 4Q for the polymers maker leading into a tough start to 2023.

- Novozymes shares falls as much as 2.2% after the company was downgraded to equalweight from overweight at Barclays.

Asian stocks eked out a small gain as Hong Kong scrapped more of its Covid restrictions, supporting sentiment ahead of inflation data that could impact the trajectory of future US interest rates.The MSCI Asia Pacific Index rose as much as 0.5%, led by financial and industrial shares. Key gauges in Hong Kong advanced while Chinese stocks linked to reopening were mostly higher, after the city’s leader said restrictions on international arrivals going to bars or eating at restaurants will be removed. Most markets rose as some investors held onto hopes that US consumer price inflation — due later Tuesday — could be soft enough to justify a slowdown in rate increases by the Federal Reserve, which sets policy later this week. The inflation data will be more critical than the Fed’s decision, according to Xi Qiao, managing director for global wealth management at UBS Group AG.

“It’s all going to depend on CPI numbers, whether the Fed is going to pivot or not,” she said on Bloomberg Television. Asian stocks are up about 17% since hitting their lowest level in more than two years in October, boosted by China’s rapid shift away from its zero-tolerance approach to Covid. It remains down about 18% of the year, thanks to its earlier losses from global monetary tightening and China’s draconian lockdown measures.

Japanese equities climbed ahead of US’ reading on consumer prices as a Federal Reserve Bank of New York survey report showed that inflation worries are subsiding. The Topix Index rose 0.4% to 1,965.68 as of market close in Tokyo, while the Nikkei advanced 0.4% to 27,954.85. Takeda Pharmaceutical Co. contributed the most to the Topix’s gain, increasing 2.7%. Out of 2,164 stocks in the index, 1,231 rose and 790 fell, while 143 were unchanged. “If the US CPI growth, released tonight, is as expected, they would have fallen for the fifth month in a row,” said Hideyuki Ishiguro, a senior strategist at Nomura Asset Management. “As the slowdown in inflation becomes decisive, there may have been some moves to adjust positions in the US market.”

In FX, the Bloomberg dollar spot index is unchanged; DKK and EUR are the weakest performers in G-10 FX, NOK and AUD outperform. The greenback was steady to weaker against most of its Group-of-10 peers, though most pairs were confined to recent, narrow ranges. Commodity currencies led the advance while the Swiss franc was the worst performer. The Treasury curve bull flattened

The euro traded in a narrow $1.0528-1.0561 range. Yields on German and Italian debt was mostly steady or slightly higher. Overnight volatility in euro-dollar may be off its 2022 highs, yet remains elevated before the much anticipated US CPI release. The gauge trades at 21.19% after touching a one-month high Monday at 23.32%; this suggests a breakeven of around 100 dollar pips

The pound inched up, advancing a fifth straight day against the US dollar, the longest rising streak in over two months. Gilts extended opening losses, pushing yields 5-7bps higher as money markets raised bets on Bank of England rate hikes ahead of its decision Thursday

Australian and New Zealand dollars advanced as China’s ambassador to the US said that the nation will continue to relax its strict Covid measures. However, gains were slowed by option-related selling attached to large strikes. Bonds in the two nations eased

The yen neared a December low against the dollar before erasing losses

In rates, Treasury futures drifted higher over Asia, early European session and outperforming core European rates with gains led by long-end of the curve. US yields richer by up to 3.5bp across long-end of the curve with 2s10s, 5s30s spreads flatter by 1.2bp and 1.7bp on the day; 10-year yields around 3.58%, outperforming bunds and gilts by 3bp and 8bp in the sector. Gilts 10-year yield up some 7 bps to 3.27% while money markets add to their BOE peak rate bets, pricing the bank rate to climb to 4.75% by August. USTs and bunds 10-year yields relatively muted in comparison, trading within Monday’s range. US auction round concludes with $18b 30-year bond reopening at 1pm, follows Monday’s 10-year note sale which tailed the WI by almost 4bp and a solid 3-year note sale. The US session focus includes November inflation print at 8:30 a.m. New York.

In commodities, WTI drifts 1% higher to trade near $73.91. Spot gold rises roughly $3 to trade near $1,785/oz.

Looking at the day ahead now, and the main highlight will be the aforementioned US CPI release for November. Otherwise though, we’ll get UK employment and Italian industrial production for October, the German ZEW survey for December, and the US NFIB small business optimism index for November. Otherwise from central banks, we’ll get the BoE’s latest Financial Stability Report and subsequent press conference.

Market Snapshot

- S&P 500 futures up 0.3% to 4,003.75

- MXAP up 0.2% to 157.43

- MXAPJ up 0.2% to 513.26

- Nikkei up 0.4% to 27,954.85

- Topix up 0.4% to 1,965.68

- Hang Seng Index up 0.7% to 19,596.20

- Shanghai Composite little changed at 3,176.33

- Sensex up 0.7% to 62,552.76

- Australia S&P/ASX 200 up 0.3% to 7,203.27

- Kospi little changed at 2,372.40

- STOXX Europe 600 up 0.4% to 438.53

- German 10Y yield little changed at 1.95%

- Euro little changed at $1.0538

- Brent Futures up 2.0% to $79.54/bbl

- Brent Futures up 2.0% to $79.56/bbl

- Gold spot up 0.2% to $1,784.14

- U.S. Dollar Index down 0.12% to 105.01

Top Overnight News from Bloomberg

- While equity traders are bracing for potentially significant stock swings after Tuesday’s US inflation data, their currency counterparts look a little more circumspect. Overnight expectations for swings in major currencies like the yen, euro and Australian dollar are elevated but well off their highs of the year. In fact they indicate the currencies are unlikely to break out of their recent trading ranges

- The gap between yields on one-year Treasury Inflation-Protected Securities and similar- dated nominal government notes stands at 2.18%, reflecting market expectations for the average inflation rate over the coming year. That would require price gains to slow by more than 5 percentage points, a pace seen in only three instances in the past six decades

- UK average earnings excluding bonuses were 6.1% higher in the three months through October than a year earlier. That’s the most since records began in 2001, barring the height of the coronavirus pandemic

- Strikes and industrial action had the biggest impact on the UK in 11 years in October — two months before the latest round of protests crippled public services. At least 417,000 days of work were lost due to labor disputes in October, the most since November 2011, the Office for National Statistics said Tuesday

- The BOE has recommended the UK take swift regulatory action to strengthen the pensions market after recent bond market turmoil exposed shortcomings in its oversight

- The investor outlook for Germany’s economy improved to its highest level since Russia’s invasion of Ukraine — the latest sign that concerns over a deep winter slump are receding. The ZEW institute’s gauge of expectations climbed to -23.3 in December from -36.7 the previous month, better than economists polled by Bloomberg had predicted

- China’s Covid wave is rippling through the nation’s financial industry, with currency volumes falling as traders call in sick and banks activating backup plans to keep operations running smoothly

- China is delaying a closely watched economic policy meeting due to start this week after Covid infections surged in Beijing, according to people familiar with the matter

- Hong Kong will remove a ban on international arrivals going to bars or eating at restaurants, and stop requiring people to use a health app to enter venues, Chief Executive John Lee said at a press conference Tuesday. He didn’t mention whether the government will retain the mask mandate

A more detailed look at global markets courtesy of Newsquawk

Asia-Pac stocks were mostly kept afloat following the gains on Wall St where the major indices unwound recent losses although the upside was capped in Asia ahead of US CPI data and a slew of central bank rate decisions. ASX 200 was underpinned by strength in tech, industrials and financials, albeit with gains limited by weakness in miners and after an improvement in consumer confidence was offset by a deterioration in business surveys. Nikkei 225 briefly reclaimed the 28,000 level which it failed to sustain amid tentativeness before the risk events. Hang Seng and Shanghai Comp were varied as Hong Kong benefitted from reopening optimism amid reports that quarantine-free travel is to begin in January and with Chief Executive Lee announcing an easing of restrictions, while the mainland lacked conviction after weaker-than-expected financing data and with Japan and the Netherlands agreeing in principle to join the US in controlling exports of chipmaking equipment to China.

Top Asian News

- China's ambassador to the US Qin Gang said he believes China's COVID-19 measures will be further relaxed in the near future and international travel to China will become easier, according to Reuters.

- China-Hong Kong quarantine-free travel is to begin in January, according to a report citing local press. Hong Kong Chief Executive Lee later announced an end to the COVID contact tracing app requirement and will eliminate the three-day arrival monitoring period, while the Amber code on international arrivals is to be lifted on Wednesday.

- Japan and Netherlands have agreed in principle to join the US in tightening controls on exports of advanced chipmaking equipment to China, according to people familiar with the matter cited by SCMP. Japanese Trade and Industry Minister Nishimura stated that they will take appropriate measures on chip-related export curbs to China taking into consideration each country's regulations, while they are checking with Japanese companies on the impact of chip curbs to China and are not hearing of any major impact.

- Japan's government is to use construction bonds for part of SDF facilities as part of efforts to boost spending, according to Kyodo. However, Japanese Finance Minister Suzuki later stated there was no decision yet on whether to issue construction bonds to pay for developing self-defence forces facilities and that generally speaking, it is difficult to regard bonds as a stable funding source, according to Reuters.

- China intends to allocate over CNY 1tln as a support package to bolster the domestic semiconductor industry, via Reuters citing sources.

- China will delay its economic policy meeting amid a surge in COVID cases in Beijing, Bloomberg reports.

European bourses are firmer across the board Euro Stoxx 50 +0.8%, though action has been choppy with fresh drivers limited. Sectors were initially mixed, but have since moved more convincingly into the green, with Tech outpacing. Stateside, US futures are firmer across the board, though have been choppy alongside European peers but the magnitudes less pronounced pre-CPI, ES +0.5%.

Top European News

- EU lawmakers agreed to tougher draft labour rules for the gig economy ahead of negotiations with EU countries to work out the details, according to Reuters.

- Swiss SECO Forecasts: confirms its previous assessment. The Swiss economy is expected to grow at a significantly below-average rate of 1.0% in 2023, followed by 1.6% in 2024.

- Germany VDMA engineering group confirmed 2022 and 2023 forecasts for German engineering production; sees +1% real production growth in 2022, and a 2% decline in 2023.

- BoE Financial Stability Report: Urgent and robust measures needed to fill gaps in LDI fund regulation; must remain resilient to higher level of rates than they can now withstand.

FX

- DXY is bid, but has been unable to convincingly breach the 105.00 mark despite a brief foray to 105.09, with peers generally contained vs USD.

- At the top of the pile is the AUD despite NAB data with Westpac consumer metrics assisting ahead of RBA's Lowe, lifting to 0.6800.

- CAD & NOK have seen a modest rebound given benchmark pricing and in wake of recent pressure, particularly in the CAD.

- EUR is modestly softer despite constructive ZEW data, albeit mixed vs exp., while USD/JPY has slipped after a failed test of 138.00.

- PBoC set USD/CNY mid-point at 6.9746vs exp. 6.9758 (prev. 6.9565)

Fixed Income

- EGBs have been pressured throughout the morning, with Bunds initially lagging though they have staged a marked rebound to downside of just 20 ticks.

- Amidst this, Gilts were dented by relatively soft UK supply, though have since reverted to pre-auction levels while BTPs were bid on their own outing.

- USTs buck the trend and remain modestly firmer ahead of 30yr supply and US CPI.

Commodities

- Overall, the crude benchmarks have been relatively steady throughout the European morning posting upside in excess of 1.0% and remain towards the top-end of yesterday’s parameters.

- Spot gold and silver are modestly firmer despite the choppy, but ultimately modestly constructive, risk tone. Though, the yellow metal is capped by USD 1790/oz and the 200-DMA a dollar below.

- Ecuador's state oil firm Petroecuador said a weather power outage affected hundreds of wells in its most productive blocks, according to Reuters.

- Italy PM Meloni says the majority of EU member states back a dynamic gas price cap; EU Commission's energy proposal is still in adequate.

Geopolitics

- US shipped the first portion of its grid equipment aid to Ukraine, according to US officials.

- EU ambassadors unanimously approved in principle a financial support package to provide Ukraine with EUR 18bln in 2023, according to the Czech Republic.

- South Korean envoy for Korean peninsula peace said North Korea is becoming more aggressive and blatant in its nuclear threat, while South Korea, Japan and the US will coordinate sanctions and close gaps in the international sanctions regime. Furthermore, the US envoy for North Korea said Pyongyang's behaviour presents one of the most serious security challenges in the region and beyond, while the Japanese envoy for North Korea said the three countries have elevated their security cooperation to an unprecedented level and they will examine all options including counter-strike capabilities and will be more vigilant against North Korea's cyber threat, according to Reuters.

US Event Calendar

- 06:00: Nov. SMALL BUSINESS OPTIMISM, est. 90.5, prior 91.3

- 08:30: Nov. CPI MoM, est. 0.3%, prior 0.4%

- 08:30: Nov. CPI YoY, est. 7.3%, prior 7.7%

- 08:30: Nov. CPI Ex Food and Energy MoM, est. 0.3%, prior 0.3%

- 08:30: Nov. CPI Ex Food and Energy YoY, est. 6.1%, prior 6.3%

- 08:30: Nov. Real Avg Hourly Earning YoY, prior -2.8%, revised -2.7%

- 08:30: Nov. Real Avg Weekly Earnings YoY, prior -3.7%, revised -3.5%

DB's Jim Reid concludes the overnight wrap

I'm still trying to recover from watching the last episode of one of the most popular TV series this year last night, namely "The White Lotus". It was a brilliantly uncomfortable series to watch. No spoilers here though. On the last EMR before Xmas I always list my top 10 TV series/box sets of the year. This will feature highly but there is currently an unusual number one that we just finished watching over the weekend. It was brilliant but I suspect not many of you will have seen it. The clue is that it is a dramatised true story about an event that happened 50 years ago this year. Anyone that gets it from that clue will win the highest-value prize our compliance team can authorise - a very big well done email.

Today we have the last in the series of another 2022 epic and that's the final US CPI to be released this year. Indeed, we don't get many days as important as the next two, and the US CPI today and the FOMC tomorrow are likely to be the difference between a big Santa Claus rally and a visit from Scrooge ahead of Christmas. Bear in mind the S&P 500’s best and worst day of the year so far have both come on a CPI day, and it was only last month that the downside surprise triggered a seismic market reaction, leading to the biggest one-day gain for the S&P 500 (+5.54%) since April 2020, and the largest daily decline in the 2yr Treasury yield (-24.7bps) since 2008. Since close of business the day before the last release the S&P 500 is +6.46%, 2yr yields -20.4bps, 10yr yields -49.6bps and the USD index -5.05%.

The big question now is whether last month’s positive surprise was like July’s, which was then followed by far more negative prints in August and September, or whether this is the start of a more durable shift in inflation that would allow the Fed to ease off.

Our colleagues in the Asset Allocation team (link here) wrote on Friday about event vol heading into the CPI data and the FOMC decisions. Their view is that a build-up of massive vol premium heading into the last two CPI prints (and its subsequent dissipation) was a key driver of the outsized rallies. They think that if the event vol premium stays at current levels, then a post-event rally is still more likely, whereas a selloff would require inflation to surprise strongly on the upside. So if they're right the risk/reward favours a rally after these two big events this week.

In terms of what to look out for today, our US economists are expecting a +0.21% monthly gain in headline CPI (consensus 0.3%), which in turn would take the year-on-year measure down to +7.2% (consensus 7.3%). On core CPI, they see it coming in at a stronger +0.29% (consensus 0.3%), which would take year-on-year measure to +6.1% (consensus 6.1%). And if we do get a surprise on either side, look out for whether that’s broad-based or driven by outliers, since one of the factors driving last month’s rally was optimism that this was a broader decline in inflation. That said, whatever the number is there won’t be any chance to hear from Fed officials, since they’re now deep into their blackout period ahead of tomorrow’s decision.

Ahead of the CPI release, yesterday saw 10yr US Treasuries edge +3.3bps higher to 3.61%, albeit having come back from an intraday low of 3.52%. The intraday turnaround started early in New York trading but was probably helped by a 10yr auction that didn’t have the best reception. It remains to be seen if that was the result of wary investors ahead of CPI or just holiday-induced lack of liquidity. For their part, 2yr Treasuries largely moved in parallel, climbing +3.1bps to 4.38%.

There was a bit of an increase in terminal rate pricing, with Fed funds futures for the May 2023 meeting up +2.0bps to 4.98%. But fundamentally it’s still in the range around 5% where it’s been for the last two months, and the big question is whether today’s release will see it durably break out from that zone in either direction. Over in Europe, there was also a modest rise in yields ahead of Thursday’s ECB decision, with those on 10yr bunds (+0.8bps) and OATs (+0.8bps) moving higher, with BTPs (-0.6bps) retreating a touch.

In the meantime, US equities posted a strong recovery following last week’s declines, with the S&P 500 up +1.43% on the day. Energy stocks were the biggest driver of that amidst a rally in oil prices, and Brent crude (+2.48%) advanced to $77.99/bbl, moving back into positive territory on a YTD basis. Overnight they’ve risen a further +1.31%, advancing to $79.01/bbl on the back of optimism about China’s reopening boosting the demand outlook. However, at the other end of the equity leaderboard were the megacap tech stocks, with the FANG+ index down -0.14% on the day. And back in Europe, equities lost ground as they caught up with the late US selloff on Friday, with the STOXX 600 down -0.49%.

Overnight, Asian equity markets have put in a mixed performance after rising shortly after the open. The Hang Seng (+0.38%) is in positive territory following the news that Hong Kong is further easing its Covid restrictions, and it was confirmed that the ban on international arrivals going to bars or restaurants would end, and people would no longer require to scan a QR code to enter venues. That was particularly beneficial to more Covid-sensitive assets, such as airlines and leisure stocks. Elsewhere, the Nikkei (+0.40%) is trading higher whilst the Shanghai Composite (-0.06%), the CSI 300 (-0.19%) and the KOSPI (-0.25%) have moved lower. In the meantime, US equity futures are pointing modestly lower ahead of today’s CPI release, with contracts on the S&P 500 (-0.06%) and the NASDAQ 100 (-0.13%) both down a bit.

There wasn’t much on the data side yesterday, although the Fed did get some promising news on inflation expectations, since the New York Fed’s latest survey showed expectations decreasing over all time horizons. For instance, the one-year measure fell to a 15-month low of +5.2%, and the three-year measure ticked down to +3.0% (vs. +3.1% previously). Elsewhere, UK GDP rose by a slightly faster-than-expected +0.5% in October (vs. +0.4% expected), but that growth was partly driven by the bounceback from the September bank holiday for the Queen’s funeral.

To the day ahead now, and the main highlight will be the aforementioned US CPI release for November. Otherwise though, we’ll get UK employment and Italian industrial production for October, the German ZEW survey for December, and the US NFIB small business optimism index for November. Otherwise from central banks, we’ll get the BoE’s latest Financial Stability Report and subsequent press conference.

Spread & Containment

The Coming Of The Police State In America

The Coming Of The Police State In America

Authored by Jeffrey Tucker via The Epoch Times,

The National Guard and the State Police are now…

Share this:

Authored by Jeffrey Tucker via The Epoch Times,

The National Guard and the State Police are now patrolling the New York City subway system in an attempt to do something about the explosion of crime. As part of this, there are bag checks and new surveillance of all passengers. No legislation, no debate, just an edict from the mayor.

Many citizens who rely on this system for transportation might welcome this. It’s a city of strict gun control, and no one knows for sure if they have the right to defend themselves. Merchants have been harassed and even arrested for trying to stop looting and pillaging in their own shops.

The message has been sent: Only the police can do this job. Whether they do it or not is another matter.

Things on the subway system have gotten crazy. If you know it well, you can manage to travel safely, but visitors to the city who take the wrong train at the wrong time are taking grave risks.

In actual fact, it’s guaranteed that this will only end in confiscating knives and other things that people carry in order to protect themselves while leaving the actual criminals even more free to prey on citizens.

The law-abiding will suffer and the criminals will grow more numerous. It will not end well.

When you step back from the details, what we have is the dawning of a genuine police state in the United States. It only starts in New York City. Where is the Guard going to be deployed next? Anywhere is possible.

If the crime is bad enough, citizens will welcome it. It must have been this way in most times and places that when the police state arrives, the people cheer.

We will all have our own stories of how this came to be. Some might begin with the passage of the Patriot Act and the establishment of the Department of Homeland Security in 2001. Some will focus on gun control and the taking away of citizens’ rights to defend themselves.

My own version of events is closer in time. It began four years ago this month with lockdowns. That’s what shattered the capacity of civil society to function in the United States. Everything that has happened since follows like one domino tumbling after another.

It goes like this:

1) lockdown,

2) loss of moral compass and spreading of loneliness and nihilism,

3) rioting resulting from citizen frustration, 4) police absent because of ideological hectoring,

5) a rise in uncontrolled immigration/refugees,

6) an epidemic of ill health from substance abuse and otherwise,

7) businesses flee the city

8) cities fall into decay, and that results in

9) more surveillance and police state.

The 10th stage is the sacking of liberty and civilization itself.

It doesn’t fall out this way at every point in history, but this seems like a solid outline of what happened in this case. Four years is a very short period of time to see all of this unfold. But it is a fact that New York City was more-or-less civilized only four years ago. No one could have predicted that it would come to this so quickly.

But once the lockdowns happened, all bets were off. Here we had a policy that most directly trampled on all freedoms that we had taken for granted. Schools, businesses, and churches were slammed shut, with various levels of enforcement. The entire workforce was divided between essential and nonessential, and there was widespread confusion about who precisely was in charge of designating and enforcing this.

It felt like martial law at the time, as if all normal civilian law had been displaced by something else. That something had to do with public health, but there was clearly more going on, because suddenly our social media posts were censored and we were being asked to do things that made no sense, such as mask up for a virus that evaded mask protection and walk in only one direction in grocery aisles.

Vast amounts of the white-collar workforce stayed home—and their kids, too—until it became too much to bear. The city became a ghost town. Most U.S. cities were the same.

As the months of disaster rolled on, the captives were let out of their houses for the summer in order to protest racism but no other reason. As a way of excusing this, the same public health authorities said that racism was a virus as bad as COVID-19, so therefore it was permitted.

The protests had turned to riots in many cities, and the police were being defunded and discouraged to do anything about the problem. Citizens watched in horror as downtowns burned and drug-crazed freaks took over whole sections of cities. It was like every standard of decency had been zapped out of an entire swath of the population.

Meanwhile, large checks were arriving in people’s bank accounts, defying every normal economic expectation. How could people not be working and get their bank accounts more flush with cash than ever? There was a new law that didn’t even require that people pay rent. How weird was that? Even student loans didn’t need to be paid.

By the fall, recess from lockdown was over and everyone was told to go home again. But this time they had a job to do: They were supposed to vote. Not at the polling places, because going there would only spread germs, or so the media said. When the voting results finally came in, it was the absentee ballots that swung the election in favor of the opposition party that actually wanted more lockdowns and eventually pushed vaccine mandates on the whole population.

The new party in control took note of the large population movements out of cities and states that they controlled. This would have a large effect on voting patterns in the future. But they had a plan. They would open the borders to millions of people in the guise of caring for refugees. These new warm bodies would become voters in time and certainly count on the census when it came time to reapportion political power.

Meanwhile, the native population had begun to swim in ill health from substance abuse, widespread depression, and demoralization, plus vaccine injury. This increased dependency on the very institutions that had caused the problem in the first place: the medical/scientific establishment.

The rise of crime drove the small businesses out of the city. They had barely survived the lockdowns, but they certainly could not survive the crime epidemic. This undermined the tax base of the city and allowed the criminals to take further control.

The same cities became sanctuaries for the waves of migrants sacking the country, and partisan mayors actually used tax dollars to house these invaders in high-end hotels in the name of having compassion for the stranger. Citizens were pushed out to make way for rampaging migrant hordes, as incredible as this seems.

But with that, of course, crime rose ever further, inciting citizen anger and providing a pretext to bring in the police state in the form of the National Guard, now tasked with cracking down on crime in the transportation system.

What’s the next step? It’s probably already here: mass surveillance and censorship, plus ever-expanding police power. This will be accompanied by further population movements, as those with the means to do so flee the city and even the country and leave it for everyone else to suffer.

As I tell the story, all of this seems inevitable. It is not. It could have been stopped at any point. A wise and prudent political leadership could have admitted the error from the beginning and called on the country to rediscover freedom, decency, and the difference between right and wrong. But ego and pride stopped that from happening, and we are left with the consequences.

The government grows ever bigger and civil society ever less capable of managing itself in large urban centers. Disaster is unfolding in real time, mitigated only by a rising stock market and a financial system that has yet to fall apart completely.

Are we at the middle stages of total collapse, or at the point where the population and people in leadership positions wise up and decide to put an end to the downward slide? It’s hard to know. But this much we do know: There is a growing pocket of resistance out there that is fed up and refuses to sit by and watch this great country be sacked and taken over by everything it was set up to prevent.

Spread & Containment

Another beloved brewery files Chapter 11 bankruptcy

The beer industry has been devastated by covid, changing tastes, and maybe fallout from the Bud Light scandal.

Share this:

Before the covid pandemic, craft beer was having a moment. Most cities had multiple breweries and taprooms with some having so many that people put together the brewery version of a pub crawl.

It was a period where beer snobbery ruled the day and it was not uncommon to hear bar patrons discuss the makeup of the beer the beer they were drinking. This boom period always seemed destined for failure, or at least a retraction as many markets seemed to have more craft breweries than they could support.

Related: Fast-food chain closes more stores after Chapter 11 bankruptcy

The pandemic, however, hastened that downfall. Many of these local and regional craft breweries counted on in-person sales to drive their business.

And while many had local and regional distribution, selling through a third party comes with much lower margins. Direct sales drove their business and the pandemic forced many breweries to shut down their taprooms during the period where social distancing rules were in effect.

During those months the breweries still had rent and employees to pay while little money was coming in. That led to a number of popular beermakers including San Francisco's nationally-known Anchor Brewing as well as many regional favorites including Chicago’s Metropolitan Brewing, New Jersey’s Flying Fish, Denver’s Joyride Brewing, Tampa’s Zydeco Brew Werks, and Cleveland’s Terrestrial Brewing filing bankruptcy.

Some of these brands hope to survive, but others, including Anchor Brewing, fell into Chapter 7 liquidation. Now, another domino has fallen as a popular regional brewery has filed for Chapter 11 bankruptcy protection.

Image source: Shutterstock

Covid is not the only reason for brewery bankruptcies

While covid deserves some of the blame for brewery failures, it's not the only reason why so many have filed for bankruptcy protection. Overall beer sales have fallen driven by younger people embracing non-alcoholic cocktails, and the rise in popularity of non-beer alcoholic offerings,

Beer sales have fallen to their lowest levels since 1999 and some industry analysts

"Sales declined by more than 5% in the first nine months of the year, dragged down not only by the backlash and boycotts against Anheuser-Busch-owned Bud Light but the changing habits of younger drinkers," according to data from Beer Marketer’s Insights published by the New York Post.

Bud Light parent Anheuser Busch InBev (BUD) faced massive boycotts after it partnered with transgender social media influencer Dylan Mulvaney. It was a very small partnership but it led to a right-wing backlash spurred on by Kid Rock, who posted a video on social media where he chastised the company before shooting up cases of Bud Light with an automatic weapon.

Another brewery files Chapter 11 bankruptcy

Gizmo Brew Works, which does business under the name Roth Brewing Company LLC, filed for Chapter 11 bankruptcy protection on March 8. In its filing, the company checked the box that indicates that its debts are less than $7.5 million and it chooses to proceed under Subchapter V of Chapter 11.

"Both small business and subchapter V cases are treated differently than a traditional chapter 11 case primarily due to accelerated deadlines and the speed with which the plan is confirmed," USCourts.gov explained.

Roth Brewing/Gizmo Brew Works shared that it has 50-99 creditors and assets $100,000 and $500,000. The filing noted that the company does expect to have funds available for unsecured creditors.

The popular brewery operates three taprooms and sells its beer to go at those locations.

"Join us at Gizmo Brew Works Craft Brewery and Taprooms located in Raleigh, Durham, and Chapel Hill, North Carolina. Find us for entertainment, live music, food trucks, beer specials, and most importantly, great-tasting craft beer by Gizmo Brew Works," the company shared on its website.

The company estimates that it has between $1 and $10 million in liabilities (a broad range as the bankruptcy form does not provide a space to be more specific).

Gizmo Brew Works/Roth Brewing did not share a reorganization or funding plan in its bankruptcy filing. An email request for comment sent through the company's contact page was not immediately returned.

bankruptcy pandemic social distancing

Government

Students lose out as cities and states give billions in property tax breaks to businesses − draining school budgets and especially hurting the poorest students

An estimated 95% of US cities provide economic development tax incentives to woo corporate investors, taking billions away from schools.

Share this:

{kind=link}

{kind=link}

Built in 1910, James Elementary is a three-story brick school in Kansas City, Missouri’s historic Northeast neighborhood, with a bright blue front door framed by a sand-colored stone arch adorned with a gargoyle. As bustling students and teachers negotiate a maze of gray stairs with worn wooden handrails, Marjorie Mayes, the school’s principal, escorts a visitor across uneven blue tile floors on the ground floor to a classroom with exposed brick walls and pipes. Bubbling paint mars some walls, evidence of the water leaks spreading inside the aging building.

“It’s living history,” said Mayes during a mid-September tour of the building. “Not the kind of living history we want.”

The district would like to tackle the US$400 million in deferred maintenance needed to create a 21st century learning environment at its 35 schools – including James Elementary – but it can’t. It doesn’t have the money.

Property tax redirect

The lack of funds is a direct result of the property tax breaks that Kansas City lavishes on companies and developers that do business there. The program is supposed to bring in new jobs and business but instead has ended up draining civic coffers and starving schools. Between 2017 and 2023, the Kansas City school district lost $237.3 million through tax abatements.

Kansas City is hardly an anomaly. An estimated 95% of U.S. cities provide economic development tax incentives to woo corporate investors. The upshot is that billions have been diverted from large urban school districts and from a growing number of small suburban and rural districts. The impact is seen in districts as diverse as Chicago and Cleveland, Hillsboro, Oregon, and Storey County, Nevada.

The result? A 2021 review of 2,498 financial statements from school districts across 27 states revealed that, in 2019 alone, at least $2.4 billion was diverted to fund tax incentives. Yet that substantial figure still downplays the magnitude of the problem, because three-quarters of the 10,370 districts analyzed did not provide any information on tax abatement agreements.

Tax abatement programs have long been controversial, pitting states and communities against one another in beggar-thy-neighbor contests. Their economic value is also, at best, unclear: Studies show most companies would have made the same location decision without taxpayer subsidies. Meanwhile, schools make up the largest cost item in these communities, meaning they suffer most when companies are granted breaks in property taxes.

A three-month investigation by The Conversation and three scholars with expertise in economic development, tax laws and education policy shows that the cash drain from these programs is not equally shared by schools in the same communities. At the local level, tax abatements and exemptions often come at the cost of critical funding for school districts that disproportionately serve students from low-income households and who are racial minorities.

In Missouri, for example, in 2022 nearly $1,700 per student was redirected from Kansas City public and charter schools, while between $500 and $900 was redirected from wealthier, whiter Northland schools on the north side of the river in Kansas City and in the suburbs beyond. Other studies have found similar demographic trends elsewhere, including New York state, South Carolina and Columbus, Ohio.

The funding gaps produced by abated money often force schools to delay needed maintenance, increase class sizes, lay off teachers and support staff and even close outright. Schools also struggle to update or replace outdated technology, books and other educational resources. And, amid a nationwide teacher shortage, schools under financial pressures sometimes turn to inexperienced teachers who are not fully certified or rely too heavily on recruits from overseas who have been given special visa status.

Lost funding also prevents teachers and staff, who often feed, clothe and otherwise go above and beyond to help students in need, from earning a living wage. All told, tax abatements can end up harming a community’s value, with constant funding shortfalls creating a cycle of decline.

Incentives, payoffs and guarantees

Perversely, some of the largest beneficiaries of tax abatements are the politicians who publicly boast of handing out the breaks despite the harm to poorer communities. Incumbent governors have used the incentives as a means of taking credit for job creation, even when the jobs were coming anyway.

“We know that subsidies don’t work,” said Elizabeth Marcello, a doctoral lecturer at Hunter College who studies governmental planning and policy and the interactions between state and local governments. “But they are good political stories, and I think that’s why politicians love them so much.”

While some voters may celebrate abatements, parents can recognize the disparities between school districts that are created by the tax breaks. Fairleigh Jackson pointed out that her daughter’s East Baton Rouge third grade class lacks access to playground equipment.

The class is attending school in a temporary building while their elementary school undergoes a two-year renovation.

The temporary site has some grass and a cement slab where kids can play, but no playground equipment, Jackson said. And parents needed to set up an Amazon wish list to purchase basic equipment such as balls, jump ropes and chalk for students to use. The district told parents there would be no playground equipment due to a lack of funds, then promised to install equipment, Jackson said, but months later, there is none.

Jackson said it’s hard to complain when other schools in the district don’t even have needed security measures in place. “When I think about playground equipment, I think that’s a necessary piece of child development,” Jackson said. “Do we even advocate for something that should be a daily part of our kids’ experience when kids’ safety isn’t being funded?”

Meanwhile, the challenges facing administrators 500-odd miles away at Atlanta Public Schools are nothing if not formidable: The district is dealing with chronic absenteeism among half of its Black students, many students are experiencing homelessness, and it’s facing a teacher shortage.

At the same time, Atlanta is showering corporations with tax breaks. The city has two bodies that dole them out: the Development Authority of Fulton County, or DAFC, and Invest Atlanta, the city’s economic development agency. The deals handed out by the two agencies have drained $103.8 million from schools from fiscal 2017 to 2022, according to Atlanta school system financial statements.

What exactly Atlanta and other cities and states are accomplishing with tax abatement programs is hard to discern. Fewer than a quarter of companies that receive breaks in the U.S. needed an incentive to invest, according to a 2018 study by the Upjohn Institute for Employment Research, a nonprofit research organization.

This means that at least 75% of companies received tax abatements when they’re not needed – with communities paying a heavy price for economic development that sometimes provides little benefit.

In Kansas City, for example, there’s no guarantee that the businesses that do set up shop after receiving a tax abatement will remain there long term. That’s significant considering the historic border war between the Missouri and Kansas sides of Kansas City – a competition to be the most generous to the businesses, said Jason Roberts, president of the Kansas City Federation of Teachers and School-Related Personnel. Kansas City, Missouri, has a 1% income tax on people who work in the city, so it competes for as many workers as possible to secure that earnings tax, Roberts said.

Under city and state tax abatement programs, companies that used to be in Kansas City have since relocated. The AMC Theaters headquarters, for example, moved from the city’s downtown to Leawood, Kansas, about a decade ago, garnering some $40 million in Promoting Employment Across Kansas tax incentives.

Roberts said that when one side’s financial largesse runs out, companies often move across the state line – until both states decided in 2019 that enough was enough and declared a cease-fire.

But tax breaks for other businesses continue. “Our mission is to grow the economy of Kansas City, and application of tools such as tax exemptions are vital to achieving that mission, said Jon Stephens, president and CEO of Port KC, the Kansas City Port Authority. The incentives speed development, and providing them "has resulted in growth choosing KC versus other markets,” he added.

In Atlanta, those tax breaks are not going to projects in neighborhoods that need help attracting development. They have largely been handed out to projects that are in high demand areas of the city, said Julian Bene, who served on Invest Atlanta’s board from 2010 to 2018. In 2019, for instance, the Fulton County development authority approved a 10-year, $16 million tax abatement for a 410-foot-tall, 27,000-square-foot tower in Atlanta’s vibrant Midtown business district. The project included hotel space, retail space and office space that is now occupied by Google and Invesco.

In 2021, a developer in Atlanta pulled its request for an $8 million tax break to expand its new massive, mixed-use Ponce City Market development in the trendy Beltline neighborhood with an office tower and apartment building. Because of community pushback, the developer knew it likely did not have enough votes from the commission for approval, Bene said. After a second try for $5 million in lower taxes was also rejected, the developer went ahead and built the project anyway.

Invest Atlanta has also turned down projects in the past, Bene said. Oftentimes, after getting rejected, the developer goes back to the landowner and asks for a better price to buy the property to make their numbers work, because it was overvalued at the start.

Trouble in Philadelphia

On Thursday, Oct. 26, 2023, an environmental team was preparing Southwark School in Philadelphia for the winter cold. While checking an attic fan, members of the team saw loose dust on top of flooring that contained asbestos. The dust that certainly was blowing into the floors below could contain the cancer-causing agent. Within a day, Southwark was closed – the seventh Philadelphia school temporarily shuttered since the previous academic year because of possible asbestos contamination.

A 2019 inspection of the John L Kinsey school in Philadelphia found asbestos in plaster walls, floor tiles, radiator insulation and electrical panels. Asbestos is a major problem for Philadelphia’s public schools. The district needs $430 million to clean up the asbestos, lead, and other environmental hazards that place the health of students, teachers and staff at risk. And that is on top of an additional $2.4 billion to fix failing and damaged buildings.

Yet the money is not available. Matthew Stem, a former district official, testified in a 2023 lawsuit about financing of Pennsylvania schools that the environmental health risks cannot be addressed until an emergency like at Southwark because “existing funding sources are not sufficient to remediate those types of issues.”

Meanwhile, the city keeps doling out abatements, draining money that could have gone toward making Philadelphia schools safer. In the fiscal year ending June 2022, such tax breaks cost the school district $118 million – more than 25% of the total amount needed to remove the asbestos and other health dangers. These abatements take 31 years to break even, according to the city’s own scenario impact analyses.

Huge subsets of the community – primarily Black, Brown, poor or a combination – are being “drastically impacted” by the exemptions and funding shortfalls for the school district, said Kendra Brooks, a Philadelphia City Council member. Schools and students are affected by mold, asbestos and lead, and crumbling infrastructure, as well as teacher and staffing shortages – including support staff, social workers and psychologists.

More than half the district’s schools that lacked adequate air conditioning – 87 schools – had to go to half days during the first week of the 2023 school year because of extreme heat. Poor heating systems also leave the schools cold in the winter. And some schools are overcrowded, resulting in large class sizes, she said.

{kind=link}

Teachers and researchers agree that a lack of adequate funding undermines educational opportunities and outcomes. That’s especially true for children living in poverty. A 2016 study found that a 10% increase in per-pupil spending each year for all 12 years of public schooling results in nearly one-third of a year of more education, 7.7% higher wages and a 3.2% reduction in annual incidence of adult poverty. The study estimated that a 21.7% increase could eliminate the high school graduation gap faced by children from low-income families.

More money for schools leads to more education resources for students and their teachers. The same researchers found that spending increases were associated with reductions in student-to-teacher ratios, increases in teacher salaries and longer school years. Other studies yielded similar results: School funding matters, especially for children already suffering the harms of poverty.

While tax abatements themselves are generally linked to rising property values, the benefits are not evenly distributed. In fact, any expansion of the tax base due to new property construction tends to be outside of the county granting the tax abatement. For families in school districts with the lost tax revenues, their neighbors’ good fortune likely comes as little solace. Meanwhile, a poorly funded education system is less likely to yield a skilled and competitive workforce, creating longer-term economic costs that make the region less attractive for businesses and residents.

“There’s a head-on collision here between private gain and the future quality of America’s workforce,” said Greg LeRoy, executive director at Good Jobs First, a Washington, D.C., advocacy group that’s critical of tax abatement and tracks the use of economic development subsidies.

As funding dwindles and educational quality declines, additional families with means often opt for alternative educational avenues such as private schooling, home-schooling or moving to a different school district, further weakening the public school system.

Throughout the U.S., parents with the power to do so demand special arrangements, such as selective schools or high-track enclaves that hire experienced, fully prepared teachers. If demands aren’t met, they leave the district’s public schools for private schools or for the suburbs. Some parents even organize to splinter their more advantaged, and generally whiter, neighborhoods away from the larger urban school districts.

Those parental demands – known among scholars as “opportunity hoarding” – may seem unreasonable from the outside, but scarcity breeds very real fears about educational harms inflicted on one’s own children. Regardless of who’s to blame, the children who bear the heaviest burden of the nation’s concentrated poverty and racialized poverty again lose out.

Rethinking in Philadelphia and Riverhead

Americans also ask public schools to accomplish Herculean tasks that go far beyond the education basics, as many parents discovered at the onset of the pandemic when schools closed and their support for families largely disappeared.

A school serving students who endure housing and food insecurity must dedicate resources toward children’s basic needs and trauma. But districts serving more low-income students spend less per student on average, and almost half the states have regressive funding structures.

Facing dwindling resources for schools, several cities have begun to rethink their tax exemption programs.

The Philadelphia City Council recently passed a scale-back on a 10-year property tax abatement by decreasing the percentage of the subsidy over that time. But even with that change, millions will be lost to tax exemptions that could instead be invested in cash-depleted schools. “We could make major changes in our schools’ infrastructure, curriculum, staffing, staffing ratios, support staff, social workers, school psychologists – take your pick,” Brooks said.

Other cities looking to reform tax abatement programs are taking a different approach. In Riverhead, New York, on Long Island, developers or project owners can be granted exemptions on their property tax and allowed instead to shell out a far smaller “payment in lieu of taxes,” or PILOT. When the abatement ends, most commonly after 10 years, the businesses then will pay full property taxes.

At least, that’s the idea, but the system is far from perfect. Beneficiaries of the PILOT program have failed to pay on time, leaving the school board struggling to fill a budget hole. Also, the payments are not equal to the amount they would receive for property taxes, with millions of dollars in potential revenue over a decade being cut to as little as a few hundred thousand. On the back end, if a business that’s subsidized with tax breaks fails after 10 years, the projected benefits never emerge.

And when the time came to start paying taxes, developers have returned to the city’s Industrial Development Agency with hat in hand, asking for more tax breaks. A local for-profit aquarium, for example, was granted a 10-year PILOT program break by Riverhead in 1999; it has received so many extensions that it is not scheduled to start paying full taxes until 2031 – 22 years after originally planned.

Kansas City border politics

Like many cities, Kansas City has a long history of segregation, white flight and racial redlining, said Kathleen Pointer, senior policy strategist for Kansas City Public Schools.

Troost Avenue, where the Kansas City Public Schools administrative office is located, serves as the city’s historic racial dividing line, with wealthier white families living in the west and more economically disadvantaged people of color in the east. Most of the district’s schools are located east of Troost, not west.

Students on the west side “pretty much automatically funnel into the college preparatory middle school and high schools,” said The Federation of Teachers’ Roberts. Those schools are considered signature schools that are selective and are better taken care of than the typical neighborhood schools, he added.

The school district’s tax levy was set by voters in 1969 at 3.75%. But successive attempts over the next few decades to increase the levy at the ballot box failed. During a decadeslong desegregation lawsuit that was eventually resolved through a settlement agreement in the 1990s, a court raised the district’s levy rate to 4.96% without voter approval. The levy has remained at the same 4.96% rate since.

Meanwhile, Kansas City is still distributing 20-year tax abatements to companies and developers for projects. The district calculated that about 92% of the money that was abated within the school district’s boundaries was for projects within the whiter west side of the city, Pointer said.

“Unfortunately, we can’t pick or choose where developers build,” said Meredith Hoenes, director of communications for Port KC. “We aren’t planning and zoning. Developers typically have plans in place when they knock on our door.”

In Kansas City, several agencies administer tax incentives, allowing developers to shop around to different bodies to receive one. Pointer said he believes the Port Authority is popular because they don’t do a third-party financial analysis to prove that the developers need the amount that they say they do.

With 20-year abatements, a child will start pre-K and graduate high school before seeing the benefits of a property being fully on the tax rolls, Pointer said. Developers, meanwhile, routinely threaten to build somewhere else if they don’t get the incentive, she said.

In 2020, BlueScope Construction, a company that had received tax incentives for nearly 20 years and was about to roll off its abatement, asked for another 13 years and threatened to move to another state if it didn’t get it. At the time, the U.S. was grappling with a racial reckoning following the murder of George Floyd, who was killed by a Minneapolis police officer.

“That was a moment for Kansas City Public Schools where we really drew a line in the sand and talked about incentives as an equity issue,” Pointer said.

After the district raised the issue – tying the incentives to systemic racism – the City Council rejected BlueScope’s bid and, three years later, it’s still in Kansas City, fully on the tax rolls, she said. BlueScope did not return multiple requests for comment.

Recently, a multifamily housing project was approved for a 20-year tax abatement by the Port Authority of Kansas City at Country Club Plaza, an outdoor shopping center in an affluent part of the city. The housing project included no affordable units. “This project was approved without any independent financial analysis proving that it needed that subsidy,” Pointer said.

All told, the Kansas City Public Schools district faces several shortfalls beyond the $400 million in deferred maintenance, Superintendent Jennifer Collier said. There are staffing shortages at all positions: teachers, paraprofessionals and support staff. As in much of the U.S., the cost of housing is surging. New developments that are being built do not include affordable housing, or when they do, the units are still out of reach for teachers.

That’s making it harder for a district that already loses about 1 in 5 of its teachers each year to keep or recruit new ones, who earn an average of only $46,150 their first year on the job, Collier said.

East Baton Rouge and the industrial corridor

It’s impossible to miss the tanks, towers, pipes and industrial structures that incongruously line Baton Rouge’s Scenic Highway landscape. They’re part of Exxon Mobil Corp.’s campus, home of the oil giant’s refinery in addition to chemical and plastics plants.

Sitting along the Mississippi River, the campus has been a staple of Louisiana’s capital for over 100 years. It’s where 6,000 employees and contractors who collectively earn over $400 million annually produce 522,000 barrels of crude oil per day when at full capacity, as well as the annual production and manufacture of 3 billion pounds of high-density polyethylene and polypropylene and 6.6 billion pounds of petrochemical products. The company posted a record-breaking $55.7 billion in profits in 2022 and $36 billion in 2023.

Across the street are empty fields and roads leading into neighborhoods that have been designated by the U.S. Department of Agriculture as a low-income food desert. A mile drive down the street to Route 67 is a Dollar General, fast-food restaurants, and tiny, rundown food stores. A Hi Nabor Supermarket is 4 miles away.

East Baton Rouge Parish’s McKinley High School, a 12-minute drive from the refinery, serves a student body that is about 80% Black and 85% poor. The school, which boasts famous alums such as rapper Kevin Gates, former NBA player Tyrus Thomas and Presidential Medal of Freedom recipient Gardner C. Taylor, holds a special place in the community, but it has been beset by violence and tragedy lately. Its football team quarterback, who was killed days before graduation in 2017, was among at least four of McKinley’s students who have been shot or murdered over the past six years.

The experience is starkly different at some of the district’s more advantaged schools, including its magnet programs open to high-performing students.

{kind=link}

Baton Rouge is a tale of two cities, with some of the worst outcomes in the state for education, income and mortality, and some of the best outcomes. “It was only separated by sometimes a few blocks,” said Edgar Cage, the lead organizer for the advocacy group Together Baton Rouge. Cage, who grew up in the city when it was segregated by Jim Crow laws, said the root cause of that disparity was racism.

“Underserved kids don’t have a path forward” in East Baton Rouge public schools, Cage said.

A 2019 report from the Urban League of Louisiana found that economically disadvantaged African American and Hispanic students are not provided equitable access to high-quality education opportunities. That has contributed to those students underperforming on standardized state assessments, such as the LEAP exam, being unprepared to advance to higher grades and being excluded from high-quality curricula and instruction, as well as the highest-performing schools and magnet schools.

“Baton Rouge is home to some of the highest performing schools in the state,” according to the report. “Yet the highest performing schools and schools that have selective admissions policies often exclude disadvantaged students and African American and Hispanic students.”

Dawn Collins, who served on the district’s school board from 2016 to 2022, said that with more funding, the district could provide more targeted interventions for students who were struggling academically or additional support to staff so they can better assist students with greater needs.

But for decades, Louisiana’s Industrial Ad Valorem Tax Exemption Program, or ITEP, allowed for 100% property tax exemptions for industrial manufacturing facilities, said Erin Hansen, the statewide policy analyst at Together Louisiana, a network of 250 religious and civic organizations across the state that advocates for grassroots issues, including tax fairness.

The ITEP program was created in the 1930s through a state constitutional amendment, allowing companies to bypass a public vote and get approval for the exemption through the governor-appointed Board of Commerce and Industry, Hansen said. For over 80 years, that board approved nearly all applications that it received, she said.

Since 2000, Louisiana has granted a total of $35 billion in corporate property tax breaks for 12,590 projects.

Louisiana’s executive order

A few efforts to reform the program over the years have largely failed. But in 2016, Gov. John Bel Edwards signed an executive order that slightly but importantly tweaked the system. On top of the state board vote, the order gave local taxing bodies – such as school boards, sheriffs and parish or city councils – the ability to vote on their own individual portions of the tax exemptions. And in 2019 the East Baton Rouge Parish School Board exercised its power to vote down an abatement.

Throughout the U.S., school boards’ power over the tax abatements that affect their budgets vary, and in some states, including Georgia, Kansas, Nevada, New Jersey and South Carolina, school boards lack any formal ability to vote or comment on tax abatement deals that affect them.

Edwards’ executive order also capped the maximum exemption at 80% and tightened the rules so routine capital investments and maintenance were no longer eligible, Hansen said. A requirement concerning job creation was also put in place.

Concerned residents and activists, led by Together Louisiana and sister group Together Baton Rouge, rallied around the new rules and pushed back against the billion-dollar corporation taking more tax money from the schools. In 2019, the campaign worked: the school board rejected a $2.9 million property tax break bid by Exxon Mobil.

After the decision, Exxon Mobil reportedly described the city as “unpredictable.”

However, members of the business community have continued to lobby for the tax breaks, and they have pushed back against further rejections. In fact, according to Hansen, loopholes were created during the rulemaking process around the governor’s executive order that allowed companies to weaken its effectiveness.

In total, 223 Exxon Mobil projects worth nearly $580 million in tax abatements have been granted in the state of Louisiana under the ITEP program since 2000.

“ITEP is needed to compete with other states – and, in ExxonMobil’s case, other countries,” according to Exxon Mobil spokesperson Lauren Kight.

She pointed out that Exxon Mobil is the largest property taxpayer for the EBR school system, paying more than $46 million in property taxes in EBR parish in 2022 and another $34 million in sales taxes.

A new ITEP contract won’t decrease this existing tax revenue, Kight added. “Losing out on future projects absolutely will.”

The East Baton Rouge Parish School Board has continued to approve Exxon Mobil abatements, passing $46.9 million between 2020 and 2022. Between 2017 and 2023, the school district has lost $96.3 million.

Taxes are highest when industrial buildings are first built. Industrial property comes onto the tax rolls at 40% to 50% of its original value in Louisiana after the initial 10-year exemption, according to the Ascension Economic Development Corp.

Exxon Mobil received its latest tax exemption, $8.6 million over 10 years – an 80% break – in October 2023 for $250 million to install facilities at the Baton Rouge complex that purify isopropyl alcohol for microchip production and that create a new advanced recycling facility, allowing the company to address plastic waste. The project created zero new jobs.

The school board approved it by a 7-2 vote after a long and occasionally contentious board meeting.

“Does it make sense for Louisiana and other economically disadvantaged states to kind of compete with each other by providing tax incentives to mega corporations like Exxon Mobil?” said EBR School Board Vice President Patrick Martin, who voted for the abatement. “Probably, in a macro sense, it does not make a lot of sense. But it is the program that we have.”

Obviously, Exxon Mobil benefits, he said. “The company gets a benefit in reducing the property taxes that they would otherwise pay on their industrial activity that adds value to that property.” But the community benefits from the 20% of the property taxes that are not exempted, he said.

“I believe if we don’t pass it, over time the investments will not come and our district as a whole will have less money,” he added.

Meanwhile, the district’s budgetary woes are coming to a head. Bus drivers staged a sickout at the start of the school year, refusing to pick up students – in protest of low pay and not having buses equipped with air conditioning amid a heat wave. The district was forced to release students early, leaving kids stranded without a ride to school, before it acquiesced and provided the drivers and other staff one-time stipends and purchased new buses with air conditioning.

The district also agreed to reestablish transfer points as a temporary response to the shortages. But that transfer-point plan has historically resulted in students riding on the bus for hours and occasionally missing breakfast when the bus arrives late, according to Angela Reams-Brown, president of the East Baton Rouge Federation of Teachers. The district plans to purchase or lease over 160 buses and solve its bus driver shortage next year, but the plan could lead to a budget crisis.

A teacher shortage looms as well, because the district is paying teachers below the regional average. At the school board meeting, Laverne Simoneaux, an ELL specialist at East Baton Rouge’s Woodlawn Elementary, said she was informed that her job was not guaranteed next year since she’s being paid through federal COVID-19 relief funds. By receiving tax exemptions, Exxon Mobil was taking money from her salary to deepen their pockets, she said.

A young student in the district told the school board that the money could provide better internet access or be used to hire someone to pick up the glass and barbed wire in the playground. But at least they have a playground – Hayden Crockett, a seventh grader at Sherwood Middle Academic Magnet School, noted that his sister’s elementary school lacked one.

“If it wasn’t in the budget to fund playground equipment, how can it also be in the budget to give one of the most powerful corporations in the world a tax break?” Crockett said. “The math just ain’t mathing.”

Christine Wen worked for the nonprofit organization Good Jobs First from June 2019 to May 2022 where she helped collect tax abatement data.

Nathan Jensen has received funding from the John and Laura Arnold Foundation, the Smith Richardson Foundation, the Ewing Marion Kauffman Foundation and the Washington Center for Equitable Growth. He is a Senior Fellow at the Niskanen Center.